Risks, Volume 6, Issue 3 (September 2018) – 41 articles

Cover Story (view full-size image):

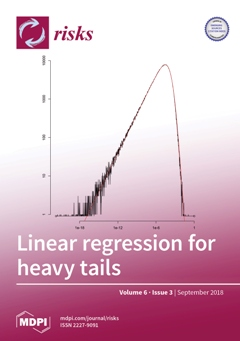

The block plot shows the frequency of the Right Median estimate for the absolute slope of the regression line based on 1,000,000 simulations of a sample of 100 observations. The error and explanatory variable both have very heavy tails. The error has a Student distribution with 1/4 degrees of freedom; the explanatory variable has a Pareto distribution that is the third power of the inverse of a standard uniform variable. The estimate is a bisector of the sample and of the 21 rightmost sample points. The red curve is the associated Exponential Generalized Prime Beta fit. View this paper.

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue