1. Introduction

The value of economic sectors is primarily evaluated based on their monetary outputs and fiscal impacts [

1]. In contrast, natural ecosystems are frequently appraised through the prism of intrinsic or non-market values, such as biodiversity, aesthetic significance, and cultural identity, often disconnected from their potential contributions to economic activity and societal well-being [

2,

3]. This dichotomy—between the economic valuation of business sectors and the moral or ecological valuation of nature—has contributed to a fragmented understanding of how different industries contribute to sustainable development. While recent advances in natural capital accounting attempt to bridge this gap [

4,

5], most industries continue to be analyzed through narrowly defined economic parameters, overlooking their broader ecological dependencies and social contributions.

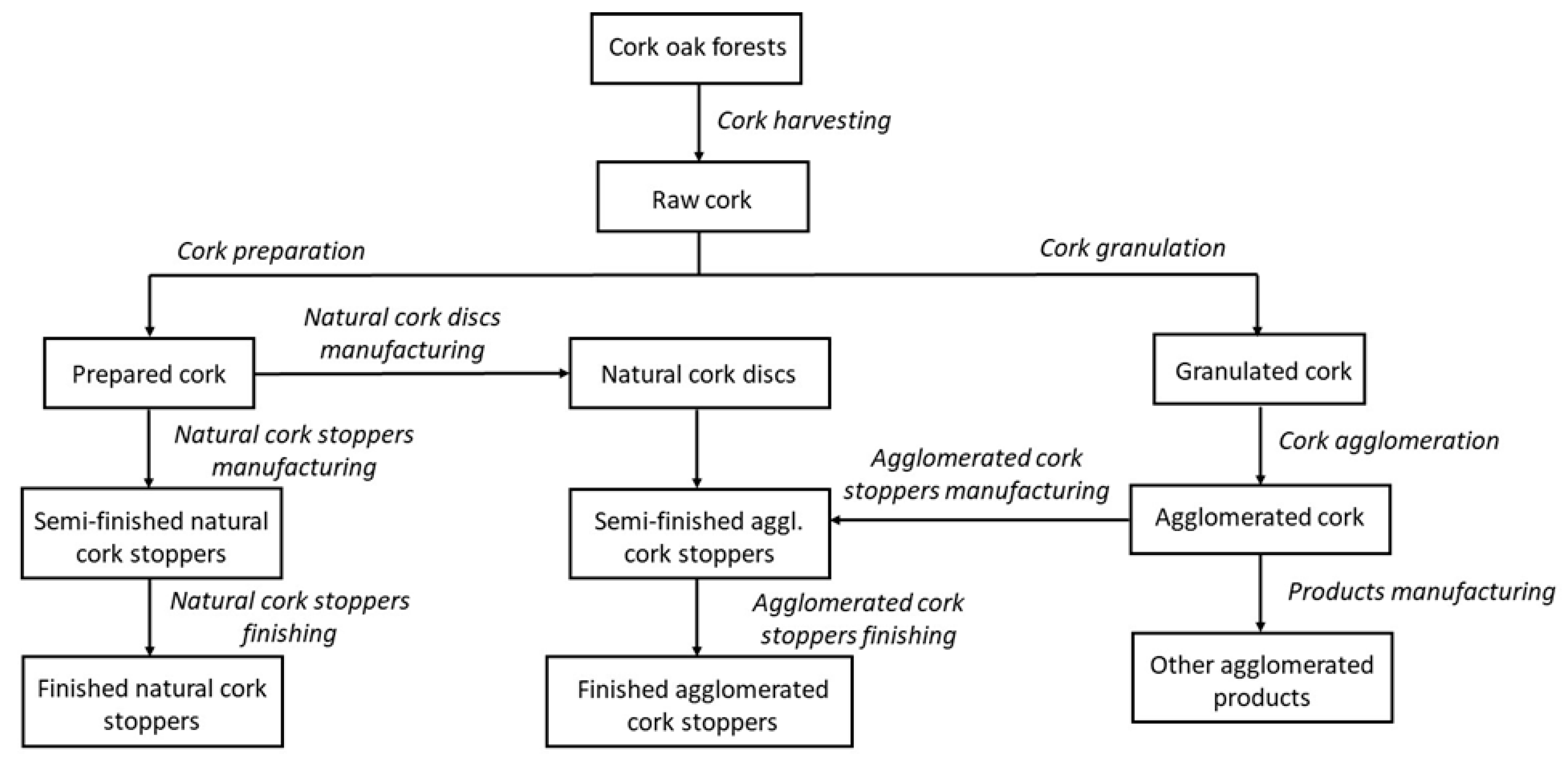

This is also the case for the cork industry, which has a long-standing tradition in some Spanish regions such as Catalonia. Beyond the economic value created by the cork industry, the ecosystems formed by the cork oak (

Quercus suber) forests also generate ecosystem services that are essential for society, such as food production, water retention, soil conservation, or carbon storage [

6]. In addition, cork extraction can be regarded as a sustainable process because it is obtained from the outer bark of cork oak without damaging the tree or affecting biodiversity [

7]. Despite widespread recognition of the potential of cork oak forests and the cork industry to generate societal value, few comprehensive efforts have been made to quantify this value.

In this paper, we seek to address this gap and attempt to analyze the overall value that the Catalan cork industry creates for society. To achieve this, we assess the socioeconomic value of a sample of Catalan cork companies by applying Integrated Social Value (ISV) analysis, a social accounting model that evaluates both the economic and social value generated by an organization for its stakeholders [

8], and that has been applied mainly to single organizations [

9]. We complement this approach with an assessment of the environmental value of the cork companies’ embeddedness in ecological systems. Specifically, we use the value transfer method [

10] to account for the provision, regulation, and cultural services of the cork oak forest ecosystems, which form the basis for the cork value chain.

Our study demonstrates the feasibility of combining ISV with ecosystem service (ES) valuation for assessing the value of the Catalan cork companies. The magnitudes of the performed value estimations show that the environmental value is at least as high as the socioeconomic value, and that the main stakeholder benefiting from the Catalan cork business activity is the environment and, indirectly, society.

Our study makes two key contributions. First, it aims to extend the application of the ISV model to an entire industry—comprising interconnected companies operating within the same business sphere—while addressing specific challenges in the value calculation. Second, it integrates ISV analysis with the existing framework for valuing ES, thereby capturing the environmental value of the natural resources on which the industry relies.

Our paper is structured as follows. The next section introduces the conceptual framework and presents the approach used for the socioeconomic and environmental value assessments. The subsequent section describes the specific methods applied for analyzing the case study of the Catalan cork companies and the steps followed to estimate the socioeconomic and environmental value generated by Catalan cork businesses. Thereupon, the results of the estimation are presented. The final section discusses the results and draws the conclusions.

5. Discussion and Conclusions

Our study attempts to analyze and monetize the overall value created for society by the Catalan cork industry. On the one hand, we calculate the socioeconomic value generated through the economic activity of a sample of Catalan cork companies, following the methodology of ISV analysis. Specifically, we estimate the SEV, the socioeconomic value created and distributed to the six main stakeholder groups that maintain market relations with Catalan cork companies (employees, shareholders, public administrations, financial entities, suppliers, and customers). In extending the ISV model to an entire industry, we have addressed some specific challenges in value calculation beyond simple data aggregation. In contrast to previous studies [

25,

26], we collected primary data directly from companies, which allowed us to account for inter-company transactions—and thus avoid double counting—as well as assess the territorial distribution of value. The result obtained for our sample’s SEV in the year 2021 is EUR 170 million. This means that, on average, every EUR 1.0 of revenue by the Catalan cork companies creates EUR 1.65 of SEV for all their stakeholders.

It is difficult to compare the SEV results with those of other industries due to the limited number of existing studies in this area. However, the SEV per company and SEV per employee ratios fall within the range of average company values observed in four different territories (the three provinces of the Basque Autonomous Community and one region in Sweden) in the study by [

25]. Regarding the distribution of value among stakeholders, Catalan cork companies show a proportionally higher distribution to customers (61%) and suppliers (20%) and a lower distribution to public administrations (8%). More recent data from companies located in European science and technology parks confirm this observation [

26].

Although our initial aim was to calculate the SEV of the entire Catalan cork industry, we faced the problem of not having all the necessary secondary data updated to the required level. Our decision to focus on a smaller sample of 11 companies, for which we were able to obtain all the required financial information, has ensured the robustness of the calculation results. The subsequent extrapolation and comparison with the estimate made for the whole Catalan cork sector show that the SEV/turnover ratio may be a reliable indicator—at least in the context of the analyzed sector.

On the other hand, our study calculates the environmental value of the forest-based cork industry, following the approach of ES valuation. After determining the equivalent cork oak forest area used by Catalan cork companies in the year 2021 (209,410 ha), its ES value is estimated by assigning a valuation proxy derived from a previous study and by attributing this value to the Catalan cork companies according to the average contribution of cork to forestry income. The result obtained for the estimation ranges between a low estimate of EUR 162 million and a high estimate of EUR 1461 million. Cork oak forests’ ESs create benefits for different stakeholders at the local, regional, and global scales, including essential regulation and maintenance services (such as climate regulation and habitat maintenance) that are enjoyed by society as a whole. Nevertheless, the cork industry—like all industries—also has associated negative environmental impacts (e.g., through energy and water consumption, waste generation, and emissions from processing and transport), which are not considered in the present study. Beyond the recurrent assertion that the cork industry’s CO

2 balance is positive because cork oak forests absorb and store more CO

2 than is released during the production and use of cork products (e.g., [

39]), it has not been possible to find more detailed data on these negative environmental impacts that could have been included in the analysis of the companies in this study.

The environmental value calculation is complex because it refers to ecosystems in different locations. The valuation proxies used are within the range found in the literature on forest ESs, where regulation and maintenance services are commonly valued higher than provisioning and cultural ones [

33]. However, the value of regulation and maintenance services is generally difficult to assess because the benefit that people derive from these services (which are not privately owned or traded) frequently cannot be directly observed or measured. In addition, the ability to transfer values from one context to another depends on the specific ES: some ESs, such as carbon sequestration, are provided at a global scale and their benefits are easily transferable; by contrast, values of local-scale services, such as hydrological regulation, may have little transferability. Although ES assessments conducted for specific cork oak forests [

50,

51,

52] determined lower values, they are less comprehensive, i.e., they consider fewer ESs than the study we used for the value transfer [

40]. In the absence of more detailed information on the site-specific parameters of the cork oak sites outside of Catalonia, the present calculated value can be considered a first reasonable estimate that indicates that the environmental value of Catalan cork companies is at least equal to their socioeconomic value. The results of this study also highlight that the main stakeholder benefiting from the Catalan cork industry is the environment and, indirectly, society.

The integration of the ES valuation framework with ISV analysis has revealed that both approaches, despite having different disciplinary roots, rely on similar principles. Both are frameworks aimed at capturing market and especially non-market value of organizations/ecosystems and estimating their utility through monetary proxies. Although ES valuation generally focuses on ecological benefits to society, often with a biophysical foundation, it also includes non-material benefits such as recreational activities and tourism, scientific and educational activities, or cultural identity and landscape [

40,

52]. The latter aspects are often those that make up the non-market social value element of ISV, i.e., the social value that companies create for their various stakeholders through non-market relationships. In this sense, ES valuation not only complements the market-based social value or socioeconomic value of organizations with a value estimate of their positive environmental footprint but also with elements of their positive social footprint. Although often conducted as an expert-driven assessment, ES valuation increasingly involves the perceptions and preferences of stakeholders [

53], and in this way resembles the approach followed by the non-market social value dimension of ISV.

Our findings contribute to the evolving discourse on social and environmental accounting by applying the ISV model to an entire industrial ecosystem rather than a single organization. Unlike other socioeconomic impact assessment methods that estimate the economic impulse created by institutions’ expenditure on regional economies (e.g., input–output analysis or multiplier effect approaches), the ISV calculation allows for assessing the benefits experienced by the stakeholders impacted by the business activity. Combined with ES valuation, the approach can also capture the benefits experienced by stakeholders from nature.

Our study demonstrates the feasibility of combining ISV with ES valuation for assessing the value of the Catalan cork industry. This approach can be applied to evaluate the societal benefits of other traditional nature-based industries, such as food production and construction, or nature-based solutions (NBSs). From a policy perspective, the results highlight the need to incorporate non-market values into regional development strategies, particularly in rural and forest-dependent areas. The cork industry in Catalonia exemplifies how traditional sectors can promote GDP contribution, employment, or tax revenue and simultaneously support biodiversity, carbon sequestration, landscape preservation, and cultural heritage.

Future research should aim to refine the SEV calculation to improve its robustness and comparability across different industrial contexts, and to complement the SEV calculation with the estimation of the non-market social value that goes beyond the benefits created by cork oak forests, such as training for employees, work–life balance initiatives, or collaborations in social projects. Furthermore, future studies should incorporate the industry’s operational negative environmental impacts, specifically the CO2 emissions that occur along the value chain and that should be subtracted from cork oak carbon sequestration at the forest stage. In general terms, research could explore more deeply the incorporation of ES valuation into social value frameworks and analyze alternative approaches to capture cultural ecosystem services, relational values, and non-material benefits that are often underrepresented in monetary valuation.

{kind=link}