Int. J. Financial Stud., Volume 11, Issue 4 (December 2023) – 36 articles

Cover Story (view full-size image):

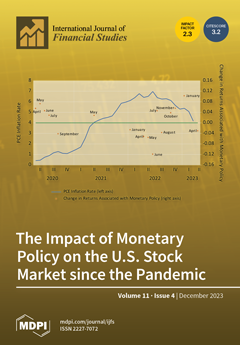

The figure plots represent the months between 2020 and 2023 when there was a statistically significant relationship between the returns of 53 assets and their betas concerning Bauer and Swanson’s monetary policy measure. The coefficients show how investors’ responses to monetary policy affected assets with an average exposure to contractionary monetary policy. The figure also shows that investors in 2020 anticipated more flexible monetary policies. Although inflation soared in 2021, investors did not foresee a tighter policy. As inflation increased in 2022, investors factored in the likelihood of contractionary monetary policy changes. It is striking how investors’ perceptions of monetary policy changed from month to month in 2022. View this paper

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue