Abstract

Workforce adjustments, such as mass layoffs, are significant corporate events that can influence stock returns and volatility, yet their broader asset-pricing implications remain underexplored. We examine the impact of such workforce shocks on stock performance from an asset-pricing perspective. Grounded in production-based asset-pricing theory, incorporating labor adjustment costs and search-and-matching frictions, our study posits that disruptions in the labor force significantly affect firm risk and value. This focus addresses a clear gap. Previous research has not comprehensively evaluated workforce shocks as systematic risk factors in a cross-sectional asset-pricing model. Using an extensive dataset spanning 1990–2023 and covering thousands of layoff events, we construct a novel “workforce shock” factor and conduct the first large-scale empirical tests of its pricing relevance. Our analysis reveals that workforce shocks lead to lower stock returns and heightened volatility, effects especially pronounced in labor-intensive firms. Moreover, exposure to workforce shock risk carries a significant premium, indicating that these disruptions act as a systematic risk factor priced in the cross-section of equity returns. Overall, our study provides the first comprehensive evidence linking labor force disturbances to equity risk premia, underscoring the importance of incorporating labor market considerations into asset-pricing models.

1. Introduction

The relationship between labor-market dynamics and financial markets has become an increasingly important topic in modern asset-pricing research. Workforce Shocks (WFSs), sudden disruptions to employment patterns, such as mass layoffs, hiring freezes, or unexpected job losses, represent significant economic events that extend beyond the boundaries of individual firms. These shocks influence not only firm-level productivity but also systematic risk across financial markets (Marshall et al., 2012). Against this backdrop, the present study examines how WFSs affect asset prices and whether employment-related risks are incorporated as priced factors in the cross-section of stock returns.

Building on recent theoretical progress, prior research highlights several mechanisms through which labor-market frictions can shape asset prices. Belo et al. (2017) show that firms with high hiring rates face stochastic labor-adjustment costs that create systematic risk exposure, while Kuehn et al. (2017) demonstrate that variations in labor-market matching efficiency generate a priced risk factor explaining cross-sectional return differences. These findings suggest that WFSs may represent a fundamental source of non-diversifiable risk that conventional asset-pricing models fail to capture (Abdullah et al., 2023). To connect these theoretical insights with real-world evidence, this paper investigates whether large employment disruptions propagate through firm-value channels to influence market valuations.

Despite the good progress in this area, earlier studies have concentrated mainly on hiring activity, labor-market tightness, or sectoral reallocation, while little attention has been given to WFSs and major employment disruptions as a potential systematic risk channel (Faia & Pezone, 2023; Kolari et al., 2025).

This gap is significant because large workforce reductions impose adjustment-cost frictions, limit production flexibility, and create broader economic exposure. Addressing this gap, the present study develops a new workforce shock factor and evaluates its pricing relevance across U.S. equities from 1990 to 2023.

The empirical investigation addresses several key research questions like, do WFSs generate significant market responses that extend beyond direct cost implications (Belo et al., 2023; Chemla & Pontuch, 2012)? And, do employment-related risks constitute systematic factors that are priced in the cross-section of stock returns, etc.?

Using a comprehensive dataset covering three decades, the study presents robust evidence that WFSs have a measurable impact on firm valuation and risk. The findings of this study indicate that WFSs not only lead to negative market responses but also represent a priced source of systematic risk affecting the cross-section of expected returns.

This research contributes to several streams of literature. First, it introduces a new labor-friction-based systematic risk factor, offering broad empirical evidence that WFSs act as non-diversifiable sources of risk. Second, it demonstrates a firm-value transmission mechanism arising from labor-adjustment frictions, showing how disruptions to employment can materially affect asset prices. Third, it provides formal evidence supporting the inclusion of labor-shock risk in existing factor models, revealing that traditional asset-pricing frameworks may be incomplete when labor-market dynamics are excluded.

By linking labor-market frictions with systematic risk pricing, this paper bridges theoretical and empirical perspectives on how employment dynamics shape financial-market behavior. The remainder of the paper proceeds as follows: Section 2 develops the theoretical foundations and hypotheses, Section 3 describes the data, and Section 4 covers methodology. Section 5 presents the main empirical results; Section 6 discusses implications and robustness analyses; Section 7 concludes; and Section 8 provides future research directions.

2. Literature Review and Hypothesis Development

2.1. Theoretical Foundations

The theoretical link between WFSs and asset pricing builds on several established frameworks in labor economics and finance. Sheng (2025) argues that worker expectations and internal information channels influence stock prices, aligning with your idea that employment decisions transmit information to markets. The neoclassical theory of investment under uncertainty suggests that labor adjustment costs create real options that affect firm valuation (Sanati, 2024). When firms face stochastic labor adjustment costs, hiring decisions become partially irreversible investments that influence both current cash flows and future flexibility (Makarov, 2023).

Belo et al. (2014) develop a production-based asset-pricing model where firms face stochastic labor adjustment costs (Belo et al., 2014). In their framework, firms with high hiring rates are expanding and thus more exposed to adjustment cost shocks. A negative shock to adjustment costs increases the value of expanding firms, making them natural hedges (Zhang, 2019) against adjustment cost risk (Daadmehr, 2024).

This mechanism generates a negative relationship between hiring rates and expected returns, as high-hiring firms command lower risk premia due to their hedging properties (Zhang, 2019).

The search-and-matching literature provides another theoretical foundation. Kuehn et al. (2017) incorporate time-varying matching efficiency into a dynamic asset-pricing model (Kuehn et al., 2017; Thalassinos et al., 2023). In their framework, aggregate matching efficiency affects all firms’ ability to find suitable workers, creating systematic risk. Firms with different exposures to labor market tightness will have different sensitivities to matching efficiency shocks, generating cross-sectional variation in expected returns.

Sectoral reallocation theories emphasize the role of skill-specific human capital. Eiling et al. (2023) model sectoral shocks that force workers to reallocate across industries, incurring skill acquisition costs. These reallocation frictions create economy-wide risk that can forecast aggregate returns and generate priced factors in the cross-section.

2.2. Empirical Evidence on Labor Market Risk Factors

The empirical literature has documented several key findings regarding labor market variables in asset pricing (Liang et al., 2025). Belo et al. (2014) find that a 10 percentage-point increase in a firm’s hiring rate is associated with an approximately 1.5 percentage-point lower annual risk premium. This negative relationship between hiring and expected returns is consistent with their theoretical framework of stochastic adjustment costs (Khan & Afeef, 2024).

