Abstract

Governments worldwide are mandating digital tax platforms, yet little is understood about what sustains taxpayer engagement beyond legally compelled minimum use. This study extends the Technology Acceptance Model (TAM) with perceived compulsion and tax literacy to examine continuous usage intention toward Coretax, Indonesia’s mandatory Core Tax Administration System. Using survey data from 535 active users analysed with PLS-SEM, six of eight hypotheses are supported: system quality drives perceived ease of use, which amplifies perceived usefulness, and both usefulness and user satisfaction independently predict continuous usage intention. Contrary to predictions derived from self-determination theory, perceived compulsion positively influences satisfaction, suggesting institutional acceptance of a mandate redirects evaluative attention toward system performance rather than generating resistance. Tax literacy does not moderate the usefulness–continuance pathway but independently increases engagement intentions, pointing to literacy programmes as direct engagement levers rather than amplifiers. These findings extend TAM into mandatory post-adoption contexts and propose institutional acceptance as a boundary condition for coercion theory in IS research.

1. Introduction

Digital transformation in public administration has fundamentally altered how governments provide services and how citizens fulfil their civic responsibilities. Among the most consequential of these shifts is the move towards obligatory digital tax systems, in which compliance is not merely encouraged but enforced by law through built-in government platforms. Indonesia’s shift to Coretax represents one of the most comprehensive mandatory tax digitisation reforms in the developing world. It parallels—and in scope surpasses—the mandatory electronic reporting frameworks that European Union (EU) member states have progressively implemented over two decades, including e-filing mandates, e-invoicing requirements, and Standard Audit File for Tax (SAF-T) reporting obligations [1,2]. Where European implementations have typically proceeded incrementally across distinct tax functions and administrative jurisdictions, Coretax consolidates all Indonesian tax obligations into a single unified platform in a single operational transition—a design and implementation ambition that is distinctive even by international standards. Launched on 31 December 2024 and fully operational from January 2025, under Ministry of Finance Regulation No. 81 of 2024, Coretax replaced dozens of fragmented legacy systems with a unified platform covering taxpayer registration, return filing, payment processing, and account management [3]. With Coretax serving as the permanent infrastructure for all Indonesian tax administration and early evaluations indicating that taxpayer perceptions of system quality during the initial rollout carry significant practical consequences, the question of how taxpayers engage with the platform beyond the legal minimum is both timely and practically urgent [3,4].

Coretax represents a fundamental architectural departure from the fragmented legacy infrastructure it replaced, which comprised more than two dozen separate platforms—each handling distinct functions such as income tax filing, Value-Added Tax (VAT) reporting, and payment processing through disconnected interfaces—now unified under one login and one data architecture [3,4]. Key design features include real-time data validation at the point of submission, automated pre-population of return fields from third-party data sources, and direct integration with the Indonesian banking system for seamless payment processing—capabilities absent from the legacy e-filing system. The anticipated advantages are substantial: reduced compliance costs for taxpayers, improved audit trail integrity for the Directorate General of Taxes (DJP), and a projected 1.5% increase in Indonesia’s tax-to-Gross Domestic Product (GDP) ratio as informal transactions become harder to conceal within an integrated data environment [3]. These advantages, however, have not been uniformly realised in the platform’s first year. Early operational reports documented significant system instability during peak filing periods, with taxpayers and tax professionals reporting slow response times, login failures, and inconsistent output validation [4]. These shortcomings are not incidental: they establish precisely why understanding the determinants of taxpayer satisfaction and continuous engagement with Coretax is both practically urgent and theoretically non-trivial. A system whose technical performance is uneven at launch, and whose users have no legally permissible alternative, creates a natural testing ground for the quality-adoption dynamics this study examines.

Academic interest in digital tax system adoption has accumulated over two decades, with TAM [5,6] establishing perceived usefulness and perceived ease of use as the dominant predictors of adoption across institutional settings, a finding extended to digital tax and e-government services by [7,8,9]. In the Indonesian context, ref. Saptono et al. [10]’s findings indicate that service quality and reduced compliance costs are the main factors that foster user satisfaction with e-filing, which, in turn, mediates tax compliance intention. Most recently, ref. Saptono et al. [4] provided an early evaluation of Coretax itself, finding that tax professionals report negative perceptions of system quality in the initial rollout—a signal that understanding sustained engagement with this platform is both timely and practically urgent. Similarly, ref. Ariyanto et al. [11], using ref. DeLone & McLean [12]’s IS success model on MSMEs in Indonesia, confirmed that the key antecedents of taxpayer compliance behaviour are system quality and user satisfaction. Ref. Abu-Silake et al. [13], examining digital tax platform usage in Jordan, found consistent cross-national support for TAM’s core constructs in tax compliance settings. Mandatory digital tax administration is increasingly a global phenomenon: EU member states have implemented e-invoicing mandates, SAF-T reporting requirements, and real-time transaction reporting systems that share the compulsory engagement logic of Coretax, though the institutional, regulatory, and technological contexts differ substantially from the Indonesian setting [1,2]. Understanding how taxpayer adoption dynamics operate under legal compulsion—and whether the institutional acceptance mechanism identified here generalises beyond Indonesia—represents a research agenda of direct relevance to tax authorities worldwide.

The existing literature on digital tax Information-System (IS) adoption has established TAM’s core constructs as reliable predictors across voluntary and semi-voluntary settings, confirmed system quality as the foundational upstream driver of ease of use and usefulness, and identified user satisfaction as the proximal antecedent of continuous usage intention [5,6,9,10,14]. What remains unexamined is whether these relationships hold—and whether they operate through the same mechanisms—when adoption is not a choice but a legal requirement.

Yet, despite this body of work, three important gaps exist. First, the existing literature is almost exclusively based on voluntary or semi-voluntary adoption scenarios—situations in which users have some real choice about how deeply they engage. Coretax is categorically different. Use is legally mandated, non-compliance carries statutory penalties, and the government has committed to the platform as the permanent infrastructure for all Indonesian tax administration. The psychological dynamics of legally compelled IS use—where perceived compulsion operates independently of any cognitive assessment of the system itself—introduce a construct that standard TAM frameworks simply do not account for [15,16,17]. No published study has examined this in the Coretax context. Beyond the construct-level gap, the existing literature has not examined how the organisational challenges inherent in large-scale government IS rollouts—implementation instability, uneven technical readiness, and the absence of exit options—shape the quality-adoption relationship in mandatory settings. This gap is addressed directly through the Coretax deployment context [2,18].

Second, prior research has predominantly treated initial adoption or behavioural intention to use as the primary dependent variable. In a mandatory deployment where first use is legally guaranteed, this outcome carries limited analytical weight. The more relevant issue is whether taxpayers engage with the system genuinely and continuously, or merely comply at the minimum level of compulsion required. Continuous usage intention—distinguished from legally enforced behaviour—is the theoretically appropriate and practically meaningful outcome to examine here.

Third, while tax literacy has been identified as an important individual-level characteristic in tax compliance research, no study has tested whether it moderates the relationship between perceived usefulness and continuous usage intention within a mandatory IS setting. This is a gap with direct implications for how tax authorities should design support and training programmes.

The novelty of this study sits at the intersection of these three gaps. To the best of the authors’ knowledge, this study is among the first empirical attempts to apply a TAM-based framework, extended with perceived compulsion as an exogenous mandatory-context construct, to Indonesia’s Coretax platform. It also contributes to the emerging global literature on nationally mandated IS deployment by examining how legal coercion interacts with cognitive system evaluations and user satisfaction in shaping continuous usage intention. Prior mandatory IS studies have largely examined compulsion as a constraint on voluntary adoption decisions rather than as an independent construct operating within a post-adoption continuous usage framework, a distinction that matters because sustained engagement under legal obligation may involve different psychological dynamics from initial adoption resistance [15,16]. By introducing perceived compulsion into a post-adoption TAM, this study provides a rare empirical test as to whether institutional acceptance modifies the coercion-resistance prediction derived from the Self-Determination Theory (SDT) when continuous usage intention, rather than initial adoption, is the outcome of interest. The study also examines tax literacy as a potential moderator of the perceived usefulness–continuous usage intention relationship, a pathway that remains underexplored in mandatory IS and digital tax research.

Three research objectives guide this study: to examine how system quality, perceived ease of use, and perceived usefulness shape user satisfaction and continuous usage intention; to assess whether perceived compulsion affects user satisfaction independently of cognitive system evaluations; and to test whether tax literacy moderates the perceived usefulness–continuous usage intention relationship.

These are operationalised through three research questions:

- RQ1.

- How do system quality, perceived ease of use, and perceived usefulness influence user satisfaction and continuous usage intention toward Coretax?

- RQ2.

- Does perceived compulsion exert a significant effect on user satisfaction, independently of cognitive system evaluations?

- RQ3.

- Does tax literacy moderate the relationship between perceived usefulness and continuous usage intention in a mandatory IS context?

2. Literature Review and Hypothesis Development

2.1. Theoretical Framework: The Technology Acceptance Model

This study is theoretically anchored in the Technology Acceptance Model (TAM), whose intellectual progression provides the analytical scaffolding for the present investigation. Ref. Davis [5] proposed that perceived usefulness and perceived ease of use are the primary determinants of technology adoption intentions, with ease of use exerting both a direct effect on intention and an indirect effect channelled through usefulness. Ref. Venkatesh & Davis [19] extended this framework by theorising that social influence and cognitive instrumental processes determine perceived usefulness. Ref. Venkatesh & Bala [20] advanced it further through TAM3, identifying system and interface quality characteristics as critical determinants of perceived ease of use—establishing the upstream antecedent pathway this study operationalises through the System Quality → Perceived Ease of Use chain.

More recent scholarship has extended TAM into digital transformation contexts. Ref. Eom & Lee [2] document that large-scale government IS deployments generate organisational and institutional challenges—workforce adaptation, governance alignment, and managing platform unintended consequences—that shape whether citizens can engage productively with new systems. Ref. Mergel et al. [21] show that performance variability at rollout shapes lasting attitudinal responses, and ref. Syed et al. [18] identify TAM’s upstream quality chain as the critical mediating pathway between implementation quality and citizen adoption in developing country government IS. This study applies that chain within precisely such a context—a nationally mandated platform whose implementation challenges were publicly documented during its first operational year [9].

Cultural and social factors are particularly salient here. Indonesia’s compliance culture is shaped by collectivist norms and high-power distance—characteristics [22] identified as conducive to the acceptance of institutionally imposed obligations rather than resistance. In high power distance societies, government mandates are more readily accepted as legitimate institutional authority rather than as violations of autonomy, creating a cultural predisposition toward institutional acceptance that SDT’s individualist framework does not account for. Ref. Syed et al. [18] further note that developing-country contexts introduce institutional trust asymmetries that produce adoption dynamics qualitatively different from those in high-income settings—conditions not controlled for in the present model but that represent plausible moderators for future cross-national research.

Beyond system-level evaluations, the broader public administration literature highlights a dimension this study does not directly model: the relationship between digital tax platform experiences and taxpayers’ attitudes toward the tax process. Tax morale research establishes that intrinsic compliance motivation is sensitive to institutional signals—including the quality and fairness of administrative processes through which obligations are discharged [10,11]. A mandatory IS that is technically unreliable or experienced as imposing may not only reduce satisfaction but erode tax morale by signalling institutional indifference to the compliance burden, while a well-functioning platform may strengthen the citizen-state relationship by demonstrating reciprocal service investment. The present study examines taxpayers as IS users evaluating a platform; future research should examine them as citizens in a public service relationship, connecting platform adoption outcomes to tax morale, procedural fairness, and institutional trust as downstream consequences of the quality-adoption dynamics documented here.

Applying this to Coretax, this study extends TAM into the post-adoption stage [23], where the theoretically meaningful outcome is continuous usage intention—taxpayers’ genuine commitment to sustained engagement beyond the legally mandated minimum. TAM provides not merely a measurement template but a causal structure within which system quality, ease of use, usefulness, satisfaction, and behavioural persistence can be systematically investigated. In the Coretax context, this architecture maps directly onto the DJP’s operational priorities: system quality investments compound into ease-of-use gains, which, alongside satisfaction, determine whether taxpayers engage genuinely or merely at the statutory minimum.

2.2. Hypothesis Development

2.2.1. System Quality on Perceived Ease of Use

Addressing Gap 1 and RQ1, H1–H4 operationalise TAM’s upstream quality chain within the mandatory Coretax context, testing whether system quality, ease of use, and usefulness drive satisfaction and continuous usage intention when adoption is legally compelled rather than voluntary. System quality captures how well an information system performs technically—its reliability, speed, and the coherence of its interface structure [12,14]. A system that loads quickly, behaves predictably, and organises its functions logically reduces the mental effort users must invest before completing their actual tasks [5,14,19]. Government IS research has consistently shown this technical-to-cognitive link holds even where use is non-negotiable [24,25,26], and since Indonesian taxpayers have no legally permissible alternative to Coretax, any drop in technical performance cannot be offset by switching channels, making ease-of-use perceptions unusually sensitive to system quality here [9,11].

It is worth noting that system quality in IS research also encompasses data security and privacy protection—dimensions particularly salient in mandatory government IS contexts where sensitive financial data flows through a centralised platform, and users cannot opt out [4,12]. European mandatory reporting contexts have documented security concerns as significant adoption barriers [1,2]. The present study operationalises system quality through reliability, response time, navigation, and functional performance—dimensions most directly linked to compliance task experience—but does not capture security and privacy as distinct constructs. Future research should explicitly model these dimensions, as Coretax’s consolidation of all Indonesian taxpayer data under a single architecture makes security perceptions a plausible independent antecedent of both system quality evaluations and user satisfaction.

H1.

System quality positively influences perceived ease of use.

2.2.2. Perceived Ease of Use on Perceived Usefulness

The relationship between ease of use and perceived usefulness is theoretically intuitive because cognitive effort is a finite resource. When system interaction requires less mental effort, users have more capacity to recognise the system’s functional benefits, such as faster return filing, automated calculations, and reduced compliance burden [5,19]. Conversely, when interaction is effortful, users’ cognitive resources are consumed by the mechanics of using the platform, making the system’s functional benefits harder to recognise even when they are objectively present [14]. Ref. Venkatesh & Davis [19] tracked this relationship across multiple organisations over time and found it to be remarkably stable, a conclusion reinforced by large-scale empirical reviews of technology adoption models [27]. More recent evidence from digital accounting and government platforms reaches the same conclusion: users who find a system easy to navigate tend to report stronger beliefs about its practical value, even after accounting for the quality of the system’s information outputs [24,28]. For Coretax users managing annual return filing, VAT submissions, and real-time payment processing under legal obligation, a system that feels complicated to operate is one whose benefits may go largely unnoticed.

H2.

Perceived ease of use positively influences perceived usefulness.

2.2.3. Perceived Ease of Use on User Satisfaction

User satisfaction is partly a cognitive judgement and partly an emotional one, as it reflects how people feel about a system after using it, not only what they think it can do [12,29]. Ease of use feeds directly into that emotional dimension. A platform that requires little effort to navigate tends to produce interactions that feel smooth and competent, and these positive interactions can accumulate over repeated use into a favourable overall impression [16]. The opposite process may also occur. Systems that are difficult to operate produce low-grade frustration at each use episode, and that frustration can build over time into durable dissatisfaction, even when the information the system produces is accurate and the outputs are ultimately useful [24]. This is particularly relevant in mandatory contexts because users cannot manage their exposure. Users of a voluntary application can discontinue use when the experience becomes frustrating. A Coretax user filing monthly VAT returns has no such option; they return to the same interface repeatedly, meaning that usability shortcomings may accumulate into a negative user experience and reduce satisfaction [25]. Indonesian e-filing research has shown that reducing interaction complexity is one of the more direct routes to improving taxpayer satisfaction with digital tax platforms, independent of the system’s outputs [10].

H3.

Perceived ease of use positively influences user satisfaction.

2.2.4. Perceived Usefulness on User Satisfaction

Perceived usefulness shapes user satisfaction because taxpayers evaluate whether Coretax delivers meaningful functional benefits in completing tax-related tasks. A platform that accelerates return filing, reduces reporting errors, and lowers compliance friction provides an instrumental payoff that can strengthen users’ overall evaluation of the system [12,30]. In contrast, a system that fails to produce visible efficiency or accuracy gains is unlikely to generate satisfaction, even if its interface is technically smooth. This distinction is important because usefulness captures the practical value of system use rather than the mechanics of interaction.

This relationship is well established in the IS literature. Ref. Wixom & Todd [14] found perceived usefulness to be one of the most consistent predictors of satisfaction because it reflects the extent to which a system helps users accomplish their objectives. Similarly, ref. Venkatesh & Davis [19], applying the DeLone–McLean framework to a tax administration ERP system, confirmed that usefulness-related evaluations shape satisfaction among users in legally mandated system environments. In the Coretax context, where taxpayers cannot avoid the compliance tasks the platform is designed to support, the link between functional value and satisfaction carries particular weight. A system that visibly reduces the burden of monthly VAT submissions or annual return filing gives users a concrete basis for positive evaluation across repeated filing cycles.

H4.

Perceived usefulness positively influences user satisfaction.

2.2.5. Perceived Compulsion on User Satisfaction

H5 directly addresses Gap 1 and RQ2 by introducing perceived compulsion as a construct independent of cognitive system evaluations, testing SDT’s prediction that legal coercion generates negative affect in mandatory IS settings—a mechanism standard TAM frameworks do not account for [15,16,17]. When people are required to use a system by external force, autonomy need frustration follows, producing negative affect and diminished well-being [31,32]. Users who experience strong compulsion tend to approach a system with a compliance orientation rather than an engagement one, framing the interaction as an imposition rather than a tool [15,16], and identical service quality is rated differently when the interaction is entered freely versus under coercion. In the Coretax context, legal penalties attach to non-use, and no exit option exists, making the compulsion signal persistent across every interaction cycle.

The mandatory IS literature has examined institutional coercion through lenses beyond SDT. Ref. Hartwick & Barki [17] established that even within coercive contexts, the quality of the institutional relationship shapes affective responses, while [16] demonstrated that perceived legitimacy of the mandate—rather than coercion per se—determines whether mandated IS use produces acceptance or resistance. Research in public administration IS contexts further shows that coercion embedded within a trusted governance structure produces qualitatively different affective outcomes than coercion perceived as arbitrary imposition [2,18], and that taxpayers in high-trust institutional environments are more likely to internalise compliance obligations as personally meaningful rather than as threats [10,11].

H5.

Perceived compulsion negatively influences user satisfaction.

2.2.6. Perceived Usefulness on Continuous Usage Intention

Satisfaction and usefulness assessments, however, do not operate independently. Where H3 and H4 established how cognitive and affective system evaluations build satisfaction, H6 examines how those evaluations extend forward into taxpayers’ intention to continue engaging with the platform beyond the legal minimum. In mandatory IS deployments where initial use is legally guaranteed, the theoretically meaningful outcome is not whether users start using the system but whether they engage with it genuinely and repeatedly beyond the legal minimum. Perceived usefulness is one of the most robust predictors of that kind of continued engagement across the IS literature [5,6]. The mechanism is relatively straightforward: users who believe a system is actually making their work better—saving time, reducing errors, simplifying compliance calculations—develop a positive performance-based rationale for continued use that operates independently of any legal compulsion [9]. This matters particularly in mandatory contexts because compulsion can secure minimum compliance but cannot generate the discretionary, deeper engagement that produces genuine system utilisation. Usefulness perceptions fill that gap by giving users an instrumental reason to go beyond the floor behaviour that legal obligation alone requires. Research on e-tax systems specifically has shown that perceived usefulness is among the strongest predictors of continuous usage intention among taxpayers, outperforming ease of use in predicting forward-looking engagement [9,13,33].

H6.

Perceived usefulness positively influences continuous usage intention.

2.2.7. User Satisfaction on Continuous Usage Intention

The relationship between satisfaction and continued IS use is one of the most consistently supported findings in the information systems literature. Ref. Bhattacherjee [30] extended ref. Oliver [34]’s expectation-confirmation theory to IS continuance and demonstrated that satisfaction is the dominant proximal predictor of continued use. Its influence outweighs both prior usage patterns and initial adoption beliefs. The logic is intuitive: users who come away from system interactions with a positive overall impression carry that impression forward as a prior evaluation, shaping their disposition toward future use [12,30,35]. In mandatory contexts, where compulsory use accumulates experience quickly and continuously, this satisfaction–continuance pathway operates alongside the legal obligation rather than replacing it. A user legally compelled to file monthly returns will do so regardless, but one who is satisfied with the process is meaningfully more likely to engage with optional features, use the platform proactively, and develop usage habits that go beyond the statutory floor [9,28]. In the Coretax context, where ongoing engagement with advanced functionality is ultimately the goal, satisfaction is the bridge between compliance and genuine adoption.

H7.

User satisfaction positively influences continuous usage intention.

2.2.8. Tax Literacy on the Relationship Between Perceived Usefulness and Continuous Usage Intention

H8 addresses Gap 3 and RQ3 by testing whether individual knowledge differences—operationalised as tax literacy—moderate the pathway through which usefulness perceptions translate into continuous usage intention in a mandatory IS context, a relationship untested in either the mandatory IS or digital tax studies. Even when users perceive a system to be useful, the strength of that perception’s influence on continuous usage intention varies depending on how equipped they are to act on the system’s functional benefits. Tax literacy—defined as an individual’s knowledge of tax obligations, rules, procedures, and ability to interpret and apply tax-related information [10,36,37]—serves as precisely this enabling condition. Following [36,37], the construct comprises two separable dimensions: cognitive tax literacy, capturing declarative knowledge of rules, procedures, and obligations; and motivational tax orientation, reflecting compliance as a personal or professional value independent of enforcement. This study operationalises the cognitive dimension, measuring taxpayers’ self-assessed knowledge of filing procedures, liability determination, and penalty structures—the dimension most directly activated when evaluating whether a platform’s features connect to known obligations. When a taxpayer understands the regulatory purpose of a function and can verify whether its outputs align with legal requirements, perceived usefulness becomes a concrete and personally meaningful asset rather than an abstract system characteristic [10,36]. For high-literacy users, the path from functional benefit to compliance outcome is clearly visible, strengthening the usefulness–continuance link; for low-literacy users, the same usefulness perception carries less decisional weight because connecting platform features to personal tax obligations is harder, weakening that link. This moderating role is consistent with findings that domain knowledge amplifies the behavioural impact of technology evaluations [10,13]. It is important to note, however, that the null moderation may partly reflect measurement limitations rather than a true absence of effect. The tax literacy scale operationalises the cognitive dimension only, and the sample skews toward relatively educated, professionally employed respondents among whom high procedural knowledge may be common. Range restriction in a moderator attenuates interaction terms in Partial Least Squares-Structural Equation Modeling (PLS-SEM), producing near-zero coefficients even when the underlying relationship exists [38,39]. Furthermore, self-assessed tax literacy captures perceived rather than objective competence, introducing socially desirable responding as a potential source of variance compression.

H8.

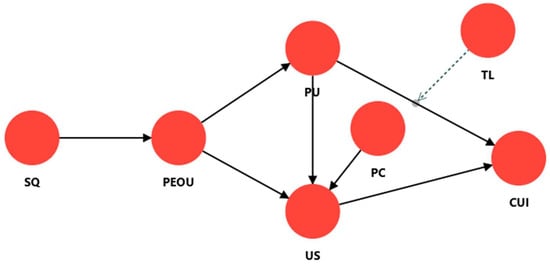

Tax literacy positively moderates the relationship between perceived usefulness and continuous usage intention. All the study’s hypotheses are presented in Figure 1.

Figure 1.

Research Framework. Solid arrows represent hypothesised direct paths; the dashed arrow represents the hypothesised moderating effect of tax literacy on the perceived usefulness–continuous usage intention relationship (H8). SQ: System Quality; PEOU: Perceived Ease of Use; PU: Perceived Usefulness; US: User Satisfaction; PC: Perceived Compulsion; TL: Tax Literacy; CUI: Continuous Usage Intention.

3. Methodology

3.1. Research Design

This study adopts a quantitative, cross-sectional survey design to examine how system quality, perceived ease of use, perceived usefulness, perceived compulsion, user satisfaction, and tax literacy jointly shape continuous usage intention among Indonesian Coretax users. A cross-sectional design is appropriate because the study examines taxpayers’ cognitive and affective evaluations during the early implementation stage of a newly mandated digital tax platform. Since Coretax became fully operational in January 2025, this design captures formative user evaluations at a point when attitudes toward the system are still developing [38].

PLS-SEM, implemented through SmartPLS 4.1.1.2, was selected as the primary analytical method. Three considerations drove this choice. First, the study is explicitly predictive and theory-extending, introducing perceived compulsion and tax literacy into a TAM-based framework rather than testing a fully specified prior theory, which aligns with PLS-SEM’s strengths over covariance-based SEM [38]. Second, PLS-SEM makes no distributional assumptions about the data, which is a practical advantage when working with self-reported Likert-scale responses from a general taxpayer population. Third, the product-indicator approach to modelling the tax literacy interaction term is natively supported within SmartPLS, simplifying the estimation of H8 without additional transformation steps.

3.2. Sampling and Data Collection

There is no publicly accessible registry of active Coretax users, so a criterion-based purposive sampling approach was adopted. The population of practical interest is narrower than all registered Indonesian taxpayers—specifically those who have actively and personally used the system to complete at least one compliance task since January 2025, as passive registrants cannot evaluate system quality or satisfaction from direct experience. Three eligibility criteria were enforced through a front-end screening module: Indonesian taxpayer status, personal Coretax operation, and at least one use since January 2025.

The survey was developed in Bahasa Indonesia, built on Google Forms, and piloted with tax practitioners and IS researchers before full distribution. The finalised instrument was distributed through tax practitioner networks, professional associations, and social media platforms between December 2025 and February 2026. A total of 535 valid responses were retained after removing submissions with missing data or straight-line responding. This sample satisfies PLS-SEM power requirements for detecting medium effect sizes (f2 = 0.15) at 80% statistical power and exceeds the ten-times-maximum-paths heuristic [38]. The sample’s occupational diversity—spanning civil servants, private sector employees, and self-employed taxpayers—supports reasonable generalisability to active Coretax users, though purposive sampling limits formal probabilistic inference.

3.3. Measurement Items

Seven constructs are measured in this study: system quality, perceived ease of use, perceived usefulness, perceived compulsion, user satisfaction, continuous usage intention, and tax literacy. Each construct is captured through five indicators rated on a seven-point Likert scale (1 = strongly disagree, 7 = strongly agree), with the wider range chosen to detect finer attitudinal differences among taxpayers legally required to use the system [38]. All items were drawn from validated measures, rewritten for the Coretax context, and translated into Bahasa Indonesia through a forward-translation process, reviewed by two Indonesian tax practitioners for naturalness and technical accuracy. The tax literacy scale captures the cognitive dimension—procedural and regulatory knowledge—rather than the motivational orientation dimension, a distinction consistent with [36,37] and explicitly acknowledged as a boundary of the present measurement approach. Full construct definitions and the complete set of measurement items are shown in Table 1.

Table 1.

Operationalisation and Measurement Items.

3.4. Common Method Bias Assessment

Common method bias was evaluated using the full collinearity VIF procedure recommended by [41], which tests all constructs in the model—both exogenous and endogenous—rather than limiting the collinearity check to predictor variables only.

3.5. Analysis Technique

PLS-SEM, implemented through SmartPLS 4.1.1.2, was selected for four reasons. First, the model is theory-extending rather than confirmatory, aligning with PLS-SEM’s strengths in predictive research introducing new constructs into established frameworks [38]. Second, it simultaneously estimates the direct path chain and moderation hypothesis without the identification constraints affecting CB-SEM. Third, it makes no distributional assumptions—an advantage for self-reported Likert-scale data. Fourth, the product-indicator approach for H8 is natively supported within SmartPLS. Analysis proceeded in two sequential phases following [39]: measurement model evaluation first, followed by structural model testing. The measurement model assessed indicator reliability through outer loadings (≥0.70), internal consistency through Cronbach’s alpha and composite reliability (both ≥0.70), convergent validity through AVE (≥0.50) [42], and discriminant validity through HTMT ratios (<0.85) [43]. The structural phase assessed R2 for explained variance, f2 for predictor-level effect sizes [44], and Q2_predict via PLSpredict for out-of-sample predictive relevance [45]. All hypotheses were tested using bootstrapping with 5000 subsamples, and H8 was estimated using the product-indicator approach with standardised indicators of tax literacy and perceived usefulness.

4. Results

4.1. Common Method Bias Test Results

The full collinearity variance inflation factor (VIF) procedure was used to check for common method bias, following [41]. This approach goes beyond conventional collinearity diagnostics by running VIF checks for every construct in the model—exogenous and endogenous alike—treating inflated values as a signal of shared method variance rather than merely multicollinearity among predictors. The VIF values ranged from 1.000 to 2.310 across all constructs and remained well below the 3.3 cut-off that [41] sets as the upper acceptable limit. Since all constructs fell below this threshold, common method bias does not appear to be a meaningful threat to the validity of the findings reported here.

4.2. Respondent Profile

The study drew on 535 Indonesian taxpayers who had used Coretax directly at least once since the system went live in January 2025. Male respondents accounted for 69.91% of the sample, while female respondents accounted for 30.09%. In terms of age, the bulk of the sample fell in the 31–39 age range (39.07%), with the 40–49 age group close behind at 32.15%. This indicates that the sample was largely composed of professionally active taxpayers. Respondents generally had relatively high educational attainment. Just over half held a bachelor’s degree (53.64%), and nearly a third had a master’s degree (29.53%)—a profile consistent with taxpayers expected to manage their own compliance through a government digital system. Regarding occupation, the sample split fairly evenly between private sector workers (39.44%) and civil servants (37.01%), together covering more than three-quarters of all respondents. The largest income group was the Rp 6–10 million monthly bracket (37.57%), with the next biggest slice in the Rp 10–15 million range (26.73%), placing the majority in Indonesia’s middle-income tier. Overall, the sample represents educated, employed middle-income taxpayers who are likely to carry direct compliance responsibilities under the Coretax system. Full demographic details are in Table 2.

Table 2.

Sample Demographics.

4.3. Validity and Reliability Assessment

SmartPLS 4.1.1.2 was used to evaluate the measurement model by assessing indicator reliability, convergent validity, internal consistency, and discriminant validity. Because all constructs were first-order reflective constructs, the measurement model was evaluated in a single stage without hierarchical component modelling. Table 1 presents the full original instrument as administered to respondents, comprising 35 items across 7 constructs, with each construct measured by 5 items. Following the outer loading assessment, 10 items below the 0.70 threshold were removed, leaving 25 retained indicators for subsequent analysis. Among the retained indicators, all factor loadings exceeded the 0.70 cut-off [38], ranging from 0.706 for PC4 to 0.941 for SQ5.

AVE values also supported convergent validity. Every construct exceeded the 0.50 threshold, ranging from 0.558 for Perceived Compulsion to 0.835 for System Quality, indicating that each construct explained more variance in its own indicators than was attributable to measurement error [42]. Reliability statistics were also satisfactory, with Cronbach’s alpha ranging from 0.713 to 0.836 and composite reliability ranging from 0.838 to 0.910, both exceeding the 0.70 threshold across all constructs [38]. These figures are presented in Table 3.

Table 3.

Convergent Validity and Reliability.

To assess discriminant validity, three complementary checks were conducted. First, the Fornell–Larcker criterion was satisfied, as Table 4 shows that the square root of each construct’s AVE exceeded its correlations with all other constructs. Second, the HTMT ratios in Table 5 were all below the conservative 0.85 cut-off recommended by [43], further supporting discriminant validity. Third, the cross-loading matrix in Table 6 confirmed that each retained indicator loaded highest on its designated construct, with no problematic cross-loadings on other constructs.

Table 4.

Fornell–Larcker Criterion.

Table 5.

Heterotrait–Monotrait (HTMT) Ratio.

Table 6.

Cross Loadings.

4.4. Model Robustness Testing

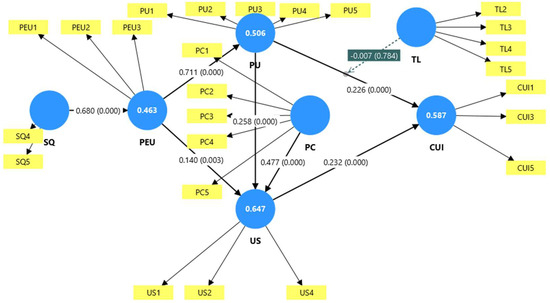

Three of the four endogenous constructs met or exceeded the moderate R2 threshold of 0.50 [40]: User Satisfaction (0.647), Continuous Usage Intention (0.587), and Perceived Usefulness (0.506). Perceived Ease of Use fell just below at 0.463. Adjusted R2 values were nearly identical throughout, indicating no model inflation from unnecessary predictors.

Effect sizes and predictive relevance statistics are consolidated in Table 7. Two paths produced large f2 values—System Quality to Perceived Ease of Use (0.861) and Perceived Ease of Use to Perceived Usefulness (1.024)—reflecting the central role of technical quality in this mandatory deployment context. Tax Literacy’s direct effect on Continuous Usage Intention and Perceived Compulsion’s effect on User Satisfaction both reached the medium range, while the remaining direct paths were small. The Tax Literacy × Perceived Usefulness interaction registered at f2 = 0.000, consistent with the non-significant H8 result.

Table 7.

Effect Sizes and Predictive Relevance.

Out-of-sample predictive relevance was assessed via PLSpredict [46]. All four endogenous constructs returned positive Q2_predict values (Table 7), confirming the model outperforms a naïve baseline on new data. The CVPAT test showed significant improvement over the indicator average benchmark across all constructs (p < 0.001). The model did not outperform the linear model benchmark, a common outcome in reflective structural models that does not undermine predictive usefulness [46]. The saturated model SRMR was 0.080, at the boundary of acceptable fit [41]. Supporting indicators—d_ULS = 2.061, d_G = 0.703, and NFI = 0.706—are retained in accordance with SmartPLS reporting norms.

4.5. Hypothesis Testing

Table 8 and Figure 2 present the full results of hypothesis testing. The upstream quality chain performed as hypothesised across H1 and H2, with system quality producing the strongest path in the model and ease of use amplifying perceived usefulness at the largest effect size observed. H3 and H4 both confirmed positive satisfaction effects, with usefulness carrying greater weight than ease of use—an ordering consistent with compliance-driven IS contexts where functional delivery matters more than interaction comfort. H5 returned a significant but directionally reversed result: perceived compulsion positively predicted user satisfaction rather than negatively, contradicting the hypothesis and SDT-based prediction. The confidence interval did not cross zero, confirming the reversal is robust rather than incidental. H6 and H7 both supported positive effects on continuous usage intention at near-equal magnitudes, establishing the dual pathway from functional and affective evaluations to sustained engagement. H8 was not supported: the tax literacy moderation interaction was non-significant, and the confidence interval straddled zero. Full path coefficients, T-values, confidence intervals, and significance levels are reported in Table 8.

Table 8.

Hypothesis Testing Results.

Figure 2.

Hypothesis Summary. Solid arrows represent significant direct paths. The dashed arrow represents the non-significant moderating path (H8, p = 0.784). Standardised path coefficients (β) are shown on each arrow with p-values in parentheses.

5. Discussion

This study examined how system quality, perceived ease of use, perceived usefulness, perceived compulsion, user satisfaction, and tax literacy jointly shape continuous usage intention toward Coretax among Indonesian taxpayers. Six of eight hypotheses were supported. The two exceptions—H5 (opposite direction) and H8 (non-significant moderation)—are analytically as important as the supported results and are addressed in turn.

H1 is the strongest path in the model (β = 0.680, f2 = 0.861). System quality, captured through taxpayers’ perceptions of Coretax’s technical reliability and overall functional performance, is a powerful upstream driver of perceived ease of use. This is consistent with [14,20], who established that system-level technical characteristics are the primary antecedents of ease-of-use perceptions. In the Coretax context—where taxpayers have no legally permissible alternative—technical friction cannot be offset by switching channels, making ease-of-use perceptions acutely sensitive to system quality. H2 further confirms that ease of use strongly predicts perceived usefulness (β = 0.711, f2 = 1.024), the largest effect in the model. When interaction is cognitively effortless, taxpayers have the cognitive capacity to notice what the system actually delivers—faster filing, improved accuracy, and reduced reporting errors. Refs. Davis, Venkatesh & Davis [5,19] anticipated precisely this mechanism, and ref. Al-Hattami & Almaqtari [28] confirmed it is especially pronounced when user discretion is constrained, which applies directly here. For Coretax specifically, this dynamic carries heightened significance: the platform was launched under active public scrutiny following well-documented early instability, meaning taxpayers’ initial ease-of-use impressions were formed amid technical stress. That the quality-ease-usefulness chain nonetheless held strongly in this sample—within the platform’s first operational year—suggests the chain is robust even when the system is still maturing, and that improvements to Coretax’s reliability would produce upstream gains in perceived usefulness that compound across the entire model. This finding is consistent with recent empirical evidence from digital government IS deployments, where system quality has been confirmed as the dominant upstream predictor of ease-of-use perceptions even during platform transition periods characterised by technical instability [18].

H3 and H4 together show that both ease of use (β = 0.140) and perceived usefulness (β = 0.258) positively influence user satisfaction, with usefulness carrying the larger weight. This ordering makes theoretical sense: in a compliance-driven IS, satisfaction is less about interaction comfort and more about whether the system delivers on its functional promise—meeting expectations, performing consistently, and supporting obligation fulfilment [14,30]. Ref. Akrong et al. [24], evaluating a tax administration ERP through the DeLone–McLean framework, reported a structurally equivalent pattern. H6 and H7 complete the supported chain, with perceived usefulness (β = 0.226) and user satisfaction (β = 0.232) both independently predicting continuous usage intention at near-equal weights. This dual-pathway result aligns with [9], who found that sustained e-filing engagement requires that cognitive utility assessments and affective satisfaction be met simultaneously—a finding replicated here with a general taxpayer population. Ref. Abu-Silake et al. [13] confirmed this dual-pathway structure among digital tax platform users in Jordan, finding that usefulness and satisfaction operate as co-predictors of continued engagement, with comparable effect magnitudes. In the Coretax context, this dual-pathway result carries a specific operational reading. Taxpayers in this sample file monthly VAT returns, submit annual income tax declarations, and manage withholding obligations—a recurring compliance calendar that accumulates satisfaction and usefulness evaluations across multiple use cycles rather than a single interaction. The fact that both usefulness and satisfaction independently predict continuance at near-equal weights suggests that neither functional performance nor affective experience alone is sufficient to sustain engagement; Coretax must deliver on both simultaneously across each successive filing cycle to retain genuine rather than merely compelled usage.

H5 is the study’s most analytically important finding. Perceived compulsion was hypothesised to negatively affect user satisfaction based on SDT [31] and [15]’s evidence that coercion generates resistance in mandatory IS settings. The path is significant but positive (β = 0.477), directly contradicting the hypothesised direction. Ref. Brown et al. [16] offer the most plausible theoretical explanation: when users accept the legitimacy of a mandate, compulsion shifts from a psychological threat to a contextual frame, redirecting evaluative attention to whether the system works rather than to the imposition itself. Ref. Vansteenkiste & Ryan [47] describe this as identified regulation—externally required behaviour becomes congruent with personal or professional values—which is credible among educated, professionally employed taxpayers who regard compliance as part of their occupational identity. Empirically, ref. Ariyanto [11] similarly found that compliance-oriented Indonesian taxpayers evaluate mandatory digital systems through a norm-congruent rather than coercion-resistant lens.

This interpretation is reinforced by the sample’s occupational composition: civil servants (37.01%) and private sector workers (39.44%) together comprise over three-quarters of respondents—individuals whose professional identities are bound up with regulatory adherence and for whom the Coretax mandate aligns with pre-existing occupational norms. It is important to acknowledge, however, that this profile may itself partly explain the positive direction. Less-educated taxpayers, informal-sector workers, and small entrepreneurs—underrepresented here but substantial in Indonesia’s broader taxpayer population—may experience compulsion very differently, potentially producing the negative satisfaction effect that SDT originally predicts. The compulsion-satisfaction finding should therefore be interpreted as specific to this occupational and educational profile rather than as a general property of Indonesian taxpayer behaviour. The practical implication is clear: system performance and functional adequacy are the more actionable levers for satisfaction; mandate legitimacy, while present, should not be assumed to be permanent.

H8 is not supported (β = −0.007, n.s., f2 = 0.000). Tax literacy—reflecting taxpayers’ self-assessed understanding of filing procedures, tax liabilities, and legal consequences of non-compliance—does not moderate the perceived usefulness–continuous usage intention relationship. In a mandatory deployment where usage is legally non-negotiable, the room for individual judgement through which literacy might differentiate users collapses [15]. The non-significant moderation does not mean tax literacy is irrelevant; however, its medium direct effect on continuous usage intention (f2 = 0.246) suggests it independently elevates engagement intentions across the sample. This distinction matters for policy: Ref. Saptono et al. [10] recommends pairing digital tax reforms with taxpayer education, and the direct effect found here supports that as a strategy for raising the overall baseline of Coretax engagement, even if literacy does not amplify the usefulness–continuance pathway at the individual level. In the Coretax context, this direct effect is particularly relevant given Indonesia’s known variability in tax literacy across taxpayer segments. The platform serves a population ranging from sophisticated corporate taxpayers to small entrepreneurs with limited formal tax education. The finding that higher cognitive literacy independently lifts continuous usage intentions suggests that taxpayer education programmes have a direct engagement payoff—not merely a compliance payoff—that justifies investment independent of any moderating function. It is important to note, however, that the null moderation may partly reflect measurement limitations rather than a true absence of effect. The tax literacy scale operationalises the cognitive dimension only—declarative procedural and regulatory knowledge—and the sample skews toward relatively educated, professionally employed respondents among whom high procedural knowledge may be common. Range restriction in a moderator attenuates interaction terms in PLS-SEM, producing near-zero coefficients even when the underlying relationship exists [38,39]. Furthermore, self-assessed tax literacy captures perceived rather than objective competence, introducing socially desirable responding as a potential source of variance compression. This interpretation would be tested more definitively by using objective tax knowledge measures or a two-dimensional tax literacy scale that captures both cognitive and motivational dimensions.

Addressing the research questions and the gaps that motivated them, the findings provide three main answers. First, RQ1, which corresponds to Gap 1, is answered affirmatively. The quality, ease-of-use, and usefulness chain operates robustly in a mandatory post-adoption context, confirming that TAM’s explanatory logic remains relevant even when initial adoption is legally guaranteed and continuous usage intention becomes the theoretically meaningful outcome. Second, RQ2, also linked to Gap 1, is answered affirmatively but not in the hypothesised direction. Perceived compulsion significantly affects user satisfaction, but the effect is positive rather than negative. This finding suggests that institutional acceptance, rather than coercion-based resistance, is the operative mechanism in this context and shows that the coercion-resistance prediction derived from SDT was not supported. Third, RQ3, which corresponds to Gap 3, is answered negatively. Tax literacy does not moderate the perceived usefulness-continuous usage intention relationship, suggesting that the mandatory deployment context may suppress individual-level moderation. However, its direct effect on continuous usage intention confirms its additive value as an engagement lever independent of the usefulness pathway.

6. Implications

6.1. Theoretical Implications

This study makes three distinct theoretical contributions that collectively advance mandatory IS post-adoption research beyond what TAM, SDT, and tax literacy frameworks have individually delivered. Critically, integrating perceived compulsion into a post-adoption TAM produces findings that neither framework alone could have generated. TAM predicts quality-driven engagement but has no mechanism for legal coercion; SDT predicts coercion-driven resistance but was theorised in voluntary contexts. Their combination reveals that institutional acceptance—not resistance—is the operative mechanism when perceived legitimacy is high, advancing coercion theory in mandatory government IS research. First, this study extends TAM beyond its predominantly voluntary adoption applications into a fully mandatory post-adoption context with an empirically validated upstream quality chain. Prior TAM studies have examined settings where perceived ease of use and perceived usefulness precede an unconstrained behavioural choice [5,6]. This study relocates that explanatory logic to a setting where initial adoption is legally guaranteed and the theoretically meaningful outcome is continuous usage intention—the degree to which taxpayers engage with Coretax beyond the compliance minimum. The finding that system quality strongly predicts ease of use (β = 0.680), which in turn predicts usefulness with the largest effect in the model (β = 0.711), empirically validates the upstream antecedent chain theorised by [21] in TAM3 within a nationally mandated IS deployment. This adds to a body of work—including [14,24]—that positions system quality as the foundational upstream lever in government IS, and it does so in a context where the stakes of that quality are particularly high: users have no alternative platform through which to discharge legally mandated obligations.

Second, and most significantly, this study challenges SDT’s predictions in mandatory IS contexts and proposes that perceived legitimacy and institutional trust serve as theoretically grounded boundary conditions that determine when coercion produces psychological resistance rather than affective acceptance. SDT predicts that externally compelled behaviour frustrates autonomy needs, generating negative affect and resistance [31,32], and ref. Xue et al. [15] operationalised this logic by expecting perceived compulsion to erode satisfaction. The positive and significant compulsion-satisfaction path (β = 0.477) directly contradicts this prediction in the Coretax context.

The theoretical account rests on a distinction SDT literature has not consistently drawn in IS research: the psychological experience of compulsion is not uniform across institutional contexts. When a mandate is perceived as illegitimate—arbitrary or imposed by an authority whose right to compel is disputed—SDT’s reactance mechanism operates as theorised, where autonomy need frustration follows, satisfaction declines, and resistance intensifies, which is the modal assumption of prior mandatory IS research drawn from workplace technology settings [15,16,17]. When the mandating institution is perceived as legitimate, however, compulsion does not register as a personal autonomy violation; it is instead framed as an institutional given, redirecting evaluative attention toward whether the system performs adequately. Ref. Brown et al. [16] theorised this mechanism through their institutional acceptance construct, and the present finding provides its clearest empirical confirmation in a nationally mandated tax IS deployment. Institutional trust introduces a complementary boundary condition: when taxpayers trust that the governing authority is acting in the public interest, compulsion carries a different affective loading, functioning as participation in legitimate public infrastructure rather than imposition [7,8]. Ref. Gagné & Deci [32] identified regulation provides the motivational mechanism—externally required behaviour becomes congruent with personal values when the mandating institution is trusted, and the activity is recognised as meaningful, which is plausible among the professionally employed, compliance-oriented Indonesians in this sample.

Together, these two boundary conditions jointly determine whether SDT’s coercion-resistance prediction holds or fails: where legitimacy is disputed, and institutional trust is low, compulsion will produce the negative affective outcomes SDT predicts; where both are high, the coercion frame is internalised and system performance becomes the operative driver of satisfaction. Future research should measure both constructs directly and test their interaction with perceived compulsion—a test that the present cross-sectional design cannot deliver, but which these findings make theoretically compelling.

Third, the study clarifies the conditions under which individual knowledge differences moderate technology adoption behaviour, advancing understanding of tax literacy in digital IS research. The non-significant moderation (β = −0.007, f2 = 0.000) is theoretically informative rather than merely null: in mandatory IS contexts, the compulsory deployment frame limits the room for individual differences to shape adoption behaviour, consistent with [15]’s argument that mandatory settings alter the cognitive architecture of technology evaluation in ways voluntarist models do not capture. The null result may further reflect the cognitive dimension’s role as background competence rather than an active amplifier—Ref. De Clercq [36] distinguishes between knowing about tax and caring about compliance, and only the former is captured here. Caution is nonetheless warranted, as range restriction within a highly educated sample, single-dimensional operationalisation, and self-assessed rather than objective measurement are all plausible sources of downward bias in the interaction estimate.

The medium direct effect of tax literacy on continuous usage intention (f2 = 0.246) nonetheless establishes it as a meaningful independent predictor—one that lifts engagement intentions without conditioning the strength of the usefulness–continuance relationship itself, a theoretical distinction that enriches the construct’s conceptualisation in IS adoption research. Beyond tax literacy, perceived risk and digital competence represent theoretically grounded alternative moderators whose inclusion in future models would clarify whether the null reflects measurement limitations, construct specificity, or genuine suppression by the mandatory deployment context. Together, these three contributions advance IS adoption theory in mandatory government platform contexts—a domain growing rapidly as tax authorities worldwide pursue digital transformation [4,13]—and provide a theoretically grounded account of why the psychological dynamics of legally compelled IS use differ systematically from those of voluntary adoption.

6.2. Practical Implications

Three groups stand to benefit most directly from this study’s findings: the Indonesian Directorate General of Taxes (DJP), as Coretax’s owner and operator; the Ministry of Finance, as the policymaker behind the reform; and employers and professional bodies whose members use the system daily.

6.2.1. For the Directorate General of Taxes

The clearest practical implication for the DJP is that system quality—specifically, whether Coretax meets taxpayers’ expectations as a tax administration system and whether it functions well overall—sits at the top of the entire chain of taxpayer experience. When these foundational technical expectations are met, ease of use, perceived usefulness, satisfaction, and continued engagement all tend to follow. This makes overall system performance the highest-leverage investment the DJP can make. The early months of Coretax’s rollout were marked by access issues and instability, and such experiences may shape later user evaluations. Going forward, the DJP should commit publicly to concrete performance standards during the periods that matter most—the annual income tax return season in March and the recurring monthly VAT submission windows—because these are the moments when taxpayer frustration is most likely to form and harden.

On the usability side, the retained dimensions that matter most to taxpayers are how quickly they can learn the platform, how smoothly they can complete their actual tax tasks using it, and how clear and understandable the interaction feels throughout. The DJP would benefit from building a structured feedback mechanism involving actual taxpayers—particularly private sector workers and civil servants—to surface difficulties along these dimensions. A quarterly usability review process, where representative users walk through real compliance tasks and flag friction points, would give the DJP a direct line into the ease-of-use factors that most affect downstream satisfaction and engagement.

On the usefulness side, the items taxpayers responded to most strongly reflect concrete instrumental outcomes: completing obligations more quickly, improving the accuracy of filings, making it easier to fulfil compliance requirements, and reducing errors in the reporting process. The DJP’s product development priorities should be anchored to these outcomes rather than to feature additions that do not directly reduce compliance effort or improve reporting accuracy. Every new functionality should be evaluated against whether it makes filing faster, more accurate, or less error-prone for the average taxpayer.

6.2.2. For Tax Policymakers and the Ministry of Finance

One of the more surprising findings is that legal compulsion does not appear to reduce taxpayers’ satisfaction with Coretax. Although respondents reported regulatory pressure, limited choice, and potential legal consequences for non-use, perceived compulsion was positively associated with satisfaction. This suggests that taxpayers may have accepted the mandate and shifted their evaluative attention toward whether the platform performs its required functions competently. For policymakers, the implication is not to ignore legitimacy-building efforts, but to prioritize execution quality. Policy attention and budget should therefore focus on improving system reliability, response speed, error prevention, and user support, since these are the aspects most likely to shape taxpayers’ satisfaction under mandatory use.

The findings also point to a specific and actionable tax literacy agenda. The retained tax literacy items capture awareness of filing procedures and deadlines, understanding of tax liability determination, knowledge of non-compliance penalties, and confidence in reporting requirements. Strengthening these forms of procedural knowledge can independently raise taxpayers’ intentions to engage continuously with Coretax, rather than merely comply at the minimum required level. The most effective delivery mechanism may be contextual literacy support embedded directly in the Coretax interface. Instead of relying only on standalone seminars or printed guides, the platform could provide brief, task-relevant explanations of deadlines, penalty implications, and links between specific obligations and system functions. Delivered at the moment taxpayers encounter these tasks, such embedded prompts are more likely to be retained and applied than information consumed separately.

6.2.3. For Employers and Professional Organisations

With private sector workers and civil servants making up the overwhelming majority of the active user base, the workplace is a natural channel for boosting platform engagement. Organisations subject to VAT, withholding tax, or corporate income tax obligations should treat Coretax proficiency as a core operational competency—specifically covering how to complete tax tasks efficiently using the platform, how to interact with it clearly and correctly, and how to fulfil compliance requirements accurately through the system. Building this into onboarding for finance and compliance staff, creating internal submission calendars aligned with Coretax’s reporting cycles, and designating internal contacts who can assist colleagues would collectively reduce the friction that currently limits sustained engagement beyond the legal minimum.

Professional associations for accountants and tax practitioners carry a parallel responsibility. Since Coretax is now the permanent infrastructure for Indonesian tax administration, operational fluency—including task completion, accuracy in filings, and understanding of how the system supports compliance requirements—belongs in continuing professional development alongside substantive tax knowledge, rather than being treated as peripheral. Sustained engagement beyond the compliance minimum is built on whether Coretax performs to expectations, whether taxpayers find it easy to learn and use for real tasks, and whether they arrive at it with enough knowledge of procedures, deadlines, and consequences to engage with it purposefully. Users have broadly accepted the mandate. The real work ahead lies in making the experience that mandate delivers genuinely worthwhile.

7. Conclusions

Under a TAM-based framework extended with perceived compulsion and tax literacy, this study provides one of the first empirical examinations of continuous usage intention toward Coretax among Indonesian taxpayers, with six of eight hypotheses supported. System quality emerged as the critical upstream lever, producing the strongest path in the model (β = 0.680) and initiating the cognitive adoption chain: ease of use strongly amplified perceived usefulness (β = 0.711), which, alongside user satisfaction, independently predicted continuous usage intention at near-equal weights (β = 0.226 and β = 0.232, respectively). Both ease of use (β = 0.140) and perceived usefulness (β = 0.258) positively influenced user satisfaction, with usefulness carrying the greater weight—an ordering consistent with compliance-driven IS contexts where functional delivery matters more than interaction comfort. Collectively, these six supported paths confirm that even within a legally mandated deployment where initial adoption is guaranteed, the cognitive quality chain theorised by TAM operates robustly, and system performance remains the dominant determinant of taxpayer engagement beyond the compliance minimum.

The two unsupported results are among the study’s most theoretically significant contributions. The positive effect of perceived compulsion on user satisfaction (β = 0.477) contradicts the SDT-derived prediction in this context, where externally imposed IS use was expected to generate resistance. Instead, the finding points to institutional acceptance as the operative mechanism. When users internalise compliance as an occupational norm, legal coercion may redirect evaluative attention toward system performance rather than being experienced primarily as personal imposition. This suggests that, in high-legitimacy mandatory deployments, governments should not rely only on legitimacy communication. Greater policy attention and budget should be directed toward system quality and functional performance, since these factors are more likely to sustain satisfaction under mandatory use.

This finding nonetheless carries a warning. Coercion-driven satisfaction is not the same as genuine engagement—users satisfied because they have internalised a mandate represent a fragile form of adoption that could reverse rapidly if legitimacy erodes or system quality deteriorates. Optimising compliance systems for satisfaction metrics without preserving user agency—the ability to provide feedback, influence system development, and engage meaningfully with the platform—risks building adoption on an institutionally contingent foundation rather than a functionally earned one. Tax literacy’s null moderation (β = −0.007, f2 = 0.000) reinforces this concern: the mandatory frame suppresses the individual-level judgement through which users would ordinarily evaluate a system on its merits. Its significant direct effect on continuous usage (f2 = 0.246), however, offers a constructive counterpoint—building tax literacy raises the baseline of genuine engagement, giving users the cognitive resources to find the system personally meaningful rather than merely obligatory. These findings collectively argue that mandatory IS design must account for user autonomy, not just compliance metrics, as both an ethical commitment and a practical safeguard against the fragility of adoption that coercion-driven satisfaction alone cannot sustain.

More broadly, future research should situate mandatory IS adoption within the public administration literature on tax morale and institutional trust, examining whether platform quality and the compulsion-satisfaction dynamics observed here have downstream consequences for taxpayers’ civic attitudes toward the tax process itself—a dimension that positions Coretax not merely as a compliance tool but as an institutional interface between citizens and the state.

Limitations and Future Research

First, this study was conducted within the first year of Coretax’s operation, meaning taxpayer perceptions reflect an early adaptation period involving a platform still under active development. Ease-of-use and usefulness evaluations formed at this stage may not represent the settled experience of a technically mature system. More importantly, the unexpected positive direction of the compulsion-satisfaction path may partly reflect the novelty of the mandate rather than a stable attitudinal orientation. Longitudinal research tracking the same taxpayer cohorts across multiple Coretax usage cycles would reveal whether the quality-ease-usefulness chain strengthens as familiarity accumulates, and whether the compulsion-satisfaction relationship weakens as the mandate transitions from a new imposition to an internalised routine, a dynamic account that cross-sectional designs cannot provide. Future research should also directly measure perceived legitimacy and institutional trust to formally test whether they moderate the compulsion-satisfaction relationship, as proposed in the boundary-condition argument in Section 6.1.

In addition, this study measures taxpayer perceptions and behavioural intentions rather than actual compliance behaviour or fiscal outcomes. Future research linking platform adoption quality to measurable changes in tax revenue, compliance rates, or administrative efficiency would provide a valuable complementary account of Coretax’s real-world impact that the present perceptual design cannot deliver. The study is also bounded by a single national context. Although the mandatory IS adoption dynamics examined here are relevant to tax authorities worldwide, including EU member states implementing SAF-T, real-time e-invoicing, and unified digital tax platforms, cross-national comparative research is needed to establish whether the institutional acceptance mechanism and quality-adoption chain generalise across different regulatory cultures, levels of institutional trust, and stages of digital infrastructure maturity.

Second, this study measured tax literacy as declarative knowledge only, capturing the cognitive dimension while leaving open whether the motivational dimension—compliance as a personal or professional value rather than mere rule awareness—would exhibit stronger moderating potential. Future research should develop a two-dimensional measure that tests both dimensions simultaneously to resolve the null moderation finding more definitively. Caution is also warranted on measurement grounds. The sample’s educational profile—over 83% holding at least a bachelor’s degree—raises the possibility of range restriction in the moderator, which attenuates product-indicator interaction terms in PLS-SEM regardless of the true effect size. Objective tax knowledge measures would provide a cleaner test than self-assessed literacy ratings.

Third, this study tested tax literacy as the sole individual-level moderator of the usefulness–continuance pathway. Perceived risk and digital competence represent two plausible alternatives—high-risk users may convert usefulness into continuance more strongly when the system visibly reduces compliance errors [5,6], while stronger digital proficiency reduces cognitive barriers to exploiting system features. Future research incorporating both constructs alongside a two-dimensional tax literacy measure would provide a more complete account of individual-level moderation in mandatory IS contexts.

Fourth, the sample’s demographic composition limits the generalisability of the H5 finding. Over 83% of respondents held at least a bachelor’s degree, and civil servants and private sector employees comprised over three-quarters of the sample—a profile systematically different from Indonesia’s broader taxpayer population, which includes large informal-sector segments and lower-education taxpayers for whom legal coercion may carry very different psychological weight. Future research should sample across education, income, and employment formality strata to test whether the institutional acceptance mechanism generalises beyond compliance-oriented, professionally employed segments.

Fifth, the present operationalisation of system quality does not capture data security and privacy protection as distinct dimensions. In centralised mandatory platforms like Coretax—where all taxpayers’ financial data is consolidated under a single architecture—security concerns represent a theoretically distinct quality dimension, as evidenced by privacy barriers documented in European mandatory e-invoicing deployments [31,43]. Future research should explicitly incorporate security and privacy perceptions into the system quality antecedent chain.

Author Contributions

Conceptualization, A.P.T. and A.D.K.S.; methodology, A.P.T., W.K. and A.D.K.S.; software, W.K. and P.P.; validation, W.K. and A.D.K.S.; formal analysis, A.P.T. and W.K.; investigation, W.K. and A.D.K.S.; resources, P.P.; data curation, A.P.T. and A.D.K.S.; writing—original draft preparation, A.P.T., W.K., P.P. and A.D.K.S.; writing—review and editing, W.K. and A.D.K.S.; visualization, P.P.; supervision, A.D.K.S.; project administration, A.P.T. and P.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Ethical review and approval were waived for this study in accordance with the National Guidelines and Ethical Standards for Health Research and Development [Pedoman dan Standar Etik Penelitian dan Pengembangan Kesehatan Nasional] issued by the Indonesian Ministry of Health [46], which exempts survey-based research involving anonymous, non-sensitive data with no risk of physical or psychological harm to participants.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author due to privacy concerns.

Acknowledgments

During the preparation of this work the authors used ChatGPT 5.2 and Grammarly 1.2.98 for the purpose of grammar and language editing. All authors have reviewed and edited the output and take full responsibility for the content of this publication.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- OECD. Tax Administration 3.0: The Digital Transformation of Tax Administration; OECD Publishing: Paris, France, 2020. [Google Scholar] [CrossRef]

- Eom, S.-J.; Lee, J. Digital government transformation in turbulent times: Responses, challenges, and future direction. Gov. Inf. Q. 2022, 39, 101690. [Google Scholar] [CrossRef]

- KPMG. New Tax Regulations for the Implementation of the Core Tax Administration System. Available online: https://kpmg.com/id/en/insights/2025/01/id-tnf-jan-2025-pmk-81-ctas.html (accessed on 1 March 2026).