The Effect of Corporate Governance in Islamic Banking on the Agility of Iraqi Banks

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. The Organizational Agility

2.2. The Quality of Corporate-Governance Mechanisms

2.3. The Quality of Corporate-Governance Mechanisms and Bank Agility

3. Research Methodology

3.1. Sample and Data Collection

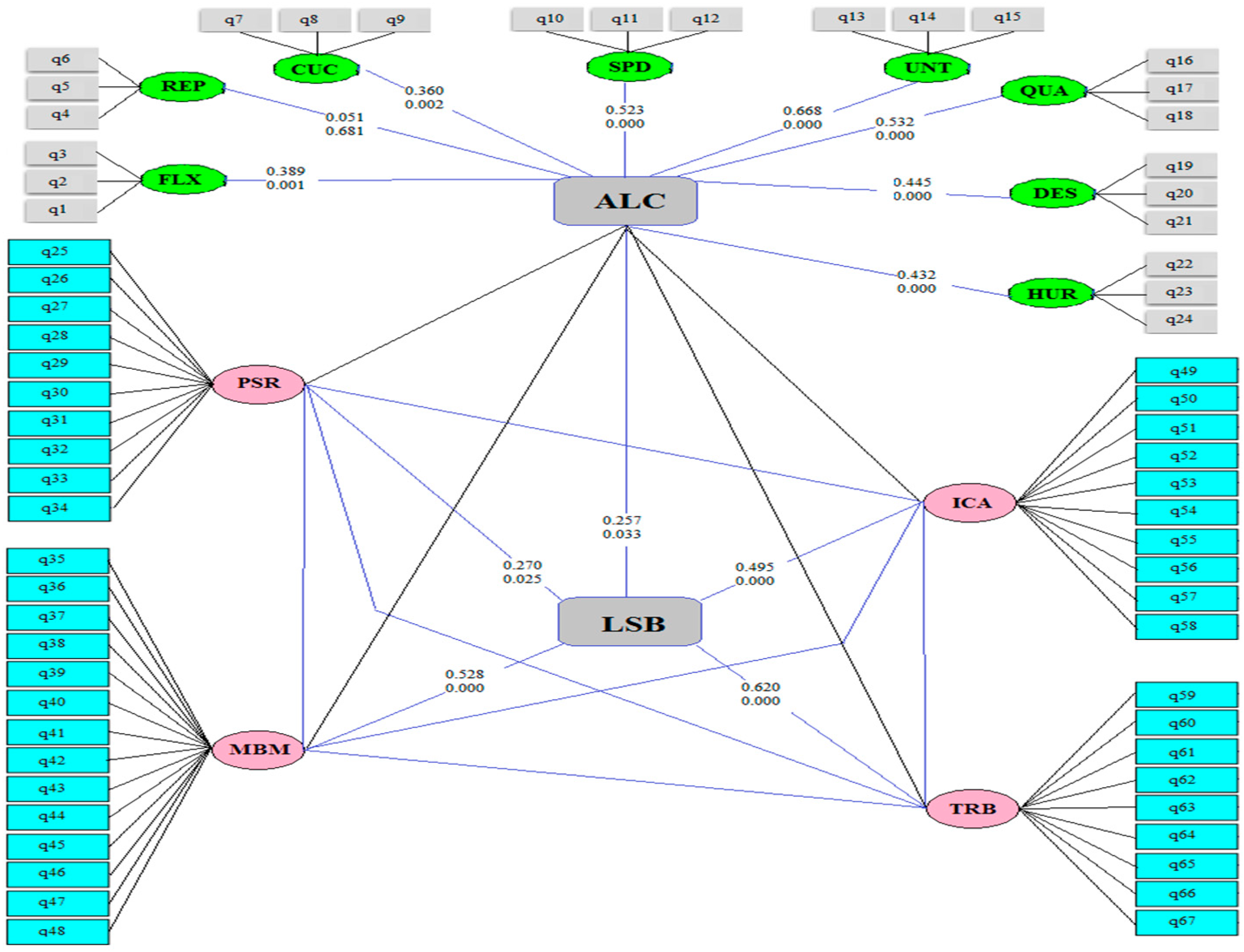

3.2. Research Model

3.3. Conceptual Model

4. Data Analysis

4.1. Descriptive Statistics

4.2. Inference from Data

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. The Employed Questionnaires

| Questions | I Completely Disagree | I Disagree | I Have No Opinion | I Agree | I Completely Agree |

| Bank agility | |||||

| Flexibility | |||||

| 1. The capability of your bank to provide various services is very high. | |||||

| 2. The capability of your bank to change the volume of services at the right time is very high. | |||||

| 3. The amount of attention to flexibility in formulating strategies in your bank is of great importance. | |||||

| Responsibility | |||||

| 4. The ability of your bank to respond to the diverse demands of customers (in terms of the variety of services and number) is very high. | |||||

| 5. The ability of your bank to react appropriately to changes in the environment (price of raw materials, inflation, government policies, etc.) is very high. | |||||

| 6. The ability of your bank to benefit from environmental opportunities (seasonal changes, popularity in society, etc.) is very high. | |||||

| Culture of change | |||||

| 7. The level of readiness and acceptance of employees for innovation in all working areas of your bank is very high. | |||||

| 8. The level of positive attitude towards changes in different areas of your bank (responsibility, technology, etc.) is very high. | |||||

| 9. The rate of identifying environmental opportunities and threats and exploiting them in your bank is very high. | |||||

| Speed | |||||

| 10. The ability of your bank’s employees to quickly learn new tasks is very high. | |||||

| 11. The speed of the employees in doing work in your bank is favorable. | |||||

| 12. The ability of your bank to produce and deliver services needed by customers is very high. | |||||

| Integrity | |||||

| 13. Your bank’s degree of coordination between the internal environment (employees, goals, laws, etc.) and the external environment (competitors, suppliers, market, etc.) is very high. | |||||

| 14. The degree of coordination in the banking process in your bank is in a favorable condition. | |||||

| 15. The level of coordination between your bank’s partners, supervisors, and auditors is very high. | |||||

| Quality | |||||

| 16. The quality of services provided by your bank is satisfactory. | |||||

| 17. The provision of necessary information about the services provided to clients in your bank is favorable. | |||||

| 18. The degree of continuity of product quality during its useful life in your bank is in a favorable condition. | |||||

| Merit | |||||

| 19. Your bank’s ability to deal with different risks simultaneously (competitor pressure, inflation, decrease in demand, government pressure, etc.) is very high. | |||||

| 20. The rate of taking measures to prevent competitors from copying the designs and technologies used by your bank is very high. | |||||

| 21. The ability of your bank to form fast cooperation with competitors is very high. | |||||

| Human resources | |||||

| 22. The level of access of employees to the information and knowledge needed in your bank is very high. | |||||

| 23. The amount of team and group work completed by your bank’s employees is good. | |||||

| 24. The level of attention to the individual initiative of the employees in your bank is very high. | |||||

| Corporate Governance in Islamic Banks of Iraq | |||||

| The first axis: the actions of the bank regarding guaranteeing the rights of shareholders and beneficiaries | |||||

| 25. The bank treat all stakeholders fairly, including shareholders, depositors, and investors. | |||||

| 26. The bank tries to avoid illegal activities that put shareholders’ rights at financial risk. | |||||

| 27. The bank has a fair structure for rewards and damages. | |||||

| 28. The bank is committed to taking immediate measures for any violation of owners’ rights. | |||||

| 29. The transfer of ownership of shares is carried out based on guaranteed legal measures. | |||||

| 30. Bank management tries to give appropriate information to the shareholders with appropriate networks. | |||||

| 31. The bank is committed to the upper limits of ownership by large shareholders (10%) and otherwise obtains in-principle approval. | |||||

| 32. The bank undertakes that the founders’ share does not exceed 20% of the shares and 50% of the capital; the rest is subscribed. | |||||

| 33. The bank’s board of directors is encouraged to build strong relationships with common stakeholders to strengthen governance practices. | |||||

| 34. Bank management is required to fulfill its obligations to debtors and other related parties based on the payment schedule. | |||||

| The second axis: the competence and independence of the board of directors and executive management | |||||

| 35. The bank has an internal regulation that guarantees candidacy for board-of-directors membership based on the criteria of experience and ability. | |||||

| 36. Most of the members of the board of directors have scientific qualifications, experience, and expertise suitable for managing banking activities. | |||||

| 37. The board of directors establishes general goals, plans, and policies based on applicable criteria by the executive management. | |||||

| 38. The board of directors tries not to share the members of the board of directors and the executive management. | |||||

| 39. The activity of the board of directors is for four years, and it is not possible to re-present as a candidate to be a member of the board of directors except by evaluation, which should not occur for more than three terms. | |||||

| 40. The board of directors tries to have two independent members outside the bank who have no direct or indirect connection with the bank. | |||||

| 41. The board of directors provides clear bills and instructions that guarantee the bank’s legal measures. | |||||

| 42. The bank has a charter and policies for proper management (training of human resources, integrated quality and job behavior, etc.). | |||||

| 43. The performance of the board of directors and executive management is evaluated by independent observers at least once a year. | |||||

| 44. The board of directors has permanent and temporary committees based on the expertise and capabilities of the members, and their duties and powers are specified. | |||||

| 45. The formed committees perform their duties efficiently and advise the board of directors based on appropriate timing. | |||||

| 46. A governance committee qualifies individuals and reports on implementing governance-criteria management. | |||||

| 47. The board of directors presents the actual amounts earned by the chairman of the board of directors and members and executive management in an annual report. | |||||

| 48. The board of directors interacts with all shareholders based on equality, which guarantees justice in rights and duties. | |||||

| The third axis: the ability and independence of audit committees | |||||

| 49. The independence and realism of the internal auditor play a role in the governance of the bank’s performance and prevents conflict of interests between the administration and the owners. | |||||

| 50. The bank tries to ensure that the internal auditors are at an excellent scientific and practical level and are familiar with the company’s process and actions. | |||||

| 51. Audit units are connected with the board of directors and its employees are independent and capable. | |||||

| 52. In the bank, there is a special audit unit called the internal-supervision department, and its employees are capable and independent. | |||||

| 53. The audit committee ensures that the financial reports issued by the banks reflect the truth of the bank’s financial strength. | |||||