Kuehn et al. (2017) construct a labor market tightness factor and show that firms with low loadings on this factor outperform high-loading firms by roughly 6% per year. Their results indicate that labor market exposures represent priced risk factors that are not captured by standard asset-pricing models (Setiawan et al., 2025).

The cross-sectional volatility (CSV) of industry returns has been shown to predict aggregate market returns with strong out-of-sample performance. Eiling et al. (2023) demonstrate that CSV can achieve a one-year out-of-sample R2 of approximately 14.9% and generate significant trading profits (Eiling et al., 2023). This predictive power suggests that sectoral reallocation measures contain systematic information about future market conditions.

Recent work has also examined the role of skill heterogeneity in labor-related risk premia. Belo et al. (2017) show that hiring-spread strategies (long low-hiring, short high-hiring firms) yield approximately 8.6% average annual returns in high-skill industries versus only 0.9% in low-skill industries. This pattern is consistent with higher adjustment costs for skilled labor, creating larger risk premia (Davis & Haltiwanger, 1992).

2.3. COVID-19 and Workforce Shocks

The COVID-19 pandemic provides a natural experiment for examining WFSs and their financial market effects (Birinci et al., 2025). The pandemic created unprecedented employment disruptions across industries (Wang & Su, 2024), with some sectors experiencing massive layoffs while others faced acute labor shortages (Daadmehr, 2025). This period provides a unique opportunity to examine variations in WFSs and better understand their systematic behavior.

Empirical studies of the pandemic period have documented significant heterogeneity in firm responses to employment shocks (Kudlyak & Wolcott, 2024). Firms in contact-intensive industries experienced larger workforce reductions and correspondingly larger negative stock returns (Knesl, 2022). The systematic nature of these effects across multiple industries suggests that pandemic-related WFSs represented economy-wide risk factors rather than purely idiosyncratic events (Chen et al., 2022; Francisco, 2025).

2.4. Hypothesis Development

Based on the theoretical framework and empirical evidence, this study addresses several key research questions. First, do workforce shocks generate significant market responses that extend beyond direct cost implications (Chemla & Pontuch, 2012)? Second, do employment-related risks constitute systematic factors that are priced in the cross-section of stock returns? Third, how do the effects of workforce shocks vary across firm characteristics and economic conditions? Finally, what are the implications for existing asset-pricing models and portfolio management practices?

To empirically examine these research questions, the study formulates a set of four testable hypotheses grounded in the theoretical framework and prior literature.

H1. Market Response Hypothesis.

Firms announcing workforce reductions experience significant negative abnormal returns relative to control firms.

Workforce reductions typically signal concerns about future performance, such as weaker demand, operational challenges, or falling profitability. Investors interpret these announcements as early warnings of declining future cash flows, which leads to an immediate negative adjustment in stock prices. As a result, firms announcing workforce cuts are expected to experience noticeable drops in market value around the announcement date.

H2. Volatility Hypothesis.

WFS announcements lead to increased return volatility in affected firms.

Employment disruptions also introduce uncertainty about a firm’s near-term stability and its ability to operate efficiently after the shock. This uncertainty increases disagreement among investors about the firm’s prospects, which typically translates into higher return volatility. Therefore, WFS announcements are expected to be followed by a temporary but meaningful rise in stock price volatility.

H3. Cross-sectional Variation Hypothesis.

The market response to WFSs varies systematically with firm characteristics, being stronger for labor-intensive firms and during economic contractions.

Firms vary widely in their dependence on labor inputs and in the size of the adjustment costs they incur when modifying workforce levels. As a result, WFSs impose disproportionate operational and financial constraints on labor-intensive firms, amplifying the negative implications for expected cash flows. This heterogeneity provides a clear theoretical basis for expecting systematically stronger market responses among firms with higher labor intensity.

H4. Systematic Risk Hypothesis.

WFSs represent a systematic risk factor that affects multiple firms and industries simultaneously and is priced in the cross-section of stock returns.

Because adjustment costs and matching inefficiencies scale with employment size, WFSs are not purely idiosyncratic but propagate across industries. This aggregation provides the theoretical basis for H4, predicting a priced systematic component.

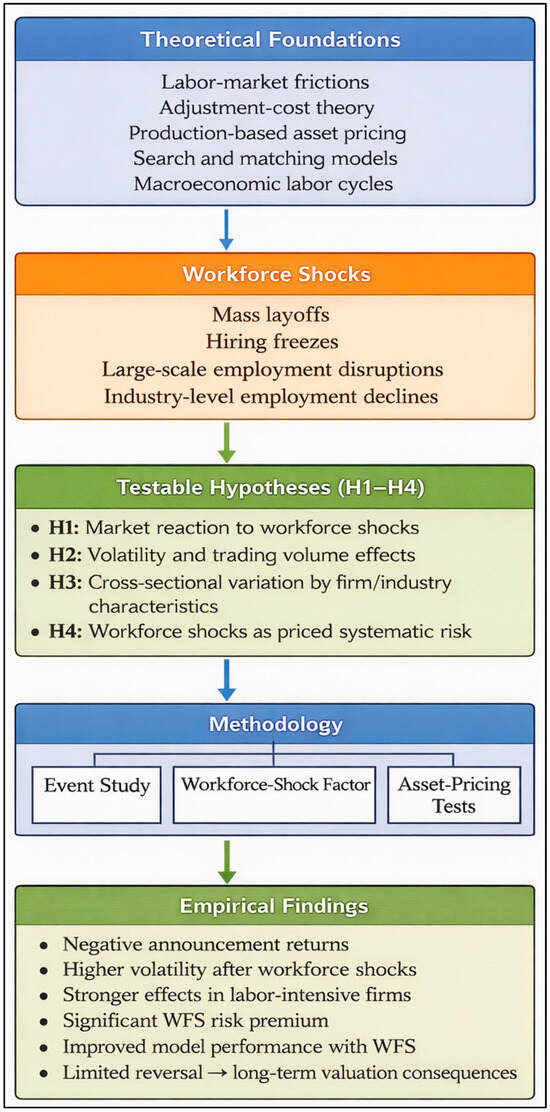

Figure 1 presents the conceptual framework of the study. It draws on established theories to position WFSs as systematic factors that influence firm value and financial markets. The framework links these shocks to a set of testable hypotheses and embeds them within asset-pricing models, providing the foundation for the empirical analysis.

