Empowering Self-Help Groups: The Impact of Financial Inclusion on Social Well-Being

Abstract

1. Introduction

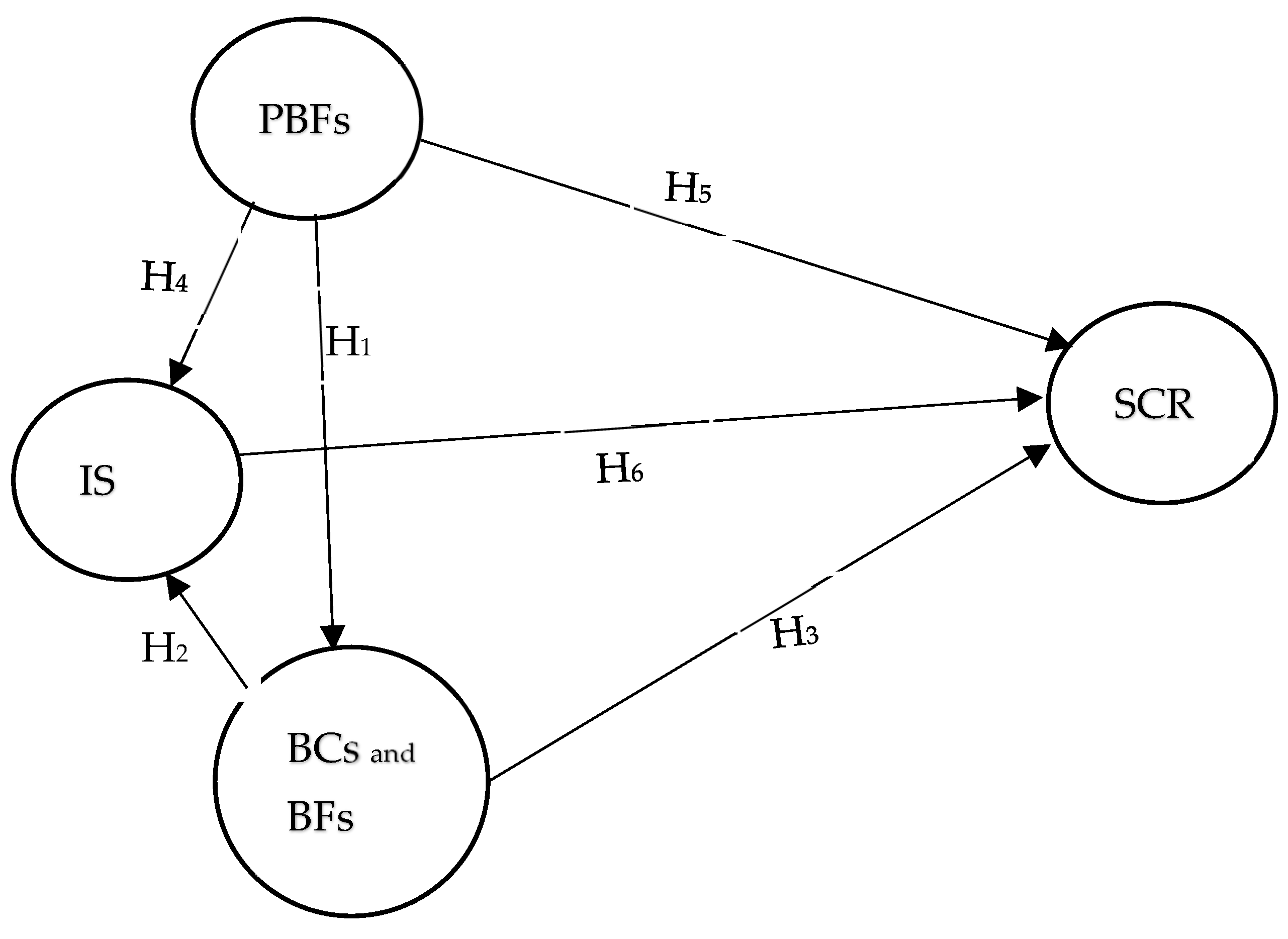

2. Research Gap, Research Questions, and Hypotheses

- RQ1: Do BCs and BFs substitute banks in branchless areas to provide financial services?

- RQ2: Do BCs and BFs enhance the insurance services in rural areas?

- RQ3: Do BCs and BFs improve the social conditions of rural households?

- RQ4: Do physical banks improve insurance services in rural areas?

- RQ5: Do physical banks improve the social conditions of rural households?

- RQ6: Do insurance services improve the social conditions of rural households?

3. Data and Research Methodology

4. Analysis and Results of the Study

4.1. Descriptive Analysis

4.2. Factor Analysis

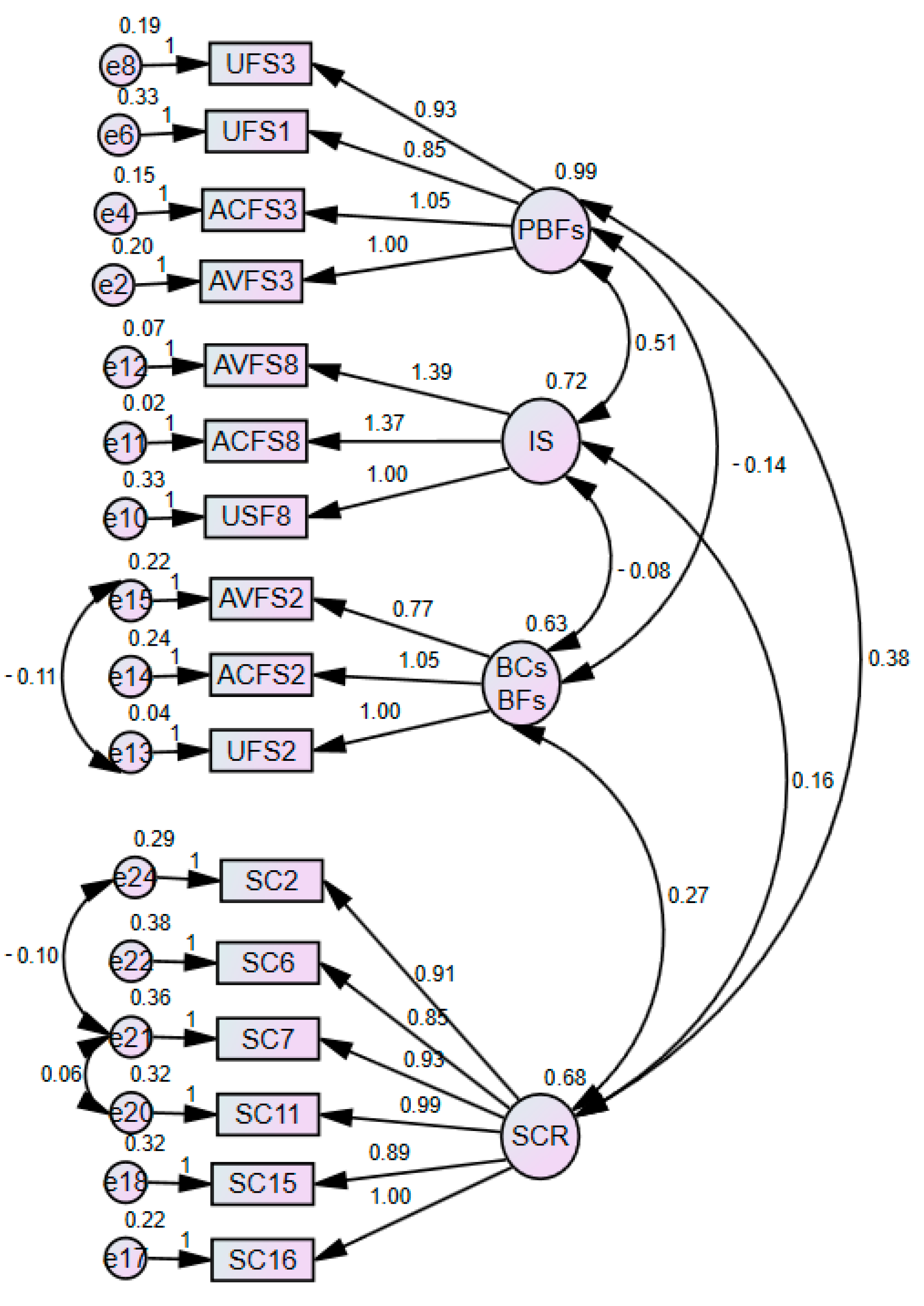

4.3. Measurement Model

Construct Validity

4.4. Structural Equation Model

4.5. Mediation Analysis

Barron and Kenny’s Mediation Model

5. Discussion

6. Conclusions and Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Abosedra, Salah, Ali Fakih, Sajal Ghosh, and Kakali Kanjilal. 2021. Financial development and business cycle volatility nexus in the UAE: Evidence from non-linear regime-shift and asymmetric tests. International Journal of Finance & Economics 28: 2729–41. [Google Scholar]

- Adedokun, Muri Wole, and Mehmet Ağa. 2021. Financial inclusion: A pathway to economic growth in Sub-Saharan African economies. International Journal of Finance & Economics 28: 2712–28. [Google Scholar]

- Ahmad, Mahyudin, and Siong Hook Law. 2022. Financial development, institutions, and economic growth nexus: A spatial econometrics analysis using geographical and institutional proximities. International Journal of Finance & Economics, 1–23. [Google Scholar] [CrossRef]

- Ahmed, Ashfaque. 2013. Perception of life insurance policies in rural India. Kuwait Chapter of the Arabian Journal of Business and Management Review 2: 17–24. [Google Scholar] [CrossRef]

