Abstract

This paper addresses tests for structural change in a weakly dependent time series regression. The cases of full structural change and partial structural change are considered. Heteroskedasticity-autocorrelation (HAC) robust Wald tests based on nonparametric covariance matrix estimators are explored. Fixed-b theory is developed for the HAC estimators which allows fixed-b approximations for the test statistics. For the case of the break date being known, the fixed-b limits of the statistics depend on the break fraction and the bandwidth tuning parameter as well as on the kernel. When the break date is unknown, supremum, mean and exponential Wald statistics are commonly used for testing the presence of the structural break. Fixed-b limits of these statistics are obtained and critical values are tabulated. A simulation study compares the finite sample properties of existing tests and proposed tests.

JEL Classification:

C10; C22

1. Introduction

This paper focuses on fixed-b inference of heteroskedasticity and autocorrelation (HAC) robust Wald statistics for testing for a structural break in a time series regression. We focus on kernel-based nonparametric HAC estimators which are commonly used to estimate the asymptotic variance. HAC estimators allow for arbitrary structure of the serial correlation and heteroskedasticity of weakly dependent time series and are consistent estimators of the long run variance under the assumption that the bandwidth (M) is growing at a certain rate slower than the sample size (T). Under consistency assumptions, the Wald statistics converge to the usual chi-square distributions. However, because the critical values from the chi-square distribution are based on a consistency approximation for the HAC estimator, the chi-square limit does not reflect the often substantial finite sample randomness of the HAC estimator. Furthermore, the chi-square approximation does not capture the impact of the choice of the kernel or the bandwidth on the Wald statistics. The sensitivity of the statistics to the finite sample bias and variability of the HAC estimator is well known in the literature; Kiefer and Vogelsang (2005) [1] among others have illustrated by simulation that the traditional inference with a HAC estimator can have poor finite sample properties.

Departing from the traditional approach, Kiefer and Vogelsang [1,2,3] obtain an alternative asymptotic approximation by assuming that the ratio of the bandwidth to the sample size, , is held constant as the sample size increases. Under this alternative nesting of the bandwidth, they obtain pivotal asymptotic distributions for the test statistics which depend on the choice of kernel and bandwidth tuning parameter. Simulation results indicate that the resulting fixed-b approximation has less size distortions in finite samples than the traditional approach, especially when the bandwidth is not small.

Theoretical explanations for the finite sample properties of the fixed-b approach include the studies by Hashimzade and Vogelsang (2008) [4], Jansson (2004) [5], Sun, Phillips and Jin (2008, hereafter SPJ) [6], Gonçalves and Vogelsang (2011) [7] and Sun (2013) [8]. Hashimzade and Vogelsang (2008) [4] provides an explanation for the better performance of the fixed-b asymptotics by analyzing the bias and variance of the HAC estimator. Gonçalves and Vogelsang (2011) [7] provides a theoretical treatment of the asymptotic equivalence between the naive bootstrap distribution and the fixed-b limit. Higher order theory is used by Jansson (2004) [5], SPJ (2008) [6] and Sun (2013) [8] to show that the error in rejection probability using the fixed-b approximation is more accurate than the traditional approximation. In a Gaussian location model, Jansson (2004) [5] proves that for the Bartlett kernel with bandwidth equal to sample size (i.e., ), the error in rejection probability of fixed-b inference is which is smaller than the usual rate of . The results in SPJ (2008) [6] complement Jansson’s result by extending the analysis for a larger class of kernels and focusing on smaller values of bandwidth ratio b. In particular, they find that the error in rejection probability of the fixed-b approximation is around . They also show that for positively autocorrelated series, which is typical for economic time series, the fixed-b approximation has smaller error than the chi-square or standard normal approximation, even when b is assumed to decrease to zero although the stochastic orders are same.

In this paper, fixed-b asymptotics is applied to testing for structural change in a weakly dependent time series regression. The structural change literature is now enormous and no attempt will be made here to summarize the relevant literature. Some key references include Andrews (1993) [9], Andrews and Ploberger (1994) [10], and Bai and Perron (1998) [11]. Andrews (1993) [9] treats the issue of testing for a structural break in the generalized method of moments framework when the one-time break date is unknown and Andrews and Ploberger (1994) [10] derive asymptotically optimal tests. Bai and Perron (1998) [11] considers multiple structural change occurring at unknown dates and covers the issues of estimation of break dates, testing for the presence of structural change and testing for the number of breaks. For a comprehensive survey of the recent structural break literature see Perron (2006) [12], Banerjee and Urga (2005) [13], and Aue and Horváth (2013) [14]. The fixed-b analysis can be extended to the case of multiple breaks but the simulation of critical values will be computationally intensive. Therefore, we leave the case of multiple breaks for future research and we consider the case of a single break in this paper.

For testing the presence of break, the robust version of the Wald statistic is considered in this paper and a HAC estimator is used to construct the test statistic. The ways of constructing HAC estimators in the context of structural change tests are well described in Bai and Perron (2003) [15] and Bai and Perron (1998) [11]. We focus mainly on the HAC estimator documented in Bai and Perron (2003) (Section 4.1, [15]) in which the usual “Newey-West-Andrews” approach is applied directly to the regression with regime dummies. Under the assumption of a fixed bandwidth ratio (fixed-b assumption), the asymptotic limit of the test statistic is a nonstandard distribution but it is pivotal. As in standard fixed-b theory, the impact of choice of bandwidth on the limiting distribution is substantial. In particular, the bandwidth interplays with the hypothesized break fraction so that the limit of the test statistic depends on both of them. For the unknown break date case, three existing test statistics (Sup-, Mean-, Exp-Wald) are considered and their fixed-b critical values are tabulated. The finite sample performance is examined by simulation experiments with comparisons made to existing tests. For practitioners, we include results using a data-dependent bandwidth rule based on Andrews (1991) [16]. This data-dependent bandwidth is calculated from the regression using the break fraction that yields the minimum sum of squared residuals (Bai and Perron, 1998 [11]). One can calculate a bandwidth ratio with this data-dependent bandwidth () and proceed to apply the fixed-b critical values corresponding to this specific value of .

The remainder of this paper is organized as follows. In Section 2, the basic setup of the full/partial structural-change model is presented and preliminary results are provided. Section 3 derives the fixed-b limit of the Wald statistic and the fixed-b critical values, for the case of unknown break dates, are tabulated in Section 4. Section 5 compares empirical null rejection probabilities and provides the size-adjusted power for tests based on the data-dependent bandwidth ratio. Section 6 concludes. Proofs and definitions are collected in Appendix A.

2. Setup and Preliminary Results

Consider a weakly dependent time series regression model with a structural break given by

where is regressor vector, is a break point, and is the indicator function. Define and Recalling that denotes the integer part of a real number, x, notice that for and for For the time being, the potential break point (fraction) λ is assumed to be known in order to develop the asymptotic theory for a test statistic and characterize its asymptotic limit. We will relax this assumption to deal with the empirically relevant case of an unknown break date. The regression model (1) implies that coefficients of all explanatory variables are subject to potential structural change and this model is labeled the ‘full’ structural change model.

We are interested in testing the presence of a structural change in the regression parameters. Consider the null hypothesis of the form

where

and is an matrix with Under the null hypothesis, we are testing that one or more linear relationships on the regression parameter(s) do not experience structural change before and after the break point. Tests of the null hypothesis of no structural change about a subset of the slope parameters are special cases. For example, we can test the null hypothesis that the slope parameter on the first regressor did not change by setting . We can test the null hypothesis that none of the regression parameters have structural change by setting . We focus on the OLS estimator of β given by

In order to establish the asymptotic limits of the HAC estimators and the Wald statistics, two assumptions are sufficient. These assumptions imply that there is no heterogeneity in the regressors across the segments and the covariance structure of the errors is assumed to be the same across segments as well.

Assumption 1.

uniformly in and exists.

Assumption 2.

where is a standard Wiener process, and ⇒ denotes weak convergence.

