- Article

The Role of Environmental Disclosure and Green Accounting in Achieving a Sustainable and Investment-Attractive Economy According to Saudi Vision 2030

- Hakim Mohamed Berradia

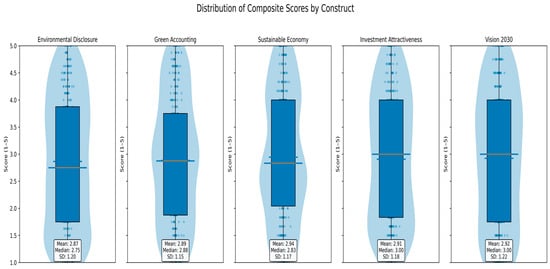

This study investigates the different mechanisms through which environmental disclosure and green accounting practices influence investment attractiveness in an emerging market context. Drawing on legitimacy theory and the resource-based view, we examine whether these environmental accountability mechanisms create value directly or through enhanced sustainability performance. Using survey data from 290 non-financial firms listed on the Saudi Stock Exchange, we employ partial least squares structural equation modeling to test a mediated-moderation model within the Saudi Vision 2030 framework. The results reveal differentiated value-creation pathways: environmental disclosure affects investment attractiveness indirectly through sustainable economic outcomes (full mediation; indirect effect β = 0.121, p < 0.001), while green accounting demonstrates both direct (β = 0.237, p < 0.001) and indirect effects (β = 0.091, p < 0.01), indicating partial mediation. Both practices are positively associated with sustainable economic outcomes (β_ED = 0.290, β_GA = 0.219, p < 0.001), which in turn are positively related to investment attractiveness (β = 0.416, p < 0.001). Unexpectedly, Vision 2030 alignment shows no significant moderating effect (β = 0.042, p = 0.498), suggesting that the sustainability–investment relationship is not significantly conditioned by perceived alignment with the national strategic framework in this sample. The model explains 25.7% of the variance in investment attractiveness and 20.0% of that in sustainable economic outcomes, indicating moderate explanatory power. These findings contribute to the environmental accounting literature by suggesting that internal management-oriented practices may be more closely associated with investment attractiveness than disclosure transparency alone. Overall, the results indicate that green accounting systems are associated with investment attractiveness, while environmental disclosure appears to require observable sustainability performance to be reflected in investment perceptions, offering measured implications for corporate strategy and regulatory policy in sustainability transitions.

18 January 2026