Are Sustainable Supply Chains Managing Scope 3 Emissions? A Systematic Literature Review

, , ,

, , ,  ,

,  ,

,

Abstract

1. Introduction

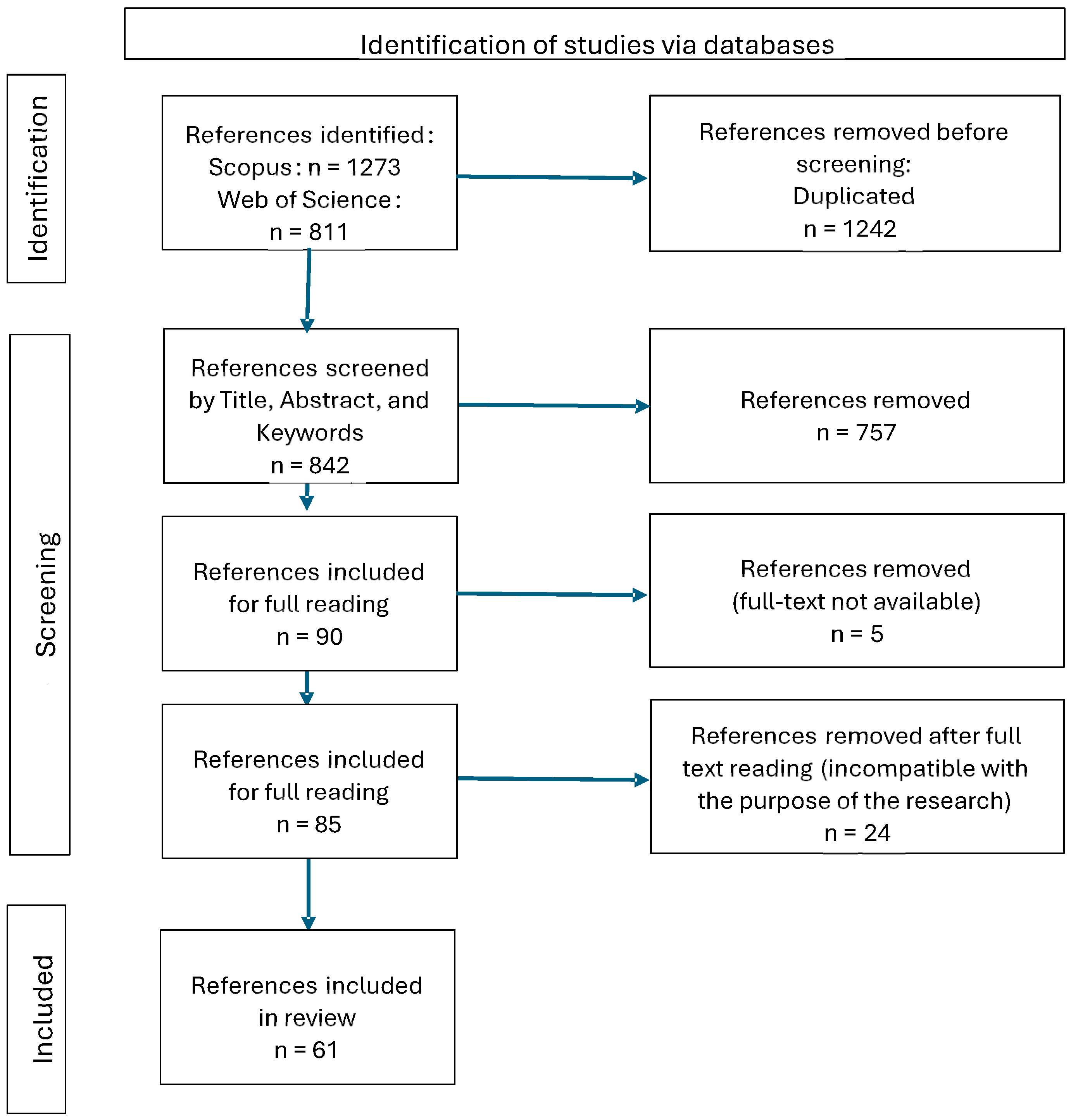

2. Methodology

3. Results

3.1. General Context

3.2. Assessing Scope 3 Emissions

3.3. Disclosing Scope 3 Emissions

3.4. SSCM Strategies Related to Scope 3 Emissions

3.5. Synthesis of the Findings

4. Discussion, Implications, and Avenues for Future Research

4.1. Academic Contributions

4.2. Further Research Avenues

4.3. Managerial Recommendations

5. Conclusions and Limitations

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| SSCM | Sustainable supply chain management |

| ESG | Environmental, social, and governance |

| PRISMA | Preferred Reporting Items for Systematic Reviews and Meta-Analysis |

| SLR | Systematic literature review |

| LCA | Life cycle assessment |

| CDP | Carbon Disclosure Project |

| MNC | Multinational company |

References

- Alves, M.Y.; Vieira, L.; Partyka, R. Suppliers’ GHG mitigation strategies (Scope 3): The case of a steelmaking company. J. Manuf. Technol. Manag. 2024, 35, 383–402. [Google Scholar] [CrossRef]

- WRI; WBCSD. Corporate Value Chain (Scope 3) Accounting and Reporting Standard. Available online: https://ghgprotocol.org/corporate-value-chain-scope-3-standard (accessed on 12 February 2024).

- Mejia, C.; Kajikawa, Y. Estimating scope 3 greenhouse gas emissions through the shareholder network of publicly traded firms. Sustain. Sci. 2024, 19, 1409–1425. [Google Scholar] [CrossRef]

- Dahlmann, F.; Roehrich, J.K. Sustainable supply chain management and partner engagement to manage climate change information. Bus. Strateg. Environ. 2019, 28, 1632–1647. [Google Scholar] [CrossRef]

- Jurburg, D.; López, A.; Carli, I.; Chong, M.; De Oliveira, L.K.; Dablanc, L.; Tanco, M.; De Sousa, P.R. Understanding the Challenges Facing Decarbonization in the E-Commerce Logistics Sector in Latin America. Sustainability 2023, 15, 15718. [Google Scholar] [CrossRef]

- Hettler, M.; Graf-Vlachy, L. Corporate scope 3 carbon emission reporting as an enabler of supply chain decarbonization: A systematic review and comprehensive research agenda. Bus. Strateg. Environ. 2024, 33, 263–282. [Google Scholar] [CrossRef]

- NIKE. Moving Together Fy23 Nike, Inc. Impact Report; NIKE: Eugene, OR, USA, 2023. [Google Scholar]

- JBS Sustainability Report 2023. Available online: https://jbsesg.com/docs/JBS_Sustainability_Report_2023.pdf (accessed on 25 October 2024).

- Google. Google Environmental Report 2023; Google: Mountain View, CA, USA, 2023. [Google Scholar]

- Hansen, A.D.; Kuramochi, T.; Wicke, B. The status of corporate greenhouse gas emissions reporting in the food sector: An evaluation of food and beverage manufacturers. J. Clean. Prod. 2022, 361, 132279. [Google Scholar] [CrossRef]

- Brander, M.; Bjørn, A. Principles for accurate GHG inventories and options for market-based accounting. Int. J. Life Cycle Assess. 2023, 28, 1248–1260. [Google Scholar] [CrossRef]

- Herth, A.; Blok, K. Quantifying universities’ direct and indirect carbon emissions—The case of Delft University of Technology. Int. J. Sustain. High. Educ. 2022, 24, 21–52. [Google Scholar] [CrossRef]

- Al Sholi, H.Y.; Wakjira, T.; Kutty, A.A.; Habib, S.; Alfadhli, M.; Aejas, B.; Kucukvar, M.; Onat, N.C.; Kim, D. How circular economy can reduce scope 3 carbon footprints: Lessons learned from FIFA world cup Qatar 2022. Circ. Econ. 2023, 2, 100026. [Google Scholar] [CrossRef]

- Popescu, I.S.; Gibon, T.; Hitaj, C.; Rubin, M.; Benetto, E. Are SRI funds financing carbon emissions? An input-output life cycle assessment of investment funds. Ecol. Econ. 2023, 212, 107918. [Google Scholar] [CrossRef]

- Anquetin, T.; Coqueret, G.; Tavin, B.; Welgryn, L. Scopes of carbon emissions and their impact on green portfolios. Econ. Model. 2022, 115, 105951. [Google Scholar] [CrossRef]

- Blanco, C.C. Supply Chain Carbon Footprinting and Climate Change Disclosures of Global Firms. Prod. Oper. Manag. 2021, 30, 3143–3160. [Google Scholar] [CrossRef]

- Patchell, J. Can the implications of the GHG Protocol’s scope 3 standard be realized? J. Clean. Prod. 2018, 185, 941–958. [Google Scholar] [CrossRef]

- Nikseresht, A.; Golmohammadi, D.; Zandieh, M. Sustainable green logistics and remanufacturing: A bibliometric analysis and future research directions. Int. J. Logist. Manag. 2023, 35, 755–803. [Google Scholar] [CrossRef]

- Mahapatra, S.K.; Schoenherr, T.; Jayaram, J. An assessment of factors contributing to firms’ carbon footprint reduction efforts. Int. J. Prod. Econ. 2021, 235, 108073. [Google Scholar] [CrossRef]

- Isil, O.; Sebastianelli, R. Arcs of carbon awareness in the value chain and their antecedents. Bus. Strateg. Environ. 2020, 29, 503–518. [Google Scholar] [CrossRef]

- Ozkan-Ozen, Y.D.; Sezer, D.; Ozbiltekin-Pala, M.; Kazancoglu, Y. Risks of data-driven technologies in sustainable supply chain management. Manag. Environ. Qual. 2023, 34, 926–942. [Google Scholar] [CrossRef]

- Roy, V.; Schoenherr, T.; Charan, P. The thematic landscape of literature in sustainable supply chain management (SSCM): A review of the principal facets in SSCM development. Int. J. Oper. Prod. Manag. 2018, 38, 1091–1124. [Google Scholar] [CrossRef]

- Baptista, R.; Thurik, a.R. The relationship between entrepreneurship and unemployment: Is Portugal an outlier? Technol. Forecast. Soc. Change 2007, 74, 75–89. [Google Scholar] [CrossRef]

- Teuteberg, F.; Wittstruck, D. Betriebliches Umwelt- und Nachhaltigkeitsmanagement: A Systematic Review of Sustainable Supply Chain Management. In Multikonferenz Wirtschaftsinformatik 2010; Universitätsverlag Göttingen: Göttingen, Germany, 2020; pp. 203–204. [Google Scholar] [CrossRef]

- Vieira, L.C.; Longo, M.; Mura, M. Impact pathways: The hidden challenges of Scope 3 emissions measurement and management. Int. J. Oper. Prod. Manag. 2024, 44, 326–334. [Google Scholar] [CrossRef]

- Steiner, B.; Münch, C.; Küffner, C.; Hartmann, E. Mapping the intellectual foundation of low-carbon supply chains: A theory-based literature review on buyer-supplier relationships. J. Clean. Prod. 2023, 425, 138961. [Google Scholar] [CrossRef]

- Yi, W.; Liang, H.; Yang, Z. The Choice of Carbon Labels and the Impact of Ambiguity Under Market Differences Based on a Game Framework. Sustainability 2025, 17, 3477. [Google Scholar] [CrossRef]

- Spaniol, M.J.; Danilova-jensen, E.; Nielsen, M.; Rosdahl, C.G.; Schmidt, C.J. Defining Greenwashing: A Concept Analysis. Sustainability 2024, 16, 9055. [Google Scholar] [CrossRef]

- Gao, Y.; Chen, Y. Watchdogs or Enablers? Analyzing the Role of Analysts in ESG Greenwashing in China. Sustainability 2024, 16, 4339. [Google Scholar] [CrossRef]

- Asif, M.S.; Lau, H.; Nakandala, D.; Fan, Y.; Hurriyet, H. Case study research of green life cycle model for the evaluation and reduction of scope 3 emissions in food supply chains. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1050–1066. [Google Scholar] [CrossRef]

- Kirst, R.W.; Borchardt, M.; de Carvalho, M.N.M.; Pereira, G.M. Best of the world or better for the world? A systematic literature review on benefit corporations and certified B corporations contribution to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1822–1839. [Google Scholar] [CrossRef]

- Tranfield, D.; Denyer, D.; Palminder, S. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Prisma. PRISMA 2020. PRISMA for Scoping Reviews (PRISMA-ScR). 2024. Available online: https://www.prisma-statement.org/scoping (accessed on 12 July 2024).

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. BMJ 2021, 372, n71. [Google Scholar] [CrossRef]

- Marti, A.; Bastida-Vialcanet, R.; Marimon, F. A systematic literature review: ESG criteria implementation in the insurance industry. Intang. Cap. 2024, 20, 193–214. [Google Scholar] [CrossRef]

- Park, Y.; Putra, A.S.; Park, H.S.; Kim, J. Characterization of the life cycle carbon footprint of the automobile industry in the Republic of Korea by environmentally extended input-output model. Environ. Eng. Res. 2024, 29, 230583. [Google Scholar] [CrossRef]

- Balci, G.; Ali, S.I. The relationship between information processing capabilities, Net-Zero capability and supply chain performance. Supply Chain Manag. 2024, 29, 351–370. [Google Scholar] [CrossRef]

- Tokito, S.; Nagashima, F.; Hanaka, T. Identifying critical transmission sectors by a new approach: Intermediate-based accounting. J. Clean. Prod. 2024, 435, 140487. [Google Scholar] [CrossRef]

- Giacomin, A.M.; Pacca, S.A. Input–output analysis as guidance for the Brazilian textile supply chain. Environ. Dev. Sustain. 2024, 26, 1–20. [Google Scholar] [CrossRef]

- Biswas, M.K.; Azad, A.K.; Datta, A.; Dutta, S.; Roy, S.; Chopra, S.S. Navigating Sustainability through Greenhouse Gas Emission Inventory: ESG Practices and Energy Shift in Bangladesh’s Textile and Readymade Garment Industries. Environ. Pollut. 2024, 345, 123392. [Google Scholar] [CrossRef]

- Dahlmann, F.; Brammer, S.; Roehrich, J.K. Navigating the “performing-organizing” paradox: Tensions between supply chain transparency, coordination, and scope 3 GHG emissions performance. Int. J. Oper. Prod. Manag. 2023, 43, 1757–1780. [Google Scholar] [CrossRef]

- Martinuzzi, A.; Hametner, M.; Windsperger, A.; Brunnhuber, N. A Framework for Assessing the Climate Impacts of Research and Innovation Projects and Programmes. Sustainability 2023, 15, 16600. [Google Scholar] [CrossRef]

- Chabot, M.; Bertrand, J.L. Climate risks and financial stability: Evidence from the European financial system. J. Financ. Stab. 2023, 69, 101190. [Google Scholar] [CrossRef]

- Emmanuel, Y.; Adenikinju, O.; Doorasamy, M.; Ayoola, T.; Oladejo, A.; Kwarbai, J.; Otekunrin, A. Carbon Emission Disclosure and Financial Performance of Quoted Nigerian Financial Services Companies. Int. J. Energy Econ. Policy 2023, 13, 628–635. [Google Scholar] [CrossRef]

- Toukabri, M.; Jilani, F. The power of critical mass to make a difference: How gender diversity in board affect US corporate carbon performance. Soc. Bus. Rev. 2023, 18, 592–617. [Google Scholar] [CrossRef]

- Linares-Rodríguez, M.C.; Gambetta, N.; García-Benau, M.A. Carbon management strategy effects on the disclosure and efficiency of carbon emissions: A study of Colombian companies’ context and inherent characteristics. J. Clean. Prod. 2022, 365, 132850. [Google Scholar] [CrossRef]

- Xia, M.; Cai, H.H. The driving factors of corporate carbon emissions: An application of the LASSO model with survey data. Environ. Sci. Pollut. Res. 2023, 30, 56484–56512. [Google Scholar] [CrossRef]

- Stridsland, T.; Biørnstad, W.; Vigen, K.; Østergaard, K.L.; Sanderson, H. No-one left behind: An open access approach to estimating the carbon footprint of a Danish clothing company. J. Clean. Prod. 2023, 426, 139126. [Google Scholar] [CrossRef]

- Ballentine, R.S. The unusual suspects: Are well-meaning environmental stakeholders and institutions undercutting the contributions that companies can make to fighting climate change? Oxford Open Clim. Change 2023, 3, kgad009. [Google Scholar] [CrossRef]

- Hall, G.; Liu, K.; Pomorski, L.; Serban, L. Supply Chain Climate Exposure. Financ. Anal. J. 2023, 79, 58–76. [Google Scholar] [CrossRef]

- Goodwin, K.; Allen, C.; Teh, S.H.; Li, M.; Fry, J.; Lenzen, M.; Farrelly, S.; Leon, C.; Lewis, S.; Chen, G.; et al. Targeting 1.5 degrees with the global carbon footprint of the Australian Capital Territory. Environ. Sci. Policy 2022, 144, 137–150. [Google Scholar] [CrossRef]

- Kennett, H.; Diaz-Rainey, I.; Biswas, P.K.; Kuruppuarachchi, D. Climate transition risk in New Zealand equities. J. Sustain. Financ. Invest. 2023, 13, 868–892. [Google Scholar] [CrossRef]

- Yasar, A.; Yalçın, N. Voluntary disclosure of scope 3 greenhouse gas emissions and earnings management: Evidence from UK companies. Cogent Bus. Manag. 2023, 10, 2275849. [Google Scholar] [CrossRef]

- Busch, T.; Johnson, M.; Pioch, T. Corporate carbon performance data: Quo vadis? J. Ind. Ecol. 2022, 26, 350–363. [Google Scholar] [CrossRef]

- Hammer, A.J.; Millar, C.; Hennige, S.J. Reducing carbon emissions in aquaculture: Using Carbon Disclosures to identify unbalanced mitigation strategies. Environ. Impact Assess. Rev. 2022, 96, 106816. [Google Scholar] [CrossRef]

- García-Alaminos; Gilles, E.; Monsalve, F.; Zafrilla, J. Measuring a university’s environmental performance: A standardized proposal for carbon footprint assessment. J. Clean. Prod. 2022, 357, 131783. [Google Scholar] [CrossRef]

- Schmidt, M.; Nill, M.; Scholz, J. Determining the Scope 3 Emissions of Companies. Chem. Eng. Technol. 2022, 45, 1218–1230. [Google Scholar] [CrossRef]

- Reavis, M.; Ahlen, J.; Rudek, J.; Naithani, K. Evaluating Greenhouse Gas Emissions and Climate Mitigation Goals of the Global Food and Beverage Sector. Front. Sustain. Food Syst. 2022, 5, 789499. [Google Scholar] [CrossRef]

- Cabernard, L.; Pfister, S.; Hellweg, S. Improved sustainability assessment of the G20’s supply chains of materials, fuels, and food. Environ. Res. Lett. 2022, 17, 034027. [Google Scholar] [CrossRef]

- Yang, Y.; Park, Y.; Smith, T.M.; Kim, T.; Park, H.S. High-Resolution Environmentally Extended Input-Output Model to Assess the Greenhouse Gas Impact of Electronics in South Korea. Environ. Sci. Technol. 2022, 56, 2107–2114. [Google Scholar] [CrossRef]

- Ellram, L.M.; Tate, W.L.; Saunders, L.W. A legitimacy theory perspective on Scope 3 freight transportation emissions. J. Bus. Logist. 2022, 43, 472–498. [Google Scholar] [CrossRef]

- Demeter, C.; Lin, P.C.; Sun, Y.Y.; Dolnicar, S. Assessing the carbon footprint of tourism businesses using environmentally extended input-output analysis. J. Sustain. Tour. 2021, 30, 128–144. [Google Scholar] [CrossRef]

- Schulman, D.J.; Bateman, A.H.; Greene, S. Supply chains (Scope 3) toward sustainable food systems: An analysis of food & beverage processing corporate greenhouse gas emissions disclosure. Clean. Prod. Lett. 2021, 1, 100002. [Google Scholar] [CrossRef]

- Giesekam, J.; Norman, J.; Garvey, A.; Betts-davies, S. Science-Based Targets: On Target ? Sustainability 2021, 13, 1657. [Google Scholar] [CrossRef]

