Abstract

Against the backdrop of environmental governance systems transitioning from command-and-control to multi-stakeholder collaboration, elucidating the mechanisms and pathways through which voluntary environmental regulations influence green technological innovation in heavily polluting enterprises holds significant implications for advancing green innovation and high-quality development. This paper systematically examines the synergistic mechanisms of command-and-control versus voluntary environmental regulations on green technological innovation in heavily polluting enterprises, utilising data from listed companies in China’s high-pollution industries between 2008 and 2024. Unlike previous studies predominantly focused on the impact of a single regulatory type, this study reveals an interactive effect between the two: moderate command-and-control regulation provides essential institutional support for voluntary environmental regulation, such as ISO 14001 certification, thereby generating a complementary enhancement effect. However, overly stringent command-and-control regulation diverts innovation resources from enterprises, thereby suppressing the incentive effect of voluntary regulation. This conclusion transcends the traditional analytical paradigm within environmental regulation theory that treats command-and-control and voluntary regulations as mutually exclusive opposites, revealing instead a dynamic relationship where both synergistic and constraining effects coexist. This discovery provides crucial theoretical underpinnings and empirical evidence for constructing an environmental governance system that combines command-and-control constraints with flexible incentives, ensuring compatibility between policy objectives and corporate behaviour.

1. Introduction

Against the global backdrop of tackling climate change and advancing the green, low-carbon transition, green technological innovation has become the core driver for achieving sustainable development. China, the largest emerging economy and carbon emitter in the world, is dedicated to promoting ecological civilization development and the green transformation of its economic structure. Green innovation in highly polluting industries is proven to be very important in this regard. However, despite the Chinese government having established a multi-faceted governance system encompassing command-and-control, market-based, and voluntary environmental regulations, its international environmental performance rankings remain notably lagging. The existing regulatory framework continues to face institutional bottlenecks in stimulating endogenous innovation among enterprises, particularly within heavily polluting industries. Incentive mechanisms and policy effectiveness for green technological innovation remain insufficiently defined, necessitating urgent clarification of the synergistic mechanisms between different regulatory instruments at both theoretical and practical levels.

Environmental regulation refers to the guidance and incentive systems implemented by a nation or region to achieve environmental protection and promote sustainable economic development. Three categories of environmental regulation are commonly found in the literature: market-based environmental regulation, voluntary environmental regulation, and command-and-control environmental regulation [1]. Voluntary environmental regulation refers to enterprises making voluntary commitments to pollution control or undertaking various forms of environmental protection activities. Its core principle is to achieve environmental protection objectives through voluntary corporate pledges and participation in environmental projects, leveraging enhanced corporate social responsibility and market competitiveness [2].

Unlike voluntary environmental regulation, market-based environmental regulation refers to policy instruments through which the government uses prices, market signals, or market-based trading mechanisms to guide enterprises in internalising the external costs of environmental pollution, thereby incentivizing them to proactively adopt emission reduction measures or engage in green innovation [3]. Such regulations primarily include emissions trading, carbon trading, environmental taxes, ecological compensation mechanisms, and renewable energy certificate trading. Their core characteristic lies in the fact that the government does not directly prescribe specific technological pathways or emission reduction standards for enterprises, but rather utilises market mechanisms to afford enterprises the flexibility to select the lowest-cost emission reduction solutions. Lu et al. further found that the impact of market-oriented environmental regulation on the commercialization of corporate green innovation follows an inverted U-shaped relationship, with its effectiveness also moderated by non-technical factors such as the degree of market development, the level of openness, and regional green innovation capacity [4]. Consequently, market-based environmental regulation does not always promote green innovation in a linear manner; its incentive effects depend on the dynamic interaction between the institutional environment and corporate response behaviour.

In 1991, American economist Michael Porter challenged conventional environmental regulation theory, proposing that stringent yet rational environmental regulations could incentivize businesses to intensify innovation efforts. This, in turn, would partially or wholly offset the costs incurred by such regulations, ultimately enhancing corporate productivity or market competitiveness. This is known as the “Porter Hypothesis”. The Porter Hypothesis posits that environmental regulations exert two distinct effects: the ‘compliance cost effect’ and the ‘innovation compensation effect’. The former denotes that environmental regulations increase enterprises’ expenditure on environmental protection, thereby diminishing corporate performance. The latter indicates that under environmental regulations, enterprises commit to green technological innovation, thereby securing greater returns for the enterprise and contributing to enhanced corporate performance [5]. Simultaneously, the positive innovation effect of voluntary environmental regulation is also mirrored in the broader context of carbon regulation. Recent research indicates that carbon peaking pressure can significantly stimulate corporate R&D investment, suggesting that well-designed environmental targets create a favourable condition for innovation-oriented corporate behaviour [6].

The “Porter hypothesis” states that proper environmental legislation can encourage technical advancement in businesses through the “innovation compensation effect,” resulting in the “dual dividend” of economic prosperity and environmental conservation [7]. However, there is a dearth of systematic investigation into the interplay between command-and-control and voluntary regulations, with the majority of current research concentrating on the effects of individual forms of environmental regulation. This is particularly true for voluntary environmental regulations, exemplified by ISO 14001 [1], which are widely acknowledged to enhance corporate green innovation levels [8]. However, whether and how its effects are modulated by command-and-control environmental regulations remains subject to theoretical disagreement and empirical gaps. The existing literature indicates that voluntary regulation can foster innovation through pathways such as resource access and reduced compliance costs [9,10]. However, few studies have examined the potential complementary, substitutive, or inhibitory relationships between voluntary and command-and-control regulation within China’s institutional context, where the latter predominates.

Within China’s unique institutional environment, voluntary regulation does not operate in isolation but is embedded within a policy framework underpinned by command-and-control regulation. On the one hand, command-and-control regulation may create the institutional conditions for implementing voluntary regulation by establishing baseline standards, providing enforcement pressure, and allocating policy resources. On the other hand, if command-and-control regulation is overly stringent, it may also divert corporate innovation resources and undermine the incentive effects of voluntary regulation. At present, there remains a lack of systematic theoretical exposition and rigorous empirical testing concerning the interactive mechanisms between the two types of regulatory instruments, their non-linear effects, and their performance under conditions of firm heterogeneity. Therefore, this paper aims to systematically examine the synergistic effects of command-and-control versus voluntary environmental regulations on green technological innovation within heavily polluting enterprises. Adopting the theoretical framework of the “Porter Hypothesis” and contextualising it within China’s institutional landscape, the study seeks to address existing theoretical gaps in the literature and provide policy implications for optimising environmental regulatory mixes.

This study makes marginal contributions in the following three aspects:

First, the driving mechanism of voluntary environmental regulation on green technological innovation has been confirmed and broadened by empirical experiments. This paper uses large-sample data to validate the role of voluntary regulation in promoting green technological innovation among heavily polluting enterprises. Secondly, the system reveals the complex interplay between command-and-control and voluntary environmental regulations. This paper employs a progressive hypothesis framework to simultaneously validate the complementary effects of dual regulations, institutional dependence, and the crowding-out effect of excessive intervention within a unified framework. This is achieved through constructing an interaction effects model and conducting heterogeneity tests. These findings enrich regulatory synergy theory and provide crucial theoretical underpinnings for optimising policy combinations. Thirdly, it has thoroughly identified the heterogeneous manifestations of regulatory effects across different institutional and corporate characteristics. By examining dimensions such as property rights characteristics, geographical location, and regulatory status, the study reveals structural variations in regulatory outcomes across different enterprise types. This provides a robust empirical foundation for tailored policy interventions and precision governance, thereby enhancing the scientific rigour and effectiveness of environmental policy design.

2. Institutional Context and Research Hypotheses

2.1. Institutional Context

As the process of Chinese-style modernization advances, ecological civilization has become a strategic pillar of national development, while the optimisation of environmental regulation constitutes the core institutional arrangement for achieving green development and fostering harmony between humanity and nature. In establishing its environmental governance system, China has progressively developed a multi-faceted regulatory framework that integrates command-and-control, market-based, and voluntary approaches. Among these, command-and-control regulation constrains corporate behaviour through command-and-control laws and standards, while market-based regulation employs economic incentives to guide emissions reduction and technological innovation. Both approaches have yielded significant results, driving sustained improvements across a range of environmental indicators. However, within global environmental performance assessment frameworks such as the Environmental Performance Index (EPI), China’s ranking remains relatively low. This reflects the persistence of structural contradictions and deep-seated challenges in environmental governance, particularly within heavily polluting industries. As the primary source of environmental pressure, these sectors continue to face practical difficulties in their green transition process, including insufficient institutional incentives, weak innovation momentum, and inadequate governance sustainability [11].

Against this backdrop, voluntary environmental regulation, as a vital component of the environmental governance system, is progressively entering the policy spotlight and advancing into the implementation phase [12]. Unlike command-and-control and market-based regulation, voluntary regulation emphasises enterprises’ autonomous participation and commitment based on social responsibility, market competitiveness, and long-term strategy. The voluntary nature of voluntary environmental regulation should be understood in contrast to command-and-control regulation, rather than judged by the criterion of “whether any external inducement exists.” The defining characteristic of command-and-control regulation is legal coercion non-compliance triggers administrative penalties or even criminal liability. By contrast, even when voluntary regulation involves external drivers such as supply chain pressure, policy incentives, or reputational considerations, firms’ decisions on whether to participate, the depth of participation, and the persistence of participation remain within their autonomous decision-making domain, and non-participation does not directly entail legal consequences. It is precisely for this reason that voluntary regulation reflects, at a deeper level, firms’ agency in internalising environmental responsibility as a strategic choice. This incentivized voluntariness represents a critical hallmark of an environmental governance system transitioning from passive compliance toward proactive stewardship. This proactive shift, however, does not occur in a policy vacuum. Importantly, green finance has been identified as a critical moderating mechanism that can alleviate the negative impacts of such uncertainty, thereby enabling firms to better translate voluntary commitments into tangible green outcomes [13].

Examples include ISO 14001 environmental management system certification, green supply chain management, and corporate environmental information disclosure. Such regulations are characterised by high flexibility, strong adaptability, and the internalisation of incentives. They can mitigate government and market failures to a certain extent, encouraging enterprises to shift from passive compliance towards proactive governance. Particularly under the innovation compensation mechanism emphasised by the Porter Hypothesis, voluntary regulation can achieve dual dividends of environmental and economic benefits by stimulating corporate green technological innovation. It thus represents a crucial breakthrough for refining China’s environmental regulatory framework and enhancing overall governance effectiveness.

Nevertheless, the development of voluntary environmental regulation in our country remains in its preliminary exploratory and institutional development phase, with its actual effectiveness, operational mechanisms, and sustainability yet to be fully validated. It is noteworthy that in China, voluntary regulation does not operate in isolation; rather, it engages in complex institutional interactions with existing command-and-control regulation: On the one hand, command-and-control environmental regulation establishes baseline standards and intensifies regulatory pressure, thereby providing the necessary institutional constraints and external impetus for voluntary environmental regulation; on the other hand, the two regulatory approaches exhibit complementarity in their policy objectives, operational mechanisms, and incentive logic. A well-designed synergistic framework can effectively stimulate green technological innovation among enterprises. However, in practice, if command-and-control regulations become overly rigid and inflexible, they may constrain enterprises’ scope for independent innovation and even dampen their willingness to undertake long-term green investments through voluntary mechanisms, thereby undermining the overall effectiveness of the regulatory framework.

Based on this, the present study, grounded in the institutional evolution and practical requirements of China’s environmental regulation framework, focuses on the driving mechanisms of voluntary regulation for green technological innovation in heavily polluting enterprises. By constructing a multidimensional analytical framework encompassing regulatory persistence, property rights interactions, complementary regulatory types, and green innovation transmission, this study aims to systematically reveal the intrinsic logic and implementation pathways through which voluntary regulation influences the green innovation behaviour of heavily polluting enterprises. This study not only contributes to deepening the theoretical validation of the “Porter Hypothesis” within the Chinese context, but also provides crucial policy references and practical guidance for advancing the transformation of China’s environmental regulatory system from “monolithic coercion” to “multifaceted coordination”, thereby promoting green innovation and high-quality development in heavily polluting industries.

2.2. Research Hypotheses

Voluntary environmental regulations, such as the ISO 14001 Environmental Management System and Green Factory Certification, provide enterprises pursuing green development with a voluntary framework for action that goes beyond command-and-control standards. These mechanisms have been demonstrated to effectively drive enterprises towards green technological innovation, with their primary modes of operation encompassing incentive effects, competitive effects, and learning effects. By enhancing the quantity and quality of enterprises’ green patent output, guide businesses to achieve a transition from compliance to innovation in environmental governance [14]. At present, the most widely used voluntary environmental regulatory tool in China is ISO 14001 Environmental Management System certification, commonly referred to as EMS certification. This environmental management system standard was established by the International Organisation for Standardisation (ISO). Within modern corporate management, ISO 14001, as a standardised environmental management system, has been widely adopted by heavily polluting enterprises to address increasingly stringent environmental regulations and societal pressure regarding corporate responsibility [15]. Similarly, green factory certification has been demonstrated to significantly promote green technological innovation within enterprises by alleviating financing constraints, strengthening internal controls, and stimulating R&D investment, with particularly pronounced effects in state-owned enterprises [16].

Voluntary environmental rules have a widespread positive impact on corporate green innovation, according to a larger body of research. Their supplemental role is especially noticeable in areas where command-and-control environmental restrictions are not adequately enforced. The connection between voluntary environmental regulation and the digitalization process further improves business performance in green innovation against the backdrop of digital transformation, mainly by reducing external funding limitations and optimising internal governance structures [17]. However, not all businesses experience the same level of the positive impact that voluntary environmental regulations have on green technical innovation. Research based on the corporate life cycle indicates that it exerts a significant stimulating effect on innovation within enterprises in the growth and maturity phases, whereas its influence on those in the formation and decline phases is comparatively limited [18]. Moreover, this effect exhibits pronounced heterogeneity in property rights and variations in factor intensity, being particularly pronounced in mature state-owned enterprises and capital- and technology-intensive manufacturing firms. Further research indicates that when enterprises place greater emphasis on digital transformation and artificial intelligence applications, or garner heightened market attention, the promotional effect of voluntary environmental regulation on their green and low-carbon technological innovation becomes more pronounced [19].

When it comes to promoting green innovation, voluntary regulation outperforms command-and-control environmental regulation. Research indicates that command-and-control environmental regulations may to some extent inhibit corporate green innovation, whereas voluntary environmental regulations exert a clear incentive effect. Government subsidies may mitigate the negative effects of the former, but they struggle to further enhance the positive effects of the latter [20]. This comparison further highlights the institutional advantages and policy value of voluntary environmental regulation in promoting green innovation.

In conclusion, current research has demonstrated its operational mechanisms, contextual reliance, and varied traits, and it supports the driving role of voluntary environmental legislation in green technological innovation from a variety of angles. On this basis, this paper proposes the following hypothesis:

H1.

Voluntary environmental regulation can drive heavily polluting enterprises to pursue green technological innovation.