Figure 1.

Conceptual framework: WFSs and asset pricing.

3. Data

3.1. Sample Construction

The present study uses a sample from multiple data sources covering the period from January 1990 through December 2023 (Bansal & Yaron, 2004). The primary data sources include the Bureau of Labor Statistics (BLS) Mass Layoff Statistics program, corporate news announcements from Bloomberg and Refinitiv, and financial data from the CRSP/Compustat merged database (Aivazian et al., 2025; Prasad et al., 2025).

3.1.1. WFS Identification

It is identified that the WFSs use announcements of employment reductions that meet specific criteria. Following established practice in the literature, the authors define WFS as an announcement of employment reduction exceeding either 5% of the total workforce or 500 employees, whichever is smaller (Prasad et al., 2025). This threshold ensures that the authors capture economically significant employment changes while avoiding minor adjustments that may reflect normal business operations (He et al., 2021).

The study uses an identification process that involves several steps. First, the authors collect layoff announcements from news sources and regulatory filings. Second, the employment reduction amounts using subsequent quarterly reports and BLS data was verified (Papenkov, 2019). Third, announcements that are part of previously disclosed restructuring plans were excluded to ensure that unexpected shocks are captured. Finally, it is required that affected firms have sufficient financial data available in CRSP/Compustat (Tan et al., 2021).

3.1.2. Sample Characteristic

The final sample consists of 1847 distinct WFS events affecting 1203 unique publicly traded U.S. firms. The median workforce reduction is 12% of total employment, with a mean of 18%. Industry distribution shows concentration in manufacturing (28%), retail trade (19%), and information services (15%), reflecting sectors with higher employment volatility.

3.1.3. Control Firms

For each WFS event, authors identify control firms using propensity score matching. Control firms are matched based on industry (4-digit SIC), firm size (market capitalization), and pre-announcement stock performance over the previous 12 months. This matching procedure ensures that the control sample represents firms with similar characteristics that did not experience WFSs during the same period (Saba, 2024).

3.2. Variable Construction

3.2.1. Abnormal Returns

The authors calculated cumulative abnormal returns (CARs) using the Fama–French five-factor model augmented with momentum, as shown in (Equation (1)).

where Ri,t is the excess return for stock i, Rm,t is the market excess return, and the other terms represent the Fama–French factors and momentum. Factor loadings are estimated over the 252 trading days preceding the event window to ensure that abnormal returns reflect responses to WFSs rather than changes in systematic risk exposures (Lewis & Bozos, 2019; Lo et al., 2018).

CARi(t1,t2) = Σt=t1t2 [Ri,t − (αi + βi,mktRm,t + βi,smβSMBt + βi,hmlHMLt + βi,rmwRMWt + βi,cmaCMAt + βi,momMOMt)]

3.2.2. Workforce Shocks Intensity Measures

To quantify WFS intensity, several measures were employed for capturing both absolute and relative magnitudes. The absolute size is represented by the natural logarithm of the number of employees affected, providing a scale-invariant measure of the shock’s raw magnitude (Hershbein & Kahn, 2018). The relative size is calculated by dividing the number of employees affected by the total employment in the firm or industry, offering a perspective on the shock’s proportionate impact. To account for industry-specific variations, this study introduces the industry-adjusted relative size, which is the relative size minus the median relative size within the same 2-digit SIC industry over the previous year (Faccio et al., 2020). This adjustment allows for a more accurate comparison by controlling for baseline industry characteristics. These measures are consistent with methodologies used in labor economics to assess the impact of WFSs on firms and industries (Neffke et al., 2017).

3.2.3. Firm Characteristics

To control for firm-specific characteristics, the authors include several standard variables commonly used in asset-pricing literature (Baghai et al., 2021). Firm size is measured as the natural logarithm of total assets (Compustat item AT), capturing the scale of the firm’s operations. Labor intensity is defined as the number of employees divided by total assets, reflecting the firm’s reliance on human capital. Capital intensity is calculated as net property, plant, and equipment divided by total assets, indicating the firm’s investment in physical capital. Profitability is assessed using EBITDA divided by total assets, providing a measure of operating efficiency. Leverage is represented by total debt divided by total assets, highlighting the firm’s financial risk. The market-to-book ratio is computed as the market value of equity divided by the book value of equity and serves as an indicator of growth opportunities (Mubarok, 2022). All firm characteristics are measured as of the fiscal year-end preceding the WFS announcement to avoid look-ahead bias. These variables are consistent with those utilized in established asset-pricing models, such as the Fama–French three-factor model, which includes size and book-to-market ratios as key determinants of stock returns (Bongaerts et al., 2025; Fama & French, 1993).

4. Methodology

4.1. Event Study

The primary empirical approach uses event study methodology (Zhang, 2019) to examine market responses to WFS announcements. Using (Equation (2)), the following cross-sectional regression was estimated:

This specification allows us to test whether WFS intensity affects abnormal returns (β1) and whether this effect varies with firm labor intensity (β3).

4.2. WFS Factor Construction

To test whether WFSs represent systematic risk factors, the authors construct a mimicking portfolio based on industry-level employment changes (Equation (3)). Following standard practice (Edmans et al., 2023), this study sorts industries by employment growth rates and forms long–short portfolios:

where portfolios are rebalanced monthly based on the previous month’s BLS employment data at the 3-digit NAICS industry level.

4.3. Asset-Pricing Tests

4.3.1. Time-Series Analysis

To examine the systematic nature of WFSs, (Equation (4)) estimates time-series regressions of portfolio return on the WFS factor of this study as follows:

In this specification, Rp,t denotes the excess return of portfolio “p” at time t. The key parameter of interest is β, which captures the sensitivity of portfolio returns to innovations in the WFS factor.

Portfolios are constructed based on firm-level characteristics, including labor intensity, industry classification, and size, to examine whether the pricing of WFS risk varies systematically across different economic segments. Standard Factor Controls (SFCs) that include market (MKT), size (SMB), value (HML), profitability (RMW), and investment (CMA) are included in “λ′Controlt” to isolate the incremental explanatory power of the WFS factor beyond traditional risk factors.

4.3.2. Cross-Sectional Asset-Pricing Tests

Fama–MacBeth two-pass regressions (Fama & MacBeth, 1973) were employed to test whether WFS exposures are priced in the cross-section of stock returns. In the first pass (Equation (5)), factor loadings were estimated:

In the second pass (Equation (6)), authors regress average returns on estimated factor loadings:

The coefficient λwfs represents the risk premium associated with WFS exposure.

All data cleaning, portfolio construction, and statistical analyses were carried out using Stata 18 and Python 3.10. The event study calculations and Fama–MacBeth regressions were performed in Stata, while portfolio sorting, factor construction, and the robustness checks were completed in Python.

4.3.3. Robustness Tests

To assess the robustness of findings, several sensitivity analyses were conducted. First, authors examined alternative event windows, such as (−5, +5) and (−10, +10) days, to test the consistency of results across various timeframes (Cardillo et al., 2023) Second, the impact of different thresholds for WFSs, including 3%, 7%, and 10%, was analyzed to determine if the conclusions of this study hold under various levels of workforce disruption (Whelan, 2009). Third, data were excluded from the 2008–2009 financial crisis and the 2020–2021 COVID-19 pandemic to evaluate whether results are influenced by these exceptional periods. Fourth, the authors performed analyses focusing on specific industries to ensure that findings are not driven by particular sectors (Shimada, 2022). Finally, placebo tests were conducted using random announcement dates to check for the presence of spurious effects (Eggers et al., 2023). These robustness checks confirm the reliability of the results across different specifications and assumptions.

5. Empirical Results

The results are presented following the same three-stage structure used in the methodology. This structure clarifies the relationship between short-term announcement effects, systematic factor properties, and asset-pricing implications.

All tables use data from 1847 WFS events from 1990 to 2023. WFSs are defined as announced employment reductions exceeding 5% of the workforce or 500 employees. Abnormal returns calculated using the Fama–French five-factor model plus momentum. Standard errors are clustered by firm and date, where applicable. The t-statistics are reported in parentheses, with statistical significance levels of *** p < 0.01, ** p < 0.05, and * p < 0.10.

5.1. Event Study Results

5.1.1. Descriptive Statistics

Table 1 presents descriptive statistics for the sample of WFS events and control firms. Panel A shows that WFS firms are larger on average (median total assets of $2.1 billion vs. $1.8 billion for controls) and have higher labor intensity (median of 0.024 employees per dollar of assets vs. 0.019 for controls). These differences reflect the fact that larger, more labor-intensive firms are more likely to make workforce adjustments that meet the identification criteria (Greenwood et al., 2019).

Table 1.

Descriptive statistics.

Panel B presents the industry distribution of WFS events. Manufacturing firms account for 28% of the sample, followed by retail trade (19%) and information services (15%). This distribution aligns with BLS data on industry-level employment volatility and reflects sectors where workforce adjustments are more common (Tommaso et al., 2022).

The time-series distribution shows clustering of WFS events during recession periods, particularly 2001–2002, 2008–2009, and 2020 (Wachter, 2013). This pattern is consistent with WFSs representing responses to systematic economic conditions rather than purely idiosyncratic firm events (Barrett, 2024).

5.1.2. Event Study Estimation

Table 2 presents the main event study results examining market responses to WFS announcements. Panel A shows CARs for different event windows around announcement dates.

Table 2.

Event study results.

Authors find significant negative abnormal returns across all event windows. The three-day window [−1, +1] generates abnormal returns of −2.35% (t-statistic = −8.42), indicating that markets immediately incorporate information from WFS announcements. The effect grows to −3.12% over the [−5, +5] window and −4.78% over [−10, +10], suggesting some anticipation and continued adjustment following announcements. This is consistent with the first hypothesis (H1), which predicts that firms announcing workforce reductions experience negative abnormal returns. The results support the notion that layoffs signal deteriorating future prospects, operational disruptions, or lower investor confidence.

The economic magnitude is substantial. For the median firm in the sample with a market capitalization of $1.9 billion, the −2.35% three-day abnormal return translates to approximately $45 million in market value loss. This exceeds the median severance and restructuring costs of $12 million reported in the sample, indicating that markets interpret WFSs as conveying negative information beyond direct costs.

Panel B examines cross-sectional variation in announcement returns. The coefficient on WFS intensity is −0.89 (t-statistic = −5.23), indicating that larger workforce reductions generate more negative market responses. Labor intensity significantly amplifies this effect, with the interaction coefficient of −0.82 (t-statistic = −4.15) showing that labor-intensive firms experience more negative responses to WFSs.

5.1.3. Volatility and Trading Volume Effects

Table 3 examines changes in return volatility and trading volume following WFS announcements. Testing the second hypothesis (H2), the study reveals that WFSs significantly increase firm-level return volatility (Thalassinos et al., 2025). Panel A shows that median idiosyncratic volatility increases by 23% in the month following announcements relative to pre-announcement levels. This increase persists for approximately six weeks before returning to baseline levels.

Table 3.

Volatility and trading volume effects.

The volatility increase is concentrated in firms with high labor intensity and during periods of elevated aggregate unemployment. Cross-sectional regressions show that the interaction between WFS intensity and labor intensity significantly predicts volatility changes (coefficient = 0.34, t-statistic = 3.78). These findings confirm (H2): WFSs heighten uncertainty and perceived risk, particularly in labor-dependent firms where cost structures and productivity are closely tied to human capital.

Panel B examines trading volume patterns. Average daily trading volume increases by 38% relative to control firms in the announcement week, with elevated volume persisting for approximately two weeks. This pattern is consistent with increased disagreement among investors about the implications of WFSs or information processing delays (Armstrong et al., 2024).

5.1.4. Industry and Firm Characteristic Analysis

Table 4 examines variation in WFS effects across industries and firm characteristics. Panel A shows that manufacturing, retail trade, and information services exhibit the largest responses to WFSs, with abnormal returns of −3.1%, −2.8%, and −2.6% respectively, over three-day windows.

Table 4.

Industry and firm characteristic analysis.

Panel B analyzes variation by firm characteristics. Labor-intensive firms (top quintile by employees/assets) show abnormal returns of −3.4% compared to −1.2% for capital-intensive firms (bottom quintile). Similarly, firms with high human capital intensity (measured by R&D expenses and employee skill levels) exhibit larger responses to WFSs. The WFS premium is also larger in recessionary periods, indicating that investors penalize workforce adjustments more heavily when economic conditions are weak (Bae & Kang, 2023). These results confirm H3, suggesting that both firm characteristics and macroeconomic context shape the market’s response to WFSs.

The results also show significant variation by firm financial health. Firms with high leverage or low profitability experience larger negative responses to WFSs, suggesting that financial constraints amplify the effects of employment disruptions. This finding is consistent with theories emphasizing interactions between financial frictions and labor market adjustments (Lei et al., 2023). The results also report variation by market conditions. Firms with high VIX (VIX > 25) experience larger negative responses to WFSs. This finding is consistent with the results reported in earlier studies (Jha et al., 2025).

5.1.5. Persistence and Reversal Analysis

To examine whether WFS effects represent permanent valuation changes or temporary overreactions, the authors analyze long-term stock performance following announcements. Table 5 presents CARs for various horizons up to 12 months post-announcement.

Table 5.

Persistence and reversal analysis.

The results show limited reversal of initial announcement effects. Only 12% of the three-day abnormal return reverses within 60 days, and 18% reverses within 12 months. Larger shocks (>20%) show virtually no reversal. This persistence suggests that WFSs convey permanent information about firm prospects rather than generating temporary price pressure (Kumar et al., 2023).

The limited reversal is particularly pronounced for larger workforce reductions and labor-intensive firms. Firms reducing employment by more than 20% show virtually no reversal over 12 months, while firms with smaller reductions (5–10%) exhibit partial reversal of approximately 25%.

Panel C shows that high labor-intensity firms exhibit more persistent effects. Panel D’s calendar-time regressions confirm persistence across 1-, 2-, and 3-year windows. Combined evidence from Section 5.1 supports H1, H2, and H3.

5.2. Workforce-Shock Factor Results

WFS Factor Construction and Properties

To test the final hypothesis (H4), that WFSs represent systematic risk factors, WFS-mimicking portfolios based on industry-level employment changes (Ai & Bhandari, 2021) were constructed. Table 6 presents results from time-series regressions of portfolio returns on the WFS factor.

Table 6.

Work Force shocks factor results.

Panel A shows that the WFS factor generates a statistically significant negative risk premium of −0.45% per month (t-statistic = −2.88). This negative premium indicates that investors are willing to pay to avoid exposure to WFS risk, consistent with WFSs representing systematic risk factors (H4).

Panel B shows that the WFS risk factor is systematically priced in returns. High-labor-intensive firms (Q5) load positively and significantly on the WFS factor (0.52, t = 4.67), while low-labor-intensive firms (Q1) load negatively (−0.18, t = −2.45). The spread portfolio (Q5–Q1) exhibits a large, highly significant WFS beta (0.70, t = 6.89), confirming that return differences across labor-intensity portfolios are strongly driven by exposure to workforce shocks. These results hold after controlling for all five Fama–French factors, indicating that WFS represents an incremental, priced source of systematic risk.

Panel C presents results from spanning tests using the Gibbons–Ross- Shanken (GRS) methodology (Gibbons et al., 1989). The WFS factor significantly improves explanatory power beyond the standard Fama–French five factors (F-statistic = 3.42, p-value = 0.01) (Fama & French, 1993). The improvement is particularly pronounced for portfolios of labor-intensive firms, where the WFS factor reduces pricing errors by approximately 25%.

5.3. Cross-Sectional Asset-Pricing Tests Results

Table 7 presents results from Fama–MacBeth cross-sectional regressions (Fama & MacBeth, 1973), testing whether WFS exposures are priced in the cross-section of stock returns.

Table 7.

Cross-sectional asset-pricing tests Results.

The risk premium associated with WFS factor loadings is −0.38% per month (t-statistic = −2.61), consistent with the time-series results. This premium remains significant after controlling for exposures to market, size, value, profitability, investment, and momentum factors. These results support (H4) and indicate that exposure to WFSs is an independent, priced dimension of risk in financial markets.

Cross-sectional variation shows that the WFS premium is concentrated in labor-intensive firms and varies over the business cycle. During recession periods, the WFS premium increases to −0.67% per month, while during expansions it averages −0.21% per month. This cyclical variation is consistent with WFSs representing more systematic risk during economic downturns.

Overall, the evidence across all models and tests consistently confirms all four hypotheses: H1, H2, H3, and H4. WFSs not only reduce firm value and increase volatility but also constitute a systematic risk factor that helps explain cross-sectional differences in stock returns.

6. Discussion and Implications

6.1. Scientific and Theoretical Implications

The findings of this study carry several important scientific implications for the growing body of work linking labor market dynamics with asset pricing. The results provide clear empirical support for the idea that labor-market frictions represent a meaningful source of priced risk, and they deepen the theoretical understanding of how workforce-related disruptions transmit into expected returns. These insights contribute to ongoing scientific discussions about the role of labor frictions within production-based and friction-based asset-pricing models (Ge et al., 2023).

The empirical findings of this study provide strong support for theoretical models that incorporate labor market frictions into asset-pricing frameworks (Ang et al., 2020). The significant negative abnormal returns following WFS announcements are consistent with models where employment decisions convey information about future cash flows and adjustment costs (Belo et al., 2014).

The systematic nature of WFS effects supports theories emphasizing economy-wide labor market conditions as sources of non-diversifiable risk. WFS factor results align with Kuehn et al. (2017), who demonstrate that labor market tightness represents a priced risk factor (Kuehn et al., 2017). The negative risk premium document suggests that investors view WFS exposure as undesirable, consistent with these shocks occurring during economic downturns when marginal utility is high.

The cross-sectional variation in WFS effects provides insight into the mechanisms through which labor market frictions affect asset prices. The stronger effects for labor-intensive firms support adjustment cost theories, while the cyclical variation in risk premia is consistent with time-varying systematic risk exposures (Bouvard & de Motta, 2021).

6.2. Asset-Pricing Model Implications

The results suggest that traditional asset-pricing models may be incomplete in their treatment of labor market variables. The significant improvement in explanatory power when including the WFS factor indicates that standard Fama–French models miss important sources of systematic risk.

The WFS factor could be incorporated into multi-factor asset-pricing models used for performance evaluation and risk management. The −0.45% monthly risk premium associated with this factor is economically significant and suggests that investors should consider labor market exposures when constructing portfolios (Liu & Wu, 2025).

For practitioners, the findings of this study imply that monitoring industry-level employment trends could provide valuable information for investment decisions. Firms in industries experiencing employment disruptions warrant additional scrutiny, particularly during economic contractions when WFS effects are amplified.

6.3. Corporate Finance Implications

The significant market response to WFS announcements has important implications for corporate managers making employment decisions. Evidence suggests that markets interpret workforce reductions as negative signals about future prospects, potentially constraining firms’ flexibility in adjusting employment levels.

The larger market responses for labor-intensive firms suggest that these companies face higher costs of workforce adjustments. This finding contributes to understanding how financial market pressures may influence real decisions and could inform debates about optimal employment policies.

The persistence of WFS effects indicates that employment decisions have long-lasting valuation consequences (Benmelech et al., 2021). Managers should consider not only the direct costs of workforce adjustments but also the signaling effects and systematic risk implications for their firms’ cost of capital.

6.4. Robustness and Limitations

Results presented in this study are robust to various alternative specifications and sample restrictions. Alternative event windows, WFS thresholds, and industry classifications yield qualitatively similar results. Excluding financial crisis periods reduces the magnitude of effects but does not eliminate statistical significance.

Several limitations should be acknowledged. First, the WFS identification relies on public announcements, which may not capture all employment adjustments. Private firms and smaller public firms may adjust employment without generating news coverage, potentially biasing the sample used toward larger, more visible firms.

Second, the control firm matching procedure, while comprehensive, may not fully capture all relevant firm characteristics. Unobservable differences between treatment and control firms could influence the results, though extensive robustness checks suggest this is unlikely to drive the main findings.

Third, the WFS factor is based on industry-level employment data, which may not fully capture firm-specific exposure to WFSs. More refined measures of WFS exposure could potentially improve the explanatory power of this factor.

7. Conclusions and Policy Implications

7.1. Conclusions

This paper provides comprehensive evidence on the relationship between WFSs and financial markets from an asset-pricing perspective. The empirical analysis demonstrates that WFSs represent systematic risk factors that generate significant market responses and are priced in the cross-section of stock returns.

Several key findings emerge from the analysis. First, WFS announcements generate significant negative abnormal returns of −2.35% over three-day event windows, with larger effects for labor-intensive firms and during economic contractions. Second, WFSs increase return volatility and trading volume, suggesting increased uncertainty and disagreement among investors. Third, the authors construct a WFS factor that generates a negative risk premium of −0.45% per month, and significantly improves explanatory power beyond standard asset-pricing models. This leads to the conclusion that WFSs may play an important role in economically meaningful and statistically significant declines in firm value, especially among labor-intensive firms.

Results contribute to understanding how real economic frictions are transmitted to financial markets and how labor market dynamics affect asset pricing. The findings have important implications for investors, corporate managers, and policymakers seeking to understand the linkages between employment dynamics and financial market outcomes.

The systematic nature of WFS effects suggests that labor market frictions represent an important source of non-diversifiable risk that traditional asset-pricing models may inadequately capture. WFS factor provides a potential enhancement to existing factor models and could be useful for portfolio management and risk assessment.

7.2. Policy Implications

The findings of this study have several policy implications. The systematic nature of WFS effects suggests that employment disruptions can transmit across firms and industries, potentially amplifying economic downturns. This transmission mechanism may justify policy interventions to stabilize employment during recessions.

The significant financial market attention to WFSs may affect the design of unemployment insurance and labor market policies. If firms anticipate negative market reactions to employment reductions, they may be more reluctant to adjust workforce levels, potentially reducing labor market flexibility.

From a regulatory perspective, results suggest that employment changes contain systematic information relevant to financial markets. Current disclosure requirements focus primarily on financial metrics, but the evidence indicates that employment data may warrant increased transparency requirements.

8. Future Research Directions

Future research might explore several extensions of the present work. International evidence would provide insight into whether the findings generalize to different institutional environments and labor market structures. An analysis of the effects of technological change and automation on WFS dynamics represents another important area for investigation. Additionally, examining the role of WFSs in corporate bond markets and credit risk assessment could provide further insight into the systematic nature of employment-related risks.

As financial markets continue to evolve and labor markets adapt to technological and demographic changes, understanding the relationship between workforce dynamics and asset pricing remains crucial for both academic research and practical applications. Findings suggest that this relationship is both economically significant and systematically important, warranting continued attention from researchers and practitioners alike.

By integrating workforce dynamics into asset pricing, this study opens a new channel for understanding how real economic shocks translate into financial market risk, a perspective that traditional models have largely overlooked.

Author Contributions

Conceptualization, S.A. and A.A.; Methodology, S.A. and J.A.; Software, S.A. and M.S.A.; Validation, S.A., R.W. and A.A.; Formal Analysis, S.A. and M.S.A.; Investigation, S.A.; Resources, A.A.; Data Curation, S.A. and J.A.; Writing—Original Draft Preparation, S.A., A.A. and J.A.; Writing—Review & Editing, S.A., J.A., A.A., R.W. and M.S.A.; Visualization, S.A. and A.A.; Supervision, S.A. and J.A.; Project Administration, S.A. and A.A. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The original data presented in the study are openly available at the website of the Bureau of Labor Statistics (BLS) Mass Layoff Statistics program (https://www.bls.gov/mls/) (accessed on 20 June 2025), corporate news announcements from Bloomberg (https://www.bloomberg.com/) (accessed on 20 June 2025) and Refinitiv, and financial data from the CRSP/Compustat merged database (https://www.crsp.org/research/crsp-compustat-merged-database/) (accessed on 20 June 2025).

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Abdullah, M., Abdou, H. A., Godfrey, C., Elamer, A. A., & Ahmed, Y. (2023). Assessing the use of gold as a zero-beta asset in empirical asset pricing: Application to the US equity market. Journal of Risk and Financial Management, 16, 204. [Google Scholar] [CrossRef]

- Ai, H., & Bhandari, A. (2021). Asset pricing with endogenously uninsurable tail risk. Econometrica, 89(3), 1471–1505. [Google Scholar] [CrossRef]

- Aivazian, V. A., Chiu, T.-T., Minutti-Meza, M., & Vyas, D. (2025). Political uncertainty and the timing of mass layoffs. Production and Operations Management, 34(10), 3193–3213. [Google Scholar] [CrossRef]

- Ang, T. C., Lam, F. Y. E. C., & Wei, K. C. J. (2020). Mispricing firm-level productivity. Journal of Empirical Finance, 58, 139–163. [Google Scholar] [CrossRef]

- Armstrong, C., Heinle, M. S., & Luneva, I. (2024). Financial information and diverging beliefs. Review of Accounting Studies, 29(3), 2082–2124. [Google Scholar] [CrossRef]

- Bae, J., & Kang, J. (2023). Human capital quality and stock returns. Journal of Banking & Finance, 152, 106857. [Google Scholar] [CrossRef]

- Baghai, R., Silva, R. C., Thell, V., & Vig, V. (2021). Talent in distressed firms: Investigating the labor costs of financial distress. The Journal of Finance, 76(6), 2907–2961. [Google Scholar] [CrossRef]

- Bansal, R., & Yaron, A. (2004). Risks for the long run: A potential resolution of asset pricing puzzles. The Journal of Finance, 59(4), 1481–1509. [Google Scholar] [CrossRef]

- Barrett, P. (2024). The dynamic effects of local labor market shocks on small firms in the united states. IMF Working Paper, 2024(63), 1–51. [Google Scholar] [CrossRef]

- Belo, F., Donangelo, A., Lin, X., & Luo, D. (2023). What drives firms’ hiring decisions? an asset pricing perspective. Review of Financial Studies, 36(9), 3825–3860. [Google Scholar] [CrossRef]

- Belo, F., Li, J., Lin, X., & Zhao, X. (2017). Labor-force heterogeneity and asset prices: The importance of skilled labor. Review of Financial Studies, 30(10), 3669–3709. [Google Scholar] [CrossRef]

- Belo, F., Lin, X., & Bazdresch, S. (2014). Labor hiring, investment, and stock return predictability in the cross section. Journal of Political Economy, 122(1), 129–177. [Google Scholar] [CrossRef]

- Benmelech, E., Bergman, N., & Seru, A. (2021). Financing labor. Review of Finance, 25(5), 1365–1393. [Google Scholar] [CrossRef]

- Birinci, S., Mercan, Y., & See, K. (2025). Mismatch unemployment during COVID-19 and the post-pandemic labor shortages. Journal of Economic Dynamics and Control, 178, 105142. [Google Scholar] [CrossRef]

- Bongaerts, D., Kang, X., & van Dijk, M. A. (2025). Revisiting asset pricing models: The case for an intangibles factor. Financial Management, e70001. [Google Scholar] [CrossRef]

- Bouvard, M., & de Motta, A. (2021). Labor leverage, coordination failures, and aggregate risk. Journal of Financial Economics, 142(3), 1229. [Google Scholar] [CrossRef]

- Cardillo, G., Onali, E., & Perdichizzi, S. (2023). Investor behavior around targeted liquidity announcements. The British Accounting Review, 56(6), 101275. [Google Scholar] [CrossRef]

- Chemla, G., & Pontuch, P. (2012, June 6–8). Labor intensity and expected stock returns [Conference paper]. FMA European Conference, Istanbul, Turkey. [Google Scholar]

- Chen, L., Li, T., Jia, F., & Schoenherr, T. (2022). The impact of governmental COVID-19 measures on manufacturers’ stock market valuations: The role of labor intensity and operational slack. Journal of Operations Management, 69(3), 404–425. [Google Scholar] [CrossRef]

- Daadmehr, E. (2024). Workplace sustainability or financial resilience? Composite-financial resilience index. Risk Management, 26, 7. [Google Scholar] [CrossRef]

- Daadmehr, E. (2025). Resilience and asset pricing in COVID-19 disaster. Economies, 13(5), 123. [Google Scholar] [CrossRef]

- Davis, S. J., & Haltiwanger, J. (1992). Gross job creation, gross job destruction, and employment reallocation. The Quarterly Journal of Economics, 107(3), 819–863. [Google Scholar] [CrossRef]

- Edmans, A., Pu, D., Zhang, C., & Li, L. (2023). Employee satisfaction, labor market flexibility, and stock returns around the world. Management Science, 70(7), 4357–4380. [Google Scholar] [CrossRef]

- Eggers, A. C., Tuñón, G., & Dafoe, A. (2023). Placebo tests for causal inference. American Journal of Political Science, 68(3), 1106–1121. [Google Scholar] [CrossRef]

- Eiling, E., Kan, R., & Sharifkhani, A. (2023). Sectoral labor reallocation and return predictability [Rotman School of Management working paper No. 2602215]. In Proceedings of Paris December 2021 finance meeting EUROFIDAI–ESSEC. Rotman School of Management University of Toronto. [Google Scholar] [CrossRef]

- Faccio, M., Mørck, R., & Yavuz, M. D. (2020). Business groups and the incorporation of firm-specific shocks into stock prices. Journal of Financial Economics, 139(3), 852–871. [Google Scholar] [CrossRef]

- Faia, E., & Pezone, V. (2023). The cost of wage rigidity. The Review of Economic Studies, 91(1), 301–339. [Google Scholar] [CrossRef]

- Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3–56. [Google Scholar] [CrossRef]

- Fama, E. F., & MacBeth, J. D. (1973). Risk, return, and equilibrium: Empirical tests. Journal of Political Economy, 81(3), 607–636. [Google Scholar] [CrossRef]

- Francisco, P. (2025). Labour intensity and systematic risk. Finance Research Letters, 86, 108475. [Google Scholar] [CrossRef]

- Ge, Y., Qiao, Z., & Zheng, H. (2023). Local labor market and the cross section of stock returns. Journal of International Money and Finance, 138, 102925. [Google Scholar] [CrossRef]

- Gibbons, M. R., Ross, S. A., & Shanken, J. (1989). A test of the efficiency of a given portfolio. Econometrica, 57(5), 1121–1152. [Google Scholar] [CrossRef]

- Greenwood, R., Shleifer, A., & You, Y. (2019). Bubbles for fama. Journal of Financial Economics, 131(1), 20–43. [Google Scholar] [CrossRef]

- He, X., Rizov, M., & Zhang, X. (2021). Workforce size adjustment as a strategic response to exchange rate shocks: A strategy-tripod application to Chinese firms. Journal of Business Research, 138, 203–213. [Google Scholar] [CrossRef]

- Hershbein, B. J., & Kahn, L. (2018). Do recessions accelerate routine-biased technological change? Evidence from vacancy postings. American Economic Review, 108(7), 1737–1772. [Google Scholar] [CrossRef]

- Jha, A., Shirvani, A., Rachev, S. T., & Fabozzi, F. J. (2025). Beyond the traditional VIX: A novel approach to identifying uncertainty shocks in financial markets. Journal of Risk and Financial Management, 18, 11. [Google Scholar] [CrossRef]

- Khan, N., & Afeef, M. (2024). Is human capital premium price in asset pricing? Insights from South Africa during the COVID-19 era. Journal of Innovative Research in Management Sciences, 5(4), 1–24. [Google Scholar] [CrossRef]

- Knesl, J. (2022). Automation and the displacement of labor by capital: Asset pricing theory and empirical evidence. Journal of Financial Economics, 147(2), 271–296. [Google Scholar] [CrossRef]

- Kolari, J. W., Huang, J. Z., Liu, W., & Liao, H. (2025). A quantum leap in asset pricing: Explaining anomalous returns. Journal of Risk and Financial Management, 18(7), 362. [Google Scholar] [CrossRef]

- Kudlyak, M., & Wolcott, E. (2024). Pandemic layoffs and the role of stay-at-home orders. Economics Letters, 242, 111894. [Google Scholar] [CrossRef]

- Kuehn, L., Simutin, M., & Wang, J. J. (2017). A labor capital asset pricing model. The Journal of Finance, 72(5), 2131–2178. [Google Scholar] [CrossRef]

- Kumar, R., Pandey, D. K., & Goodell, J. W. (2023). Market reactions to layoff announcements during crises: Examining impacts and conditioners. Finance Research Letters, 58, 104423. [Google Scholar] [CrossRef]

- Lei, W., Li, Z., & Mei, D. (2023). Financial crisis, labor market frictions, and economic volatility. PLoS ONE, 18(9), e0291106. [Google Scholar] [CrossRef]

- Lewis, Y., & Bozos, K. (2019). Mitigating post-acquisition risk: The interplay of cross-border uncertainties. Journal of World Business, 54(5), 100996. [Google Scholar] [CrossRef]

- Liang, Y., Kiosse, P. V., & Tarsalewska, M. (2025). Labour unemployment insurance and pension asset allocations. British Journal of Management, 36, 930–945. [Google Scholar] [CrossRef]

- Liu, Y., & Wu, X. (2025). Labor links, comovement, and predictable returns. Journal of Financial and Quantitative Analysis, 1–31. [Google Scholar] [CrossRef]

- Lo, C. K. Y., Tang, C. S., Zhou, Y., Yeung, A. C. L., & Fan, D. (2018). Environmental Incidents and the market value of firms: An empirical investigation in the chinese context. Manufacturing & Service Operations Management, 20(3), 422–439. [Google Scholar] [CrossRef]

- Makarov, R. N. (2023). Option pricing and portfolio optimization under a multi-asset jump-diffusion model with systemic risk. Risks, 11, 217. [Google Scholar] [CrossRef]

- Marshall, A., McColgan, P., & McLeish, S. A. (2012). Why do Stock Prices decline in response to employee layoffs? UK evidence from the 2008 global financial crisis. The Journal of Financial Research, 35(3), 375–396. [Google Scholar] [CrossRef]

- Mubarok, F. (2022). Revealing the structure of financial performance on stock prices. Jurnal Organisasi Dan Manajemen, 18(2), 74–86. [Google Scholar] [CrossRef]

- Neffke, F., Otto, A., & Weyh, A. (2017). Inter-industry labor flows. Journal of Economic Behavior & Organization, 142, 275–292. [Google Scholar] [CrossRef]

- Papenkov, M. (2019). An empirical asset pricing model accommodating the sector-heterogeneity of risk. Atlantic Economic Journal, 47(4), 499–520. [Google Scholar] [CrossRef]

- Prasad, T. S. L., Gunda, M., Esargundi, R., & Kandagatla, G. (2025). Predicting employee layoffs with machine learning: A social network and data mining approach. Global Journal of Engineering Innovations and Interdisciplinary Research, 5(4), 070. [Google Scholar] [CrossRef]

- Saba, Z. (2024). Layoffs and corporate performance: Evidence based on the US tech industry. Journal of Economics and Finance, 48(3), 644–667. [Google Scholar] [CrossRef]

- Sanati, A. (2024). How does labor mobility affect corporate leverage and investment? Journal of Financial and Quantitative Analysis, 60, 1146–1184. [Google Scholar] [CrossRef]

- Setiawan, H., Setyanto, A., Utami, E., & Kusrini, K. (2025). Advancements and challenges in financial forecasting models: A systematic literature review. In Advances in transdisciplinary engineering. IOS Press. [Google Scholar] [CrossRef]

- Sheng, J. (2025). Asset pricing in the information age: Employee expectations and stock returns. The Review of Asset Pricing Studies, 15(1), 74–101. [Google Scholar] [CrossRef]

- Shimada, E. (2022). Industry-specific analysis of the impact of changes in the macroeconomic environment on corporate profits and estimation of corporate tax revenue. International Journal of Economic Policy Studies, 17(1), 1–61. [Google Scholar] [CrossRef]

- Tan, K. J. K., Zhou, Q., Pan, Z., & Faff, R. W. (2021). Business shocks and corporate leverage. Journal of Banking & Finance, 131, 106208. [Google Scholar] [CrossRef]

- Thalassinos, E., Khan, N., Afeef, M., Zada, H., & Ahmed, S. (2025). The role of human capital in explaining asset return dynamics in the indian stock market during the COVID era. Risks, 13(7), 136. [Google Scholar] [CrossRef]

- Thalassinos, E., Khan, N., Ahmed, S., Zada, H., & Ihsan, A. (2023). A comparison of competing asset pricing models: Empirical evidence from pakistan. Risks, 11, 65. [Google Scholar] [CrossRef]

- Tommaso, M. R. D., Prodi, E., Pollio, C., & Barbieri, E. (2022). Conceptualizing and measuring “industry resilience”: Composite indicators for postshock industrial policy decision-making. Socio-Economic Planning Sciences, 85, 101448. [Google Scholar] [CrossRef]

- Wachter, J. A. (2013). Can time-varying risk of rare disasters explain aggregate stock market volatility? The Journal of Finance, 68(3), 987–1035. [Google Scholar] [CrossRef]

- Wang, Y.-C., & Su, H.-L. (2024). Unraveling exogenous shocks, financial stress and US economic performance. Studies in Economics and Finance, 42(2), 259–273. [Google Scholar] [CrossRef]

- Whelan, K. T. (2009). Technology shocks and hours worked: Checking for robust conclusions. Journal of Macroeconomics, 31(2), 231–239. [Google Scholar] [CrossRef]

- Zhang, M. B. (2019). Labor-technology substitution: Implications for asset pricing. The Journal of Finance, 74(4), 1793–1839. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.