For later use, we define a nonsingular matrix A such that and where is standard Wiener process. For a more detailed discussion about the regularity conditions under which Assumptions 1 and 2 hold, refer to Kiefer and Vogelsang (2002) [3] and see Davidson (1994) [17], Phillips and Durlauf (1986) [18], Phillips and Solo (1992) [19], and Wooldridge and White (1988) [20] for more details.

The matrix Q is the second moment matrix of and is typically estimated using the quantity . The matrix is the asymptotic variance of which is, for a covariance stationary series, given by

Consider the non-structural change regression equation where and this coefficient parameter is estimated by OLS . In this particular setup, the long run variance, is commonly estimated by the kernel-based nonparametric HAC estimator given by

where , M is a bandwidth, and is a kernel weighting function.

Under some regularity conditions (see Andrews (1991) [16], DeJong and Davidson (2000) [21], Hansen (1992) [22], Jansson (2002) [23] or Newey and West (1987) [24]), is a consistent estimator of Σ, i.e., . These regularity conditions include the necessary condition that as . This asymptotics is called “traditional” asymptotics throughout this paper.

In contrast to the traditional approach, fixed-b asymptotics assumes where b is held constant as T increases. Assumptions 1 and 2 are the only regularity conditions required to obtain a fixed-b limit for . Under the fixed-b approach, for , Kiefer and Vogelsang (2005) [1] show that

where is a p-vector of standard Brownian bridges and the form of the random matrix depends on the kernel. Following Kiefer and Vogelsang (2005) [1], we consider three classes of kernels which give three forms of . Let denote a generic vector of stochastic processes. denotes its transpose. is defined in Appendix A.

Getting back to our structural change regression model, fixed-b results depend on the limiting behavior of the following partial sum process given by

Under Assumptions 1 and 2, the limiting behavior of and the partial sum process are given as follows.

Proposition 1.

Let be given. Suppose the data generation process is given by (1) and let denote the integer part of where . Then, under Assumptions 1 and 2 as

and

where

and

See Appendix A for the proof.

It is easily seen that the asymptotic distributions of and are Gaussian and are independent of each other. Hence the asymptotic covariance of and is zero. The asymptotic variance of is given by where

In order to test the null hypothesis (2), HAC robust Wald statistics are considered. These statistics are robust to heteroskedasticity and autocorrelation in the vector process, The generic form of the robust Wald statistic is given by

where

and is a HAC robust estimator of Ω.

We consider a particular way of constructing the HAC estimator. This estimator is the same one as in Bai and Perron (2003) [15]. Denoted by it is constructed using the residuals directly from the dummy regression (1):

where . We denote the components of as and . Notice that is the variance estimator one would be using if the usual “Newey-West-Andrews” approach is applied directly to the dummy regression (1).

Using we can write as

Three important observations are in order. First, the main component of the two diagonal blocks are within regime HAC estimators of Σ, the long run variance of However, one should see that the “effective” bandwidth ratio being applied to is not b but which is bigger than b since Similarly, the effective bandwidth ratio for is . As documented in fixed-b literature (e.g., Kiefer and Vogelsang (2005) [1]), the bias in HAC estimators not accounted by traditional inference increases as the bandwidth ratio gets bigger. So, when the HAC estimator is constructed as in (8), traditional inference might be often exposed to size distortion—more than expected—due to this mechanism of determining effective bandwidths. The second issue is that the above estimator has non-zero off-diagonal blocks. So, the methodology based on partial samples such as in Andrews (1993) [9] does not exactly cover this case because the off-diagonal blocks in Andrews (1993) [9] are assumed to be zero, matching the zero asymptotic covariance of the OLS estimators of the slope coefficients between pre- and post-regimes. It is presumable that the influence of having non-zero off diagonal terms might be small since the off-diagonal blocks converge to zero under the traditional assumption as sample size grows (see a proof in Cho (2014) [25] for the Bartlett kernel) but it might still negatively affect the performance of tests in finite samples and we need to develop an alternative asymptotic theory to explicitly reflect the presence of these components. Third, there is another issue when a researcher uses a data-dependent bandwidth as in Andrews (1991) [16]. For a given hypothesized break fraction, a data-dependent bandwidth can be calculated based on the pooled series of and This method would result in an optimal bandwidth which minimizes the MSE in estimating Σ but the presence of non-zero off-diagonal terms are not taken into account in this procedure. Moreover, when the break date is treated as unknown, a sequence of data-dependent bandwidth across potential break dates will be generated. In this case, the fixed-b limits are not useful approximations because the sequence of the data-dependent bandwidth is random by nature so the limiting distributions of corresponding test statistics cannot be characterized by a single particular value of

Denote by , the Wald statistic given by (6) using the break date with used for . Tests for a potential structural break with an unknown break date are well studied in Andrews (1993) [9], Andrews and Ploberger (1994) [10], and Bai and Perron (1998) [11]. Andrews (1993) [9] considers several tests based on the supremum across breakpoints of Wald and Largrange multiplier statistics and shows that they are asymptotically equivalent. Andrews and Ploberger (1994) [10] derives tests that maximize average power across potential breakpoints.

As argued by Andrews (1993) [9] and Andrews and Ploberger (1994) [10], break dates close to the end points of the sample cannot be used and so some trimming is needed. To that end, define with to be the set of admissible break dates. The tuning parameter, ϵ, denotes the amount of trimming of potential break dates. We consider the three statistics following Andrews (1993) [9]1 and Andrews and Ploberger (1994) [10]2 defined as

The next section provides asymptotic results for the robust Wald statistics under the fixed-b asymptotics.

3. Asymptotic Results

3.1. Asymptotic Results under the Fixed-b Approach

We now provide fixed-b limits for the HAC estimators and the test statistics in the full structural change model (1). The fixed-b limits presented in the next Lemma and Corollary approximate the diagonal blocks of by random matrices. Also, it is shown that the fixed-b approach gives a non-zero limit for the off-diagonal blocks, which further distinguishes fixed-b asymptotics from traditional asymptotics.

Lemma 1.

Let be given and suppose Then under Assumptions 1 and 2, as ,

where

and is defined by (A1)–(A3) with .

See Appendix A for the proof.

Next, Corollary presents alternative representations for for three classes of kernels. The definitions of these classes of kernels (Classes 1, 2 and 3) are given in Appendix A. Three popular kernels—the Quadratic Spectral, Bartlett and Parzen kernels—belong to Classes 1, 2 and 3, respectively. See Cho (2014) [25] for the proof of this Corollary.

Corollary 1.

where

for Classes 1,2 and 3 kernels respectively.

The expression for in this Corollary makes it easier to compare the fixed-b limit of with the standard fixed-b limit (see (3)) appearing in a non-structural change setting. Since each diagonal block of is basically a HAC estimator (up to a scale factor; see (8)) based on one of the pre- or post- break data, its limit should take the same form as (3), which is verified in this Corollary. So, each diagonal component of serves to reflect the randomness and bandwidth/kernel-dependence of the associated HAC estimator. Second, unlike the traditional approach, the fixed-b limit of the off-diagonal component is non-zero. This implies that the fixed-b approach is able to take account of the covariance between and which is generally non-zero in finite samples. The limits of the Wald statistics can be derived by using Lemma 1 and the result is presented in the next Theorem.

Theorem 1.

Let be given. Suppose Then under Assumptions 1 and 2, as ,

See Appendix A for the proof.

The next Corollary provides an alternative representation for the limit given in (17). The proof for this Corollary is given in Cho (2014) [25].

Corollary 2.

For a given value of , the fixed-b limit of has the same distribution as

where

and and are Brownian Bridge processes which are independent of each other and of

The limit in (18) shows how the components of affect the distribution of As mentioned earlier, the random matrix reflects the random nature of which is part of the estimator of the asymptotic variance of . Notice that the effective bandwidth for turns out to be not Thus, we implicitly use the bandwidth ratio for when we use a full sample bandwidth ratio b for constructing The second component, , is related to (and in exactly the same fashion. Finally, the third component, , captures the impact of finite sample covariance between and on structural change inference.

