J. Risk Financial Manag., Volume 16, Issue 6 (June 2023) – 20 articles

Cover Story (view full-size image):

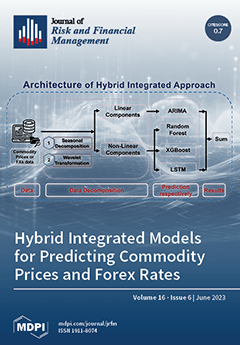

This study examines the effectiveness of using a large dataset and advanced methodologies, including sentiment analysis and machine learning, to forecast foreign exchange rates (FX) and commodity prices. Using a large dataset, we explore whether combining sentiment analysis with machine learning outperforms in terms of FX. We employ techniques such as random forest, extreme gradient boosting, long short-term memory, and autoregressive integrated moving average (ARIMA) to compare their forecasting performance. The study proposes novel methodologies that integrate seasonal decomposition and wavelet transformation with ARIMA and machine learning techniques and applies them to gold futures prices and euro FX against the US dollar to demonstrate the superiority of the proposed approaches. View this paper

- Issues are regarded as officially published after their release is announced to the table of contents alert mailing list.

- You may sign up for e-mail alerts to receive table of contents of newly released issues.

- PDF is the official format for papers published in both, html and pdf forms. To view the papers in pdf format, click on the "PDF Full-text" link, and use the free Adobe Reader to open them.

Previous Issue

Next Issue