Voluntary environmental regulation serves as a vital complement to command-and-control environmental regulation in enhancing the environmental performance of heavily polluting enterprises. Command-and-control environmental regulation is typically government-led, mandating that businesses meet specific environmental standards. Command-and-control and voluntary environmental regulations demonstrate a potential complementary relationship in promoting green technological innovation within enterprises. While voluntary regulations provide the most flexibility of any regulatory measure, studies have shown that command-and-control environmental restrictions are the most consistent and effective in promoting green innovation. However, research also indicates that findings regarding the validation of the ‘Porter Hypothesis’ exhibit heterogeneity, partly attributable to differences in analytical frameworks. This suggests that regulatory effects may manifest complex interactions under varying combinations of contexts and institutional arrangements [21]. Within supply chain contexts, customer-driven voluntary environmental regulations can significantly promote suppliers’ green innovation through demand feedback and knowledge spillover mechanisms. Equity linkages within the supply chain and the state-owned property rights nature of suppliers amplify this effect, indicating that the efficacy of voluntary regulations may be influenced by both formal and informal institutional arrangements such as inter-firm relationships and property rights structures [22]. This suggests that voluntary regulation may interact with the external formal institutional environment.

The influence of digital transformation on company ESG performance is significantly moderated by environmental regulations, according to additional research. Among these, voluntary environmental regulations exert a stronger regulatory effect than command-and-control environmental regulations. This underscores that, within the context of digital transformation, the synergistic application of different types of environmental regulations can more effectively guide corporate sustainable development. Moreover, public environmental concern, as a form of informal regulatory pressure, can indirectly reduce urban carbon emissions by enhancing governmental environmental oversight. This reveals a relationship of transmission and reinforcement between informal social pressure and formal governmental regulation [23]. This mechanism, analogous to voluntary regulation, may enhance or supplement the enforcement outcomes of command-and-control regulation, jointly influencing enterprises’ green behaviour.

Of particular significance is that one of the primary motivations for enterprises implementing voluntary environmental regulations such as ISO 14001 certification lies in accessing critical resources, including government subsidies and bank credit facilities. This demonstrates the dependence of voluntary actions upon the resource support provided by formal institutional frameworks [24]. From the perspective of resource allocation, the effective implementation and incentive effects of voluntary regulation cannot be achieved without the support of the resource allocation functions controlled by the formal institutional system represented by command-and-control regulation. The two are not isolated from one another. Command-and-control environmental regulations establish baseline requirements and control resource allocation channels, whereas voluntary environmental regulations provide enterprises with flexible pathways to access additional resources and enhance reputation by exceeding compliance standards and pursuing proactive innovation. The synergistic effect of both approaches is expected to stimulate greater impetus for green technological innovation among enterprises than either regulatory model operating in isolation. Based on this, the following hypothesis is proposed:

H2.

Command-and-control and voluntary environmental regulations exhibit complementary effects in promoting green technological innovation among heavily polluting enterprises. Their coordinated implementation enhances innovation-driven outcomes more effectively than relying solely on voluntary regulations.

Command-and-control environmental regulation establishes fundamental thresholds and behavioural frameworks for environmental governance through the binding force of laws and regulations, serving as the cornerstone for constructing a comprehensive environmental policy system. Research indicates that its carbon emission reduction effects exhibit a clear threshold effect, whereby only when regulatory intensity reaches a certain level can carbon emissions be effectively curbed and the potential for structural upgrading and technological innovation be unlocked [25,26]. Concurrently, the top-down target constraints in policy implementation, coupled with the upward competition mechanism among local governments, further reinforced the regulatory effectiveness in practice [27]. These findings indicate that effective command-and-control regulation can establish stable institutional expectations, generate pervasive environmental protection pressures, and create the necessary policy environment for other governance tools to function effectively.

On the one hand, the strengthening and enforcement of command-and-control environmental regulations at the governmental level serves as a crucial institutional safeguard driving enterprises to undertake green investments. Research indicates that local governments’ environmental focus can effectively stimulate corporate green investment by strengthening local environmental regulations and expanding green credit supply. This effect is particularly pronounced among heavily polluting enterprises and in regions with robust environmental regulation enforcement [28]. This reveals that command-and-control regulation not only directly establishes environmental thresholds but also, by shaping the policy environment and resource allocation, provides the essential incentives and constraints for environmentally responsible behaviour among heavily polluting enterprises.

On the other hand, while voluntary environmental regulations can incentivize firms to increase environmental governance investments, their effects may trigger economic restructuring such as industrial relocation rather than directly driving local green technological innovation [29]. This indirectly suggests that without robust formal command-and-control environmental regulations serving as a stabilising framework and baseline safeguard, relying solely on informal or voluntary pressure may prove insufficient to systematically guide enterprises towards sustained resource allocation for green technological innovation—which possesses long-term characteristics and positive externalities. Instead, firms may be inclined to opt for comparatively lower-cost end-of-pipe treatment or locational adjustment strategies. Therefore, an effective and command-and-control environmental regulations framework may provide the indispensable institutional stability and directional guidance for voluntary regulation to drive profound green innovation. On this basis, this paper proposes the following hypothesis:

H3.

Command-and-control environmental regulation is important for enabling voluntary environmental regulation to drive green technological innovation.

The direct impact of command-and-control regulation on green innovation may not be positive; indeed, it may even suppress firms’ willingness to innovate due to compliance pressures, a phenomenon particularly pronounced among non-state-owned enterprises [30]. This reflects the limitations of relying solely on coercive measures to incentivize innovation, and underscores the necessity of introducing more flexible policy instruments. Simultaneously, at a broader level, strategic and regulatory policies should be employed to grant local authorities and enterprises the flexibility to innovate [31]. This demonstrates that the core function of command-and-control regulation lies in establishing minimum standards and defining clear boundaries. Its effective implementation actually provides the prerequisite conditions and platform for flexible tools such as voluntary regulation to function.

The impact of command-and-control environmental regulation on green innovation is complex and non-monotonic. Research has found that command-and-control and market-incentive environmental regulations exert negative effects on green innovation [32]. This indicates that command-and-control regulations themselves may, due to their rigid compliance requirements and high enforcement costs, divert resources away from corporate research and development, thereby potentially inhibiting progress in green technologies. Further research has revealed the specific form and critical threshold at which this negative impact manifests, demonstrating a pronounced U-shaped relationship between command-and-control environmental regulation and green innovation [33]. This relationship is of paramount importance, as it indicates that the effects of command-and-control regulation exhibit an inflexion point: at lower levels of intensity, its constraints may compel enterprises to undertake preliminary improvements; However, when regulatory intensity continues to increase and exceeds a certain optimal threshold, its impact takes a sharp turn for the worse, transforming from a potential incentive into a clear disincentive.

So, how precisely does this “excessive” command-and-control regulation diminish the driving effect of voluntary regulation? Its core mechanism lies in crowding-out effects and incentive distortions. Relevant research provides circumstantial evidence of the mechanism whereby substantial government subsidies to specific enterprises exert a significant crowding-out effect on green innovation among their industry peers [34,35]. This phenomenon reveals that excessive or unbalanced policy intervention distorts fair market competition, crowding out innovation resources and market space for unsupported enterprises. Concurrently, excessive external coercive pressure can distort corporate motivations, shifting the original intent behind participation in voluntary environmental programmes from proactive innovation to gain competitive advantage towards passive compliance to avoid penalties. This fundamentally erodes the flexibility and endogenous incentive foundation upon which voluntary regulation relies for effectiveness, ultimately diminishing its capacity to drive green technological innovation. On this basis, this paper proposes the following hypothesis:

H4.

Excessive command-and-control environmental regulation, when imposed over and above voluntary environmental regulation, may diminish its effectiveness in driving green technological innovation.

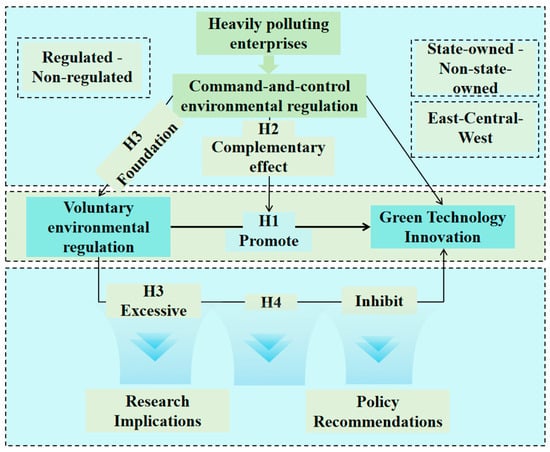

Figure 1 presents the research framework diagram for this paper.

Figure 1.

Research Framework Diagram.

3. Materials and Methods

3.1. Data Explanation

The research sample for this study consists of listed businesses in highly polluting industries from China’s Shanghai and Shenzhen A-share exchanges between 2008 and 2024. The Green Patent Research Database (GPRD), China Securities Market Research (CSMAR) data service centre, and China National Research Data Service (CNRDS) are the sources of the data used. This study is based on the Ministry of Environmental Protection’s 2010 Guidelines for Environmental Information Disclosure by Listed Companies. This guide, based on the 2008 Catalogue of Environmental Verification Industry Classification Management for Listed Companies, explicitly states that multiple sectors including thermal power generation, steel production, and cement manufacturing are categorised as heavily polluting industries. In accordance with the Guidelines for the Classification of Listed Companies by Industry, the specific heavy pollution industry codes defined herein include B06, B07, B08, B09, C17, C19, C22, C25, C26, C28, C29, C30, C31, C32, and D44. In terms of data processing, to ensure the rigour of this paper and the accuracy of the data, companies such as ST and *ST were first excluded; secondly, samples lacking key financial indicators were excluded; finally, to mitigate the impact of outliers on the findings, all financial variables underwent tail trimming at the 1% and 99% levels using Winsorization. Following the aforementioned meticulous and systematic data screening and processing, this paper ultimately yielded 9891 valid sample observation points.

3.2. Variable Selection

3.2.1. Explanatory Variables

An international standard for certifying environmental management systems is ISO 14001, centred on the identification and control of environmental risks. It guides enterprises in formulating environmental protection programmes, reducing pollutant emissions, complying with national environmental regulations, and cultivating a green and sustainable brand image. Concurrently, ISO 14001 adopts the concept of the ‘life cycle’, requiring organisations to implement environmental management across all stages of a product’s design, production, distribution, use and disposal [36]. This comprehensive management approach assists heavily polluting enterprises in systematically identifying pollution sources and reducing environmental impacts.

This research uses ISO 14001 environmental management system certification as the primary proxy variable for voluntary environmental regulation, in order to examine its driving effect on corporate green technological innovation. The variable is defined as a binary dummy variable, taking the value 1 if firm i holds a valid ISO 14001 certificate in year t, and 0 otherwise.

It is particularly important to note that ISO 14001 certification is, by institutional design, not a one-time event with permanent validity. According to the rules established by the International Organisation for Standardisation (ISO) and the China National Accreditation Service for Conformity Assessment (CNAS), certified enterprises must undergo annual surveillance audits conducted by accredited certification bodies, and must pass recertification audits every three years. Firms that fail these periodic audits face suspension, withdrawal, or non-renewal of their certificates. This dynamic review mechanism implies that, for a firm to be coded as 1 across multiple consecutive years, it must continuously invest resources in maintaining its environmental management system and passing periodic external audits. In other words, what our variable actually captures is the firm’s dynamic commitment to continuously maintaining valid certification status, rather than the static fact of having ever obtained certification. This institutional feature substantially mitigates the concern that “post-certification complacency cannot be identified”, firms that experience substantive slackening typically fail recertification and are automatically coded as 0 in subsequent years.

Furthermore, regarding whether ISO 14001 certification fully aligns with the characteristic of “voluntary proactivity,” our position is as follows: in environmental regulation theory, the core meaning of “voluntariness” is not “purely altruistic behaviour free of any external inducement” such pure voluntariness rarely exists in real economic activity but rather refers to firms’ autonomous choice to go beyond legal minimum requirements. Even when certification motives include compliance demands from downstream customers, expectations of obtaining government green subsidies, or preferences from green credit lenders, firms still retain decision-making autonomy over whether to apply, when to apply, and at what depth to engage, and non-participation does not directly constitute a legal violation. This is fundamentally distinct from the institutional logic of command-and-control regulation, which relies on legal coercion and penalty enforcement. Leading studies in this field, all endorse this “mixed-motive but voluntary-in-form” theoretical positioning when employing ISO 14001 as a proxy for voluntary regulation. Our variable specification thereby maintains consistency with established literature and ensures comparability of findings.

3.2.2. Dependent Variable

The dependent variable in this study is the level of green technological innovation within enterprises. The methodology for constructing the indicators draws upon the patent-based indicator construction approach outlined in Cheng et al. [37]. Indicators for corporate green technological innovation levels comprise three categories: overall green patents (EnvrPat), green invention patents (EnvrInvPat), and green utility model patents (EnvrUtyPat). This study employs the Green Patent Index (EnvrPat) as the dependent variable, whilst the other two metrics undergo validation through robustness tests. To mitigate the impact of zero values, the number of green patent applications was adjusted by adding one before taking the logarithm during data processing. The same adjustment method was applied to the construction of data for green invention patents and green utility model patents.

3.2.3. Control Variables

In the research design of this paper, we incorporated several control variables to comprehensively capture factors such as corporate financial characteristics, growth potential, market valuation, and governance structures that may influence the study’s findings. The control variables in this paper are as follows: ① Enterprise size (Size). The existing literature indicates that enterprise size constitutes a significant factor influencing corporate innovation. Generally speaking, larger enterprises typically undertake relatively stable research and development expenditure to maintain their technological advancement levels, thereby ensuring the sustainability of their own development [38]. ② Return on Assets (ROA). Return on Assets serves as a crucial metric for evaluating an enterprise’s overall profitability and operational efficiency. A higher ratio indicates stronger capacity to generate profits from assets, potentially signifying more abundant internal funds available to support long-term investments such as green technological innovation [39]. ③ Total Asset Turnover (ATO). Total asset turnover reflects the operational efficiency and management level of an enterprise’s assets. A higher ratio indicates greater efficiency in asset utilisation and stronger operational vitality, suggesting a greater propensity to maintain or enhance operational effectiveness through technological innovation [40]. ④ Cash Flow Ratio (Cashflow). The cash flow ratio measures a company’s capacity to generate cash from its operating activities, serving as a key indicator of liquidity and financial flexibility. Adequate cash flow provides internal financing support for corporate R&D expenditure, thereby reducing financial constraints on innovation activities [41]. ⑤ Whether the enterprise is loss-making (loss). The financial health of a business directly influences its resource allocation and strategic direction. Loss-making enterprises often face heightened survival pressures and financial constraints, potentially leading to reduced or deferred investment in long-term initiatives such as green technological innovation [42]. ⑥ Board size (Board). The size of the board of directors constitutes a significant dimension of corporate governance structures, potentially influencing the efficiency and quality of strategic decision-making. Boards of moderate size may be more conducive to thorough deliberation and informed decision-making, thereby impacting long-term investments such as green innovation [43]. ⑦ Proportion of Independent Directors (Indep). The proportion of independent directors reflects the supervisory independence and governance effectiveness of the board. A higher proportion of independent directors may strengthen oversight of corporate environmental responsibilities and promote strategic actions aligned with long-term sustainable development, such as green innovation [44]. ⑧ Shareholding Proportion of the Top Ten Shareholders (Top10). Shareholding concentration is a significant factor influencing corporate governance and agency issues. When the shareholding proportion of the top ten shareholders is high, major shareholders may possess greater motivation and capacity to oversee management in driving green transformation, though risks of self-dealing may also arise [45].⑨ The ratio of a firm’s market value to its capital replacement cost, known as the Tobin’s Q ratio (TobinQ). A firm’s Tobin Q ratio reflects its capacity for social value creation. Generally, a higher value indicates that the firm generates greater societal wealth and possesses a stronger innovative ethos [46]. ⑩ Dual role (Dual). Whether the chairmanship and chief executive positions are combined constitutes a key feature of corporate leadership structures, potentially influencing decision-making efficiency and checks on management power. While dual roles may enhance decision-making consistency, they may also weaken board oversight of management, thereby impacting long-term investments such as green innovation [47]. The calculation methods for these control variables are as shown in Table 1.

Table 1.

Variable Descriptions.

3.2.4. Moderating Variables

To capture the intensity of command-and-control environmental regulation faced by enterprises, this study employs regional environmental administrative penalty intensity (EnvPenalty) as the moderating variable. The construction of this variable follows the established measurement approach in the environmental regulation literature, which uses actual environmental penalty amounts rather than the number of penalty cases or formal regulatory texts as a proxy for the substantive enforcement intensity of command-and-control regulation [25,48,49]. Standardisation by regional industrial output further follows common practice in studies of Chinese environmental regulation, which serves to remove cross-provincial differences in economic scale and isolate the relative stringency of enforcement. Drawing on environmental enforcement records compiled in the CSMAR Environmental Penalty Database and the China Environmental Statistics Yearbook, this variable is constructed as the natural logarithm of one plus the total monetary amount of environmental administrative penalties imposed on enterprises in the province where firm is registered in year , scaled by the province’s gross industrial output value of the same year. The specific calculation formula is

where denotes the province in which firm is located. This intensity-based, output-scaled measure offers two advantages over a simple count of penalties or absolute fine amount. First, scale by industrial output controls for cross-provincial differences in economic and industrial scale, ensuring that the variable reflects the relative stringency of enforcement rather than the absolute size of the regional economy. Second, use monetary penalty amounts rather than the number of penalty cases as it more accurately captures the substantive deterrent intensity of enforcement, as a single high-value penalty exerts greater disciplinary pressure than multiple low-value ones. Higher values of EnvPenalty indicate that firms in the corresponding province operate under more intensive command-and-control environmental enforcement.

3.3. Descriptive Statistics

According to the descriptive statistics presented in Table 2, the total sample comprises 9891 observations, encompassing multiple variables, including corporate environmental innovation, financial performance, and governance structures. Overall distribution characteristics reveal varying degrees of dispersion and central tendency across the variables within the sample. The mean value for environmental patents (EnvrPat) was 0.389, with a standard deviation of 0.763 and a median of 0. This indicates that over half of the enterprises did not obtain environmental patents during the sample period, revealing a pronounced right skew in the distribution. A small number of enterprises demonstrated exceptional performance, with the maximum value reaching 6.906. Regarding corporate certifications, the mean for ISO certification stands at 0.423, signifying that approximately 42.3% of enterprises obtained relevant certification, indicating a degree of environmental management awareness.

Table 2.

Descriptive Statistics.

3.4. Model Specifications

This study employs a fixed-effects model to examine the impact of ISO 14001 certification on green technological innovation within heavily polluting enterprises. The benchmark regression Equation (2) is designed as follows:

is the dependent variable, representing the level of green technological innovation for firm in year . The benchmark regression model (2) employs the total volume of green patent applications as a metric. serves as the core explanatory variable, indicating whether a firm obtained ISO 14001 certification in year t. A value of 1 is assigned if the firm held valid certification during that year, otherwise 0. refer to a series of variables designed to regulate the potential impact of corporate heterogeneity on green innovation. denotes the firm-specific fixed effect, used to control for firm characteristics that do not change over time. denotes the fixed effect for the year, used to control for macro-level time trends, common policy shocks, and economic cycles. denotes the random disturbance term. and represent the regression coefficients, with being the core coefficient of interest: if is significantly positive, this indicates that ISO 14001 certification significantly promotes green technological innovation in heavily polluting enterprises. If is not significant, this indicates that voluntary environmental regulation has not produced a significant driving effect; if is significantly negative, this indicates that certification may have produced an inhibitory effect. Model (2) presents only the aggregate volume of green patent applications filed by enterprises. The robustness tests below further examine green invention patent applications () and green utility model patent applications ().

3.5. Methods

This study employs a two-way fixed effects panel model to examine the impact of voluntary environmental regulation (ISO 14001 certification) on green technological innovation, using data from Chinese heavily polluting listed companies (2008–2024). To test the interactive mechanism between regulatory types, an interaction term between ISO certification and command-and-control regulation intensity is incorporated. Robustness checks include replacing dependent variables, altering sample periods, propensity score matching (PSM), and placebo tests, while heterogeneity analyses examine variations across ownership types, regions, and regulatory statuses.

4. Results

4.1. Benchmark Regression

Column (1) presents the results of the univariate test. Column (2) displays the regression results incorporating fixed effects for individual (ID) and year (Year) on top of the data in Column (1). Column (3) incorporates regression results with control variables (Controls) based on Column (1), while Column (4) presents the full estimation results for Model (1). Table 3 reveals that the coefficient for ISO in the regression results for columns (1) to (4) is statistically significant at the 1% level. This indicates that voluntary environmental regulation (ISO 14001 certification) exerts a statistically significant and economically meaningful driving effect on green technological innovation within heavily polluting enterprises. Hypothesis H1 is thus substantiated, establishing an empirical foundation for subsequent in-depth exploration of its underlying mechanisms and boundary conditions.

Table 3.

Benchmark Regression Results.

4.2. Robustness Test

We performed several robustness tests to validate our main results, Table 4 presents the detailed outcomes.

Table 4.

Robustness Test Results.

4.2.1. Replacing the Dependent Variable

Substituting the measurement indicators for corporate green technological innovation levels with green invention patents (EnvrInvPat) and green utility model patents (EnvrUtyPat), the regression results are presented in columns (1) and (2) of Table 4. The findings indicate that the coefficients for ISO are consistently significantly positive, with the conclusion remaining unchanged.

4.2.2. Altering the Sample Period

To mitigate the impact of the 2008 financial crisis, the sample data for 2008 was excluded, and the sample period was adjusted to 2009–2024. The regression results are presented in Column (3) of Table 4. The findings indicate that the coefficients for ISO remain significantly positive, and the conclusion remains unchanged.

4.2.3. Exclusion of COVID-19 Impact

As the COVID-19 pandemic erupted in early 2020, this study excluded data samples from 2020, 2021, 2022, and 2023. The regression results in column (4) of Table 4 indicate that the ISO coefficient remains significantly positive, demonstrating that the COVID-19 shock does not undermine the fundamental conclusions of this paper.

4.2.4. PSM Propensity Score Matching Test

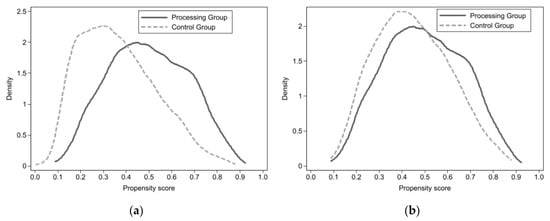

This study employs heavily polluting enterprises that have never obtained ISO 14001 certification as the control group, while designating those that have attained ISO 14001 certification as the experimental group. This approach aims to examine the impact of different factors on the level of green technological innovation within heavily polluting enterprises. This study employed 1:1 propensity score matching and conducted balance tests to evaluate matching effectiveness. The regression results in column (5) of Table 4 demonstrate statistical significance, further validating the robustness of the baseline regression outcomes. Table 5 presents a comparison of sample characteristics before and after PSM matching, revealing a significant reduction in differences between the experimental and control groups post-matching. Figure 2a,b illustrate the kernel density distribution of propensity scores.

Table 5.

Comparison of Sample Characteristics Before and After PSM Matching.

Figure 2.

Kernel density plots of propensity scores before and after matching; (a) Kernel density plots of propensity scores before matching; (b) Kernel density plots of propensity scores after matching.

4.2.5. Placebo Test

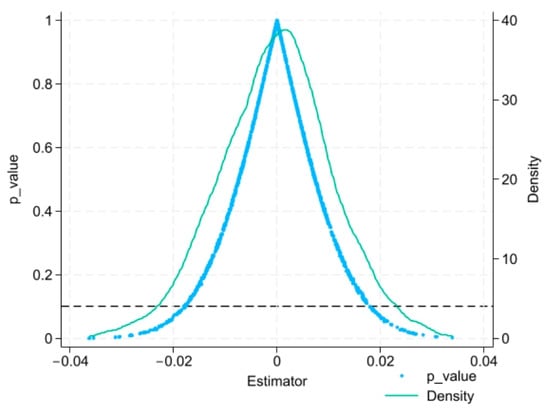

To eliminate the potential influence of unobservable factors or random disturbances on the benchmark regression results, this paper employs a placebo test to validate the robustness of ISO 14001 certification’s driving effect on green technological innovation. During the verification process, the original model specifications, control variables, and fixed effects remain unchanged. The actual variable is replaced with a randomly generated dummy treatment variable. Using the Monte Carlo simulation method, the certification status of enterprises is randomly assigned 1000 times. For each regression, the coefficient estimate and its standard error for the dummy variable are extracted, forming the empirical distribution of the random coefficient. As shown in Figure 3, the results indicate that the coefficients from the random simulation are densely clustered around the zero point, with the vast majority having absolute values below 0.02. This demonstrates that the model exhibits no systematic bias in the absence of genuine certification effects. In contrast, the true coefficient from the benchmark regression (0.0489) is significantly different from zero and lies well outside the range of the random estimates. Therefore, the placebo test confirms that the promotion of green technological innovation by ISO 14001 certification is not driven by unobservable random factors, and the robustness of the benchmark regression conclusions is established.

Figure 3.

Placebo Test Results. The horizontal dashed line represents the reference line at p = 0.1.

4.2.6. Instrumental Variables Tests

Although the preceding two-way fixed-effects specification, PSM matching, and placebo tests have substantially mitigated endogeneity concerns, potential endogeneity issues may still exist between ISO 14001 certification and corporate green technological innovation. On the one hand, reverse causality may arise, as firms with higher levels of green technological innovation may be more inclined to proactively obtain ISO 14001 certification to reinforce their environmental management image. On the other hand, unobservable factors such as corporate environmental strategy orientation and managerial environmental preferences may simultaneously influence both certification decisions and green innovation outputs, giving rise to omitted variable bias. To further alleviate these concerns, this paper draws on the methodological approaches of research and estimates the baseline model using an instrumental variable (IV) approach.

Specifically, drawing on the instrumental variable design of Hu et al. [1], this paper constructs the average ISO 14001 certification rate of all other firms within the same industry-year cell, excluding the focal firm itself, as the instrument for the endogenous variable ISO. The validity of this instrument rests on two grounds. With respect to relevance, the certification behaviour of peer firms within the same industry significantly influences the focal firm’s certification decision through peer effects, industry standard convergence, and competitive pressure, thereby satisfying the relevance condition. With respect to exogeneity, after excluding the focal firm itself, the industry-level certification rate of other firms is unlikely to be reversely affected by the focal firm’s own green innovation output, nor is it likely to directly influence the focal firm’s green technological innovation through channels other than its certification decision, thus satisfying the exclusion restriction.

Table 6 reports the results of the two-stage least squares (2SLS) estimation. Column (1) presents the first-stage results, in which the coefficient of the instrument (IV) is 0.009 and significantly positive at the 1% level, indicating a strong positive correlation between the instrument and the endogenous variable ISO. Furthermore, the Kleibergen–Paap rk Wald F statistic equals 387.558, far exceeding the Stock–Yogo critical value at the 10% maximal IV size level (16.38), thereby rejecting the null hypothesis of weak instruments; the Kleibergen–Paap rk LM statistic equals 346.075 and is significant at the 1% level, rejecting the null hypothesis of underidentification. These diagnostics jointly confirm the validity of the selected instrument. Column (2) reports the second-stage results: after re-estimation using the IV approach, the coefficient of ISO 14001 certification on green technological innovation (EnvrPat) is 0.151, significantly positive at the 10% level, which remains consistent with the baseline regression. This finding further corroborates the robustness of the core conclusion that voluntary environmental regulation significantly drives green technological innovation in heavily polluting enterprises.

Table 6.

Results of the robustness test using the instrumental variables method.

4.3. Mechanism Analysis

The benchmark regression and a series of robustness tests have consistently confirmed that ISO 14001 certification, as a typical form of voluntary environmental regulation, exerts a significantly positive driving effect on green technological innovation in heavily polluting enterprises. However, the theoretical hypotheses developed in Section 2 invoke multiple underlying mechanisms, including financing-constraint mitigation, learning effects, and interactive effects with command-and-control regulation that have not yet been directly tested in the empirical analysis. To bridge the gap between the theoretical narrative and the empirical evidence, this section conducts mechanism analyses along two complementary dimensions: a mediation analysis that opens the “black box” of the internal transmission path through which voluntary regulation affects green innovation, and a moderation analysis that examines how the external institutional environment, in particular the intensity of command-and-control regulation, shapes the effectiveness of voluntary regulation.

4.3.1. Mediation Analysis

The benchmark regression results have established the existence of a significant positive effect of ISO 14001 certification on green technological innovation, but the specific channel through which this effect operates remains to be identified. This part further conducts a mediation analysis along the financing-constraint transmission path, so as to align the empirical evidence with the theoretical narrative. ISO 14001 certification, as an important green signal that firms transmit to the capital market, can reduce the degree of information asymmetry between firms and investors and enhance the corporate image of environmental responsibility, thereby alleviating the external financing constraints faced by firms [50]; the mitigation of financing constraints, in turn, provides indispensable financial support for the long-cycle, capital-intensive, and high-risk R&D activities required for green technological innovation. In light of this, this paper measure corporate financing constraints using the SA index [51], and constructs the mediation models (3) and (4) to examine the mediating role of financing constraints in the process through which ISO 14001 certification affects corporate green technological innovation. Table 7 reports the regression results. The coefficient of ISO 14001 certification on the financing-constraint level (SA) reported in Column (2) of Table 7 is 0.005, which is significantly positive at the 1% level, indicating that ISO 14001 certification significantly alleviates the financing constraints faced by firms. Combined with the significantly positive effect of ISO 14001 certification on green technological innovation documented in the baseline regression of Table 3, as well as the result in Column (1) of Table 7, which shows that the coefficient of ISO 14001 certification on green technological innovation remains significantly positive after incorporating the financing-constraint variable into the model, it can be concluded that financing constraints play a significant mediating role in the process through which ISO 14001 certification drives corporate green technological innovation.

Table 7.

Mediation Analysis Results.

4.3.2. Moderating Effect

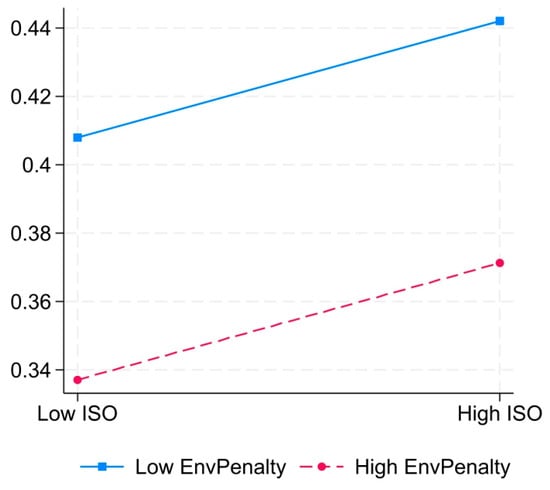

The ISO 14001 certification examined in this paper represents voluntary environmental regulation for enterprises. Beyond this, businesses may also face government command-and-control environmental regulations, which establish fundamental thresholds for compliance with environmental standards and form the initial baseline for corporate environmental conduct. Therefore, the intensity of command-and-control environmental regulation may interact with the implementation outcomes of voluntary environmental regulation by enterprises. In light of this, this paper constructs an interaction effect model integrating command-and-control environmental regulation, ISO 14001 certification, and their interaction term to analyse their impact on corporate green technological innovation. The moderation model (5) incorporates regional environmental administrative penalty intensity (EnvPenalty) and its interaction term with ISO 14001 certification (ISO × EnvPenalty). Table 8 column (1) reports the regression results. The coefficient for the interaction term ISO × EnvPenalty is 0.017, which is significantly positive at the 5% level. This indicates that the intensity of regional environmental administrative penalties (EnvPenalty) significantly enhances the driving effect of ISO 14001 certification on green technological innovation. As shown in Figure 4, the results of the moderation analysis indicate that command-and-control environmental regulation and voluntary environmental regulation are not mutually exclusive, but rather exhibit a significant complementary enhancement effect. This finding supports research hypothesis H2.

Table 8.

Moderation Effect Results.

Figure 4.

Moderation Effect Diagram.

4.4. Heterogeneity Test

4.4.1. Heterogeneity Test by Regulatory Status

By distinguishing between regulated and non-regulated enterprises, this study conducts an in-depth analysis of the structural role played by command-and-control environmental regulation in driving green technological innovation. The heterogeneity test results in Table 9 indicate that the effectiveness of voluntary environmental regulations (represented by ISO 14001 certification) is highly contingent upon whether enterprises operate within an environment constrained by mandatory regulations. Within the sample of enterprises subject to stringent environmental regulations, ISO certification exerts a significant and robust effect on promoting green technological innovation. Conversely, in the sample of non-regulated enterprises, the coefficient for ISO certification is merely 0.003 and exhibits weak statistical significance. This stark contrast demonstrates that, in the absence of a command-and-control regulatory framework, businesses often regard voluntary certification as a token gesture of compliance rather than a substantive driver of innovation [21].

Table 9.

Heterogeneity Analysis Results for Regulated and Non-Regulated Enterprises.

Therefore, environmental policy frameworks cannot rely solely on voluntary corporate action but must maintain the foundational role of command-and-control regulation [52]. Appropriate command-and-control standards and regulatory measures can foster a level playing field in the market, thereby creating the necessary conditions for the implementation of voluntary regulation [53]. This conclusion substantiates Hypothesis H3.

4.4.2. Nature of Enterprise Ownership

The nature of property rights, as a key dimension of corporate heterogeneity, profoundly influences firms’ responses to environmental regulations. For regression analysis, the complete sample is split into two categories in this paper: state-owned businesses and non-state-owned businesses. The results are presented in columns (1) and (2) of Table 10. Research indicates that while ISO 14001 certification significantly promotes green technological innovation in both types of enterprises, the intensity of its impact varies markedly. Research indicates that ISO 14001 certification exerts an innovation-driving effect in both types of enterprises, but the response intensity differs markedly between them: in the non-SOE sample, the ISO coefficient is significant at the 5% level, whereas in the SOE sample, it is only marginally significant at the 10% level. More importantly, the Chow test confirms that the difference in regression coefficients between the two subsamples is statistically significant, indicating that voluntary environmental regulation exerts a more robust and reliable driving effect on green technological innovation among non-state-owned enterprises.

Table 10.

Results of Heterogeneity in Enterprise Ownership Structure.

This finding resonates significantly with the earlier conclusion that command-and-control environmental regulation can promote green technological innovation among ISO 14001-certified enterprises, further illuminating the complex boundaries of regulatory effects [53]. For non-state-owned enterprises, operational decisions are more aligned with market logic, subject to stringent financing constraints and competitive pressures. Moderate command-and-control regulation can provide clear external incentives and legitimacy support for their adoption of ISO certification. However, should government regulation become excessively stringent, it may substantially increase compliance costs and operational burdens for non-state-owned enterprises, diverting resources away from research and development [54]. Our finding that excessive command-and-control regulation may divert innovation resources is consistent with recent evidence showing that firms under carbon peaking pressure engage in earnings management as a coping strategy [55]. This would conversely undermine the effectiveness of voluntary regulation, thereby confirming Hypothesis H4.

4.4.3. Verification of the Company’s Geographical Location

This study divides the sample into three sub-samples: Eastern, Central, and Western regions for separate regression analysis. The results of the geographical heterogeneity analysis reveal significant regional variations in the impact of voluntary environmental regulations (represented by ISO 14001 certification) on green technological innovation among heavily polluting enterprises. Specifically, a gradient effect is observed, with the influence diminishing progressively from the Eastern region towards the Central and Western regions. The regression results are presented in Table 11. This regional disparity can be explained through three dimensions: institutional environment, market conditions, and resource endowment. Firstly, the eastern regions possess a more robust environmental regulatory enforcement framework and face stricter oversight pressures [56]. This compels enterprises not merely to meet compliance requirements, but to proactively pursue ISO 14001 certification to enhance environmental management capabilities in response to persistent regulatory challenges. Consequently, certification is transformed into substantive innovation. Secondly, the eastern regions possess more mature factor markets and stronger demand for green technologies. Green innovation can deliver more pronounced competitive advantages and economic benefits for enterprises, incentivising them to internalise voluntary regulations into their innovation strategies. Moreover, the eastern regions harbour a greater concentration of innovation resources, including highly skilled talent, research and development institutions, and green financial support, thereby providing essential backing for enterprises to pursue green technological innovation [57].

Table 11.

Results of Enterprise Geographical Location Heterogeneity.

By contrast, central and western regions exhibit relative weaknesses in environmental enforcement intensity, market incentives, and innovation resources. Enterprises there frequently regard ISO 14001 certification as a symbolic measure to meet basic compliance requirements or secure legitimacy, rather than a strategic tool to drive technological innovation [58]. Particularly in the western regions, the coefficients are insignificant, and the influence of control variables such as firm size and profitability is relatively weak, reflecting that systemic constraints faced by enterprises in this region during the green transition are more pronounced.

5. Discussion

This study, drawing on a sample of Chinese heavy-polluting listed companies from 2008 to 2024, systematically examines the driving effect of voluntary environmental regulation on green technological innovation and its interactive mechanisms with command-and-control regulation. The empirical findings provide robust support for all four working hypotheses and warrant interpretation in dialogue with the existing literature.

5.1. Voluntary Regulation as a Driver of Green Innovation

Our benchmark results Table 3 show that ISO 14001 certification exerts a significantly positive effect on green technological innovation, with the effect remaining robust across multiple sensitivity tests. This finding supports Hypothesis H1 and aligns closely with previous studies [1,9,10], which document the innovation-driving effects of voluntary environmental certification. More importantly, our results provide empirical validation for the Porter Hypothesis within the Chinese context, suggesting that appropriately designed environmental institutions can stimulate the “innovation compensation effect” emphasised by Porter. In contrast to studies that interpret voluntary regulation primarily as a signalling device, our findings indicate that ISO 14001 certification has a substantive innovation-driving function among heavy-polluting enterprises.

5.2. The Complementary Effect Between Command-and-Control and Voluntary Regulation

The moderation analysis Table 8 reveals that regional environmental administrative penalty intensity significantly amplifies the innovation-driving effect of ISO 14001 certification, supporting Hypothesis H2. This finding offers an important extension to the existing literature. Whereas prior studies such as Wang tend to treat command-and-control and voluntary regulations as mutually exclusive instruments [20], our results reveal a complementary rather than substitutive relationship: command-and-control regulation, by establishing baseline standards and providing enforcement pressure, creates the institutional environment in which voluntary regulation can take effect. The findings document that formal institutional arrangements and informal pressures can jointly shape corporate green innovation, and provide direct evidence for the theoretical proposition of regulatory synergy [22].

5.3. Command-and-Control Regulation as an Important Enabling Condition

The heterogeneity analysis based on regulatory status Table 9 shows that ISO 14001 certification significantly drives green innovation among regulated enterprises, while the effect is essentially absent in non-regulated enterprises. This stark contrast supports Hypothesis H3 and is consistent with the findings of Zhang et al., who observe that environmental regulation effects depend heavily on the underlying institutional context [21]. Our findings further indicate that without command-and-control regulation as a stabilising institutional foundation, voluntary certification tends to degenerate into symbolic compliance rather than translating into substantive innovation, offering a plausible explanation for the divergent effects of voluntary instruments observed across countries and regions.

5.4. The Crowding-Out Effect of Excessive Regulation

The heterogeneity analyses based on ownership structure Table 10 and geographical location Table 11 show that the innovation-driving effect of ISO 14001 certification is more pronounced in non-state-owned enterprises and eastern-region firms, supporting Hypothesis H4. These findings corroborate the U-shaped relationship between command-and-control regulation and green innovation, complement the crowding-out evidence [33,34]. Our results suggest that the relationship between regulatory intensity and innovation is non-monotonic: moderate command-and-control regulation, when paired with voluntary regulation, generates synergy, but excessive coercive regulation distorts firms’ incentive structures, reorienting their motives from proactive innovation toward passive compliance. This insight indicates that the pursuit of stronger regulation is not always conducive to green innovation, and that an optimal regulatory mix must balance constraint and flexibility.

5.5. Limitations of Variable Measurement and Robustness Considerations

This study employs ISO 14001 certification as a proxy for voluntary environmental regulation. While this choice offers advantages in terms of data availability, international comparability, and clear institutional content, it also entails three limitations that we transparently acknowledge. First, as a binary dummy variable, it cannot finely capture the actual operational intensity or depth of internal environmental management systems. Although the annual surveillance and three-year recertification mechanisms of ISO 14001 institutionally filter out post-certification complacency, firms that abandon system maintenance ultimately lose their certification. The risk of audit formalism cannot be entirely ruled out. Second, firms’ motives for obtaining certification are mixed, potentially encompassing strategic voluntariness, supply chain compliance, and the pursuit of policy incentives simultaneously. Our empirical design cannot fully disentangle the differentiated effects of these distinct motives. However, it bears emphasising that the theoretical validity of voluntary regulation does not require purity of motive but rather autonomy of decision, a feature that fundamentally distinguishes it from the legal coercion of command-and-control regulation. Third, this study has not incorporated other voluntary regulatory instruments that have rapidly emerged in recent years for composite measurement. Future research could employ continuous indicators such as ESG ratings to more precisely characterise environmental management depth, and incorporate emerging voluntary instruments like Green Factory certification for composite measurement.

5.6. Future Research Directions

Building on the limitations identified above, several promising avenues warrant future exploration. First, future studies could move beyond binary measurement by employing continuous or multidimensional indicators, such as ESG ratings, environmental disclosure quality scores, or text-mining-based indices to more precisely characterise the operational depth of corporate environmental management. Second, with the rapid emergence of new voluntary regulatory instruments such as Green Factory certification, CDP disclosure, and science-based targets, future research could construct composite measurement frameworks integrating multiple instruments to capture the heterogeneity of voluntary regulation and examine whether different instruments exert differentiated or synergistic effects. Third, the interactive mechanism between command-and-control and voluntary regulation revealed in this study opens up further inquiries, including the identification of optimal regulatory intensity thresholds through threshold regression models, the dynamic evolution of regulatory synergy as institutional environments mature, and cross-country comparative studies testing whether the synergy mechanism documented in the Chinese context generalises to other institutional settings. We hope this study can serve as a useful starting point for these future inquiries.

6. Conclusions

Using ISO 14001 environmental management system certification as the primary proxy variable, this study systematically investigates the driving effect of voluntary environmental regulation on green technological innovation and its interactive mechanism with command-and-control environmental regulation. It is based on sample data from listed companies in China’s heavily polluting industries between 2008 and 2024. The research yields the following principal conclusions:

Firstly, voluntary environmental regulation (ISO 14001 certification) significantly promotes green technological innovation among heavily polluting enterprises, supporting the applicability of the “Porter Hypothesis” in China. This shows that endogenous innovation inside businesses can be stimulated by moderate environmental regulation, yielding benefits for both the environment and the economy. Secondly, there exists a significant complementary effect between command-and-control and voluntary environmental regulations. The intensification of regional environmental administrative penalties has amplified the driving force of ISO 14001 certification for green technological innovation, demonstrating that the coordinated implementation of these two regulatory approaches can form a more effective policy combination, jointly propelling corporate green innovation.

Thirdly, command-and-control environmental regulation serves as a crucial prerequisite for voluntary regulation to be effective. Research indicates that within enterprises subject to stringent environmental controls, ISO 14001 certification exerts a more pronounced effect in stimulating green technological innovation. Conversely, in non-regulated enterprises, this effect is negligible, demonstrating that voluntary actions lacking binding constraints struggle to translate into substantive innovation drivers.

Fourthly, excessive command-and-control regulation may undermine the motivational effect of voluntary regulation. In particular, in non-state-owned enterprises, high-intensity external oversight may divert innovation resources and distort behavioural incentives, thereby dampening enthusiasm for green technological innovation. In other words, excessively prescriptive command-and-control regulation can divert resources away from innovation and undermine the effectiveness of voluntary regulation, which suggests that the relationship between regulatory intensity and innovation is non-monotonic and that an optimal regulatory mix must balance constraint with flexibility.

Moreover, heterogeneity analyses reveal that the innovation-stimulating effects of voluntary regulation exhibit structural variations across different property rights regimes, geographical regions, and regulatory environments. These effects are particularly pronounced among non-state-owned enterprises, firms in eastern regions, and those operating under stringent regulatory frameworks.

7. Policy Recommendations

7.1. General Policy Recommendations

This study makes the following policy recommendations in light of the research findings mentioned above: