Abstract

This paper examines how financial development shapes total factor energy efficiency (TFEE) across the European Union (EU-27) and Western Balkans (WB-6) via a two-stage methodology. We develop DEA-based TFEE indicators from 2006 to 2021 via a window approach that reflects short- and medium-term changes. The production technique integrates primary energy, capital, and labor as inputs, with GDP as a desirable outcome and CO2 emissions as an undesirable output. In the second stage, we estimate a fixed-effects Tobit model that associates latent TFEE scores with standard and composite indices of financial and economic development, while accounting for unobserved country heterogeneity, common temporal shocks, and non-linearities in gross domestic product per capita. While similar Tobit frameworks have been implemented for EU-27, this represents the first case, to our knowledge, of estimating such a model for six Western Balkan countries within a unified EU–WB context. This extension is both methodological and substantive as it integrates the Western Balkans into the finance–energy efficiency discourse and offers policy-relevant evidence regarding the effectiveness of current financial architectures in the region in facilitating the transition mandated by the European Green Deal and the Green Agenda for the Western Balkans.

1. Introduction

Energy efficiency has been recognized as a central pillar of the global low-carbon transition and is sometimes referred to as the “first fuel” in climate and energy security policies. In the International Energy Agency’s net-zero routes, enhancements in energy efficiency provide a significant portion of the necessary emission reduction (IEA, 2019). This priority is further supported by global policy initiatives, such as the Paris Agreement, Green New Deal in the United States (US), the European Green Deal and the Green Agenda for the Western Balkans (WB-6) (United Nations, 2015; European Commission, 2020, 2024; U.S. House of Representatives, 2019).

Within the European Union (EU), the European Green Deal aims for climate neutrality by 2050 and specifically demands faster improvements in energy efficiency across buildings, industry, and transport, emphasizing “energy efficiency first” and extensive restoration of the existing building stock (European Commission, 2024). The EU’s priorities have been expanded to its neighborhood, including the Western Balkans, via the Green Agenda for the Western Balkans and associated Energy Community commitments. As part of the long European integration process that WB-6 began in 2003 and in accordance with the Stabilization Association Agreement (SAA), WB6 countries are required to transpose, or adopt if full transposition is not practicable, the European Union acquis (European Union, n.d.). Improving energy efficiency and converging with EU standards are critical for the Western Balkans in aligning economic, technological, and regulatory frameworks to enable deeper European integration and sustainable development. The priorities set in the Green Agenda for the Western Balkans explicitly define energy efficiency as essential for sustainable growth and social welfare (European Commission, 2020).

Despite this policy focus, significant cross-country disparities in energy performance exist across Europe. The six Western Balkan economies have energy intensity levels that are nearly three times greater than the EU average, indicating an aged energy system, inefficient industrial and building stock, and a slower adoption of new technologies. Even within the EU-27, there is significant variation in energy efficiency outcomes due to varied historical fuel mixes, sectoral structures, and policy initiatives (IEA, 2008; Serreqi & Shahini, 2025).

While the promotion of energy efficiency is widely supported, it must be acknowledged that improving efficiency entails substantial costs and significant credit needs. The ongoing legal modifications resulting from these strategic documents and action plans necessitate adjustments in production processes and consumption behavior by various agents, including individuals, firms, and institutions. In mature financial systems, facilitating access to credit at reduced costs, enhanced information availability and robust monitoring mechanisms promote financing for the research and development of innovative products that advance energy-efficient technologies (Lin et al., 2015; Moshirian et al., 2021). These financial markets mitigate the uncertainty associated with investments overall and, more specifically, in energy efficiency investments by facilitating the creation of risk management instruments. A sophisticated financial sector denotes a diverse framework of specialized financial institutions that cater to various requirements and enhance capital allocation, risk distribution and management, and information dissemination (Adom et al., 2023; Chen et al., 2019; Hsu et al., 2014). On the other hand, if financial development primarily drives the expansion of energy and carbon-intensive sectors, economies may be locked onto high-emission pathways. Emerging and mature economies have shown the energy-raising and energy-saving effects of financial development, as well as non-linear relationships that vary depending on finance structure, regulatory frameworks, and stage of economic development (S.-C. Chang, 2015; Ma & Fu, 2020; Çoban & Topcu, 2013; Xie et al., 2022).

Another issue is figuring out how energy efficiency is measured. Common single-factor metrics, such as energy intensity (energy consumption per unit of GDP), fail to capture the combined contribution of numerous inputs and outputs, such as capital, labor, desirable output, and emissions (Patterson, 1996; Ang, 2006). In response, a growing body of work has used non-parametric approaches such as Data Envelopment Analysis (DEA) to develop total factor energy efficiency (TFEE) indicators that assess how close each country is to a best-practice frontier based on its input–output mix (Berndt, 1978; Hu & Wang, 2006; Charnes et al., 1994). DEA-based TFEE measurements have been applied to the Organization for Economic Co-operation and Development (OECD) and EU member states, indicating continuous differences between the top performers and the bottom performers while also documenting the influence of structural change, technical innovation, and environmental legislation in driving efficiency trajectories (Ziolo et al., 2020).

This article contributes to these discussions by employing an applied empirical investigation via a two-stage methodology. First, it generates DEA-based total factor energy efficiency indicators for 33 European and Western Balkan economies (EU-27 plus WB-6) from 2006 to 2021, utilizing an empirical established window analytic methodology to capture short- and medium-term changes. The TFEE indicators consider primary energy use, capital and labor as inputs, GDP as a desirable outcome, and carbon dioxide (CO2) emissions as an undesirable output. This provides a more comprehensive view of energy environment performance than single-ratio metrics. The novelity of this stage is the inclusion of Kosovo1 to conclude the analysis with the full set of EU-27 and WB-6 countries. To our knowledge, this is the first study to provide a consistent TFEE frontier for all six Western Balkan economies.

Second, and most importantly, this paper examines how various aspects of financial development are linked to TFEE once unobserved country heterogeneity and common time shocks are controlled for. By employing a fixed-effects Tobit, this analysis relates latent TFEE with conventional financial development variables (domestic credit to the private sector), foreign direct investment (FDI), and financial composite indexes that define the framework of the financial system while permitting a non-linear impact on economic development via a GDP per capita variable. While similar Tobit frameworks have been implemented for samples of EU member states, this represents the first case, to our knowledge, of estimating such a model for Western Balkan countries within a unified EU–WB context. This extension is both methodological and substantive as it integrates the Western Balkans into the finance–energy efficiency discourse and offers policy-relevant evidence regarding the effectiveness of current financial architectures in the region in facilitating the transition mandated by the European Green Deal and the Green Agenda for the Western Balkans.

2. Literature Review

The earliest studies linking financial development with the energy market examine the relationship between financial indicators and energy consumption. Numerous papers, using different methodologies and covering various economies, have found that financial development stimulates the overall demand for energy in an economy (Ma & Fu, 2020; Al-Mulali & Lee, 2013; Islam et al., 2013; Mahalik et al., 2017; Sadorsky, 2010; Shahbaz & Lean, 2012). The literature analyzes the business expansion mechanism by which financial development affects energy demand. Grechyna (2018) and C. Arellano et al. (2012) demonstrate that reduced borrowing costs and enhanced credit availability promote capital deepening, the expansion of production lines, and scaling at the firm level. Expansions that are typically energy-intensive correlate with increased overall energy demand. In economies with advanced financial markets, households encounter reduced credit constraints and lower financing costs, leading to increased purchases of energy-intensive durable goods and, consequently, higher overall energy consumption (S.-C. Chang, 2015).

A complementary body of research emphasizes an opposing efficiency mechanism. Decreases in financing costs can expedite technological advancement and the spread of energy-efficient capital, thus reducing overall energy consumption. Access to efficient financial markets and affordable credit promotes investments by firms in energy-efficient machinery and production processes (Maskus et al., 2012; Assi et al., 2020; Farhani & Solarin, 2017; Rafindadi & Mika’ilu, 2019). Contemporary literature has shifted attention toward identifying the non-linear relationships between financial development and energy consumption. Research indicates a strong correlation between the finance–energy efficiency nexus and the economic development stages of countries. Previous time-series analyses utilizing linear specifications typically indicate straightforward proportional relationships. Recent studies utilizing panel datasets, semiparametric (S. Yue et al., 2019), and spatial econometric methods (Yu et al., 2022) reveal intricate dynamics that linear models often overlook.

In economies characterized by underdeveloped financial systems, the expansion of credit frequently supports scale-intensive industrial sectors, thereby increasing energy demand, in line with cross-country findings reported by Ma and Fu (2020). When financial development surpasses specific efficiency thresholds, capital is increasingly allocated to energy-efficient firms and technologies, facilitating the emergence of finance’s constraining or demand-reducing effects (Y. Wang & Gong, 2020). Evidence from the European Union further substantiates these heterogeneous dynamics (Çoban & Topcu, 2013). Additionally, recent nonlinear and dynamic models illustrate state-dependent effects of financial development on energy consumption in emerging economies (Adom et al., 2023; Hsu et al., 2014; Xie et al., 2022).

Nonetheless, the empirical literature, although being limited, indicates a more intricate relationship between financial development and energy efficiency. Employing energy intensity as an indicator of efficiency, Pan et al. (2019) demonstrate that financial progress reduces energy intensity in the long term via a structural vector autoregression (SVAR) framework. In a similar work, Chen et al. (2019) utilize data from 98 economies to demonstrate that financial growth, as indicated by bank credit to the private sector, reduces long-term energy intensity, employing a two-way fixed-effects model.

Other authors demonstrate that the relationship is positive yet unstable, reliant upon a country’s level of financial growth and several contextual elements (Atta Mills et al., 2021; Yao et al., 2021). Atta Mills et al. (2021) assess intertemporal energy efficiency for 58 Belt and Road economies via a dynamic DEA model, with energy stock regarded as a carry-over variable. They subsequently analyze the non-linear impacts of financial development, represented by the International Monetary Fund Financial Development Index, utilizing Estimated Generalized Least Squares (EGLS) and Tobit panel regressions, and conducting projection analysis. Their findings reveal a low average efficiency of roughly 0.44, with only seven DEA-efficient nations, and a deterioration post-2013. Financial development exerts a beneficial impact at lower levels of advancement but becomes negligible upon surpassing elevated thresholds. A recent literature analysis affirms the variability of these impacts and highlights the conditional characteristics of the finance–energy efficiency relationship (Fan et al., 2025).

Ziaei (2015) utilizes a panel Vector Autoregressive (PVAR) analysis for 13 European and 12 East Asia–Oceania countries from 1989 to 2011, demonstrating that financial shocks affect energy consumption in an asymmetric manner. Equity market shocks increase energy consumption over extended periods in East Asia–Oceania, whereas in Europe, energy-use shocks have a more pronounced impact on stock returns, and credit market shocks are comparatively weak. The findings indicate that, when analyzed in terms of energy intensity, market-driven financial deepening may lead to increased energy intensity due to finance promoting investment booms. In contrast, in more developed financial systems, the relationship between finance and energy is less pronounced, with energy-to-finance feedback prevailing. This pattern underscores that the finance–energy intensity relationship is contingent upon the measurement of financial development (equity markets versus credit markets) and the developmental stages of countries.

A study conducted by Hübler and Keller (2009), which analyzed panel data from 60 developing countries between 1975 and 2004, concludes that the frequently cited ordinary least squares (OLS) finding indicating that FDI inflows decrease energy intensity is predominantly spurious when considering broader determinants and conducting robustness checks. Aggregate FDI does not consistently lead to a reduction in energy intensity, while foreign development aid correlates with enhancements in energy efficiency. This evidence suggests that the characteristics and circumstances of external finance may play a more significant role in decreasing energy intensity than the total amount of foreign direct investment (FDI).

Empirical research indicates that financial development may lead to decreased energy intensity, thus enhancing overall energy efficiency. Adom et al. (2019) analyze the relationship in Ghana using a dynamic OLS framework, concluding that more developed financial systems significantly reduce energy intensity following thorough robustness checks. Their findings indicate that energy prices, trade openness, and industrial structure serve as significant complementary determinants. The authors contend that the finance–intensity relationship is complex yet significantly relevant to policy. They highlight that financial development can facilitate macro-level enhancements in energy efficiency and advocate for the creation of specialized green financing institutions, such as a Green Bank, to direct capital towards energy-efficient technologies.

Shahbaz et al. (2015) analyze Portuguese data from 1971 to 2011 to identify a long-run cointegrated relationship among CO2 emissions, energy intensity, economic growth, and financial development. Their methodology includes Zivot–Andrews unit-root tests, autoregressive distributed lag (ARDL) bounds testing, and vector error correction model (VECM)-based Granger causality analysis. The findings suggest that economic growth and energy intensity contribute to increased CO2 emissions, while financial development has a mitigating effect on CO2 levels, aligning with a financing mechanism that promotes cleaner technologies. Causality tests indicate a reciprocal relationship between energy intensity and CO2 emissions, alongside a unidirectional influence from economic growth and financial development to CO2 emissions. According to the authors, financial development can also play its role in improving the environmental quality by encouraging investment in energy-efficient technology to enhance domestic production and save the environment from degradation. In support of this evidence, Chen et al. (2019) employed a two-way fixed-effects framework analyzing 21 OECD and 77 non-OECD countries from 1990 to 2014. Their findings indicate that financial development reduces energy intensity predominantly in non-OECD economies, whereas the impact is constrained in OECD contexts, aligning with the characteristics of established financial systems. In developing economies, a U-shaped relationship between finance and intensity is identified, indicating that initial financial deepening may decrease intensity. However, benefits may diminish or reverse after certain thresholds, with technological advancement and innovation serving as critical transmission mechanisms. These findings suggest that enhancing and strategically allocating finance can be utilized to reduce emissions and energy intensity through investments in energy efficiency, while policymakers navigate the trade-offs between growth and environmental concerns (Shahbaz et al., 2015; Chen et al., 2019).

Canh et al. (2020) analyze a global panel of 81 economies from 1997 to 2013, employing multidimensional indicators of financial development that assess depth, access, and efficiency for both institutions and markets. Their findings indicate that the finance–energy intensity nexus is specific to particular domains and contingent upon income levels. In terms of production, overall financial activity tends to elevate energy intensity, unless enhanced efficiency within financial institutions counteracts this effect. Financial depth and access generally lead to a reduction in energy intensity on the consumption side, while financial efficiency may increase it. Over the long term, financial institutions tend to elevate consumption intensity, whereas financial markets exert a downward pull on it. The authors document significant heterogeneity across income groups; for instance, finance diminishes production intensity in high-income economies while enhancing it in upper-middle-income economies. The development of specific finance components, in combination with a country’s income level, significantly influences the potential for policy interventions aimed at enhancing energy efficiency.

Ziolo et al. (2020) analyze 37 OECD economies from 2000 to 2018 using DEA-based total factor energy efficiency indicators and second-stage regressions. Their findings indicate a modest upward trend in TFEE, alongside persistent cross-country disparities, with more developed OECD members achieving higher average scores. The results regarding the finance–energy efficiency nexus reveal mixed effects of sustainable financial development proxies. Research and development and health expenditures exhibit a positive association with TFEE, the composite index of financial institutions shows a negative association with TFEE, while FDI is not statistically significant. On the other hand, higher TFEE is demonstrated to support sustainable financial development over the long term and is linked to reduced CO2 emissions. The structure and orientation of finance are significant. Innovation-oriented spending correlates with enhanced energy efficiency, while broad institutional depth alone does not ensure efficiency improvements according to this study.

The literature exhibits geographical differences. Empirical evidence connecting financial development and energy efficiency in EU member states is limited, with a notable absence of studies specifically addressing the Western Balkans. This gap emphasizes the necessity for systematic analyses of the interaction between financial development and energy efficiency in both advanced and emerging European economies, underscoring the originality and significance of research aimed at addressing this deficiency.

A fundamental initial step in assessing energy efficiency performance and its determinants is to define the term “energy efficiency” (Patterson, 1996; Ang, 2006). Previous contributions indicate that no singular definition prevails in the literature. A commonly accepted perspective defines energy efficiency as the ratio of useful energy services derived to the quantity of energy spent. The EU Directive 2006/32/EC (2006) on energy end-use efficiency and energy services employs a comprehensive approach, defining energy efficiency as the ratio of performance, service, commodities, or energy output to the energy input utilized. These alternate formulations emphasize various aspects of the input–output connection, resulting in disparate empirical indicators that might produce divergent evaluations of energy efficiency trends and varied policy implications (Berndt, 1978). The literature framework for quantifying and comparing energy efficiency performance across countries and sectors is extensive. In literature reviews, the following two indicators emerge as the most used: energy intensity and total factor energy efficiency (TFEE). Energy intensity is defined as total energy consumption per unit of GDP. The inverse of energy intensity serves only as an approximate indicator of efficiency since it is simultaneously influenced by economic structure, climate, and behavioral factors.

TFEE was introduced in 2006 by Hu and Wang (2006). By recognizing that energy does not generate output independently but operates jointly with labor and capital, they constructed the TFEE index, which integrates multiple production inputs into a unified efficiency framework by employing data envelopment analysis (Charnes et al., 1978; Charnes et al., 1994; Cooper et al., 2000). DEA is a linear non-parametric frontier approach used to evaluate the relative efficiency of a set of different entities called decision-making units (DMU) that use different inputs to produce desirable and sometimes non-desirable output (Charnes et al., 1994). This method has recently gained popularity in efficiency analysis in general (P. Yue, 1992; Asmild et al., 2004; S. Wang et al., 2018) and in energy efficiency in particular (Zahirović et al., 2025; Yan et al., 2021; Cheng et al., 2020; Zhou & Ang, 2008; Mardani et al., 2017; X.-P. Zhang et al., 2011).

3. Methodology

In this paper, we employ a two-stage methodology. In the first stage, the DEA-window analysis approach is used to measure total factor energy efficiency of all European Union member countries and six Western Balkan countries (n = 33). TFEE is evaluated for the period 2006–2021 because of the absence of the data for Western Balkan in early years. Subsequent to the evaluation of the TFEE, we analyze the relationship between energy efficiency and financial development in the EU-27 and WB-6 economies. We consider several indicators of financial development, contingent upon the availability of data in standardized international databases, consistent with the literature on the finance–energy efficiency nexus. All data processing and analysis for DEA analysis were conducted in R version 4.5.0, while panel data regression Tobit was conducted in Stata 17.

3.1. Total Factor Energy Efficiency Evaluation

Efficiency measurement methodologies can be categorized into parametric methods (stochastic frontier analysis-SFA) and non-parametric methods (DEA). We employ DEA, as it is more appropriate to use to benchmark the economies of EU-27 and WB-6 within a common frontier, applying various inputs and both desirable and undesirable outputs. By using DEA, we also refrain from imposing a certain functional form on production technology as required by SFA. In heterogeneous cross-country panels, parametric estimate may be vulnerable to functional-form and distributional assumptions. Data Envelopment Analysis mitigates this risk by directly generating the frontier from observed input–output combinations. We additionally employ DEA window analysis rather than its traditional approach analysis, as it improves the discriminatory capability and robustness of the benchmarking process when the number of decision-making units (DMU) per year is constrained, thereby augmenting the quantity of assessed DMUs and facilitating a transparent evaluation of efficiency dynamics over time (Mardani et al., 2017; X.-P. Zhang et al., 2011).

DEA window analysis enhances conventional cross-sectional DEA by considering each country in each year as an independent DMU, allowing for the evaluation of a country’s performance in a specific year against both other countries and its own previous performance within a fixed-width moving time window, denoted as (Asmild et al., 2004; AlKhars et al., 2022; Kupeli et al., 2019; Sueyoshi & Wang, 2018; Camioto et al., 2018). For each window, all DMUs observed across those consecutive years are included in a singular DEA, and efficiency scores are computed on the premise that technology remains constant inside that window. By shifting the window, we generate a series of “locally intertemporal” frontiers that enhances the volume of observations utilized in the efficiency evaluation and facilitates the identification of performance trends and convergence patterns (Charnes et al., 1978; Charnes et al., 1994). In accordance with the literature (Asmild et al., 2004), we employ one relatively narrow timeframe assuming that no technical drastic changes happened in such a period of time. In our analysis, we consider even the wider window to account for the fact that several Central and Eastern European (CEE) countries have experienced limited technological progress over the period under study (World Intellectual Property Organization, 2025). The choice of window width involves a compromise between minimizing unjust comparisons over time and guaranteeing an adequate sample size and discriminatory power in DEA window estimation. A short window reduces the robustness of the “constant technology” approximation, but larger windows can enhance stability by augmenting the number of country–year DMUs utilized to establish each boundary. In accordance with the DEA window recommendation, which stipulates that the window should be minimized while still ensuring an adequate sample size, we utilize a five-year window as our primary specification and present a ten-year window as a robustness and smoothing verification. Furthermore, window analysis evaluates a series of localized intertemporal frontiers by progressively moving the window over time, ensuring that the “constant technology” assumption is applicable only within each window rather than imposed across the whole sample period.

The total factor energy efficiency evaluation employes input variables such as capital stock, supply of labor and energy consumption and output variables such as economic output and carbon dioxide emissions as suggested by the literature (Cheng et al., 2020; Zhou & Ang, 2008; Mardani et al., 2017; X.-P. Zhang et al., 2011; Kupeli et al., 2019; Sueyoshi & Wang, 2018; Camioto et al., 2018). In this paper, we account for emmisions as an inevitable by-product of the economic output. In this context, is an undesirable output in the DEA window analysis and should be reduced. All data are retrieved from international harmonized databases to ensure comparability among countries (World Bank, n.d.-a, n.d.-b; Ritchie et al., 2025; Ritchie & Roser, 2025; Kosovo Agency of Statistics, n.d.; International Monetary Fund, n.d.). Details on used variables are given in Table 1 and Table 2.

Table 1.

Details on variables for TFEE evaluation.

Table 2.

Descriptive statistics of data for TFEE evaluation.

For a given window width w, the number of windows is: With , this implies windows for , and windows for . Each window contains DMUs, i.e., DMUs when and DMUs when . The total number of DMUs evaluated across all windows is therefore: which yields DMUs for and DMUs for .

The input vector for country in year is shown in the following Equation (1):

and the output vector is shown in Equation (2) as follows:

For each window , let denote the set of all country–year observations included in that window. Here, indexes countries and indexes years within window ℓ; thus, each pair represents a country–year DMU belonging to that window. The input-oriented variable returns to scale (VRS) DEA model for the TFEE score of country in year within window is estimated using the following Equations (3)–(9):

subject to

The convexity constraint imposes variable returns to scale. Because each country–year observation appears in several overlapping windows, multiple efficiency scores are obtained. The final DEA window-based TFEE indicator used in the next part of the paper is defined as the simple mean over all windows as shown by the following Equation (10):

where is the set of windows covering year and is the number of such windows.

3.2. Panel Data Regression Tobit

Subsequent to the evaluation of the TFEE indicators, we analyze the relationship between energy efficiency and financial development in the EU-27 and WB-6 economies. A rising part of the literature employs this two-stage methodology (Z. Wang & Wang, 2022; Iqbal et al., 2025; L. Zhang & Cui, 2024; Shuai & Fan, 2020; Borozan, 2018). Initially, TFEE is evaluated, and subsequently, the derived efficiency scores are regressed against a series of exogenous or institutional determinants to determine their influences. DEA efficiency scores are estimated quantities and may be affected by bias relative to the unobservable “true” efficiency. We acknowledge that the double-bootstrap approach proposed by Simar and Wilson (2007) is frequently advised to enhance inference in two-stage DEA analyses. This methodology is predominantly designed and executed for cross-sectional DEA contexts where DMUs are regarded as independent. In our case, the TFEE is calculated by DEA window analysis on a country-level panel, indicating repeated observations for each country and dependence arising from overlapping windows. Utilizing the Simar–Wilson approach in this situation, and in all panel datasets, necessitates supplementary, complex assumptions and a customized bootstrap design to address both panel reliance and window overlap, which exceeds the scope of this applied paper (Badunenko & Tauchmann, 2019). The scope of this paper is interpreting the second-stage outcomes as policy-relevant correlations rather than direct causality.

In this context, ordinary least squares (OLS) and Tobit models are the predominant econometric instruments, with a panel dataset. A two-limit Tobit model is frequently favored due to the bounded nature of TFEE scores, which range from 0 to 1 and can thus be regarded as a censored dependent variable (Tobin, 1958; Rosett & Nelson, 1975). We take TFEE as a continuous, bounded variable ranging from 0 to 1. We refrain from converting TFEE into categorical efficiency categories (e.g., low/medium/high) as categorization necessitates arbitrary thresholds and diminishes the informational value and cross-national comparability of the efficiency metric. Retaining the continuous indicator enables us to fully utilize within-country and time variation, while the Tobit specification is tailored for constrained dependent variables, therefore making it appropriate for second-stage inference. Consistent with the above vast literature, we utilize panel fixed-effect Tobit regressions to evaluate the impact of several characteristics of financial development on total factor energy efficiency. A fixed-effect structure mitigates omitted-variable bias by controlling for time-invariant heterogeneity.

We consider several indicators of financial development, contingent upon the availability of data in standardized international databases. Consistent with the literature on the finance–energy efficiency nexus, we incorporate the following explanatory variables: domestic credit to the private sector by banks; financial markets index; financial institutions index; health expenditure; net inflows of foreign direct investment and gross domestic product per capita. Details on the variables are given in Table 3 and Table 4.

Table 3.

Details on variables for financial and economic development.

Table 4.

Descriptive statistics of data for financial and economic development.

