J. Risk Financial Manag. 2026, 19(5), 373; https://doi.org/10.3390/jrfm19050373 - 20 May 2026

Abstract

Climate-related financial risks have become a central concern for financial institutions and regulators, particularly within the European financial system. This paper examines how climate-related risks are integrated into governance, risk assessment, and regulatory practices in European financial institutions. Using a structured narrative literature

[...] Read more.

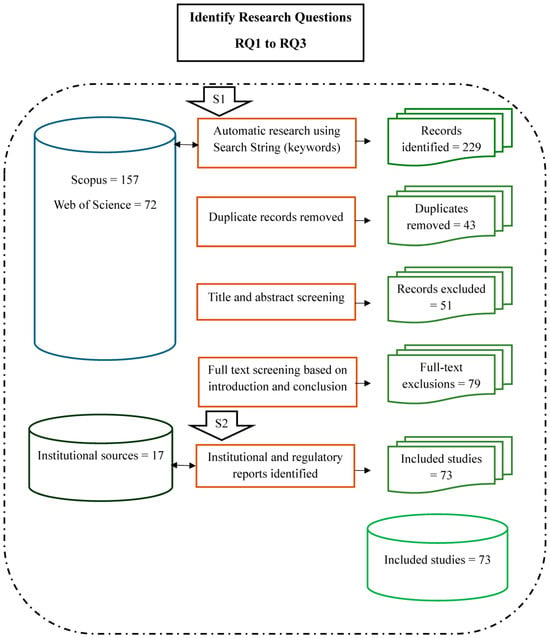

Climate-related financial risks have become a central concern for financial institutions and regulators, particularly within the European financial system. This paper examines how climate-related risks are integrated into governance, risk assessment, and regulatory practices in European financial institutions. Using a structured narrative literature review of academic and institutional sources published between 2015 and 2026, the study synthesizes evidence on physical, transition, and liability risks, as well as the frameworks and tools used to assess them, including climate stress testing, scenario analysis, and climate value-at-risk models. The findings indicate that climate considerations are increasingly embedded within governance structures and supervisory frameworks; however, implementation remains fragmented due to inconsistent data, methodological limitations, and institutional barriers. The review further highlights that existing risk models often struggle to capture the long-term and non-linear nature of climate-related uncertainty. This paper contributes to the literature by linking financial stability theory and institutional theory to explain the persistent gap between regulatory ambition and institutional practice within the European context. The study concludes by discussing implications for supervisory policy, disclosure standardization, and climate-risk integration in financial decision-making.

Full article

(This article belongs to the Section Sustainability and Finance)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}