J. Risk Financial Manag., Volume 17, Issue 6 (June 2024) – 39 articles

Cover Story (view full-size image):

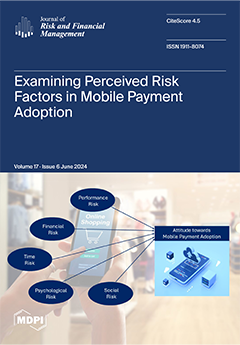

The proliferation of smartphones has led to a surge in the popularity of mobile payment options, primarily due to their inherent convenience. This study delves into the attitudes regarding the adoption of mobile payment, specifically examining component risks including performance, financial, time, psychological, and social risks. Data were collected via a survey of 361 mobile payment users in the United States. Analysis with SPSS and AMOS revealed that both performance and psychological risks have a significant negative impact on attitudes towards mobile payment. These findings underscore the need for mobile payment service providers to implement effective risk management strategies to alleviate user concerns and improve the overall acceptance and adoption of their platforms. View this paper

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue