1. Introduction

The financial sector is vital to the economy, as it encourages economic growth. Therefore, modelling the extremes and risk management of financial markets, such as stock returns and losses as well as currency exchange rates, is vital to the economic development and growth of both emerging and developing countries. In the financial markets, extreme events occur but are sparse in nature. Extreme value theory (EVT) assesses extreme events in the tails that diverge from the normal distribution and investigates how the samples of extremes behave. The problem of the limited amount of information has inspired the present study to examine the extreme value behaviour of Johannesburg stock exchange (JSE) financial market data using the r-largest-order statistics and peaks-over-threshold (POT) approaches. Rather than making use of a single maximum value within a block, the r-largest-order statistics and POT retain more data, therefore making maximum use of the available information. The r-largest-order statistics technique belongs to the block maxima approach.

The main purpose of this study is to model the extreme behaviour of the JSE financial market data and compare the block maxima approach and the POT approach in terms of their ability in modelling the financial market data. This research study is based on the use of advanced EVT methods such as the r-largest generalised extreme value theory (GEVD), the newly-proposed blended GEVD (bGEVD), and the Poisson point process. In South Africa, several studies have been conducted using EVT in the fields of hydrology, environmental sciences, and climatology, and there is a dearth of literature on research that uses advanced EVT techniques in the financial industry.

The findings in this study reveal a clear distinction between block maxima and POT return level estimates. The results from this study show that the POT approach return level estimates are comparably higher than the block maxima estimates. The block maxima return level estimates of roughly 11,100 and R19.23 for the all-share total return index (ALSTRI) and the United States dollar (USD) against the South African rand (ZAR) (USD–ZAR) exchange rate, respectively, are closer to reality than the POT estimates in this study. Another contribution of this study is the use of bGEVD in the financial markets, which has not been done in previous studies. The study further revealed that the bGEVD is more suitable for relatively short-term forecasting since it cuts off at the 50-year return level. The findings of this study imply that investors will experience higher gains in the ALSTRI and that the South African rand will become unstable in the long run. Therefore, the present study will add value to the literature and knowledge of statistics and econometrics. Furthermore, the results of this study will assist investors, investment analysts, risk experts, financial economists, financial analysts, and financial regulators in assessing the probability of rare events in modelling and predicting uncertainties and occurrences using limited available data. In the future, advanced studies on bGEVD, vine copulas, and r-largest-order bGEVD can be conducted in the financial markets and/or finance sector.

The rest of the paper is organised as follows:

Section 2 presents the literature review, and

Section 3 and its subsections present the research methodology and analytical procedures.

Section 4 presents the results and discussions of the research findings.

Section 5 presents the concluding remarks and recommendations for the study, including proposed areas for future research.

2. Literature Review

The primary engine of the economy that fosters economic growth and development is the financial system. Financial infrastructure enables economic development and growth by distributing funds from financial entities to potential investors (

Darškuvienė 2010). In general, financial markets are frequently referred to as the global economy’s "barometer" of the nation (

Wei and Han 2021). There are three main components of the financial system of an economy, namely financial regulators, financial intermediaries, and financial markets. The financial markets comprise, amongst others, the exchange rate, stock markets, government bonds, credit default swap markets, equity markets, debt markets, and derivatives markets (

Darškuvienė 2010;

Wei and Han 2021). According to

Su (

2020), the risk in one stock market is very likely to be diffused to another stock market because the global markets are not regulated and integrated. There are rare events that contribute towards the negative impact on the financial markets, such as pandemics and financial crises. Due to the instability and unpredictability of the financial markets, the manifestation of financial crises and pandemics can put investors, financial economists, and risk experts in an uneasy situation, not knowing whether the investments will return gains or losses, as well as not knowing the impact of these rare events on the stock and financial markets.

Several global financial crises worldwide emerged as early as the nineteenth century.

Bordo and Landon-Lane (

2010) identified the six global crises that occurred in the years 1880, 1890–1891, 1907–1908, 1913–1914, 1931–1932, and 2007–2008. According to

Chikobvu and Jakata (

2020), other international crises include but are not limited to the United States of America (USA) recession of the period of 1937–1938, the 1971 Brazilian stock market crash, the Japanese “asset price bubble” of the period from 1986 to 1991, and the 1997 Asian financial crises. These financial crises caused great recessions around the globe, which affected both emerging and advanced markets. Measurement of market risk, with a focus on the tails, is of primary relevance to investors and financial risk managers in determining the potential severity of market losses (

Makatjane and Moroke 2021;

McNeil and Frey 2000). The volatility in the financial markets leads to criticism about the existing risk management systems and motivates the search for more appropriate methodologies that can be able to cope with rare extreme events with heavy consequences (

Gilli and Këllezi 2006). In accordance with

Zhang and Hamori (

2021), one of the examples of rare events instigated by health crisis was the Spanish flu outbreak, which occurred in the year 1918. The most recent pandemic worldwide is the coronavirus of 2019 (COVID-19) pandemic. Since the year 2020, the COVID-19 pandemic has been raging globally and has had a traumatic impact on the global economy, trade, and other aspects (

Zhang and Hamori 2021).

The Johannesburg stock exchange (JSE) is the South African stock exchange located in Sandton, Johannesburg city, in the Gauteng province of South Africa. The JSE was established on 8 November 1887 by Benjamin Wollan and is currently the largest stock exchange in Africa (

JSE Limited 2023). In addition to giving investors a return on their investment in the form of dividends, the JSE also helps the economy by reinvesting money. Among other things, it provides a capability for effective pricing determination as well as a method for managing price risk. Under the Securities Services Act of 2004 and Section 8 of the Financial Markets Act of 2012, the JSE is a licensed self-regulatory organisation and frontline provider of regulatory services, which provides services that include, but are not limited to, the equity markets, debt or interest rate markets, commodity markets, and foreign exchange markets (

JSE Limited 2023;

Makhwiting et al. 2014).

In accordance with

Iyke and Ho (

2021), one of the leading currencies in Africa is the South African rand (ZAR). Due to disrupted financial markets during the COVID-19 pandemic, the ZAR suffered even more. However, some sectors have benefited from exchange rate exposure, which includes, among others, personal and consumer goods, tobacco, beverages, and technology (

Iyke and Ho 2021). South Africa is the dominant player in the southern African export markets in sectors and industries such as mining, tobacco, and beverages, but tends to import electric or electronic equipment, as well as automobile and car parts. Generally, the sectors and industries that are import or export-dependent experience an increase or decline in stock returns if the local currency depreciates. According to

Takyi and Bentum-Ennin (

2021), as the pandemic continued, economies of many countries were exposed to a great threat posed to economic growth and development. Evaluating the probability of the occurrence of rare and extreme events is crucial in the financial industry. The extreme value theory (EVT) is the best-suited statistical method to assist with the evaluation and modelling of extreme events. In accordance with

Gencay and Selçuk (

2004), EVT is able to model the left and the right tails independently, which is important because risk and reward are not equally likely, especially in emerging markets. EVT has become a fairly robust framework for the tail behaviours of distribution with regard to the probability of extreme events in the financial markets (

Andreev et al. 2012).

The newly developed EVT approach called the bGEVD was employed by

Vandeskog et al. (

2021b) to model the annual extremes of the short-term precipitation of south Norway. This approach comprises the right tail of the Fréchet distribution and the left tail of the Gumbel distribution. The yearly precipitation maxima were modelled in order to generate better return levels of spatial maps. The study by

Vandeskog et al. (

2021b) applied the Bayesian hierarchical model along with the latent Gaussian field to model the annual short-term precipitation maxima over the period from 1967 to 2020. The integrated nested Laplace approximation (INLA) was used to perform inference. The research results indicated that the bGEVD performed better than the traditional block maxima models. Thus, the bGEVD generated good estimates for the large returns of the short-term precipitation.

