Abstract

The increasing penetration of renewable and distributed resources signals a global boom in energy transition, but traditional grid utilities have yet to share in much of the triumph at the current stage. Higher grid management costs, lower electricity prices, fewer customers, and other challenges have emerged along the path toward renewable energy, but many more opportunities await to be seized. Most importantly, there are insufficient studies on how grid utilities can thrive within the hydrogen economy. Through a case study on the State Grid Corporation of China, we identify the strengths, weaknesses, opportunities, and threats (SWOT) of grid utilities within the hydrogen economy. Based on these factors, we recommend that grids integrate hydrogen into the energy-as-a-service model and deliver it to industrial customers who are under decarbonization pressure. We also recommend that grid utilities fund a joint venture with pipeline companies to optimize electricity and hydrogen transmissions simultaneously.

1. Introduction

Climate change is a global challenge that threatens the well-being of humans in various ways [1]. Previous studies have indicated that climate change will bring uncertainties to production activities [2], cause economic losses [3], and jeopardize physical [4] and mental health [5]. Since most greenhouse gas (GHG) emissions come from energy-related activities [6], taking action in energy transition becomes imperative in mitigating climate change. Indeed, the energy sector could contribute to the largest reduction in carbon emissions at a reasonable cost [7] given the continuous downtrend in the cost of renewable energies [8]. However, grid utility, a traditional key player in the energy system, may confront some consequential challenges, either technical or business-related. For instance, intermittency [9] and curtailment [10] in renewable energy systems are two major technical challenges, and vast changes in generation source portfolios may also pose a business challenge to utilities [11,12,13,14,15,16]. While technical challenges are critical, this paper will mainly focus on business challenges and assess how a traditional grid utility can adapt to this transition through new business strategies, which have drawn increasing attention in recent energy transition research [12,15].

From the business perspective, the increasing penetration of renewables will affect the traditional revenue model of grid utilities. Revenue-wise, empirical results indicate the existence of a negative correlation between the share of renewables in power generation and the ultimate electricity price [17]; other findings also reveal that the growth in distributed energy resources has diminished end customers’ dependence on grids [16,18], threatening the growth and maintenance of this customer base. In this sense, as the energy system becomes more renewable and decentralized, the total volume of electricity may no longer be the most appropriate reference for grids to charge customers and, thus, project future incomes; the maximum power capacity delivered may work better instead [13,14]. Cost-wise, grid utilities are confronting economic pressures to upgrade local substation capacities, allowing for better access to this distributed resource [19]; more investment in energy storage and other alternatives will be needed to cope with the intermittency of renewables and, thus, improve the reliability of the grids [20].

Many researchers have conducted studies on business model innovations for grid utilities in a high-renewable-penetrated electricity sector. Alova reviewed the generation portfolios of more than 3000 grid utilities globally between 2001 and 2018 and found that grid utilities play a relatively passive role in energy transition [21]. She found that only about one-third of grid utilities expand their portfolios, mainly in the form of fossil fuel units; even among those with renewable assets dominating their portfolio expansions, 60% of them have expanded their fossil fuel units at the same time. Pereira et al. studied the evolution of 20 European grid utility business models by examining their mergers and acquisitions (M&A), investments, and strategic alliances [22]. They discovered that European grid utility companies prefer renewable generators, especially wind power, and tend to increase capacity via M&A. Bryant et al. further identified four more emerging business models that deal with higher renewable penetration based on studies of 50 grid utilities in Europe and Australia [11].

However, these papers have not well explained the different roles of generation companies, transmission grid operators, and distribution operators. Therefore, they have not presented the most comprehensive strategy sets they could possibly consider within the grid utility ecosystem. As more deregulation policies are implemented around the world [23], it will become more common for grid utilities to be unable to own large generation assets and focus on transmission and distribution (T&D) networks only. Furthermore, even if some research projects have elaborated business innovations at the T&D level, they focused more on distributed generation [24,25] and smart grids [26,27], paying little attention to hydrogen.

Indeed, hydrogen is considered a key component in smart grid systems [28]. While some papers have proposed integrating hydrogen storage into smart grids [29,30,31], other researchers take a further step in the analysis of hydrogen vehicle applications within smart grids [32,33]. Besides distribution aspects, hydrogen is also considered at the transmission level. Based on a lifecycle cost analysis, Semeraro compared high voltage direct current (HVDC) transmission lines with hydrogen pipelines and concluded that hydrogen pipelines could be a more competitive option at transmission distances of more than 1000 miles by 2030 [34]. A levelized cost analysis by Patel et al. delivered a similar conclusion, in that hydrogen pipelines could become more competitive than HVDC in 2050 at transmission distances of more than 350 km [35]. Wu et al. optimized the transmission capacities of hydrogen pipelines, natural gas pipelines, and high-voltage transmission lines in China to determine the lowest system transmission cost [36]. Zwaan et al. depicted scenarios in which Europe imports both electricity and hydrogen from Africa via HVDC transmission lines and hydrogen pipelines in a collaborative manner [37].

In this paper, we will address the knowledge gap in how a T&D company could participate in the hydrogen economy by conducting a case study on the State Grid Corporation of China. In other words, this research tries to answer two questions: (1) whether T&D companies should enter the hydrogen industry, and (2) if they should, what are the most appropriate business strategies to take? The remainder of this paper is structured as follows: Section 2 outlines the research method, the strength–weakness–opportunity–threat (SWOT) analysis framework, and the background of the company; Section 3 elaborates on the identification of SWOT factors; Section 4 provides business strategy recommendations based on the SWOT analysis; and Section 5 ends the paper with a conclusion and the implication we learned from the case study.

2. Materials and Methods

2.1. SWOT Analysis

SWOT analysis is a traditional, yet popular, analytic tool that helps organizations navigate their business strategies with a better understanding of their internal and external circumstances [38,39]. Other traditional strategic tools, such as Porter’s five force framework, are usually applicable in analyzing more general scenarios rather than specific new business cases [40]. Newly invented complex strategic planning tools, such as the fuzzy analytical hierarchy process model [41], are also useful, but they may not be the best tools to communicate with the ultimate decisionmakers in companies. In this sense, SWOT is a more suitable tool. Strengths and weaknesses are internal factors that can be identified through organizational analyses, and opportunities and threats are external factors that can be identified through environmental analysis. The factor identification process will be further navigated using the value chain model and the policy, economic, socio-cultural, and technological (PEST) framework to yield a more rigorous and systematic analysis. Organizations consider all these factors to build four strategies, SO, ST, WO, and WT, which are known as the SWOT/TOWS matrix [39]. Despite the clarity and popularity of the SWOT method, it has been criticized for its reliance on subjective perceptions, highlighting the importance of stakeholder engagement during the process [42]. Thus, in this paper, SWOT is combined with expert elicitation to yield more insightful results.

SWOT analyses have been widely applied in the energy industry. Recent applications include analyses of renewable energy development in India, China, Iceland, Sweden, and the US [43]; wind energy development in Pakistan, India, and Bangladesh [44]; hydropower development in Pakistan [45]; and nuclear development in Ghana [46]. As for hydrogen development in China, Ren et al. conducted a SWOT analysis in 2013 in which they prioritize the hydrogen development strategies for China but not for any corporations [47]; later in 2021, Li et al. updated the SWOT factors and focused more on large-scale green hydrogen [48]. The popularity of SWOT in the hydrogen and energy world also helps justify the use of its framework as the main analytic tool in this paper.

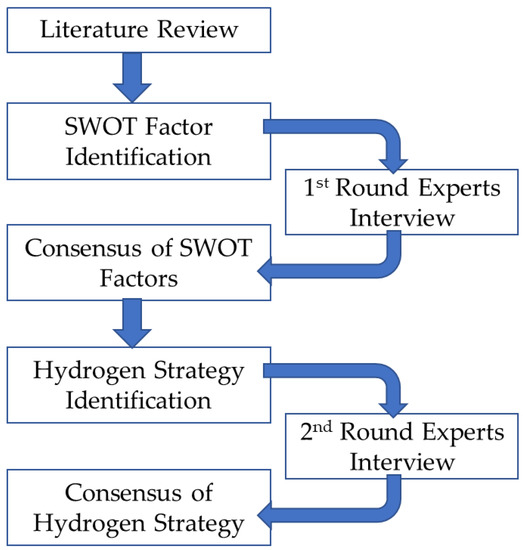

The SWOT analysis in this paper was carried out in three steps, following Figure 1.

Figure 1.

Workflow of the analysis.

- Preliminary SWOT factors were identified through brainstorming and a literature review by applying the value chain and PEST models, from which preliminary strategies may be derived.

- The preliminary findings on the SWOT factors were subject to revision after receiving feedback, comments, and insights from a small group of experts from the grid sector, academia, and hydrogen-related industries (Table 1).

Table 1. Description of the expert group interviewed.

Table 1. Description of the expert group interviewed. - Strategies were developed based on the SWOT factors and were further polished based on input from experts via interviews.

Since the expert group was relatively small, only the SWOT factors and strategies that received no objections will be identified and discussed in this paper.

2.2. The State Grid Corporation of China

In 2022, the State Grid Corporation of China (SGCC) is the largest company in China by revenue, with more than 800,000 employees and 1 billion customers. Its core business covers the electricity grid in terms of investments, construction, operations, transmission, and distribution. While the SGCC also has a footprint in finance, real estate, and other industries, this research will mainly focus on its business stake in electricity transmission and distribution. In the past, the SGCC played the role of a retailer in its transmission and distribution business; it could sell electricity directly to end customers and profit from the difference between retail and wholesale prices. With recent rounds of market reform [49] that encourage customers to participate in the wholesale market, the SGCC, as a transmission company, may only charge transmission fees. In this sense, engaging in the hydrogen market may be a necessary move to maintain the SGCC’s market leadership.

The analyses and conclusions of this research can also be extended within or outside the SGCC’s ecosystem. Besides its domestic operations, the SGCC invests in many electricity companies overseas. Once the SGCC proves the effectiveness of its business models and market strategies regarding hydrogen in China, it can promote these experiences to its global networks, contributing to global energy transitions and hydrogen economy development. Furthermore, as an electricity transmission and distribution company, the SGCC shares many similarities with other grid companies all over the globe; thus, some SWOT factors identified in this paper might also serve as valuable references for other companies.

3. Results: SWOT Factor Identification

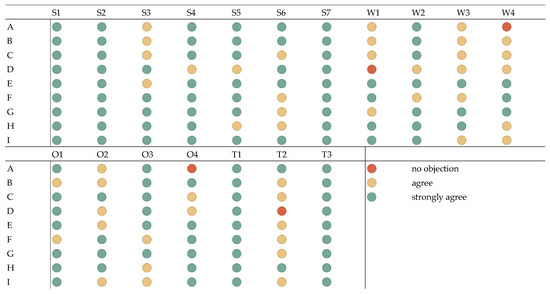

Table 2 summarizes the identified SWOT factors, and Figure 2 presents expert opinions on those factors. This section will discuss these factors in detail.

Table 2.

Summary of identified SWOT factors.

Figure 2.

Expert opinions on the identified factors.

3.1. Strengths

3.1.1. Leading Electricity Transmission Technology

The SGCC has unequivocal advantages in its ultrahigh-voltage transmission technology [50], and this could benefit the construction of hydrogen pipelines to some extent. At first glance, this strength does not directly contribute to the hydrogen economy due to the competitive relationship between hydrogen pipelines and HVDC lines, as they can both deliver energy, in different forms, to end customers [36]. However, the acknowledgment of such a relationship can yield more precise judgments on the development of hydrogen pipelines, as well as potential synergy. For instance, in an area that has already planned for HVDC lines, building hydrogen pipelines will be less economical, but setting up electrolyzers for onsite hydrogen generation would be an effective way to meet the local demands for hydrogen. As demonstrated by previous research [34,35], in some cases, by better understanding the cost of HVDC lines, system planners can assess the economic advantages of hydrogen pipelines under certain conditions (e.g., distance) more accurately.

3.1.2. Leading Smart Grid Technology

Another key technical advantage lies in the smart grid field, which can include hydrogen integration. The SGCC has published several technical standards on smart grids and is a pioneer in implementing smart grid and Internet of Things pilot projects [51,52,53]. Given these achievements, the SGCC has already initiated research or pilot projects for hydrogen integration within microgrids. For instance, the SGCC started several research projects on hydrogen–wind–solar microgrid management in 2020. In 2022, it also constructed a pilot project in Cixi City and another on Dachen Island, both within Zhejiang Province. This leadership in smart grids provides a solid technical foundation to test the business model of hydrogen applications.

3.1.3. Mature and Efficient R&D Mechanism

The SGCC could leverage its advantageous R&D mechanisms to ensure its leadership in smart grid and transmission technologies. Rikap stated that the SGCC has the potential to become a global intellectual property monopoly, benefiting from public research grants and national innovation system resources [54]. As the SGCC’s mature and high-quality research and development mechanism continues to prosper, it is expected to maintain its leadership in ultrahigh-voltage transmission, smart grids, and many other technologies. This will likely bring synergy, thus allowing the SGCC to maintain its unique leadership position in the hydrogen industry for the foreseeable future.

3.1.4. Solid Economic and Operational Foundation

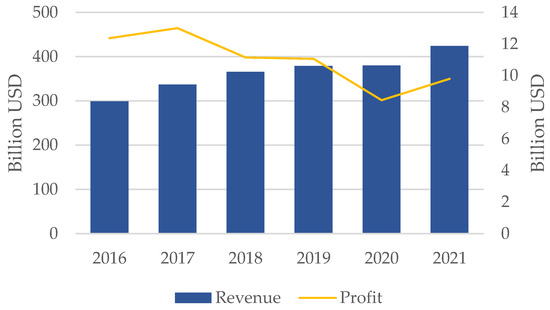

Fundamentally, the SGCC is one of the companies with the highest operating revenues in China and around the globe, offering a solid monetary foundation for any new business strategies. It serves 1.1 billion customers across 26 provinces or equivalent administrative divisions in China, and such huge client coverage offers an ideal channel to promote new hydrogen-related businesses. In 2021, the SGCC earned more than CNY 2.9 trillion in revenue (approx. USD 0.4 trillion, assuming an exchange rate of USD 1 = CNY 7) and CNY 68.6 billion in profit (approx. USD 9.8 billion) [55]. As shown in Figure 3, despite fluctuating profits, this revenue shows an upward trend in the last five years. Such a strong financial performance provides considerable flexibility and capability for new business development options, including in-house incubation, mergers and acquisitions, and joint ventures.

Figure 3.

Historical revenue and profits of the SGCC, assuming USD 1 = CNY 7.

3.1.5. Robust Bargaining Power in Capital Market

Furthermore, the SGCC has strong bargaining power in the financial market, ensuring the financial stability of new projects during the investment process. Being a state-owned enterprise (SOE) and given its proven track record in successfully managing many capital-intensive projects, the SGCC could receive a better credit rating and, thus, more favorable terms in the capital market. Furthermore, the SGCC actively explores emerging financial instruments, such as carbon-neutral bonds [55], to further enhance its capital-raising capabilities, embracing new opportunities in the green finance market.

3.1.6. Firm Commitment to Carbon Neutrality

In the SGCC’s corporate responsibility report, its determination to reduce carbon emissions is emphasized in both the corporate action plan and corporate culture sections [56]. However, such plans cannot just stay on paper. The SGCC has already taken actions to support the energy transition via resource coordination, new transmission development, and guidance on energy development and integration [57]. Given the important role that hydrogen can play in realizing ultimate carbon neutrality, it is possible that green hydrogen-related businesses will be integrated into the plan in the future; once this happens, more internal resources will be skewed toward green hydrogen development.

3.1.7. Tight Involvement in Policymaking and Implementation

As the largest SOE in China, the SGCC possesses considerable influence over national policymaking processes given its tight connection to national and regional Chinese administrations [58]. It is also evident that it would be socially responsible for the SGCC to pioneer pilot projects or implement national policies regardless of many foreseeable or unforeseeable difficulties, climate policies included. With this in mind, the SGCC could initiate new policies with governments and other stakeholders to promote hydrogen-related businesses.

3.2. Weaknesses

3.2.1. Potential Organizational Inertia

It is almost inevitable for the SGCC to go through comprehensive, yet complicated, decision-making processes to obtain its desired outcomes, just as many other large corporations do, and this kind of inertia could hinder the progress of future projects. Caution is important in the decision-making process of capital-intensive projects involving multiple stakeholders, and the outstanding financial performance of the SGCC’s traditional transmission line business may be the best evidence of this. However, such a conservative way of managing projects may no longer be the best-fit strategy in response to the quickly evolving business environment in the hydrogen industry. However, the SGCC has established innovation centers with relatively high autonomy to accelerate its responses to any emerging needs.

3.2.2. Large Readiness Gap in Hydrogen Technology

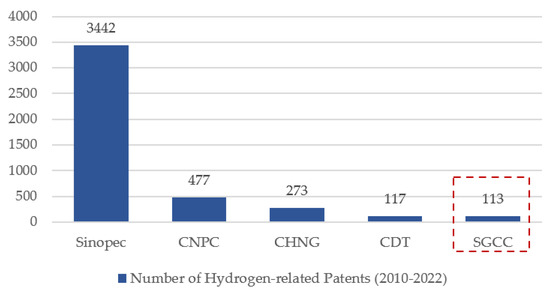

Even though the entire hydrogen industry is still at an early stage of development, the SGCC does not yet possess a full set of technical solutions to confidently blend into the hydrogen industry’s value chain, and this gap is not likely to be filled anytime soon. Currently, the SGCC faces direct technical challenges throughout the lifecycle of hydrogen production, storage and transmission, and utilization. Still, it is possible to leverage the SGCC’s efficient and effective innovation system to catch up with other hydrogen companies’ technological competencies; however, the comparative advantage in innovation development may not necessarily hold in comparison with other large SOEs, such as Sinopec, which have already engaged in hydrogen-related projects and gathered talent, patents, and track records, as they also benefit from involvement in the national innovation system. As shown in Figure 4, although the SGCC accumulated 113 hydrogen-related patents between 2010 and 2022, it has the smallest number of patents among the listed SOE peers. Petrochemical companies such as Sinopec and the China National Petroleum Corporation (CNPC) have received far more hydrogen-related patents than others, followed by power generation groups such as the China Huaneng Group (CHNG) and the China Datang Corporation (CDT), making the SGCC’s achievements less impressive.

Figure 4.

Number of hydrogen-related patents from the key SOE players in China’s hydrogen industry. Hydrogen-related patents here are defined as patent titles that include hydrogen. The records were retrieved from Google Patent Database with filling years ranging from 2010 to 2022. Sinopec: China Petroleum and Chemical Corporation; CNPC: China National Petroleum Corporation; CHNG: China Huaneng Group; CDT: China Datang Corporation.

Another risk scenario rising from managerial expectations may be the stereotype relating to Chinese SOE measures of innovative achievement, which often emphasizes the number of innovations over the quality [57], resulting in insufficient organizational breakthroughs in hydrogen technologies despite tremendous resources and effort.

3.2.3. Potential Impact of Policy Factors on Financial Performance

The SGCC has delivered impressive financial figures, but ongoing reform in the Chinese electricity market also brings uncertainties to its future performance. Since at least March 2015, this has profoundly changed the landscape of the grid business, and deeper reforms are expected in the near future [59]. In the past, grid utilities such as the SGCC could purchase electricity from generators at wholesale prices and sell it to end customers at retail prices, earning the difference. Now, guided by new policies, grid utilities can no longer serve as brokers. Instead, they can only charge transmission fees, which narrows the SGCC’s margins. Furthermore, end customers are now encouraged to directly participate in the electricity market. End customers can also ask grid utilities to purchase electricity on their behalf, but grids are no longer allowed to charge service fees [49], which could further weaken the SGCC’s revenue stream. Lastly, the emerging ancillary service market in China, which is supposedly designed to compensate grid utility companies for their grid management costs, is still evolving [60], and its effects require more feedback and further examinations to justify financial expectations.

3.2.4. Potential Anti-Trust Challenges

The grid and transmission industry is a natural monopoly, and anti-trust probes are an almost inevitable hurdle to every grid utility. While the SGCC’s traditional electricity-related business is strictly regulated by the Electric Power Law of the People’s Republic of China, legislative concerns about this grid utility’s qualifications in entering the hydrogen market are possible if the SGCC starts to gain a considerable share of this business. In the worst-case scenario, the SGCC may need to spin off its hydrogen business. The main concern lies in the transmission sector of the hydrogen business. Since the SGCC already dominates the electricity transmission sector, transmitting another type of energy could draw regulatory attention. It is also worth noting that the SGCC may not enter the hydrogen production business. The SGCC was first created as a result of splitting the electricity generation and transmission functions of the National Electric Power Company, indicating a gray zone for the SGCC to engage in the production of different energy types, hydrogen included. However, other aspects, including hydrogen delivery and utilization, may be less regulatorily pressured sections of the hydrogen business for the SGCC to consider.

3.3. Opportunities

3.3.1. Tremendous Governmental Support at Various Levels in China

Hydrogen is a key pillar contributing to the energy transition in China, and governmental support will play an essential role in improving the industry, at least in the early stages. While the national government has published ambitious action plans to promote the development of the hydrogen industry [61], local governments have also introduced numerous supporting policies, such as direct subsidies to equipment manufacturers, hydrogen refilling stations, and hydrogen vehicles. Previous research has demonstrated that effectively implementing supporting policies in China, especially in the form of investment-based subsidies and income tax cuts, could promote the rapid development of the local green hydrogen industry at this early stage [62]. Numerous supporting policies for the hydrogen industry have emerged since 2019 [63], and they represent a great opportunity for interested parties to engage in the hydrogen market, even if these policies will be gradually retired as the costs of the supported hydrogen technologies and corresponding applications reach a reasonable readiness level. Additionally, these supporting policies have also improved public awareness and acceptance of hydrogen [47,64], creating a more friendly public opinion about the implementation of hydrogen projects. A detailed summary of supporting policies related to hydrogen development in China can be found in Appendix A.

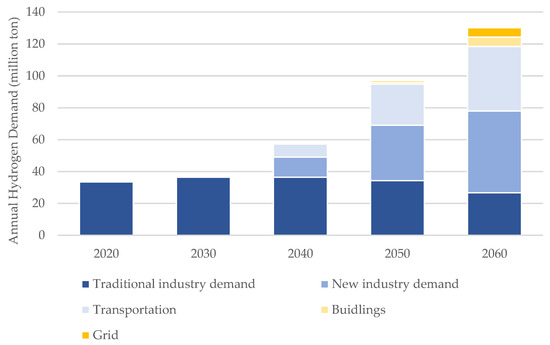

3.3.2. Growing Hydrogen Demands Resulting from Decarbonization Goals in China

China’s “30–60” decarbonization goal will drive up the expected overall demand for hydrogen. In 2021, China already had the second largest electrolyzer manufacturing capacity, right after Europe, and the largest operational electrolysis capacity (200 MW) in the world [65] within the hydrogen production sector; however, such a huge production capacity may still be inadequate for China’s ambitious goal of reaching a “carbon peak in 2030 and carbon neutrality in 2060”. As shown in Figure 5, the China Hydrogen Alliance estimates that the demand for hydrogen could reach 37 million tons in 2030 and 130 million tons in 2060 [66]. The booming downstream demand will, without a doubt, benefit all players in the entire value chain of the hydrogen industry. Additionally, China, leveraging its experience as a “world factory”, could also undertake hydrogen needs from other countries, such as Japan [67], from which players may seize market opportunities by specifically transitioning to the liquified hydrogen transportation business.

Figure 5.

Future hydrogen demand in China projected by the China Hydrogen Alliance [66].

3.3.3. Evident Cost Advantages in Hydrogen Production in China

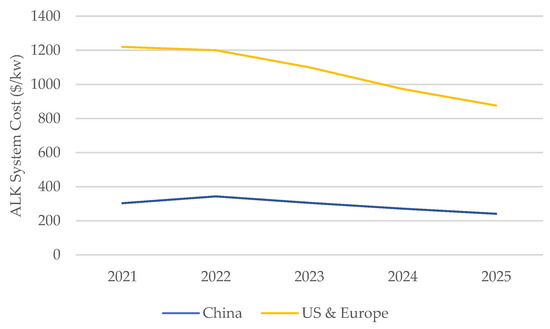

China has a significant advantage in hydrogen production costs, allowing for market competitiveness and profitability. Equipment-wise, Bloomberg estimated that the price of alkaline electrolysis systems (ALKs) in China was only a quarter of that in Europe and the US in 2021 [68]; in 2025, the price of electrolyzers in China will be USD 241/kW, still much lower than USD 876/kW in the EU and US after a period of rapid innovation and cost reduction (Figure 6). The cost of solar and wind power is another key cost element in the production of green hydrogen, and a recent IRENA study estimated that China has the lowest LCOE for solar PV and is one of the countries with the lowest LCOE for wind [69]. Both factors could help Chinese players, hydrogen producers included, in the hydrogen industry to better control costs and set pricing strategies accordingly.

Figure 6.

Future alkaline electrolysis system costs projected by Bloomberg [68].

3.3.4. Emerging Chances to Seize a First-Mover Advantage

The hydrogen industry, similar to other capital-intensive, emerging high-tech industries, could favor first-movers and ultimately become an oligopolistic market, especially in the infrastructure sector. Hydrogen infrastructures, including equipment used in hydrogen production, storage, transmission, and utilization, have high technical barriers to entry, and some components, such as pipelines, require heavy initial investments to realize the economy of scale—the difficulties will only be amplified as the market becomes more mature. On the one hand, such high barriers set tough requirements on the technical capabilities of new participants, and successful players could leverage technical strengths to lead technical standards and specifications, reinforcing their leadership over time. On the other hand, these barriers also limit the capacity of the market pool, encouraging the entire industry to move toward a more oligopolistic market along the industry’s lifecycle [70]. In this sense, companies that have, or could develop, competitive technical strengths will more likely gain and secure more market shares if they enter the hydrogen industry at such an exploratory moment.

3.4. Threats

3.4.1. Amplified Geopolitical Uncertainty to Challenges Supply Chain Stability

High technical barriers bring opportunities for early participants with relevant capabilities, but establishing and maintaining these capabilities may rely on a well-structured supply chain with global efforts, which will become more difficult because of current geopolitical uneasiness. In the hydrogen industry, key components, such as catalysts, carbon paper, proton exchange membranes, and metal bipolar plates, can only be procured from international vendors [71]; even if other components, such as membrane electrodes, can be purchased from Chinese suppliers, the quality may be less competitive than that of international competitors [71]. Such technical incompetence poses a geopolitical threat to the development of the Chinese hydrogen industry, which will be sensitive to challenges, such as increased tariffs, trade bans, and other sanctions [70,71].

3.4.2. Emerging Technologies Disrupt the Existing Competitive Landscape

Emerging technologies could overturn the current landscape, threatening the market share, financial performance, and the even survival of existing players or projects. These new technologies could bring better cost-efficiency or introduce new applications, bringing higher profits to stakeholders. Taking the hydrogen production sector as an example, currently, most of the electrolyzers in China are alkaline systems, and the China Hydrogen Alliance expects the PEM will gain more market share in the future [66]. Such competition is within expectations and not disruptive. The concern lies in technologies with more uncertainties, such as methane pyrolysis, which can turn natural gas into hydrogen and carbon [72]. Sometimes, the industry may be affected by the collateral impact of disruptive technologies emerging in other industries. For example, if there is a breakthrough in battery technology, certain sectors in transportation—including heavy-duty vehicles, aviation transportation, and marine transportation, which could become customers with high hydrogen energy demands—may switch to electricity solutions instead. Hydrogen market players will have to make clear judgments and considerable efforts to remain alert and prompt in responding to any emerging disruptive technologies.

3.4.3. Heavy Investment Required to Build Hydrogen Infrastructure in China

The intensity of capital investment has always been a major concern regarding infrastructure construction in the hydrogen economy [48,71], and this challenge is worthy of extra attention, especially in China. In China, most renewable resources are located in the northern and western parts of the country, but most consumption occurs in the east [73]. Thus, either green hydrogen or green electricity transmission systems from the west to the east will be essential in building an effective green hydrogen system. However, transmitting hydrogen is much more expensive than oil or natural gas transmission networks due to hydrogen’s erosive properties, which also impose higher costs on hydrogen storage systems. When hydrogen is delivered to a city, additional distribution infrastructures, such as refilling stations, are needed to enable end-customer deliveries. All these capital thresholds will likely hinder the rapid development of the hydrogen industry in China.

4. Results: Recommended Strategies

Based on the identified SWOT factors, we can construct related strategies. Although the SWOT matrix defines four types of strategies (SO, ST, WO, and WT), some strategies can be consolidated into a more comprehensive strategy or even a business model. In this section, we will also draft business models for suitable strategies based on our SWOT analysis.

4.1. WO Strategies (Mini-Maxi)

With the trend of transitioning to a low-carbon economy, the SGCC must confront uncertainties in keeping up with its current financial performance (W3). In addition, Chinese companies in the chemical, cement, and steel industries, under direct pressure from decarbonization policies and regulations, will actively seek low-carbon alternatives, such as hydrogen, to fuel production, creating a huge growth opportunity for hydrogen (O2). Capturing the hydrogen demand from these companies could bring the SGCC a new revenue stream that could be substantial enough to help manage the uncertainties of its future profitability and mitigate other risks during the transition. Noteworthily, a large number of companies with hydrogen demands are state-owned, just as the SGCC is. State-owned companies are more connected to each other by nature, making it easier for the SGCC to gain the trust of these companies and acquire potential business opportunities, assisting in hedging the risk of revenue declines due to market reforms.

The comprehensive policy incentives from both national and local governments (O1) indicate tolerance, to some extent, for the less-organized development of hydrogen businesses at an early stage. Even if there are concerns about the emergence of possible anti-trust challenges, once the SGCC shows significant dominance in the hydrogen industry (W4), relevant policies are not likely to be introduced in the near future. Indeed, by the time anti-trust actions raise sufficient attention, the SGCC will have already established firm financial and technical foundations to maintain its strength and resilience in the hydrogen field based on first-mover advantages (O4). A hydrogen solution unit, even if it is spun off, could maintain strong competitiveness.

Based on the above analyses, despite an expected future spinoff of its hydrogen business, it is recommended that the SGCC enter the hydrogen industry, especially to meet the demands of industrial customers. Following up on this recommendation, there are a few factors the SGCC may take into strategic consideration. Since China has, evidently, more cost-effective solutions and corresponding suppliers to produce hydrogen (O3) and potentially realize other hydrogen-related applications, the SGCC may not need to go beyond its capability in building all necessary equipment from scratch (W1) or trying even harder to achieve technical leadership (W2). In fact, building up a more reliable vendor network in hydrogen production solutions should be placed in a more prioritized position in the SGCC’s hydrogen action plan.

4.2. WT Strategies (Mini-Mini)

Since the SGCC currently does not lead in the capabilities or technologies regarding any hydrogen industry sectors, including hydrogen production, storage, transportation, and utilization (W2), it would need a reliable and quickly evolving vendor network. On the one hand, the SGCC should pay extra attention to any international suppliers that may be vulnerable to geopolitical risks (T1), ensuring the long-term stability of the global supply chain. On the other hand, since new emerging technologies may disrupt the existing competitive landscape (T2), it is important for the SGCC to examine the adaptability of each vendor and to renew its vendor pool on a regular basis. In this sense, local vendors, inclusive strategic partnerships, flexible procurement contracts, and vendor support programs, may provide good strategy examples to ensure and strengthen the consistency and resilience of the supply chain network in the future.

Furthermore, the SGCC alone cannot bear the full costs required to establish a set of self-contained hydrogen infrastructures in China (T1); it should establish firm investment partnerships as well. Concerning potential financial uncertainties in the SGCC’s traditional grid business (W3) and potential anti-trust challenges to the SGCC’s future hydrogen business (W4), electricity generators could be appropriate partners. There are two key reasons for backing this partnership. The first is that, with the ongoing electricity market reform, which will improve market efficiency and boost electricity generators’ income, electricity generators will have stronger financial standings and, thus, more patience for the development of a less mature industry. The second is that, given the co-opetition relationship between electricity and hydrogen, cooperating with electricity generators could help the SGCC, as a hydrogen market player, hedge weak market demands or seek better positioning if the development of hydrogen falls short of expectations. For instance, there are debates on whether hydrogen fuel cells or electric batteries will dominate the fueling of future transportation (T2), but a partnership between hydrogen businesses and electricity generators would at least secure a position in future transportation markets. Additionally, most of the giant electricity generation companies are also state-owned and could be effectively coordinated by national or local governments. Many of them, such as the China Energy Investment Corporation, have already acquired many hydrogen-related technologies and initiated pilot projects, providing a concrete cornerstone for future partnerships.

4.3. SO Strategies (Maxi-Maxi)

Developing hydrogen solutions aligns with the SGCC’s commitment and efforts to achieve carbon neutrality (S6), but starting a new business line in the field from scratch could be a challenging task for a huge corporate such as the SGCC (W1). A more feasible approach would be developing entry strategies based on the corporation’s current technical reserves and business strengths. As a starting point, the SGCC could leverage its strength in smart grid technology (S2) and grid client coverage (S4) to further explore hydrogen applications. For instance, besides serving as an electricity storage medium, hydrogen generated in grid networks could be used by industrial companies for heating or consumed directly as a raw material by specific industries, such as steel and chemicals, accelerating the ultimate realization of their decarbonization goals (O2).

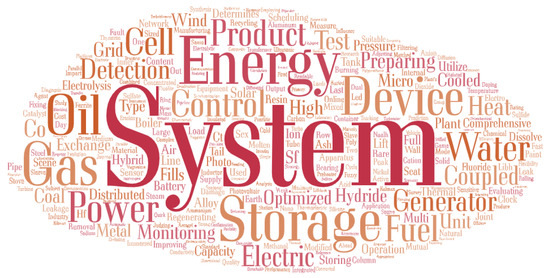

Based on its rich experience in smart grids and grid management, the SGCC could look into Energy-as-a–Service (EaaS), a popular business model that copes with the needs of professional management due to an increasing number of distributed energies, prosumers, and electric vehicles [11,16], from which hydrogen can be added to the SGCC’s service menu. Figure 7 shows the frequency of words in the titles of hydrogen-related patents from the SGCC. Among these hydrogen-related technical capabilities, the SGCC focuses more on the aspects of grid system management and device control when integrating hydrogen.

Figure 7.

Word cloud of the titles of hydrogen-related patents from the SGCC, where a larger word size represents a higher frequency in patent titles. For example, the word “system” appears 61 times.

Under the EaaS model, the SGCC could enhance its role as an energy service provider by directly acquiring the management right of micro-grids, which are built by customers themselves or the SGCC’s partners with or without the SGCC’s limited monetary involvement and charging management fees for its services for managing the micro-grids. Not only will the SGCC shift from being a CAPEX-dominant business model to an OPEX-dominant model [74], but it can also smoothly extend its energy service portfolio from electricity alone to a combination of electricity, hydrogen, and heat. Given the generally small scale of each micro-grid, compared with traditional transmission assets, EaaS will not inflict a heavy financial burden on the SGCC; it also lays the groundwork for the SGCC to strengthen its vendor network’s diversity; more importantly, EaaS companies are often more customer-oriented rather than asset-centric [74], which is crucial for building trust in promoting new services, such as hydrogen. With successful pilot experiences at local branches, the wider adoption of this model within the SGCC can proceed.

Other strengths include the SGCC’s influence on policymakers (S7) and its leadership in technical innovation (S3). The former can have a greater social impact by facilitating the development of hydrogen, and the latter may strengthen the SGCC’s technical advancement and, thus, market presence. The SGCC could easily identify and reach out to appropriate industrial customers through its large client network (S4), but it may still endure hardship in convincing customers to adopt its future hydrogen services, even if national and local governments are motivated to support the hydrogen industry (O1). Nevertheless, the SGCC could assist governments in compiling or revising relevant policies to provide more tailored incentives for the wider adoption of hydrogen solutions. Furthermore, the SGCC could accumulate technical know-how via its many ongoing projects to seize a first-mover advantage given the early stage of the industry (O4). For example, if the SGCC starts to manage many smart grids with hydrogen, it can summarize lessons and develop a new control system or platform accordingly, which, in the future, will establish a barrier to protect its market share from an over-competitive market environment.

4.4. ST Strategies (Maxi-Mini)

Within the EaaS model, the capital-intensive nature of constructing hydrogen transmission networks may place any participants in a less competitive position than other well-funded competitors (T3), but the SGCC could stand out by utilizing its knowledge of electricity transmission lines (S1) and experience in managing capital-intensive projects (S5) to optimize the planning of new hydrogen pipelines. Hydrogen pipelines and electricity transmission infrastructure could overlap in the functions of meeting certain types of end customers’ energy needs [36,37]; without careful planning, unwanted waste may be caused. To enable more optimal planning for both electricity transmission lines and hydrogen pipelines, the SGCC may consider partnerships with pipeline companies such as PipeChina, another large, state-owned enterprise focusing on the transmission of oil and natural gas in various forms. Through these partnerships, i.e., co-investments or joint ventures, both electricity transmission lines and hydrogen pipelines can be better arranged and utilized, and financial gains due to higher utilization could be shared by stakeholders. From an EaaS model perspective, investments in hydrogen transmission infrastructure serve as a form of backward integration, resulting in both cost reductions and revenue generation.

Tight involvement in policymaking and standard setting (S7) equips the SGCC with the necessary tools to prepare for amplified geopolitical uncertainties and consequential impacts on supply chain stability (T1). Active engagement in policymaking should be extended once the SGCC enters the hydrogen business, i.e., by assisting in compiling hydrogen-equipment-related trade policies. Participation in national and international policy discussions and implementation could also cause many vendors to join the ecosystem, especially technically competitive startups with limited political bargaining power.

4.5. Strategy Summary

To summarize, we recommend that the SGCC and similar grid companies consider the following strategies. Expert opinions on these four strategies are presented in Figure 8. Only the strategies with consensus are discussed and presented.

Figure 8.

Expert opinions on the four proposed strategies.

- Build a flexible hydrogen vendor network with limited international suppliers, and establish investment partnerships with electricity generation companies;

- Integrate hydrogen services into an Energy-as-a-Service (EaaS) model and deliver a more comprehensive portfolio of energy services to industrial customers;

- Create a joint venture with pipeline companies to co-optimize and co-invest in the planning and construction of electricity transmission networks and hydrogen pipelines;

- Engage in domestic policy discussions related to EaaS business models and foreign policy discussions related to the hydrogen supply chain.

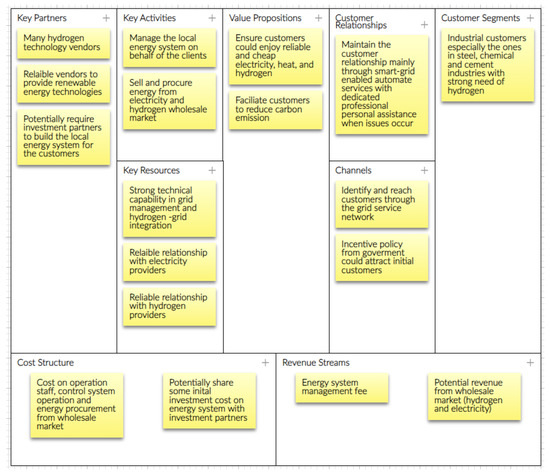

The business model for Energy-as-a-Service involving hydrogen is summarized in Figure 9. Compared with a traditional Energy-as-a-Service provider that only covers electricity and heating services, this business model focuses more on customers with stable demands for hydrogen as a raw material rather than as energy. This model also requires many hydrogen vendors with high flexibility rather than relatively stable and mature renewable vendors. This model also benefits from backward integration if the company invests in gas pipelines and electricity transmission.

Figure 9.

Summary of one potential business model for the SGCC to consider.

When investing in hydrogen energy, a key consideration is utilizing hydrogen’s advantages to store excessive electric energy, thus improving grid management and deferring a proportion of the investment in transmission infrastructure. However, the current low efficiency of electricity–hydrogen–electricity systems makes them less competitive in comparison with other electric energy storage systems. A potential advantage of hydrogen storage systems in grid management is that they can be used to generate and sell hydrogen. In the SGCC’s case, if the hydrogen generated during grid management is directly sold to end customers, the whole process will fall under the umbrella of the Energy-as-a-Service model described above; if the hydrogen is sold to market-makers or other participants, the idea is likely to face the anti-trust risk noted above, as we expect that grid utilities may not participate in the energy generation business (W4).

5. Discussion

The global hydrogen industry is still at an early development stage, but it has the power to reshape the landscape of renewables, and grid utilities are eagerly seeking new growth opportunities. Using a strategy analysis in this case study, we successfully brought up a suitable and promising strategy that could possibly navigate grid utilities to enter the hydrogen industry. The State Grid of China, one of the biggest grid utilities in the world, has already started to take action to engage in the hydrogen field, and this could provide significant references for the SGCC’s peers around the world.

The SGCC is gradually building its influence, networks, and other foundations needed to succeed in the field. By initiating an increasing number of pilot projects, the SGCC not only accumulates many hands-on project credentials but also builds a reliable network of both vendors and partners. For instance, in 2022, the SGCC built megawatt-scale hydrogen–wind–solar microgrid system with the Mingtian Hydrogen Energy Technology Company, a fuel cell startup, and the Dalian Institute of Chemical Physics, a subsidiary of the Chinese Academy of Science; in Cixi, Zhejiang, the SGCC also collaborated with the Ningbo Lvdong Fuel Cell company, a startup backed by the State Power Investment Corporation, to begin another pilot hydrogen microgrid project. In addition, following its digital transition strategy, the SGCC has explored the Energy-as-a-Service model [55], which could quickly integrate hydrogen services into a full-service menu once ready. In fact, in 2020, the State Grid Integrated Energy Service Group, a subsidiary of the SGCC, was established to undertake tasks related to Energy-as-a-Service, grid management, and the Internet of things.

There are also tasks the SGCC could start paying attention to. One is partnerships with pipeline companies, whose importance to grid utilities will gradually be shown. PipeChina and PetroChina now lead the development of hydrogen pipelines in China, and they will likely start to consider co-planning hydrogen and electricity transmission systems to reach the most optimal configuration if hydrogen transmission technology starts to mature. Another is involvement in policymaking, creating a more favorable setting for global grid utilities. There are many gaps in policies and regulations waiting to be filled, both domestically and globally, to construct a functional hydrogen service environment for grid utilities. For example, there are incentive policies imposed by both national and regional governments in China that subsidize EaaS providers, yet there are insufficient regulatory policies to follow up with operational outcomes and protect end customer interests; globally, rules, regulations, and standards on the hydrogen supply chain are still lagging in terms of progress.

The SGCC’s lessons could be applied to other grid companies around the world. These recommended strategies, if successfully implemented, could illustrate a feasible path for integrating hydrogen into an EaaS business model for other grid utilities. In other words, since most grid utility companies possess huge customer populations in carbon-intensive industries and have abundant experience in grid management, they can leverage these strengths, together with other technical and investment partners, to promote hydrogen services in a more timely and less risky manner. Grid utilities that engage in businesses other than electricity transmission and distribution could adjust the recommended strategies accordingly to realize their business goals. For example, British Gas, which offers both gas and electricity to customers, does not need to partner with additional gas suppliers to establish an Energy-as-a-Service business. Additionally in the UK, because the Office of Gas and Electricity Markets (Ofgem) regulates both gas and electricity, it has experience in optimizing the configuration of electricity and gas transmissions, providing a mature methodology for managing hydrogen transmissions. Vertically integrated grid utilities that own generator assets could also consider entering the green hydrogen production business, which could potentially improve the financial status of their assets with a high curtailment rate.

There are also a few limitations in this study. The first is the relatively small size of the expert group, leading to the possibly insufficient representation of all market participants. In the future, we would prefer to conduct a wider range of surveys to enable a more comprehensive assessment. Another relevant challenge is the absence of a hydrogen pipeline company in the expert group. Collaboration with pipeline companies is a recommended strategy based on the analyses, but this has not yet been validated by experts from the corresponding companies. Furthermore, the strategies discussed above may be applied by large or giant grid utilities, especially those similar to the SGCC, but they may not share the same reference value for small- and medium-sized companies. It would be helpful to tailor strategies suitable for smaller companies in future studies. Last but not least, as a strategic analysis, our study has not touched on the quantitative assessment aspects of the proposed business model’s financial feasibility. If pilot projects accumulate sufficient data, a more quantitative analysis could be conducted to validate the proposed business model.

Future studies may be inspired by these limitations to further explore the business model for grid utilities in the hydrogen economy. The low-hanging fruit for improvement may be greater involvement from different stakeholders. As mentioned above, the next batch of interviews should expand the number of interviewees, including more small grid companies, pipeline companies, and governments. Future studies may also design a well-formulated questionnaire with a rating scheme to make the analysis more quantitative.

Author Contributions

Conceptualization, D.X. and R.S.; methodology, R.S. and H.W.; validation, D.X. and Z.L.; formal analysis, D.X., Z.L. and R.S.; writing—original draft preparation, D.X., Z.L. and R.S.; writing—review and editing, H.W. and H.Z. All authors have read and agreed to the published version of the manuscript.

Funding

Authors appreciate the funding from the Science and Technology Innovation Program of the State Grid Zhejiang Electric Power Company (No. B311JZ220003).

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki, and approved by the Ethics Committee of Carbon Baseline (protocol code ECCB22001 and date of approval is 28 June 2022).

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

The authors thank Yi Han, Yijiing Xin, and Linkun Ji for their help in organizing interviews and data collection. The authors also thank the interviewees for their valuable insights.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Summary of national policies supporting hydrogen development in China.

References

- Masson-Delmotte, V.; Zhai, P.; Pörtner, H.-O.; Roberts, D.; Skea, J.; Shukla, P.R.; Pirani, A.; Moufouma-Okia, W.; Péan, C.; Pidcock, R. Global Warming of 1.5 °C: An IPCC Special Report on the Impacts of Global Warming of 1.5° C Above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change; World Meteorological Organization: Geneva, Switzerland, 2018. [Google Scholar]

- Hino, M.; Belanger, S.T.; Field, C.B.; Davies, A.R.; Mach, K.J. High-Tide Flooding Disrupts Local Economic Activity. Sci. Adv. 2019, 5. [Google Scholar] [CrossRef] [PubMed]

- Liu, J.; Hertel, T.W.; Diffenbaugh, N.S.; Delgado, M.S.; Ashfaq, M. Future Property Damage from Flooding: Sensitivities to Economy and Climate Change. Clim. Change 2015, 132, 741–749. [Google Scholar] [CrossRef]

- Vicedo-Cabrera, A.M.; Scovronick, N.; Sera, F.; Royé, D.; Schneider, R.; Tobias, A.; Astrom, C.; Guo, Y.; Honda, Y.; Hondula, D.M.; et al. The Burden of Heat-Related Mortality Attributable to Recent Human-Induced Climate Change. Nat. Clim. Change 2021, 11, 492–500. [Google Scholar] [CrossRef] [PubMed]

- Ebi, K.L.; Vanos, J.; Baldwin, J.W.; Bell, J.E.; Hondula, D.M.; Errett, N.A.; Hayes, K.; Reid, C.E.; Saha, S.; Spector, J.; et al. Extreme Weather and Climate Change: Population Health and Health System Implications. Annu. Rev. Public Health 2021, 42, 293–315. [Google Scholar] [CrossRef]

- Friedlingstein, P.; O’Sullivan, M.; Jones, M.W.; Andrew, R.M.; Hauck, J.; Olsen, A.; Peters, G.P.; Peters, W.; Pongratz, J.; Sitch, S.; et al. Global Carbon Budget 2020. Earth Syst. Sci. Data 2020, 12, 3269–3340. [Google Scholar] [CrossRef]

- Akimoto, K.; Sano, F.; Homma, T.; Oda, J.; Nagashima, M.; Kii, M. Estimates of GHG Emission Reduction Potential by Country, Sector, and Cost. Energy Policy 2010, 38, 3384–3393. [Google Scholar] [CrossRef]

- He, G.; Lin, J.; Sifuentes, F.; Liu, X.; Abhyankar, N.; Phadke, A. Rapid Cost Decrease of Renewables and Storage Accelerates the Decarbonization of China’s Power System. Nat. Commun. 2020, 11, 2486. [Google Scholar] [CrossRef]

- Gowrisankaran, G.; Reynolds, S.S.; Samano, M. Intermittency and the Value of Renewable Energy. J. Political Econ. 2016, 124, 1187–1234. [Google Scholar] [CrossRef]

- Frew, B.; Sergi, B.; Denholm, P.; Cole, W.; Gates, N.; Levie, D.; Margolis, R. The Curtailment Paradox in the Transition to High Solar Power Systems. Joule 2021, 5, 1143–1167. [Google Scholar] [CrossRef]

- Bryant, S.T.; Straker, K.; Wrigley, C. The Typologies of Power: Energy Utility Business Models in an Increasingly Renewable Sector. J. Clean Prod. 2018, 195, 1032–1046. [Google Scholar] [CrossRef]

- Mazur, C.; Hall, S.; Hardy, J.; Workman, M. Technology Is Not a Barrier: A Survey of Energy System Technologies Required for Innovative Electricity Business Models Driving the Low Carbon Energy Revolution. Energies 2019, 12, 428. [Google Scholar] [CrossRef]

- Bichler, M.; Buhl, H.U.; Knörr, J.; Maldonado, F.; Schott, P.; Waldherr, S.; Weibelzahl, M. Electricity Markets in a Time of Change: A Call to Arms for Business Research. Schmalenbach J. Bus. Res. 2022, 74, 77–102. [Google Scholar] [CrossRef]

- Kopin, D.J.; vanden Bergh, R.G. The Rationale for Reforming Utility Business Models. Energy J. 2023, 44. [Google Scholar] [CrossRef]

- Hall, S.; Mazur, C.; Hardy, J.; Workman, M.; Powell, M. Prioritising Business Model Innovation: What Needs to Change in the United Kingdom Energy System to Grow Low Carbon Entrepreneurship? Energy Res. Soc. Sci. 2020, 60, 101317. [Google Scholar] [CrossRef]

- Richter, M. Business Model Innovation for Sustainable Energy: German Utilities and Renewable Energy. Energy Policy 2013, 62, 1226–1237. [Google Scholar] [CrossRef]

- Maciejowska, K. Assessing the Impact of Renewable Energy Sources on the Electricity Price Level and Variability—A Quantile Regression Approach. Energy Econ. 2020, 85, 104532. [Google Scholar] [CrossRef]

- Fares, R.L.; Webber, M.E. The Impacts of Storing Solar Energy in the Home to Reduce Reliance on the Utility. Nat. Energy 2017, 2, 17001. [Google Scholar] [CrossRef]

- Brockway, A.M.; Conde, J.; Callaway, D. Inequitable Access to Distributed Energy Resources Due to Grid Infrastructure Limits in California. Nat. Energy 2021, 6, 892–903. [Google Scholar] [CrossRef]

- Luburić, Z.; Pandžić, H.; Plavšić, T.; Teklić, L.; Valentić, V. Role of Energy Storage in Ensuring Transmission System Adequacy and Security. Energy 2018, 156, 229–239. [Google Scholar] [CrossRef]

- Alova, G. A Global Analysis of the Progress and Failure of Electric Utilities to Adapt Their Portfolios of Power-Generation Assets to the Energy Transition. Nat. Energy 2020, 5, 920–927. [Google Scholar] [CrossRef]

- Pereira, G.I.; Niesten, E.; Pinkse, J. Sustainable Energy Systems in the Making: A Study on Business Model Adaptation in Incumbent Utilities. Technol. Soc. Change 2022, 174, 121207. [Google Scholar] [CrossRef]

- Necoechea-Porras, P.D.; López, A.; Salazar-Elena, J.C. Deregulation in the Energy Sector and Its Economic Effects on the Power Sector: A Literature Review. Sustainability 2021, 13, 3429. [Google Scholar] [CrossRef]

- Anaya, K.L.; Pollitt, M.G. Going Smarter in the Connection of Distributed Generation. Energy Policy 2017, 105, 608–617. [Google Scholar] [CrossRef]

- Horváth, D.; Szabó, R.Z. Evolution of Photovoltaic Business Models: Overcoming the Main Barriers of Distributed Energy Deployment. Renew. Sustain. Energy Rev. 2018, 90, 623–635. [Google Scholar] [CrossRef]

- Hiteva, R.; Foxon, T.J. Beware the Value Gap: Creating Value for Users and for the System through Innovation in Digital Energy Services Business Models. Technol. Soc. Change 2021, 166, 120525. [Google Scholar] [CrossRef]

- Shomali, A.; Pinkse, J. The Consequences of Smart Grids for the Business Model of Electricity Firms. J. Clean. Prod. 2016, 112, 3830–3841. [Google Scholar] [CrossRef]

- Lin, R.H.; Zhao, Y.Y.; Wu, B.D. Toward a Hydrogen Society: Hydrogen and Smart Grid Integration. Int. J. Hydrogen Energy 2020, 45, 20164–20175. [Google Scholar] [CrossRef]

- Bellosta von Colbe, J.; Ares, J.R.; Barale, J.; Baricco, M.; Buckley, C.; Capurso, G.; Gallandat, N.; Grant, D.M.; Guzik, M.N.; Jacob, I.; et al. Application of Hydrides in Hydrogen Storage and Compression: Achievements, Outlook and Perspectives. Int. J. Hydrogen Energy 2019, 44, 7780–7808. [Google Scholar] [CrossRef]

- Valverde, L.; Rosa, F.; Bordons, C.; Guerra, J. Energy Management Strategies in Hydrogen Smart-Grids: A Laboratory Experience. Int. J. Hydrogen Energy 2016, 41, 13715–13725. [Google Scholar] [CrossRef]

- Petrollese, M.; Valverde, L.; Cocco, D.; Cau, G.; Guerra, J. Real-Time Integration of Optimal Generation Scheduling with MPC for the Energy Management of a Renewable Hydrogen-Based Microgrid. Appl. Energy 2016, 166, 96–106. [Google Scholar] [CrossRef]

- Alavi, F.; Park Lee, E.; van de Wouw, N.; de Schutter, B.; Lukszo, Z. Fuel Cell Cars in a Microgrid for Synergies between Hydrogen and Electricity Networks. Appl. Energy 2017, 192, 296–304. [Google Scholar] [CrossRef]

- Bernstein, P.A.; Heuer, M.; Wenske, M. Fuel Cell System as a Part of the Smart Grid. In Proceedings of the 2013 IEEE Grenoble Conference PowerTech, POWERTECH 2013, Grenoble, France, 16–20 June 2013. [Google Scholar] [CrossRef]

- Semeraro, M.A. Renewable Energy Transport via Hydrogen Pipelines and HVDC Transmission Lines. Energy Strategy Rev. 2021, 35, 100658. [Google Scholar] [CrossRef]

- Patel, M.; Roy, S.; Roskilly, A.P.; Smallbone, A. The Techno-Economics Potential of Hydrogen Interconnectors for Electrical Energy Transmission and Storage. J. Clean. Prod. 2022, 335, 130045. [Google Scholar] [CrossRef]

- Wu, W.P.; Wu, K.X.; Zeng, W.K.; Yang, P.C. Optimization of Long-Distance and Large-Scale Transmission of Renewable Hydrogen in China: Pipelines vs. UHV. Int. J. Hydrogen Energy 2022, 47, 24635–24650. [Google Scholar] [CrossRef]

- Van der Zwaan, B.; Lamboo, S.; Dalla Longa, F. Timmermans’ Dream: An Electricity and Hydrogen Partnership between Europe and North Africa. Energy Policy 2021, 159, 112613. [Google Scholar] [CrossRef]

- Hill, T.; Westbrook, R. SWOT Analysis: It’s Time for a Product Recall. Long Range Plann. 1997, 30, 46–52. [Google Scholar] [CrossRef]

- Weihrich, H. The TOWS Matrix—A Tool for Situational Analysis. Long Range Plann. 1982, 15, 54–66. [Google Scholar] [CrossRef]

- Grundy, T. Rethinking and Reinventing Michael Porter’s Five Forces Model. Strateg. Change 2006, 15, 213–229. [Google Scholar] [CrossRef]

- Kutlu Gündoğdu, F.; Kahraman, C. A Novel Spherical Fuzzy Analytic Hierarchy Process and Its Renewable Energy Application. Soft Comput. 2020, 24, 4607–4621. [Google Scholar] [CrossRef]

- Phadermrod, B.; Crowder, R.M.; Wills, G.B. Importance-Performance Analysis Based SWOT Analysis. Int. J. Inf. Manag. 2019, 44, 194–203. [Google Scholar] [CrossRef]

- Madurai Elavarasan, R.; Afridhis, S.; Vijayaraghavan, R.R.; Subramaniam, U.; Nurunnabi, M. SWOT Analysis: A Framework for Comprehensive Evaluation of Drivers and Barriers for Renewable Energy Development in Significant Countries. Energy Rep. 2020, 6, 1838–1864. [Google Scholar] [CrossRef]

- Irfan, M.; Hao, Y.; Panjwani, M.K.; Khan, D.; Chandio, A.A.; Li, H. Competitive Assessment of South Asia’s Wind Power Industry: SWOT Analysis and Value Chain Combined Model. Energy Strategy Rev. 2020, 32, 100540. [Google Scholar] [CrossRef]

- Sibtain, M.; Li, X.; Bashir, H.; Azam, M.I. Hydropower Exploitation for Pakistan’s Sustainable Development: A SWOT Analysis Considering Current Situation, Challenges, and Prospects. Energy Strategy Rev. 2021, 38, 100728. [Google Scholar] [CrossRef]

- Agyekum, E.B.; Ansah, M.N.S.; Afornu, K.B. Nuclear Energy for Sustainable Development: SWOT Analysis on Ghana’s Nuclear Agenda. Energy Rep. 2020, 6, 107–115. [Google Scholar] [CrossRef]

- Ren, J.; Gao, S.; Tan, S.; Dong, L. Hydrogen Economy in China: Strengths–Weaknesses–Opportunities–Threats Analysis and Strategies Prioritization. Renew. Sustain. Energy Rev. 2015, 41, 1230–1243. [Google Scholar] [CrossRef]

- Li, Y.; Shi, X.; Phoumin, H. A Strategic Roadmap for Large-Scale Green Hydrogen Demonstration and Commercialisation in China: A Review and Survey Analysis. Int. J. Hydrogen Energy 2022, 47, 24592–24609. [Google Scholar] [CrossRef]

- National Development and Reform Commission. Organizing the Grid Companies to Purchase Electricity on Behalf of End Customers; National Development and Reform Commission: Beijing, China, 2021.

- Dai, R.; Liu, G.; Zhang, X. Transmission Technologies and Implementations: Building a Stronger, Smarter Power Grid in China. IEEE Power Energy Mag. 2020, 18, 53–59. [Google Scholar] [CrossRef]

- Geng, J.; Du, W.; Yang, D.; Chen, Y.; Liu, G.; Fu, J.; He, G.; Wang, J.; Chen, H. Construction of Energy Internet Technology Architecture Based on General System Structure Theory. Energy Rep. 2021, 7, 10–17. [Google Scholar] [CrossRef]

- Wang, Y.; Ruan, D.; Gu, D.; Gao, J.; Liu, D.; Xu, J.; Chen, F.; Dai, F.; Yang, J. Analysis of Smart Grid Security Standards. In Proceedings of the 2011 IEEE International Conference on Computer Science and Automation Engineering, CSAE 2011, Shanghai, China, 10–12 June 2011; Volume 4, pp. 697–701. [Google Scholar] [CrossRef]

- Ngar-yin Mah, D.; Wu, Y.Y.; Ronald Hills, P. Explaining the Role of Incumbent Utilities in Sustainable Energy Transitions: A Case Study of the Smart Grid Development in China. Energy Policy 2017, 109, 794–806. [Google Scholar] [CrossRef]

- Rikap, C. Becoming an Intellectual Monopoly by Relying on the National Innovation System: The State Grid Corporation of China’s Experience. Res. Policy 2022, 51, 104472. [Google Scholar] [CrossRef]

- State Grid Corporation of China. State Grid Corporation of China 2021 Annual Report; State Grid Corporation of China: Beijing, China, 2022. [Google Scholar]

- State Grid Corporation of China. 2021 Corporate Social Responsibility Report of State Grid Corporation of China; State Grid Corporation of China: Beijing, China, 2022. [Google Scholar]

- Pan, E.; Liu, S.; Liu, J.; Qi, Q.; Guo, Z. The State Grid Corporation of China’s Practice and Outlook for Promoting New Energy Development. Energy Convers. Econ. 2020, 1, 71–80. [Google Scholar] [CrossRef]

- Yi-chong, X. China’s Giant State-Owned Enterprises as Policy Advocates: The Case of the State Grid Corporation of China. China J. 2018, 79, 21–39. [Google Scholar] [CrossRef]

- Pollitt, M.G. Measuring the Impact of Electricity Market Reform in a Chinese Context. Energy Clim. Change 2021, 2, 100044. [Google Scholar] [CrossRef]

- National Development and Reform Commission; National Energy Administration. Guidance about Accelerating National Electricity Market; National Development and Reform Commission, National Energy Administration: Beijing, China, 2022.

- National Development and Reform Commission; National Energy Administration. Hydrogen Energy Development Plan 2021-2035; National Development and Reform Commission, National Energy Administration: Beijing, China, 2022.

- Li, C.; Zhang, L.; Ou, Z.; Ma, J. Using System Dynamics to Evaluate the Impact of Subsidy Policies on Green Hydrogen Industry in China. Energy Policy 2022, 165, 112981. [Google Scholar] [CrossRef]

- H2in-EN.com 14 Provinces Have Published Support Policy for Hydrogen Development. Available online: https://h2.in-en.com/html/h2-2411271.shtml (accessed on 13 October 2022).

- Fan, J.L.; Wang, Q.; Yang, L.; Zhang, H.; Zhang, X. Determinant Changes of Consumer Preference for NEVs in China: A Comparison between 2012 and 2017. Int. J. Hydrogen Energy 2020, 45, 23557–23575. [Google Scholar] [CrossRef]

- Hydrogen Council; McKinsey & Company. Hydrogen Insight 2022; McKinsey & Company: New York, NY, USA, 2022. [Google Scholar]

- China Hydrogen Alliance. China Hydrogen and Fuel Cell Industry White Paper (2020); China Hydrogen Alliance: Beijing, China, 2021. [Google Scholar]

- Song, S.; Lin, H.; Sherman, P.; Yang, X.; Nielsen, C.P.; Chen, X.; McElroy, M.B. Production of Hydrogen from Offshore Wind in China and Cost-Competitive Supply to Japan. Nat. Commun. 2021, 12, 6953. [Google Scholar] [CrossRef]

- China Leading Race to Make Technology Vital for Green Hydrogen—Bloomberg. Available online: https://www.bloomberg.com/news/articles/2022-09-21/china-leading-race-to-make-technology-vital-for-green-hydrogen?leadSource=uverify%20wall (accessed on 13 October 2022).

- IRENA. Renewable Power Generation Costs in 2021; IRENA: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- Peltoniemi, M. Reviewing Industry Life-Cycle Theory: Avenues for Future Research. Int. J. Manag. Rev. 2011, 13, 349–375. [Google Scholar] [CrossRef]

- Ren, X.; Dong, L.; Xu, D.; Hu, B. Challenges towards Hydrogen Economy in China. Int. J. Hydrogen Energy 2020, 45, 34326–34345. [Google Scholar] [CrossRef]

- Sánchez-Bastardo, N.; Schlögl, R.; Ruland, H. Methane Pyrolysis for Zero-Emission Hydrogen Production: A Potential Bridge Technology from Fossil Fuels to a Renewable and Sustainable Hydrogen Economy. Ind. Eng. Chem. Res. 2021, 60, 11855–11881. [Google Scholar] [CrossRef]

- Li, M.; Virguez, E.; Shan, R.; Tian, J.; Gao, S.; Patiño-Echeverri, D. High-Resolution Data Shows China’s Wind and Solar Energy Resources Are Enough to Support a 2050 Decarbonized Electricity System. Appl. Energy 2022, 306, 117996. [Google Scholar] [CrossRef]

- Helms, T. Asset Transformation and the Challenges to Servitize a Utility Business Model. Energy Policy 2016, 91, 98–112. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).