Now consider the unknown break date case and let denote the limit of where the form of depends on whether traditional or fixed-b asymptotic theory is being used. In the case of fixed-b theory, is given in (17). Under the traditional assumption that the bandwidth ratio goes to zero as T grows,

The asymptotic limits of Sup-, Mean-, and Exp-Wald statistics immediately follow from the continuous mapping theorem given by

3.2. Extension to the Partial Structural Change Model

This section derives the fixed-b limit of in the partial structural change model. The main result of this section is that the limit is the same as the limit for the full structural change model. The regression model with partial structural change is given by

where is and is vector and

The coefficients on the regressors are unrestricted in terms of a structural change whereas the coefficients on the regressors are assumed to not have structural change. Denote

The parameters are estimated by OLS and the OLS residual vector can be written as

where

The residual for an individual observation is given by

Also, note that

The following assumptions replace Assumptions 1 and 2:

Assumption 3.

where is a matrix, is a matrix, and is a vector of independent Wiener process.

Assumption 4.

and uniformly in , and and exist.

We continue to focus on tests of the null hypothesis of no structural change in the slope parameters of the form

with

Recall that the OLS estimator, can be rewritten as

Proposition 2.

Under Assumptions 3 and 4, as

and

where

See Appendix A for the proof.

As seen from the above proposition, and are not asymptotically independent in the partial structural change regression model. This is true because we are projecting out the variation of explanatory variables so that and depend on the entire series of and . The dichotomy that is dependent only on the pre-break data and that depends only on the post-break data no longer holds in the partial structural change model. The dependence manifests in the common term, , in Proposition 2. However, this term cancels out in (23) when the restriction matrix takes the form of (21). As a result, and also as suggested by Equation (23), in principle we need to estimate only for testing for partial structural change. Because , extended for the case of partial structural change, does not impose any restrictions on the asymptotic correlation between and , continues to allow asymptotically pivotal fixed-b tests for partial structural change. While not obvious at first glance, has the same fixed-b limit in the partial structural change case as it does in the full structural change case.

The Wald statistic for testing for partial structural change is given by

where . For constructing , we use the HAC estimator which is computed using :

where By the Frisch-Waugh-Lovell Theorem, this is the straightforward extension of to the case of partial structural change.

The next Lemma provides the limit of the scaled partial sum process of premultiplied by an appropriate term.

Lemma 2.

Let . Under Assumptions 3 and 4, as

where

See Appendix A for the proof.

As Lemma 2 shows, the partial sums of the inputs to are asymptotically proportional to the same nuisance parameters as . This is the key condition for a pivotal fixed-b limit. The next Theorem provides the fixed-b limit of

Theorem 2.

Let be given. Suppose . Then, under Assumptions 3 and 4, weakly converges to the same limit in (17), i.e., as ,

See Appendix A for the proof.

According to Theorem 2, the limit of in the partial structural change model is the same as in the full structural change model.

4. Critical Values

While the fixed-b limiting distributions are nonstandard, asymptotic critical values are easily obtained via simulations. We approximate the Wiener processes in the limiting distributions using scaled partial sums of 1000 i.i.d. random variables. Critical values are tabulated based on 50,000 replications3.

In Table 1, fixed-b critical values for and are provided for , and for Critical values over the entire grid of 0.02-increment of b are available upon request.

5. Finite Sample Properties

In this section, we report the results of a finite sample simulation study that illustrates the performance of fixed-b critical values relative to traditional critical values. The data generating process (DGP) is given by (1) with where is a scalar time series, , and . We use the break point . The regressor and the regression error are generated as and where and are independent of each other with i.i.d. . We use the parameter values: and (see Table 2):

Table 2.

Parameter values for simulations

The value of θ measures the persistence of the time varying regressor The parameters ρ and φ jointly determine the serial correlation structure of the error term . Bigger values of these three parameters lead to higher persistence of the series except for specification A where bigger values of θ would not increase persistence in . We set , and , . Under the null hypothesis of no structural change, , whereas for there is structural change in both the intercept and slope parameters. We report results for sample sizes and 1000 and the number of replications is 2500. The nominal level of all tests is 5%. We compute the //- statistics for testing the joint null hypothesis of no structural change in both the intercept and slope parameters. The frequency of rejections for the case of measures the empirical type-I error.4

We report empirical rejection frequencies for traditional inference and for fixed-b inference. In traditional inference, we select the bandwidth following Andrews (1991) [16] for each hypothesized break date using the AR(1) plug-in formula. For fixed-b inference, we report results for different values of b to show how the null rejection probability varies with the choice of We also give results for another test in which a single data-dependent bandwidth ratio, denoted by is used across all hypothetical break dates and a fixed-b critical value is applied. The data-dependent bandwidth ratio, is computed as follows. We find the break date which minimizes the sum of squared residuals; we use that break date to select Andrews (1991) [16] data-dependent bandwidth () with the AR(1) plug-in formula and calculate the implied bandwidth ratio (); we implement the test using the fixed-b critical values for

The rationale behind is as follows. If a different bandwidth is used for each potential break point within the trimming range, then the fixed-b limits of the sup/mean/exp statistics will be functions of those bandwidth ratios and tabulation of fixed-b critical values will be computationally prohibitive. To provide practitioners with a data-dependent bandwidth approach that can be implemented with fixed-b critical values, we need a single data-dependent bandwidth to be used for all potential break points in which case the tabulated critical values can be used. Given the nice properties of the least squares estimator of the break point under the alternative of structural change (see Bai and Perron (1998) [11]), it is natural to use the least squares estimator of the break point to generate residuals needed to implement the Andrews (1991) [16] plug-in formula. Under the null of no structural change, any break point, including the least squares break point, will generate useful residuals for the Andrews (1991) [16] plug-in formula. Crainiceanu and Vogelsang (2007) [28] also considered using the least squares estimator of the break point to deal with the nonmonotonic power of the CUSUM test.

Table 3 provides empirical null rejection frequencies for the traditional tests. For each hypothetical break date, the HAC estimator is constructed using the data-dependent bandwidth. For DGP A with zero persistence, all tests using are subject to severe size distortions when the sample size is 100. Having more data or using more trimming helps reduce the size distortions. The null rejections decrease towards the 5% nominal level for all statistics when T is 500 and Under the DGP B, as the sample size increases from 100 to 500, the null rejection probabilities drop to 0.194 from 0.594 for the supremum test with and the QS kernel being used. The T = 500 rejection rate is still far from the nominal level. Size distortions get worse under more persistent data (DGP C). The mean test, which has the least size distortion of the three statistics, only attains a null rejection of 0.368 with the larger trimming value and T = 500. While traditional inference provides tests with reasonable size under DGPs with zero or mild persistence, as the DGP becomes more persistent, over-rejections can be substantial.

Table 3.

Empirical Null Rejection Probabilities, traditional - tests with 5% Nominal Size, : No Structural Change ().

Table 4, Table 5 and Table 6 present simulation results for fixed-b inference. A single bandwidth ratio, is applied across all hypothetical break dates in constructing HAC estimators. We report results for and These tables also contain the null rejection probability when the traditional critical values in Andrews (1993) [9] or Andrews and Ploberger (1994) [10] are used. The traditional critical values are not designed to work well with relatively large bandwidths and this can be clearly seen in the tables. In general, as the bandwidth ratio gets bigger, the tendency to over-reject becomes more and more pronounced because using more lags generates a systematic downward bias in the HAC estimator and pushes up the value of test statistic. The traditional critical values do not take this impact of lag-choice into account. Because the effective bandwidths play important roles for the behavior of the HAC estimator (8), the impact of using large values of b is greater than for HAC estimators in non-structural change settings.

Table 4.

Empirical Null Rejection Probabilities, test with 5% nominal size, , : No Structural Change (), .

Table 5.

Empirical Null Rejection Probabilities, test with 5% nominal size, , : No Structural Change (), .

Table 6.

Empirical Null Rejection Probabilities, test with 5% nominal size, , : No Structural Change (), .

For fixed-b inference, several patterns stand out in Table 4 for the supremum test. Rejections using fixed-b critical values are similar to the rejections in traditional inference when a small bandwidth ratio is used. However, as the bandwidth increases, rejections using fixed-b critical values systematically decrease towards the nominal level of 0.05. Under DGP B, the null rejections decrease as 0.131→0.096→0.083→0.086 over the range of b with T = 500 and the Bartlett kernel and being used. Even under DGP C, the null rejections approach the nominal level as b increases for all sample sizes when the QS kernel and the trimming value of 0.2 are used.

Table 7 gives null rejection probabilities when using the data-dependent bandwidth ratio . Columns on the left give rejections using fixed-b critical values whereas columns on the right give rejections using traditional critical values. Patterns in Table 7 are similar to patterns in Table 4, Table 5 and Table 6. Over-rejections are often large when traditional critical values are used. Over-rejections are systematically smaller when fixed-b critical values are used and works reasonably well if the sample size is large enough relative to the strength of the persistence in the data. This is particularly true when the QS kernel is used with 0.2 trimming for the mean statistic and 0.05 trimming for the supremum and exponential statistics.

Table 7.

Empirical Null Rejection Probabilities, - test using bandwidth ratio with 5% nominal size, No Structural Change (), .

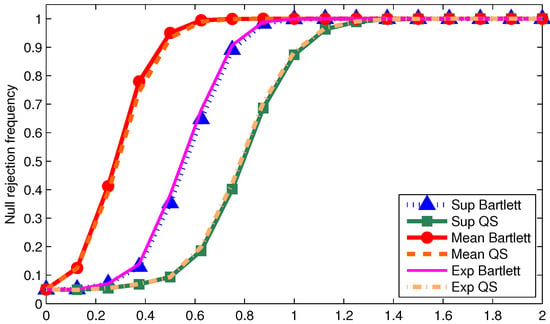

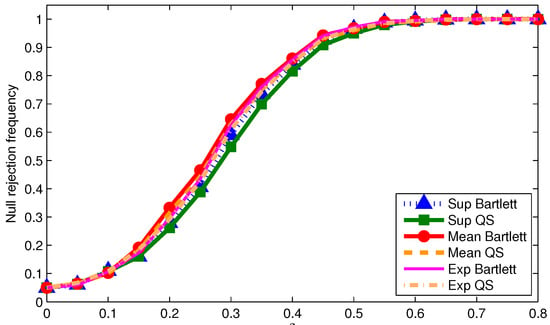

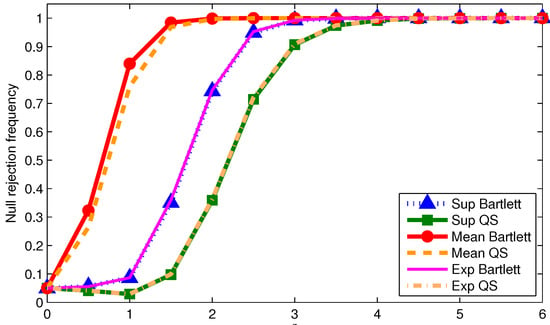

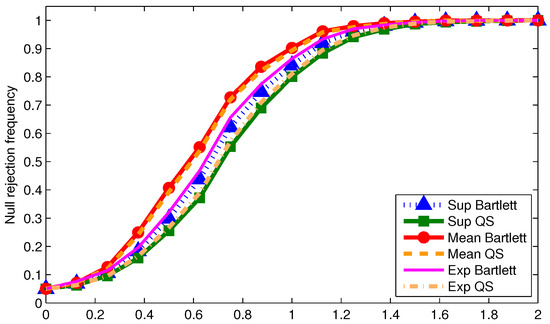

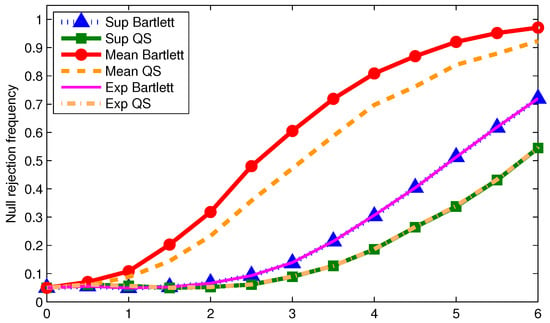

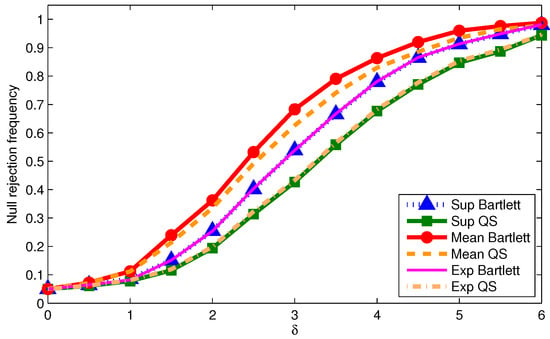

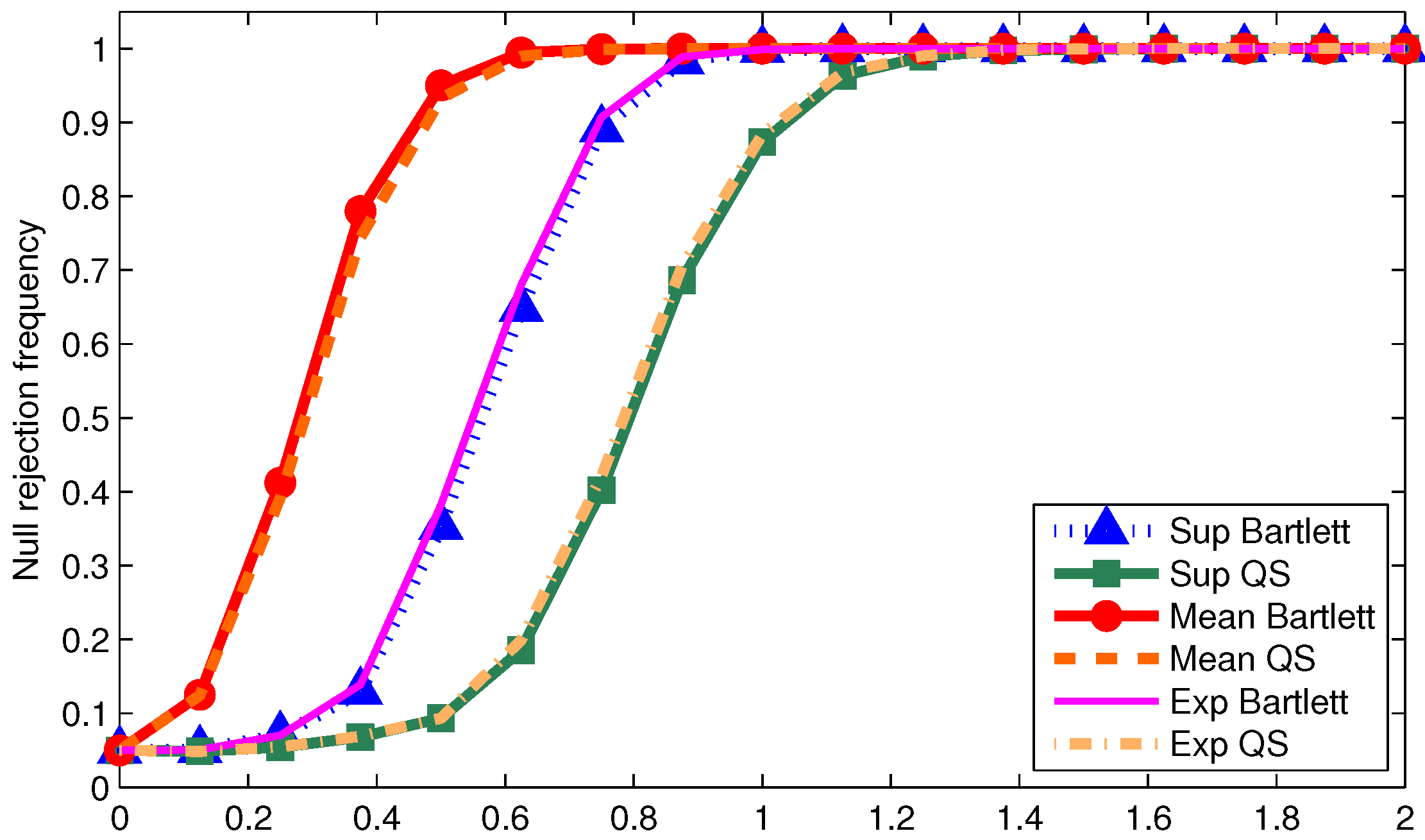

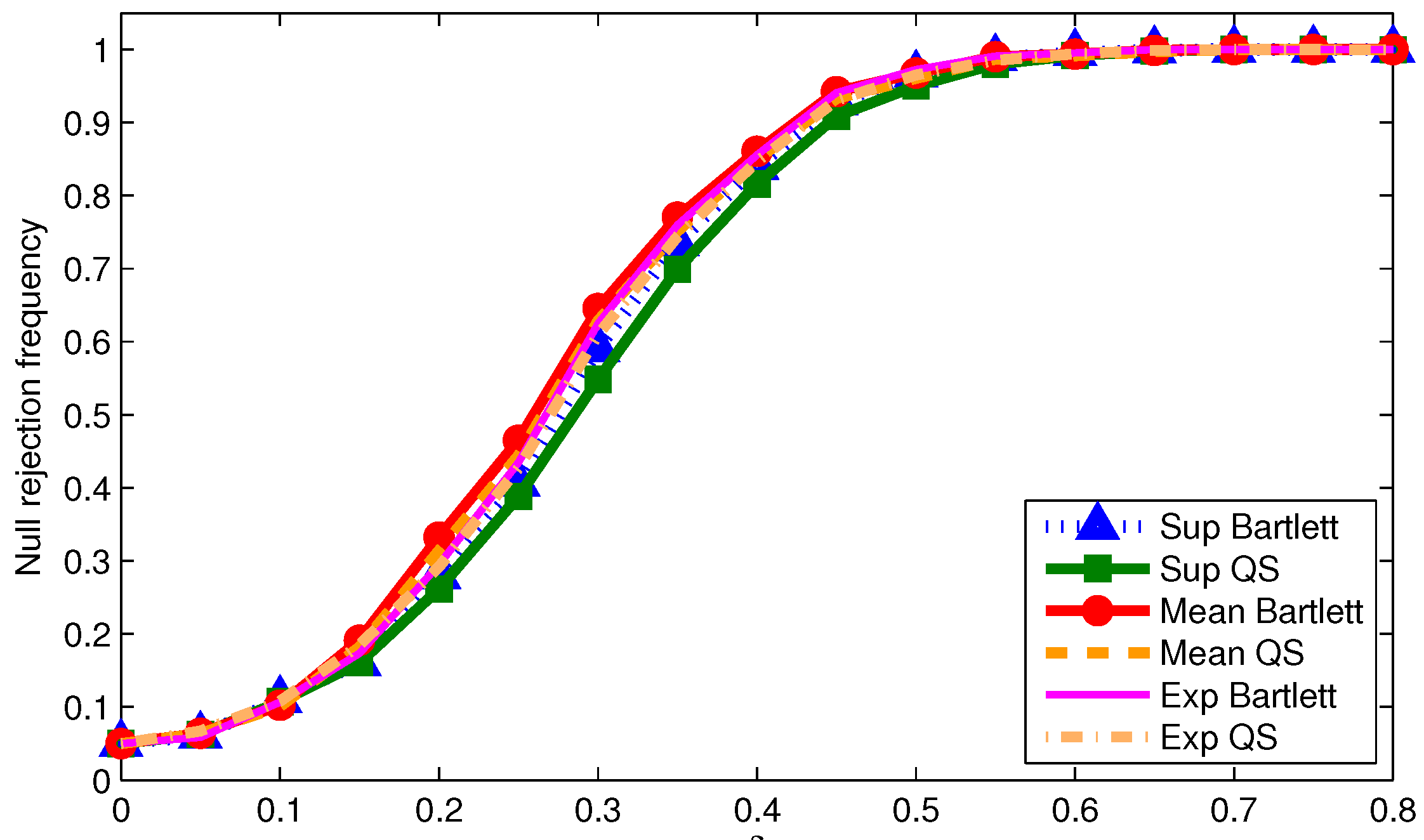

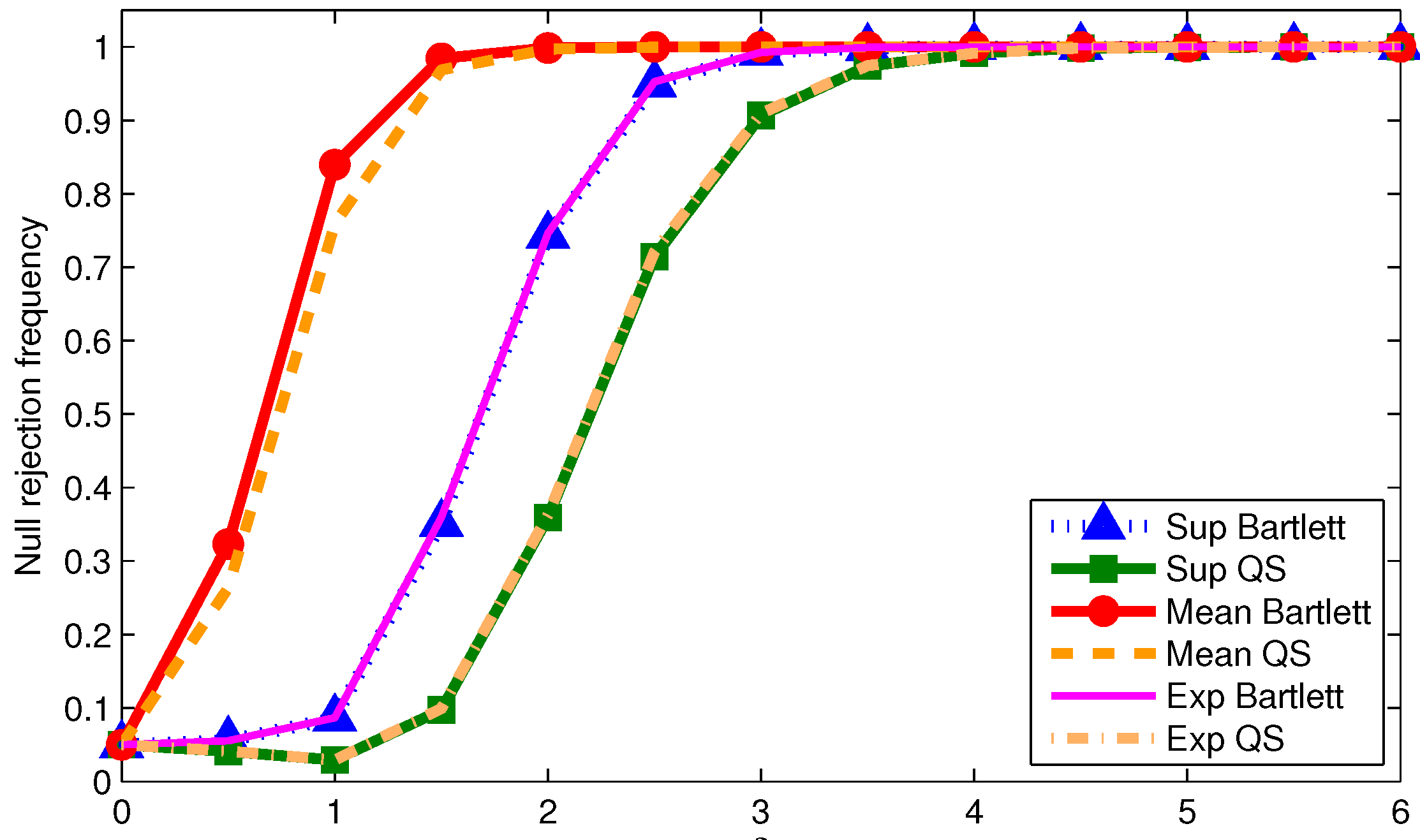

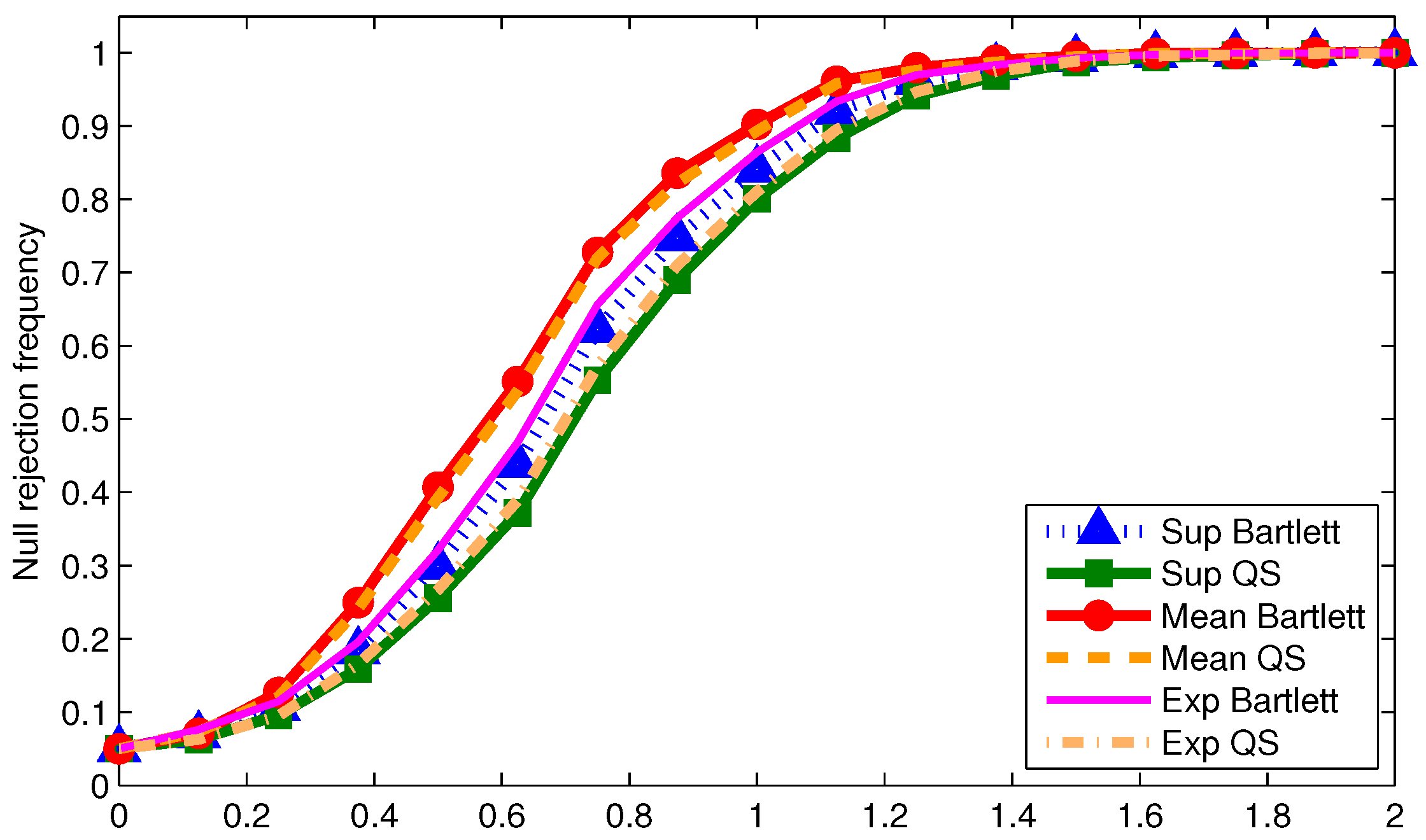

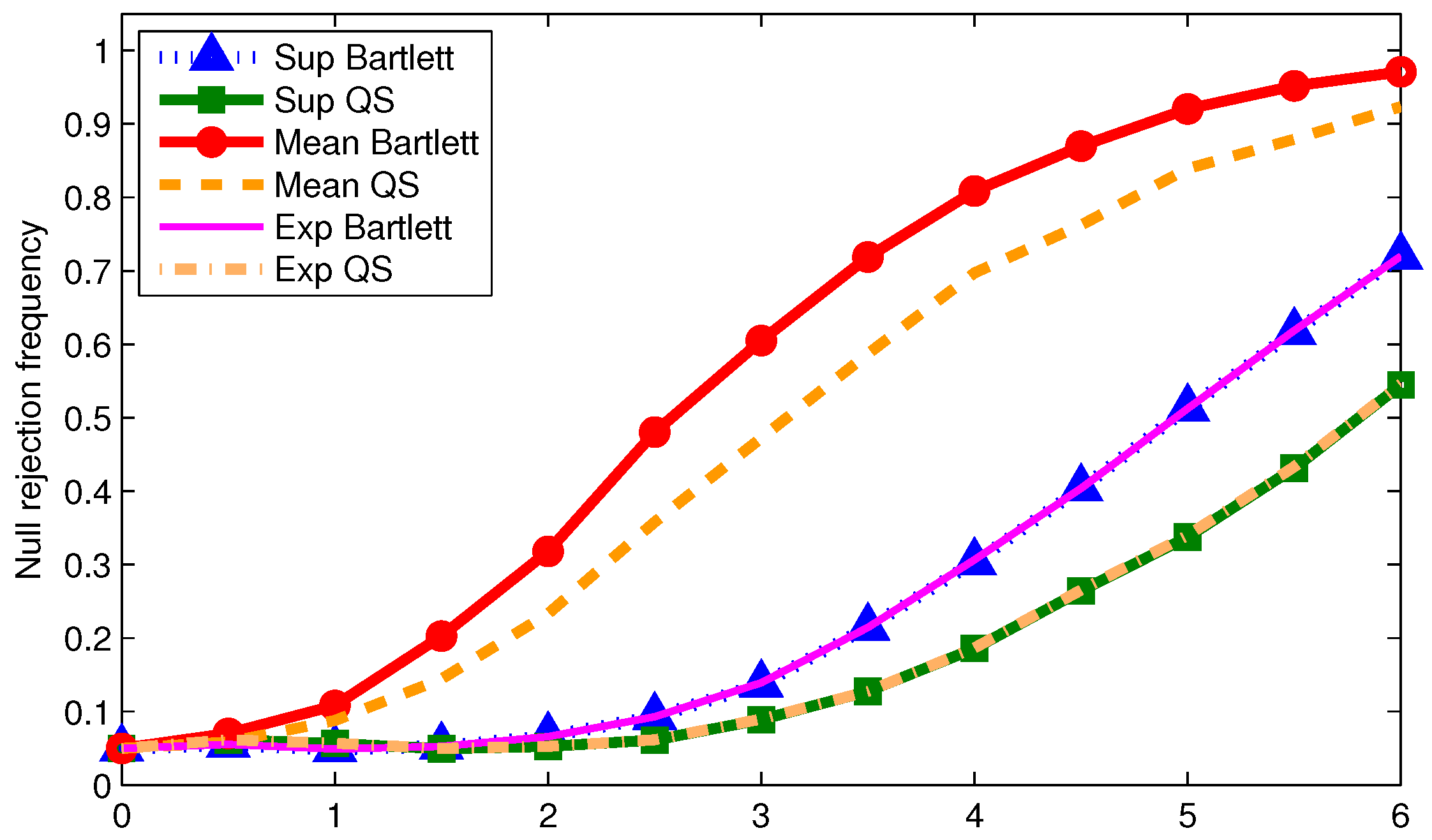

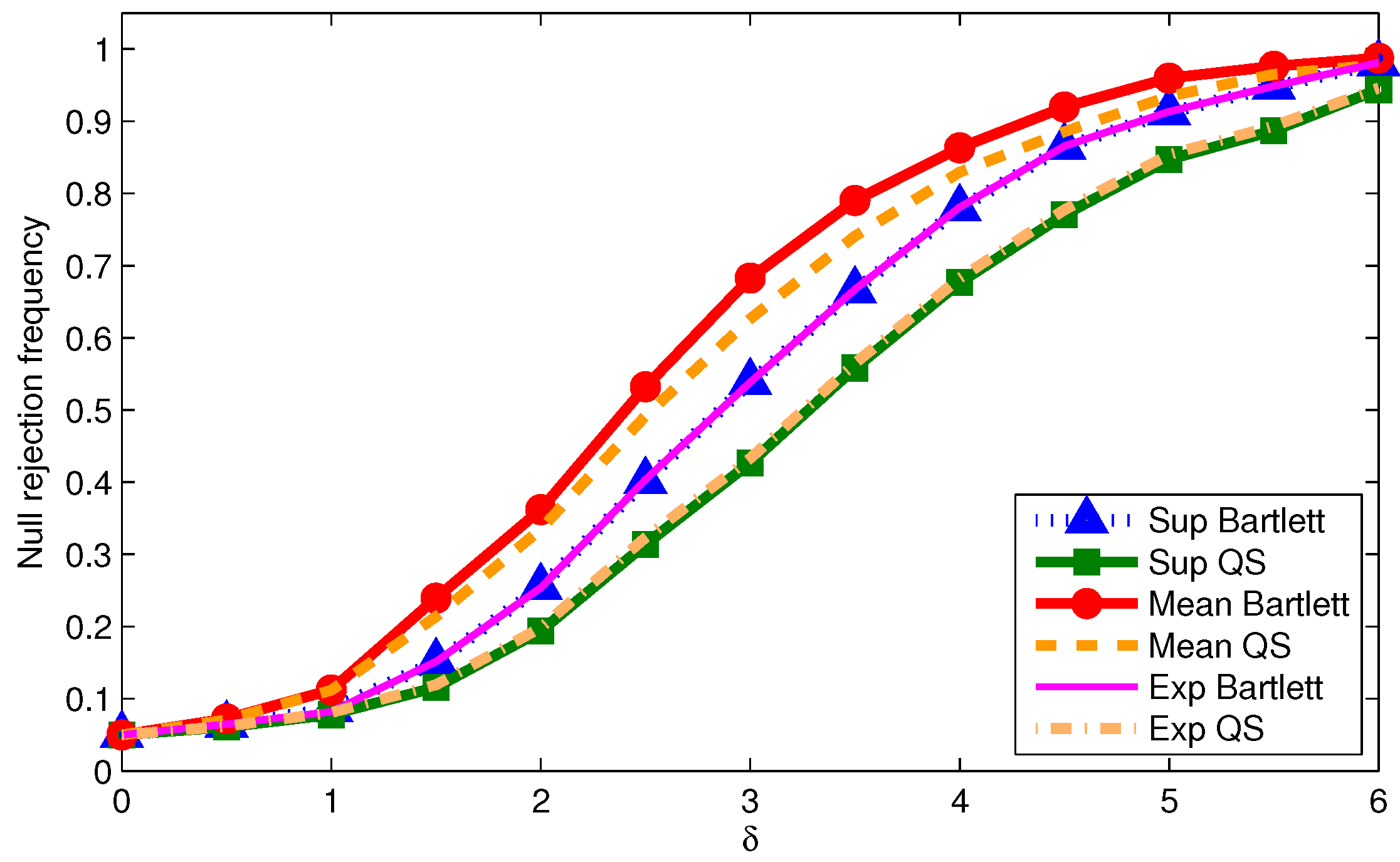

We now examine the power of the tests when using We report size-adjusted power for T = 200 in Figure 1, Figure 2, Figure 3, Figure 4, Figure 5 and Figure 6. Recall the break point under the alternative is Odd (even) numbered figures give results with 0.05 (0.2) trimming. Results are given for the three DGPs used for the tables. First note that more trimming leads to higher power in all cases as one would expect. Second, the mean statistic tends to have the highest power regardless of the DGP or kernel. This is not surprising given the power optimality properties of the mean statistic derived by Andrews and Ploberger (1994) [10] using traditional asymptotics. Third, for a given kernel, the supremum and exponential statistics have almost the same power across DGPs and trimming. This is somewhat surprising given that under traditional asymptotics, the exponential statistic is in the class of power optimal tests but the supremum statistic is not. This finding could be driven by values of being far away from zero in which case the traditional asymptotics might not be accurately reflecting finite sample power. Finally, the Bartlett kernel tends to give tests with higher power than the QS kernel; a similar finding was made by Kiefer and Vogelsang (2005) [1] in models without structural change.

Figure 1.

Size adjusted power, DGP A, T = 200.

Figure 2.

Size adjusted power, DGP A, T = 200.

Figure 3.

Size adjusted power, DGP B, T = 200.

Figure 4.

Size adjusted power, DGP B, T = 200.

Figure 5.

Size adjusted power, DGP C, T = 200.

Figure 6.

Size adjusted power, DGP C, T = 200.