Vandeskog et al. (

2021a) used bGEVD to model block maxima. The main aim of the study focused on the newly advanced two-step hierarchical method, which considered the block maxima and the peaks-over-threshold (POT) as well as testing the performance of the bGEVD in a simulation study. The research findings illustrated that the bGEVD outperformed the traditional GEVD because it generates accurate estimates, caters for smaller and faster inference, and estimates good return levels. The bGEVD is considered to be the promising alternative to the GEVD for modelling block maxima. The two-step model was found to have the potential to improve the inference by using more data. The yearly maxima of sub-daily precipitation from the southern part of Norway were modelled by (

Vandeskog et al. 2022) using the bGEVD. The yearly precipitation maxima were modelled using a Bayesian hierarchical model with a latent Gaussian field and bGEVD instead of the traditional generalised extreme value distribution (GEVD). The bGEVD’s scale parameter was modelled utilising the two-step method employing the POT to draw conclusions. Along with the stochastic partial difference equation technique, R-INLA was employed to perform inference. In order to create the spatial maps of the return level estimates, the model was fitted with the annual sub-daily precipitation maxima from south Norway. It was discovered that while modelling the yearly maxima of the sub-daily precipitation data with bGEVD, the two-step proposed method offered a better model fit than the traditional inference method.

Andreev et al. (

2012) carried out a study in Russia that applied the POT approach of EVT to model the Russian stock market. The study utilised daily log losses (negative returns) of the largest Russian stock, namely the RTS index, over a 15-year period from 1995 to 2009. The proposed methods were employed to evaluate and model the tail-related risk and to test the volatility of risk-management tools. The maximum likelihood estimator (MLE) approach was used to estimate the parameters. The two most widely used methods in EVT, namely the block maxima and the POT, were applied to model the tail returns in order to integrate the EVT estimates into the risk measures. The Hill plot was used to determine the optimal threshold. The outcomes of the study illustrated that the generalised Pareto distribution (GPD) performed better and fitted the tail distribution of financial products more accurately compared to the traditional methods of risk measures. In the USA,

Longin and Pagliardi (

2016) employed EVT to investigate the correlation between the transaction volume and returns associated with crashes and booms in the USA stock markets. The authors utilised the daily Standard and Poor’s (S&P) 500 for the period from 3 January 1950 to 30 September 2015. The GPD values for each marginal distribution as well as the Gumbel copula models were fitted to assess model dependence. The POT approach was used to extract extreme returns and volumes in order to select the threshold exceedances for returns that lie above or below the extremes. The Gumbel copula function was used to model the dependence between bivariate exceedances. The findings of the study indicated that there was a very low significant correlation between the return and volume in the left and the right tails of the return distribution during the crashes and the boom of the stock markets. This implies that the returns do not depend on the transaction volumes.

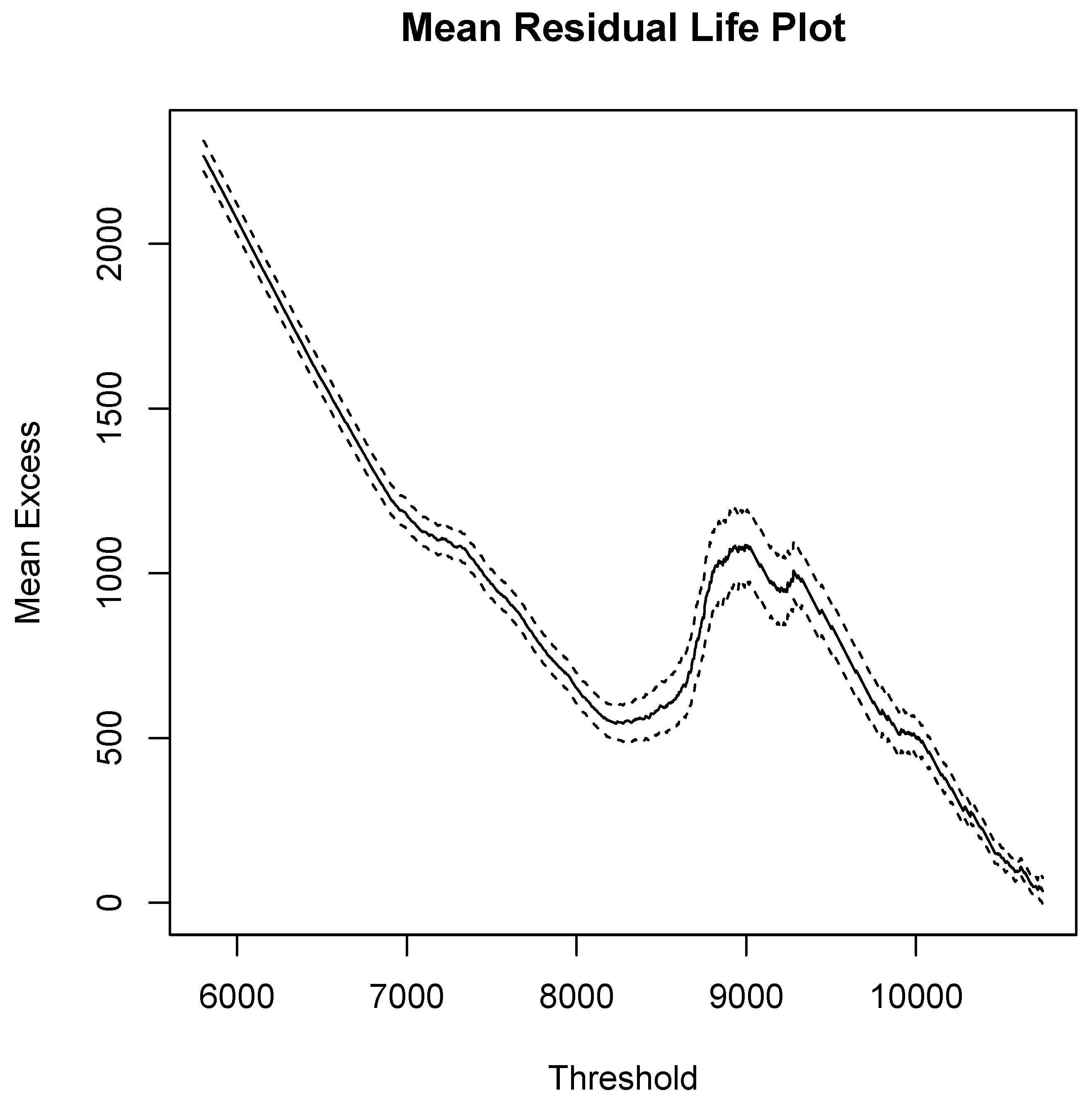

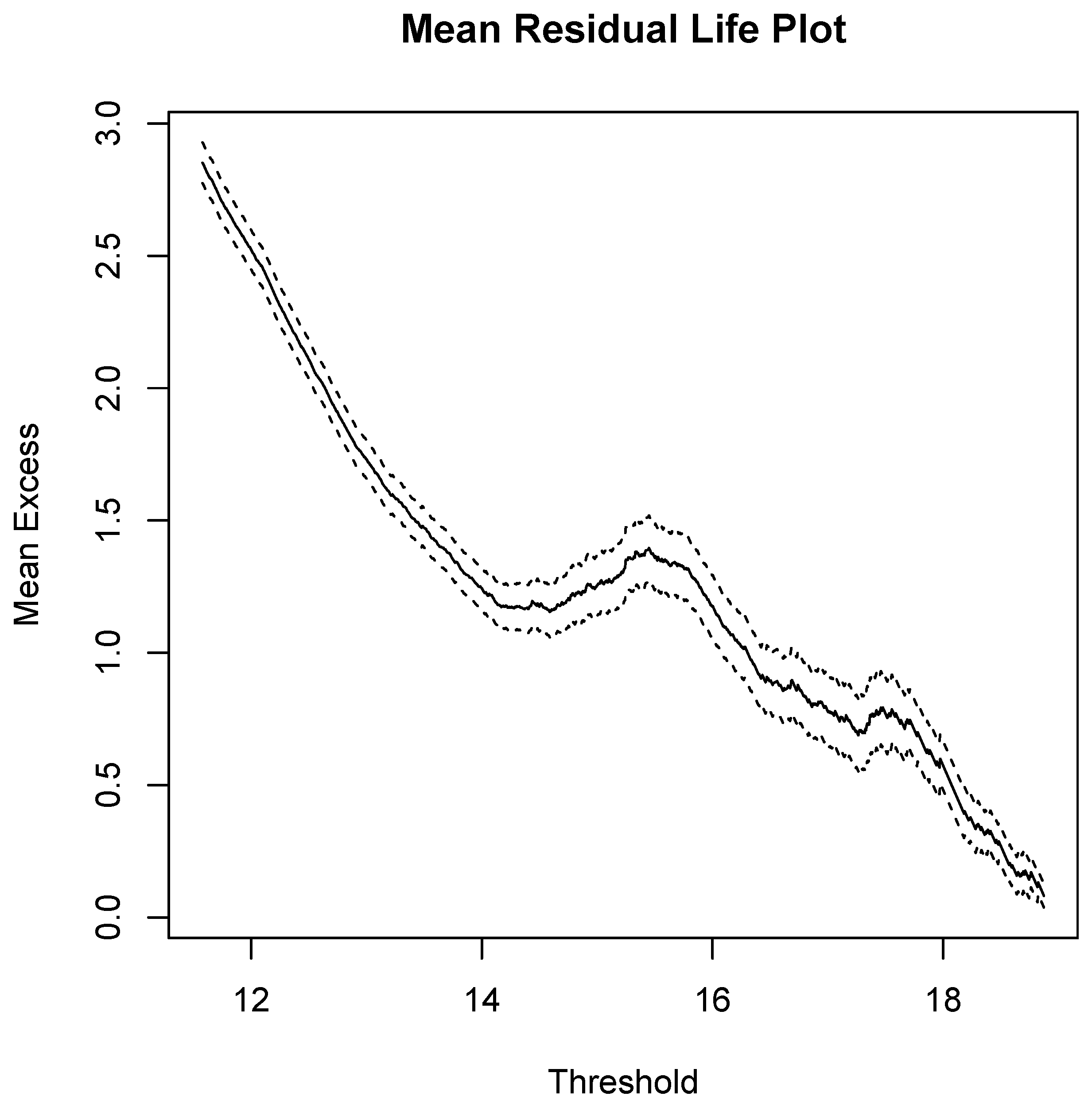

Rydman (

2018) applied the GPD to the automobile property insurance data in the USA, aiming at setting an appropriate threshold, and analysing and modelling the data. In order to set a threshold, rules of thumb and graphical methods such as the mean residual life plot and the parameter stability plot were employed. The MLE and the probability-weighted moments (PWM) were explored for estimating the parameters. It was found that the PWM parameter estimation approach was more efficient for small samples; thus, the MLE approach was selected as the best parameter estimation approach to fit the GPD using the automobile insurance claims data. The extreme behaviour of stock market returns for the five BRICS countries which comprise Brazil, Russia, India, China, and South Africa for the period 1995 to 2015 was studied by

Afuecheta et al. (

2023). The study was carried out to measure financial risk using EVT. Various copula models were fitted to determine the tail dependence of the markets. The Gumbel copula was found to be the best suitable model with significant relationships for all pairs of the markets for BRICS countries, and the GEVD was found to be the best fit.

Extremal dependence of monthly maximum temperatures of the Limpopo province in South Africa for the period 1994 to 2009 was modelled by

Maposa et al. (

2021). The authors employed two modelling approaches in the study, namely the bivariate conditional extremes model and time-varying threshold. The study was conducted in four meteorological stations located in the Limpopo province, namely Mara, Messina, Polokwane, and Thabazimbi. The research results showed significant positive and negative extremal dependence in some pairs of meteorological stations.

Sikhwari et al. (

2022) fitted EVT to extreme daily and monthly maximum rainfalls in Limpopo Province, South Africa. The extreme rainfall dataset was fitted using the yearly block maxima and the

r-largest-order statistics approach. The automatic selection algorithm approach was employed to choose the maxima in the situation, where

. The findings showed that GEVD

was determined to be the most suitable fit for the data.

Nemukula and Sigauke (

2018) utilised the

r-largest-order statistics to model the average maximum daily temperature from 2000 to 2010 excluding the non-winter season. The aim of the study focused on reducing the risk of disasters occurring due to heatwaves and extremely high temperatures using the South African Weather Service (SAWS) and Eskom data. The research results showed that out of the 10-order statistics,

was considered to be the best fit. The

r-largest-order statistics based on the joined GEVD was employed by

Kajambeu et al. (

2020) to model the probability of the extreme return levels of the flood heights of the Limpopo River at the Beitbridge. The

r-largest-order statistics method was regarded to be a more effective approach for modelling the flood heights as compared to the traditional block maxima approach.

Van der Merwe et al. (

2018) conducted a study titled: “Bayesian extreme value analysis of stock exchange data”. The authors explored the use of EVT in financial modelling using the share losses on the daily JSE Top 40 Index over a period of 10 years. Visual methods such as the mean excess plot, Hill plot, and the Pareto quantile plot were applied to select the threshold. The classical parameter estimation methods were employed and compared with the Bayes method. A simulation study was executed in order to compare the various estimators. The GPD above the threshold was combined with the non-parametric technique below the threshold. The Bayes estimator method was the best estimation technique and it was used in order to fit the POT model. The authors indicated that the Bayes estimator method can improve parameter estimation and computation of risk measures. The South African financial index (J580) for the period from 1995 to 2018 was analysed and modelled by

Chikobvu and Jakata (

2020) through the GEVD to estimate the extreme gains and losses. The quarterly block maxima and minima of the monthly returns were fitted to the GEVD and comparative analysis with GPD was conducted. The main findings of the research demonstrated that EVT is a proficient approach for forecasting potential high risks in advance.

A study carried out by

Makatjane et al. (

2021) focused on EVT to predict the tail behaviours of the Financial Times stock exchange/Johannesburg stock exchange (FTSE/JSE) closing banking indices. The closing banking indices of the five major South African banks, namely ABSA, Capitec, FNB, Nedbank, and Standard Bank, were considered to investigate the tail behaviour of the stock returns and relative risk. The MLE approach was used to estimate the parameters of the GEVD and GPD. The GEVD for the block minima was utilised as well as the GPD for the POT. It was found that all parameters of the GEVD were significantly positive for all five major banks in South Africa and the shape parameter was greater than zero. This implied that all the closing banking indices of the FTSE/JSE could be fitted with a Frèchet family of distribution.

Jakata and Chikobvu (

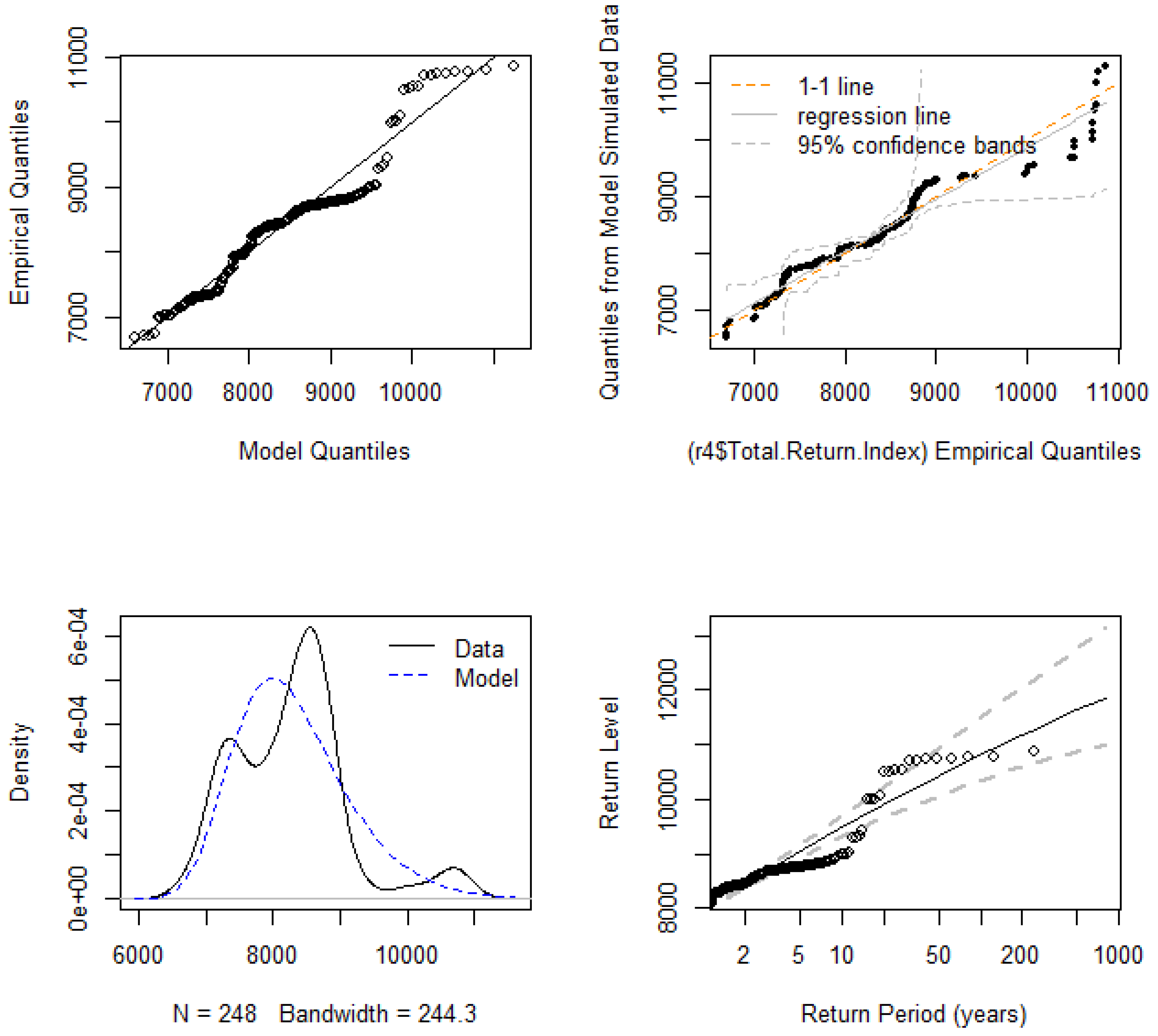

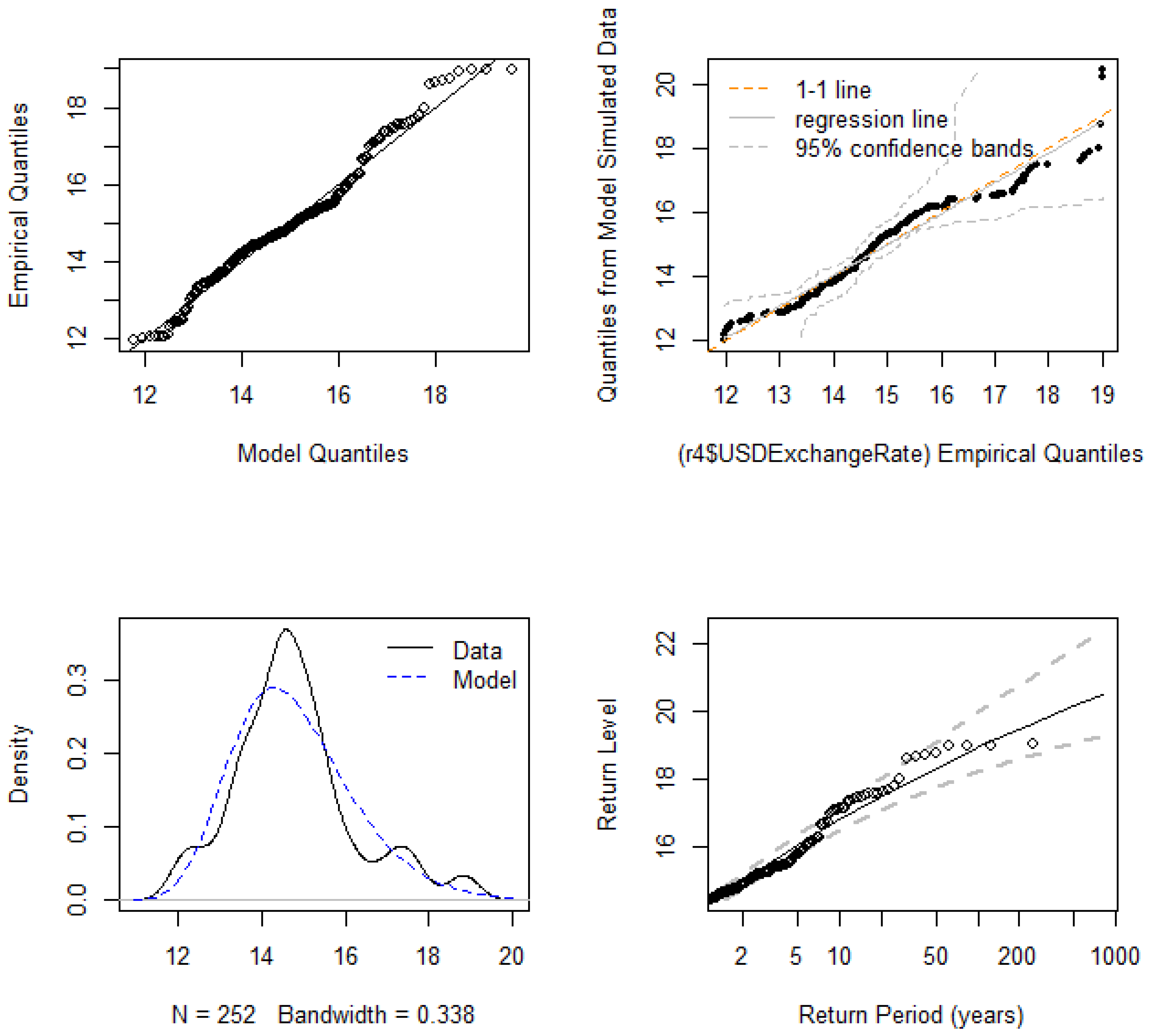

2022) applied EVT to model the monthly returns of the South African industrial index (J520) for the period from 1995 to 2018. The POT approach was used to assess the tail-related risk measure of the returns. The parameter estimation method employed in the study was MLE. Graphical assessment of goodness-of-fit of the models was carried out using approaches such as probability–probability (P-P) plots, quantile–quantile (Q-Q) plots, residual plots, scatter plots, return level and density plots. The findings of the study illustrated that the GDP provided a suitable fit for extreme gains and losses.

Rationale

Makhwiting et al. (

2014) applied the GEVD to model the tail behaviour of daily share returns of the JSE markets over the period from 2002 to 2011. The findings of the study indicated that the daily share returns of the JSE follow the Weibull class distribution, implying that the GEVD offers a better fit for the daily share returns.

Gencay and Selçuk (

2004) applied EVT to examine the performance and the value-at-risk (VaR) of the emerging markets. The study aimed at investigating the non-linear estimation and forecasting of daily stock market returns of the emerging markets. The study focused on block maxima and minima. The results indicated that the GPD was the perfect fit for the left and the right tails of daily stock market returns.

Santos da Silva and Ferraz do Nascimento (

2019) employed the Bayesian parameter estimation approach to estimate parameters of the

r-largest-order statistics applied to economic and environmental data. The study used daily maximum temperature data as well as the mean daily return index of the Sao Paulo stock exchange (BOVESPA). In addition, the GEVD parameter estimation and return levels were compared to the

r-largest-order statistics. The simulation findings showed that the Bayesian method performed comparably the same as the MLE in terms of parameter estimation. However, the Bayesian approach was more accurate compared to other estimators. The results indicated that

r-largest-order statistics is an appropriate method for analysing enormous amounts of data with reduced observations.

Several authors in South Africa applied EVT in the financial industry to model the tail behaviour of returns and financial risk using JSE financial market data concentrating on the GPD and GEVD (

Chikobvu and Jakata 2020;

Kajambeu et al. 2020;

Makatjane et al. 2021). Few studies have been conducted using advanced EVT methods in the financial sector such as the GEVD

, bGEVD, and the Poisson point process. The literature on studies that apply advanced EVT methods in the financial industry is scarce in South Africa. Thus, this study employed advanced EVT methods such as the GEVD

, bGEVD, and Poisson point process to model the behaviour of extremes of the JSE daily financial market data.

5. Conclusions and Recommendations

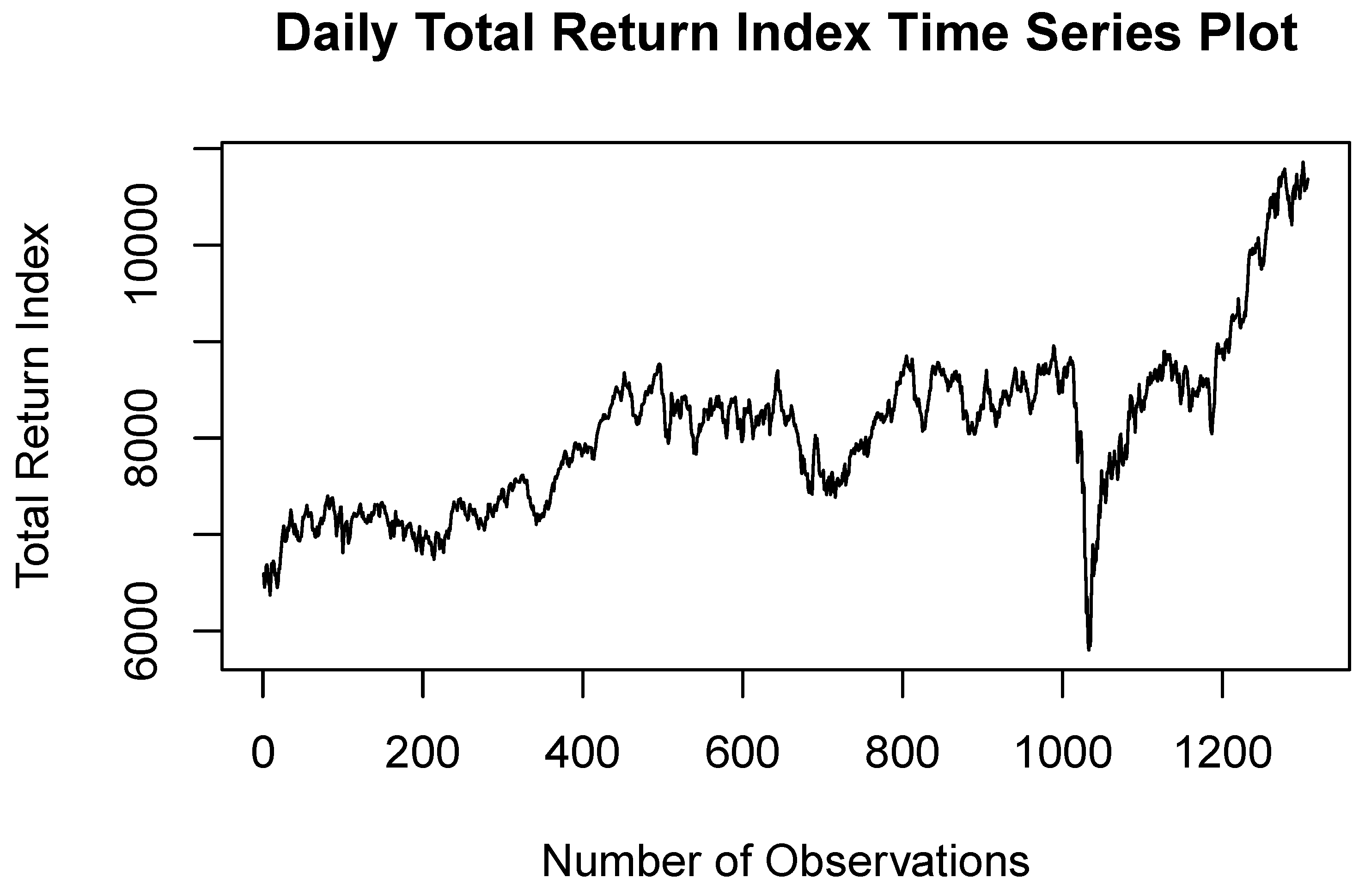

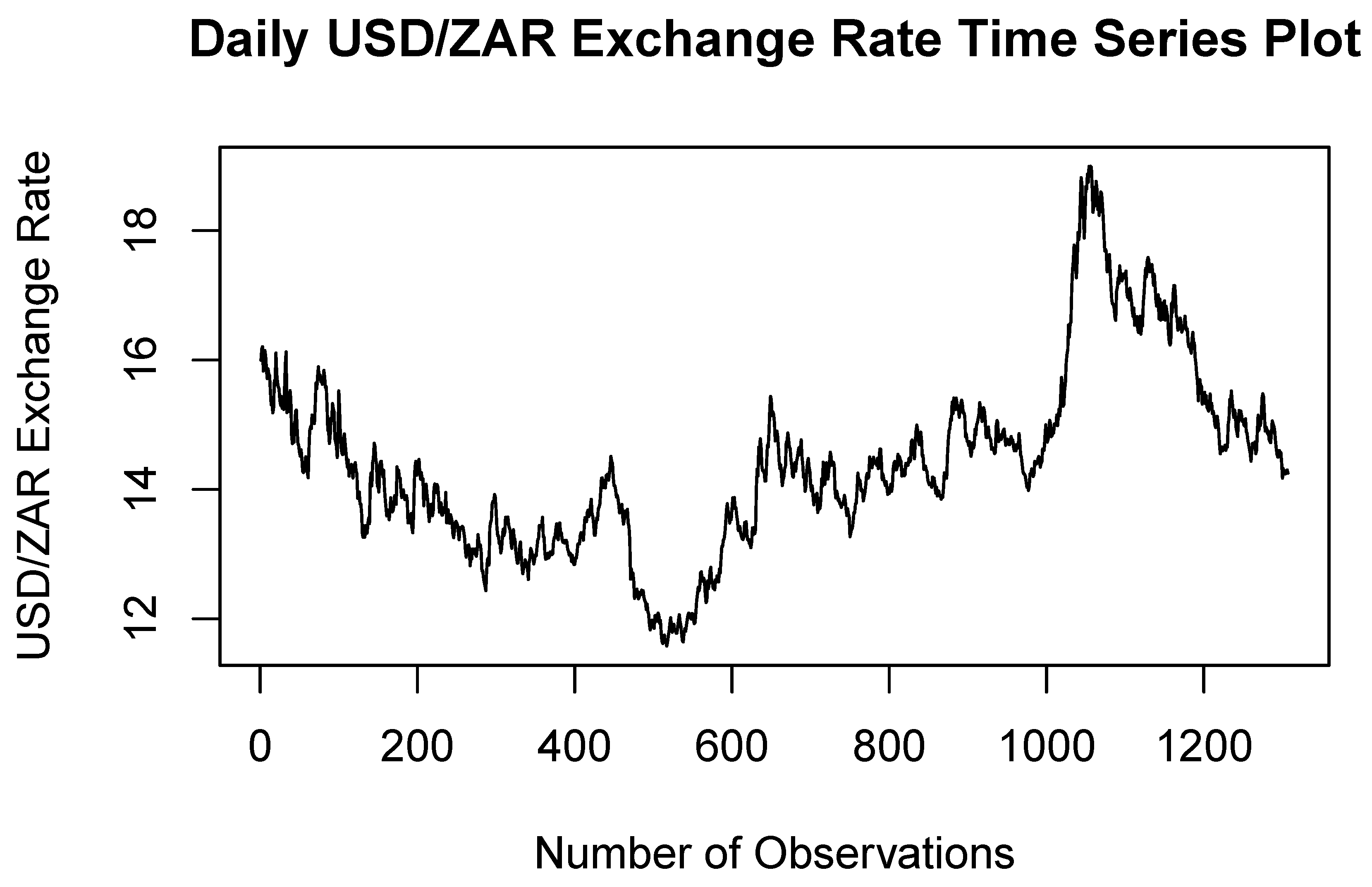

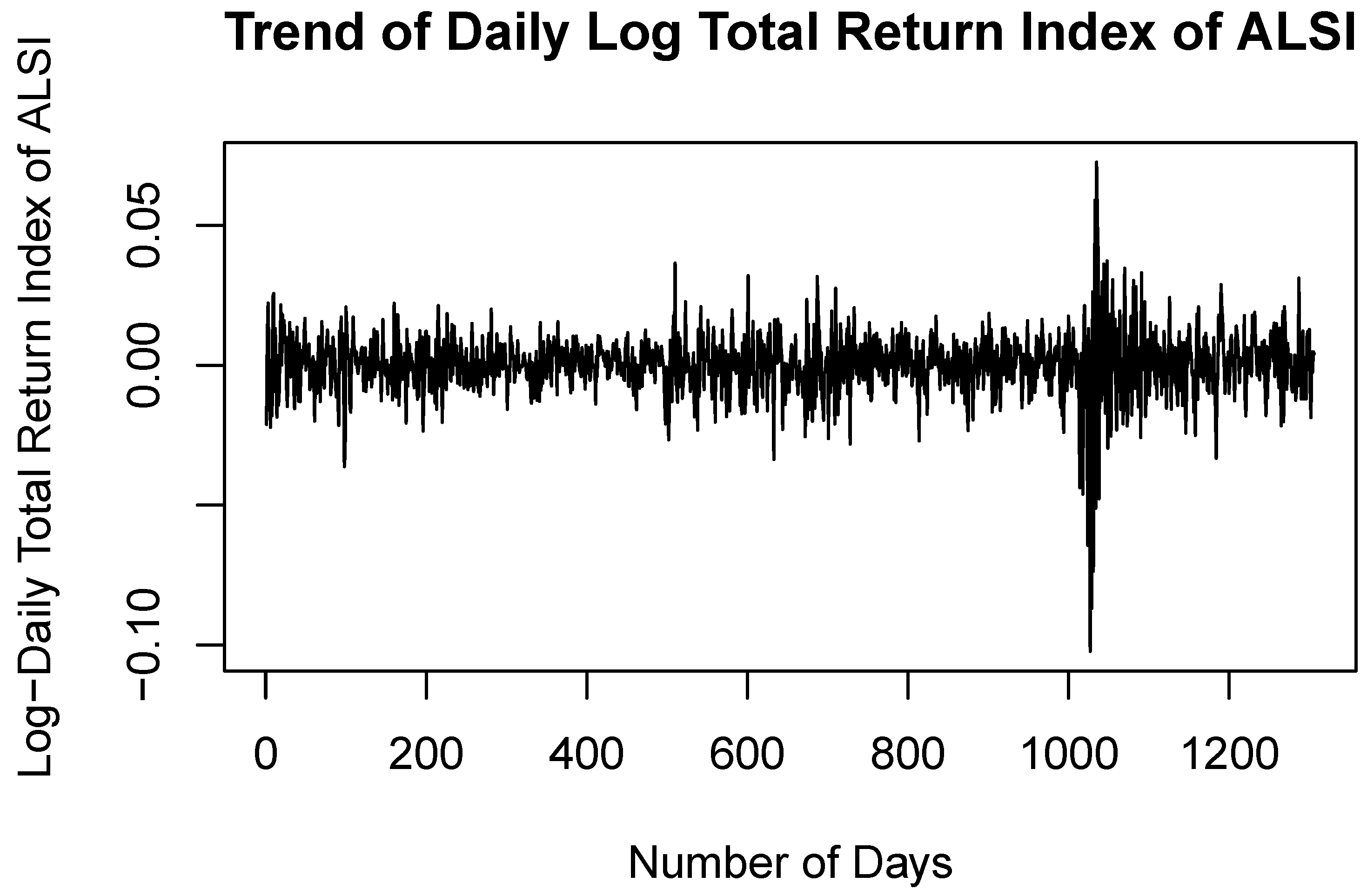

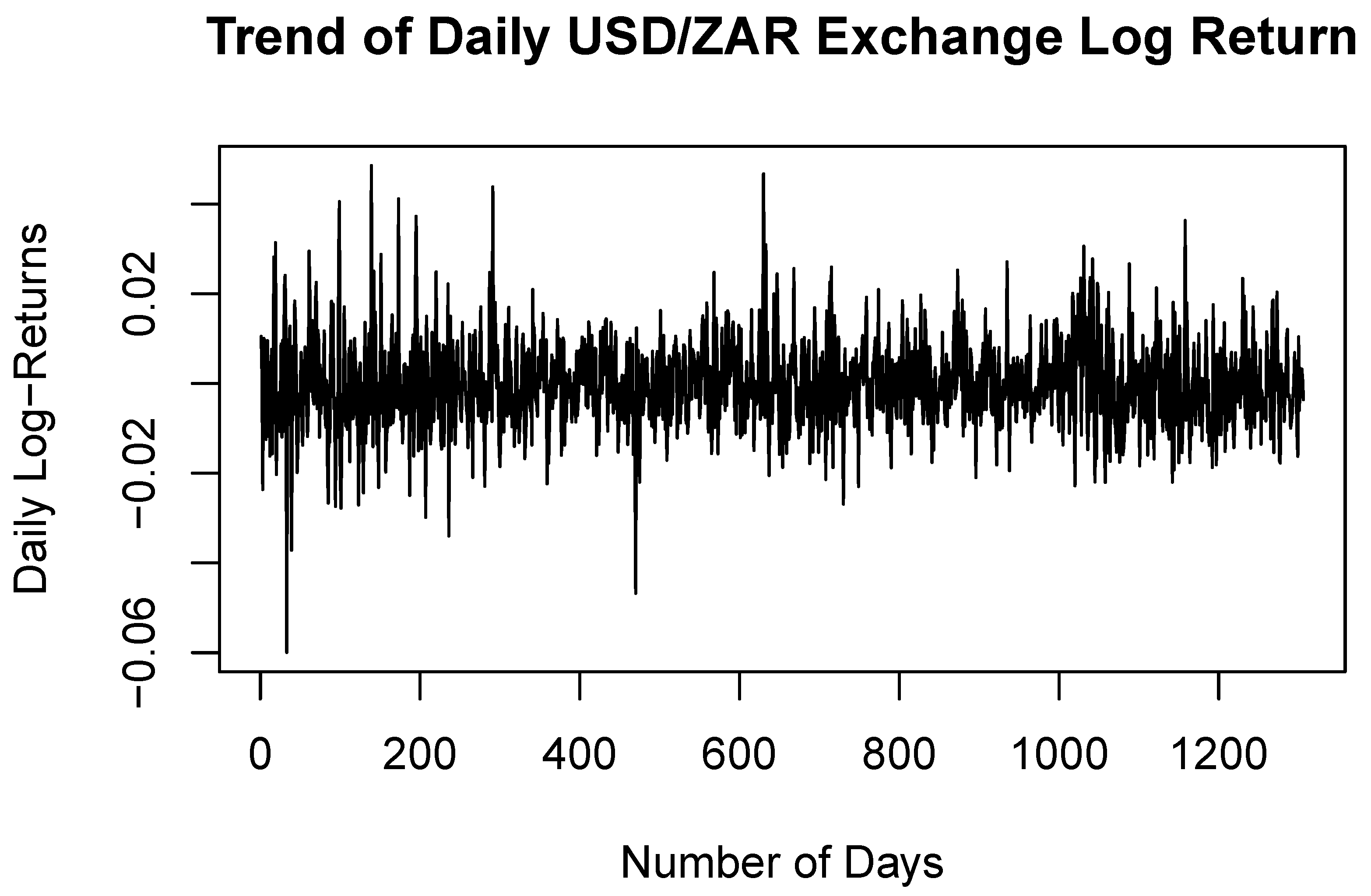

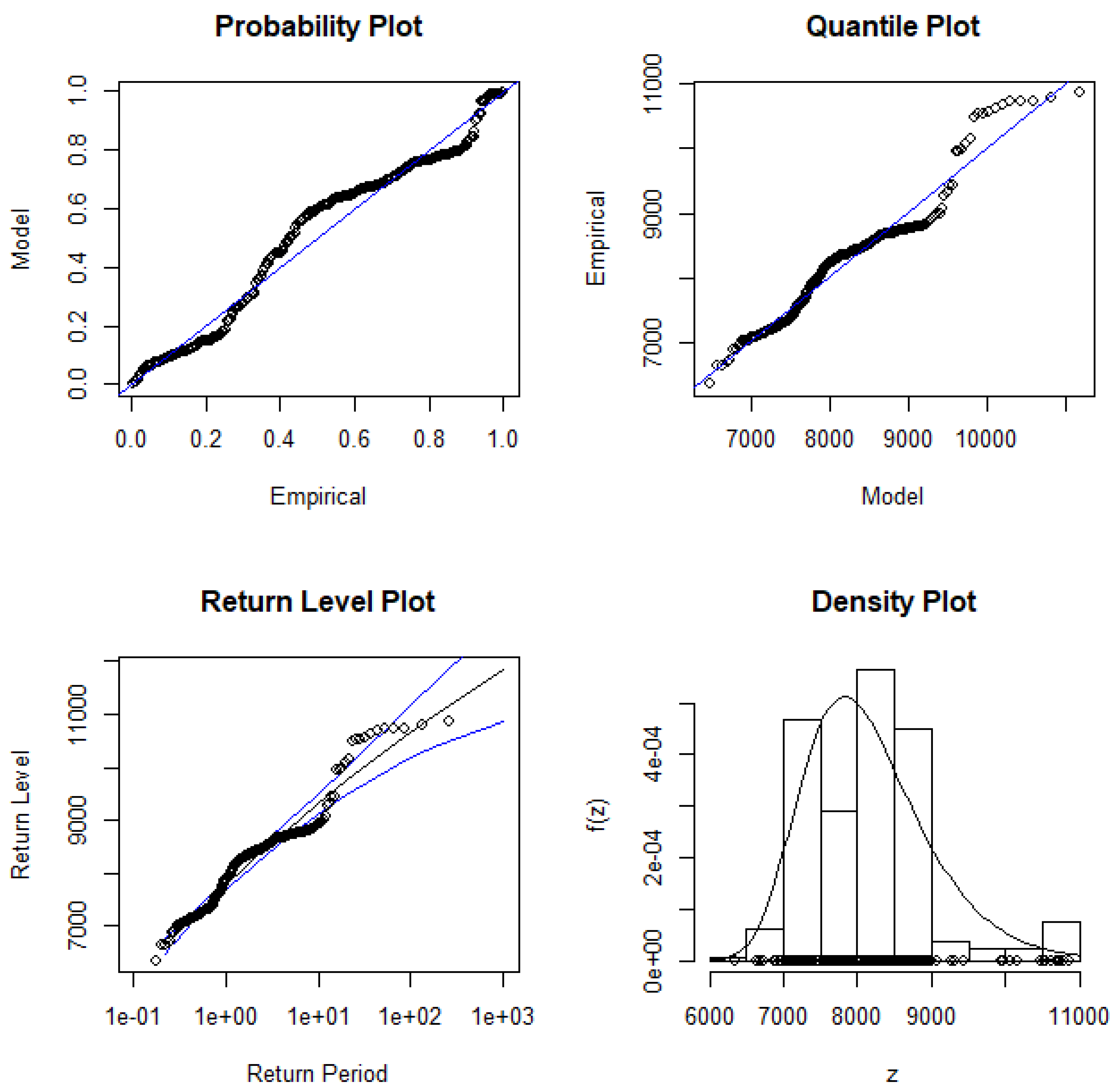

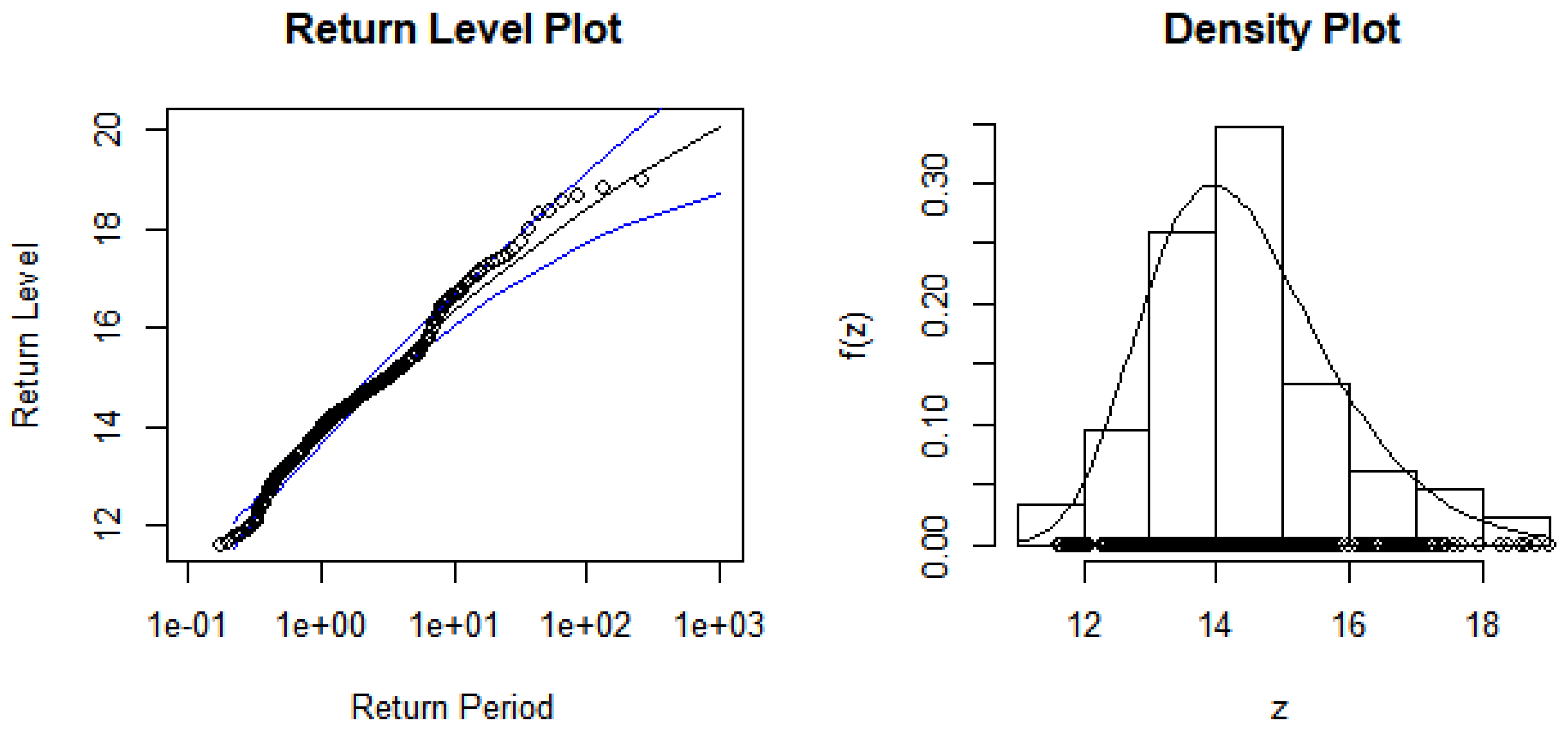

The main purpose of this study was to model the extreme behavious of the Johannesburg stock exchange (JSE) financial market data and compare the block maxima approach and the POT approach in terms of their ability in modelling the financial market data. The volatility of the markets and day-to-day fluctuation in prices were highlighted by positive spikes displaying daily profits and negative spikes showing daily losses in the study. The first recorded COVID-19 case and the first national lockdown in South Africa caused the USD–ZAR exchange rate to spike in March 2020 and reach its peak in April 2022, and there were significant losses of the ALSTRI during March 2020. The data for both the ALSTRI and USD–ZAR exchange rate stabilised after the log transformation and became stationary.

In conclusion, based on the GEVD findings, it will be expected that South Africa will experience an extreme increase in the USD–ZAR exchange rate. There will not be any unexpectedly high total returns for the ALSTRI, due to the fact that the 100-year return of the ALSTRI monthly maxima is roughly comparable to the maximum observation. The GEVD return levels reveal that the ALSTRI and USD–ZAR exchange rate will exceed 11,100.08 and R19.23, respectively, at least once in 100 years. The monthly maxima data were used in modelling the ALSTRI and the USD–ZAR exchange rate using the bGEVD method, which is an alternative to the GEVD technique. The bGEVD smoothly incorporates the left tail of a Gumbel distribution and the right tail of a Fréchet distribution. The results reveal that there is a positive linear trend term indicating an increase in the ALSTRI and the USD–ZAR exchange rate over time. The explanatory variables have a greater effect on the location parameter. The 100-year return levels are slightly equivalent to the maximum observed values for both the ALSTRI and the USD–ZAR exchange rate. Thus, the bGEVD return levels reveal that the ALSTRI and the USD–ZAR exchange rate will exceed 10,860 and R18.99, respectively. In conclusion, the findings of the return levels for the bGEVD and GEVD models suggest that the two models result in similar outcomes. This implies that bGEVD can be a feasible alternative to the GEVD for modelling block maxima. The 100-year return levels of the monthly GEVD, bGEVD, and GEVD models are almost equal to the maximum observations of the financial markets, while the 100-year return levels for the GPD and the Poisson point process models were very much higher than the maximum observations of the financial market data. The Poisson point process return level estimates are quite comparable with the GPD estimates. In actual fact, the ALSTRI and USD–ZAR exchange rate will surpass 17,501.63 and R23.72, respectively, at least once in 100 years. Overall, the findings in this study suggest that investors will experience higher gains in the total returns of the ALSI. The USD–ZAR exchange rate return levels suggest that the ZAR will become more unstable in the long run. As the ZAR goes higher it will affect the inflation and the economy of South Africa. The USD will become much stronger, and this will affect the ZAR as the USD appreciates or strengthens, which will depreciate or weaken the South African currency.

In conclusion, both the block maxima and POT approaches have revealed long-run increases in the ALSTRI and USD–ZAR exchange rate. One of the major findings of this study is that the return level estimates of the block maxima and POT approaches are not comparable for the JSE financial market data, although both approaches can be used to predict future volatility in the financial markets. The study further revealed that the bGEVD is more suitable for relatively short-term forecasting since it cuts off at the 50-year return level.

5.1. Recommendations