| 54. The monitoring committee follows the work of the internal auditor and ensures their independence. | |||||

| 55. The internal-audit department has an active role in risk management by determining and evaluating important areas at risk in the bank. | |||||

| 56. The internal-audit department is under the internal control of the periodical evaluation process, and attempts are made to investigate its problems and follow through with its correction. | |||||

| 57. Internal audit plays a role in guaranteeing the right of shareholders to comment on the appointment of board members. | |||||

| 58. Internal audit helps guarantee shareholders’ right to vote in person or by proxy, and all votes are given the same value. | |||||

| The fourth axis: the transparency policy in the bank | |||||

| 59. All information with relative importance, in addition to that specified by the law, is provided at the right time and guaranteed to reach all stakeholders. | |||||

| 60. Equal opportunity exists to ensure that information reaches everyone at the right time and at the lowest cost. | |||||

| 61. The bank provides future perspectives and risks periodically and continuously. | |||||

| 62. The bank’s transparency policy aligns with international accounting standards or the National Control Department. | |||||

| 63. The bank provide the governance structure and policies and the degree of their implementation in the bank. | |||||

| 64. The process of providing transparent information is continuous and available to the public at a specified time and with simple tools at no cost. | |||||

| 65. Commitment to the transparency and accuracy of the information and providing it at a specified time increases the trust of shareholders and customers. | |||||

| 66. The board of directors is committed to publishing specific information about the capital structure and related facilities to protect the interests of small owners. | |||||

| 67. Transparency is pervasive and assesses the bank’s financial strength and risk-taking activities. | |||||

References

- Aburub, Faisal. 2015. Impact of ERP systems usage on organizational agility: An empirical investigation in the banking sector. Information Technology & People 28: 570–88. [Google Scholar] [CrossRef]

- Adams, Renee B., Benjamin E. Hermalin, and Michael S. Weisbach. 2010. The role of boards of directors in corporate governance: A conceptual framework and survey. Journal of Economic Literature, American Economic Association 48: 58–107. [Google Scholar] [CrossRef]

- Aghina, Wouter, Aaron De Smet, and Weerda Kirsten. 2015. Agility: It rhymes with stability. McKinsey Quarterly 51: 58–69. [Google Scholar]

- Barnett, William P., and Glenn R. Carroll. 1987. Competition and mutualism among early telephone companies. Administrative Science Quarterly 32: 400–21. [Google Scholar] [CrossRef]

- Bhattrai, Himal. 2017. Effect of corporate governance on financial performance of bank in Nepal. ZENITH International Journal of Multidisciplinary Research 7: 97–110. [Google Scholar]

- Börjesson, Anna, and Lars Mathiassen. 2005. Improving software organizations: Agility challenges and implications. Information Technology & People 18: 359–82. [Google Scholar]

- Byrne, Barbara M. 2012. Choosing Structural Equation Modeling Computer Software: Snapshots of LISREL, EQS, AMOS, and Mplus. In Handbook of Structural Equation Modeling. Edited by Rick Hoyle and Cahyono St. New York: The Guilford Press, pp. 307–24. [Google Scholar]

- Coulson-Thomas, Colin. 2007. Developing Directors; A Handbook for Building an Effective Boardroom Team. Peterborough: Policy Publications. [Google Scholar]

- Coulson-Thomas, Colin. 2021a. Strategic Foresight in the Boardroom. Director Today VII: 46–49. [Google Scholar]

- Coulson-Thomas, Colin. 2021b. Strategic Thinking and Corporate Governance. Effective Executive 24: 7–29. [Google Scholar]

- Coulson-Thomas, Colin. 2022. Executive, Board and Corporate Agility. Effective Executive 25: 13–33. [Google Scholar]

- Daemigah, Ali. 2020a. A Meta-Analysis of Audit Fees Determinants: Evidence from an Emerging Market. Iranian Journal of Accounting, Auditing and Finance 4: 1–17. [Google Scholar] [CrossRef]

- Daemigah, Ali. 2020b. Does Financial Statements Information Contribute to Macroeconomic Indicators? Iranian Journal of Accounting, Auditing and Finance 4: 61–79. [Google Scholar] [CrossRef]

- Dahmardeh, Nazar, and Sayyid Ali Banihashemi. 2010. Organizatinal Agility and Agile Manufacturing. European Journal of Economics, Finance and Administrative Sciences 27: 1450–2275. [Google Scholar]

- Daniel, Vázquez-Bustelo, and Avella Lucía. 2006. Agile manufacturing: Industrial case studies in Spain. Technovation 26: 1147–61. [Google Scholar]

- Davis, Gerald F., and Michael Useem. 2002. Top management, company directors and corporate control. In Handbook of Strategy and Management. Edited by Andrew M. Pettigrew, Howard Thomas and Richard Whittington. London: Sage. [Google Scholar]

- Demir, Ender, and Gamze Ozturk Danisman. 2021. Banking sector reactions to COVID-19: The role of bank-specific factors and government policy responses. Research in International Business and Finance 58: 101508. [Google Scholar] [CrossRef] [PubMed]

- Dobrev, Stanislav, Tai-Young Kim, and Michael Hannan. 2001. Dynamics of niche width and resource partitioning. American Journal of Sociology 106: 1299–337. [Google Scholar] [CrossRef]

