Risks 2026, 14(6), 142; https://doi.org/10.3390/risks14060142 (registering DOI) - 22 Jun 2026

Abstract

►

Show Figures

Green fintech operates at the intersection of sustainable finance, digital innovation, and financial-sector risk governance. It promises to improve the allocation of capital toward environmentally sustainable activities by lowering information costs, scaling disclosure tools, automating environmental verification, and widening access to green investment

[...] Read more.

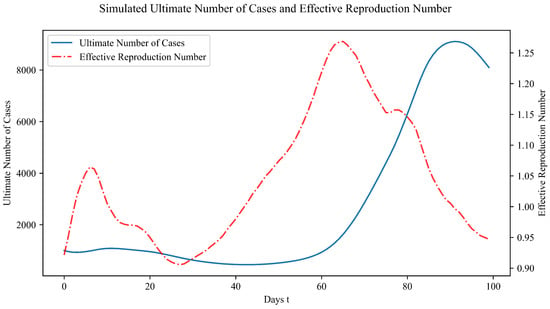

Green fintech operates at the intersection of sustainable finance, digital innovation, and financial-sector risk governance. It promises to improve the allocation of capital toward environmentally sustainable activities by lowering information costs, scaling disclosure tools, automating environmental verification, and widening access to green investment products. Yet the same digital features that make green fintech attractive—speed, scalability, data intensity, platform intermediation, cross-border distribution, and algorithmic decision-making—can also transform apparently local regulatory weaknesses into broader financial-stability concerns. This article examines how regulatory risk associated with green fintech may evolve into systemic risk under conditions of market concentration, weak data governance, regulatory fragmentation, greenwashing amplification, and financial interconnectedness. It develops a mechanism-based conceptual framework rather than an econometric test. The framework connects three regulatory dimensions—regulatory clarity and scope, supervisory consistency, and innovation facilitation—with five systemic-risk transmission channels: market concentration, data and model risk, regulatory arbitrage, greenwashing amplification, and financial interconnectedness. The article draws on sustainable-finance regulation, the financial-stability literature, fintech scholarship, and official supervisory documents, including the EU Sustainable Finance Disclosure Regulation, the EU Taxonomy Regulation, the Digital Operational Resilience Act, and the ESG Ratings Regulation. The central argument is cautious but policy-relevant: green fintech does not automatically create systemic risk, but regulatory uncertainty and supervisory gaps may become systemic when they are embedded in digital infrastructures that scale quickly and are relied upon by multiple financial institutions. The article contributes to risk scholarship by shifting the analysis from compliance-level regulatory risk to transmission mechanisms through which green-finance innovation may affect market integrity and financial stability.

Full article

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}