- Arora, Rashmi Umesh. 2010. Measuring financial access. Griffith Business School Discussion Papers Economics 1: 1–21. [Google Scholar]

- Asfaw, Abay, and Joachim Von Braun. 2005. Innovations in health care financing: New evidence on the prospect of community health insurance schemes in the rural areas of Ethiopia. International Journal of health care Finance and Economics 5: 241–53. [Google Scholar] [CrossRef] [PubMed]

- Asif, Mohammad, Mohd Naved Khan, Sadhana Tiwari, Showkat K. Wani, and Firoz Alam. 2023. The impact of fintech and digital financial services on financial inclusion in India. Journal of Risk and Financial Management 16: 122. [Google Scholar] [CrossRef]

- Aziz, Khairi Azhar, Marzanah A. Jabar, Salfarina Abdullah, and Rozi Nor Haizan Nor. 2022. Challenges from the disastrous COVID-19 pandemic: Exposure to opportunities for branchless banking in Malaysia. Bulletin of Electrical Engineering and Informatics 11: 2339–47. [Google Scholar] [CrossRef]

- Bakshi, P. 2012. Financial Inclusion-BC/BF Model-What’s new? TEN, The Journal of Indian Institute of Banking & Finance, 5–11. [Google Scholar]

- Barik, Barik, Sanjaya Kumar Lenka, and Jajati K. Parida. 2022. Financial Inclusion and Human Development in Indian States: Evidence from the Post-Liberalisation Periods. Indian Journal of Human Development 16: 513–27. [Google Scholar] [CrossRef]

- Bhaskar, Vijaya P. 2006. Financial Inclusion by Extension of Banking Services—Use of Business Facilitators and Correspondents. Reserve Bank of India, Bulleting. January. Available online: https://rbi.org.in/scripts/BS_CircularIndexDisplay.aspx?Id=2718 (accessed on 24 April 2024).

- Cbilamge, Pandit. 2015. Marketing of Insurance Products In Rural India: A Big Challenge. CLEAR International Journal of Research in Commerce & Management 6: 28. [Google Scholar]

- Chatterjee, Chandrima, Narayan Chandra Nayak, and Jitendra Mahakud. 2023. Factors affecting the incidence of health insurance penetration among elderly: Evidence from India. Journal of Public Affairs 23: e2848. [Google Scholar] [CrossRef]

- Chauhan, Swati. 2014. Access to finance in Madhya Pradesh: An exploratory study. Indian Journal of Commerce and Management Studies 5: 8–17. [Google Scholar]

- Demirgüç-Kunt, Asli, and Leora F. Klapper. 2012. Measuring Financial Inclusion: The Global Findex Database. World bank policy research working paper 6025. Washington, DC: World Bank Group. [Google Scholar]

- Department of Finance Service Ministry of Finance Government of India. 2021. Pradhan Mantri Jan—Dhan Yojana (PMJDY) Progress Report. Available online: https://pmjdy.gov.in/account (accessed on 24 April 2024).

- De Silva, M. M. G. T., and Akiyuki Kawasaki. 2018. Socioeconomic vulnerability to disaster risk: A case study of flood and drought impact in a rural Sri Lankan community. Ecological Economics 152: 131–40. [Google Scholar] [CrossRef]

- Goel, Sweta, and Rahul Sharma. 2017. Developing a financial inclusion index for India. Procedia Computer Science 122: 949–56. [Google Scholar] [CrossRef]

- Gupta, Pallavi, and Bharti Singh. 2013. Role of literacy level in financial inclusion in India: Empirical evidence. Europe 1: 272–76. [Google Scholar] [CrossRef]

- Habib, Shifa Salman, Shagufta Perveen, and Hussain Maqbool Ahmed Khuwaja. 2016. The role of micro health insurance in providing financial risk protection in developing countries-a systematic review. BMC Public Health 16: 281. [Google Scholar] [CrossRef]

- Hair, Joseph F., Rolph E. Anderson, Barry J. Babin, and William C. Black. 2010. Multivariate Data Analysis: A Global Perspective. Upper Saddle River: Pearson, vol. 7. [Google Scholar]

- Handoo, Jatin. 2010. Financial inclusion in India: Integration of technology, policy and market at bottom of the pyramid. Policy and Market at Bottom of the Pyramid. [Google Scholar] [CrossRef]

- Iqbal, Badar Alam, and Shaista Sami. 2017. Role of banks in financial inclusion in India. Contaduría y Administración 62: 644–56. [Google Scholar] [CrossRef]

- Jha, Chandan Kumar, and Fatih Kırşanlı. 2023. Arab Spring, democratization of corruption, and income inequality. International Journal of Finance & Economics, 1–14. [Google Scholar] [CrossRef]

- Jobson, J. D. 2012. Applied Multivariate Data Analysis: Volume II: Categorical and Multivariate Methods. New York: Springer Science & Business Media. [Google Scholar]

- Jütting, Johannes P. 2004. Do community-based health insurance schemes improve poor people’s access to health care? Evidence from rural Senegal. World Development 32: 273–88. [Google Scholar] [CrossRef]

- Kaur, Simrit, and Cheshta Kapuria. 2020. Determinants of financial inclusion in rural India: Does gender matter? International Journal of Social Economics 47: 747–67. [Google Scholar] [CrossRef]

- Khanal, Dilli Raj. 2007. Banking and Insurance Services Liberalization and Development in Bangladesh, Nepal, and Malaysia: A Comparative Analysis. ARTNeT Working Paper Series No. 41; Bangkok: Asia-Pacific Research and Training Network on Trade (ARTNeT). [Google Scholar]

- Kolloju, Naveen. 2014. Business correspondent model vis-a-vis financial inclusion in India: New practice of banking to the poor. International Journal of Scientific and Research Publications 4: 289–95. [Google Scholar]

- Kumar, Munish, and Sandhir Sharma. 2017. Customer’s Demographics, Adoption & Usage Pattern and Service Quality in Case of Alternate Banking Channels: A Literature Review. International Journal of Applied Business and Economic Research 15: 191–203. [Google Scholar]

- Kumar, Naveen. 2011. Financial Inclusion and its determinants: Evidence from state level empirical analysis in India. Proceedings of the 13th Annual Conference on Money and Finance in the Indian Economy, Mumbai, India, February 25–26. [Google Scholar]

- Kuri, Pravat Kumar, and Arindam Laha. 2011. Financial inclusion and human development in India: An inter-state analysis. Indian Journal of Human Development 5: 61–77. [Google Scholar] [CrossRef]

- Laha, Arindam, and Pravat Kumar Kuri. 2015. Measuring access of microfinance on poverty in India: Towards a comprehensive index. International Journal of Financial Management 5: 11–17. [Google Scholar] [CrossRef]

- Lal, Tarsem. 2021. Impact of financial inclusion on economic development of marginalized communities through the mediation of social and economic empowerment. International Journal of Social Economics 48: 1768–93. [Google Scholar] [CrossRef]

- Murphy, Enda, and Mark Scott. 2014. Household vulnerability in rural areas: Results of an index applied during a housing crash, economic crisis and under austerity conditions. Geoforum 51: 75–86. [Google Scholar] [CrossRef]

- Murthy, C. H. Vishnu, and G. Raju Kumar. 2023. Indian life insurance industry–Future looks good. Asian Journal of Management and Commerce 4: 156–60. [Google Scholar]

- Myeni, Siphesihle, Marshall Makate, and Nyasha Mahonye. 2020. Does mobile money promote financial inclusion in Eswatini? International Journal of Social Economics 47: 693–709. [Google Scholar] [CrossRef]

- Nandru, Prabhakar, Madhavaiah Chendragiri, and Arulmurugan Velayutham. 2021. Examining the influence of financial inclusion on financial well-being of marginalized street vendors: An empirical evidence from India. International Journal of Social Economics 48: 1139–58. [Google Scholar] [CrossRef]

- Niankara, Ibrahim. 2022. Government and private sectors’ electronic transfer practices and financial inclusion in the economic community of the West African States. International Journal of Finance & Economics 27: 4018–47. [Google Scholar]

- Ofoeda, Isaac, Lordina Amoah, Ebenezer Bugri Anarfo, and Joshua Yindenaba Abor. 2022. Financial inclusion and economic growth: What roles do institutions and financial regulation play? International Journal of Finance & Economics 29: 832–48. [Google Scholar]

- Ozili, Peterson K., Adekemi Ademiju, and Semia Rachid. 2023. Impact of financial inclusion on economic growth: Review of existing literature and directions for future research. International Journal of Social Economics 50: 1105–22. [Google Scholar] [CrossRef]

- Ozili, Peterson K., and Paul Terhemba Iorember. 2023. Financial stability and sustainable development. International Journal of Finance & Economics, 1–27. [Google Scholar] [CrossRef]

- Pailwar, Veena K., Jaspreet Kaur, Khushboo Saxena, and Mitesh Nijhara. 2010. Impact of membership of financial institutions on rural saving: A micro-level study. International Business & Economics Research Journal (IBER) 9. [Google Scholar] [CrossRef]

- Prinja, Shankar, Akashdeep Singh Chauhan, Anup Karan, Gunjeet Kaur, and Rajesh Kumar. 2017. Impact of publicly financed health insurance schemes on healthcare utilization and financial risk protection in India: A systematic review. PLoS ONE 12: e0170996. [Google Scholar] [CrossRef] [PubMed]

- Pushp, Aman, Rahul Singh Gautam, Vikas Tripathi, Jagjeevan Kanoujiya, Shailesh Rastogi, Venkata Mrudula Bhimavarapu, and Neha Parashar. 2023. Impact of Financial Inclusion on India’s Economic Development under the Moderating Effect of Internet Subscribers. Journal of Risk and Financial Management 16: 262. [Google Scholar] [CrossRef]

- Radhika, Radhika, and Ramesh Kumar Satuluri. 2019. A study on life insurance penetration in India. International Journal of Human Resource Management and Research (IJHRMR) 9: 119–24. [Google Scholar]

- Raman, Atul. 2012. Financial inclusion and growth of Indian banking system. IOSR Journal of Business and Management 1: 25–29. [Google Scholar] [CrossRef]

- Ramasubbian, Hemavathy, and Ganesan Duraiswamy. 2012. The aid of banking sectors in supporting financial inclusion-an implementation perspective from Tamil Nadu state, India. Research on Humanities and Social Sciences 2: 38–46. [Google Scholar]

- Rastogi, Shailesh, and Ragabiruntha E. 2018. Financial inclusion and socioeconomic development: Gaps and solution. International Journal of Social Economics 45: 1122–40. [Google Scholar] [CrossRef]

- Rupa, K. N., and H. R. Uma. 2015. Role of Lead Bank in Financial Inclusion A Case Study of H D Kote Taluk. International Journal in Management and Social Science 3: 240–48. [Google Scholar]

- Sarma, Mandira, and Jesim Pais. 2011. Financial inclusion and development. Journal of International Development 23: 613–28. [Google Scholar] [CrossRef]

- Saxena, Rajeev K., and Akhilesh Kumar Mishra. 2016. BC Model: A tool for reaching out to the unreached. Journal of Reviews and Research 4: 1–12. [Google Scholar]

- Serrao, Manohar Vincent, Aloysius H. Sequeira, and Vedamani Basil Hans. 2012. Designing a methodology to investigate accessibility and impact of financial inclusion. Household Finance e-Journal-CMBO. [Google Scholar] [CrossRef]

- Sethi, Dinabandhu, and Susanta Kumar Sethy. 2018. Financial inclusion matters for economic growth in India: Some evidence from cointegration analysis. International Journal of Social Economics 46: 132–51. [Google Scholar] [CrossRef]

- Sharma, Anupama, and Sumita Kukreja. 2023. Pradhan Mantri Jan Dhan Yojna: A Tool for Financial Inclusion. Productivity 64: 54–61. [Google Scholar] [CrossRef]

- Singh, Charan, and Gopa Naik. 2018. Financial Inclusion after PMJDY: A Case Study of Gubbi Taluk, Tumkur. IIM Bangalore Research Paper, no. 568. Bangalore: IIM Bangalore. [Google Scholar] [CrossRef]

- Singh, Sunny Kumar, and Chandan Kumar Jha. 2023. Are financial development and financial stability complements or substitutes in poverty reduction? The European Journal of Finance 29: 2001–31. [Google Scholar] [CrossRef]

- Survase, Madan, and Krishna Murthy Inumula. 2019. Financial Inclusion: Scale Modification and Validation of Socio-Economic Indicators. SCMS Journal of Indian Management 16: 31–40. [Google Scholar]

- Survase, Madan, Ratri Parida, and George V. Antony. 2021. A study on the sustainable financial inclusion in selected SAARC countries: A gender-based perspective. Empirical Economics Letters. in press. [Google Scholar]

- Swamy, Vighneswara. 2014. Financial inclusion, gender dimension, and economic impact on poor households. World Development 56: 1–15. [Google Scholar] [CrossRef]

- Waikar, Vaishali, and Yamini Karmarkar. 2017. Pradhan Mantri Jan Dhan Yojana-An Exploratory Study of Banks Participation in Financial Inclusion In Indore District. International Journal of Research in Commerce & Management 8: 3. [Google Scholar]

- Xu, Fang, Xiaoru Zhang, and Di Zhou. 2022. Does digital financial inclusion reduce the risk of returning to poverty? Evidence from China. International Journal of Finance & Economics, 1–23. [Google Scholar] [CrossRef]

- Yusuf, T. O., Ayantunji Gbadamosi, and Dallah Hamadu. 2009. Attitudes of Nigerians towards insurance services: An empirical study. African Journal of Accounting, Economics, Finance and Banking Research 4: 34–46. [Google Scholar]

- Zouari-Hadiji, Rim. 2023. Financial innovation characteristics and banking performance: The mediating effect of risk management. International Journal of Finance & Economics 28: 1214–27. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Demographics | Household Details (N = 426) | % of Respondents |

|---|---|---|

| Age | Less than 25 years | 13 |

| 26 to 35 years | 39.4 | |

| 36 to 45 years | 34.9 | |

| More than 45 years | 12.7 | |

| Caste | SC | 22.1 |

| ST | 33.5 | |

| OBC | 27.9 | |

| Secondary and Higher | 16.5 | |

| Education | Illiterate | 8.7 |

| Below Secondary | 48.3 | |

| Secondary and Higher Secondary | 36.8 | |

| Graduation and Diploma | 3.8 | |

| Post-Graduation and above | 2.4 | |

| Occupation | Self Employed | 13.9 |

| Private Sector Employee | 18.6 | |

| Public Sector Employee | 3.1 | |

| Farmer | 46.9 | |

| Daily Labor | 15.1 | |

| Unemployed | 2.4 | |

| District | Pune | 36.1 |

| Thane | 30.2 | |

| Palghar | 33.7 |

| Construct | SCR | PBF | IS | BCs and BFs |

|---|---|---|---|---|

| SCR | 1.000 | |||

| PBF | 0.499 ** | 1.000 | ||

| IS | 0.256 ** | 0.577 ** | 1.000 | |

| BCs and BFs | 0.44 ** | −0.177 ** | −0.129 ** | 1.000 |

| Construct | No. Items | Cronbach’s Alpha (Reliability) |

|---|---|---|

| PBFs | 8 | 0.933 |

| IS | 3 | 0.95 |

| BCs and BFs | 3 | 0.875 |

| SCR | 9 | 0.934 |

| Rotated Matrix a | ||

|---|---|---|

| Construct | Items | Factor Loading |

| SC | SC2—Helped for all Health Access | 0.782 |

| SC3—Improved confidence level | 0.661 | |

| SC6—Improved nutritional status | 0.744 | |

| SC7—Access to basic sanitation facilities (i.e., lavatory) | 0.781 | |

| SC11—Personal care access (i.e., oral, hair, and body care) | 0.834 | |

| SC12—Entertainment (i.e., movies) | 0.590 | |

| SC15—Helped in Family and Cultural Function | 0.768 | |

| SC16—Improved Social Security (i.e., feeling of security in the society) | 0.871 | |

| SC17—Improved Overall Social Status | 0.876 | |

| PBF | AVFS1—The bank branch is available at your place | 0.828 |

| AVFS3—Automated Teller Services (ATMs) is available | 0.881 | |

| AVFS10—Deposit/withdrawing cash facility is available | 0.699 | |

| ACFS3—Automated Teller Services (ATMs) are easily accessible | 0.846 | |

| ACFS6—Cheque book is easily available to you | 0.641 | |

| UFS1—Availed financial services through the bank branch | 0.785 | |

| UFS3—Use of Automated Teller Services (ATMs) is frequent | 0.842 | |

| UFS9—Availed overdraft facility of the bank | 0.533 | |

| IS | AVFS8—Insurance schemes are available | 0.882 |

| ACFS8—Insurance facilities are easily accessible to you | 0.886 | |

| USF8—Availed insurance facilities through the bank/BC/BF | 0.872 | |

| AVFS2—BC and BF are available at your place | 0.744 | |

| BC and BF | ACFS2—BC/BF are easily approachable | 0.894 |

| UFS2—Availed financial services through BC/BF | 0.845 | |

| Total cumulative variance: 72.342 | ||

| Extraction Method: Principal Component Analysis. | ||

| Rotation Method: Varimax with Kaiser Normalization. a | ||

| a. Rotation converged in 7 iterations. | ||

| Measure | Initial Measurement | Final Measurement | Acceptable Fit Criterion |

|---|---|---|---|

| CMIN/DF | 3.554 | 2.675 | ≤3 indicates an acceptable fit ≤5 indicates a reasonable fit |

| CFI | 0.956 | 0.974 | ≥0.90 indicates an acceptable fit ≥0.95 indicates an excellent fit |

| SRMR | 0.068 | 0.0574 | ≤0.05 indicates an acceptable fit |

| RMSEA | 0.078 | 0.063 | ≤0.05 indicates an excellent fit ≤0.08 indicates an acceptable fit |

| PCLOSE | 0 | 0.012 | ≥0.05 the model is considered to have a close fit |

| Construct | No. Items | AVE | CR |

|---|---|---|---|

| PBFs | 8 | 0.58 | 0.86 |

| IS | 3 | 0.77 | 0.88 |

| BCs and BFs | 3 | 0.68 | 0.82 |

| SCR | 9 | 0.59 | 0.88 |

| Measure | Estimate | Threshold | Interpretation |

|---|---|---|---|

| CMIN/DF | 2.675 | Between 1 and 3 | Excellent |

| CFI | 0.974 | >0.95 | Excellent |

| SRMR | 0.057 | <0.08 | Excellent |

| RMSEA | 0.063 | <0.06 | Acceptable |

| PCLOSE | 0.012 | >0.05 | Acceptable |

| Hypotheses | Path | Estimate (β) | p Values ≤ 0.01 | Result | ||

|---|---|---|---|---|---|---|

| H1 | BCs and BFs | ← | PBFs | −0.14 | *** | Supported |

| H2 | IS | ← | BCs and BFs | −0.01 | 0.835 | Rejected |

| H3 | SCR | ← | BCs and BFs | 0.53 | *** | Supported |

| H4 | IS | ← | PBFs | 0.52 | *** | Supported |

| H5 | SCR | ← | PBFs | 0.50 | *** | Supported |

| H6 | SCR | ← | IS | −0.08 | 0.11 | Rejected |

| Measure | Estimate | Threshold | Interpretation |

|---|---|---|---|

| CMIN/DF | 2.647 | Between 1 and 3 | Excellent |

| CFI | 0.975 | >0.95 | Excellent |

| SRMR | 0.057 | <0.08 | Excellent |

| RMSEA | 0.062 | <0.06 | Acceptable |

| PCLOSE | 0.015 | >0.05 | Acceptable |

| Path | Estimate (β) | p Values ≤ 0.01 | ||

|---|---|---|---|---|

| SCR | ← | PBF | 0.378 | *** |

| BC and BF | ← | PBF | −0.151 | *** |

| SCR | ← | BC and BF | 0.361 | *** |

| Path | Estimate (β) | p Values ≤ 0.01 | ||

|---|---|---|---|---|

| SCR | ← | PBF | 0.55 | *** |

| BC and BF | ← | PBF | −0.18 | *** |

| SCR | ← | BC and BF | 0.51 | *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Survase, M.; Gohil, A. Empowering Self-Help Groups: The Impact of Financial Inclusion on Social Well-Being. J. Risk Financial Manag. 2024, 17, 217. https://doi.org/10.3390/jrfm17060217

Survase M, Gohil A. Empowering Self-Help Groups: The Impact of Financial Inclusion on Social Well-Being. Journal of Risk and Financial Management. 2024; 17(6):217. https://doi.org/10.3390/jrfm17060217

Chicago/Turabian StyleSurvase, Madan, and Atmajitsinh Gohil. 2024. "Empowering Self-Help Groups: The Impact of Financial Inclusion on Social Well-Being" Journal of Risk and Financial Management 17, no. 6: 217. https://doi.org/10.3390/jrfm17060217

APA StyleSurvase, M., & Gohil, A. (2024). Empowering Self-Help Groups: The Impact of Financial Inclusion on Social Well-Being. Journal of Risk and Financial Management, 17(6), 217. https://doi.org/10.3390/jrfm17060217