- Doz, Yves. 2020. Fostering strategic agility: How individual executives and human resource practices contribute. Human Resource Management Review 30: 100693. [Google Scholar] [CrossRef]

- Drew, Stephen, and Colin Coulson-Thomas. 1997. Transformation through teamwork: The path to the new organization? Team Performance Management: An International Journal 3: 162–78. [Google Scholar] [CrossRef]

- El-Chaarani, Hani, Rebecca Abraham, and Yahya Skaf. 2022. The Impact of Corporate Governance on the Financial Performance of the Banking Sector in the MENA (Middle Eastern and North African) Region: An Immunity Test of Banks for COVID-19. Journal of Risk and Financial Management 15: 82. [Google Scholar] [CrossRef]

- Faysal, Saad, Mahdi Salehi, and Mahdi Moradi. 2020. The impact of ownership structure on the cost of equity in emerging markets. Management Research Review 43: 1221–39. [Google Scholar] [CrossRef]

- FRC. 2016. Corporate Culture and the Role of Boards: Report of Observations. London: FRC (Financial Reporting Council). [Google Scholar]

- Ganguly, Anirban, Roshanak Nilchiani, and John V. Farr. 2009. Evaluating agility in corporate enterprises. International Journal Production Economics 118: 410–23. [Google Scholar] [CrossRef]

- Georgantopoulos, Andreas G., and John Filos. 2017. Corporate governance mechanisms and bank performance: Evidence from the Greek banks during crisis period. Investment, Management and Financial Innovations 14: 160–72. [Google Scholar] [CrossRef]

- Hayek, Friedrich A. 1945. The Use of Scientific Knowledge in Society. American Economic Review 35: 519–30. Available online: https://www.sec.gov/Archives/edgar/data/80424/000090266417002944/p17-1517dfan14a.htm (accessed on 6 January 2021).

- He, Yuanqiong, Zhilong Tian, and Yun Chen. 2007. Performance implications of nonmarket strategy in China. Asia Pacific Journal of Management 24: 151–69. [Google Scholar] [CrossRef]

- Hoskisson, Robert E., Lorraine Eden, Chung Ming Lau, and Mike Wright. 2000. Strategy in emerging economies. Academy of Management Journal 43: 249–67. [Google Scholar] [CrossRef]

- Jackson, Mats, and Christer Johansson. 2003. An Agility Analysis from a Production System Perspective. Integrated Manufacturing Systems 14: 482–88. [Google Scholar] [CrossRef]

- Jallali, Safa, and Faten Zoghlami. 2022. Does risk governance mediate the impact of governance and risk management on banks’ performance? Evidence from a selected sample of Islamic banks. Journal of Financial Regulation and Compliance 30: 439–64. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1986. Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review 76: 323–29. [Google Scholar]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1992. Specific and general knowledge, and organizational structure. also published in. In 1992 Contract Economics. Edited by Lars Werin and Hans Wijkander. Oxford: Blackwell. Available online: http://papers.ssrn.com/ABSTRACT=6658 (accessed on 6 January 2021).

- Jensen, Michael C., and William H. Meckling. 1995. Specific and General Knowledge, and Organizational Structure. Journal of Applied Corporate Finance 8: 4–18. [Google Scholar] [CrossRef]

- Khatib, Saleh F. A., and Abdul-Naser Ibrahim Nour. 2021. The impact of corporate governance on firm performance during the COVID-19 pandemic: Evidence from Malaysia. Journal of Asian Finance, Economics and Business 8: 0943–52. [Google Scholar]

- Lamichhane, Pitambar. 2018. Corporate governance and financial performance in Nepal. NCC Journal 3: 108–20. [Google Scholar] [CrossRef]

- Lehn, Kenneth, Sukesh Patro, and Mengxin Zhao. 2009. Determinants of the size and composition of US corporate boards: 1935–2000. Financial Management 38: 747–80. [Google Scholar] [CrossRef]

- Lehn, Kenneth. 2021. Corporate governance and corporate agility. Journal of Corporate Finance 66: 101929. [Google Scholar] [CrossRef]

- Li, Yongping, Ahmad Sobri Hashim, Liangliang Zhang, Riza Sulaiman, and Hussam Alrabaiah. 2022. The relationship investigating between decision support and departmental agility with the mediating role of departmental learning in bank branches. Information Processing & Management 59: 102847. [Google Scholar] [CrossRef]

- Linck, James S., Jeffry M. Netter, and Tina Yang. 2008. The effects and unintended consequences of the Sarbanes-Oxley act on the supply and demand for directors. The Review of Financial Studies 22: 3287–328. [Google Scholar] [CrossRef]

- Marina, Brogi, and Valentina Lagasio. 2022. Better safe than sorry. Bank Corporate Governance, Risk-Taking, and Performance, Finance Research Letters 44: 102039. [Google Scholar] [CrossRef]

- Mayer, Colin. 2018. Prosperity: Better Business Makes the Greater Good. Oxford: Oxford University Press. [Google Scholar]

- Mertzanis, Charilaos, Mohamed A. K. Basuony, and Ehab K. A. Mohamed. 2019. Social institutions, corporate governance and firm-performance in the MENA region. Research in International Business and Finance 48: 75–96. [Google Scholar] [CrossRef]

- Miletkov, Mihail K., Annette B. Poulsen, and M. Babajide Wintoki. 2017. Foreign independent directors and the quality of legal institutions. Journal of International Business Studies 48: 267–92. [Google Scholar] [CrossRef]

- Miller, Danny, and Peter H. Friesen. 1984. Organizations: A Quantum View. Englewood Cliffs: Prentice-Hall. [Google Scholar]

- Nguyen, Quang Khai. 2022a. Audit committee structure, institutional quality, and bank stability: Evidence from ASEAN countries. Finance Research Letters 46: 102369. [Google Scholar] [CrossRef]

- Nguyen, Quang Khai. 2022b. The impact of risk governance structure on bank risk management effectiveness: Evidence from ASEAN countries. Heliyon 8: e11192. [Google Scholar] [CrossRef] [PubMed]

- Nguyen, Thi Dieu Chi, Huu Nghi Phan, Hung Son Le, Thi Thuy Trang Nguyen, and Aleksandr Petrov. 2020. Corporate governance and bank performance: A case of the Vietnam banking sector. Journal of Security and Sustainability Issues 10: 63–75. [Google Scholar] [CrossRef]

- Panda, Sukanya, and Santanu Kumar Rath. 2017. The effect of human IT capability on organizational agility: An empirical analysis. Management Research Review 40: 800–20. [Google Scholar] [CrossRef]

- Panda, Sukanya, and Santanu Kumar Rath. 2021. How information technology capability influences organizational agility: Empirical evidences from Indian banking industry. Journal of Indian Business Research 13: 564–85. [Google Scholar] [CrossRef]

- Peng, Mike W., and Peggy Sue Heath. 1996. The growth of the firm in planned economies in transition: Institutions, organizations, and strategic choice. Academy of Management Review 21: 492–528. [Google Scholar] [CrossRef]

- Permatasari, Ika. 2020. Does corporate governance affect bank risk management? Case study of Indonesian banks. International Trade, Politics and Development 4: 127–39. [Google Scholar] [CrossRef]

- Peterson, Ryan, Marilyn Parker, and Pieter Ribbers. 2002. Information technology governance processes under environmental dynamism: Investigating competing theories of decision making and knowledge sharing. Paper presented at the International Conference on Information Systems (ICIS), Barcelona, Spain, December 15–18; pp. 563–72. Available online: https://aisel.aisnet.org/icis2002/52/ (accessed on 7 December 2002).

- Rediker, Kenneth J., and Anju Seth. 1995. Boards of directors and substitution effects of alternative governance mechanisms. Strategic Management Journal 16: 85–99. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Ali Daemi Gah, Farzana Akbari, and Nader Naghshbandi. 2021. Does accounting details play an allocative role in predicting macroeconomic indicators? Evidence of Bayesian and classical econometrics in Iran. International Journal of Organizational Analysis 29: 194–219. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Ali Daemi, and Farzana Akbari. 2020. The effect of managerial ability on product market competition and corporate investment decisions: Evidence from Iran. Journal of Islamic Accounting and Business Research 11: 49–69. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Farzaneh Komeili, and Ali Daemi Gah. 2019a. The impact of financial crisis on audit quality and audit fee stickiness: Evidence from Iran. Journal of Financial Reporting and Accounting 17: 201–21. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Mohamad Reza Fakhri Mahmoudi, and Ali Daemi Gah. 2019b. A meta-analysis approach for determinants of effective factors on audit quality: Evidence from emerging market. Journal of Accounting in Emerging Economies 9: 287–312. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Nasrin Ziba, and Ali Daemi Gah. 2018. The relationship between cost stickiness and financial reporting quality in Tehran Stock Exchange. International Journal of Productivity and Performance Management 67: 1550–65. [Google Scholar] [CrossRef]

- Salem, Rami Ibrahim A., Ernest Ezeani, Ali M. Gerged, Muhammad Usman, and Rateb Mohammmad Alqatamin. 2021a. Does the quality of voluntary disclosure constrain earnings management in emerging economies? Evidence from Middle Eastern and North African banks. International Journal of Accounting & Information Management 29: 91–126. [Google Scholar]

- Salem, Rami, Muhammad Usman, and Ernest Ezeani. 2021b. Loan loss provisions and audit quality: Evidence from MENA Islamic and conventional banks. The Quarterly Review of Economics and Finance 79: 345–59. [Google Scholar] [CrossRef]

- Scherer, Andreas Georg, and Christian Voegtlin. 2020. Corporate governance for responsible innovation: Approaches to corporate governance and their implications for sustainable development. Academy of Management Perspectives 34: 182–208. [Google Scholar] [CrossRef]

- Sehen Issa, Jabbar, Mohammad Reza Abbaszadeh, and Mahdi Salehi. 2022. The Impact of Islamic Banking Corporate Governance on Green Banking. Administrative Sciences 12: 190. [Google Scholar] [CrossRef]

- Senan, Nabil Ahmed Mareai, Aida Abdulaziz Ali Noaman, Borhan Omar Ahmad Al-dalaien, and Eissa A. Al-Homaidi. 2021. Corporate social responsibility disclosure and profitability: Evidence from Islamic banks working in Yemen. Banks and Bank Systems 16: 91–102. [Google Scholar] [CrossRef]