- Malik, A.; Egan, M.; du Plessis, M.; Lenzen, M. Managing sustainability using financial accounting data: The value of input-output analysis. J. Clean. Prod. 2021, 293, 126128. [Google Scholar] [CrossRef]

- Dou, X.; Deng, Z.; Sun, T.; Ke, P.; Zhu, B.; Shan, Y.; Liu, Z. Global and local carbon footprints of city of Hong Kong and Macao from 2000 to 2015. Resour. Conserv. Recycl. 2021, 164, 105167. [Google Scholar] [CrossRef]

- Wiedmann, T.; Chen, G.; Owen, A.; Lenzen, M.; Doust, M.; Barrett, J.; Steele, K. Three-scope carbon emission inventories of global cities. J. Ind. Ecol. 2021, 25, 735–750. [Google Scholar] [CrossRef]

- Novaes das Virgens, T.A.; Andrade, J.C.S.; Hidalgo, S.L. Carbon footprint of public agencies: The case of Brazilian prosecution service. J. Clean. Prod. 2020, 251, 119551. [Google Scholar] [CrossRef]

- He, K.; Hertwich, E.G. The flow of embodied carbon through the economies of China, the European Union, and the United States. Resour. Conserv. Recycl. 2019, 145, 190–198. [Google Scholar] [CrossRef]

- Martinez, S.; Delgado, M.d.M.; Martinez Marin, R.; Alvarez, S. The Environmental Footprint of the end-of-life phase of a dam through a hybrid-MRIO analysis. Build. Environ. 2018, 146, 143–151. [Google Scholar] [CrossRef]

- Radonjič, G.; Tompa, S. Carbon footprint calculation in telecommunications companies—The importance and relevance of scope 3 greenhouse gases emissions. Renew. Sustain. Energy Rev. 2018, 98, 361–375. [Google Scholar] [CrossRef]

- Hertwich, E.G.; Wood, R. The growing importance of scope 3 greenhouse gas emissions from industry. Environ. Res. Lett. 2018, 13, 104013. [Google Scholar] [CrossRef]

- Meng, F.; Liu, G.; Yang, Z.; Hao, Y.; Zhang, Y.; Su, M.; Ulgiati, S. Structural analysis of embodied greenhouse gas emissions from key urban materials: A case study of Xiamen City, China. J. Clean. Prod. 2017, 163, 212–223. [Google Scholar] [CrossRef]

- Blanco, C.; Caro, F.; Corbett, C.J. The state of supply chain carbon footprinting: Analysis of CDP disclosures by US firms. J. Clean. Prod. 2016, 135, 1189–1197. [Google Scholar] [CrossRef]

- Zhang, X.; Wang, F. Hybrid input-output analysis for life-cycle energy consumption and carbon emissions of China’s building sector. Build. Environ. 2016, 104, 188–197. [Google Scholar] [CrossRef]

- Davies, J.C.; Dunk, R.M. Flying along the supply chain: Accounting for emissions from student air travel in the higher education sector. Carbon Manag. 2015, 6, 233–246. [Google Scholar] [CrossRef]

- Kucukvar, M.; Egilmez, G.; Onat, N.C.; Samadi, H. A global, scope-based carbon footprint modeling for effective carbon reduction policies: Lessons from the Turkish manufacturing. Sustain. Prod. Consum. 2015, 1, 47–66. [Google Scholar] [CrossRef]

- Onat, N.C.; Kucukvar, M.; Tatari, O. Scope-based carbon footprint analysis of U.S. residential and commercial buildings: An input-output hybrid life cycle assessment approach. Build. Environ. 2014, 72, 53–62. [Google Scholar] [CrossRef]

- Ozawa-Meida, L.; Brockway, P.; Letten, K.; Davies, J.; Fleming, P. Measuring carbon performance in a UK University through a consumption-based carbon footprint: De Montfort University case study. J. Clean. Prod. 2013, 56, 185–198. [Google Scholar] [CrossRef]

- Matisoff, D.C.; Noonan, D.S.; O’Brien, J.J. Convergence in environmental reporting: Assessing the carbon disclosure project. Bus. Strateg. Environ. 2013, 22, 285–305. [Google Scholar] [CrossRef]

- Brown, L.H.; Buettner, P.G.; Canyon, D.V.; Crawford, J.M.; Judd, J. Estimating the life cycle greenhouse gas emissions of Australian ambulance services. J. Clean. Prod. 2012, 37, 135–141. [Google Scholar] [CrossRef]

- Huang, Y.A.; Weber, C.L.; Matthews, H.S. Categorization of scope 3 emissions for streamlined enterprise carbon footprinting. Environ. Sci. Technol. 2009, 43, 8509–8515. [Google Scholar] [CrossRef]

- Dahlmann, F.; Branicki, L.; Brammer, S. Managing Carbon Aspirations: The Influence of Corporate Climate Change Targets on Environmental Performance. J. Bus. Ethics 2019, 158, 1–24. [Google Scholar] [CrossRef]

- Ströher, T.; Körner, M.F.; Paetzold, F.; Strüker, J. Bridging carbon data’s organizational boundaries: Toward automated data sharing in sustainable supply chains. Electron. Mark. 2025, 35, 33. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Castka, P. ESG and Industry 5.0: The role of technologies in enhancing ESG disclosure. Technol. Forecast. Soc. Change 2023, 195, 122806. [Google Scholar] [CrossRef]

- Gan, K.; Ye, S. Window Dressing in Impression Management: Does Negative Media Coverage Drive Corporate Green Production? Sustainability 2024, 16, 861. [Google Scholar] [CrossRef]

- Pinheiro, A.B.; dos Santos, J.I.A.S.; Cherobim, A.P.M.S.; Segatto, A.P. What drives environmental, social and governance (ESG) performance? The role of institutional quality. Manag. Environ. Qual. 2024, 35, 427–444. [Google Scholar] [CrossRef]

- Tarifa-Fernández, J.; Céspedes-Lorente, J.; de Burgos Jiménez, J. Drivers of environmental sustainability: Environmental capabilities and supply chain integration. Manag. Environ. Qual. 2023, 34, 843–861. [Google Scholar] [CrossRef]

{kind=link}

| Item | Inclusion Criteria | Observation/Exclusion Criteria |

|---|---|---|

| Limited date to search | Until 6 March 2024 (i.e., the final date of the database search). | Excluded papers published after 6 March 2024. |

| Database definition | Scopus and Web of Science. | Web of Science and Scopus are the most recognized and important international scientific databases [35]. Papers from other databases were not considered. |

| Search strings definition | “SUSTAINABLE SUPPLY CHAIN” AND “SCOPE 3”, “SUPPLY CHAIN” AND “SCOPE 3”, and “SCOPE 3” AND “DISCLOSURE” | Based on research questions focusing on how the sustainable supply-chain literature has discussed Scope 3 emissions. Publications that addressed only Scope 1 and Scope 2 emissions without mentioning Scope 3 were excluded. |

| Search filter | Within Title, Abstract, Keywords. | |

| Language | Only records in English. | Other languages were not considered. |

| Type of records | Only articles and reviews. | Other types of records were not considered. |

| Type of publication | Only peer-reviewed journals. | Other types of publications were not considered. |

| Categories within the database | In Scopus: fields included are environmental science; engineering; business, management, and accounting; energy; social science; economics, econometrics, and finance; decision science; earth and planetary sciences; and computer science. In Web of Science: fields included environmental science; green sustainable science technology; management; business finance; environmental studies; business; engineering environmental; computer science and information systems; engineering manufacturing; operations research management; engineering biomedical; engineering electrical and electronic; engineering industrial; food science technology; information science; and materials science and biomaterials. | Other categories were not considered. |

| Reference | Prevalent Theme in the Paper | Journal | ||

|---|---|---|---|---|

| Accounting or Assessing Scope 3 Emissions | Disclosing or Reporting Scope 3 Emissions | SSCM: Strategies and Practices Related to Scope 3 Emissions | ||

| [36] | ✓ | Environmental Engineering Research | ||

| [1] | ✓ | Journal of Manufacturing Technology Management | ||

| [37] | ✓ | Supply Chain Management | ||

| [6] | ✓ | Business Strategy and the Environment | ||

| [38] | ✓ | Journal of Cleaner Production | ||

| [3] | ✓ | Sustainability Science | ||

| [39] | ✓ | Environment, Development and Sustainability | ||

| [40] | ✓ | Environmental Pollution | ||

| [41] | ✓ | International Journal of Operations and Production Management | ||

| [10] | ✓ | Journal of Cleaner Production | ||

| [42] | ✓ | Sustainability | ||

| [43] | ✓ | Journal of Financial Stability | ||

| [44] | ✓ | International Journal of Energy Economics and Policy | ||

| [45] | ✓ | Society and Business Review | ||

| [14] | ✓ | Ecological Economics | ||

| [46] | ✓ | Journal of Cleaner Production | ||

| [47] | ✓ | Environmental Science and Pollution Research | ||

| [48] | ✓ | Journal of Cleaner Production | ||

| [13] | ✓ | Circular Economy | ||

| [49] | ✓ | Oxford Open Climate Change | ||

| [50] | ✓ | Financial Analysts Journal | ||

| [51] | ✓ | Environmental Science and Policy | ||

| [12] | ✓ | International Journal of Sustainability in Higher Education | ||

| [52] | ✓ | Journal of Sustainable Finance and Investment | ||

| [53] | ✓ | Cogent Business and Management | ||

| [18] | ✓ | International Journal of Logistics Management | ||

| [54] | ✓ | ✓ | Journal of Industrial Ecology | |

| [55] | ✓ | ✓ | Environmental Impact Assessment Review | |

| [56] | ✓ | Journal of Cleaner Production | ||

| [57] | ✓ | Chemical Engineering & Technology | ||

| [58] | ✓ | Frontiers in Sustainable Food Systems | ||

| [30] | ✓ | Corporate Social Responsibility and Environmental Management | ||

| [59] | ✓ | Environmental Research Letters | ||

| [60] | ✓ | Environmental Science and Technology | ||

| [61] | ✓ | Journal of Business Logistics | ||

| [62] | ✓ | Journal of Sustainable Tourism | ||

| [63] | ✓ | Cleaner Production Letters | ||

| [16] | ✓ | Production and Operations Management | ||

| [19] | ✓ | International Journal of Production Economics | ||

| [64] | ✓ | Sustainability | ||

| [65] | ✓ | Journal of Cleaner Production | ||

| [66] | ✓ | Resources, Conservation and Recycling | ||

| [67] | ✓ | ✓ | Journal of Industrial Ecology | |

| [68] | ✓ | ✓ | Journal of Cleaner Production | |

| [20] | ✓ | Business Strategy and the Environment | ||

| [4] | ✓ | Business Strategy and the Environment | ||

| [69] | ✓ | Resources, Conservation & Recycling | ||

| [70] | ✓ | Building and Environment | ||

| [71] | ✓ | Renewable and Sustainable Energy Reviews | ||

| [72] | ✓ | Environmental Research Letters | ||

| [17] | ✓ | Journal of Cleaner Production | ||

| [73] | ✓ | Journal of Cleaner Production | ||

| [74] | ✓ | Journal of Cleaner Production | ||

| [75] | ✓ | Building and Environment | ||

| [76] | ✓ | Carbon Management | ||

| [77] | ✓ | Sustainable Production and Consumption | ||

| [78] | ✓ | Building and Environment | ||

| [79] | ✓ | Journal of Cleaner Production | ||

| [80] | ✓ | Business Strategy and the Environment | ||

| [81] | ✓ | Journal of Cleaner Production | ||

| [82] | ✓ | Environmental Science and Technology | ||

| Synthesis | Challenges |

|---|---|

| “Assessing Scope 3 Emissions” | |

| 38 papers in this theme; Scope 3 emissions represent 75% to 90% of a firm’s total carbon footprint [49]; Several quantification methods are mentioned, as follows:

| Transparency and timely flow of information among supply-chain partners [1,3,36]; Data accuracy and availability [48]; Lack of evaluation standards [48]. |

| “Disclosing Scope 3 Emissions” | |

| 15 papers in this theme; Scope 3 emissions reporting did not improve significantly over a decade (2003–2010) [6,10,54,63,80]; Possibly due to the voluntary nature of reporting, firms engage only if they anticipate financial benefits, selectively disclose positive information, and/or lead to greenwashing [16,54]; Recommendations: integrating financial accounts [65] and harmonizing methodologies and reporting standards; Feasibility concerns for a complex value chain [10]. | Poor data quality and inconsistency in reporting [6,10,41,54,63]; Avoiding greenwashing [16,54]; Lack of executive experience [6]; High transaction costs to engage stakeholders [17,54]; Difficulty in engaging suppliers [4,10]; Country-specific discrepancies and regulations [1,63]; Data scarcity for small- and medium-sized enterprises [44,54]. |

| “SSCM Strategies Related to Scope 3 Emissions” | |

| 12 papers in this theme; Effective SSCM hinges on robust collaboration and stakeholder engagement [18,83], and long-term transparency efforts [41]; Relevant role of focal firms in leveraging actions and strategies to asses and monitor Scope 3 emissions [83]; Focal firms should redesign their business models to incorporate concepts like circular economy, reverse logistics, and digitalization to foster sustainable supply chains [18]; Specific Mitigation Strategies:

| Upstream versus Downstream Focus: assessment and integration of Scope 3 emissions are much higher in upstream than downstream [20]; Transparency: tensions among firms within the same supply chain in managing Scope 3 emissions [41]; Engagement gaps: many firms do not engage with supply-chain partners on climate change actions; engagement is often limited to only one or two tiers [83]; Transaction Costs: Scope 3 emissions management extends focal firm responsibilities, amplifying governance costs due to multiple transaction partners. Power influences a firm’s strategies to extract information from transaction partners [17]; Using new digital technologies and product designs, requiring supply chain adjustments [17]; Lack of goals and reporting in specific areas (e.g., transportation emissions): most firms do not view their disclosure and reduction as essential for legitimacy [61]; External Factors and Limited Experience: competition, regulatory factors, public policies, and limited experience with Scope 3 targets impact the focal enterprise’s role in setting sustainable purchasing goals [6]; Underestimation of Climate Risks: limited disclosure concerning Scope 3 emissions and low carbon prices mean that material climate transition risks are not likely to be fully priced into stock values [52], and these risks are most likely underestimated [43]. |

| Challenges/Inhibitors | Further Research Opportunities |

|---|---|

| “Assessing Scope 3 Emissions” | |

| Lack of accurate data across the supply chain. | Compare and propose methods and metrics to account for Scope 3 emissions, considering each region’s specificities, such as consumption habits, energy matrix, logistic infrastructure, and availability of natural resources and their use. |

| Lack of standard methods and appropriate metrics. | |

| Scope 3 reporting is voluntary; in some industries, only approximately 50% of global companies measure and report Scope 3. | Analyze whether the data are more accurate in segments or countries where Scope 3 emissions accounting and reporting are mandatory and whether the adopted practices have reduced emissions. |

| Lack of data sharing and integration among the value chain stakeholders. | Propose and test integrated systems using digital technologies to support the accounting and reporting of Scope 3 emissions. |

| “Disclosing Scope 3 Emissions” | |

| Lack of transparency in reporting Scope 3 emissions. | Analyze auditors’ role and methods, proposing improvements to identify inconsistencies, lack of transparency, or missing data. |

| Data inconsistency. | |

| Lack of data quality. | |

| Firms only report Scope 3 emissions if they envision a tangible financial benefit. | Analyze the possibility of standardizing reports, pressing the presence of complete data about Scope 3. Study the availability of classifying firms according to their reports’ quality and reliability. |

| Reporting is often used for greenwashing. | |

| Firms purposely disclose positive climate-related information while withholding negative information. | |

| Reports cover only part of the value chain. | Studying the consequences and complexity of obliging reports covers all value chains. |

| Transaction costs to engage with stakeholders to measure and report emissions. | |

| Low experience level in reporting Scope 3 emissions. | |

| “SSCM Strategies Related to Scope 3 Emissions” | |

| Lack of regulation and standards. | Evaluate the availability of a standard considering specific characteristics from regions and countries. |

| Different requirements among countries. | |

| Investor pressure or customer requirements. | Understanding the impact of investor pressure or customer requirements contrasting firms’ values and vision. |

| Difficulty determining the role of other players external to the supply chain. | Analyzing the role of each external player in the supply chain and how their policies and procedures have influenced the reduction in Scope 3 emissions. |

| Difficulty establishing governance and leadership commitment with all stakeholders; tensions among firms. | Study the role of the focal enterprise in coordinating the Scope 3 emissions measurement, disclosure, and reduction. |

| Difficulty in evaluating financial gains from measuring and reporting Scope 3. | Analyze the long-term perspective considering the risks to the firm from climate change. |

| Lack of effective practices to measure and reduce Scope 3 emissions. | Analyze the efficiency and efficacy of mitigation strategies, such as ISO 14001, circular economy, reverse logistics, and sustainable purchasing policy goals. |

| Small- and medium-sized enterprises face financial, technical, and knowledge barriers to accounting for emissions. | |

| Lack of studies discussing the social pillar of sustainability and how it is impacted by Scope 3 emissions or the actions to reduce such emissions. | Compare the disclosed social results self-declared by firms, related to Scope 3, with the implemented practices and their effects on all value chain stakeholders. |

| Theme | Managerial Recommendations | Observation |

|---|---|---|

| “Assessing Scope 3 Emissions” | Communicating effectively with investors, stakeholders, and customers, clarifying its purpose concerning Scope 3 emissions. | The purpose is to get the commitment of all stakeholders, investors, and customers to invest in Scope 3 emissions management. |

| Establishing the proper method for Scope 3 emissions assessment. | Possibly, the focal firm should provide guidelines and training to providers. | |

| Using digital technologies to gather and exchange data and information among value chain stakeholders. | Establishing a code of ethics for data and information sharing could facilitate firms’ adherence. | |

| “Disclosing Scope 3 Emissions” | Using the reports as a tool to guide improvements on Scope 3 emissions, not only to show positive numbers to investors or the market. | |

| “SSCM Strategies Related to Scope 3 Emissions” | Integrating environmental practices along the supply chain. | Examples: circular economy, reverse logistics, reusing or recycling material, replacing energy from fossil sources with non-fossil, and ISO 14000 adherence. |

| Considering the risks of climate change challenges and social disruption for businesses, as well as their impact on business models and the supply chain’s resilience. | Recommendation: evaluate the business model and consider restructuring the supply chain reconfiguration (shorter and fewer providers). | |

| Considering a long-term perspective to transaction costs related to Scope 3 emissions and their impact on the firm’s financial issues. | ||

| Establishing social issues in the value chain and measurement tools for the social results. | ||

| General | Improving the criteria and standards that facilitate the Scope 3 emissions assessment and unify requirements from different regions and countries. | Recommendation to policymakers. |

| Establishing a rigorous Scope 3 emissions report analysis to check whether only positive results have been reported or whether some results have been distorted. | Recommendation to investors committed to sustainability. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Borchardt, M.; Pereira, G.; Milan, G.; Pereira, E.; Lima, L.; Bianchi, R.; Scavarda do Carmo, A. Are Sustainable Supply Chains Managing Scope 3 Emissions? A Systematic Literature Review. Sustainability 2025, 17, 6066. https://doi.org/10.3390/su17136066

Borchardt M, Pereira G, Milan G, Pereira E, Lima L, Bianchi R, Scavarda do Carmo A. Are Sustainable Supply Chains Managing Scope 3 Emissions? A Systematic Literature Review. Sustainability. 2025; 17(13):6066. https://doi.org/10.3390/su17136066

Chicago/Turabian StyleBorchardt, Miriam, Giancarlo Pereira, Gabriel Milan, Elisabeth Pereira, Leandro Lima, Renata Bianchi, and Annibal Scavarda do Carmo. 2025. "Are Sustainable Supply Chains Managing Scope 3 Emissions? A Systematic Literature Review" Sustainability 17, no. 13: 6066. https://doi.org/10.3390/su17136066

APA StyleBorchardt, M., Pereira, G., Milan, G., Pereira, E., Lima, L., Bianchi, R., & Scavarda do Carmo, A. (2025). Are Sustainable Supply Chains Managing Scope 3 Emissions? A Systematic Literature Review. Sustainability, 17(13), 6066. https://doi.org/10.3390/su17136066