Evaluation of Factors Contributing to the Effectiveness of Internal Audit Quality in Pakistani Commercial Banks

Abstract

:1. Introduction

- (a)

- Internal audit function must involve formal standing, responsibilities, powers and authorities with the help of international best practices, guidelines, and standards etc.

- (b)

- To maintain the internal audit effectiveness, the internal control environment must be effective for the internal auditor openly and independently express their opinion on different affairs.

- (c)

- Chief internal auditors, auditors, and managers must perform day-to-day roles and responsibilities and proper check and balance on every activity while performing audit.

- (d)

- Internal auditors have free access to banks records, data, files, information, meeting, properties, and people.

- (e)

- According to the nature of the problem and situation IAF provided consultancy if required.

- (f)

- Independence of internal auditors depends on the IAF that is set by the organization.

- (g)

- The basic report system of who reports to whom in IAF provides clear insights to BAC and related members, such as internal stakeholders.

- (h)

- In case of external suggestions, opinion if require it’s all clearly defined to what extent is needed mentioned in IAF.

- (i)

- In this charter also defined to what extent CIA evaluation mechanisms are included.

- (j)

- It is mandatory that assurance of IAF must be assessed by IIA standards and periodically updated with time and situation.

2. Background of the Study and Research Hypotheses

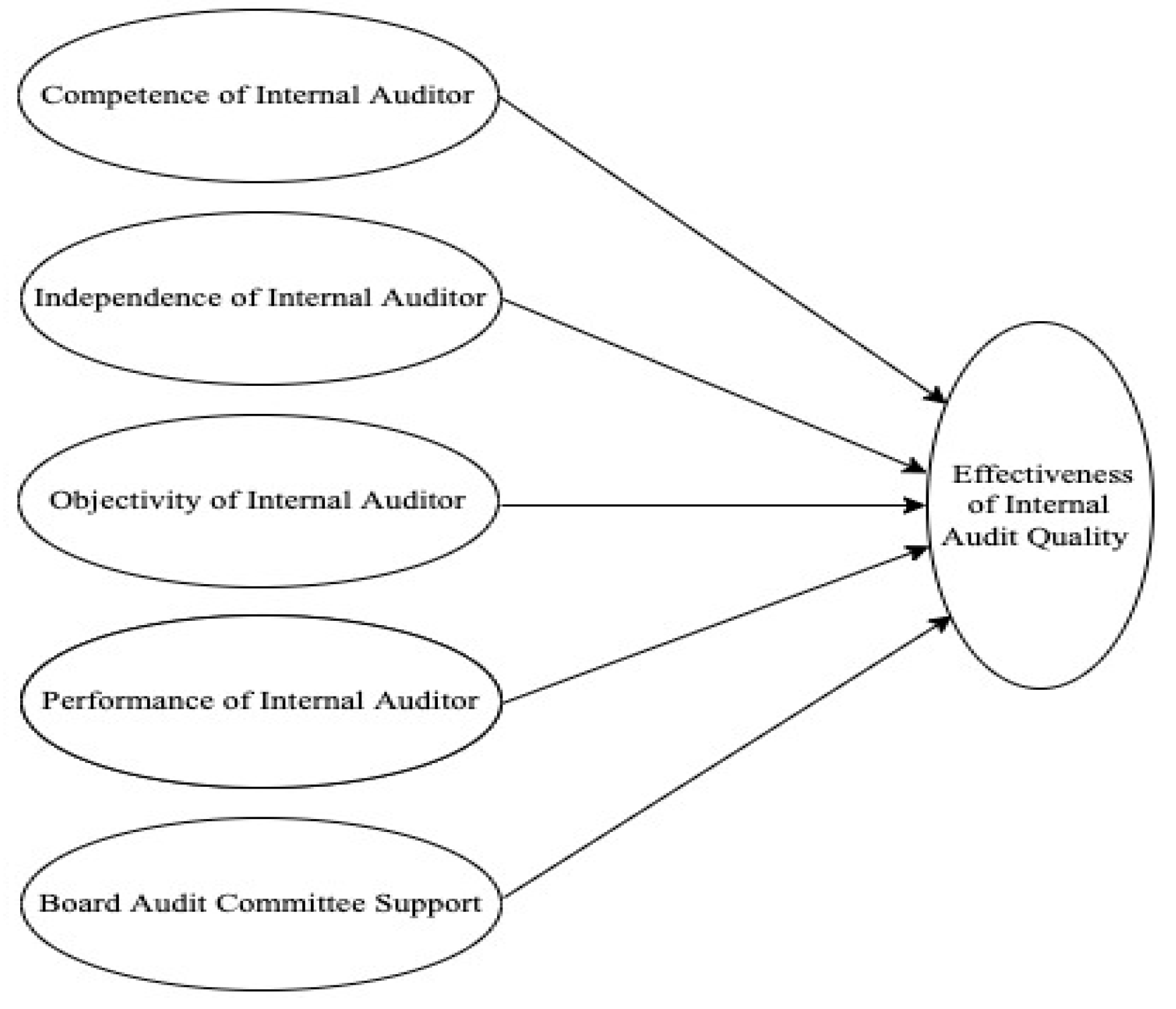

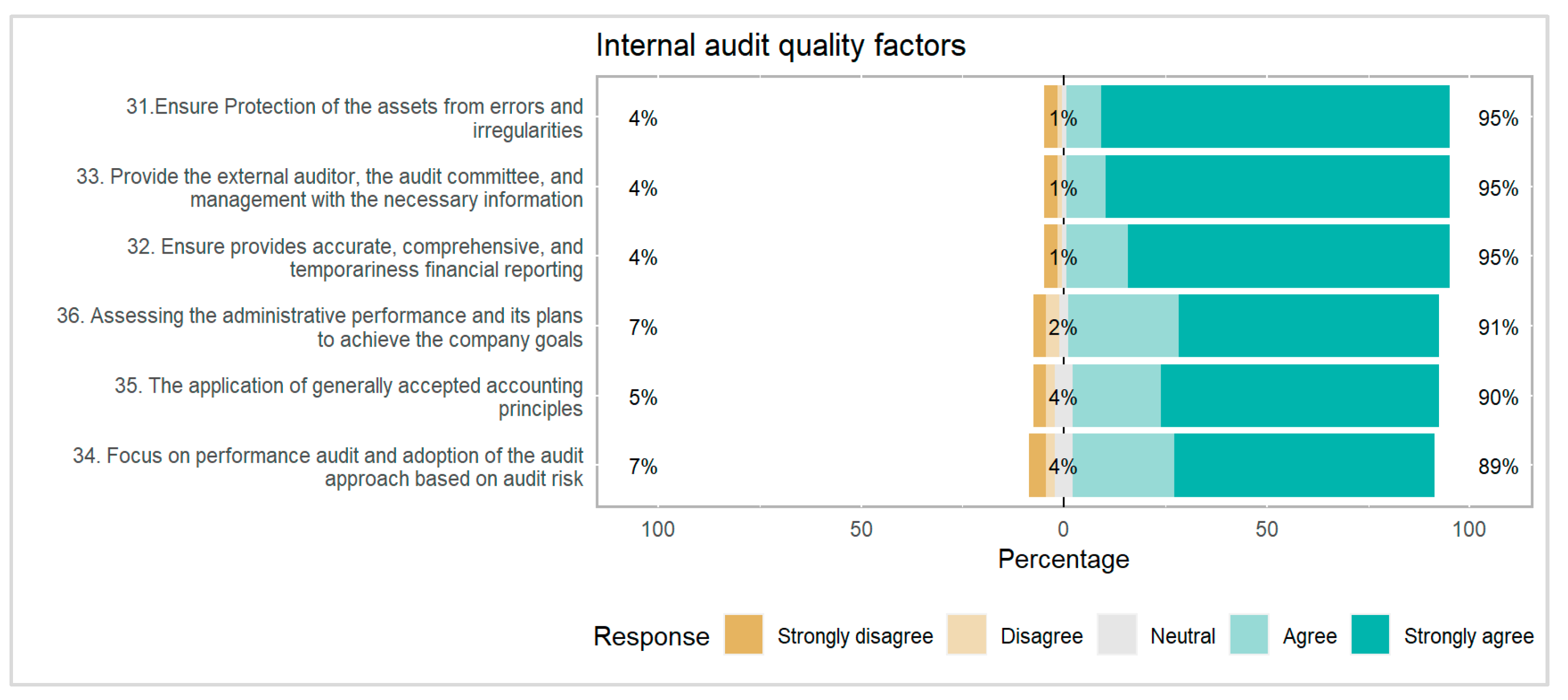

2.1. Effectiveness of Internal Audit Quality

2.2. Research Hypothesis

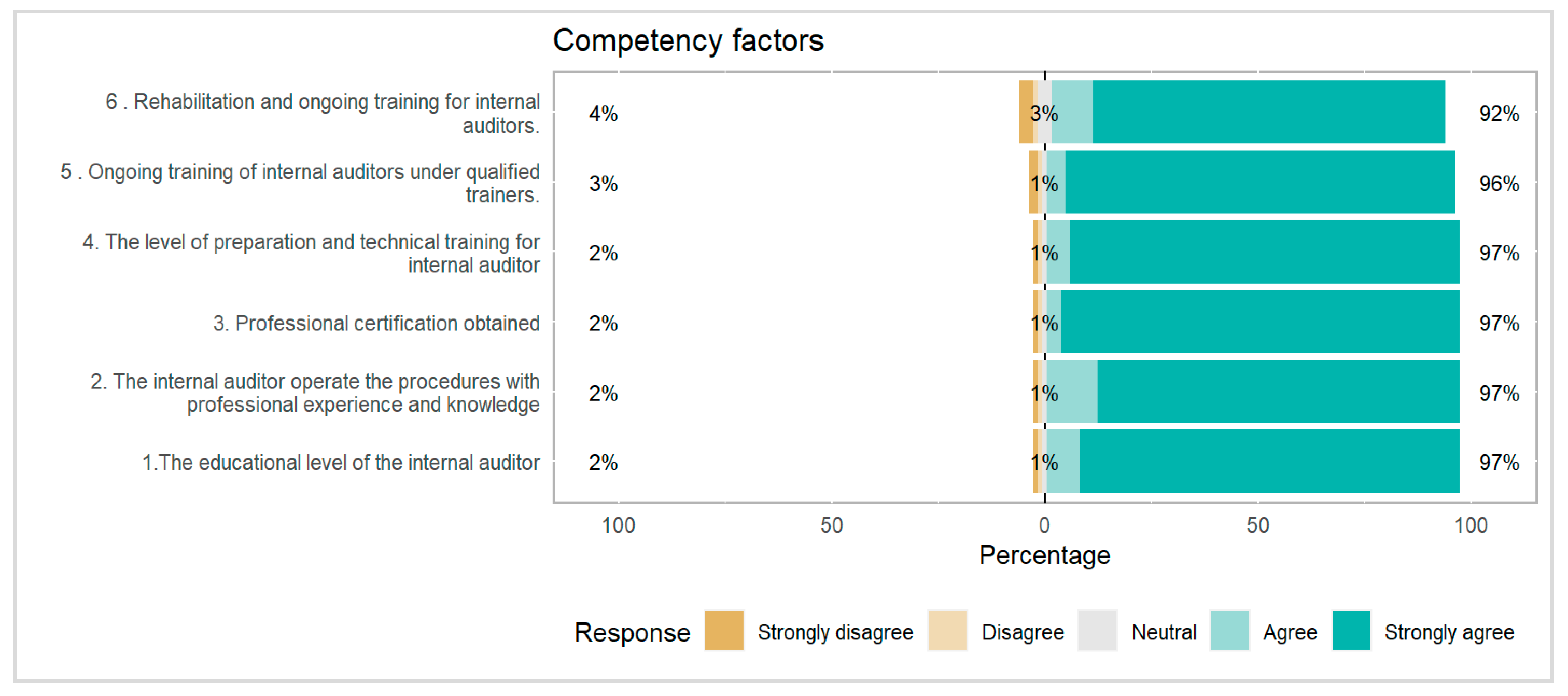

2.3. Competence of Internal Auditor

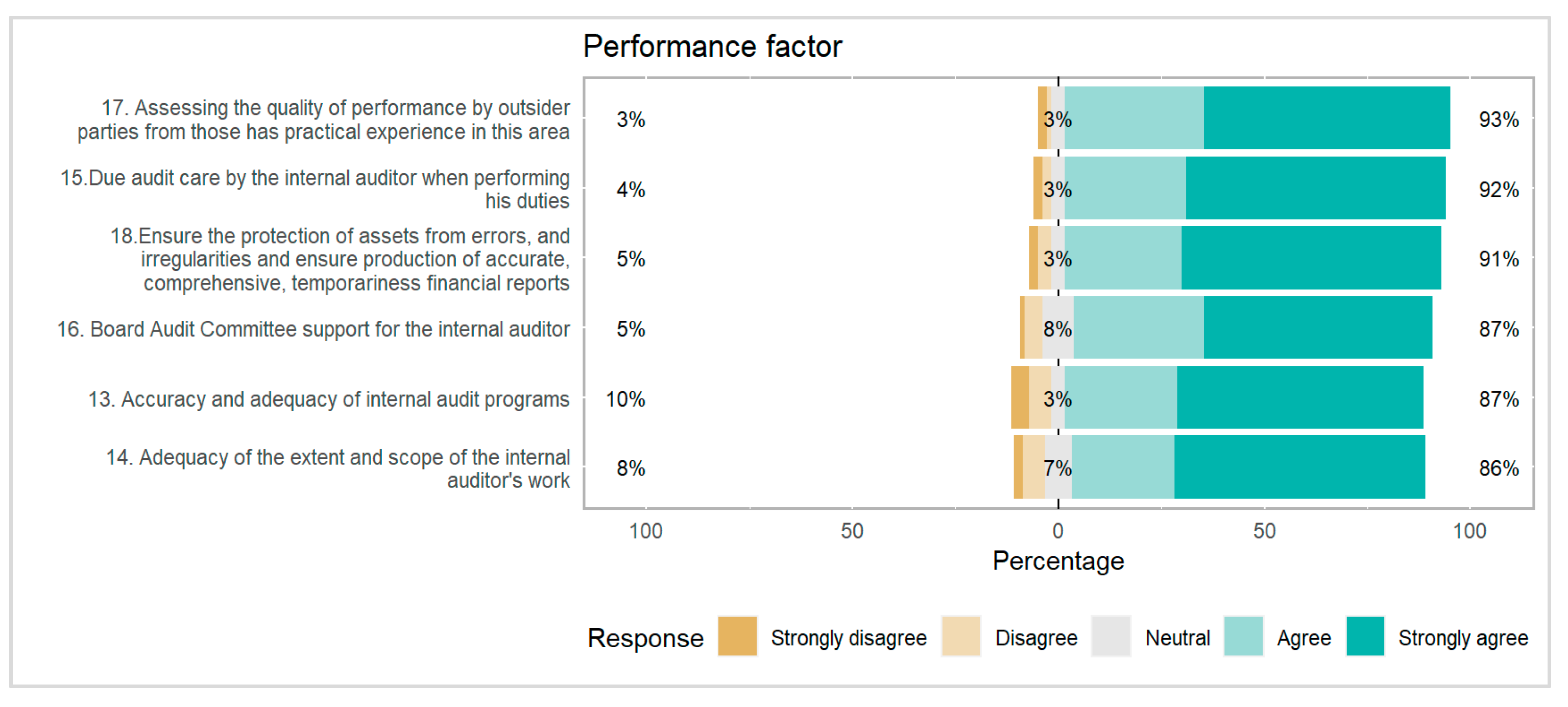

2.4. Performance of Internal Auditor

2.5. Independence of Internal Auditor

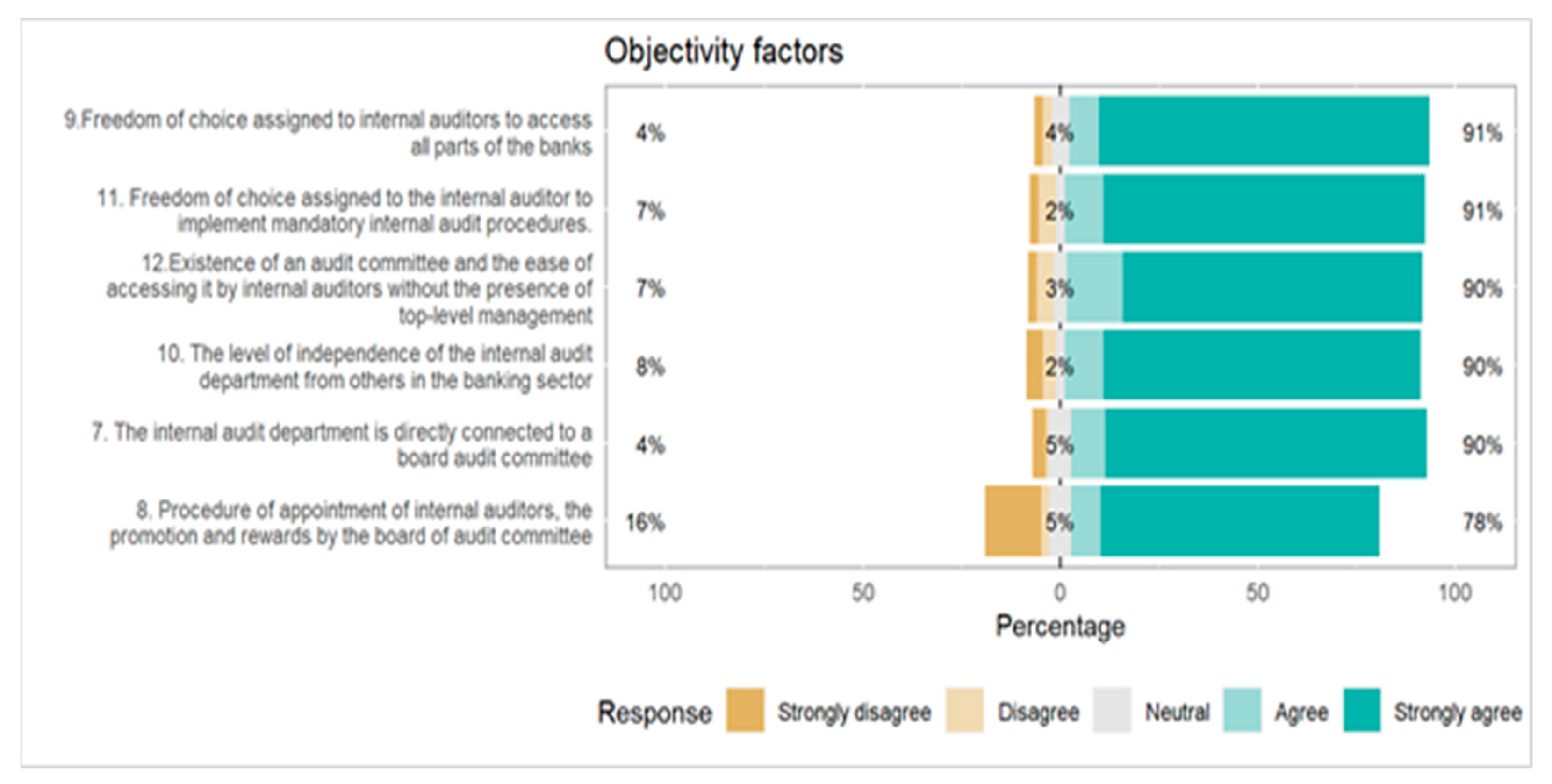

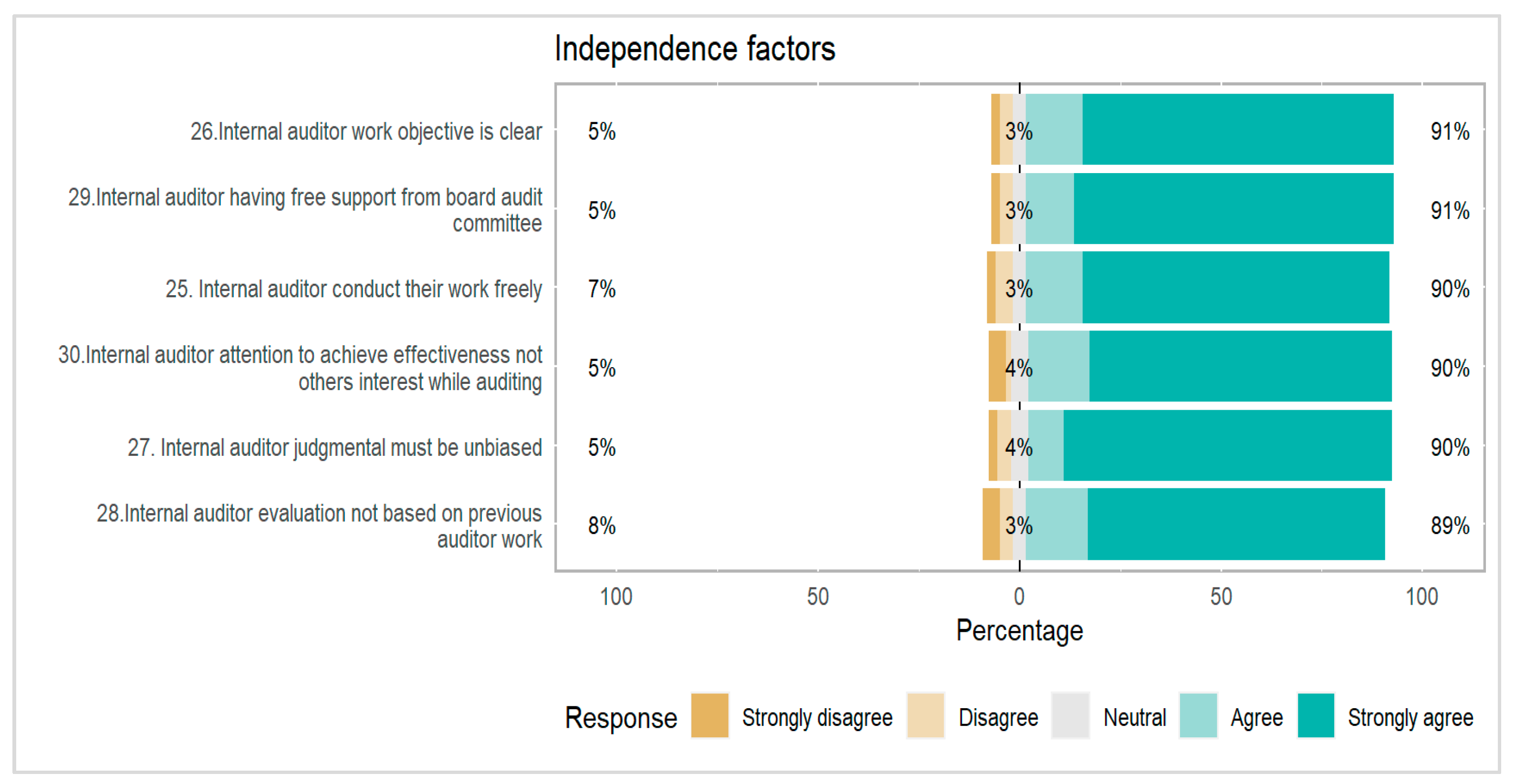

2.6. Objectivity of Internal Auditor

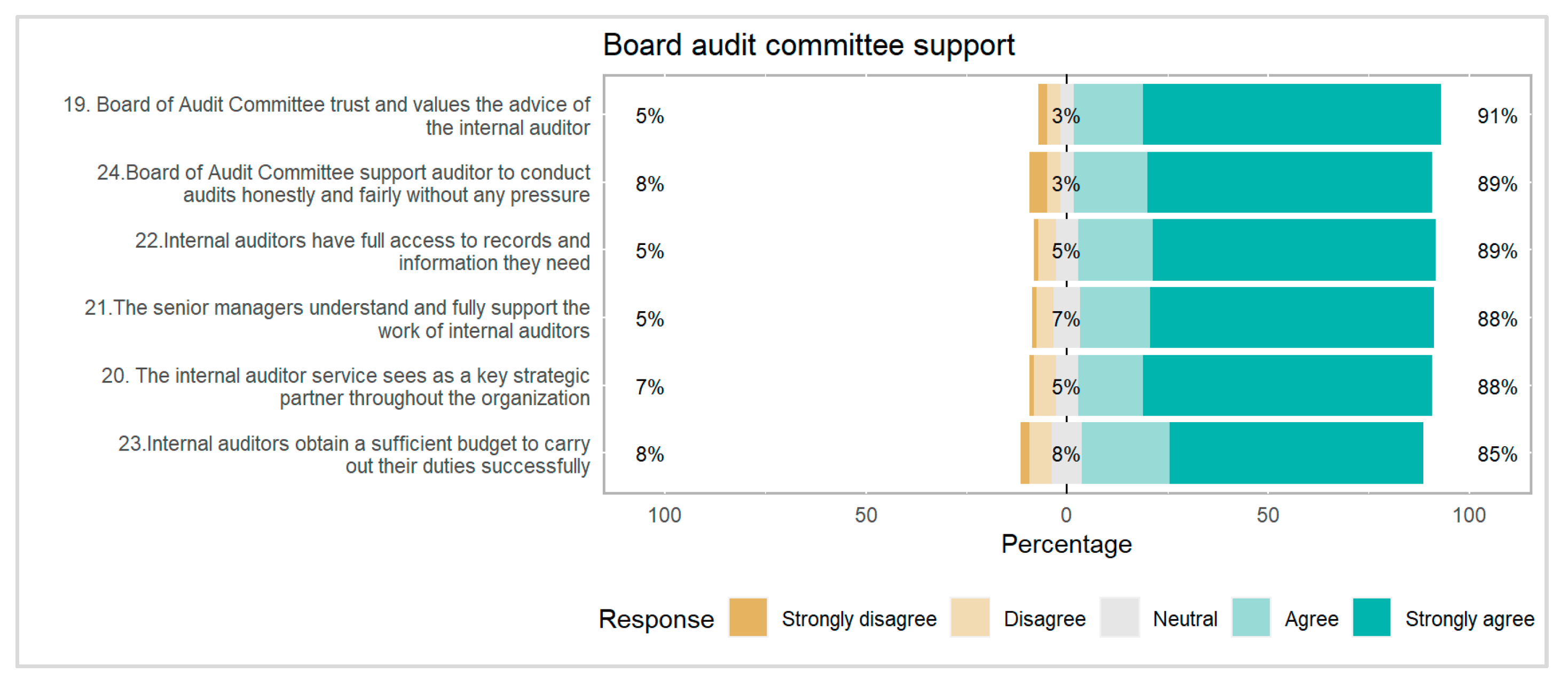

2.7. Board Audit Committee Support

3. Research Methodology

3.1. Research Data

3.2. Research Approach

3.3. Sample and Data Collection

3.4. Research Model Development

3.5. The Logit Model

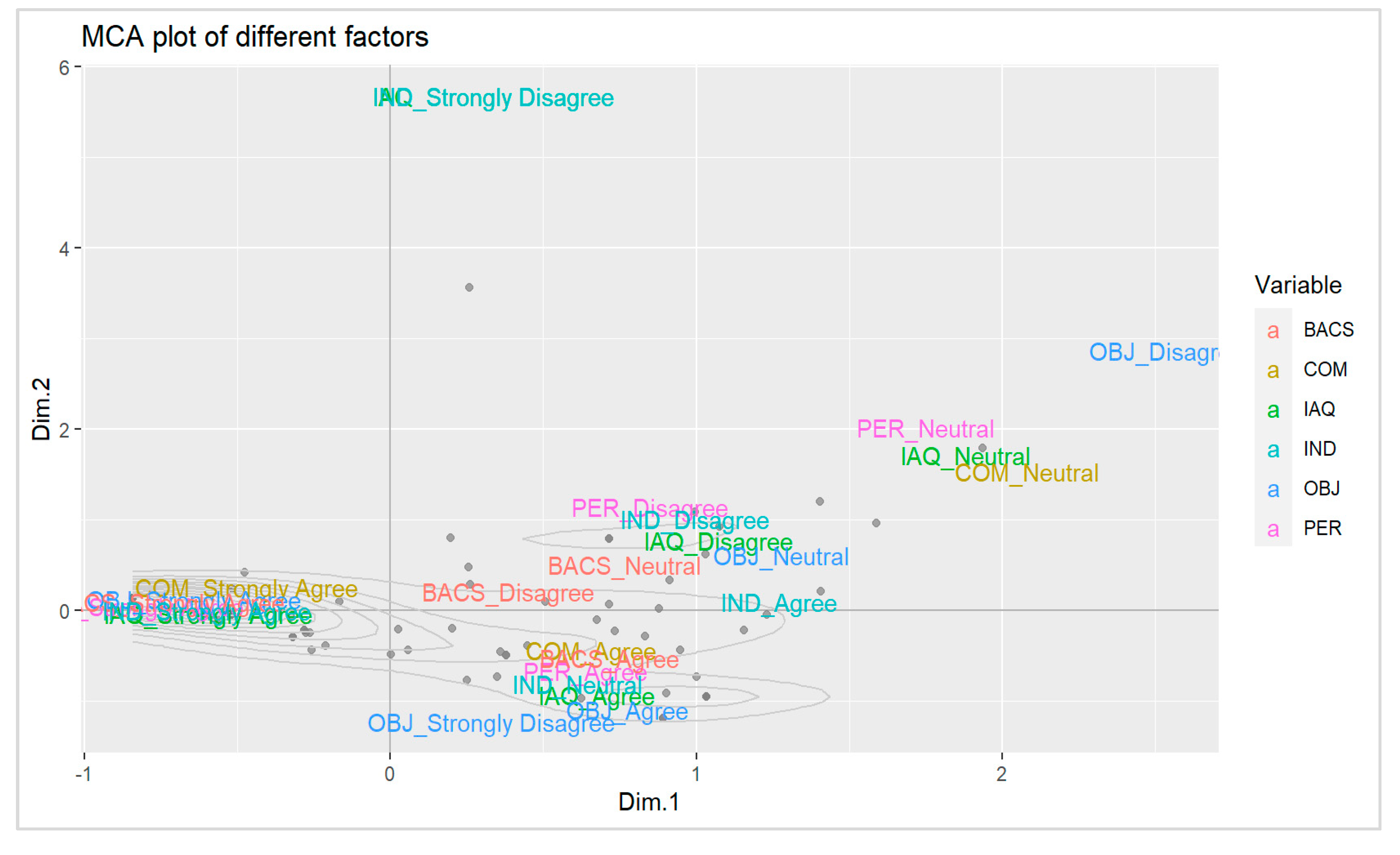

4. Results of the Study

5. Conclusions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abdelrahim, Ayman, and Husam-Aldin N. Al-Malkawi. 2022. The Influential Factors of Internal Audit Effectiveness: A Conceptual Model. International Journal of Financial Studies 10: 71. [Google Scholar] [CrossRef]

- Ado, Abdullahi Bala, Norfadzilah Rashid, Umar Aliyu Mustapha, and Lateef Saheed Ademola. 2020. The impact of audit quality on the financial performance of listed companies Nigeria. Journal of Critical Reviews 7: 37–42. [Google Scholar]

- Ahmet, O. N. A. Y. 2021. Factors affecting the internal audit effectiveness: A research of the Turkish private sector organizations. Ege Academic Review 21: 1–15. [Google Scholar]

- Al Nuaimi, Bader Khamis, Mehmood Khan, and Mian Ajmal. 2020. Implementing sustainable procurement in the United Arab Emirates public sector. Journal of Public Procurement 2: 97–117. [Google Scholar] [CrossRef]

- Al-Okaily, Manaf, Hamza Mohammad Alqudah, Anas Ali Al-Qudah, and Abeer F. Alkhwaldi. 2022. Examining the critical factors of computer-assisted audit tools and techniques adoption in the post-COVID-19 period: Internal auditors’ perspective. VINE Journal of Information and Knowledge Management Systems 12: 0311. [Google Scholar] [CrossRef]