- Sivaprasad, Sheeja, and Sudha Mathew. 2021. Corporate governance practices and the pandemic crisis: UK evidence. Corporate Governance 21: 983–96. [Google Scholar] [CrossRef]

- Vicnente-Ramos, Wagner, Keythi Reymundo, Lizbbet Pari, Neisha Rudas, and Pedro Rodriguez. 2020. The effect of good corporate governance on banking profitability. Management Science Letters 10: 2045–52. [Google Scholar] [CrossRef]

- Weber, Yaakov, and Shlomo Y. Tarba. 2014. Strategic Agility: A State of the Art Introduction to the Special Section on Strategic Agility. California Management Review 56: 5–12. [Google Scholar] [CrossRef]

- Zhang, Zhengwen, and Hossein Sharifi. 2000. A methodology for achieving agility in manufacturing organizations. International Journal of Operations & Production Management 20: 496–512. [Google Scholar]

- Zhen, Jie, Zongxiao Xie, and Kunxiang Dong. 2021. Impact of IT governance mechanisms on organizational agility and the role of top management support and IT ambidexterity. International Journal of Accounting Information Systems 40: 100501. [Google Scholar] [CrossRef]

- Zimon, Grzegorz, Arash Arianpoor, and Mahdi Salehi. 2022. Sustainability Reporting and Corporate Reputation: The Moderating Effect of CEO Opportunistic Behavior. Sustainability 14: 1257. [Google Scholar] [CrossRef]

{kind=link}

| No. | Percentage | ||

|---|---|---|---|

| Gender | Male | 25 | 0.36 |

| Female | 45 | 0.64 | |

| Position in bank | Head of branch | 6 | 0.09 |

| Deputy | 7 | 0.10 | |

| Senior | 20 | 0.29 | |

| Employee | 37 | 0.53 | |

| Work experience | 5 years or less | 24 | 0.34 |

| 6 to 10 years | 14 | 0.20 | |

| 11 to 15 years | 10 | 0.14 | |

| More than 15 years | 22 | 0.31 | |

| Field of study | Accounting and auditing | 21 | 0.30 |

| Economics | 12 | 0.17 | |

| Financial management | 18 | 0.26 | |

| Other | 19 | 0.27 | |

| Age | 20–25 | 1 | 0.01 |

| 26–30 | 23 | 0.33 | |

| 31–35 | 9 | 0.13 | |

| 35 and higher | 37 | 0.53 | |

| Education | Associate’s degree | 0 | 0.00 |

| Bachelor’s degree | 17 | 0.24 | |

| Master’s degree | 25 | 0.36 | |

| PhD or higher | 28 | 0.40 |

| Question | Mean | Median | Mode | Question | Mean | Median | Mode |

|---|---|---|---|---|---|---|---|

| Flexibility | Integrity | ||||||

| Q1 | 1.990 | 2 | 2 | Q13 | 2.000 | 2 | 2 |

| Q2 | 2.200 | 2 | 2 | Q14 | 1.760 | 2 | 2 |

| Q3 | 2.140 | 2 | 2 | Q15 | 1.660 | 2 | 2 |

| Responsibility | Quality | ||||||

| Q4 | 1.970 | 2 | 2 | Q16 | 1.940 | 2 | 2 |

| Q5 | 2.060 | 2 | 2 | Q17 | 1.690 | 2 | 2 |

| Q6 | 2.130 | 2 | 2 | Q18 | 1.890 | 2 | 2 |

| Culture of change | Qualification | ||||||

| Q7 | 2.100 | 2 | 2 | Q19 | 2.190 | 2 | 2 |

| Q8 | 1.910 | 2 | 2 | Q20 | 1.840 | 2 | 2 |

| Q9 | 2.010 | 2 | 2 | Q21 | 1.930 | 2 | 2 |

| Speed | Human resources | ||||||

| Q10 | 2.030 | 2 | 2 | Q22 | 2.290 | 2 | 2 |

| Q11 | 1.740 | 2 | 2 | Q23 | 1.690 | 2 | 2 |

| Q12 | 2.300 | 2 | 2 | Q24 | 1.770 | 2 | 2 |

| Question | Mean | Median | Mode | Question | Mean | Median | Mode |

|---|---|---|---|---|---|---|---|

| The first axis: bank measures regarding guaranteeing the rights of shareholders and beneficiaries | The third axis: the ability and independence of audit committees | ||||||

| Q1 | 1.590 | 2 | 2 | Q13 | 1.940 | 2 | 2 |

| Q2 | 1.730 | 2 | 2 | Q14 | 2.030 | 2 | 2 |

| Q3 | 2.200 | 2 | 2 | Q15 | 1.910 | 2 | 2 |

| Q4 | 1.810 | 2 | 2 | Q16 | 1.930 | 2 | 2 |

| Q5 | 1.630 | 2 | 2 | Q17 | 1.830 | 2 | 2 |

| Q6 | 1.910 | 2 | 2 | Q18 | 1.810 | 2 | 2 |

| Q7 | 1.590 | 2 | 2 | Q19 | 2.340 | 2 | 2 |

| Q8 | 1.870 | 2 | 2 | Q20 | 2.140 | 2 | 2 |

| Q9 | 1.890 | 2 | 2 | Q21 | 2.390 | 2 | 2 |

| Q10 | 1.770 | 2 | 2 | 2.370 | 2 | 2 | |

| The second axis is: the competence and independence of the board of directors and executive management | The fourth axis is: the transparency policy in the bank | ||||||

| Q11 | 2.070 | 2 | 2 | Q35 | 2.210 | 2 | 2 |

| Q12 | 2.100 | 2 | 2 | Q36 | 2.300 | 2 | 2 |

| Q13 | 1.860 | 2 | 2 | Q37 | 2.090 | 2 | 2 |

| Q14 | 1.910 | 2 | 2 | Q38 | 1.970 | 2 | 2 |

| Q15 | 1.900 | 2 | 2 | Q39 | 2.010 | 2 | 2 |

| Q16 | 1.970 | 2 | 2 | Q40 | 2.290 | 2 | 2 |

| Q17 | 1.740 | 2 | 2 | Q41 | 1.710 | 2 | 2 |

| Q18 | 2.100 | 2 | 2 | Q42 | 1.960 | 2 | 2 |

| Q19 | 1.890 | 2 | 2 | Q43 | 1.910 | 2 | 2 |

| Q20 | 1.930 | 2 | 2 | ||||

| Q21 | 1.890 | 2 | 2 | ||||

| Q22 | 1.910 | 2 | 2 | ||||

| Q23 | 2.200 | 2 | 2 | ||||

| Q24 | 2.100 | 2 | 2 | ||||

| Cronbach’s Alpha | Composite-Reliability Coefficient | AVE |

|---|---|---|

| 0.912 | 0.869 | 0.659 |

| Index Name | Sing | Calculation | Acceptable | Ideal |

|---|---|---|---|---|

| χ2 significance | χ2 | <0.001 | 0.050 < p ≤ 1.000 | 0.010 < p ≤.0500 |

| Optimized Chi-square | χ2/df | 1.325 | 0.000 < χ2/df ≤ 5.000 | 0.000 ≤ χ2/df ≤ 3.000 |

| Goodness of fit | GFI | 0.925 | 0.800 ≤ GFI < 0.950 | 0.950 ≤ GFI ≤ 1.000 |

| Adjusted goodness of fit | AGFI | 0.904 | 0.800 ≤ GFI < 0.950 | 0.950 ≤ GFI ≤ 1.000 |

| Root mean square residual | RMR | 0.028 | 0.000 < RMR ≤ 0.100 | 0.000 ≤ RMR ≤ 0.050 |

| Comparative goodness of fit | CFI | 0.918 | 0.900 ≤ CFI< 0.970 | 0.970 ≤ CFI ≤ 1.000 |

| Root mean square of the estimation error | RMSEA | 0.029 | 0.050 < RMSEA ≤ 0.080 | 0.00 ≤ RMSEA ≤ 0.050 |

| Components | Questions | Cronbach’s Alpha | Factor Analysis |

|---|---|---|---|

| Agility of banks | 24 | 0.904 | 0.951–0.879 |

| Flexibility | 3 | 0.859 | 0.914–0.772 |

| Responsiveness | 3 | 0.902 | 0.957–0.883 |

| Culture of change | 3 | 0.921 | 0.957–0.883 |

| Speed | 3 | 0.842 | 0.898–0.705 |

| Integrity | 3 | 0.748 | 0.887–0.689 |

| Quality | 3 | 0.951 | 0.957–0.883 |

| Merit | 3 | 0.914 | 0.957–0.883 |

| Human resources | 3 | 0.879 | 0.898–0.705 |

| Corporate governance | 43 | 0.847 | 0.898–0.705 |

| The first axis: guaranteeing the rights of shareholders | 10 | 0.889 | 0.911–0.762 |

| The second axis: the competence of the board of directors | 14 | 0.941 | 0.928–0.883 |

| The third axis: independence of audit committees | 10 | 0.902 | 0.917–0.835 |

| The fourth axis: bank transparency | 9 | 0.899 | 0.815–0.805 |

| Variable | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|

| Agility of banks | 2.116 | 0.491 | 1.000 | 3.333 |

| Flexibility | 2.053 | 0.311 | 1.333 | 3.000 |

| Responsiveness | 2.010 | 0.286 | 1.333 | 2.667 |

| Culture of change | 2.034 | 0.358 | 1.333 | 2.667 |

| Speed | 1.802 | 0.444 | 1.000 | 3.333 |

| Integrity | 1.836 | 0.306 | 1.333 | 2.667 |

| Quality | 1.981 | 0.379 | 1.000 | 3.000 |

| Merit | 1.918 | 0.359 | 1.000 | 2.667 |

| Human resources | 1.969 | 0.160 | 1.500 | 2.583 |

| Corporate governance | 1.800 | 0.148 | 1.500 | 2.200 |

| The first axis: guaranteeing the rights of shareholders | 1.967 | 0.191 | 1.500 | 2.429 |

| The second axis: the competence of the board of directors | 2.069 | 0.219 | 1.667 | 2.700 |

| The third axis: independence of audit committees | 2.053 | 0.247 | 1.556 | 2.667 |

| The fourth axis: bank transparency | 1.972 | 0.100 | 1.696 | 2.198 |

| FLX | REP | CUC | SPD | UNT | QUA | DES | HUR | ALC | PSR | MBM | ICA | TRB | LSB | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FLX | 1.000 | |||||||||||||

| REP | −0.340 *** | 1.000 | ||||||||||||

| CUC | 0.271 ** | −0.190 | 1.000 | |||||||||||

| SPD | −0.004 | 0.086 | −0.083 | 1.000 | ||||||||||

| UNT | 0.107 | −0.006 | 0.080 | 0.434 *** | 1.000 | |||||||||

| QUA | −0.024 | −0.079 | −0.019 | 0.261 ** | 0.383 *** | 1.000 | ||||||||

| DES | −0.093 | 0.037 | 0.183 | 0.089 | 0.113 | 0.142 | 1.000 | |||||||

| HUR | 0.083 | −0.121 | 0.088 | 0.009 | 0.061 | 0.277 ** | 0.132 | 1.000 | ||||||

| ALC | 0.388 *** | 0.051 | 0.360 *** | 0.523 *** | 0.668 *** | 0.532 *** | 0.445 *** | 0.432 *** | 1.000 | |||||

| PSR | 0.072 ** | −0.235 * | 0.070 | −0.206 * | −0.439 *** | −0.192 | 0.123 | 0.166 | −0.242 ** | 1.000 | ||||

| MBM | 0.116 | −0.241 ** | 0.070 | −0.107 | −0.215 * | 0.097 | −0.019 | 0.011 | −0.082 | 0.151 | 1.000 | |||

| ICA | −0.173 | 0.152 | −0.102 | 0.047 | 0.081 | 0.018 | −0.205 * | −0.039 | −0.078 | −0.207 * | −0.022 | 1.000 | ||

| TRB | 0.128 | 0.289 ** | −0.085 | −0.095 | −0.161 | −0.171 | −0.170 | −0.239 ** | −0.140 | −0.093 | 0.016 | 0.060 | 1.000 | |

| LSB | 0.0130 | 0.059 | −0.049 | −0.159 | −0.318 *** | −0.120 | −0.179 | −0.102 | 0.257 ** | 0.270 ** | 0.528 *** | 0.495 *** | 0.620 *** | 1.000 |

| Model 1 (LSB on ALC) | Model 2 (PSR on ALC) | Model 3 (MBM on ALC) | Model 4 (ICA on ALC) | Model 5 (TRB on ALC) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Variable | Coefficient | p-Value | Coefficient | p-Value | Coefficient | p-Value | Coefficient | p-Value | Coefficient | p-Value |

| LSB | 0.056 | 0.039 | ||||||||

| PSR | 0.145 | 0.002 | ||||||||

| MBM | 0.034 | 0.000 | ||||||||

| ICA | 0.015 | 0.019 | ||||||||

| TRB | 0.025 | 0.022 | ||||||||

| Education | 0.036 | 0.000 | 0.021 | 0.000 | 0.055 | 0.001 | 0.012 | 0.000 | 0.048 | 0.000 |

| Age | 0.066 | 0.152 | 0.042 | 0.247 | 0.058 | 0.091 | 0.016 | 0.174 | 0.089 | 0.158 |

| Experience | −0.052 | 0.183 | −0.034 | 0.189 | −0.059 | 0.172 | −0.012 | 0.112 | −0.077 | 0.227 |

| Position | 0.029 | 0.360 | 0.021 | 0.351 | 0.022 | 0.289 | 0.012 | 0.087 | 0.034 | 0.098 |

| Gender | −0.523 | 0.010 | −0.502 | 0.000 | −0.488 | 0.000 | −0.358 | 0.015 | −0.169 | 0.018 |

| Constant | 2.819 | 0.000 | 2.254 | 0.000 | 1.845 | 0.000 | 2.268 | 0.000 | 3.048 | 0.000 |

| Obs | 70 | 70 | 70 | 70 | 70 | |||||

| R2 Adj. | 52.250 | 53.380 | 55.400 | 56.400 | 50.200 | |||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sehen Issa, J.; Abbaszadeh, M.R. The Effect of Corporate Governance in Islamic Banking on the Agility of Iraqi Banks. J. Risk Financial Manag. 2023, 16, 292. https://doi.org/10.3390/jrfm16060292

Sehen Issa J, Abbaszadeh MR. The Effect of Corporate Governance in Islamic Banking on the Agility of Iraqi Banks. Journal of Risk and Financial Management. 2023; 16(6):292. https://doi.org/10.3390/jrfm16060292

Chicago/Turabian StyleSehen Issa, Jabbar, and Mohammad Reza Abbaszadeh. 2023. "The Effect of Corporate Governance in Islamic Banking on the Agility of Iraqi Banks" Journal of Risk and Financial Management 16, no. 6: 292. https://doi.org/10.3390/jrfm16060292

APA StyleSehen Issa, J., & Abbaszadeh, M. R. (2023). The Effect of Corporate Governance in Islamic Banking on the Agility of Iraqi Banks. Journal of Risk and Financial Management, 16(6), 292. https://doi.org/10.3390/jrfm16060292