The size and power results for the statistics implemented with point to the typical size-power tradeoff when using HAC variance estimators. Configurations that give the least size distortions also tend to have low power. As long as the data is not too persistent relative to the sample size, a reasonable approach for practice that balances size distortions and power is to use the mean statistic with 0.2 trimming implemented with the QS kernel with and fixed-b critical values.

6. Summary and Conclusions

In this paper, fixed-b asymptotics is applied to the problem of testing for the presence of a structural break in a weakly dependent time series regression. The statistic is the Wald statistic that one obtains when structural change is expressed in terms of dummy variables interacted with regressors as in Bai and Perron (1998, 2003) [11,15]. We derived the fixed-b limit of the statistic. In both the full structural change and partial structural change model, the Wald statistic has the same pivotal fixed-b limit. We tabulated fixed-b critical values for - statistics which are commonly used for testing parameter instability when the break point is unknown. In a simulation study, we examined the finite sample properties of traditional and fixed-b inference. With persistent data, traditional inference suffers from substantial size distortions. Using fixed-b critical values markedly improves over-rejection problem. A reasonable approach for practice that balances size distortions and power is to use the mean statistic with 0.2 trimming implemented with the QS kernel, and fixed-b critical values.

Acknowledgments

We thank the editor and three anonymous referees for helpful suggestions and comments.

Author Contributions

Both authors contributed equally to the paper.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A. Definitions and Proofs

Definitions

Case 1.

Suppose is twice continuously differentiable everywhere (Class 1) such as the Quadratic Spectral kernel (QS), then

where is the second derivative of the kernel

Case 2.

Suppose is the Bartlett kernel (Class 2), then

Case 3.

Suppose is continuous, for , and is twice continuously differentiable everywhere except for (Class 3) (e.g., Parzen kernel), then

where i.e., is the derivative of from the left at

The following expression is a general representation of the HAC estimators:

This representation can be rewritten in terms of the partial sum processes following Kiefer and Vogelsang (2005) [1] and Hashimzade and Vogelsang (2008) [4] as follows. Let . Then, for the kernels in Class 1, we have

where

For the Class 2 kernel (Bartlett), we have

For the kernels in Class 3, we have

Proof of Proposition 1.

The limit of the follows immediately under Assumptions 1 and 2. Also, plugging the limits of and into Equation (4) yields, for

and for

Thus, we can rewrite this result by using indicator functions as

where

☐

Proof of Lemma 1.

Plugging the limit of the partial sum process in Proposition 1 into the HAC estimators in (A4)–(A6), the desired result follows from direct application of the continuous mapping theorem to obtain the desired result in (12). ☐

Proof of Theorem 1.

Recall that

Using it follows that

Using Assumption 1 and Lemma 1,

By writing in the form (A1)–(A3) using , we obtain, after some algebra, the following expression for the above limit:

Now apply the transformation: with and conclude

yielding the desired result:

☐

Proof of Proposition 2.

Standard algebra gives

and it immediately follows that

Under Assumptions 3 and 4, it follows in a straightforward manner that

In order to derive the limit of , the following standard results are useful:

Also, well known matrix algebra properties (see e.g., Schott (1997) [29]), we can write

and using (A8), one can further show that

where

Now plug (A9) into (A7) to conclude that

The following lemma is used in the proof of Lemma 3.

Lemma 3.

Let . Then it holds that .

Proof of Lemma 3.

One can easily show

The desired result comes from the identity by substituting Equation (A9) for . ☐

Proof of Lemma 2.

First note that implicit in the proof of Proposition 2 is the result that . For , it follows that

using (A9). The scaled partial sum process is given by

For the first term in (A11) satisfies

Hence with from (A10) and (A12), it follows that

For the first part of the second term in (A11), it follows that

where Hence with

which combined with (A7) and Lemma 3 immediately yields

Finally, premultiplying the third term in (A11) by gives

Combining the results for the three terms gives

Similar results can be obtained for

and

Now combining the results for the three terms gives Thus, we obtain for

☐

Proof of Theorem 2.

To save space, the proof for this Theorem is provided only for the case of the Bartlett kernel with (i.e., ). However, the proof given here is applicable to other kernels and different values of b. Note that with , the HAC estimator can be rewritten as (see Kiefer and Vogelsang (2002a) [2]) . With this HAC estimator, the term within the inverse in (24) is given by

where the limit is obtained directly from Lemma 3 and the continuous mapping theorem. The result for (24) can be obtained by using similar arguments as those used in Theorem 1 where we use the transformation: for a p.d. matrix satisfying .

References

- N.M. Kiefer, and T.J. Vogelsang. “A New Asymptotic Theory for Heteroskedasticity-Autocorrelation Robust Tests.” Econom. Theory 21 (2005): 1130–1164. [Google Scholar] [CrossRef]

- N.M. Kiefer, and T.J. Vogelsang. “Heteroskedasticity-autocorrelation robust standard errors using the Bartlett kernel without truncation.” Econometrica 70 (2002): 2093–2095. [Google Scholar] [CrossRef]

- N.M. Kiefer, and T.J. Vogelsang. “Heteroskedasticity-Autocorrelation Robust Testing Using Bandwidth Equal to Sample Size.” Econom. Theory 18 (2002): 1350–1366. [Google Scholar] [CrossRef]

- N. Hashimzade, and T.J. Vogelsang. “Fixed-b Asymptotic Approximation of the Sampling Behavior of Nonparametric Spectral Density Estimators.” J. Time Ser. Anal. 29 (2008): 142–162. [Google Scholar] [CrossRef]

- M. Jansson. “The Error Rejection Probability of Simple Autocorrelation Robust Tests.” Econometrica 72 (2004): 937–946. [Google Scholar] [CrossRef]

- Y. Sun, P.C.B. Phillips, and S. Jin. “Optimal Bandwidth Selection in Heteroskedasticity-Autocorrelation Robust Testing.” Econometrica 76 (2008): 175–194. [Google Scholar] [CrossRef]

- S. Gonçalves, and T.J. Vogelsang. “Block Bootstrap HAC Robust Tests: The Sophistication of the Naive Bootstrap.” Econom. Theory 27 (2011): 745–791. [Google Scholar] [CrossRef]

- Y. Sun. Fixed-Smoothing Asymptotics in a Two-Step GMM Framework. Working Paper; La Jolla, CA, USA: Department of Economics, University of California, San Diego, 2013. [Google Scholar]

- D.W.K. Andrews. “Tests for Parameter Instability and Structural Change with Unknown Change Point.” Econometrica 61 (1993): 821–856. [Google Scholar] [CrossRef]

- D.W.K. Andrews, and W. Ploberger. “Optimal Tests When a Nuisance Parameter is Present Only Under the Alternative.” Econometrica 62 (1994): 1383–1414. [Google Scholar] [CrossRef]

- J.S. Bai, and P. Perron. “Estimating and Testing Linear Models with Multiple Structural Breaks.” Econometrica 66 (1998): 47–78. [Google Scholar] [CrossRef]

- P. Perron. “Dealing with structural breaks.” Palgrave Handb. Econom. 1 (2006): 278–352. [Google Scholar]

- A. Banerjee, and G. Urga. “Modelling structural breaks, long memory and stock market volatility: An overview.” J. Econom. 129 (2005): 1–34. [Google Scholar] [CrossRef]

- A. Aue, and L. Horváth. “Structural breaks in time series.” J. Time Ser. Anal. 34 (2013): 1–16. [Google Scholar] [CrossRef]

- J. Bai, and P. Perron. “Computation and analysis of multiple structural change models.” J. Appl. Econom. 18 (2003): 1–22. [Google Scholar] [CrossRef]

- D.W.K. Andrews. “Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation.” Econometrica 59 (1991): 817–854. [Google Scholar] [CrossRef]

- J. Davidson. Stochastic Limit Theory. New York, NY, USA: Oxford University Press, 1994. [Google Scholar]

- P.C.B. Phillips, and S.N. Durlauf. “Multiple Regression with Integrated Processes.” Rev. Econom. Stud. 53 (1986): 473–496. [Google Scholar] [CrossRef]

- P.C.B. Phillips, and V. Solo. “Asymptotics for Linear Processes.” Ann. Stat. 20 (1992): 971–1001. [Google Scholar] [CrossRef]

- J.M. Wooldridge, and H. White. “Some invariance principles and central limit theorems for dependent heterogeneous processes.” Econom. Theory 4 (1988): 210–230. [Google Scholar] [CrossRef]

- R.M. DeJong, and J. Davidson. “Consistency of Kernel Estimators of Heteroskedastic and Autocorrelated Covariance Matrices.” Econometrica 68 (2000): 407–424. [Google Scholar]

- B.E. Hansen. “Consistent Covariance Matrix Estimation for Dependent Heterogenous Processes.” Econometrica 60 (1992): 967–972. [Google Scholar] [CrossRef]

- M. Jansson. “Consistent Covariance Estimation for Linear Processes.” Econom. Theory 18 (2002): 1449–1459. [Google Scholar] [CrossRef]

- W.K. Newey, and K.D. West. “A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix.” Econometrica 55 (1987): 703–708. [Google Scholar] [CrossRef]

- C.K. Cho. “Essays on Time Series Econometrics.” Ph.D. Thesis, Department of Economics, Michigan State University, East Lansing, MI, USA, 2014. [Google Scholar]

- D.W. Andrews. “Tests for parameter instability and structural change with unknown change point: A corrigendum.” Econometrica 71 (2003): 395–397. [Google Scholar] [CrossRef]

- C.K. Cho, and T.J. Vogelsang. Fixed-b Inference for Testing Structural Change in a Time Series Regression. Working Paper; East Lansing, MI, USA: Department of Economics, Michigan State University, 2014. [Google Scholar]

- C. Crainiceanu, and T.J. Vogelsang. “Non-monotonic Power for Tests of Mean Shift in a Time Series.” J. Stat. Comput. Simul. 77 (2007): 457–476. [Google Scholar] [CrossRef]

- J.R. Schott. Matrix Analysis for Statistics. New York, NY, USA: Wiley InterScience Publication, 1997. [Google Scholar]

- 1.We used the critical values provided in Andrews (2003) [26] for traditional inference.

- 2.The definitions for the mean and exponential statistics are slightly different in the divisor of the summation. For traditional inference, we adjusted the critical values in Andrews and Ploberger (1994) [10] to our definitions of the statistics.

- 3.For the case of a known break date, the 95% critical values for l = 2 are available for selected values of b and λ in Cho and Vogelsang (2014) [27]. The critical values display two main patterns. First, for each given λ the critical values increase as the bandwidth gets bigger. This can be expected given the well known downward bias induced into HAC estimators from estimation error. The fixed-b approximation captures this downward bias and reflects it through larger critical values. Second, for a given value of the bandwidth, the critical values display a V-shaped pattern as a function of As the break point moves closer to zero or one, the critical values increase and the minimum critical values occur at .

- 4.Cho and Vogelsang (2014) [27] also contains results for the known break date case along with a local power analysis.

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC-BY) license ( http://creativecommons.org/licenses/by/4.0/).