Let denote the efficiency score for country in year , with and . Due to data limitations, in particular the absence of the full set of several key explanatory variables required for the financial–energy efficiency nexus analysis, Malta, Kosovo, and Montenegro could not be included in this second stage. We explored the use of proxy variables, but this was not feasible in a credible and comparable way. To avoid introducing measurement inconsistency and reducing cross-country comparability, we therefore restrict the second-stage analysis to countries with sufficiently complete data coverage. The estimation of fixed-effects (FE Tobit) regression for the panel data of 30 countries is shown by Equations (11) and (12), as follows:

where is a constant term; measure the marginal effects of the financial indicators on latent efficiency; captures unobserved, time-invariant country heterogeneity; are time effects (common shocks affecting all countries in year t); and is an idiosyncratic error term.

The observed TFEE scores are generated from the latent variable through the standard Tobit mechanism with censoring at 0 and 1, shown as follows:

4. Results

The results for total factor energy efficiency calculated by DEA window analysis allow us to explore the evaluation of energy performance for the period 2006–2021 for the EU-27 countries and WB-6. The DEA window analysis results indicate that, on average, countries function at relatively high yet distinctly sub-frontier efficiency levels. The mean TFEE values for both the five-year and ten-year windows are observed to be within the range from 0.75 to 0.80. The fixed-effect Tobit with upper and lower bounds at 1 and 0 suggests that financial development contributes to explaining the differences in TFEE once unobserved country heterogeneity and common time shocks are controlled for.

4.1. Energy Efficiency Results

The general overview of the DEA–TFEE mean scores for the five-year window is shown in Table 5. The results from the five-year window indicate that the sample-wide mean TFEE varies between 0.72 and 0.80, with a standard deviation between about 0.17 and 0.21. Annual variations in the mean TFEE are rather modest, suggesting that total factor energy efficiency has maintained a generally stable trajectory throughout the study period, rather than demonstrating significant advancements or notable declines.

Table 5.

Country-level DEA–TFEE mean scores for the five-year window, 2006–2021.

Numerous countries consistently demonstrate TFEE scores equal to or almost one, signifying their status as the efficient benchmark in a particular year. Luxembourg, Italy, Germany, Malta, and Montenegro exhibit TFEE values that are either equal to or very slightly below unity over much of the period, indicating that their production–energy emissions combinations are consistently challenging to surpass. Other EU nations, like Denmark, France, Ireland, the Netherlands, and Sweden, consistently exhibit elevated TFEE values, generally above 0.90 in most years, thereby situating them near the frontier. Bulgaria, Romania, Kosovo, Bosnia and Herzegovina, North Macedonia, and, to a lesser degree, Slovakia, Slovenia, and Latvia often have TFEE values below 0.60. Consequently, these countries function farther away from the efficiency frontier and exhibit considerable potential for enhancing the utilization of energy and other inputs to produce economic output while minimizing emissions. From the list of countries that perform relatively low, Bulgaria, Romania, and Kosovo exhibit improvement over time, as can be seen more clearly in Figure A1 (in Appendix A). Nonetheless, the general disparity with the top performers remains substantial by the conclusion of the period.

The results in Table 6 for the ten-year window confirm the above patterns when efficiency is assessed over an extended timeframe. The average TFEE at the sample level is marginally reduced in the ten-year window (about 0.69–0.78) compared to the five-year window, exhibiting a comparable level of variability. A prolonged timeframe increases the difficulty of maintaining frontier performance over several years, hence making the group of countries that achieve such performance increasingly limited. Nevertheless, the classification of countries exhibits considerable stability throughout both timeframes. Table 7 illustrates that Luxembourg, Italy, and Germany consistently rank at the top, exhibiting mean TFEE values of 0.998, 0.995, and 0.994 in the five-year period and 0.993, 0.986, and 0.981 in the ten-year period, respectively. The lowest performing countries are Bulgaria, Kosovo, and Romania.

Table 6.

Country-level DEA–TFEE mean scores for ten-year window, 2006–2021.

Table 7.

Country-level DEA–TFEE average scores.

Ultimately, the comparison of the five- and ten-year average values in Table 7 offers insight into the persistence of energy efficiency performance. In most countries, the disparity between the two window durations is rather minor, resulting in only tiny alterations to their ranked places. This robustness signifies that TFEE trends are not influenced by transient variations but rather represent fundamental aspects of national energy systems, economic structures, and policy frameworks. In instances where disparities between the five- and ten-year averages are more evident, particularly in lower-ranking nations, they indicate either recent enhancements or declines that have yet to be fully integrated into the longer-term analysis.

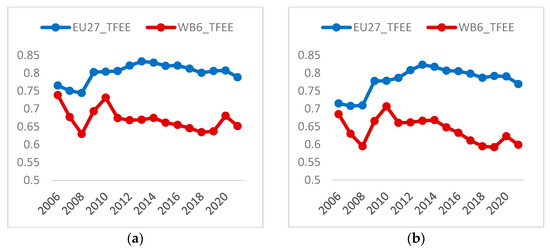

The cross-country rating indicates a continual disparity between a core group of highly efficient economies, predominantly in Western and Northern Europe, and a peripheral of less efficient nations in the Western Balkans, as shown in Figure 1 for both time periods. Excluding Montenegro, the Western Balkans continue to encounter significant obstacles in aligning with EU norms on the efficient utilization of energy and other resources.

Figure 1.

Average DEA–TFEE in the EU-27 and WB-6, 2006–2021: (a) DEA–TFEE estimated with five-year window; (b) DEA–TFEE estimated with ten-year window.

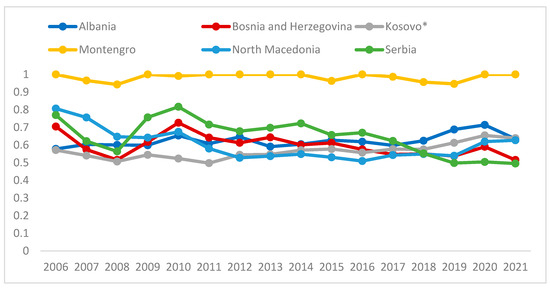

The DEA–TFEE results indicate that there is also diversity among the Western Balkan countries as shown in Figure 2. Montenegro is a distinct outlier in the region, exhibiting an average TFEE near unity in both the five-year and ten-year windows, signifying its consistent position on the efficiency frontier.

Figure 2.

Total factor energy efficiency (TFEE) in the Western Balkan Six (WB6) countries, 2006–2021, estimated with five-year DEA window. * This designation is without prejudice to positions on status and is in line with UNSCR 1244 and the ICJ Opinion on the Kosovo declaration of independence.

In contrast, Albania, Bosnia and Herzegovina, Kosovo, North Macedonia, and Serbia all demonstrate below-average TFEE. Albania’s average TFEE is approximately 0.62 over the five-year window and 0.59 over the ten-year window. Despite some improvement in recent years, it continues to reside in the lower half of the distribution. Bosnia and Herzegovina and Kosovo exhibit even lower average ratings (about 0.60 and 0.56, respectively), categorizing them as some of the least efficient countries in the sample. North Macedonia and Serbia exhibit performances below the EU average, with average TFEE values of approximately 0.60 and 0.65 over a five-year period and 0.57 and 0.61 over a ten-year period, respectively.

4.2. Financial Development–Energy Efficiency Nexus

Subsequent to the construction of the TFEE indicator, we analyze the relationship between energy efficiency and financial development in the 30 countries of the European Union and the Western Balkans. The depended variable choosen is the total factor energy efficiency index based on a five-year DEA window, , observed for 30 European Union and Western Balkan countries over 2006–2021 (480 country–year observations). The indicator lies in [0, 1] by construction and exhibits substantial mass at the upper limit; about 7.5% of observations have (36 out of 480), while no country–year combination records a zero score as shown in Table A1 (in Appendix B).

Domestic credit and financial variable proxies exhibit significant variation across countries and over time and report normal dispersion across samples, as shown in Table A2 (in Appendix B), while foreign direct investment inflows exhibit pronounced skewness. The mean is 10.4, while the distribution ranges from –296 to 432. Net FDI inflows can exhibit substantial skewness in cross-country panels, with very large positive spikes potentially linked to exceptional inflow episodes and large negative values. To reduce the influence of extreme observations, as shown in Table A3 (in Appendix B), the FDI series is winsorized at the 1st and 99th percentiles, yielding the transformed variable (Shete et al., 2004; Leone & Wasley, 2019). This approach preserves the full sample and the relative ranking of observations while limiting the influence of extreme tails, and it is less distortive than trimming, which would remove those observations entirely. Winsorization leaves the mean almost unchanged (from 10.38 to 10.40) but substantially reduces dispersion, with the standard deviation falling from 40.7 to 31.8 as presented in Table A4 (in Appendix B). Boxplots in Figure A2 (in Appendix B) of the original and winsorized series confirm that the transformed variable preserves the bulk of the underlying variation while trimming a small number of outliers.

GDP per capita averages about 27,400 (with wide cross-country variation from roughly 3000 to 112,000). For the regression analysis, is rescaled to tens of thousands as shown by the following Equation (13):

GDP per capita in tens of thousands is then centered around its sample mean as shown by Equation (14). This transformation of the economic development variable is implemented to mitigate the problems arising from the high correlation between the variable and its squared term (Ismaeel et al., 2021; Schroeder et al., 1990; Shieh, 2011).

To allow for non-linear effects of economic development on energy efficiency, the corrected squared term is also calculated as shown in Equation (15), as follows:

Pairwise correlations indicate a moderate association between the financial indicators and GDP per capita, which is consistent with expectations for a panel largely composed of European economies. As shown in Table A5 (in Appendix B), the correlation between and its squared term is very high (0.93). After re-specifying the model using centered GDP per capita and its square, the variance inflation factors (VIFs) decline substantially. In the diagnostic OLS regression with as the dependent variable, the VIF is 7.24 for and 4.78 for , while the remaining regressors have VIFs between 1.3 and 3.7, with an average of about 3.6 as shown in Table A6 (in Appendix B). Overall, these values suggest that multicollinearity is present but remains within acceptable bounds and mainly reflects the non-linear specification of GDP (Shrestha, 2020; Das, 2019).

The OLS diagnostic model, incorporating country and year dummies, indicates that the Breusch–Pagan/Cook–Weisberg tests reject the assumption of homoskedasticity, as shown in Table A7 (in Appendix B). This finding implies that the error variance is not constant. All subsequent parametric regressions report heteroskedasticity-robust standard errors clustered at the country level (Bramati & Croux, 2007; Ismaeel & Midi, 2018; M. Arellano, 2003). Regression estimation is performed by a fixed-effects Tobit with upper and lower bounds at 1 and 0, and robust standard errors clustered at the country level, as shown in Table 8.

Table 8.

Fixed-effects Tobit regression for the TFEE five-year window.

The coefficient of domestic credit to the private sector by banks is negative, relatively small and statistically insignificant. The coefficient in the financial market index is negative and statistically significant at the 1% level with clustered standard errors. Interpreted at the mean, a 0.1 increase in the relative development of financial markets is associated with a reduction of approximately 0.028 points in the latent TFEE index. This suggests that, conditional on country and year effects and the other covariates, improved market-based finance is correlated with lower energy efficiency performance.

The coefficient for is negative and statistically significant An increase of 0.1 in the financial institutions index correlates with a decrease in latent efficiency of approximately 0.032 points. The coefficient on h is minimal and statistically indistinguishable from zero ( ≈ 0.0016, p = 0.87), indicating a lack of significant correlation between health expenditure and TFEE after accounting for other financial variables and fixed effects.

The winsorized FDI variable exhibits a positive yet small coefficient and lacks statistical significance . Within the observed data range, FDI inflows do not exhibit a distinct marginal impact on energy efficiency. For comparability, we also report marginal effects evaluated at the sample means (bottom panel of Table 8). The marginal effects yield the same qualitative conclusions regarding the sign and significance of the financial variables, confirming the robustness of the interpretations based on the Tobit coefficients (W. Wang & Griswold, 2015).

The negative coefficient on the centered GDP per capita term, coupled with a positive and significant squared term, indicates a U-shaped income–energy efficiency profile. In low- and middle-income contexts, an increase in GDP per capita correlates with a decline in total factor energy efficiency, reflecting energy-intensive growth in developing nations. Above a certain income threshold, approximately 80,000 constant 2015 US dollars as shown by Equations (16)–(19), the marginal effect of income ultimately becomes positive. This indicates that only the wealthiest EU members start to decouple economic growth from energy inputs through investments in energy-efficient technologies and the implementation of stricter regulatory frameworks. These equations are shown as follows:

and the sample mean is

Thus, the turning point in actual GDP per capita is roughly:

A joint test of the two GDP terms rejects the null that they both equal zero, confirming that GDP per capita is an important determinant of TFEE as shown in Table A9 (in Appendix B).

As shown in Table A8 (in Appendix B), country fixed effects are almost all large and positive, reflecting persistent cross-country differences in average TFEE beyond what can be explained by the included regressors. Year dummies are generally positive and significant from 2009 onwards, indicating a gradual improvement in efficiency relative to the base year 2006, with some moderation in recent years.

The fixed-effects Tobit model, incorporating country and time dummies, demonstrates a good fit for the data. The Tobit regression model is statistically significant. This implies that, as a group, the financial variables and economic development together contribute significantly to explaining cross-country and temporal variation in energy efficiency, as shown in Table A10 (in Appendix B).

Additional checks were carried out to assess the adequacy of the FE Tobit specification. The distribution of residuals from the fixed-effects Tobit model was evaluated using a histogram, as shown in Figure A3 (in Appendix B). The generalized residuals are centered very close to zero and do not display pronounced skewness or kurtosis, which is consistent with the Tobit error assumptions conditional on the fixed-effects. The relationship between residuals and the linear predictor is plotted in Figure A4 (in Appendix B). The scatter plot reveals no clear systematic patterns. The residuals are approximately symmetrically distributed around zero, and there is no visual evidence of fanning-out. This suggests that, after clustering standard errors at the country level, any remaining heteroskedasticity is unlikely to materially affect the main conclusions (Bramati & Croux, 2007; Ismaeel & Midi, 2018; M. Arellano, 2003).

5. Discussions

The DEA-derived total factor energy efficiency indicators for both the five-year and ten-year periods indicate that, on average, the 33 European and Western Balkan economies function relatively highly, yet they are still some distance away from the best performance. The cross-sectional mean of TFEE varies between 0.75 and 0.80 from 2006 to 2021, exhibiting a minor enhancement until the early 2010s, followed by a slight stabilization or decrease thereafter. The minimum average efficiency occurred between 2007 and 2008, coinciding with the global financial crisis, after which the mean TFEE recuperates and stabilizes at marginally elevated levels. This trend aligns with recent findings for EU member states, where dynamic DEA analyses reveal incremental advancements in energy efficiency and eco-efficiency until approximately 2010–2012, succeeded by a deceleration in progress (Zahirović et al., 2025; Vlahinić-Dizdarević & Šegota, 2012; Borozan, 2018; M.-C. Chang, 2020; Vlahinić Lenz et al., 2018).

High-income EU countries often possess capital and knowledge-intensive production frameworks, characterized by more efficient industrial machinery and infrastructure (Borozan, 2018). Core EU members have been prompt and comparatively stringent in the implementation of EU energy efficiency directives, construction regulations, and industry standards (European Commission, 2025; Altmann et al., 2010). Denmark is frequently seen as a frontrunner in energy efficiency policy, integrating established building standards, proactive district heating initiatives, and incentives for industrial efficiency investments. Such policy frameworks increase the expense associated with energy waste and promote the use of efficient technology. Final energy consumption trends vary across Member States. Countries like Luxembourg, the Netherlands, and Finland have shown significant decreases in final energy use, while others, including Croatia, and Portugal, have observed rises since 2019. The most significant savings have occurred in the residential sector, succeeded by industry and services, primarily due to enhancements in building energy efficiency (European Commission, 2025). Italy and Luxembourg, among others, established more ambitious energy-saving objectives in their National Energy Efficiency Action Plans (NEEAPs), while CEE countries such as Czech Republic seem to fall short, especially regarding the comprehensiveness, transparency, and clarity of their declared intended initiatives in framework of their energy efficiency policies (Altmann et al., 2010).

Denmark and Germany have swiftly expanded their wind and solar capacity as components of their energy transitions (Agora Energiewende, n.d.; Umweltbundesamt, 2025). By the early 2020s, renewable energy sources accounted for over fifty percent of electricity in Germany and a comparably high proportion in Denmark, while the European Union collectively derived about seventy-five percent of its power from renewables and nuclear energy (Eurostat, n.d.-a, n.d.-b, n.d.-c). This transition to low-carbon, capital-intensive generation and contemporary grid infrastructure diminishes CO2 emissions per unit of electricity and frequently decreases technical losses, which, in a DEA framework, results in enhanced total factor energy efficiency.

At the lower end of the TFEE distribution, DEA findings indicate that Bulgaria, Romania, Kosovo, Bosnia and Herzegovina, North Macedonia, Slovakia, Hungary, the Czech Republic, and, to a lesser degree, Serbia and Latvia exhibit average TFEE values within the 0.50–0.65 range, contingent upon the window length. These post-socialist EU nations and Western Balkan economies inherited an industrial framework focused on heavy, energy-intensive sectors, with district heating systems and building inventories that were not constructed according to contemporary energy efficiency standards (Popov, 2023; Tian et al., 2024). CEE economies exhibit higher energy consumption relative to their economic production and living standards compared to Western Europe, with this inefficiency directly associated with increased energy poverty, deteriorating air quality and diminished industrial competitiveness (Popov, 2023).

Reports from the Energy Community and papers indicate that the Western Balkans exhibit minor advancement in the transposition and enforcement of energy efficiency legislation, characterized by fragmented institutional responsibilities and constrained capability within local authorities (Serreqi & Shahini, 2025; United Nations Development Programme, 2024; World Bank, 2018; Knez et al., 2022; Pijalović & Kapo, 2017; Frey, 2024). Lower-performing countries (e.g., Kosovo, Bosnia and Herzegovina) rely heavily on domestic lignite, which is extremely carbon-intensive and often burned in old plants with low thermal efficiency (Eurostat, n.d.-a, n.d.-b, n.d.-c). In contrast, Albania and Montenegro, which have substantial hydropower resources, tend to appear relatively more efficient in TFEE terms than their income level alone would suggest. Hydropower allows them to generate electricity with relatively low CO2 emissions, and in Albania’s case, energy intensity has fallen significantly over time as the economy has shifted away from heavy industry (Ministry of Infrastructure and Energy, 2021). Beyond the role of a relatively “cleaner” electricity mix, Montenegro’s economic structure is characterized by a comparatively small industrial base. The share of industry (including construction), typically among the most energy-intensive sectors, is markedly lower (only 13%) compared to 20–24% in neighboring countries, according to World Bank (n.d.-a, n.d.-b). Montenegro also appears to benefit from comparatively stronger societal and business awareness of environmental and energy issues. This may translate into greater acceptance of efficiency-oriented measures, as well as a business environment that is more receptive to adopting energy-efficient technologies and operational practices. Over time, such behavioral and organizational factors can complement structural conditions and contribute to performance closer to the efficient frontier (Serreqi & Shahini, 2025). Our results are consistent with those of the authors, which has evaluated TFEE using Data Envelopment Analysis for EU-27 countries and WB countries without Kosovo (Zahirović et al., 2025).

Our findings on the contribution of the financial development variable show that domestic credit and the development of the financial market and institutions negatively impact energy effieicncy. The results for and indicate that more developed financial systems do not necessarily correlate with higher total factor energy efficiency; rather, they seem to be associated with increased energy consumption relative to output. A substantial body of empirical literature indicates that more developed financial systems frequently increase energy consumption and CO2 emissions, particularly when financial deepening predominantly supports conventional, energy-intensive industries instead of targeted green investments (Çoban & Topcu, 2013; Sadorsky, 2010; Ziaei, 2015; Shahbaz et al., 2015; Batóg & Pluskota, 2023; Bayar et al., 2021). Research on emerging and middle-income nations typically indicates that advancements in financial and stock market sectors elevate energy consumption and emissions (Sadorsky, 2010; Hübler & Keller, 2009).

The foreign direct investment coefficient is marginally positive although statistically insignificant. This aligns closely with the extensive literature. Certain studies indicate that foreign direct investment can enhance energy efficiency in some countries by introducing cleaner technologies and management techniques. Other countries direct their investments towards energy-intensive and lightly regulated sectors. In a fixed-effects framework, that heterogeneity dissipates into a statistically insignificant average effect. Hübler and Keller (2009) and Ziolo et al. (2020) additionally document a non-significant impact of FDI on TFEE for OECD nations.

Elevated health expenditure may indicate a more robust welfare state, superior institutions, and heightened political focus on well-being. This may be associated with more stringent environmental policies, more environmental awareness, and supplementary investments in clean technologies. In contrast to Ziolo et al. (2020), who report a positive correlation between health expenditure and total factor energy efficiency in OECD nations, our coefficient for our health expenditure proxy (h) is minimal and statistically insignificant in the fixed-effects Tobit model. This indicates that short-term variations in overall health expenditure do not result in consistent alterations in energy efficiency when accounting for financial development, income levels, and unobserved nation heterogeneity. One explanation is that health expenditure is a broad social policy aggregate, only weakly connected to energy use.

This pattern of relationship between energy efficiency and economic development closely resembles an energy efficiency variant of the Environmental Kuznets Curve (EKC) (Ekins, 1997). During the initial and intermediate phases of development, growth is predominantly dependent on energy-intensive industrialization, infrastructure, and motorization; only at elevated income levels do advanced technologies, rigorous environmental policies, and a predominance of the service sector begin to enhance efficiency (Wen et al., 2022). Evidence of the Environmental Kuznets Curve concerning CO2 emissions and energy intensity in EU nations is prevalent, with numerous studies explicitly attributing the reduction in emissions at elevated income levels to enhanced energy efficiency and technological advancements (Kolasa-Więcek et al., 2025; Mohammed et al., 2024; Ahmad, 2024; López-Menéndez et al., 2014; Jóźwik et al., 2021; Simionescu, 2021). Although the estimated quadratic specification implies a turning point at a relatively high level of GDP per capita, this value lies in the far-right tail of the sample distribution. Accordingly, the “upturn” should be interpreted as relevant only for a limited number of very high-income countries. For the central range of observations, which represents the majority of the sample, the estimated marginal relationship between GDP per capita and TFEE is dominated by the declining segment.

6. Conclusions

This study analyzed the relationship between financial development and total factor energy efficiency across a panel of European and Western Balkan economies from 2006 to 2021. The analysis integrated a DEA–TFEE indicator, calculated using a window approach utilizing both desired (GDP) and undesirable (CO2 emissions) outputs, with a fixed-effects Tobit model that associates efficiency with several financial and macroeconomic parameters. This study enhances the existing literature regarding the influence of financial system structure on the energy efficiency trajectories of both established and emerging economies in Europe.

The DEA window approach results indicate that, on average, countries function at relatively high yet distinctly sub-frontier efficiency levels. The mean TFEE values for both the five-year and ten-year windows are observed to be within the range from 0.75 to 0.80. The cross-country distribution of TFEE across countries exhibits significant heterogeneity. Northern and Western European countries, specifically Luxembourg, Italy, Germany, Denmark, Sweden, the Netherlands, and France, consistently rank near or on the efficiency frontier in both window specifications. These economies exhibit high per-capita income and robust institutional quality, and they often utilize cleaner or more efficient power mixes alongside advanced energy technologies, contributing to elevated TFEE scores. Conversely, various economies in the Central, Eastern, and Western Balkans, such as Bulgaria, Romania, Bosnia and Herzegovina, Kosovo, and North Macedonia consistently fall short of the frontier. Within this group, there are notable exceptions like Albania and Montenegro, whose TFEE performance aligns more closely with that of high-performing EU members. This highlights the significance of country-specific policies and energy mixes over regional considerations alone.

In the fixed-effects Tobit model, traditional financial indicators such as domestic credit and foreign direct investment do not show a strong association with higher total factor efficiency (TFEE). Conversely, the structure and depth of the financial system, as measured by market-based finance and financial institution indexes, exhibit a significant negative relationship with latent efficiency. This indicates that, from 2006 to 2021, increasing and improved finance has predominantly directed credit and market funding towards sectors and activities that enhance output while failing to adequately account for energy and climate externalities. The relationship between GDP per capita and TFEE is non-linear. This suggests that higher income correlates with lower TFEE; however, this negative effect diminishes and ultimately reverses at elevated income levels, specifically around 79,000 constant 2015 US dollars. Importantly, this turning point lies in the upper tail of the sample distribution, implying that the potential reversal is relevant for only a limited number of very high-income countries, whereas for the majority of observations, the relationship is dominated by the declining segment. This pattern aligns with an “energy efficiency Kuznets” relationship. Catching-up economies typically industrialize and invest in energy-intensive industries, whereas wealthier nations, benefitting from stricter regulations, advanced technologies, and heightened environmental preferences, are more capable of enhancing energy efficiency as their incomes increase.

From a policy perspective, these findings have numerous repercussions. To close the efficiency gap between high-performing EU members and underperforming Central, Eastern, and Western Balkan economies, it is essential to not just implement conventional energy efficiency initiatives but also to enhance the alignment of financial institutions with energy and climate goals. This necessitates the implementation of blended-finance instruments that direct both bank-based and market-based financing towards energy-efficient buildings, transportation, industry, and power systems. Secondly, the non-linear correlation between income and TFEE highlights the risk that catching-up economies in the Western Balkans and Eastern EU may experience lower efficiency unless green conditionality and targeted investment support are integrated into their developmental trajectory. The limited influence of FDI and typical credit expansion in explaining TFEE shows that the quality, sectoral distribution, and conditionality of capital flows are more significant than just their mere magnitude.

Author Contributions

Conceptualization, L.S. and M.S.; methodology, L.S., software, L.S., validation, L.S. and M.S.; formal analysis, L.S., investigation, M.S., resources, L.S., data curation, L.S., writing—original draft, M.S., writing—review & editing, L.S. and M.S., visualization, L.S., supervision, L.S. and M.S., project administration, L.S. and M.S., funding acquisition, L.S. and M.S. All authors have read and agreed to the published version of the manuscript.

Funding

The research has received funding from the National Agency for Scientific Research and Innovation of Albania.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The original data presented in the study are openly available in World Development Indicator dataset at https://databank.worldbank.org/source/world-development-indicators (accessed on 3 November 2025); in World Bank dataset at https://data.worldbank.org/indicator/NV.IND.TOTL.ZS (accessed on 3 November 2025); in Financial development index dataset at https://data.imf.org/en/Data-Explorer?datasetUrn=IMF.MCM:FDI(1.0.0) (accessed on 3 November 2025); in Our world in data at https://ourworldindata.org/co2-emissions (accessed on 3 August 2025) and https://ourworldindata.org/grapher/primary-energy-cons (accessed on 3 August 2025) and in Kosovo Agency of Statistics at https://askdata.rksgov.net/pxweb/sq/ASKdata/ASKdata__Labour%20market__Anketa%20e%20Fuqis%C3%AB%20Pun%C3%ABtore__Annual%20labour%20market/tab24.px/ (accessed on 3 November 2025).

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

Figure A1.

Country-level total factor energy efficiency (TFEE) scores in EU-27 and WB-6, 2006–2021, five-year DEA window () and ten-year DEA window ().

Figure A1.

Country-level total factor energy efficiency (TFEE) scores in EU-27 and WB-6, 2006–2021, five-year DEA window () and ten-year DEA window ().

Appendix B

Table A1.

Distribution of boundary TFEE scores (0 and 1).

Table A1.

Distribution of boundary TFEE scores (0 and 1).

| Variable | Value | Count | In % |

|---|---|---|---|

| 0 | 0 | 0 | |

| 1 | 36 | 7.5% | |

| 0 | 0 | 0 | |

| 1 | 26 | 5.4% |

Table A2.

Summary statistics of TFEE and financial development indicators.

Table A2.

Summary statistics of TFEE and financial development indicators.

| Stats | dc | fm | fi | h | fdi | gdpc | ||

|---|---|---|---|---|---|---|---|---|

| N | 480 | 480 | 480 | 480 | 480 | 480 | 480 | 480 |

| Mean | 0.770 | 0.747 | 80.831 | 0.389 | 0.625 | 8.235 | 10.383 | 27,390.05 |

| SD | 0.174 | 0.179 | 43.490 | 0.288 | 0.154 | 1.821 | 40.712 | 22,076.6 |

| Min | 0.390 | 0.349 | 21.694 | 0.001 | 0.257 | 4.475 | −296.013 | 2894.36 |

| Max | 1 | 1 | 254.552 | 0.950 | 0.925 | 12.902 | 431.789 | 112,417.9 |

| p1 | 0.462 | 0.437 | 25.710 | 0.001 | 0.324 | 5.022 | −40.108 | 3459.247 |

| p5 | 0.514 | 0.482 | 33.176 | 0.004 | 0.392 | 5.463 | −3.276 | 4408.291 |

| p10 | 0.554 | 0.523 | 37.206 | 0.014 | 0.432 | 6.000 | 0.067 | 5694.548 |

| p25 | 0.601 | 0.582 | 48.958 | 0.062 | 0.496 | 6.629 | 1.708 | 11,837.98 |

| p50 | 0.757 | 0.729 | 72.216 | 0.443 | 0.621 | 8.214 | 3.386 | 19,836.79 |

| p75 | 0.955 | 0.925 | 100.051 | 0.630 | 0.756 | 9.589 | 7.441 | 42,164.26 |

| p90 | 0.998 | 0.988 | 136.925 | 0.759 | 0.839 | 10.741 | 20.410 | 50,916.93 |

| p95 | 1 | 1 | 168.998 | 0.785 | 0.857 | 11.188 | 45.891 | 58,459.27 |

| p99 | 1 | 1 | 242.425 | 0.877 | 0.898 | 12.072 | 234.311 | 107,592 |

Table A3.

Summary statistics for FDI and GDPC.

Table A3.

Summary statistics for FDI and GDPC.

| Metric | fdi | gdpc |

|---|---|---|

| Std_dev | 40.71171 | 22,076.6 |

| Variance | 1657.443 | 0.0000000487 |

| Skewness | 4.431287 | 1.665099 |

| Kurtosis | 49.47815 | 6.47924 |

Table A4.

Summary statistics for FDI and winsorized FDI.

Table A4.

Summary statistics for FDI and winsorized FDI.

| Variable | Mean | Std_dev | Min | Max | p1 | p5 | p50 | p95 | p99 |

|---|---|---|---|---|---|---|---|---|---|

| fdi | 10.38298 | 40.71171 | −296.013 | 431.7885 | −40.1083 | −3.27558 | 3.386472 | 45.8912 | 234.3106 |

| 10.39931 | 31.81294 | −40.1083 | 234.3106 | −40.1083 | −3.27558 | 3.386472 | 45.8912 | 234.3106 |

Figure A2.

Boxplot of foreign direct investment (FDI): (a) FDI; (b) Winsorized FDI.

Figure A2.

Boxplot of foreign direct investment (FDI): (a) FDI; (b) Winsorized FDI.

Table A5.

Pairwise correlation matrix.

Table A5.

Pairwise correlation matrix.

| dc | fm | fi | h | ||||

|---|---|---|---|---|---|---|---|

| dc | 1 | 0.58 | 0.65 | 0.35 | 0.35 | 0.41 | 0.24 |

| fm | 0.58 | 1 | 0.77 | 0.57 | 0.06 | 0.64 | 0.41 |

| fi | 0.65 | 0.77 | 1 | 0.52 | 0.06 | 0.67 | 0.50 |

| h | 0.35 | 0.57 | 0.52 | 1 | −0.17 | 0.27 | 0.02 |

| 0.35 | 0.06 | 0.06 | −0.17 | 1 | 0.12 | 0.13 | |

| 0.41 | 0.64 | 0.67 | 0.27 | 0.12 | 1 | 0.93 | |

| 0.24 | 0.41 | 0.50 | 0.02 | 0.13 | 0.93 | 1 |

Table A6.

Variance inflation factors for explanatory variables.

Table A6.

Variance inflation factors for explanatory variables.

| Variable | VIF | 1/VIF |

|---|---|---|

| 7.24 | 0.138143 | |

| 4.78 | 0.209192 | |

| fm | 3.69 | 0.270768 |

| fi | 3.58 | 0.279648 |

| dc | 2.27 | 0.439602 |

| h | 2.19 | 0.456605 |

| 1.32 | 0.759171 |

Table A7.

Breusch–Pagan/Cook–Weisberg test for Homoskedasticity.

Table A7.

Breusch–Pagan/Cook–Weisberg test for Homoskedasticity.

| Null Hypothesis (H0) | Test Statistic (χ2) | df | p-Value | Conclusion |

|---|---|---|---|---|

| Constant variance (homoskedasticity) | 19.23 | 1 | 0 | Reject H0: evidence of heteroskedasticity |

Table A8.

Fixed-effects Tobit regression for five-year and ten-year windows, full output.

Table A8.

Fixed-effects Tobit regression for five-year and ten-year windows, full output.

| Variables | tfee_w5 | tfee_w10 |

|---|---|---|

| dc | −0.000174 | −0.0000322 |

| (0.000268) | (0.000254) | |

| fm | −0.2799 *** | −0.255 *** |

| (0.0979) | (0.0881) | |

| fi | −0.317 ** | −0.299 * |

| (0.141) | (0.158) | |

| h | 0.00161 | 0.00362 |

| (0.0101) | (0.00994) | |

| 0.0000899 | 0.000088 | |

| (0.000088) | (0.0000782) | |

| −0.120 *** | −0.100 ** | |

| (0.0439) | (0.0472) | |

| 0.0115 ** | 0.0114 ** | |

| (0.00497) | (0.00535) | |

| 2.country_id | 1.009 *** | 0.901 *** |

| (0.217) | (0.235) | |

| 3.country_id | 1.058 *** | 0.952 *** |

| (0.210) | (0.229) | |

| 4.country_id | 0.0172 | 0.00183 |

| (0.0301) | (0.0318) | |

| 5.country_id | 0.0925 ** | 0.0790 |

| (0.0457) | (0.0518) | |

| 6.country_id | 0.368 *** | 0.347 *** |

| (0.0796) | (0.0870) | |

| 7.country_id | 0.750 *** | 0.681 *** |

| (0.151) | (0.161) | |

| 8.country_id | 0.296 *** | 0.266 ** |

| (0.0964) | (0.104) | |

| 9.country_id | 1.266 *** | 1.121 *** |

| (0.248) | (0.268) | |

| 10.country_id | 0.236 *** | 0.212 ** |

| (0.0880) | (0.0951) | |

| 11.country_id | 0.987 *** | 0.887 *** |

| (0.214) | (0.231) | |

| 12.country_id | 1.151 *** | 1.059 *** |

| (0.208) | (0.227) | |

| 13.country_id | 1.179 *** | 1.084 *** |

| (0.214) | (0.231) | |

| 14.country_id | 0.747 *** | 0.706 *** |

| (0.120) | (0.128) | |

| 15.country_id | 0.252 *** | 0.232 *** |

| (0.0780) | (0.0812) | |

| 16.country_id | 1.234*** | 1.098 *** |

| (0.245) | (0.264) | |

| 17.country_id | 1.120 *** | 1.045 *** |

| (0.186) | (0.200) | |

| 18.country_id | 0.183 *** | 0.160 ** |

| (0.0611) | (0.0657) | |

| 19.country_id | 0.277 *** | 0.258 *** |

| (0.0632) | (0.0683) | |

| 20.country_id | 1.290 *** | 1.086 *** |

| (0.240) | (0.255) | |

| 21.country_id | 1.204 *** | 1.094 *** |

| (0.231) | (0.249) | |

| 22.country_id | 0.0261* | 0.0228 |

| (0.0145) | (0.0162) | |

| 23.country_id | 0.436 *** | 0.402 *** |

| (0.0719) | (0.0758) | |

| 24.country_id | 0.747 *** | 0.686 *** |

| (0.134) | (0.145) | |

| 25.country_id | 0.0752 * | 0.0709 * |

| (0.0397) | (0.0418) | |

| 26.country_id | 0.0854 *** | 0.0723 ** |

| (0.0297) | (0.0314) | |

| 27.country_id | 0.196 ** | 0.178 ** |

| (0.0774) | (0.0842) | |

| 28.country_id | 0.446 *** | 0.407 *** |

| (0.117) | (0.128) | |

| 29.country_id | 0.950 *** | 0.867 *** |

| (0.175) | (0.187) | |

| 30.country_id | 1.233 *** | 1.095 *** |

| (0.243) | (0.262) | |

| 2007.y | 0.00168 | 0.00410 |

| (0.0118) | (0.00905) | |

| 2008.y | −0.0184 | −0.00698 |

| (0.0136) | (0.0117) | |

| 2009.y | 0.0347 ** | 0.0582 *** |

| (0.0170) | (0.0160) | |

| 2010.y | 0.0453 *** | 0.0680 *** |

| (0.0148) | (0.0145) | |

| 2011.y | 0.0306 | 0.0616 *** |

| (0.0194) | (0.0179) | |

| 2012.y | 0.0359 | 0.0748 *** |

| (0.0224) | (0.0214) | |

| 2013.y | 0.0534 ** | 0.0913 *** |

| (0.0208) | (0.0209) | |

| 2014.y | 0.0462 ** | 0.0864 *** |

| (0.0220) | (0.0208) | |

| 2015.y | 0.0431 * | 0.0800 *** |

| (0.0225) | (0.0217) | |

| 2016.y | 0.0439 * | 0.0775 *** |

| (0.0233) | (0.0231) | |

| 2017.y | 0.0450 * | 0.0769 *** |

| (0.0247) | (0.0246) | |

| 2018.y | 0.0344 | 0.0656 ** |

| (0.0263) | (0.0266) | |

| 2019.y | 0.0426 | 0.0728 ** |

| (0.0325) | (0.0325) | |

| 2020.y | 0.0366 | 0.0605 * |

| (0.0313) | (0.0326) | |

| 2021.y | 0.0240 | 0.0472 |

| (0.0352) | (0.0365) | |

| var(e.tfee_w5) | ||

| Constant | 0.363 ** | 0.326 ** |

| (0.144) | (0.150) | |

| Observations | 480 | 480 |

Robust standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table A9.

Joint significance test for GDP per capita variables in the fixed-effects Tobit model.

Table A9.

Joint significance test for GDP per capita variables in the fixed-effects Tobit model.

| Hypothesis | F | df1 | df2 | p-Value |

|---|---|---|---|---|

| 2.34 | 2 | 459 | 0.0979 |

Table A10.

Significance test of the overall fixed-effects Tobit model.

Table A10.

Significance test of the overall fixed-effects Tobit model.

| Hypothesis | F | df1 | df2 | p-Value |

|---|---|---|---|---|

| 2.3 | 7 | 459 | 0.026 |

Figure A3.

Histogram of the residuals from the fixed-effects Tobit model.

Figure A3.

Histogram of the residuals from the fixed-effects Tobit model.

Figure A4.

Residuals versus fitted values from the fixed-effects Tobit model.

Figure A4.

Residuals versus fitted values from the fixed-effects Tobit model.

Note

| 1 | This designation is without prejudice to positions on status and is in line with UNSCR 1244 and the ICJ Opinion on the Kosovo declaration of independence. |

References

- Adom, P. K., Amuakwa-Mensah, F., & Akorli, C. D. (2023). Energy efficiency as a sustainability concern in Africa and financial development: How much bias is involved? Energy Economics, 120, 106577. [Google Scholar] [CrossRef]

- Adom, P. K., Appiah, M. O., & Agradi, M. P. (2019). Does financial development lower energy intensity? Frontiers in Energy, 14, 620–634. [Google Scholar] [CrossRef]

- Agora Energiewende. (n.d.). Variable renewable energy grid integration: Success stories—Denmark—Electricity [Report]. Agora Energiewende. Available online: https://www.agora-energiewende.org/fileadmin/Success_Stories/BP/BP_DK_RE-integration/A-E_287_Succ_Stor_BP_Denmark_Grid-Integration_WEB.PDF (accessed on 3 November 2025).

- Ahmad, S. (2024). Economic indicators and environmental expenditure: A re-evaluation of the Kuznets curve in the EU-27. Journal of Environmental Science and Economics, 3(4), 156–178. [Google Scholar] [CrossRef]

- AlKhars, M. A., Alnasser, A. H., & AlFaraj, T. (2022). A survey of DEA window analysis applications. Processes, 10, 1836. [Google Scholar] [CrossRef]

- Al-Mulali, U., & Lee, J. Y. M. (2013). Estimating the impact of financial development on energy consumption: Evidence from the GCC countries. Energy, 60, 215–222. [Google Scholar] [CrossRef]

- Altmann, M., Michalski, J., Brenninkmeijer, A., Lanoix, J.-C., Tisserand, P., Egenhofer, C., Behrens, A., Fujiwara, N., Ellison, D., & Linares, P. (2010). EU energy efficiency policy—Achievements and outlook. European Parliament, Policy Department A: Economic and Scientific Policy. [Google Scholar]

- Ang, B. W. (2006). Monitoring changes in economy-wide energy efficiency: From energy–GDP ratio to composite efficiency index. Energy Policy, 34, 574–582. [Google Scholar] [CrossRef]

- Arellano, C., Bai, Y., & Zhang, J. (2012). Firm dynamics and financial development. Journal of Monetary Economics, 59, 533–549. [Google Scholar] [CrossRef]

- Arellano, M. (2003). Panel data econometrics. Oxford University Press. [Google Scholar]

- Asmild, M., Paradi, J. C., Aggarwall, V., & Schannit, C. (2004). Combining DEA window analysis with the malmquist index approach in a study of the Canadian banking industry. Journal of Productivity Analysis, 21, 67–89. [Google Scholar] [CrossRef]

- Assi, A. F., Zhakanova Isiksal, A., & Tursoy, T. (2020). Highlighting the connection between financial development and consumption of energy in countries with the highest economic freedom. Energy Policy, 147, 111897. [Google Scholar] [CrossRef]

- Atta Mills, E. F. E., Dong, J., Yiling, L., Baafi, M. A., Li, B., & Zeng, K. (2021). Towards sustainable competitiveness: How does financial development affect dynamic energy efficiency in Belt & Road economies? Sustainable Production and Consumption, 27, 587–601. [Google Scholar] [CrossRef]

- Badunenko, O., & Tauchmann, H. (2019). Simar and Wilson two-stage efficiency analysis for Stata. The Stata Journal, 19(4), 950–988. [Google Scholar] [CrossRef]

- Batóg, J., & Pluskota, P. (2023). Renewable energy and energy efficiency: European regional policy and the role of financial instruments. Energies, 16, 8029. [Google Scholar] [CrossRef]

- Bayar, Y., Ozkaya, M. H., Herta, L., & Gavriletea, M. D. (2021). Financial development, financial inclusion and primary energy use: Evidence from the European Union transition economies. Energies, 14, 3638. [Google Scholar] [CrossRef]

- Berndt, E. R. (1978). Aggregate energy, efficiency, and productivity measurement. Annual Review of Energy, 3. [Google Scholar] [CrossRef]