- Alqudah, Hamza Mohammad, Noor Afza Amran, and Haslinda Hassan. 2019. Factors affecting the internal auditors’ effectiveness in the Jordanian public sector: The moderating effect of task complexity. EuroMed Journal of Business 3: 251–73. [Google Scholar] [CrossRef]

- Alsabti, Haider Alaaldin, and Azam Abdelhakeem Khalid. 2022. Factors Influencing Internal Accounting And Financial Audit Effectiveness: Evidence From Oman. Academy of Accounting and Financial Studies Journal 26: 1–11. [Google Scholar]

- Alzeban, Abdulaziz, and David Gwilliam. 2014. Factors affecting the internal audit effectiveness: A survey of the Saudi public sector. Journal of International Accounting, Auditing and Taxation 23: 74–86. [Google Scholar] [CrossRef]

- Anojan, Vickneswaran. 2022. Factors Affecting Internal Audit Reporting on Public Sector in Sri Lanka. Journal of Accounting and Business Education 6: 22–33. [Google Scholar] [CrossRef]

- Badara, Mu’azu Saidu, and Siti Zabedah Saidin. 2013. The relationship between audit experience and internal audit effectiveness in the public sector organizations. International Journal of Academic Research in Accounting, Finance and Management Sciences 3: 329–39. [Google Scholar] [CrossRef] [PubMed]

- Baharud-din, Zulkifli, Alagan Shokiyah, and Mohd Serjana Ibrahim. 2014. Factors that contribute to the effectiveness of internal audit in public sector. International Proceedings of Economics Development and Research 70: 126. [Google Scholar]

- Cohen, Aaron, and Gabriel Sayag. 2010. The effectiveness of internal auditing: An empirical examination of its determinants in Israeli organisations. Australian Accounting Review 20: 296–307. [Google Scholar] [CrossRef]

- Dellai, Hella, and Mohamed Ali Brahim Omri. 2016. Factors affecting the internal audit effectiveness in Tunisian organizations. Research Journal of Finance and Accounting 7: 208–11. [Google Scholar]

- El Gharbaoui, Bouteïna, and Abdeslam Chraibi. 2021. Internal audit quality and financial performance: A systematic literature review pointing to new research opportunities. Revue International des Sciences de Gestion 4: 2. [Google Scholar]

- Enekwe, Chinedu, Chike Nwoha, and Sergius Nwannebuike Udeh. 2020. Effect of audit quality on financial performance of listed manufacturing firms in nigeria (2006–2016). Advance Journal of Management, Accounting and Finance 5: 1–12. [Google Scholar]

- Filfilan, Assaf. 2022. Determinants of internal audit effectiveness: Evidence from Saudi Arabia. Journal of Management Information & Decision Sciences 25: 158–60. [Google Scholar]

- George, Drogalas, Karagiorgos Theofanis, and Arampatzis Konstantinos. 2015. Factors associated with internal audit effectiveness: Evidence from Greece. Journal of Accounting and Taxation 7: 113–22. [Google Scholar]

- Gramling, Audrey A., Mario J. Maletta, Arnold Schneider, and Bryan K. Church. 2004. The role of the internal audit function in corporate governance: A synthesis of the extant internal auditing literature and directions for future research. Journal of Accounting literature 23: 194. [Google Scholar]

- Gros, Marius, Sebastian Koch, and Christoph Wallek. 2017. Internal audit function quality and financial reporting: Results of a survey on German listed companies. Journal of Management & Governance 21: 291–329. [Google Scholar]

- Hazaea, Saddam A., Jinyu Zhu, Nabil Alsharabi, Saleh F. A. Khatib, and Li Yueying. 2020a. On the effectiveness of audit committee characteristics in commercial banks: Evidence From Yemen. Journal of Critical Reviews 7: 2096–115. [Google Scholar]

- Hazaea, Saddam A., Jinyu Zhu, Saleh F. A. Khatib, and Muhammad Arshad. 2020b. A comparative study of the internal audit system between China and the Gulf Cooperation council countries. Proceeding of International Conference on Business, Economy, Management and Social Studies towards Sustainable Economy 1: 1–7. [Google Scholar]

- Hazaea, Saddam A., Mosab I. Tabash, Saleh F. A. Khatib, Jinyu Zhu, and Ahmed A. Al-Kuhali. 2020c. The impact of internal audit quality on financial performance of Yemeni commercial banks: An empirical investigation. The Journal of Asian Finance, Economics and Business 7: 867–75. [Google Scholar] [CrossRef]

- Hoai, Tu Thanh, Bui Quang Hung, and Nguyen Phong Nguyen. 2022. The impact of internal control systems on the intensity of innovation and organizational performance of public sector organizations in Vietnam: The moderating role of transformational leadership. Heliyon 8: 08954. [Google Scholar] [CrossRef] [PubMed]

- Joshi, Prem Lal. 2022. The Institutional Theory on the Internal Audit Effectiveness: The Case of India. Iranian Journal of Management Studies 15. [Google Scholar]

- Jung, Yusun, and Moon-Kyung Cho. 2022. Impacts of reporting lines and joint reviews on internal audit effectiveness. Managerial Auditing Journal 4: 486–518. [Google Scholar] [CrossRef]

- Kassie, Workneh Dilie. 2021. Bank Specific Determinants of Internal Audit Effectiveness: Evidence from Private Banks in Ethiopia. Order 13: 5. [Google Scholar]

- Khatib, Saleh F. A., Dewi Fariha Abdullah, Ahmed A. Elamer, and Raed Abueid. 2021. Nudging toward diversity in the boardroom: A systematic literature review of board diversity of financial institutions. Business Strategy and the Environment 30: 985–1002. [Google Scholar] [CrossRef]

- Le, Thi Tam, Thi Mai Anh Nguyen, and Thi Hai Chau Ngo. 2022. Risk-based approach and quality of independent audit using structure equation modeling–Evidence from Vietnam. European Research on Management and Business Economics 28: 100196. [Google Scholar] [CrossRef]

- Lenz, Rainer, and Ulrich Hahn. 2015. A synthesis of empirical internal audit effectiveness literature pointing to new research opportunities. Managerial Auditing Journal 30: 5–33. [Google Scholar] [CrossRef]

- Lenz, Rainer, Gerrit Sarens, and Kim Klarskov Jeppesen. 2018. In search of a measure of effectiveness for internal audit functions: An institutional perspective. Edpacs 58: 1–36. [Google Scholar] [CrossRef]

- Li, Xiao. 2022. The mediating effect of internal control for the impact of institutional shareholding on corporate financial performance. Asia-Pacific Journal of Financial Studies 51: 194–222. [Google Scholar] [CrossRef]

- Muñoz-Izquierdo, N., M. D. M. Camacho-Miñano, M. J. Segovia-Vargas, and D. Pascual-Ezama. 2019. Is the external audit report useful for bankruptcy prediction? Evidence using artificial intelligence. International Journal of Financial Studies 7: 20. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai. 2020. Audit committee structure and bank stability in Vietnam. ACRN Journal of Finance and Risk Perspectives 8: 240–55. [Google Scholar]

- Nguyen, Quang Khai. 2022. Audit committee structure, institutional quality, and bank stability: Evidence from ASEAN countries. Finance Research Letters 46: 102369. [Google Scholar] [CrossRef]

- Octavia, Evi. 2013. The effects of implementation on internal audit and good corporate governance in corporate performance. Journal of Global Business & Economics 6: 77–87. [Google Scholar]

- Otache, Innocent, Ifeoma Jeraldine Echukwu, Kadiri Umar, Acho Yunusa, and Samson Audu. 2022. Internal factors affecting the performance of employee-based savings and credit cooperatives: Evidence from Nigeria. Journal of Enterprising Communities: People and Places in the Global Economy. ahead-of-print. [Google Scholar] [CrossRef]

- Phan, T., T. Lai Le, and D. Tran. 2020. The impact of audit quality on performance of enterprises listed on Hanoi Stock Exchange. Management Science Letters 10: 217–24. [Google Scholar] [CrossRef]

- Pooe, Jabile Brenda, Karin Barac, Kato Plant, and Blanche Steyn. 2022. Signalling of internal audit effectiveness. South African Journal of Accounting Research 36: 213–49. [Google Scholar] [CrossRef]

- Potjanajaruwit, Pisit. 2022. The Structural Relationship between Personnel’s Professional Skills, Internal Control System, and Efficiency of Supply Management of Transport Organization in Thailand. Transportation Research Procedia 63: 2434–41. [Google Scholar] [CrossRef]

- Prasad, Nishaal, David Hay, and Li Chen. 2022. Use of in-house internal audit functions in New Zealand. Meditari Accountancy Research. ahead-of-print. [Google Scholar] [CrossRef]

- Singh, Karpal Singh Dara, Sajitha Ravindran, Yuvaraj Ganesan, Ghazanfar Ali Abbasi, and Hasnah Haron. 2021. Antecedents and internal audit quality implications of internal audit effectiveness. International Journal of Business Science & Applied Management (IJBSAM) 16: 1–21. [Google Scholar]

- Ta, Thu Trang, and Thanh Nga Doan. 2022. Factors affecting internal audit effectiveness: Empirical evidence from Vietnam. International Journal of Financial Studies 10: 37. [Google Scholar] [CrossRef]

- Turetken, Oktay, Stevens Jethefer, and Baris Ozkan. 2020. Internal audit effectiveness: Operationalization and influencing factors. Managerial Auditing Journal 35: 238–71. [Google Scholar] [CrossRef]

- Umar, Hussaini, and Muhammed Umar Dikko. 2018. The effect of internal control on performance of commercial banks in Nigeria. International Journal of Management Research 8: 13–32. [Google Scholar]

- Vashdi, Dana R., Anna Uster, Eran Vigoda-Gadot, and Moshe Mizrahi. 2022. Is Auditing Worth the Effort? The Impact of Internal Auditing on Local Fiscal Outcomes. Public Performance & Management Review 45: 1398–430. [Google Scholar]

- Wang, Xiong, Fernando AF Ferreira, and Ching-Ter Chang. 2022. Multi-objective competency-based approach to project scheduling and staff assignment: Case study of an internal audit project. Socio-Economic Planning Sciences 81: 101182. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Bank Name | Frequency | Percentage |

|---|---|---|

| Al Baraka | 1 | 1.09 |

| Allied Bank Limited | 4 | 4.35 |

| Askari Bank | 4 | 4.35 |

| Bank Al Habib | 4 | 4.35 |

| Bank Alfalah | 4 | 4.35 |

| Bank Islamic | 1 | 1.09 |

| Barclays Bank | 3 | 3.26 |

| Citibank Pakistan | 3 | 3.26 |

| Faysal Bank | 4 | 4.35 |

| First Women Bank | 4 | 4.35 |

| Habib Bank Limited | 4 | 4.35 |

| Habib Metropolitan Bank | 1 | 1.09 |

| HSBC Pakistan | 4 | 4.35 |

| JS Bank | 5 | 5.43 |

| KASB Bank Limited | 4 | 4.35 |

| MCB Bank | 4 | 4.35 |

| Meezan Bank | 4 | 4.35 |

| Maybank | 3 | 3.26 |

| National Bank of Pakistan | 4 | 4.35 |

| NIB Bank Pakistan | 4 | 4.35 |

| Royal Bank of Scotland | 3 | 3.26 |

| Silkbank Limited | 3 | 3.26 |

| Soneri Bank | 4 | 4.35 |

| Standard Charted Bank | 4 | 4.35 |

| Summit Bank | 4 | 4.35 |

| The Bank of Punjab | 1 | 1.09 |

| United Bank Limited | 4 | 4.35 |

| Qualification | Frequency | Percentage |

|---|---|---|

| Bachelor | 30 | 33.0 |

| Master | 24 | 26.4 |

| CA | 2 | 2.20 |

| CIA | 2 | 2.20 |

| CPA | 4 | 4.40 |

| ICMA | 17 | 18.7 |

| PIPFA | 4 | 4.40 |

| ACCA | 8 | 8.79 |

| Level of Experience | Frequency | Percentage |

|---|---|---|

| Above five less than ten years | 23 | 25.0 |

| Above ten years | 4 | 4.35 |

| Above two less than five years | 32 | 34.8 |

| Less than two | 33 | 35.9 |

| Specialization | Frequency | Percentage |

|---|---|---|

| Accounting and finance | 30 | 33.0 |

| Business administration | 24 | 26.4 |

| Management | 8 | 8.79 |

| Factors | Cronbach’s α with 95% CI |

|---|---|

| Competency | 0.79 (0.70–0.85) |

| Objectivity | 0.79 (0.56–0.89) |

| Performance | 0.88 (0.83–0.92) |

| Board audit committee support | 0.85 (0.77–0.90) |

| Independence | 0.91 (0.80–0.95) |

| Internal audit quality | 0.88 (0.73–0.95) |

| Overall | 0.93 (0.89–0.95) |

| Factor | Univariate Analysis | Multivariable Analysis | |||

|---|---|---|---|---|---|

| Response | Crude OR (95% CI) | p-Value | adj. OR (95% CI) | p-Value | |

| Performance | Disagreement | 1.00 (Ref.) | 1.00 (Ref.) | ||

| Agreement | 15.867 (4.641, 54.242) | <0.001 | 15.836 (2.827, 88.704) | 0.0017 | |

| Competence | Disagreement | 1.00 (Ref.) | 1.00 (Ref.) | ||

| Agreement | 6.667 (2.565, 17.327) | <0.001 | 7.351 (2.109, 25.625) | 0.0017 | |

| Objectivity | Disagreement | 1.00 (Ref.) | 1.00 (Ref.) | ||

| Agreement | 7.526 (2.369, 23.907) | <0.001 | 7.213 (1.389, 37.452) | 0.0187 | |

| Board audit committee support | Disagreement | 1.00 (Ref.) | 1.00 (Ref.) | ||

| Agreement | 1.743 (0.634, 4.789) | 0.2812 | 2.166 (0.416, 11.267) | 0.3583 | |

| Independence | Disagreement | 1.00 (Ref.) | 1.00 (Ref.) | ||

| Agreement | 0.516 (0.153, 1.74) | 0.2863 | 0.11 (0.013, 0.942) | 0.0439 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Afzal, M. Evaluation of Factors Contributing to the Effectiveness of Internal Audit Quality in Pakistani Commercial Banks. Int. J. Financial Stud. 2023, 11, 129. https://doi.org/10.3390/ijfs11040129

Afzal M. Evaluation of Factors Contributing to the Effectiveness of Internal Audit Quality in Pakistani Commercial Banks. International Journal of Financial Studies. 2023; 11(4):129. https://doi.org/10.3390/ijfs11040129

Chicago/Turabian StyleAfzal, Madiha. 2023. "Evaluation of Factors Contributing to the Effectiveness of Internal Audit Quality in Pakistani Commercial Banks" International Journal of Financial Studies 11, no. 4: 129. https://doi.org/10.3390/ijfs11040129

APA StyleAfzal, M. (2023). Evaluation of Factors Contributing to the Effectiveness of Internal Audit Quality in Pakistani Commercial Banks. International Journal of Financial Studies, 11(4), 129. https://doi.org/10.3390/ijfs11040129