There are rare events that contribute towards the negative impact on the financial markets, such as pandemics and financial crises. Due to the instability and unpredictability of the financial markets, the manifestation of the financial crises and pandemics can put investors, financial economists, and risk experts in an uneasy situation, not knowing whether the investments will return gains or losses, as well as not knowing the impact of these rare events on the stock and financial markets. Financial market volatility can result in risk, whether big or small, that can be concealed in the tails rather than the mean. Therefore, it is recommended that risk management systems consider cutting-edge techniques such as advanced EVT methods, which comprise, among others, the Poisson point process, r-largest-order statistics, and bGEVD for anticipating the uncommon extreme occurrences with significant ramifications that could be harmful to the financial industry. Financial disasters can be mitigated by using the advanced EVT techniques to identify and examine the characteristics of extreme value behaviour and thereby prevent the risk. The insufficient amount of data available for model estimation is an inherent challenge in any extreme value investigation. Since extremes are by definition rare, the model estimates, particularly those of extreme return levels, have a high degree of variance. Instead of focusing merely on the traditional methods of block maxima, the use of advanced extreme value methods that accommodates even small datasets such as r-largest-order statistics, bGEVD, and the Poisson point process is encouraged. The use of statistical methods that can predict the occurrence of extremes, focusing on the tails of the distribution to predict the future events, is recommended.

5.2. Future Studies

The researchers discovered that there are no studies conducted on bGEVD in the field of finance or financial markets. In the future, more studies on bGEVD, vine copulas, and r-largest-order bGEVD can be conducted in the financial markets and/or finance sector. The frequency of the occurrence of extreme returns in the financial sector can be studied to assist in enhancing risk management systems.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}