J. Risk Financial Manag. 2026, 19(8), 555; https://doi.org/10.3390/jrfm19080555 (registering DOI) - 25 Jul 2026

Abstract

Geopolitical uncertainty represents a growing source of systemic risk that reshapes international markets, disrupts cross-border operations, and challenges firms’ ability to sustain financial performance. This research examines the mechanisms through which geopolitical instability relates to firm financial outcomes in Southeast Asian economies by

[...] Read more.

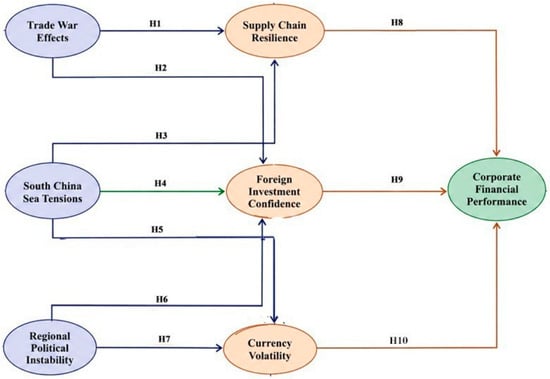

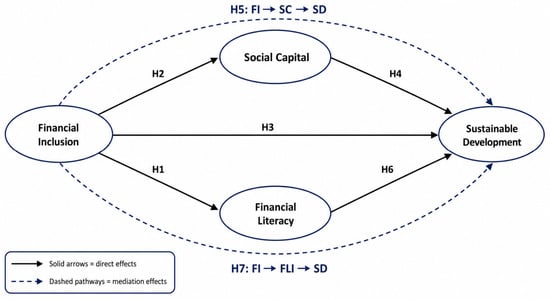

Geopolitical uncertainty represents a growing source of systemic risk that reshapes international markets, disrupts cross-border operations, and challenges firms’ ability to sustain financial performance. This research examines the mechanisms through which geopolitical instability relates to firm financial outcomes in Southeast Asian economies by assessing the mediating roles of supply chain resilience, currency volatility, and foreign investment confidence. Based on a quantitative cross-sectional design, data were collected from 308 firms across Southeast Asian Economies and analyzed using partial least squares structural equation modeling (PLS-SEM). The findings indicate that geopolitical risks significantly influence financial performance, with the strongest effects transmitted through financial channels. Currency volatility and foreign investment confidence emerge as critical mediators, demonstrating that exchange rate instability and investor risk perceptions substantially shape firm performance under geopolitical pressure. While supply chain resilience enhances firms’ capacity to adapt to external disruptions, its direct contribution to financial performance remains insignificant. The model explains 66.7% of the variance in financial performance, reflecting strong explanatory capability. These findings extend existing knowledge by integrating financial, operational, and institutional mechanisms to clarify how geopolitical disruptions propagate into firm-level outcomes. The results underscore the importance of financial preparedness, institutional effectiveness, governance quality, and adaptive capabilities in managing geopolitical uncertainty.

Full article

(This article belongs to the Section Applied Economics and Finance)

►

Show Figures

Figure 1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}