Risks, Volume 7, Issue 1 (March 2019) – 34 articles

Cover Story (view full-size image):

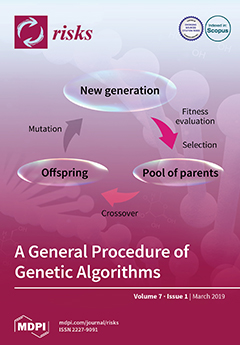

A genetic algorithm (GA) simulates the evolution process. Starting with the initial population, it is more likely for highly fitting solutions to be selected and crossover to produce new offspring. Mutation is further employed to generate a new generation. The GA repeats the procedure until a satisfactory solution is achieved. View this paper.

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue