Abstract

The objective of this research is to analyze the impact of consumer price index, exchange rate, broad money supply, and export on tax revenue in Cambodia. The short-run effects from the ARDL cointegration model suggest that inflation negatively influences tax revenue. Changes in the exchange rate also had a negative effect on tax revenue, although the power of this influence was large. On the other hand, an increase in money supply was realized to improve tax revenue performance as revealed by a positive and statistically significant coefficient of broad money. The empirical results also indicate that the impact of exports on tax revenue was insignificant. The error correction term indicates that the flow adjustment was fast, in that about 83.76% of short-run deviations were corrected in one period, thus enabling the quick restoration to the long-run equilibrium after transient disturbances. In the long-run, only exchange rate and broad money were found to be statistically significant determinants of tax revenue. The relationship was found to be negative for exchange, but positive for broad money.

1. Introduction

The literature suggests that tax yields are highly correlated to macroeconomic factors, particularly economic growth and the structure of the economy. State revenue tends to rise during economic expansion as incomes, consumption spending, and corporate profits rise, thus expanding the tax base and promoting increases in collections (Bayer, 2015). As a result, GDP aggregates such as gross domestic product (GDP), consumption, exports and employment are often adopted in empirical tax revenue models as central explicative factors. Cross-sectional and time series studies have shown positive association between economic growth and tax revenue, especially for indirect taxes like value-added tax which is consumption driven (Streimikiene et al., 2018).

Investment and institution, in addition to macroeconomic growth, matter for tax revenue performance. The effectiveness of tax collection, stability of the tax structure and costs of compliance impact taxpayers’ capacity and willingness to pay taxes. Cross-country evidence from OCED countries indicates that the higher the administrative burden of tax systems, the more detrimental the impact they can have on macroeconomic performance although higher income categories may still be able to induce high tax burdens without necessarily being exposed to competitive pressures (Lentner et al., 2022).

Empirical evidence also emphasizes the role of government spending, human development and governance in influencing tax revenue. Government spending has expansionary effects on economic activity and thus, the tax base, further strengthening revenues through spend-tax by way of mechanism. Meanwhile, increased human development—improved education and health outcomes—increases productivity and long-run growth, which indirectly boosts tax capacity. It is found that in Indonesia, government spending and human development have a positive and significant effect on tax revenue, in which economic growth acts as a mediation variable whereas corruption weakens the ability to collect revenues by negatively affecting taxpayers’ compliance and administrative bureaucracy performance (Maryantika & Wijaya, 2022).

The empirical evidence underpins the importance of economic growth for tax revenue. Increasing income and production levels work to broaden the tax base by enlarging taxable consumption, corporate profits, and personal incomes, which boosts government tax receipts. Evidence from developed and emerging countries indicates a significant positive relationship between per capita income or GDP growth, and tax revenue effort (Mawejje & Odhiambo, 2022). Corresponding results are identified at the cross-country level where the author notes better expansions of economic activity boost tax capacity; however, this impact is different according to economic structure and institutional quality (Chettri et al., 2023).

Apart from growth, the composition of the economy also has important implications for the mobilization of tax revenues. A high share of agriculture in GDP is also linked to low tax revenue because it is normally very hard to tax agriculture for informal, subsistence and wide exempt reasons. Empirical evidence from Africa and other developing countries suggests that agrarian-dominated economies experience less efficient taxation (Ibrahim & Jairo, 2023; Chamisa & Sunde, 2024). On the other hand, increased trade openness and financial sector development might also increase tax revenue through an enlarged base of taxable transactions and an improved compliance, although in some cases, the net effect of openness is indeterminate (Chettri et al., 2023).

Institutional and administrative aspects are also vital in determining tax revenue performance. Tax collection is hampered by weak tax administration, low enforcement capacity, corruption, and sizable informal economies. For example, what can be said from studies concentrating on East African countries is that the improvements in the tax administration’s operational efficiency, such as staff productivity and taxpayer’s coverage, substantially increase the revenue performance, particularly in the short term (Ibrahim & Jairo, 2023). On the other hand, a low standard institutional quality and growth of shadow economy have an adverse impact on tax collection ability, whereby the effective tax collection is effectively reduced (Chamisa & Sunde, 2024).

Furthermore, there is an impact of macroeconomic stability on the tax revenue dynamics. Realistic behavior of tax collections depends on expectations of inflation, interest rates and external sector conditions. Inflation may raise nominal revenue in the short term, though it can be easily shown to weaken real tax performance over time by distorting economic incentives and compliance (Chamisa & Sunde, 2024). Fiscal performance is also highly correlated with the overall macroeconomic situation, and tax receipts in particular respond pro-cyclically to economic activity (Mawejje & Odhiambo, 2022). A study has shown that more income and output expand the tax base by raising consumption, corporate profits, and personal incomes, leading to more revenue collection for the government (Garg et al., 2024; Kebede et al., 2024). More interestingly, there is empirical evidence from developing and emerging economies that GDP growth and per capita income are positively correlated with tax revenue; however, the nature of this relationship varies depending on economic structure and policy effectiveness (Abidar et al., 2025).

Tax potential is also heavily influenced by the economic structure. For instance, a high magnitude in the agricultural sector is frequently accompanied by low levels of tax revenue generation due to its informality, subsistence orientation and administrative challenges for taxation (Kebede et al., 2024). Manufacturing and services are normally less difficult to tax and are slightly more dependable as revenue sources. The study has also indicated that a greater percentage of manufacturing and services in GDP has a positive impact on tax revenue performance in the developing regions (Abidar et al., 2025). Moreover, institutional and governance aspects have received more attention in the recent literature. Inefficient institutions, corruption, and sizable informal sectors erode tax compliance and revenue-yield potential. On the other hand, better quality of governance and administrative capacity lead to more efficient collection of taxes. Recently, there is widespread attention on the role of digitalization and e-government in increasing tax revenue mobilization through lowering compliance costs; improved transparency and limiting opportunities for tax evasion is highlighted in recent studies (Tolossa & Melese, 2024).

Tax income is a key component for the funding of public expenditure, promoting economic growth and fiscal sustainability in developing countries where alternative provenance of public finance are constrained. A well-functioning tax system is the cornerstone for governments to deliver critical public goods and services, reduce inequality and ensure macroeconomic stability. Nevertheless, heavy exposure to economic shocks, poor tax administration, and structural impediments to domestic resource mobilization meant that many low-income developing countries still have not been able to generate the necessary level of revenue from taxation. Cambodia is not different either as the tax-to-GDP level is lower relative to regional counterparts, which means that understanding factors contributing to the performance of tax revenue becomes crucial. As such, the purpose of this paper is to examine which macroeconomic factors including consumer price index, foreign exchange rate, broad money, and export have significant effect on tax revenues in Cambodia. Welfare policy implication for the government to improve tax revenue performance is also attempted in this research.

The Cambodia tax revenues are classified into three categories: taxes on income, profits, and capital gains; taxes on goods and services; and taxes on international trade and transactions. The budget deficits of the central government, recently, are financed by government bonds issued by the Ministry of Economy and Finance. The major investors include institutional investors, such as private companies, finance companies, and banks.

The organizational structure of the study is subdivided into five sections. Section 1 and Section 2 present the introduction and literature review, respectively. Section 3 outlines the methodology of the study, while Section 4 presents the empirical results. Finally, Section 5 provides the conclusions and policy implications.

2. Literature Review

Economic growth is often seen as the principal driver of tax revenue, as higher income levels expand the tax base by encouraging consumption, output and employment. Empirical findings from emerging markets indicate a direct link between real GDP, income per capita, and tax revenue results. In addition, tax capacity increases with economic activity as tax base expansion occurs and administration effectiveness improves. There is also a great benefit to be derived from macroeconomic stability. Inflation affects tax revenues in both the nominal and real sense, through a long-term channel of price instability, which serves to depress real revenue yields, undermine compliance and discourage economic activity (Maganya, 2020). Related to the above are monetary permissive conditions and financial development effects on tax revenue mobilization. Broad money aggregates are widely used as associates for monetization and financial depth in the economy. A larger money supply allows for greater ease in economic transactions, enhances traceability for flows of income, and diminishes dependence on informality-based cash economies, leading to efficiency gains in tax collection. Empirically, there is a positive association between broad money and tax revenue for the developing world but the reverse can be the case if inflation accelerates faster than output due to overhauling of the monetary sector (Mukhtarov et al., 2020; Maganya, 2020).

Exchange rates can also affect tax revenue by influencing trade and domestic price levels. Devaluation of the currency may raise domestic value of imports and exports leading to higher tax revenues from trade; however, excessive volatility can lead to lower levels of international activity discouraging trade and investment, which may adversely affect revenue collections (Mukhtarov et al., 2020; Kamasa et al., 2025). The influence of exchange rate variation on tax revenue overall depends on the trade structure and price elasticity of economic agents. Apart from macroeconomic fundamentals, institutional quality is critical to progressive revenue collection. Poor governance, corruption and political instability along with administrative inefficiency mitigate tax compliance as well as revenue capacity. Evidence from Pakistan suggests that better government stability, higher law enforcement and relatively lower rates of internal and external conflicts led to a significantly higher yield of tax revenues in the short as well as long run (Hassan et al., 2021). Empirical evidence suggests that good governance influences the elasticity of the link between economic activity and tax revenue by improving enforcement, transparency and confidence. On the other hand, weak institutions lead to tax evasion as well as make the tax policy measures less efficient. Revenue performance is highly influenced by fiscal policy tools such as tax reform and public spending strategy. This worked so well that there are clear examples from Ghana that show the importance of smart and well-managed tax reforms in ensuring better revenue mobilization over time. They improved the tax base, administrative efficiency and compliance, although their success relies on enabling factors like education, prudent debt management and institutional capability (Kamasa et al., 2025).

A key strand of literature focuses on the macroeconomic drivers of tax revenues, including economic growth, inflation and public debt dynamics. Applying data from Sri Lanka, the empirical findings of a research indicate that real GDP growth has a positive effect on both the short- and long-run tax revenues (particularly direct taxes), implying that economic enlargement widens the specific taxable foundation with enhanced accumulation of revenue. They also found that inflation and exchange rate dynamics have indirect effects on tax collections due to their effect on public debt and fiscal sustainability, showing that macroeconomic instability can negatively affect revenue collection strengths (Vinayagathasan & Ranjith, 2021).

The entrepreneurial structure of fiscal policy and particularly the interrelationships between government revenues, expenditures and fiscal deficits is another important determinant underlined in the literature. In Pakistan, a strong long-run relationship between government revenues and expenditures is revealed, where fiscal deficits react to variations in both components. The study provides evidence in favor of the spend-and-tax hypothesis, which suggests that an increase in government expenditures calls for increased tax revenues if at all government expansion is reversible. This linkage implies that tax revenues are not determined independently but are endogenously related to public spending choices and deficit paths (Chandia et al., 2022). In addition to macroeconomic and fiscal interrelationships, composition and design of taxation are indeed important in shaping revenue performance. Evidence from South Africa indicates that not all tax instruments have the same impact on economic performance and, by implication, revenue potential. Income taxes and value-added tax emerge as more conducive to long-run productivity, and hence to a durable tax base, even though many taxes present adverse short-run effects (Phiri & Mbaleki, 2022).

Tax institutions, and particularly tax compliance and evasion, have emerged as core factors of tax revenue performance. The Indonesian evidence suggests that widespread tax evasion reduces potential revenue significantly and the financial sector development appears to help counteract this loss. There is a non-trivial relationship between financial development and tax evasion: the higher the participation in financial markets, the higher penetration of loans to reduce informality, and the higher the level of tax evasion. These results emphasize that the development of good governance and financial transparency may influence revenue mobilization (Safuan et al., 2022). Based on a Spanish sample, a study finds out that both tax revenues and government spending have long- and short-run effects to the output, but these influences are asymmetric according to directions of fiscal policy changes. Results point to the fact that ill-justified tax increases may cool down economic activity and reduce future revenue collection, whereas appropriately calibrated fiscal policies can help create the conditions for growth and fiscal soundness (Sosvilla-Rivero & Rubio-Guerrero, 2022).

It is generally acknowledged that economic growth is a key driving factor for tax performance, because increasing income and output creates a bigger tax base, hence generating higher capability in revenue collection. This is further confirmed by evidence from the Baltic region where municipalities experience a significant positive effect of higher GDP per capita on tax revenues, implying, as expected, higher income levels and larger fiscal capacity in more advanced economies. Trade openness and industrial value added is also favorable by expanding the tax base and the level of transactions. Larger government spending typically contributes to increased taxes because of additional economic activity and higher revenue performance. On the other hand, increased public debt and macroeconomic instability such as inflation and exchange rate volatility undermine tax receipts due to low investor confidence, passive economic activities and disloyalty (Mirović et al., 2023).

The sectoral composition is also an important determinant in the results of tax revenues. The transition from agriculture to nonagricultural is generally thought to be conducive to increased revenue, as taxing the formal sector is considered less complex. Evidence from Tanzania shows that service-sector expansion has a marked positive effect on tax revenue, especially government services and tradable output processing, which can be more effectively captured by tax authorities. This result is consistent with the proposition that structural change towards services can bolster tax bases in developing economies (Mapunda et al., 2023). Another key determinant of tax revenue is foreign direct investment (FDI), but the results on its impact are mixed across theoretical studies. FDI can bring about increased economic activity, employment and corporate profits; however, aggressive tax incentives and repatriation of profits could undermine potential tax savings. Time series findings from South Africa show that FDI has a statistically significant negative long-term impact on tax revenue, thereby implying that the positive effects of investment inflows may be outweighed by tax holidays and aggressive investment policies. These results reveal that the relationship between FDI and tax revenue is complicated and throw its challenges in promoting investment alongside sound policy (Jemiluyi & Jeke, 2023).

Development of the financial sector can additionally promote tax mobilization as it normalizes formal financial transactions and enhances the efficiency of tax administration. A well-developed financial system improves the tracking facility on income and consumption, which in return promotes high tax compliance and efficiency of tax collection especially in developing countries moving more to financial inclusion (Jemiluyi & Jeke, 2023). Most interestingly, the empirical findings in Taiwan indicate that the relationship between economic growth and tax revenues is nonlinear; total tax revenue and direct tax revenue capturing an N-shaped relation with GDP, due to the erosion of the tax base at higher levels of taxation. The reason is that the effective package of taxation is intensified and underground economy grows in size when tax burdens go beyond certain levels. Second, indirect taxes have either a slow or a high positive relationship with economic growth due to better compliance and lower evasion opportunities (Wang, 2022). Segmentation and the diversity of revenue streams are also essential for tax revenues sustainability. The composition and diversification of sources are also important factors in the sustainability of tax revenues. Evidence from Indian states suggests that heavy dependence on a small number of taxes, especially sales taxes, enhances revenue volatility and undermines fiscal stability. Sectorial composition, urbanization and agricultural development are among the main economic factors influencing the degree of revenue diversification and tax capacity (Darshini & Gayithri, 2023).

In Lithuania, it has been found that in the short and long-run economic growth stimulates tax revenues where is a more significant effect on corporate and indirect taxes which is related to better compliance of taxpayers and decrease in shadow economy (Ulvidienė et al., 2023). Realized tax revenues are also highly dependent from the macroeconomic stability. Inflation and fiscal dis-equilibria deteriorates real tax revenues due to inefficient collection lags, non-compliant laws. Exchange rate changes and external sector variables also affect tax revenue notably in trade dependent embraces with consumption taxes (Garg et al., 2024). Furthermore, an empirical evidence from sub-Saharan African context shows that inclusive growth has a large and statistically significant positive impact on tax revenue mobilization through improving compliance of taxpayers and by broadening the tax base in support for the fiscal exchange theory and resource bargaining theories (Adeosun et al., 2025). In the case of resource-dependent economies, however, revenue instability is largely determined by changes in commodity prices and this highlights the need to have revenue sources that are diversified as well as viable non-oil tax bases (Kutu & Ohonba, 2024). In addition, FDI and openness of trade have contradictory effects on tax revenue for which weak institutional capacity may permit profit shifting and erode the tax base (Omodero & Yado, 2024).

Monetary and financial conditions are often cited as major factors affecting revenues. Some evidence from Sub-Saharan Africa suggests that the tax revenue can be influenced indirectly by monetary policy transmission, through private sector credit and liquidity conditions. Inadequate private credit supply limits business development and lowers taxable profit, which in turn undermines tax revenue (Omodero, 2024). The role of external financial flows in determining tax revenue outcomes is also important. Money transfers perhaps more than in any other area, the impact of remittances on tax revenues through indirect effects is quite evident in post-socialist countries. Household consumption financed through remittances increases the indirect tax base, while an increase in entrepreneurship helps the direct taxes despite that remittances are largely not taxed (Vusal & Zohrab, 2024).

Analysis of WAEMU countries shows that the increase in current expenditures, debt service and security spending leads to reduction in the fiscal space, which tends to curb the government’s room for mobilizing additional tax revenue. Broadening the tax base and bringing under-taxed sectors, such as agriculture, into the net of formal taxes are also recognized to be key elements in boosting revenue resilience (Dao et al., 2025). In addition, macroeconomic instability is detrimental to the tax effort. Empirical evidences from East African nations also show that exchange rate volatility has a negative and significant long-run impact on tax revenue expenditure because of the discouragement in investment, limitation of economic efficiency and reduction in consumption-based tax bases (Fisseha, 2025). Evidence from the Azerbaijani context also suggests that use of digital tax design and automation, focused reforms, technology deployment are vehicles to drive efficient revenue collection both in the short as well as long run while frequent shifts in laws sow legislation-related ambiguity and undermine revenue efficiency (Gazanfarli & Zhelev, 2025).

The performance of tax revenues in oil-dependent economies is significantly shaped by the size of the economy, diversification efforts, and structural vulnerabilities. Evidence from the Sultanate of Oman suggests that programs of economic activity and diversification have a positive impact on tax revenue, but inflation, foreign direct investment (FDI) inflows and the shadow economy have negative impacts through reducing compliance and depleting the tax base. These results underscore the budget risks related to an excessive dependence on natural resource rents and low non-oil taxation. Furthermore, the continuation of or informal economy routines gradually depresses tax revenue in a uniform manner among developing economies via reduction in taxable base and rise in enforcement costs (Maashani et al., 2025).

Firm-level analysis for Nigeria reveals that both domestic currency broad money and credit availability increase corporate tax revenue by encouraging business growth, while high lending rate and exchange rate volatility depress tax base and diminish efficiency in the administration of taxes. In addition, institutional and structural factors also condition tax effort. Speedy administration reforms, pro-active tax policy and stiff financial regulation create a surplus of revenue productivity by reducing the incidence of evasion and encouraging compliance while frequent legislation is against revenue efficiency (Omodero & Yado, 2025). Corroborative situations from Sub-Saharan Africa show that both inflation and FDI have mixed short- and long-run impact on tax revenue even as openness to trade and per capita income increase revenue capacity only under certain macroeconomic stability conditions (Omodero, 2025). In addition, more provocatively, political uncertainty is another restraint on tax collection. For example, the factual facts of Türkiye clearly indicate that economic policy uncertainty has a significant effect on decreasing tax revenues by affecting investment decisions, taking prohibitive actions and simulations to avoid taxes as well as weakening production activities. Tax revenues decline directly because of uncertainty, by reducing compliance and indirectly, via lower consumption, employment and corporate profitability (Tazegül et al., 2025).

Research on tax determinants has been performed in many countries and areas through qualitative and quantitative methods. However, there is no broad research on the factors of tax in Cambodia—to be precise, econometric works regarding taxation issues in Cambodia are still very scarce. From the above reviewed literature, it is clear that tax revenue is affected by economic and noneconomic determinants. However, this study deviates from previous ones as it focuses on the consumer price index, exchange rate, broad money aggregate and exports to tax revenue in Cambodia applying one of the most popular single equation econometric approaches, which is the ARDL model.

3. Methodology

The ARDL model exhibits a number of important properties that have contributed to its popularity in applied economic studies. One distinguishing feature is its capacity to estimate short-run and long-run relationships simultaneously in a single equation setting. The ARDL model is applicable whether the base series are both pure I(0), I(1), or mixed, provided none of them is an I(2) variable. It also works well with a small sample size and it allows each lag length to be optimal across variables that adds flexibility and robustness of the model in the empirical testing (Pesaran et al., 2001). Among the key aspects of the model, to achieve the purpose of this study in analyzing data, an ARDL model is used including short- and long-run model estimation. The following equations represent the ARDL models specification.

3.1. ARDL Model

The general ARDL(p, q1, q2, q3, q4) model is specified as follows:

where TAX is tax revenues, CPI is the consumer price index, FX is foreign exchange rate, M2 denotes broad money or money supply and EXPORT indicates the goods exports value. The coefficients of interest in the model are ; is an intercept and is a white noise error term. The lagged dependent variable is included to take account of the persistence in tax revenues. Moreover, the lagged response terms also reflected that consumer price index, exchange rate, broad money and exports could exert influence on tax revenues over time. In addition, all variables are log transformed (ln). It is worth highlighting that the first difference (Δ) of a time series whose values are in logarithms can be considered as its growth rate.

3.2. ARDL Bound Test Model

The ARDL model is re-parameterized to the unrestricted ECM for a long-run (cointegrating) relationship test, on which the bound test is built:

With respect to Equation (2), the null hypothesis (H0) and alternative hypothesis (H1) of the Bound test can be stated as follows:

With respect to the bounds test it should be mentioned that if F-statistic is lower than the lower bound, the null hypothesis of no long-run relationship would not be rejected. When the F-statistic exceeds the upper bound, however, it means that there is cointegration. The null hypothesis cannot be rejected if the F-statistic lies between the lower and upper bounds.

3.3. Short-Run Model

Once cointegration is established the short-run dynamics are estimated using the Error Correction Model (ECM):

where the error correction term (ECT) is as follows:

represents the speed of adjustment and is expected to be negative and significant.

3.4. Long-Run Model

The long-run equilibrium relationship between tax revenues and its determinants is as follows:

From the estimated ARDL model, the long-run coefficients are computed as follows:

3.5. Data and Data Analysis

This paper uses monthly time series data from January 2010 to May 2025. The consumer price index, exchange rate, broad money and exports are extracted from the International Financial Statistics data established by the International Monetary Fund. Tax revenue figures are also obtained from the Ministry of Economy and Finance in Cambodia.

The analysis of the data starts with descriptive statistics that consist of mean, median, standard deviation, minimum, and maximum values. Since the study uses time series data, the Augmented Dickey–Fuller (ADF) test will be carried out for all variables as a next step. If the time series data utilized in this investigation are I(0) or I(1) integrated process, then ARDL bounds test shall be used to investigate whether there exist a long-run relationship between tax revenue and its determinants. After cointegration detection, a short-run model estimate and a long-run model estimate are made. The last stage also includes the testing of hypotheses and the interpretation of findings.

4. Empirical Results

The data analysis is initiated with the descriptive statistics in order to obtain a preliminary understanding of characteristics, trends and distributions of variables included in the study. This is just a first step to get an overview over the data and spot potential outliers. Then, the ADF unit root test is performed on all the time series variables in order to investigate the data stationary properties and to eliminate spurious regression outcomes. After establishing the order of integration, ARDL Bounds testing is used to check if a long-run relationship exists between tax revenues, consumer price index, exchange rates, broad money supply, and exports. Eventually, short-run and long-run models are estimated paying special attention to hypothesis testing in order to consider the statistical relevance and also site the economic importance of the relations.

Descriptive statistics of the main variables in the analysis are shown in Table 1. The mean of the increase in tax revenues (∆lnTAX) is positive (1.181), reflecting a growth in tax revenues during the period studied; yet, the median negative result (–0.368) means that deceleration in tax revenue was more frequent than extreme increases. The high standard deviation (28.15) along with a broad range from minimum (–95.03) to the maximum (97.62) suggests that growth of tax revenues moved in wide variations over time. The inflation rate (∆lnCPI) has a mean value of 0.236 and median of 0.283, indicating relatively steady price increases. Its low standard deviation (0.531) and small range imply little in the way of variation in inflation. Moreover, the mean (–0.021) of changes in FX (∆lnFX) is moderately negative and its median value is zero, implying little long-term trend but some large short-run variations, as gauged by the standard deviation (0.514). Rate of change in broad money supply (∆lnM2) has a mean (1.458) and median (1.418) that are positive, suggesting continuous increase in real money stocks; however, the range between –12.64 and 16.624 suggests episodes of monetary contraction and rapid growth periods respectively throughout the period under review. Finally, mean growth of export (∆lnEXPORT) is positive (1.295), with a higher median value (1.988), but this strong variability is maybe much more evident for the mean and standard deviation values and range, because it did not show that much in terms to volatility around variation over time.

Table 1.

Descriptive statistics.

The ADF unit root test is applied to examine the stationarity characteristics of time series data under three model specifications, including with a constant term; with both a constant and trend terms; without a constant or trend terms. Table 2 reports the results of ADF tests. The findings suggest that the order of integration has mixed orders among the variables. The lnTAX is level stationary since the ADF statistic is significant at 5% in constant, implying an order of integration I(0). Likewise, the lnCPI is also found to be stationary at level when trend and constant are included with I(0) behavior. In addition, the lnEXPORT is also stationary at level for both constant and constant-with-trend definitions. Conversely, the lnFX and lnM2 are I(1), as the series have significant ADF statistics at first difference but not level. In addition, these ADF results suggest that the variables are integrated of mixed orders I(0) and I(1), where the ARDL bounds testing approach is further investigated.

Table 2.

ADF test.

Results of the ARDL bounds testing approach to cointegration employed to examine the existence of a long-run relationship among model variables are shown in Table 3 grouped as Panel A and Panel B. Panels A and B are respectively used to show the F-Statistics and W-Statistics and their corresponding critical bounds at 95% and 90 percent significance levels. The calculated F-Statistic of 28.185 is much greater than the upper bound critical values at either the 95% level (4.681) or 90% level (4.119). In the same way, the W-Statistic value of 140.925 is higher than the corresponding upper bound critical values at levels 95% and 90%. As both test statistics are higher than the corresponding upper critical values, we may strongly reject the null hypothesis of no long-run relationship between the series. These outcomes offer strong evidences of cointegration, thus confirming that there is a stable long-run equilibrium association between tax revenue, inflation, foreign exchange, broad money supply and exports. Accordingly, it is fitting that estimation of the long-run and error correction ARDL models can be pursued.

Table 3.

Bound test.

Estimated short-run dynamic coefficients and error correction term (ECT) results are shown under Panel A of Table 4, covering the transient effects of explanatory variables on tax revenue as well as the adjusting speed for long-term equilibrium. The short-run results show that the inflation (∆lnCPI) has a negative and statistically significant level of 10% influence in the tax revenue in the short-run, which means that prices increasing may temporarily decrease real tax receipts. Variations in the foreign exchange (∆lnFX) has a negative and very significant influence at 1%, which means that short-run devaluation of the exchange rate would negatively affect tax revenue. Broad money supply growth (∆lnM2) is, however, positive and highly significant; this implies that money expansion supports short run tax revenue growth. In addition, export growth (∆lnEXPORT) has a negative sign although it is not statistically significant, meaning that no significant short-run effect is seen. The negative and significantly high ECT coefficient (–0.8376) suggests a long-run stable relationship and adjusts for about 84% of short-run disequilibrium in each period. The model has already been found to be well-specified as indicated by the high F-statistic.

Table 4.

Empirical results based on ARDL model.

Panel B of Table 4 presents estimated long-run coefficients of the ARDL model which measures the lasting relationships between tax revenue and its main macroeconomic determinants. The lnCPI coefficient is positive (1.4048), indicating that a higher rate of inflation is linked to an increase in tax revenue in the long run. This finding implies that the relative price effect on nominal tax revenue due to inflation may be offset by policy responses, indexation rules or real responses. On the other hand, lnFX is negatively and highly significant (−9.9781) at 1% level, signaling a long-run negative impact of changes in exchange rate movements on tax revenue collection. This result suggests that the one consequence of currency depreciation could be erosion of the tax base due to lower quantities of taxed imports, lower real income activity, higher input prices, or greater uncertainty about economic conditions affecting taxes collected over time. The lnM2 exhibits a positive and statistically strong long-run coefficient, 1.9412, which suggests that monetary expansion has had an important role in sustaining the growth of tax revenues. A monetary expansion would presumably get the economic wheels moving through investment and consumption that increases an influx to the tax base and boosts government revenue in the long-run. The lnEXPORT is negative but not statistically significant, well suggesting that exports do not exert any significant long-run impact on tax revenue. This could be indicative of weak export tax bases, perhaps due to typical export tax exemptions, incentives or small export structures dominated by low-value-added products. The time trend variable is positive and significant, indicating a rising trend in tax revenue over time at the structural level. It follows from this that gains in economic development, institutional capacity building, tax administration and policy reforms had led to the continued rise in tax revenue beyond those of the macroeconomic variables alone. Lastly, the negative and highly significant constant accounts for the average level of tax collections in the cases where all other explanatory variables assumed zero values and thus lends further support to overall soundness and stability of our estimated long-run model.

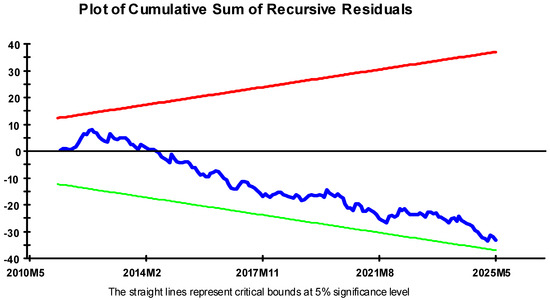

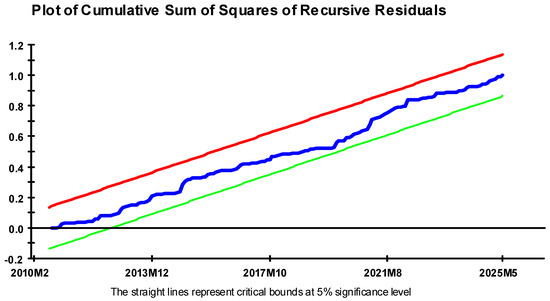

The diagnostic test statistics of the ARDL model to check the validity, stability, and overall fitness of estimated model are presented in Panel C of Table 4. The LM test on serial autocorrelation, which has a value level of 0.5562, is significantly higher than the commonly used thresholds for normal significance. This means that the null hypothesis of no serial correlation cannot be rejected, suggesting that residuals follow a zero-order serially uncorrelated process and the dynamic specification is correct. The Ramsey’s RESET test statistics is 0.4213, which suggests that there is no evidence of model specification error. This finding indicates that the ARDL model functional form is appropriately specified and no crucial nonlinear terms or missed variables exist. The LM heteroscedasticity test results indicate a value of 0.0340 (p-value = 0.854), suggesting that residuals are homoscedastic. This indicates that the error-term variance is constant over time, and that robust standard errors make valid statistical inferences. Furthermore it is observed that Cumulative Sum (CUSUM) and CUSUM of Squares (CUSUMQ) of recursive residuals tests also exhibit stability, which brings evidence that the estimated coefficients are stable at a given sample period without any such breakage (See Figure 1 and Figure 2). Finally, the high adjusted R2 of 0.8909 shows a good explanatory power of the model, suggesting that around 89% of tax revenue variation is explained by the model.

Figure 1.

CUSUM.

Figure 2.

CUSUMQ.

The short-run results indicate that inflation has negative influence on tax revenue, signaling to the fact that increasing levels of prices erode real purchasing power and deteriorate real tax bases in the short run. Similar short-term inflationary distortions to tax collection have been found in developing-country settings, where price volatility disrupts efficient tax administration and compliance (Maganya, 2020). However, the positive long-run inflation elasticity implies that outturns of nominal tax revenues ultimately increase with continuing price level increases, which is consistent with research showing that indexation provisions, fiscal drag and a lack of nominal bracket creep can offset some underlying inflationary erosion (Hassan et al., 2021). In addition, the empirical results of this research are consistent with results in the extant literature on macroeconomic determinants of tax revenue and feedstock market for both developing and emerging economies. In the short term, inflation has a negative and statistically significant effect on tax revenue; this implies that increases in prices erode real tax receipts for a while. This result is consistent with the findings of a negative short-run effect of inflation on tax collection due to lags in policy administration and erosion of real tax bases, more so for economies with significant absence of indexing mechanisms. There has also been short-run inflationary distortion in few Sub-Saharan African settings (Maashani et al., 2025).

Currency devaluation typically lowers the amount of imports, raises costs and slows real economic activity, thus in turn reducing the tax base. This result confirms the findings of previous studies for Sri Lanka and other developing countries, which suggested that exchange rate volatility erodes fiscal performance in the long-run (Vinayagathasan & Ranjith, 2021). It also lends credence to the assertion that exchange rate volatility leads to an uncertainty, which negatively impinges on revenue generation in long term (Maheswaranathan & Jeewanthi, 2021). More interestingly, due to the negative effects of exchange rate depreciation on import costs, trade volumes and domestic economic activity, its impact is generally to lower tax revenues. This result is in line with recent results for the East African countries, showing that exchange rate instability weakens tax collection achievement particularly in the long run. The large negative long-run coefficient on the exchange rate is consistent with the perspective that sustained currency devaluation undermines the tax base through decreased investment, compressed imports and higher macroeconomic uncertainty (Fisseha, 2025).

Monetary expansion is believed to boost economic activity by way of higher consumption and investment as well as more financial intermediation thus expanding the tax base. South African and Ghana have also reported comparable results as financial development and monetary expansion were found to contribute towards continuous increase in the growth of tax receipts. More interestingly, broad money has a strong positive and significant relationship with tax revenue in both the short run and the long run; this outcome is consistent with monetary transmission mechanisms and empirical evidence, suggesting that monetary expansion increases liquidity, spurs economic growth, and broadens the tax base through increased consumption and investment (Omodero, 2025). This is also confirmed in oil-exporting countries; moreover, money supply growth helps maintain fiscal capacity (Maashani et al., 2025).

In contrast, the lack of export significance in the short and long runs is also corroborated by research focusing on many developing countries, which finds that export incentives or exemptions, as well as low value-added exports make them contribute little to tax receipts. This trend has been unfolding in Indonesia and a number of other developing countries with few export tax bases (Safuan et al., 2022).

Moreover, the magnitude and sign of the error correction term support an existence of a long-run relationship as well a fast adjustment towards equilibrium, thus adding further credibility to the ARDL framework as has been reported in earlier empirical evidence (Sosvilla-Rivero & Rubio-Guerrero, 2022).

5. Concluding Remarks and Policy Implications

The objectives of this study are to analyze how the consumer price index, exchange rate, broad money supply and exports affect tax revenue in an ARDL approach to cointegration. The empirical results unambiguously reflect short-run and long-run dynamic interrelationships between macroeconomic variables and tax revenue. In the short term, inflation and exchange rate movements have negative effects on tax revenue, which means that price instability and currency fluctuations can lead to a temporary deterioration in the collection of real taxes. On the other hand, broad money supply has a positive and significant impact on tax revenue in the short run, which relates to the effect of liquidity and economic activities on enlarging the tax base. The error correction term also signals a clear and robust long-run equilibrium with a high speed of adjustment, which suggests that discrepancies to the long-run tax revenue trend are quickly eliminated. In the long term, the findings show exchange rate depreciation to be significantly negative for tax revenue, while broad money continues to support revenue growth. Both inflation and exports, however, do not present statistically significant long-run effects, indicating that their impact on tax revenue is short-lived or structurally weak. The estimated significance of the trend variable underlines those structural factors (economic development, institutional improvements or reforms in tax administration) that sustain long-term growth of aggregate tax revenues are here at play. In general, the results indicate how responsive tax revenue is to macroeconomic stability and monetary circumstance.

There are some policy implications following from the empirical findings. The first is that policymakers should focus on exchange rate stability since short-run and long-run evidence seems to point towards the conclusion that tax revenue will be highly eroded by currency depreciation. In the same vein, when it comes to exchange rate stabilization and tax base protection, the policies should aim a stronger foreign exchange reserve position; export diversification efforts; and greater macroeconomic credibility. These attributes may help in dampening the volatility of the exchange rate. Second, policies should avoid the mistake of hurting economic growth in order to squash inflation. The positive and significant impact of broad money further indicates that coordinated monetary expansion can be an impetus to economic activity, while having higher tax collection. However, any increase must be consistent with productivity growth, to avoid inflationary pressures which are likely to cut real tax receipts in the short term. Third, the low and ambiguous effect of exports on tax revenue has serious implications for reforming structure of the export sector. Policymakers can expand the export tax base, reduce excessive exemptions and increase the contribution of exports to government revenue by encouraging value-added exports. Last but not least, investment should also be sustained in tax administration reform, institutional capacity building and economic diversification. The positive trend effect demonstrates that long-term reforms in governance, compliance and economic structure are key to the sustainability of tax revenue growth. Building such structural foundations will help make the tax system and revenue more robust under macroeconomic shocks, thereby promoting fiscal sustainability over time.

Author Contributions

Conceptualization, R.E. and S.L.; methodology, R.E. and S.L.; software, R.E. and S.L.; validation, R.E. and S.L.; formal analysis, R.E. and S.L.; investigation, R.E.; resources, R.E.; data curation, R.E. and S.L.; writing—original draft preparation, R.E. and S.L.; writing—review and editing, R.E.; visualization, R.E.; supervision, R.E.; project administration, R.E.; funding acquisition, R.E. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by CamEd Business School grant number CamEd-2026 and The APC was funded by CamEd Business School.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Dataset available on request from the authors.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abidar, B., Ed-Dafali, S., & Kobiyh, M. (2025). Determinants of value-added tax revenue transfers in municipalities of emerging economies. Economies, 13(5), 117. [Google Scholar] [CrossRef]

- Adeosun, O. A., Olomola, P. A., Adedokun, A., & Tabash, M. I. (2025). Examining the relationship between inclusive growth and tax revenue mobilization: Additional evidence from sub-Saharan African countries. African Journal of Economic and Management Studies, 16(2), 219–236. [Google Scholar] [CrossRef]

- Bayer, O. (2015). Relevance of input data time series for tax revenue forecasting. Procedia Economics and Finance, 25, 518–529. [Google Scholar] [CrossRef][Green Version]

- Chamisa, M. G., & Sunde, T. (2024). Key determinants of tax revenue in Zimbabwe: Assessment using autoregressive distributed lag (ARDL) approach. Cogent Economics & Finance, 12(1), 2386130. [Google Scholar] [CrossRef]

- Chandia, K. E., Iqbal, M. B., Aziz, S., Gul, I., & Sarwar, B. (2022). An analysis of the management of fiscal deficit of Pakistan: An econometric study of auto-regressive distributive lags (ARDL) approach. The Singapore Economic Review, 67(02), 655–684. [Google Scholar] [CrossRef]

- Chettri, K. K., Bhattarai, J. K., & Gautam, R. (2023). Determinants of tax revenue in South Asian countries. Global Business Review, 09721509231177784. [Google Scholar] [CrossRef]

- Dao, A., Ouedraogo, I. M., Ondo Ossa, A., & Diarra, M. (2025). Determinants of the fiscal space of WAEMU member countries. Cogent Economics & Finance, 13(1), 2584517. [Google Scholar] [CrossRef]

- Darshini, J. S., & Gayithri, K. (2023). An econometric analysis of revenue diversification among selected Indian states. South Asia Economic Journal, 24(1), 41–63. [Google Scholar] [CrossRef]

- Fisseha, F. L. (2025). Exchange rate volatility and tax revenue: Empirical evidence from east African countries. Studies in Economics and Econometrics, 1–22. [Google Scholar] [CrossRef]

- Garg, S., Narwal, K. P., & Kumar, S. (2024). Building the empirical puzzle on impact of macroeconomic determinants on GST revenue: An empirical investigation via ARDL bound test perspective. Journal of Public Affairs, 24(3), e2947. [Google Scholar] [CrossRef]

- Gazanfarli, M., & Zhelev, Z. (2025). Dynamic modeling the impact of tax reforms on tax revenue: Evidence from Azerbaijan. Journal of International Studies, 18(1), 99–115. [Google Scholar] [CrossRef]

- Hassan, M. S., Mahmood, H., Tahir, M. N., Yousef Alkhateeb, T. T., & Wajid, A. (2021). Governance: A source to increase tax revenue in Pakistan. Complexity, 2021(1), 6663536. [Google Scholar] [CrossRef]

- Ibrahim, A. J., & Jairo, I. J. (2023). Determinants of tax revenue performance in the East African countries. African Journal of Economic Review, 11(2), 55–73. [Google Scholar]

- Jemiluyi, O. O., & Jeke, L. (2023). Foreign direct investment and tax revenue mobilization in South Africa: An ARDL bound testing approach. Development Studies Research, 10(1), 2197156. [Google Scholar] [CrossRef]

- Kamasa, K., Nortey, D. N., Boateng, F., & Bonuedi, I. (2025). Impact of tax reforms on revenue mobilisation in developing economies: Empirical evidence from Ghana. Journal of Economic and Administrative Sciences, 41(1), 1–15. [Google Scholar] [CrossRef]

- Kebede, T. N., Erena, O. T., & Bawiso, E. P. (2024). Determinants of tax revenue: A cointegration and causality analysis for Ethiopia, 1992–2022. Journal of Tax Reform, 10(3), 493–509. [Google Scholar] [CrossRef]

- Kutu, A. A., & Ohonba, A. (2024). The impact of crude oil price fluctuation on revenue generation in the oil dependent economy: Nigeria. International Journal of Energy Economics and Policy, 14(5), 181–190. [Google Scholar] [CrossRef]

- Lentner, C., Hegedűs, S., & Nagy, V. (2022). Correlations of taxation and macroeconomic indicators in the OECD member countries from 2014 to the first year of the crisis caused by COVID-19. Journal of Risk and Financial Management, 15(10), 464. [Google Scholar] [CrossRef]

- Maashani, S. S. S., Gamal, A. A. M., Shaarani, A. Z., Rambeli, N., & Zulkifli, N. (2025). The role of specific macroeconomic factors on tax revenue policy in an oil-dependent economy: Evidence from Oman. Review of Economics and Political Science, 11(1), 60–78. [Google Scholar] [CrossRef]

- Maganya, M. H. (2020). Tax revenue and economic growth in developing country: An autoregressive distribution lags approach. Central European Economic Journal, 7(54), 205–217. [Google Scholar] [CrossRef]

- Maheswaranathan, S., & Jeewanthi, K. M. N. (2021). Empirical investigation of the influence of fiscal policy on Sri Lankas economic growth from 1990 to 2019. Asian Journal of Economic Modelling, 9(2), 122–131. [Google Scholar] [CrossRef]

- Mapunda, M., Kira, A. R., & Ngomuo, S. (2023). Does service sector growth influence tax revenue in Tanzania? Cogent Business & Management, 10(3), 2259615. [Google Scholar] [CrossRef]

- Maryantika, D. D., & Wijaya, S. (2022). Determinants of tax revenue in Indonesia with economic growth as a mediation variable. JPPI (Jurnal Penelitian Pendidikan Indonesia), 8(2), 450–465. [Google Scholar] [CrossRef]

- Mawejje, J., & Odhiambo, N. M. (2022). The determinants and cyclicality of fiscal policy: Empirical evidence from East Africa. International Economics, 169, 55–70. [Google Scholar] [CrossRef]

- Mirović, V., Kalaš, B., Milenković, N., & Andrašić, J. (2023). Different modelling approaches of tax revenue performance: The case of Baltic countries. E+ M Ekonomie a Management, 26, 20–32. [Google Scholar] [CrossRef]

- Mukhtarov, S., Alalawneh, M. M., Azizov, M., & Jabiyev, F. (2020). The impact of monetary policy and tax revenues on foreign direct investment inflows: An empirical study on Jordan. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 68(6), 1011–1018. [Google Scholar] [CrossRef]

- Omodero, C. O. (2024). Central bank financial policy mechanism and taxation earning in Sub-Saharan Africa. Ekonomika, 103(4), 112–128. [Google Scholar] [CrossRef]

- Omodero, C. O. (2025). Monetary and macroeconomic determinants of tax revenue in Sub-Saharan Africa. Ekonomika, 104(3), 6–22. [Google Scholar] [CrossRef]

- Omodero, C. O., & Yado, J. L. (2024). Effects of foreign direct investment and trade openness on tax earnings: A study of selected Sub-Saharan African economies. Economies, 12(12), 342. [Google Scholar] [CrossRef]

- Omodero, C. O., & Yado, J. L. (2025). Financial policies and corporate income tax administration in Nigeria. International Journal of Financial Studies, 13(2), 52. [Google Scholar] [CrossRef]

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. [Google Scholar] [CrossRef]

- Phiri, A., & Mbaleki, C. (2022). Fiscal expenditures, revenues and labour productivity in South Africa. Cogent Economics & Finance, 10(1), 2062912. [Google Scholar] [CrossRef]

- Safuan, S., Habibullah, M. S., & Sugandi, E. A. (2022). Eradicating tax evasion in Indonesia through financial sector development. Cogent Economics & Finance, 10(1), 2114167. [Google Scholar] [CrossRef]

- Sosvilla-Rivero, S., & Rubio-Guerrero, J. J. (2022). The economic effects of fiscal policy: Further evidence for Spain. The Quarterly Review of Economics and Finance, 86, 305–313. [Google Scholar] [CrossRef]

- Streimikiene, D., Rizwan Raheem, A., Vveinhardt, J., Pervaiz Ghauri, S., & Zahid, S. (2018). Forecasting tax revenues using time series techniques—A case of Pakistan. Economic Research-Ekonomska Istraživanja, 31(1), 722–754. [Google Scholar] [CrossRef]

- Tazegül, S., Yılmaz, T., Aslantaş, M. F., & Çapanoğlu, M. F. (2025). Türkiye’de ekonomik politika belirsizliği ve vergi gelirleri arasindaki ilişki: DOLS, FMOLS ve CCR zaman serisi eşbütünleşme yaklaşimi. Sosyoekonomi, 33(64), 471–492. [Google Scholar] [CrossRef]

- Tolossa, G., & Melese, W. E. (2024). Revisiting determinants of tax revenue mobilization in Sub-Saharan African countries: Does e-government matter? Cogent Social Sciences, 10(1), 2399937. [Google Scholar] [CrossRef]

- Ulvidienė, E., Meškauskaitė, I., Stavytskyy, A., & Giedraitis, V. R. (2023). An investigation of the influence of economic growth on taxes in Lithuania. Ekonomika, 102(1), 41–59. [Google Scholar] [CrossRef]

- Vinayagathasan, T., & Ranjith, J. G. S. (2021). Public debt, budget deficit and tax policy reforms for fiscal consolidation in Sri Lanka: Rationale and feasibility. Sri Lanka Journal of Social Sciences, 44(1), 97–109. [Google Scholar] [CrossRef]

- Vusal, A., & Zohrab, P. (2024). Money transfers and tax revenue in post-socialist countries: Evidence from the panel ARDL model. Regional Science Policy & Practice, 16(5), 100016. [Google Scholar] [CrossRef]

- Wang, Y. K. (2022). Measuring the tax revenue and tax base erosion: Evidence from Taiwan. Journal of Development Economics and Finance, 3(2), 437–452. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.