Abstract

In the context of economic globalization, robust corporate social responsibility (CSR) serves as a critical source of legitimacy and competitive advantage for multinational enterprises (MNEs). However, institutional and competitive disparities between host and home countries frequently lead overseas subsidiaries of MNEs to deviate from parent company standards by substituting symbolic for substantive CSR practices and thereby creating potential threats to MNEs’ group-wide reputation. Although external stakeholder monitoring is widely recognized, most studies adopt static, dyadic perspectives and thus rarely examine the dynamic interplay between external monitoring and MNEs’ CSR governance. To address this gap, this study constructs a tripartite evolutionary game model involving the parent company, overseas subsidiaries, and external stakeholders, systematically analyzes the evolutionary pathways and the stability of their strategic interactions and uses numerical simulations to identify the conditions for system equilibriums and the influence of key parameters. The findings demonstrate that moderate incentives and penalties from the parent company and active monitoring by external stakeholders significantly promote overseas subsidiaries’ adoption of substantive CSR. This equilibrium becomes more stable when the benefits of substantive CSR increase or its costs decrease for overseas subsidiaries. However, excessive incentive expenditures may weaken the parent company’s willingness to implement strict supervision. Furthermore, information synergies and collaborative governance between the parent company and external stakeholders reduce cross-border supervision and coordination costs, thereby increasing the likelihood of an equilibrium with strict supervision and substantive CSR. By moving beyond conventional static and binary analytical frameworks, this study proposes governance pathways, including optimizing incentive mechanisms, strengthening external stakeholder monitoring, and fostering information synergies, thereby offering new theoretical perspectives and managerial implications for understanding the evolution of CSR behavior in MNEs.

1. Introduction

Amid deepening globalization and increasingly complex business environments, CSR has become a strategic pillar for MNEs to secure legitimacy, enhance competitiveness, and achieve sustainable development in global markets [1]. As major drivers of global economic growth, MNEs face exacting expectations for CSR performance. KPMG Global Survey of Sustainability Reporting 2024 reports that 95% of the Global 250 have set carbon reduction targets and 97% publish sustainability reports, signaling that disclosure has become the norm [2]. MNEs actively engage in sustainability reporting, corporate websites, and targeted advertising to showcase their CSR efforts. These activities are intended to strengthen their global reputation and shape a responsible brand identity [3]. Prior research shows that a strong MNE reputation spills over to overseas subsidiaries, helping them mitigate the liability of foreignness and gain advantages such as market access and legitimacy [4]. Negative spillovers also arise when subsidiaries fail to implement group-wide CSR standards consistently, and the resulting reputational damage can spread to parent companies and other affiliates [5]. In 2015, Volkswagen’s U.S. subsidiary was found to have installed defeat devices in emissions testing, and the impact quickly expanded beyond the local operation. After disclosure, Volkswagen’s share price fell by about 37% within days, and the group ultimately incurred more than US$30 billion in fines, settlements, and remediation costs worldwide, illustrating how misconduct at the subsidiary level can escalate into a group-wide crisis.

For overseas subsidiaries, reputational capital derived from their parent companies helps them establish themselves in host markets and secure competitive advantages. However, differences in policy regimes and competitive pressures between host and home countries shape distinct cost–benefit considerations for subsidiaries’ CSR decisions [6]. Durand and Jacqueminet find that when subsidiaries face strong external pressures, attention to headquarters-imposed CSR norms declines [7]. Under such conditions, subsidiaries may shift resources away from high-quality CSR toward operational investments that raise profits, expand output, or outpace rivals [8]. In response, parent companies deploy accountability mechanisms, incentive systems, dedicated CSR governance units, and expatriate assignments to monitor subsidiary conduct [9].

Effective CSR not only helps MNEs build reputational capital and reduce operational risk, but also generates positive externalities by improving social welfare and environmental governance in host countries [10]. Therefore, external stakeholders such as governments, the media, and nongovernmental organizations (NGOs) have strong incentives to monitor subsidiaries’ CSR performance. Legislation, investigative oversight, and public pressure from external stakeholders increase the expected cost of CSR opportunism and, in turn, work in concert with parent company supervision to promote mutually beneficial outcomes [11]. However, existing research rarely uses evolutionary game-theoretic models to capture dynamic feedback among headquarters, subsidiaries, and external stakeholders. Instead, most studies conceptualize external stakeholder pressures as exogenous institutional or environmental constraints on firms’ behavior. In other words, these pressures are typically not modeled as the outcome of stakeholders’ own strategic monitoring choices [12].

To address these limitations, we adopt a dynamic and interactive perspective by endogenizing external monitoring strategies to examine the evolution of the CSR governance system jointly shaped by the parent company, the overseas subsidiary, and external stakeholders. Building on this logic, this study addresses the following core research question. Under what parameter conditions does the triadic evolutionary game among the parent company, the overseas subsidiary, and external stakeholders converge to a stable equilibrium in which the parent company adopts strict supervision, the subsidiary engages in substantive CSR, and external stakeholders choose active monitoring? Furthermore, how do variations in these conditions reshape the co-evolution of the three actors’ strategies? To address this research question, we develop a triadic evolutionary game-theoretic model and use analytical derivations and numerical simulations to trace equilibrium paths and assess how parameter configurations shape these trajectories.

The main contributions of this study are as follows:

First, this study moves beyond the static analytical paradigm by developing a tripartite evolutionary game model that reveals the dynamic coupling between multi-actor strategic interactions and system evolution in MNE CSR governance. This addresses the literature’s prevailing focus on dyadic relationships and offers a new theoretical perspective for analyzing MNEs’ CSR governance systems under the influence of external stakeholders.

Second, by focusing on the inherent tension between the MNE headquarters’ global CSR standards and their implementation by overseas subsidiaries, this study highlights external stakeholders as a complementary monitoring force. The analysis shows that active monitoring generates information synergies that enhance the headquarters’ supervisory efficacy, thereby extending the conventional view that relies primarily on mechanisms based on incentives or penalties.

Finally, by integrating theoretical modeling with numerical simulations, this study identifies the players’ convergence pathways across alternative parameter configurations and shows how cost–benefit structures shape the system’s evolutionary trajectories and equilibrium stability.

Taken together, these contributions advance research on evolutionary game theory in MNEs’ CSR governance and inform the design of balanced governance strategies that enhance MNEs’ CSR performance.

The rest of the paper is organized as follows. Section 2 presents the literature review. Section 3 delineates the interests and claims of the parties in the CSR governance system of MNEs. Section 4 develops the tripartite evolutionary game and its assumptions. Section 5 presents the analysis of the model. Section 6 reports numerical simulations on stability and parameter sensitivity. Section 7 offers policy and managerial implications to help achieve the desired systemic equilibrium.

2. Literature Review

2.1. Corporate Social Responsibility

The concept of Corporate Social Responsibility (CSR) emerged in the mid-twentieth century. After decades of development, CSR has moved beyond “doing good” or “risk management” to become a practical imperative that integrates social and environmental concerns into core strategy and operations [13]. The World Business Council for Sustainable Development (WBCSD) defines CSR as “The commitment of business to contribute to sustainable economic development, working with employees, their families, the local community and society at large to improve their quality of life.” In other words, modern CSR requires firms to balance economic, environmental, and social considerations—the triple bottom line—in business decisions and actions.

Studies have shown that strong CSR performance benefits society in multiple ways. Flammer finds that issuing green bonds for environmental projects can enhance environmental performance by reducing CO2 emissions and carbon intensity [14]. Based on sustainability reports from hundreds of MNEs, Eang and Behnam document contributions to local communities through employment, infrastructure investment, and targeted poverty alleviation [15]. Leading firms’ high standards can also diffuse upstream and downstream, encouraging suppliers to adopt green collaboration practices and improving supply chain environmental performance [16].

Since the early 2000s, the digital economy, climate governance, and green development have reshaped the global economic landscape. In this context, CSR has expanded to new domains. Lobschat et al. argue that digital-era CSR centers on data privacy, algorithmic ethics, and digital inclusion; protecting user privacy, ensuring algorithmic fairness and transparency, preventing misuse of technology, and bridging the digital divide are now core responsibilities [17]. At the same time, accelerating climate risks have elevated climate action within the CSR agenda. Corporate investment in green innovation and transitions to low-carbon supply chains are essential for achieving carbon neutrality goals [18].

Effective CSR not only generates positive externalities for stakeholders but also serves as a strategic asset for MNEs by fostering long-term value, strengthening organizational resilience, and securing operational legitimacy [19]. Wang et al. show that CSR performance shapes consumers’ future purchase intentions by affecting brand equity, brand trustworthiness, and brand reputation [20]. In capital markets, Ghoul et al. find that strong CSR signals lower risk and higher managerial quality, which can reduce the cost of capital, attract long-term investors, and support valuation premiums [21]. Lins et al. document that during financial crises, firms with stronger CSR exhibit higher stock returns and greater profitability, consistent with superior resilience and recovery capacity [22].

In summary, robust CSR practices enhance competitive advantage and generate social benefits. Examining how MNEs evolve toward sound CSR through dynamic interactions among the parent company, the overseas subsidiary, and external stakeholders has clear practical value for fostering sustainable growth in complex environments and for improving social welfare in host countries.

2.2. CSR in Multinational Enterprises

As discussed above, proactive CSR yields reputational benefits for firms. In MNEs, Meyer et al. find that overseas subsidiaries can draw on resources from their parent companies, including global reputation [23]. While subsidiaries benefit from legitimacy and competitive advantages derived from their parents’ strong reputation, negative CSR incidents at the subsidiary level can quickly erode the reputational value of MNE networks through spillovers. Parent companies, as the ultimate owners of global brands, bear most of the resulting costs [24]. They therefore have strong incentives to design and implement uniform, high-standard global CSR strategies to protect brand integrity, meet the expectations of global investors and consumers, and mitigate system-wide risks arising from local failures [25].

However, Kostova and Roth show that overseas subsidiaries operate within host-country institutional environments that often differ from those of their parent companies [26]. Market competition, cost pressures, regulatory intensity, and cultural expectations frequently diverge, creating objective constraints on subsidiary operations. To survive fierce local competition or secure short-term profits, managers may take opportunistic actions such as reducing environmental safeguards or diluting labor standards, thereby failing to implement their parents’ more costly Substantive CSR standards [27].

When uniform Substantive CSR standards conflict with local survival pressures, subsidiaries often prefer Symbolic CSR to gain legitimacy [7]. Symbolic actions emphasize messaging and appearances over substantive improvements in performance, with the aim of managing stakeholder expectations, securing legitimacy and reputational capital, and deflecting criticism [28]. In the context of multinational enterprises, symbolic CSR by overseas subsidiaries typically takes the form of adopting formal policies, certifications, and selectively disclosed CSR reports or campaigns that are closely aligned with the rhetoric of global CSR standards, but only loosely coupled with actual changes in local operating practices. This approach allows subsidiaries to signal compliance and avoid direct accountability to headquarters while preserving local operational flexibility and cost advantages, thereby navigating the tension between global standardization and local responsiveness [29].

By contrast, Substantive CSR requires committed resources to deliver tangible changes in core processes, organizational structures, and management systems, producing verifiable and effective social responsibility outcomes that are more costly and harder to imitate [30]. In a cross-border setting, substantive CSR by overseas subsidiaries implies embedding CSR requirements into local production, employment, and environmental practices in ways that simultaneously conform to group-level CSR standards and respond to host-country regulatory and societal expectations. Rather than decoupling communication from practice, substantive CSR narrows the gap between global CSR commitments and on-the-ground implementation, thereby strengthening headquarters’ control over CSR quality and enhancing the credibility of the MNE’s overall CSR posture in the eyes of diverse internal and external stakeholders.

In summary, overseas subsidiaries’ CSR choices are shaped by the need to adapt to host-country institutions while meeting parent company standards that protect the global brand reputation of MNEs. This tension is central to the CSR governance system of MNEs and helps explain the complexity of subsidiaries’ CSR decision making.

2.3. External Stakeholder Influence on MNEs’ CSR

In the CSR practices of MNEs, external stakeholders, including communities, consumers, government and regulatory authorities, the media, industry associations, NGOs, and social movement organizations, influence subsidiaries’ CSR strategies by imposing legitimacy requirements, restricting market entry, exercising public scrutiny, and providing cost-sharing and technical support [31,32].

Using quasi-natural evidence from China’s central environmental inspections, Jia and Chen show that stronger, centralized environmental enforcement raises detection probabilities and penalty costs, reduces pollutant emission intensity, and improves corporate environmental performance [33]. Beyond strict regulation, governments can also reshape corporate incentives by tightening constraints while increasing positive inducements, thereby curbing opportunism and promoting substantive, long-term CSR engagement [34]. The host-country institutional environment also provides the backdrop for MNEs’ CSR strategies. Marano and Kostova find that where institutions are weak and regulation is inadequate, MNEs may lower CSR standards, whereas in settings with mature institutions and stringent oversight, they tend to adopt higher-level, more strategic CSR practices to secure legitimacy and reputation [35].

In parallel, NGOs complement state enforcement through monitoring and disclosure. She’s research indicates that NGOs can monitor MNEs by exposing corporate irresponsibility via social media and online networks [36]. Dyck et al. highlight the media and public opinion as vital forces in external governance, showing that negative coverage can trigger a legitimacy crisis and push MNEs to enhance CSR performance to restore reputation and social acceptance [37]. The digital media environment has reshaped public oversight of CSR. Crane and Glozer discuss the dialogic and diffusive nature of CSR communication on social media, noting that these platforms accelerate the spread of negative information and pose immediate threats to MNEs’ brand value [38]. Examining multinational financial firms, Chalmers et al. study how systemic financial stress indicators, media coverage, and public attention metrics relate to CSR reporting and commitments, finding that greater media coverage and public scrutiny are associated with more targeted CSR commitments and greater transparency by MNEs [39].

As crucial stakeholders, consumers primarily influence MNEs’ CSR strategies through purchase behavior and public opinion pressure. Across multiple experiments, Sen and Bhattacharya show that awareness of corporate CSR information improves consumers’ overall firm evaluations, purchase intentions, and willingness to advocate [40]. The spread of social media enables consumers to monitor and publicly condemn CSR failures more efficiently and in real time [41]. Amid recurrent global crises, He and Harris argue that in the post-pandemic era, consumers increasingly prefer brands that show genuine concern for employees, communities, and the environment during crises, looking beyond the product itself [42].

Taken together, MNEs’ CSR practices are collectively shaped and monitored by diverse external stakeholders. Through a combination of regulatory pressure, social scrutiny, and market selection, these actors form an external-governance system that continually pushes MNEs toward more proactive and substantive engagement in social responsibility.

2.4. Evolutionary Game Theory

Evolutionary Game Theory (EGT) provides an analytical framework for studying strategic interactions under bounded rationality and dynamic adaptation. Unlike traditional game theory, which emphasizes static Nash equilibria, EGT models the adjustment process in which populations update strategy frequencies in response to relative payoffs [43,44].

In recent years, EGT has become a prominent lens for corporate CSR research. Li et al. develop an evolutionary game to study carbon-emission reduction between governments and firms, analyzing how peer incentives and the intensity of rewards and penalties shape system evolution [45]. Yao et al. build a tripartite evolutionary game including government, carbon-labeled product manufacturers, and consumers under media supervision and show that stronger media scrutiny and higher label credibility complement regulation, standardize production, and increase consumer trust and purchase intention for carbon-labeled products [46]. Hao et al. propose a tripartite game among firms, investors, and rating agencies to examine governance of ESG disclosure greenwashing, demonstrating that raising audit probabilities and penalties for misreporting improves the credibility of sustainability ratings [47]. Liu et al. construct a tripartite game among regulators, firms, and investors to analyze greenwashing in green financial products and assess collaborative mechanisms to curb such behavior [48]. Xue et al. develop a government–enterprise–consumer game and find that increasing violation costs, strengthening verification, and deploying credible technological tools effectively suppress false environmental claims [49].

In summary, EGT is well suited to complex CSR governance problems. By simulating multi-agent interactions and dynamic adjustments, it enables the analysis of long-term system trajectories under changing external conditions, providing a powerful tool for understanding the decision-making mechanisms that drive corporate CSR practices.

2.5. Summary and Research Gaps

Taken together, prior research identifies global reputation as a strategic asset for MNEs. Overseas subsidiaries benefit from this reputational capital, but they may prioritize short-term gains over protecting group-wide reputation when facing host-country cost pressures and institutional differences.

At the same time, although studies acknowledge the supervisory role of external pressures in MNEs’ CSR, they rarely examine how these forces interact dynamically with parent–subsidiary tensions within MNEs. External stakeholder monitoring is often modeled as a static or binary deterrent, leaving the strategic feedback between external stakeholders and parent–subsidiary units underexplored.

Against this backdrop, we employ evolutionary game theory to develop a tripartite model comprising the parent company, the overseas subsidiary, and the external stakeholder. This framework characterizes equilibrium states and evolutionary trajectories of their strategic choices. Through parameter sensitivity analysis, we identify mechanisms that steer the system toward desirable equilibria and provide a theoretical basis for optimizing CSR governance and monitoring in MNEs.

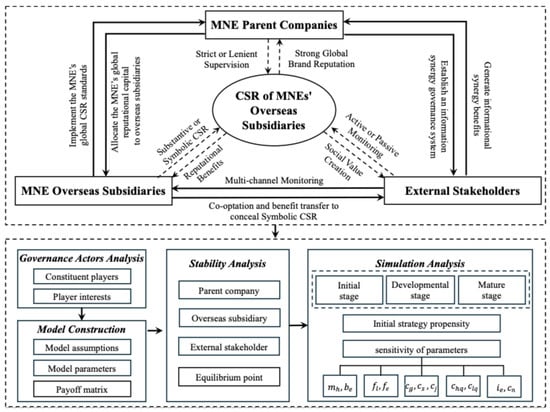

3. Governance Actor Analysis

3.1. Constituent Players

In the CSR governance system of MNEs, the core participants can be classified into three distinct groups [50,51,52]. First, MNE parent companies act as the primary rule-makers, establishing global CSR standards and exercising supervisory authority. Second, overseas subsidiaries serve as the strategic implementers, adapting these global standards to host-country contexts. Third, external stakeholders, encompassing host-country governments, regulatory agencies, NGOs, media, consumers, local communities, suppliers, and investors, collectively monitor subsidiaries’ CSR performance through legislative, monitoring, reputational, and market channels.

In the complex landscape of multinational operations, the CSR practices of overseas subsidiaries are simultaneously influenced by and constrained by a range of external actors, including governmental agencies, nongovernmental organizations (NGOs), the media, and the broader public. Together, these entities form a multilayered and interwoven network of external influence within which subsidiaries operate under both pressure and support. Although these external stakeholders differ markedly in their nature, motivations, and modes of action, they share important similarities [53]. For example, governments impose mandatory institutional constraints through laws and regulations, NGOs generate social pressure through advocacy and evaluation, and the media shape corporate reputation through public exposure. At a fundamental level, all of these actors perform a similar function: by exerting pressure or transmitting information, they systematically alter the expected benefit–cost structure associated with different CSR choices made by overseas subsidiaries. Specifically, stringent regulation and sanctions directly raise the financial and compliance costs of inaction, while active media scrutiny and NGO advocacy amplify the reputational consequences of corporate behavior and thereby affect market demand and public approval.

Building on this shared functional mechanism, the present study classifies these diverse entities under a unified category of “external stakeholders”. This theoretical abstraction does not deny the heterogeneity of external actors in practice; rather, it is adopted to maintain a clear analytical focus and to construct a tractable evolutionary game-theoretic model centered on the core interaction logic. By integrating the influence of governments, NGOs, the media, and other societal actors into the strategic behavior of a single external stakeholder, we strip away contextual complexity and are able to systematically investigate how the stability of overseas subsidiaries’ CSR strategy choices changes when the payoff structure is affected by external factors. In other words, regardless of whether external influence originates from regulatory pressure, media oversight, or shifts in consumer preferences, it ultimately operates through modifying the payoff matrix of the game and thereby drives the subsidiary’s behavior toward different steady states.

This classification approach strengthens the generalizability of the study’s conclusions. It highlights that the core mechanism of CSR governance in overseas subsidiaries lies in how they respond to changes in the economic consequences of CSR behavior induced by external pressure. Accordingly, the managerial implications derived from the analysis are not confined to dealing with any single type of external actor; instead, they apply to any external force capable of reshaping the costs and benefits of subsidiaries’ CSR decisions, thereby enhancing the broader relevance of the findings for the strategic management of CSR in multinational enterprises.

Thus, the tripartite CSR governance framework in this study consists of three core actors: the MNE parent company, overseas subsidiary, and external stakeholder, as illustrated systematically in Figure 1.

Figure 1.

The research framework.

3.2. Analysis of the MNE Parent Company

In today’s competitive global landscape, MNE parent companies face considerable expansion pressures. A strong reputation offers distinctive competitive advantages, making it imperative for parent companies to ensure that all members uphold robust CSR practices. To build legitimacy and a globally recognized brand image, many MNEs invest substantially in visible CSR initiatives. Yet these efforts risk being undermined when overseas subsidiaries fail to maintain consistent responsible conduct [5]. Because reputational resources are shared and transmissible within MNE networks, subsidiaries’ irresponsible behavior directly damages parent companies’ brands and transmits risks across their corporate systems. Consequently, parent companies have strong incentives to supervise and intervene in subsidiaries’ CSR performance, although supervision costs rise with greater supervision intensity. By establishing information-sharing arrangements with external stakeholders, parent companies can achieve more efficient and effective supervision. This approach helps build resilient, agile, and unified group-wide CSR governance networks that constrain and guide subsidiaries’ conduct, ultimately turning CSR into a strategic asset that protects MNEs’ global reputations, secures operational legitimacy, and sustains long-term competitive advantages.

3.3. Analysis of the Overseas Subsidiary

For MNE subsidiaries, their parents’ strong international reputations help mitigate the liability of foreignness in host-country markets [4]. They also signal quality, reliability, and a commitment to compliance to host-country stakeholders, reducing information asymmetry and lowering transaction costs. However, host countries where subsidiaries operate often differ from their home countries in development levels, institutional environments, and competitive pressures. In adapting to local conditions, subsidiaries’ strategic choices often deviate from parent companies’ expectations [27]. Implementing high-quality substantive CSR entails substantial costs. During the market entry phase, subsidiaries face unfamiliar regulations and intense competition, and these pressures may lead them to economize by relaxing standards or shifting from substantive to symbolic CSR, thereby reallocating resources to competitive positioning [8]. Consequently, supervision by parent companies and monitoring by external stakeholders are essential to securing overseas subsidiaries’ substantive CSR and curbing their symbolic CSR.

3.4. Analysis of the External Stakeholder

As direct bearers of the consequences of overseas subsidiaries’ operations, external stakeholders can benefit from proactive monitoring by capturing the positive outcomes of substantive CSR and avoiding negative externalities, thereby contributing to local social welfare and sustainable development. However, their choice of monitoring strategies is shaped by multiple influences. When subsidiaries engage in symbolic CSR, they often employ non-market strategies to influence external stakeholders’ decisions, reducing both the willingness and the intensity of monitoring [54]. For example, Lyon and Montgomery show that firms can project an image of responsible corporate citizenship through carefully managed CSR communications and green branding campaigns [55]. Although there may be a gap between projected images and actual conduct, resource-constrained external stakeholders face high information-verification costs to assess true performance. Consequently, when surface evidence appears favorable, they often regard active monitoring as unnecessary and costly and instead adopt passive monitoring, which lowers their incentives to monitor [56].

Moreover, subsidiaries may cultivate vested interests with key stakeholders—through reciprocal alliances, political lobbying, community engagement, or local-media advertising—creating private benefits that motivate stakeholders to preserve mutually beneficial arrangements [57]. Under these conditions, co-optation by overseas subsidiaries reduces external stakeholders’ incentives to monitor actively and inclines them toward passive monitoring.

By contrast, incentives from parent companies can provide external stakeholders with the resources needed to support monitoring. Information feedback from stakeholders can also broaden parent companies’ information channels and reduce the cost of strict supervision, in turn strengthening parents’ willingness to supervise [58]. Therefore, effective supervision of subsidiary CSR conduct requires coordination between parent companies and external stakeholders.

4. Model Assumptions and Construction

4.1. Model Assumptions

To investigate the evolution of decision making in the MNE’s CSR governance system under the influence of external stakeholders, this study develops an analytical framework based on evolutionary game theory (EGT). The framework captures dynamic strategic adaptation among the parent company, the overseas subsidiary, and the external stakeholder through mathematical modeling, simulating how strategies evolve under varying conditions [47]. By identifying key parameters and interaction patterns, it enables systematic optimization of decisions and strengthens the adaptability and sustainability of the MNE’s governance system. The model rests on the following assumptions, which enable analysis of equilibrium stability and the mechanisms through which parameters affect outcomes:

Assumption 1.

The MNE parent company is designated as Player 1, the overseas subsidiary as Player 2, and the external stakeholder as Player 3. Each player represents a population of boundedly rational agents whose strategy frequencies evolve over time and may converge to a stable equilibrium.

Assumption 2.

The strategy set of the parent company is defined as , where denotes the probability of selecting , and that of . The overseas subsidiary’s strategy set is , with representing the probability of choosing , and that of . The external stakeholders’ strategy set is , where indicates the probability of adopting , and that of . In this setting, strict supervision means that the parent company adopts a high-intensity monitoring regime to enforce group-wide CSR standards, whereas lenient supervision denotes a low-intensity or largely hands-off approach. Substantive CSR refers to the subsidiary’s allocation of real resources to adjust core operations and management systems to achieve genuine social and environmental performance, while symbolic CSR emphasizes communication and formal policies that project CSR compliance with only limited changes in underlying practices. Active monitoring captures the external stakeholders’ choice to invest effort in collecting, verifying, and reacting to information on the subsidiary’s CSR behavior, whereas passive monitoring reflects a low-effort stance that fails to exert effective oversight over the subsidiary’s CSR behavior.

Assumption 3.

Under strict supervision, the parent company incurs a supervision cost . It provides financial support to an overseas subsidiary that adopts substantive CSR and imposes a financial penalty on a subsidiary engaging in symbolic CSR. When the external stakeholder chooses active monitoring, the parent company offers enhanced cooperation ; when the external stakeholder chooses passive monitoring, the level of cooperation is reduced by . Under lenient supervision, the parent company does not bear supervision costs but suffers an image loss . If the subsidiary engages in symbolic CSR under lenient supervision, the parent company additionally incurs a reputational loss and subsequent public relations and management costs . Substantive CSR by the subsidiary generates a reputational benefit for the parent company. Active monitoring by the external stakeholder creates an information synergy benefit for the parent, whereas passive monitoring requires the parent company to bear an additional information acquisition cost in its supervision efforts.

Assumption 4.

The overseas subsidiary earns a reputational benefit from CSR activities in the host country and bears a fixed operating cost for routine CSR reporting and related activities. The implementation cost of substantive CSR is , while symbolic CSR costs , with , reflecting the higher resource intensity of substantive CSR relative to symbolic CSR. When pursuing symbolic CSR, the subsidiary incurs a co-optation cost through public relations efforts and benefit transfers to external stakeholders to avoid exposure of inconsistent practices, where so that symbolic CSR remains privately attractive in the absence of effective monitoring. Symbolic CSR also entails a speculative cost , mainly associated with false advertising and fabricated CSR activities, and a potential cost if symbolic CSR is exposed. If symbolic CSR is detected through active monitoring by the external stakeholder, the subsidiary is unable to obtain reputational benefits. By contrast, when the subsidiary adopts substantive CSR, it can receive a feedback benefit from an actively monitoring external stakeholder, including capital market returns, cost sharing, and technical support.

Assumption 5.

Substantive CSR by the overseas subsidiary produces a benefit for the external stakeholder (e.g., improved environmental and social outcomes). When the external stakeholder engages in active monitoring, it bears a monitoring cost ; passive monitoring involves a lower direct cost but carries a potential cost arising from credibility loss, environmental deterioration, and ethical consequences, with . This ordering captures the idea that passive monitoring appears cheaper in the short run but may be more costly in the long run if symbolic CSR persists. Under passive monitoring, the external stakeholder may accept a co-optation benefit from the subsidiary and may facilitate the concealment of symbolic CSR practices.

The inequality conditions (e.g., , , and ) ensure the economic plausibility of the parameterization and provide a consistent ordering of costs and benefits across strategies. In the numerical experiments, all parameter values were chosen to satisfy these orderings, and the simulations varied the levels of key parameters within these plausible ranges to examine how changes in the payoff structure affect the evolutionary trajectories and the stability of alternative equilibria. The model parameters and their meanings are summarized in Table 1.

Table 1.

Description of model parameters and meanings.

4.2. Model Construction

The payoff matrix is the fundamental analytical instrument in the tripartite evolutionary game. It maps the payoffs of the parent company, the overseas subsidiary, and the external stakeholder for each strategy profile. The matrix clarifies the logic of payoff allocation in CSR governance and provides the basis for the replicator dynamics. Furthermore, it allows assessment of the economic plausibility of various evolutionary stable states. Accordingly, Table 2 reports the complete payoff matrix for the three players.

Table 2.

Payoff matrix of tripartite game.

5. Evolutionary Game Analysis

The stability analysis of each player’s strategy clarifies how the parent company, the subsidiary and external stakeholders adjust their behaviors under different cost–benefit structures. It highlights the key parameters and thresholds that drive their respective strategy choices in the evolutionary game.

5.1. Stability Analysis of the Parent Company’s Strategy

The parent company’s expected returns for strict supervision , lenient supervision and its average return are as follows:

The replicator dynamics equation for the parent company is given by:

The first derivative of is

According to the stability theorem of replicator dynamics, the parent company’s strategy of strict supervision reaches a stable state when , and , at which point it constitutes an evolutionarily stable strategy (ESS).

(1) When

, indicates that all variables are in a stable state, and the stabilization strategy cannot be determined.

(2) When , and emerge as two possible equilibrium points of . According to the stability theorem of replicator dynamics, a state constitutes an ESS when .

① When At this point, is the ESS for the parent company, which corresponds to the choice of strict supervision.

② When Under this condition, constitutes the ESS for the parent company, which corresponds to a tendency toward lenient supervision. Based on the preceding analysis, the phase diagram for the parent company’s strategy evolution is shown in Figure 2, the arrows indicate how the system moves over time toward its stable state under different situation.

Figure 2.

Phase diagram for the parent company’s strategy evolution.

As shown in Figure 2, the volume represents the probability of the parent company adopting strict supervision, while the probability of lenient supervision equals the volume . The calculations are as follows:

The partial derivatives of with respect to each element are obtained as follows:

Which shows that parent companies’ propensity for strict supervision increases with reputational costs, reputational repair expenses, penalties on subsidiaries for symbolic CSR, reduced cooperation with passively monitoring stakeholders, and informational benefits from actively monitoring stakeholders. Conversely, it decreases with increases in the costs of supervision, the costs of information acquisition, the rewards granted to subsidiaries for substantive CSR, and collaborative investment in actively monitoring stakeholders.

The stability analysis of the parent company’s strategy yields clear managerial levers. To effectively incentivize strict supervision, the parent company should acknowledge the potential reputational damage () and subsequent remediation cost () associated with subsidiary misconduct and treat proactive supervisory investment () as a means of preventing these losses. Furthermore, the parent company can strategically reconfigure its resource allocation by linking substantial penalties for symbolic CSR () directly to increased support for substantive practice , and by calibrating cooperation benefit (, ) to actively reward stakeholders who contribute to its information network. Ultimately, by building collaborative platforms with key external stakeholders, the parent company can leverage external monitoring to lower its own information acquisition cost (), creating a cost-effective system to safeguard the MNE’s global reputation.

5.2. Stability Analysis of the Overseas Subsidiary’s Strategy

The overseas subsidiary’s expected returns for substantive CSR , symbolic CSR and its average return are as follows:

The replicator dynamics equation for the overseas subsidiary is given by:

The first derivative of is

According to the stability theorem of replicator dynamics, the overseas subsidiary’s substantive CSR strategy reaches a stable state when , and , at which point it constitutes an ESS.

(1) When

, indicates that all variables are in a stable state, and the stabilization strategy cannot be determined.

(2) When , and emerge as two possible equilibrium points of . According to the stability theorem of replicator dynamics, a state constitutes an ESS when .

① When . At this point, is the ESS for the overseas subsidiary, which corresponds to the choice of symbolic CSR.

② When Under this condition, constitutes the ESS for the overseas subsidiary, which corresponds to a tendency toward substantive CSR. Based on the preceding analysis, the phase diagram for the overseas subsidiary’s strategy evolution is shown in Figure 3, the arrows indicate how the system moves over time toward its stable state under different situation.

Figure 3.

Phase diagram for the overseas subsidiary’s strategy evolution.

As shown in Figure 3, the volume represents the probability of the overseas subsidiary choosing substantive CSR, while the probability of symbolic CSR equals the volume . The calculations are as follows:

The partial derivatives of with respect to each element are obtained as follows:

The results indicate that the probability of overseas subsidiaries adopting substantive CSR increases with several factors: reputational benefits from substantive CSR, positive stakeholder feedback, co-optation costs of concealing symbolic CSR, speculative costs, and potential exposure costs of symbolic CSR. This probability also increases with stronger parental incentives and penalties, and a narrowing cost advantage of symbolic over substantive CSR.

The stability analysis of the subsidiary’s strategy reveals that its choice is not inherently fixed but is a rational response to the incentive structure shaped by the parent company and external stakeholders. Substantive CSR becomes the subsidiary’s stable strategy only when the combined reputational, financial, and feedback benefits ( + + ) sufficiently exceed the net advantages of symbolic CSR, which are determined by its cost savings (−) minus the co-optation, speculative, and expected penalty costs ( + + + ). For the parent company, this implies that merely setting CSR mandates is insufficient; it must actively engineer a payoff structure that makes substantive CSR the most rational and attractive choice for subsidiary managers. This can be achieved by systematically enhancing the tangible rewards for substantive actions while simultaneously increasing the tangible costs and risks associated with symbolic ones. Conversely, a laissez-faire approach that fails to bridge the cost differential between substantive and symbolic CSR or to ensure credible deterrence is likely to lead subsidiaries to gravitate toward the more economically advantageous, albeit irresponsible, strategy, thereby undermining the MNE’s global CSR objectives.

5.3. Stability Analysis of the External Stakeholder’s Strategy

The external stakeholder’s expected returns for active monitoring , passive monitoring and its average return are as follows:

The replicator dynamics equation for the external stakeholder is given by:

The first derivative of is

According to the stability theorem of replicator dynamics, the external stakeholder’s active monitoring strategy reaches a stable state when , and , at which point it constitutes an ESS.

(1) When

, indicates that all variables are in a stable state, and the stabilization strategy cannot be determined.

(2) When , and emerge as two possible equilibrium points of . According to the stability theorem of replicator dynamics, a state constitutes an ESS when .

① When At this point, is the ESS for external stakeholders, which corresponds to the choice of passive monitoring.

② When Under this condition, constitutes the ESS for external stakeholders which corresponds to a tendency toward active monitoring. Based on the preceding analysis, the phase diagram for the external stakeholders’ strategy evolution is shown in Figure 4, the arrows indicate how the system moves over time toward its stable state under different situation.

Figure 4.

Phase diagram for the external stakeholders’ strategy evolution.

As shown in Figure 4, the volume represents the probability of the external stakeholder adopting active monitoring, while the probability of passive monitoring equals the volume . The calculations are as follows:

The partial derivatives of with respect to each element are obtained as follows:

The results indicate that the likelihood of external stakeholders adopting active monitoring increases with the parent company’s cooperative investment and the cost of passive monitoring. Conversely, it is diminished by both the direct costs of active monitoring and the subsidiary’s co-optation of stakeholders to conceal symbolic CSR practices.

The stability analysis of external stakeholder strategies suggests that the parent company cannot simply assume that external monitoring will always function as a reliable governance substitute. Active monitoring is more likely to be sustained only when the benefits that external stakeholders derive from substantive CSR and cooperation with the parent company are sufficiently substantial to justify continued monitoring efforts. For the parent company, this implies that offering credible cooperation benefits be are not merely “nice-to-have” instruments, but key levers to keep external stakeholders in an active, co-governance role and thereby reduce its own effective supervision cost. Conversely, if the parent company fails to create such incentive-compatible conditions, external stakeholders may remain locked in passive monitoring, forcing the parent company to rely more heavily on costly internal supervision or to face a higher risk that symbolic CSR at the subsidiary level goes undetected.

5.4. Stability Analysis of Equilibria in the Evolutionary Game

The overall stability analysis evaluates the joint dynamical system and compares the stability of all equilibrium points. It shows under which parameter constellations the tripartite game converges to a virtuous cycle such as , thereby providing a theoretical basis for treating this equilibrium as the target CSR governance regime.

Based on an analysis of the strategic stability among the three parties, we model the system’s dynamics using the following three-dimensional replicator dynamics:

From it can be obtained that there are eight system equilibrium points in the evolutionary system:

. Following the methods of Zhou et al. and Zeng et al. [59,60], the stability of equilibrium points can be analyzed using the system’s eigenvalues. The Jacobian matrix of the differential system is obtained as:

Using the first method of Lyapunov, an equilibrium is locally asymptotically stable if all eigenvalues of the Jacobian evaluated at that point have negative real parts. If at least one eigenvalue has a positive real part, the equilibrium is unstable. The stability analysis of equilibrium points to is shown in Table 3.

Table 3.

Stability analysis of equilibrium points.

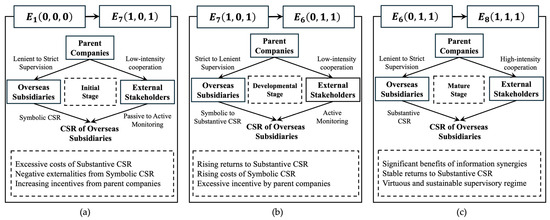

The stability conditions are reported in Table 4. Analysis of the eight equilibria shows that the strategic choices of parent companies, overseas subsidiaries, and external stakeholders are governed by their relative benefits and costs. Under appropriate parameter values, the system converges to strict supervision by the parent company, substantive CSR by overseas subsidiaries, and active monitoring by external stakeholders. Reflecting the typical trajectory of subsidiaries entering host markets, we delineate three stages in the evolution of CSR behavior: the initial stage, the development stage, and the mature stage.

Table 4.

Analysis of stability conditions.

Initial stage: During the initial entry phase, overseas subsidiaries encounter significant adaptation pressures and intense competition (Figure 5). The high cost of implementation makes Substantive CSR economically unattractive. In the absence of stringent supervision from parent companies and active monitoring by external stakeholders, subsidiaries often free ride on the MNEs’ reputational resources to gain legitimacy. As a result, they adopt symbolic CSR and conceal such behavior through co-optation tactics.

Figure 5.

Stages in the evolution of MNEs’ CSR governance. (a) Initial Stage; (b) Developmental Stage; (c) Mature Stage.

Constrained by limited information and high supervision costs, parent companies lack accurate insight into subsidiary activities and rationally choose lenient supervision. Similarly, external stakeholders face considerable information asymmetry and monitoring costs in the early stage. Influenced by the MNE’s global reputation and targeted co-optation activities by the subsidiary, they tend to adopt passive monitoring.

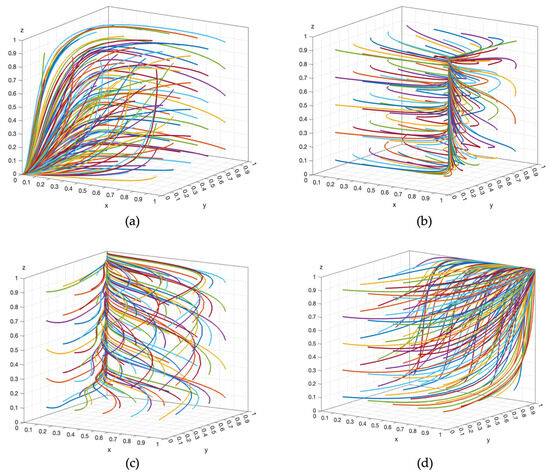

Therefore, the system stabilizes at equilibrium in the initial stage, which corresponds to lenient supervision, symbolic CSR, and passive monitoring. The specific stability conditions are reported in Table 4, and the corresponding evolutionary path is shown in Figure 6a, each color represents a trajectory of the system under a different initial condition.

Figure 6.

The evolution path of the system equilibrium points. (a) Evolutionary trajectory in the initial stage; (b) Evolutionary trajectory in the developmental stage ①; (c) Evolutionary trajectory in the developmental stage ②; (d) Evolutionary trajectory in the mature stage.

Developmental Stage ①: As overseas subsidiaries continue operating in the host country, the sustained practice of symbolic CSR gradually reveals its negative impacts (Figure 5). In response to the reputational damage, parent companies adopt proactive reward and punishment mechanisms to mitigate these effects. Meanwhile, external stakeholders turn to active monitoring when the negative externalities generated by the subsidiary exceed the benefits gained from its co-optation efforts. The system stabilizes at , with the evolutionary path shown in Figure 6b.

Developmental Stage ②: After intervention by parent companies and external stakeholders, overseas subsidiaries face rising costs of symbolic CSR alongside growing benefits from substantive CSR (Figure 5). As operations expand in host countries, the long-term value of substantive CSR becomes more apparent. Driven by these combined pressures and incentives, overseas subsidiaries shift toward substantive CSR practices.

However, strict supervision entails high costs for parent companies. If external stakeholders do not provide sufficient benefits from information synergies to offset these costs, and overseas subsidiaries have already adopted substantive CSR, parent companies may gradually relax supervision under budgetary constraints [52]. The system reaches equilibrium , as depicted in Figure 6c.

Mature Stage: In the mature stage, sustained active monitoring by external stakeholders provides parent companies with effective benefits from information synergies, substantially lowering supervision costs. At the same time, reputational risks associated with previous lenient supervision motivate parent companies to resume a sustainable level of strict supervision.

With external stakeholders maintaining active monitoring, overseas subsidiaries are consistently motivated to adopt substantive CSR to preserve long-term reputation. The system thus achieves the desired equilibrium , as shown in Figure 6d. All phase simulations in Figure 6 are based on 50 evolutionary iterations.

6. Numerical Simulations of the Evolutionary Game Model

The numerical simulation complements the analytical results by visualizing evolutionary trajectories and testing robustness to initial conditions and parameter changes. It verifies that the chosen parameter values lead the system toward the desired equilibrium and offers intuitive insight into how policy levers and governance arrangements affect long-run CSR outcomes.

To visually verify the evolutionarily stable strategies of the three players and investigate the impacts of initial propensities and key parameters on system dynamics, we conduct a numerical analysis of the tripartite evolutionary game using MATLAB (2021b). Equilibrium signifies that the system has entered a virtuous cycle, defined by strict parental supervision, substantive subsidiary CSR, and active external monitoring, representing the most desirable evolutionary outcome. Therefore, we configure the model parameters to satisfy the stability conditions for : .

Existing tripartite evolutionary game studies provide useful guidance for calibrating the relative magnitudes of costs, penalties and reputational payoffs in our model. Chang et al. show that green production only becomes evolutionarily stable when the combined benefits of government supervision, public participation, subsidies and reputational gains exceed the associated production and monitoring costs [61]. Liu et al. find that sufficiently strong penalties and rewards are required to deter manufacturers’ greenwashing in the electric-vehicle industry [62]. Li et al. demonstrate that blockchain-based information transparency substantially raises the expected cost of greenwashing [63]. Liu et al. show that only appropriately scaled rewards and sanctions can make truthful ESG disclosure evolutionarily stable under heterogeneous risk preferences [64].

Taken together, these studies suggest that the costs of substantive CSR practices are far higher than those of symbolic initiatives, while strong external regulatory sanctioning mechanisms and reputational considerations in practice exert a significant influence on firms’ CSR strategy choices. From the perspective of CSR practice in MNEs, the OECD Global Corporate Sustainability Report 2024 and the KPMG Global Survey of Sustainability Reporting 2024 document pronounced differences in the quality, credibility and enforcement of sustainability reporting among large multinational enterprises, thereby providing practice-based references for our parameter setting [2,65]. Considering this practical context of CSR supervision in MNEs and drawing on the above literature and reports, we therefore assign the initial parameter values in the model as follows:

6.1. Simulation Analysis of Initial Strategies

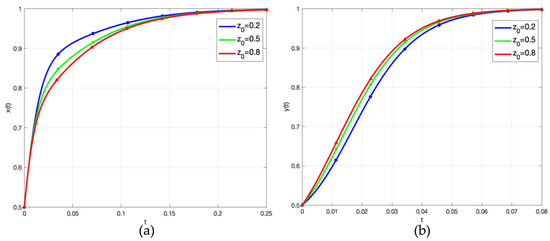

To examine the impact of initial strategies on system evolution, we further conduct numerical simulations by varying the initial propensities of strict supervision by parent companies, substantive CSR by overseas subsidiaries, and active monitoring by the external stakeholders, assigning values of 0.2, 0.5, and 0.8 to represent low, medium, and high initial propensities, respectively. This setup allows a systematic analysis of how initial strategic inclinations shape the system’s evolutionary path.

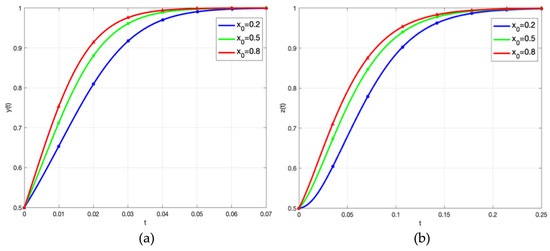

6.1.1. Impact of the Parent Company’s Initial Strategy

Figure 7a shows that when , a higher initial propensity of strict supervision by parent companies accelerates overseas subsidiaries’ convergence to substantive CSR. This suggests that a strong initial supervisory stance from parent companies effectively promotes substantive CSR by overseas subsidiaries. Correspondingly, Figure 7b indicates that a higher also hastens the convergence of external stakeholders toward active monitoring under the same conditions.

Figure 7.

Impact of initial strategic propensity of the parent company. (a) Impact of initial strategic propensity of the parent company on the overseas subsidiary; (b) Impact of initial strategic propensity of the parent company on the external stakeholder.

6.1.2. Impact of the Overseas Subsidiary’s Initial Strategy

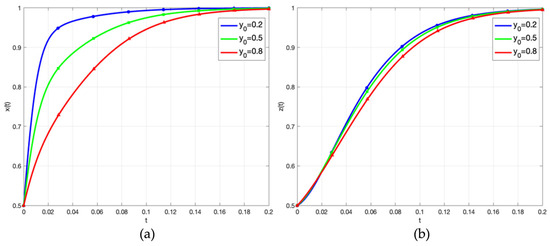

As shown in Figure 8a, with , a lower initial propensity of overseas subsidiaries for substantive CSR accelerates parent companies’ convergence to strict supervision. This implies that irresponsible CSR behavior by subsidiaries triggers stricter parental supervision.

Figure 8.

Impact of initial strategic propensity of the overseas subsidiary. (a) Impact of initial strategic propensity of the overseas subsidiary on the parent company; (b) Impact of initial strategic propensity of the overseas subsidiary on the external stakeholders.

Meanwhile, Figure 8b reveals that a low slows the convergence of external stakeholders toward active monitoring. However, as the game evolves, subsidiaries’ low CSR commitment induces stricter parental supervision, which subsequently promotes active monitoring among external stakeholders through enhanced incentives. This dynamic reflects the complex strategic interdependence among the three players.

6.1.3. Impact of the External Stakeholders’ Initial Strategy

As shown in Figure 9a, when , a lower initial propensity of active monitoring by external stakeholders accelerates parent companies’ convergence to strict supervision. Conversely, Figure 9b shows that a higher speeds overseas subsidiaries’ convergence to substantive CSR. These findings suggest that active monitoring by external stakeholders both reduces supervision pressure on parent companies and fosters more substantive CSR by overseas subsidiaries.

Figure 9.

Impact of initial strategic propensity of the external stakeholder. (a) Impact of initial strategic propensity of the external stakeholder on the parent company; (b) Impact of initial strategic propensity of the external stakeholder on the overseas subsidiary.

6.2. Simulation Analysis of Parameter Sensitivity

To analyze the impact of different parameters on tripartite decision making, this section conducts a sensitivity analysis under the equilibrium .

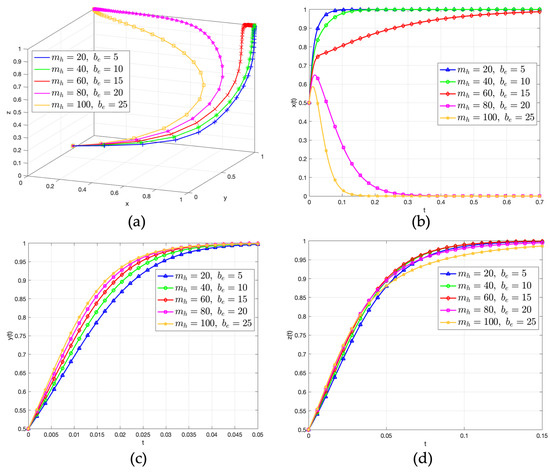

6.2.1. Impact of Parent Company Incentives on Evolutionary Outcomes

Figure 10 shows the evolutionary trajectories of the three players when the parent company’s financial incentive for subsidiaries’ substantive CSR () is set to 20, 40, 60, 80, 100, and its collaborative investment with external stakeholders () is set to 5, 10, 15, 20, 25, respectively, while other parameters remain at baseline values.

Figure 10.

Impact of parent company incentives () on evolutionary trajectories. (a) The system evolution results; (b) Impact of parent company incentives on the parent company; (c) Impact of parent company incentives on the overseas subsidiary; (d) Impact of parent company incentives on the external stakeholder.

Analysis of Figure 10a,b indicates that a moderate incentive level promotes the system’s convergence to the desired tripartite equilibrium . When incentives exceed a threshold, the parent company’s willingness to maintain strict supervision weakens and the system tends to converge to . Figure 10c,d further show that increasing incentive intensity accelerates the overseas subsidiary’s convergence toward substantive CSR and external stakeholders’ convergence toward active monitoring. However, once the incentive intensity becomes excessively high, the parent company shifts from strict supervision to lenient supervision. These results imply that properly calibrated incentives foster substantive CSR and active monitoring, but excessive incentives raise costs and crowd out strict supervision. Therefore, a stable, high-performing equilibrium cannot rely solely on incentives; it also requires robust multi-stakeholder collaborative governance.

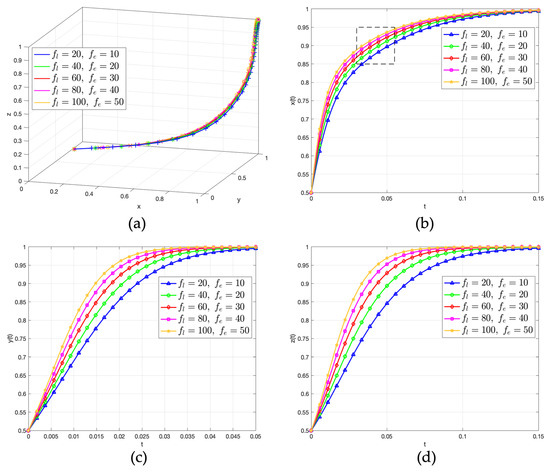

6.2.2. Impact of Parent Company Penalties on Evolutionary Outcomes

Figure 11 shows the evolutionary trajectories of the three players when the parent company’s penalty for subsidiaries’ symbolic CSR () is set to 20, 40, 60, 80, 100, and its reduced cooperation with external stakeholders () is set to 10, 20, 30, 40, 50, respectively, while other parameters remain at baseline values.

Figure 11.

Impact of parent company penalties () on evolutionary trajectories. (a) The system evolution results; (b) Impact of parent company penalties on the parent company; (c) Impact of parent company penalties on the overseas subsidiary; (d) Impact of parent company penalties on the external stakeholder.

Analysis of Figure 11a indicates that, with other parameters held constant, higher penalty intensity from the parent company accelerates the system’s convergence to the desired equilibrium . Figure 11b–d further show that higher penalty intensity increases the probability of the parent company’s strict supervision and accelerates the overseas subsidiary’s convergence toward substantive CSR and external stakeholders’ convergence toward active monitoring. These results imply that properly calibrated penalties raise the expected cost of symbolic CSR and passive monitoring, thereby improving enforceability and deterrence and facilitating cooperation under strict supervision. Therefore, in designing CSR governance for MNEs, parent companies should establish clear penalty clauses and, where effective, moderately intensify them as a key instrument within robust multi-stakeholder collaborative governance.

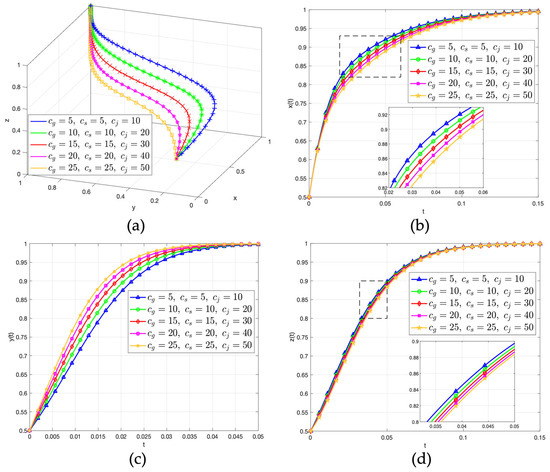

6.2.3. Impact of Overseas Subsidiary Opportunism-Related Costs on Evolutionary Outcomes

Figure 12 shows the evolutionary trajectories of the three players when the co-optation cost of symbolic CSR () is set to 5, 10, 15, 20, and 25, the opportunism cost () is set to 5, 10, 15, 20, and 25, and the potential cost of exposure () is set to 10, 20, 30, 40, and 50, while other parameters remain at baseline values.

Figure 12.

Impact of opportunism-related costs () on evolutionary trajectories. (a) The system evolution results; (b) Impact of opportunism-related costs on the parent company; (c) Impact of opportunism-related costs on the overseas subsidiary; (d) Impact of opportunism-related costs on the external stakeholder.

Figure 12a shows that, holding other parameters constant, increases in the opportunity, co-optation, and potential exposure cost of symbolic CSR for overseas subsidiaries accelerate the system’s convergence to the desired equilibrium . Furthermore, Figure 12b–d show that, as the opportunism-related costs rise, subsidiaries accelerate their transition toward substantive CSR, whereas the parent company’s shift to strict supervision and external stakeholders’ move to active monitoring both decelerate. Higher opportunism-related costs increase the relative payoff of substantive CSR for profit-maximizing subsidiaries, prompting a shift that reduces the parent companies’ pressure for strict supervision and thereby lowers their willingness to maintain strict supervision. At the same time, increased co-optation investment by overseas subsidiaries raises the relative payoff of passive monitoring for external stakeholders, thereby slowing their transition to active monitoring. Overall, changes in the subsidiary’s cost structure not only steer its own behavior but also reconfigure the payoff landscape for all three players, reshaping the system’s evolutionary trajectory.

6.2.4. Impact of Substantive and Symbolic CSR Cost on Evolutionary Outcomes

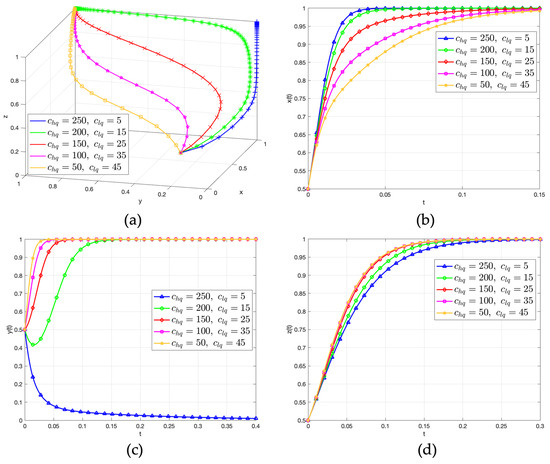

Figure 13 shows the evolutionary trajectories of the three players when the cost of substantive CSR for overseas subsidiaries ( is set to 250, 200, 150, 100, 50 and the cost of symbolic CSR ( is set to 5, 15, 25, 35, 45, respectively, while all other parameters remain at their baseline values.

Figure 13.

Impact of substantive and symbolic CSR cost () on evolutionary trajectories. (a) The system evolution results; (b) Impact of substantive and symbolic CSR cost on the parent company; (c) Impact of substantive and symbolic CSR cost on the overseas subsidiary; (d) Impact of substantive and symbolic CSR cost on the external stakeholder.

As shown in Figure 13a, with all other parameters held constant, a decrease in the cost of substantive CSR relative to symbolic CSR shifts the evolutionary outcome from to the desired equilibrium . By contrast, Figure 13b indicates that a widening cost gap accelerates the parent company’s move toward strict supervision, while Figure 13c shows a declining propensity among overseas subsidiaries to adopt substantive CSR. Once this gap exceeds a critical threshold, overseas subsidiaries revert to symbolic CSR and external stakeholders scale back active monitoring (Figure 13d). These findings highlight that narrowing the cost gap between substantive and symbolic CSR is essential for promoting sustainable governance, suggesting that MNEs should consider providing technical assistance, enhancing supply chain transparency, and pursuing third-party certification to lower the implementation costs of substantive CSR and facilitate convergence to the high-level governance equilibrium.

6.2.5. Impact of the Benefit from Information Synergies and the Additional Information Acquisition Cost on Evolutionary Outcomes

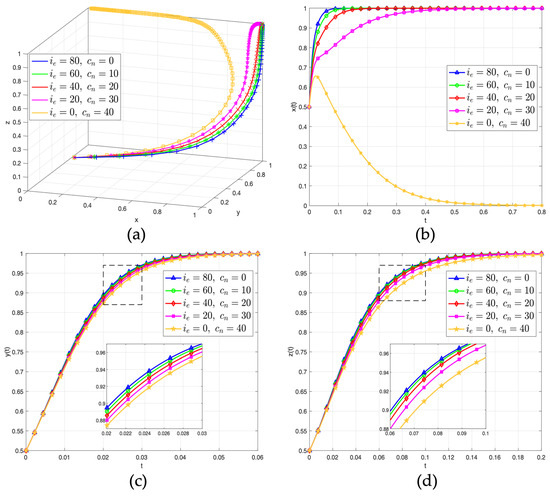

Figure 14 shows the evolutionary trajectories of the three players when the benefit from information synergies () is set to 80, 60, 40, 20, 0, and the information acquisition cost () is set to 0, 10, 20, 30, 40, respectively, while other parameters remain at baseline values.

Figure 14.

Impact of the benefit from information synergies and the additional information acquisition cost () on evolutionary trajectories. (a) The system evolution results; (b) Impact of Information Synergies and information acquisition costs on the parent company; (c) Impact of Information Synergies and information acquisition costs on the overseas subsidiary; (d) Impact of Information Synergies and information acquisition costs on the external stakeholder.

As shown in Figure 14a, with all other parameters held constant, an increase in the benefit from information synergies together with a reduction in the additional information acquisition cost shifts the evolutionary outcome from equilibrium to the desired tripartite equilibrium by increasing the parent company’s payoff from strict supervision. Figure 14b–d show that a greater benefit from information synergies and a lower additional information acquisition cost increase the parent company’s incentive to enforce strict supervision, which in turn accelerates subsidiaries’ adoption of substantive CSR and external stakeholders’ shift to active monitoring. Conversely, as the benefit from information synergies declines and the additional information acquisition cost rises, the parent company’s convergence toward strict supervision gradually slows; when the disparity between cost and benefit becomes sufficiently large, supervision shifts toward leniency. Therefore, MNEs should strengthen collaboration with external stakeholders, for example, by establishing information-sharing platforms, to expand information synergies, reduce information acquisition costs, and facilitate faster convergence of the CSR governance system toward the desired equilibrium.

7. Discussion and Conclusions

7.1. Conclusions

Based on the evolutionary interactions among decision-makers in MNEs’ CSR governance systems, this study develops a tripartite evolutionary game model encompassing the MNE parent companies, their overseas subsidiaries, and external stakeholders. By examining the interests, behaviors, and key determinants of these actors, we analyze the dynamic evolution and stability of CSR governance under the influence of external stakeholders. Our stability analysis and numerical simulations lead to three principal conclusions.

First, parent companies are more likely to adopt strict supervision when the expected losses from reputational damage, group-wide spillover risks, and high ex post remediation costs exceed the direct costs of strict supervision. Benefits from information-sharing governance with external stakeholders further strengthen this propensity. However, excessive incentive outlays can weaken parent companies’ tendency to strict supervision, consistent with Cuervo-Cazurra et al. [66].

Second, for overseas subsidiaries, adopting substantive CSR is a rational choice when institutional and market pressures make its net benefits, including parental incentives, host-country reputational capital, and lower compliance risk, exceed the opportunistic gains from symbolic CSR.

Finally, external stakeholders are more likely to engage in active monitoring when cooperation from parent companies and reputational returns to vigilant oversight exceed co-optation benefits from overseas subsidiaries and monitoring costs. An effective CSR supervision framework should calibrate the cost–benefit interdependencies among all players. With appropriate institutional design, the tripartite interaction can reach a synergistic governance equilibrium that delivers a stable and efficient system outcome.

7.2. Theoretical Contributions

The findings of this study add a dynamic, triadic governance perspective to stakeholder theory. Existing stakeholder research typically conceptualizes governments, NGOs, the media, and other societal actors as external sources of pressure that influence firms’ CSR choices, but often treats their influence as exogenous and unidirectional. In our evolutionary game, the monitoring strategy of the external stakeholder is modeled as a strategic response to the expected benefits and costs of engaging in scrutiny, exposure, or support. Under certain parameter constellations, external stakeholders may endogenously evolve into “co-governors” of CSR rather than remaining passive audiences.

More specifically, the model indicates that when monitoring costs are sufficiently low, sanctions for CSR opportunism are sufficiently strong, and information synergies between the parent company and external stakeholders are sufficiently high, active monitoring can become self-reinforcing. In such cases, the external stakeholder’s expected payoff from continued engagement exceeds the payoff from passivity, which is consistent with stakeholder theory’s emphasis on the importance of both motivation and influence capacity for stakeholder action. At the same time, the presence of an alternative stable configuration characterized by lenient supervision, symbolic CSR, and passive monitoring suggests that, although the CSR behavior of overseas subsidiaries is closely intertwined with the social welfare of external stakeholders, under certain parameter conditions, these stakeholders may nonetheless withdraw from active oversight because the payoff structure does not justify sustained monitoring. This outcome implies a risk of ineffective external regulation.

By explicitly endogenizing the external stakeholders’ strategy and tracing its co-evolution with the strategies of the parent company and the overseas subsidiary, this study contributes to stakeholder theory in at least two ways. First, it provides a formal micro-foundation for when and how external stakeholders can move from the periphery to the center of CSR governance in multinational settings, complementing internal control mechanisms rather than simply exerting background pressure. Second, it highlights the role of information synergies between headquarters and external stakeholders as a distinct channel through which firms can shape stakeholder engagement, suggesting that firms are not only constrained by stakeholder pressure but may also strategically configure the information environment to activate or strengthen external monitoring.

7.3. Managerial Implications

Based on the study’s findings, the following recommendations are offered to advance MNE CSR governance toward a synergistic equilibrium among the three actors.

For MNE parent companies, sustaining a global brand image requires not only curbing subsidiary opportunism through incentives and sanctions, but also empowering subsidiaries to engage in substantive CSR with technological, financial, and managerial support. Furthermore, they should also build an information synergy governance system with external stakeholders to convert host-country feedback into effective supervisory resources, thereby lowering monitoring costs caused by information asymmetry. Greater transparency and disclosure at the parent level can raise awareness of subsidiaries’ CSR standards and performance, increasing the expected cost of Symbolic CSR.

For overseas subsidiaries, implementing global CSR standards requires reframing CSR from a compliance expense to a strategic investment in long-term competitiveness. Short-term opportunistic actions may reduce immediate costs, but they entail substantial reputational and regulatory risks. In contrast, substantive CSR engagement helps subsidiaries gain legitimacy and consumer trust in host markets. Therefore, overseas subsidiaries should integrate CSR into local strategy and daily operations while maintaining transparency to preserve the MNE’s global reputation. Through such efforts, they can foster collaborative relationships with parent companies and external stakeholders, positioning themselves for sustainable and stable growth in their host countries.

For external stakeholders, whose monitoring strongly influences CSR implementation. Objective and professional monitoring enhances their credibility, thereby enabling them to impose meaningful constraints on corporate behavior while offering market-based reputational incentives to overseas subsidiaries with proven CSR performance. By sharing information and coordinating with parent companies, stakeholders can generate governance synergies that improve CSR performance across subsidiaries, thereby contributing to social welfare in host countries.

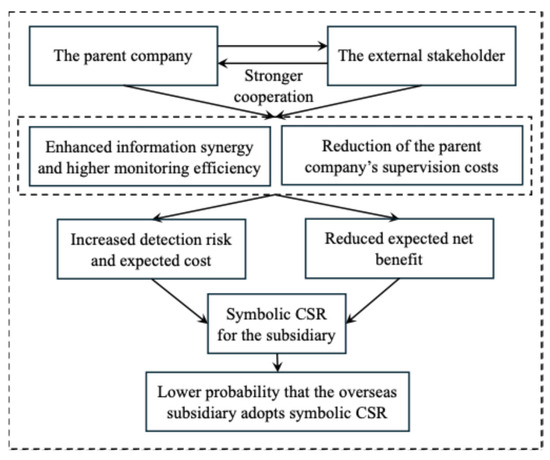

Practically, Figure 15 shows that stronger cooperation between the parent company and external stakeholders enhances information synergy and monitoring efficiency while reducing the parent company’s supervision costs, which in turn increases the detection risk and expected cost of symbolic CSR and lowers its expected net benefit for the subsidiary, thereby reducing the probability that the overseas subsidiary adopts symbolic CSR. This framework is especially relevant for MNEs operating in high-risk, stakeholder-sensitive sectors such as extractives, apparel, and digital platforms, where cross-border reputational spillovers and NGO/media scrutiny closely mirror the triadic governance structure modeled in this study. Moreover, by recalibrating key parameters such as monitoring costs, penalty intensity, and reputational returns to reflect differences in institutional strength and civil society capacity, the model can be adapted to compare CSR governance trajectories across regional contexts.

Figure 15.

Mechanism linking parent company–stakeholder cooperation to the probability of overseas subsidiaries’ symbolic CSR.

7.4. Limitations and Future Research

While this study offers systematic insights into the evolutionary trajectory of MNEs’ CSR governance under the influence of external stakeholders, several limitations remain, which could lead to further refinement in future research.

First, by grouping diverse entities such as governments, local communities, NGOs and the media into a single category of “external stakeholders,” the model may over-simplify the structural complexity of real-world CSR governance systems. This study does not distinguish between specific external actors in order to maintain analytical tractability and focus on the core interaction mechanism. This abstraction prevents us from capturing the heterogeneous roles, motivations and influence channels of individual external actors, as well as their potential interactions, complementarities and conflicts. As a result, the model cannot reveal how different combinations of regulatory agencies, NGOs, media and other societal actors may generate distinct CSR governance outcomes. Future research could therefore develop more fine-grained, multi-actor evolutionary game models that explicitly differentiate these external stakeholders and examine how their distinct roles and interdependencies jointly shape the evolution of subsidiaries’ CSR strategies.

Second, the model relies on theoretically informed parameters and idealized assumptions, and it abstracts from host-country heterogeneity, sectoral CSR requirements, and information asymmetry between different stakeholder groups, all of which are likely to shape the payoff structure and the salience of particular actors in practice. Subsequent studies could improve empirical grounding by incorporating real-world data and scenario-based simulations, and by explicitly modeling these contextual differences, to enhance the model’s practical relevance and predictive accuracy.

Finally, while this study focuses on equilibrium conditions for effective CSR management, it does not examine how MNEs strategically respond at the group level to reputational damage caused by subsidiary misconduct in weak institutional environments. Future work could explore multi-unit interaction mechanisms and ex post remediation strategies within MNE CSR governance systems.

In summary, although this study advances the understanding of evolutionary mechanisms in MNE CSR governance systems, there remains significant scope to enhance actor granularity, model realism, and empirical validation. Further efforts in these directions will help build a more robust theoretical and practical foundation for MNE CSR governance, ultimately contributing to greater social welfare and more sustainable development.

Author Contributions

W.Z. was responsible for conceptualization, methodology, data curation, formal analysis, writing the original draft, and validation. P.L. was responsible for formal analysis, methodology, project administration, as well as reviewing and editing the draft. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement