Abstract

This study estimates the effect of interest-free agriculture credit on the market participation and urban-rural linkages of rice growers in Pakistan. A survey was conducted to collect primary data using purposive and simple random sampling techniques from Punjab, Pakistan. This study applied the Instrument Variable (IV) approach and Ordinary Least Square (OLS) to evaluate the impact of interest-free credit on market participation and income. The results show a mixed influence of interest-free credit on rice growers’ market participation and urban-rural linkages. In general, the effect is negative when farmers obtained credit for six months. However, it shows a positive impact when farmers’ received credit for the next consecutive crop. Our findings suggest that the provision of interest-free credit for one year served a better purpose as it significantly attempted to alleviate budget constraints and endorsed farmers to increase land size under rice cultivation and improve productivity, market participation, and urban-rural linkages. The study provides three valid instruments and, therefore, a superior estimate of effect is achieved which can be leveraged to better support coherent agri-food policymaking.

1. Introduction

The progressive move towards market-oriented agriculture instigates a virtuous cycle helping leapfrog productivity and farmers’ income which, in turn, contribute to poverty reduction, food security, improved urban-rural linkages, and economic growth [1,2]. In this transformation, profit maximization drives input and production decisions and reinforces a vertical and well-integrated linkage between input and output markets [3]. Nonetheless, out of 575 million total farms worldwide, 475 million farms own less than 2-hectares of land and produce for auto-consumption [4,5]. Like other developing countries, the dominance of small farmers in Pakistan coupled with the failure of formal credit institutions affects smallholder farmers’ production decision(s), triggers disintegration between rural and urban markets, and widens the productivity, income, and food security gap [6,7]. Only 16% of smallholders obtain institutional credit in Pakistan, whereas 31% directly depend on commercial sector banks and microfinance lending institutions. Almost 71% of smallholder farmer’s depend on market intermediaries for credit, input and other operational services [8]. Although market intermediaries—village-level brokers, assemblers and local traders—are the financial powerhouse that offers credit services to overcome these snags, their role is often regarded as that of parasites [9,10]. These agents take advantage of their provided services, farmers’ low social status and weak bargaining power, and grab a significant share of benefits accrued from the sale of crops, leaving farmers to sell their produce in village-level unregulated markets at low price [11,12,13]. This further reduces the farmers’ commercialization scope and weakens the degree of integration between urban and rural markets [1]. Hence, most of the farmers get trapped in a vicious circle of poverty characterized, inter alia, by low productivity, on the one hand, and the existence of an oligopsony or monopsony type market structure, on the other hand, yielding low economic returns [3,14].

Agricultural credit is the fuel of broader agribusiness and boosts the farmers’ commercial activities through increased market participation in rural and urban-centered markets [15]. Limited access to agricultural financial services, including insurance, credit, and savings, tends to mar farmers’ commercial activities, income, and market participation [16,17,18]. Like other developing countries, due to credit constraints, the high cost of lending money and high credit dependence on market intermediaries, only 23% of the smallholder farmers sell their produce in regulated urban markets. Similarly, only 34% of rice farmers made their way to such output markets and obtained a fair price [8]. To usher broader commercial agriculture and economic trajectory and meet the agenda of financial inclusion and broader urban-rural integration, Pakistan has fostered institutional financial markets by launching an E-Credit scheme to provide interest-free agriculture credit [19]. Objectively, this scheme was initiated to protect smallholders and tenant farmers from informal money lenders’ exploitation, reduce the production cost, improve productivity, income, market participation, and outreach of digital and formal financial services. Thus, with such development objectives, total agricultural credit increased from Rupees 248,120 Million in 2010 to Rupees 704,448 Million in 2018. Under this scheme, 314,000 farmers amongst 149,271 rice growers in specialized production and export areas have been facilitated so far [8]. This scheme was implemented to improve financial capacity building and the commercial and entrepreneurial capabilities of farmers. Importantly, in the wake of enormous potential opportunities and economic benefits arising along with the China-Pakistan Economic Corridor (CPEC), the resulting improved regional integration might not be possible to achieve without a plausible agriculture credit policy [20,21]. However, considering many challenges, inter alia, there is a dire need to ’balance increasing productivity, farmers’ income, and commercialization to ensure sufficient food supply while reducing the exploitative nature of the credit market and informal money lenders.

Understanding the extent and drivers of the move towards smallholder commercialization has significant scope for coherent policymaking. Many studies show that agriculture credit provision affects farmers’ market participation and urban-rural linkages [22,23,24,25]. Mariyono [26] documents that agriculture credit participation fulfills the need for operating capital and enforces high-level agriculture commercialization. Contrary, recent evidence based on randomized designs reveals that microcredits fail to produce high-returns due to the high cost of lending [27,28,29], thereby resulting in a decline in smallholder farmers’ market participation and urban-rural integration. Linh et al. [27] reviewed previous literature on agriculture credit impact, and whilst positive results are common, they noted considerable variability within these results that should be treated with caution when overcoming econometric challenges. Likewise, Pham and Lensink [28] underpin that, in terms of access, formal and informal agriculture credit are entirely different, and thus imply that they are unrelated and independent in their impacts on the level of market participation. Indeed, existing studies provide inconclusive and inconsistent findings regarding the effect of agriculture credit on the level of market participation, mainly due to several variations: decision to borrow, institutional and non-institutional sources of agriculture credit, size of the amount, and the interest rate charged [27,28,29,30]. Further, no research has studied the impact of interest-free agriculture credit on smallholder market participation and urban-rural linkages in a developing country context. Yet it remains unanswered whether the provision of interest-free agriculture credit might work as a lever to 1) lower short-run credit constraints, 2) impact production decisions by employing more factors), particularly land, and 3) foster smallholder farmer’s market participation, both in the case of six-month loans or crop loans (short-term) and one-year loans, and urban-rural linkages. Moreover, studying the impact of interest-free agriculture credit, particularly in a developing country, is a new avenue for linking small farmers to urban food value chains that might be a promising tool for rural poverty alleviation. Policymakers also need to ensure ’value for money’ by going beyond the overall interventions’—interest-free credit—ripple effects and represent it as a worthy investment. Given these factors, estimating the impact of interest-free agriculture credit is prudent to ensure an unbiased outcome that robustly addresses the plethora of confounding factor(s), endogeneity, and self-selection bias, measurement error, and other related econometric challenges [31,32,33].

In a nutshell, investigating the effect of interest-free agriculture credit is a novel gauge that is important for many reasons: (a) a good policy lever to reduce imperfections in credit markets, (b) a robust instrument for changing cash-strapped farmers’ interest in employing factors of production adequately, when studying the transition from subsistence to commercialized systems, (c) distinguish between the level of market participation caused by formal (interest charged), informal and interest-free agriculture credit, and (d) envisioning a well-integrated vertical linkage between input and output markets, urban-rural integration, productivity, and income to avoid surplus production and, therefore, the burden of agriculture subsidies. In this regard, we used an Instrumental Variable (IV) approach to draw on positive goals. First, we examine the effect of interest-free agriculture credit on farmers’ level of market participation and urban-rural integration. Second, we establish and compare various indexes to explore the extent of market participation, market-orientation, agriculture commercialization, and integration into the cash economy. Lastly, we measure the impact of credit participation on productivity and farmers’ income.

The next section of the study is the conceptual framework. Section 3 represents detailed information on interventions, data, and empirical measures used. Section 4 reports results and discussion on these results. Subsequently, concluding remarks, limitations and future research directions are examined.

2. Conceptual Framework

Investing in agriculture, particularly among smallholders in developing countries, might be a plausible lever to foster urban-rural linkages, reduce rural poverty and reach sustainable development [14]. Timmer [34] endorses that investment in agriculture is a fundamental commercialization tool that ushers in productivity, rural transformation, and economic diversification. Investing in agriculture-based economies—like Pakistan’s, where most of the population (43%) relies on agriculture, increases productivity, gives access to market and modern food supply chains, and helps move towards market-oriented and/or commercial agriculture [35,36,37]. Further, investing in smallholder agriculture can encourage sustainability in the face of mounting environmental and food crises [38,39,40]. Therefore, there is a need to understand and design programs and interventions that recognize the heterogeneity of smallholder agriculture and shedding a significant impact on their market participation level is a matter of foremost concern [41]. Likewise, an alternative argument is poorly supported by research failing to explore smallholders’ capacities to engage in commercial activities [42], particularly when they are provided with interest-free operating capital.

Why is smallholders’ market participation vital for rural poverty reduction, urban-rural linkages and farmer’s welfare? We can trace the answer from rational choice theory. Generally, this theory offers a foundation to study individual farmers’ behavior in market participation decision making. This theory is based on the core principle of individual decision-making, where individuals face snags while making choices among market goods and services. In such situations, it provides insights on how individuals decide upon participation in interest-free agriculture credit to achieve or maximize utility, constrained by uncontrollable factors. The rational choice theory discourse states that the demand for agriculture credit generally involves several aspects: (1) the type and nature of credit services provided, (2) the need for financial services (i.e., credit, saving, insurance, etc.), and (3) the terms and conditions under which market intermediaries or financial institutions provide these services [43]. Thus, under given circumstances, i.e., the interest-free nature of credit, farmers are encouraged to participate in interest-free credit and, therefore, make choices to enhance areas under rice production to expand market participation in the presence of uncontrolled factors. Further, the interactions developed due to improved information sharing and market participation instigate larger-scale production and the adoption of dynamic technologies that improve productivity, farm income, urban-rural linkages and welfare of the rural communities [44,45]. Robustly, on the supply side, transaction cost theory provides the foundations for participation in interest-free agriculture credit. Transaction cost theory opines that smallholders would not be encouraged to participate in the market until the lending cost is kept to the lowest level [46]. Net welfare gains from market-oriented production are not just because of trade-off, but perhaps come more from the opportunities emerging from vertical integration and large-scale commercial production in the presence of sunk or nontrivial fixed cost of production [47].

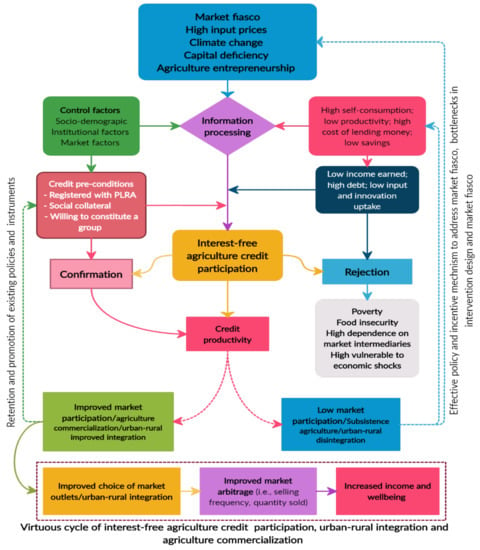

What does it take to break the trap or vicious cycle of auto-consumption and semi-subsistence agriculture poverty traps in a developing country like Pakistan? According to Barrett and Swallow [48], limited access to credit and poor physical infrastructure represent low-level equilibria. Given this, lack of credit and related incentives prompt auto-consumption and/or semi-consumption, characterized by, inter alia, poverty trap (low-level equilibrium), a rudimentary production, capital constraints, and modest market participation and urban-rural integration. Contrary, holding other factor(s) constant, interest-free agriculture credit might help achieve a virtuous cycle of agriculture commercialization (high-level equilibria) by increasing the area under rice production, technology use, productivity and income, and reducing the cost of production [49]. Thus, under given circumstances, farmers are encouraged to rationally make choices to achieve a higher income and welfare gains in the presence of uncontrolled factors (see Figure 1).

Figure 1.

Interest-free agriculture credit participation, urban-rural integration and agriculture commercialization.

3. Data and Estimation

3.1. Intervention Overview and Participation Criterion

The government of Punjab (GOP) has taken the initiative to promote smallholders’ market participation by providing easy and interest-free agriculture credit. For that purpose, interest-free loans are being provided through two commercial banks (National Bank of Pakistan, and Zarari Taraqiati Bank Limited) and three Micro Financial Institutions (MFIs) (National Rural Support Program, Telenor Micro Finance Bank, and Akhuwat Islamic Microfinance). The GOP provided a revolving fund of Rs. 2 billion to Akhuwat Islamic Microfinance (AIM), while other MFIs and commercial banks managed to arrange this from their own resources. Initially, GOP started this project for a selected 14 districts of Punjab. Akhuwat (https://akhuwat.org.pk/) is the leading institution for budgeting and financing interest-free credit. The GOP contributed a progressive share, increased over the years, into the Akhuwat interest-free fund, which relied on donations and charity from abroad and domestic donors. Within the past decade, Akhuwat has experienced a sevenfold increase in its interest-free credit portfolio with a credit recovery rate of 99.9%. The public sector audit department and Akhuwat administrative body conduct an annual audit of the various interest-free products offered by Akhuwat and submit this to the Chief Minister of Punjab. So far, Akhuwat is successfully operating in 14 selected, least developed Punjab province districts, but the government of Punjab is planning to extend its network throughout the province [50]. Under this scheme, during the fiscal year 2019–2020, Rs. 600 million have been allocated, and therefore interest-free loans worth Rs. 40,000 and Rs. 30,000 per acre are being provided for summer and winter crops, respectively. This program was initiated for smallholder farmers in the 14 least developed agricultural districts of the Punjab Province. A farmer holding agricultural land up to 12.5 acres is eligible for this program; however, the interest-free loan can be granted for up to five acres simultaneously. Further, this scheme has solved the long-standing problems of farmers’ land registration and 470,810 farmers have been registered with Punjab Land Record Authority (PLRA), so far [8]. This project has achieved unparalleled success in reducing the spate of poverty, empowering millions of the vulnerable through resource mobilization for several other initiatives and products aiming to promote inclusive growth [51].

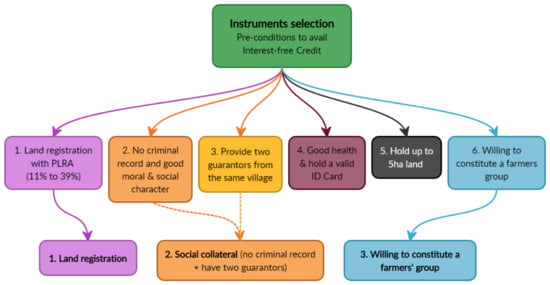

The GOP, in collaboration with lending partners, established essential parameters for the distribution of interest-free loans. Some of these critical eligibility criteria are as follows: (1) farmer must be registered with PLRA, (2) must provide social collateral, i.e., two personal guarantors from the same village, (3) farmer should have good moral and social character and not be convicted of any crime, (4) must be in good health and hold a valid citizen identification card, (5) own land up to five hectares, and (6) willing to constitute a group. Given these parameters, every farmer in every district has an equal probability of seeking interest-free credit subject to eligibility criteria. Upon success, the interest-free loan was granted in the corresponding village within one week of application through an easy process, having zero processing charges. Initially, the loan will be given for six months; however, it can be further granted for consecutive crops for another six months upon successful repayment.

3.2. Data Collection and Summary Statistics

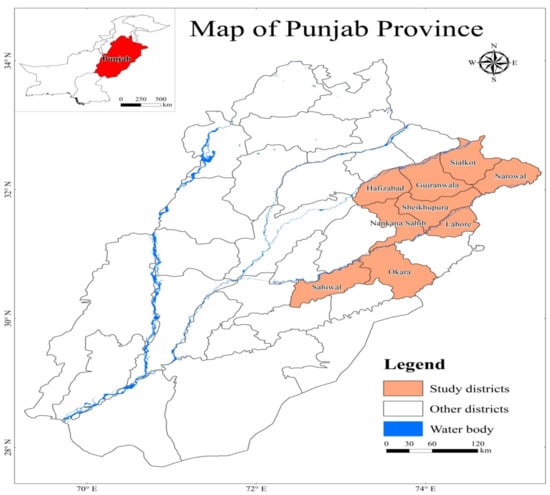

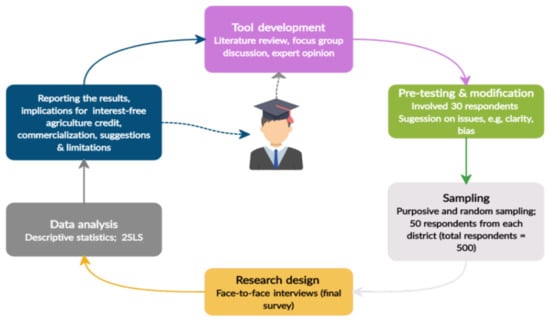

This study was conducted in Punjab, Pakistan. For this purpose, the tool was formulated based on a literature review and confirmed after pre-testing, focus group discussions, and expert opinion engaged in field research in a similar domain. The sample was purposively designed from nine rice-growing districts out of 36 total districts of Punjab province, Pakistan (see Figure 2). Most of the sampled districts fall in the Kalar tract—a specialized area for rice production and export. We used two-step procedures to reach the respondents: (1) random sampling technique was used to select five villages from every district, (2) purposive sampling technique was employed to collect information from five participants in interest-free credit from each village, whereas we used random sampling to select five non-participants from the same village. In total, we collected information from 10 respondents (5+5) via face-to-face interviews with farmers from each village using purposive and random sampling techniques to compile the initial data set comprising 650 respondents. We obtained the lists of participants in interest-free agriculture credit from the agriculture department, banks and Micro Finance Institutions (MFIs) to facilitate data collection and obtain appropriate information. Lastly, we cleaned the data set and removed the questionnaire with empty sections and missing key information, finalizing a data set consisting of 500 respondents for this study. Figure 3 represents the various stages of the research process through which this study was accomplished.

Figure 2.

Map of the study districts.

Figure 3.

Stages of the research process.

Detailed information on the study variables and covariates are represented in Table 1. This shows a lower quantity, averaging 14.32 mounds per acre, sold in a regulated market compared with the average mounds per acre rice yield (42.47). This represents that most of the small farmers sold their produce to rural assemblers or intermediaries. It indicates that 47% of respondents obtained interest-free credit for the latest rice crop, whereas the average income earned was rupees 32,185. Regarding the three treatments used, results illustrate 55% of respondents had social collateral, 61% of respondents were willing to constitute a farmers group, and 53% registered their land with PLRA. Further information on the exogenous variables and covariates is given in Table 1.

Table 1.

Data description and summary statistics.

3.3. Empirical Estimation

Informed by the above outlined conceptual framework, we followed a step-wise empirical estimation procedure to test the hypothesized objectives. First, we estimated the determinants of participation in interest-free agriculture credit. Second, we assessed the effect of interest-free agriculture credit on farmers’ market participation using two different outcome variables—farmers who received credit for the first time and those who successfully obtained credit for the next consecutive crop. Third, we calculated various market participation and commercialization indexes for non-participants and for those who participated in the first, the second, and more than two periods, to compare and to examine the degree of integration between urban-rural linkages: Market Participation Index (MPI), Marketability Index (MI), Market Orientation Index (MOI), Agriculture Commercialization Index (ACI), commercialization of rural economy, degree of integration into the cash economy, and vertical urban-rural integration of output (see Appendix A, Table A1). Finally, we estimated the impact of interest-free agriculture credit on productivity and farmers’ income. Based on the different type of outcome variables used in this study, we employed the following estimation techniques:

- Probit model for assessing the determinants of participation in interest-free agriculture credit.

- Two-Stage Least Square (2SLS) for estimating the effect of interest-free agriculture credit on farmers’ market participation and income.

- The ratio of various indexes for calculating: the extent of market participation, commercialization, and integration into the cash economy.

- Ordinary Least Squares (OLS) for estimating the impact of interest-free agriculture credit on smallholders’ productivity.

We undertook these estimations for various treatment variables, control variables, and outcome variables. In this study, we alternatively and collectively applied three treatment variables to measure the effect of interest-free agriculture credit on the level of farmers’ market participation. The first one is farmers’ registration with PLRA, one of the pre-conditions to obtain interest-free credit. Registered farmer(s), therefore, take advantage of interest-free agriculture credit. Nonetheless, land registration is a private good, as only 39% of the total farmers are registered with PLRA, which certainly creates a difference between participants and non-participants [8]. The second is social collateral. This indicates that a farmer can only be eligible to obtain interest-free credit if he/she has not been convicted of any criminal offense and has two guarantors who pledge against timely repayment of the received principal amount. Hence, using social collateral as a criterion for participation in credit provides a coherent justification as it also shows the personal (private) character of a farmer which distinguishes participants from others. Likewise, we choose willingness to constitute a group as the third treatment for credit participation. Group participation is one of the fundamental elements in eligibility criteria, which aims explicitly to establish rural cooperatives, promoting collective actions that reduce the cost of production through bridging market participation and inclusive growth. McKenzie and Rapoport [52] report that network or group effect is essential when one’s use of a product affects its usage for others, and thus group membership is meant to capture the impact of such groups in the study area. Figure 4 represents the information on credit participation pre-conditions.

Figure 4.

Credit participation pre-conditions and instrument(s) selection.

We included covariates (control variables) in all models to better control heterogeneity, endogeneity and improve IVs’ strength. Table 1 illustrates the information on control, treatment, and outcome variables (see Table 1). Most of the variables given in Table 1 are taken as controls, except outcome variables. We included farmer personal characteristics, age, advisory participation, and literacy status to control for heterogeneity in farmer skills. We included market access factors such as distance from the all-weather road, distance from market, ownership of logistics, and smartphone ownership to control for heterogeneity in farmers’ access to the market. Likewise, we included the size of total cultivated land to control heterogeneity in the total production quantity that might affect farmers’ market participation. Further, livestock ownership, tenancy status, tube well ownership, and the number of floods were incorporated to control heterogeneity in credit demand. Other explanatory variables were included based on the need and nature of dependent variables.

3.3.1. Endogeneity Tests

Participation in interest-free agriculture credit by itself is an endogenous variable that might depend on the farmers’ characteristics and, therefore, could be correlated with the dependent variable’s error term. To ensure the validity of estimates, we used the two-stage procedure suggested by Wooldridge [53]. First, we estimated a probit model in which participation in interest-free agriculture credit is a function of two types of independent variables: covariates and instruments. Thus, we included both to satisfy the orthogonality condition of IVs. Finding a robust instrument is challenging; we chose three IVs, which we think are appropriate and strongly affect participation in interest-free agriculture credit but have no direct connection with the outcome variable (market participation). Given the prerequisite, validity, relevance, and statistical robustness, we have confidence that the chosen instruments are amply effective in combating econometric challenges. These are as follows: (1) land registration, (2) willingness to constitute a farmers’ group, and (3) social collateral. This refines the sample and helps undertake a robust estimation which otherwise might cause endogeneity [54]. In the second-stage estimate, we used these variables as treatments for participation in interest-free agriculture credit. Further, we run various tests, Durban chi-square, Wu-Hausman, first-stage regression statistics, Sargan chi-square, and Basmann to estimate endogeneity, the robustness of used instruments, and over-identification restrictions, respectively. Therefore, in the absence of endogeneity and self-selection bias, we performed our 2SLS estimations inflating the asymptotic variance of the used estimators [55].

3.3.2. Reliability Analysis

To test the study scales’ reliability and degree of consistency, Cronbach’s Alpha (CA) was used to confirm the data after repeated traits. The estimated CA coefficient ensures the tool’s reliability and internal consistency for the 25 items used in this study (see Table 2). According to Santos [56], a CA value equal to 0.75 or above is considered an acceptable reliability level. Since the CA indicates a good fit for the item used, it justifies further analysis and discussion.

Table 2.

Cronbach’s Alpha Reliability Test.

4. Results and Discussion

Given the presumption that OLS might lead to biased estimates, we ran OLS in addition to IV models to illustrate the difference between both estimations to address the endogeneity concerns. Next, the three IVs were inserted individually and collectively for first and second-time participation to monitor their effects on market participation and subsequent diagnostic checks. Thus, in total, six models were estimated: one using OLS, and five 2SLS, using individually and collectively three IVs for both models, respectively. Furthermore, the results based on calculated market participation and commercialization (urban-rural integration) indexes are presented. Finally, the impact of credit participation on productivity and farmers’ income is estimated.

4.1. First Stage Results

Based on the preceding debate, we ran a probit function (first-stage of IV process) estimating the determinants of participation in interest-free agriculture credit, presented in Table 2. Most of the covariates and IVs included showing the expected sign. Age and literacy have a significant effect on participation in interest-free credit. As expected, literate and young farmers are more inclined to seek progressive opportunities than illiterate and old farmers, and thus have a greater probability of participating in interest-free credit. Livestock heads as a source of farmers’ immediate wealth were found to have a negative effect on credit participation. This indicates that better-off farmers do not tend to participate in interest-free credit. Interestingly, distance from all-weather roads as an indicator of market access shows a negative effect on interest-free credit participation. This justifies that under-development in the area creates substantial transportation costs, which hinders farmers from engaging in progressive opportunities aimed at broader agriculture commercialization. Fortunately, all of the three chosen IVs that are also among the pre-conditions of participation, the willingness to constitute a group, land registration with PLRA, and social collateral, also show a significant positive effect on participation in interest-free agriculture credit. This clarifies that farmers with entrepreneurial mindsets who prefer collaborations and are more concerned about land property rights and public sector initiatives have a higher possibility of participating in interest-free credit than those who pay no heed to policy change and remain wrapped up in the social evils which frequently occur in rural districts. Furthermore, the diagnostic check results confirm endogeneity using OLS and, therefore, endorse the validity of instruments applied using 2SLS (see Table 3).

Table 3.

Determinants of interest-free agriculture credit participation in rural Punjab.

4.2. Second Stage Results

The second-stage involves inserting the chosen valid and statistically appropriate treatment of the endogenous regressor into the main structural model, both individually and collectively, and applying them to the outcome variable. Accordingly, Table 4 represents the results of IV estimates for the key variable of interest, credit participation, with diagnostic statistics for clarity, including other covariates, available in Appendix A, Table A2, Table A3 and Table A4. Further, the results of the OLS estimation are also presented for comparison.

Table 4.

Parameter estimates for farmers’ market participation and diagnostic checks.

The OLS estimates show a consistent negative effect of first-period credit participation on farmers’ market participation. It indicates four mounds per acre decrease in rice crop output sold in the market, ceteris paribus. This estimation suffers the endogeneity problem as the coefficients of IV models predict more consistent estimates. The results of selected diagnostic statistics also validate the need for IV models. It shows 16 mounds per acre decrease in market participation when collectively applying the three IVs. However, it indicates a consistent but fairly slight decrease when applying the individual IV. This reflects that provision of a crop loan only for six months tends to decrease market participation. There might be several reasons for this decrease. First, credit is being granted before crop cultivation (meeting running expenses, i.e., purchase of inputs, land preparation, and buying other crop inputs) and, therefore, farmers must need to return it at the crop harvest or sometimes before. Second, during the focus group discussion, several farmers’ claimed that lending for such a meager period worsens their plight and further increases their engagement with village-level stakeholders, i.e., local dealers and traders. Third, farmers also highlight that while providing social collateral, usually they were asked to provide two guarantors from influential village families or their immediate family members and, therefore, while being pledged on the farmers’ behalf, they started visiting farmers one or two months ahead of the deadline which, in turn, put greater pressure on them. Indeed, at the time of crop harvest, due to surplus rice production in the country, prices are usually at their lowest level, leaving them to lend from market intermediaries to meet pledged repayment before the deadline. Accordingly, this forced them into a cash-strapped dilemma which initiates a debt cycle where farmers seek credit to repay previously due loans. These findings are in line with Hung et al. [57], Kirimi [58], and Arinloye [59]. Further, these findings complement Feder’s [60] arguments indicating the divergent role of short-term credit. Hence, it suggests that ’crop credit’ is often utilized to pay over-due farm credit and consumption and fails to transform from subsistence to commercialized agriculture systems.

Contrary, results based on consecutive second-period credit participation (interaction second period) show a positive connection between interest-free credit and market participation (see Table 4). Approximately, it indicates 25 mounds per acre increase in rice output sold in the market. It reinstates that provision of interest-free credit for another consecutive period increases farmers’ ability to store their rice produce for a period until they find fair market prices and sell in markets rather than the village and to local stakeholders at lower prices. Further, inter alia, interest-free capital reduced production cost by enabling cash payments, decreased farmers’ reliance on local stakeholders for credit and crop inputs, and thus got rid of the integrated and spillover effect improved market participation. Interestingly, most of the covariates represent significant effects, but credit participation introduces the largest impact on market participation (see Appendix A, Table A2, Table A3 and Table A4). This suggests that the form of the lending institution, interest-free nature, and relaxation in the repayment period reflect farmers’ market participation. Similar findings have been noted by prior studies [22,23,24,28,29].

4.3. Extent of Commercialization and Urban-Rural Integration

The extent of market participation and agriculture commercialization is a distinctive measure when dealing with the sampled households, consisting of auto-consumer and semi-commercial households [61]. We followed the presumption that the provision of interest-free credit might be a phenomenal lever to change production decisions among smallholders and could create a differential change between participants and non-participants, notably, in terms of increased agriculture commercialization and vertical urban-rural integration. For the purpose, we calculated indexes as follows: (1) market participation index, (2) marketability index, (3) market orientation index, (4) agriculture commercialization index of input, (5) agriculture commercialization index of output, (6) commercialization of rural economy, (7) degree of integration into the cash economy, (8) vertical urban-rural integration of input, (9) and vertical urban-rural integration of output. The value of these indexes varies between 0 and 1. However, a value equal or slightly above 0.50 indicates that a household has escaped from auto-consumption and entered into semi-commercialization, whereas a value close to 1 shows a high extent of commercialization and urban-rural vertical linkage. These indexes help indicate the difference in non-participants, first-period participants, second period, and above two-period participants [62,63], as illustrated in Table 5.

Table 5.

The extent of market participation and commercialization—urban-rural integration.

First, we calculated the market participation index for all the designated categories herein. This is the ratio of the value of rice products sold in the market and the total value of rice products produced at the average market price. Results indicate that the provision of interest-free credit for only one period decreased rice crop market participation. However, it shows a significant improvement in market participation for farmers who secured credit for consecutive next crop and/or above two periods. This reinforces our empirical results and implies that credit provision for a very short period (six months) adds to farmers’ plight. This protects smallholder entry into commercialized agriculture from auto-consumption or subsistence systems. In fact, farmers having secured credit for the immediate next crop have a greater possibility of waiting for stability in market prices for rice and make no hurry to sell their produce at the time of harvest. Hence, they do not feel any immediate credit liability and participate in the market rather than selling their produce to rural stakeholders. Thus, the provision of credit for one year serves a better function in improving rice crop market participation in Pakistan. Next, we examined farmers’ marketability index. This refers to the ratio of the total value of all crops sold in the market and the total value of quantity produced at the average market price. Results show that both non-participants and one period credit participants fall into auto-consumption or subsistence agriculture; therefore, credit for only one crop fails to meet the proposed agenda. Conversely, second and above two times participation shows a substantial improvement in farmers’ marketability extent, bringing them into a high level of agriculture commercialization from subsistence agriculture. This clarifies that the provision of interest-free credit provides synergies, helping bridge resource constraints that, in turn, improve productivity, production, and market participation.

Once the marketability index was calculated, the market orientation index in land allocation was computed. This states the weighted ratio of the farmer’s land allocation pattern by the crop’s marketability index. Results reinstate no difference in non-participants and six-month credit participants, despite being involved in subsistence agriculture systems. However, it indicates a high extent of market orientation among consecutive second and above two-time credit participants. This reflects that having secured credit for another consecutive term allows farmers’ to better respond to the market signals and allocate more land to marketable commodities. Specifically, under auto-consumption and semi-commercialized agriculture systems, resource allocation (land, labor, and capital) and production decision making play a conclusive role. Thus, the provision of interest-free running capital plays fuels resource transformation and allows farmers to allocate more land to commercial crops. This implies that the provision of interest-free credit for one year or above substantially improves market orientation. Subsequently, commercialization of input for rice was computed. This reports the ratio of the total value of inputs purchased from the market and the total value of rice crop produce. Computations illustrate a significant difference between first period participants and non-participants—where non-participants either highly depend on rural input providers or use little input while operating under subsistence agriculture systems (see Table 4). Similarly, results justify the notable impact of the second and above two periods’ credit participation on the commercialization of rice crop input. This implies that credit participation raises commercialization interests and allows farmers’ to move towards markets rather than being dependent on rural stakeholders and/or create improved demand for crop inputs as farmers shift from subsistence to commercialized agriculture.

The output commercialization index for rice was computed; this is the ratio of the total rice output value sold in the market and the total rice crop produce value. Results highlight that both non-participants and first period participants tend to show similar lower engagements in output commercialization. This indicates the vast prevalence of auto-consumption or subsistence agriculture systems where either the household consumes most of the rice production or sells a meager portion in the market. Conversely, results show a higher degree of rice output commercialization for farmers who participated for the second or above two periods. This finding complements the 2SLS results and develops a line of argument that credit provision for only a six month period further decreases output market participation. It implies that such an intervention fails to meet its purpose, whereas relaxation in repayment time would offer a substantial improvement in agriculture’s commercialization. Afterward, the extent of the commercialization of the rural economy was estimated. It examines the total value of agricultural products and services—including the value of in-kind payments—attained through market transactions in relation to the total agriculture income. Results disclose a significant difference between non-participants and first period participants—complementing the relevance of interest-free credit in transforming the rural economy. Likewise, the provision of credit for a consecutive second period or above two periods offers a comparatively high extent of rural commercialization.

Finally, the degree of integration into the cash economy was computed. This refers to the ratio of the total value of agricultural products and services attained through cash transactions to the total agriculture income. Computations clarify the notable effect of first-period credit participation on the degree of integration into the cash economy. Put simply, the provision of credit enables farmers to deal in cash payments and, therefore, protects them from lending crop inputs on credit which often turns costly. It implies that putting money into farmers’ pockets might work as a foremost gauge to integrate rural areas into the cash economy. Further, results for second and above two-period credit participation reinforce that, the greater the relaxation in the repayment period, the greater the degree of integration into the cash economy. Lastly, we examined vertical urban-rural integration of input and output. The results indicate that second and above two-period credit participation serves a better function in fostering better urban-rural vertical linkage. From these findings, we see that market intermediaries often act like parasites [11], forcing farmers into cash-strapped auto-consumption or/and semi-commercialized systems, which weakens urban-rural vertical linkages, bolstering their vulnerabilities to poverty and food insecurity.

4.4. Credit Participation, Income and Productivity

While most of the prior literature identifies a positive impact of credit on income, the IV approach presented in this study develops a valid estimation that comprehensively addresses endogeneity concerns. First, we ran OLS to examine the impact of credit participation, followed by IV estimated and diagnostic statistics. Further, we repeat a similar practice for assessing the impact of credit participation on rice productivity. Accordingly, Table 6 represents the results of IV and OLS estimates for variable interest (credit participation) with diagnostics statistics for clarity. However, including covariates and independent variables are available in Appendix A, Table A5, Table A6 and Table A7.

Table 6.

Parameter estimates for farmers’ income and diagnostic checks.

The OLS estimate shows a consistent negative effect of first-time credit participation on farmers’ income. It indicates a 0.131 units decrease in farmers’ income, ceteris paribus. This estimation suffers the endogeneity problem as the coefficients of IV models predict more consistent estimates. The results of selected diagnostic statistics also validate the need for IV estimation. It shows a 0.175 units decrease in farmers’ income when collectively applying the three IVs. This reflects that the provision of a crop loan—only for six months-tends to reduce farmers’ income. The potential causes might be as follows: (1) the amount obtained per acre credit might not be sufficient to cover the cost of production and other running expenses, (2) strict and less repayment time, and (3) the greater influence of social collateral. Consequently, inter alia, cash-strapping hinders escape from auto-consumption and/subsistence systems. Thus, these systems add to farmers’ plight, leaving them to borrow from market intermediaries to meet their credit needs and remaining trapped in a vicious cycle of poverty. These findings are amply supported by the prior literature [3,8,10,61].

Conversely, results based on consecutive second-period credit participation (interaction second period) show its positive impact on farmers’ income (see Table 4). It indicates a 0.588 units decrease in farmers’ income. This reinforces that the provision of interest-free credit for another consecutive period improves storage and marketing decision-making, which increases income. Among other advantages, interest-free running capital reduced the cost of production and enhanced economic independence, allowing them to choose between profitable, cost-effective and reliable channels that spur vertical integration between farms and markets. This implies that the provision of interest-free credit for one year serves a better function in integrating farmer-market linkage that might be translated into improved farm income. Similar findings have been reported by prior studies [64,65,66,67]. Lastly, we examined the impact of interest-free credit participation on rice crop productivity. Diagnostic statistics justify estimation using OLS as no endogeneity was detected. Results indicate a positive impact of credit participation on productivity. Approximately, it shows a 13 mounds per acre increase in crop productivity with credit participation. This implies that credit provision helps duly meet crop financial requirements for key inputs and ensures proper application of improved seeds, mechanization, fertilizers, and, subsequently, increased productivity. These findings are amply supported by prior literature [65,68,69,70].

Smallholder farmer(s) received different prices for similar rice variety in the studied region. Table 7 presents the rice prices received by non-participants, first-period participants, and second-period participants. Further, it illustrates the average annual prices for rice in the sampled districts and compares the smallholders’ prices. These variations might be attributed to the participation in interest-free credit. We disaggregated the mean prices for three categories of the sampled smallholders to estimate how credit participation helps obtain higher prices for different crops. The results indicate that the second-period participants received relatively higher prices for rice, obtaining 8.5% higher than non-participants and 7.6% higher than first-period participants. Comparatively, first-period participants received per mound higher price (rupees 27 or USD 0.18) than non-participants and lower than second-period participants (rupees 190 or USD 1.23). Put simply, in terms of profit, second-period participants with an average market participation rate of 14.32 mounds (see Table 1) obtained 3,104 rupees (USD 20) per acre. Likewise, with the average area under rice production of 4.67 acres in this study (see Table 1), second-period participants received an additional 14,495 rupees (USD 93) than non-participants. This implies that second-period credit participation substantially improves smallholder farmers’ income and, therefore, improved income enhances their credit repayment capacity and future participation in such programs. Hence, the interest-free nature of agriculture credit encourages smallholder farmers’ to participate in programs aimed at broader agriculture commercialization and improved urban-rural linkages. Contrary, it is also evident from results that there is a meager per acre average difference (rupees 386 or USD 2.5) between prices received by non-participants and first-period participants. In case of short-term credit repayment, the farmer would not be encouraged to participate in agriculture commercialization. Therefore, it suggests that second-period credit participation substantially improved income earned (rupees 3.104 or USD 20 per acre) from market participation and further encourages farmers’ credit participation.

Table 7.

Variation in producer prices among smallholders.

5. Conclusions

Credit is fuel in agriculture production systems. It allows farmers’ to meet the cash need induced by the agriculture production cycle which characterizes land preparation, planting, cultivating, managing and harvesting the crop, which is usually done over a lean/slack period of several months. In developing countries, formal institutions have largely failed to satisfy farmers’ credit needs, which extend local traders’ or intermediaries’ opportunistic role and leave farmers to operate in auto-consumption systems. Thus, this deteriorates urban-rural vertical linkages in terms of the food supply. Further, these agents take advantage of farmers’ weak bargaining power and low social status and grab a significant share of benefits accrued from the sale of crops, leaving farmers to sell their produce to them in the village at low prices. Hence, most smallholders become cash-strapped which further instigates a vicious cycle of poverty characterized, inter alia, by low productivity, on the one hand, and the existence of oligopsony or a monopsony type market structure, on the other hand, yielding low economic returns. Given this, we studied the effect of interest-free agriculture credit on market participation and urban-rural integration for first and second-period credit participants using the IV approach.

The results show a mixed impact of interest-free credit on the market participation of rice growers. In general, the effect is negative on market participation and income when farmers obtained credit for six months, forcing farmers into cash-strapped, auto-consumption and/or semi-commercialized systems. However, it shows a positive impact when farmers’ received credit for the next consecutive crop altogether. The provision of interest-free credit for one year serves a better function as it significantly improved land size under rice production, market participation, income, and productivity. Further, computed indexes complement these empirical results, indicating a positive impact on the extent of commercialization and urban-rural vertical linkages. The study is relatively novel in several aspects: the effect of interest-free credit on market participation and urban-rural vertical linkages is rarely undertaken in the prior literature; the subjects being non-participants, first, and second-period participant smallholders. Rice growers were chosen through a systematic approach, thus making the study findings highly relevant for coherent policymaking. Further, this study comprehensively addresses endogeneity concerns and presents the three valid IVs, land registration, willingness to constitute a farmers’ group, and social collateral, which can be further applied using the criterion developed herein. Likewise, the estimates applying these IVs—individually and collectively—unanimously show the higher effect of credit participation than OLS estimates; thus, the results presented are superior estimates of the impact of credit on market participation. Moreover, the study also contains findings for the farmers: (1) participation in and strengthening of the role of the agriculture cooperative would be an alternative strategy to boost smallholder agriculture transformation from subsistence to commercial agriculture, (2) ensuring first-period credit retirement would enhance second-period credit participation which, in turn, would substantially improve productivity and income and instigate a virtuous cycle of agriculture commercialization, and (3) improved agriculture commercialization fosters market arbitrage and, therefore, enhances information flow within the farming community through already established agriculture cooperatives.

In terms of policy implications, the study suggests the positive effect of one-year interest-free credit on smallholder decisions by alleviating the credit constraints and increasing area under rice cultivation which, in turn, increased the probability of market participation, commercialization, urban-rural vertical integration and farmers’ income. Likewise, the development of agriculture cooperatives, a by-product of interest-free credit, would offer lasting benefits for farmers and rural communities. Further, improved smallholder farmers’ resilience, social status, bargaining power, and income, can shed substantial impact(s) on agriculture production systems, urban-rural food supply chains and the wellbeing of both rural and urban communities. Moreover, these findings complement the notion in the prior literature that the provision of short-term credit (crop loans) forces farmers to become cash-strapped that, in turn, keeps them trapped in a vicious cycle of poverty and subsistence-oriented agriculture systems. Thus, relaxation in repayment time is suggested to encourage the increased transformation into commercial agriculture and ensure ’value for money’ by increasing the overall intervention ripple effect on a smallholders’ wellbeing, broader agribusiness trajectory, and vertical urban-rural integration, and economic growth. Further, policymakers must consider a more targeted approach that incentivizes the purchase of farm machinery for market participants, i.e., smallholders having a good credit retirement record, and contributes to interest-free credit funds. However, this requires policymakers to further identify the effect of different levels of market engagement. Nonetheless, policy actions set for agriculture commercialization should be adequately supported by a dynamic and effective credit service.

The study provides three valid instruments and robust estimation of interest-free credit on market participation and income. However, several caveats need to be considered when applying an IV approach, and future studies are needed to complement the findings of this study. First, the appropriateness and validity of an instrument is key when applying the IV approach. Although we are quite sure of the suitability of the applied instruments and, therefore, diagnostic statistics commend their validity, it is logical to admit that some other instruments could be applied. Second, the sample size used consists of smallholder farmers which, nevertheless, provides sound justification for the developed models herein. However, categorizing farmers’ into extra-small, small, medium and large scales would offer additional support to the estimation and help explore the extent of market participation, varying with the degree of farm size and resource endowments. Third, the study’s findings provide a foundation to build upon the unbiased and robust IV approach, therefore, ensuring the policymakers’ objective that ’value for public money’ is met, requiring further step-wise evaluations. Therefore, future research studies could investigate and compare the productivity, effectiveness, and impact of various credit forms, i.e., institutional, non-institutional, and interest-free on smallholders. Lastly, this research studied the particular context of interest-free agriculture credit in the least developed Punjab, Pakistan districts, where interest-free credit participation is subjected to some pre-conditions. Therefore, research findings are generalizable for developing countries with a similar context.

Author Contributions

A.S. and G.L. conceived and designed the study; A.S. and S.M. collected the data; H.A. analyzed the data; A.S., S.M., H.A., and G.L. wrote the first draft paper; H.A. contributed to revising the paper and adjusted the framing of the first draft and enriched it to the final draft for submission. All authors have read and agreed to the published version of the manuscript.

Funding

This research was sponsored by the National Natural Science Foundation of China (Projects ID: 71573135; 72073070), and the Priority Academic Program Development (PAPD) of Jiangsu Higher Education Institutions, China.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data sharing not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Indexes used and their computations.

Table A1.

Indexes used and their computations.

| Indexes | Calculations |

|---|---|

| Market participation index | Where Pj is the average price received, Sij denotes ith crop sold at market, and QJi represents the quantity sold |

| Market ability index | Where Sij is ith crop sold at market, and QJi represents quantity sold ith crop sold |

| Market orientation index | Where represents marketability index, LiJ indicate land allocation under rice in current year, and LJi denotes previous year land allocation under rice cultivation |

| Agriculture commercialization index of input | |

| Agriculture commercialization index of output | |

| Commercialization of rural economy | |

| Degree of integration into the cash economy |

Table A2.

Full table of IV estimate of first-period credit and market participation.

Table A2.

Full table of IV estimate of first-period credit and market participation.

| Qty Sold in Market | Coefficient | Standard Error |

|---|---|---|

| Credit Participation | −17.47 ** | 7.427 |

| Age | −0.078 | 0.139 |

| Literacy | 1.767 | 3.343 |

| Tube well | −4.904 * | 3.061 |

| Advisory service | 2.231 | 3.195 |

| Livestock heads | −1.198 * | 0.744 |

| Cultivated land size | 0.546 | 0.508 |

| Farm logistic | 12.07 *** | 4.685 |

| Market distance | −0.46 * | 0.217 |

| Distance from all-weather road | −1.26 * | 0.786 |

| Floods | −0.744 | 0.575 |

| Tenant | −4.365 | 8.001 |

| Own a mobile phone | 15.061 * | 8.086 |

| Constant | 53.946 *** | 13.531 |

Note: *** p < 0.01, ** p < 0.05, * p < 0.1.

Table A3.

Full table of IV estimate of first-period credit and market participation.

Table A3.

Full table of IV estimate of first-period credit and market participation.

| Qty Sold in Market | Coefficient | Standard Error |

|---|---|---|

| Credit Participation | −15.77 ** | 7.088 |

| Age | −0.076 | 0.138 |

| Literacy | 1.771 | 3.326 |

| Tube well | −4.861 * | 2.78 |

| Advisory service | 2.266 | 3.178 |

| Livestock heads | −1.178 * | 0.68 |

| Cultivated land size | 0.533 | 0.505 |

| Farm logistic | 11.954 ** | 4.658 |

| Market distance | −0.459 * | 0.265 |

| Distance from all-weather road | −1.24 * | 0.701 |

| Floods | −0.746 | 0.572 |

| Tenant | −3.963 | 7.944 |

| Own a mobile phone | 14.599 * | 8.024 |

| Constant | 52.841 *** | 13.393 |

Note: Instrument variable: ‘Interest-free credit = Willingness to constitute a group’. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table A4.

Full table of IV estimate of first-period credit and market participation.

Table A4.

Full table of IV estimate of first-period credit and market participation.

| Qty Sold in Market | Coefficient | Standard Error |

|---|---|---|

| Credit Participation | −19.468 ** | 7.689 |

| Age | −0.08 | 0.14 |

| Literacy | 1.763 | 3.366 |

| Tube well | −4.955 * | 3.082 |

| Advisory service | 2.189 | 3.217 |

| Livestock heads | −1.222 * | 0.75 |

| Cultivated land size | 0.56 | 0.512 |

| Farm logistic | 12.206 *** | 4.719 |

| Market distance | −0.461 * | 0.259 |

| Distance from all-weather road | −1.283 * | 0.792 |

| Floods | −0.743 | 0.579 |

| Tenant | −4.838 | 8.068 |

| Own a mobile phone | 15.603 ** | 8.156 |

| Constant | 55.246 *** | 13.674 |

Note: Instrument variable: ‘Interest-free credit = Social collateral’. *** p < 0.01, ** p < 0.05, * p < 0.1.

Table A5.

Full table of Ordinary Least Square (OLS) estimate of first-period credit and market participation.

Table A5.

Full table of Ordinary Least Square (OLS) estimate of first-period credit and market participation.

| Income | Coefficient | Standard Error |

|---|---|---|

| Interest-free credit | −0.131 * | 0.892 |

| Age | 0.003 | 0.004 |

| Literacy | 0.277 *** | 0.088 |

| Tube well | 0.051 * | 0.081 |

| Group membership | 0.137 * | 0.084 |

| Lending turn | 0.054 *** | 0.019 |

| Cultivated land size | 0.029 ** | 0.012 |

| Market participation index | 0.003 ** | 0.001 |

| Market distance | −0.003 | 0.008 |

| Mark visits | 0.039 ** | 0.015 |

| Tenant | −0.029 | 0.198 |

| Farm logistics | 0.251 * | 0.137 |

| Distance from all-weather road | −0.009 | 0.021 |

| Own mobile phone | 0.134 | 0.199 |

| Village-level credit penetration | 0.001 | 0.006 |

| Constant | 3.596 *** | 0.342 |

Note: *** p < 0.01, ** p < 0.05, * p < 0.1.

Table A6.

Full table of IV estimate of second-period credit and market participation.

Table A6.

Full table of IV estimate of second-period credit and market participation.

| Qty Sold in Market | Coefficient | Standard Error |

|---|---|---|

| Credit Participation | 26.297 ** | 12.127 |

| Age | −0.144 | 0.147 |

| Literacy | 3.011 | 3.457 |

| Tube well | −6.148 | 3.214 |

| Advisory service | 2.403 | 3.258 |

| Livestock heads | −0.989 | 0.754 |

| Cultivated land size | 0.432 | 0.515 |

| Farm logistic | 12.956 | 4.849 |

| Market distance | 0.38 | 0.304 |

| Distance from all-weather road | −1.304 * | 0.805 |

| Floods | −0.673 | 0.588 |

| Tenant | −5.126 | 8.281 |

| Own a mobile phone | 17.011 ** | 8.568 |

| Constant | 64.012 *** | 16.25 |

Note: Instrument variable: ‘interest-free credit = Land registration + Willingness to constitute a group + Social collateral’ *** p < 0.01, ** p < 0.05, * p <0.1.

Table A7.

Full table of OLS estimate of second-period credit and market participation.

Table A7.

Full table of OLS estimate of second-period credit and market participation.

| Qty Sold in Market | Coefficient | Standard Error |

|---|---|---|

| Credit Participation | 29.049 ** | 12.766 |

| Age | −0.153 | 0.149 |

| Literacy | −3.137 | 3.505 |

| Tube well | −6.325 ** | 3.262 |

| Advisory service | 2.383 | 3.30 |

| Livestock heads | −0.989 | 0.764 |

| Cultivated land size | 0.433 | 0.522 |

| Farm logistic | −13.173 *** | 4.919 |

| Market distance | 0.373 | 0.309 |

| Distance from all-weather road | −1.331 * | 0.816 |

| Floods | −0.664 | 0.596 |

| Tenant | −5.638 | 8.412 |

| Own a mobile phone | 17.712 ** | 8.723 |

| Constant | 66.254 *** | 16.701 |

Note: Instrument variable: ‘interest-free credit = Land registration’. *** p < 0.01, ** p < 0.05, * p < 0.1.

References

- World Bank. World Development Report 2008: Agriculture for Development; No. E14 231; World Bank: Washington, DC, USA, 2008; Available online: https://openknowledge.worldbank.org/handle/10986/5990 (accessed on 7 September 2020).

- Barrett, C.B. Smallholder market participation: Concepts and evidence from eastern and southern Africa. Food Policy 2008, 33, 299–317. [Google Scholar] [CrossRef]

- Olwande, J.; Smale, M.; Mathenge, M.K.; Place, F.; Mithöfer, D. Agricultural marketing by smallholders in Kenya: A comparison of maize, kale and dairy. Food Policy 2015, 52, 22–32. [Google Scholar] [CrossRef]

- Lowder, S.K.; Skoet, J.; Singh, S. What Do We Really Know about the Number and Distribution of Farms and Family Farms in the World? Background paper for The State of Food and Agriculture; Food and Agriculture Organization of the United Nations (FAO): Roma, Italy, 2014; Available online: http://www.fao.org/3/a-i3729e.pdf (accessed on 7 September 2020).

- Thapa, G.; Gaiha, R. Smallholder farming in Asia and the Pacific: Challenges and opportunities. In Proceedings of the International Conference on Dynamics of Rural Transformation in Emerging Economies, New Delhi, India, 14–16 April 2010. [Google Scholar]

- Ahmed, U.I.; Ying, L.; Bashir, M.K.; Abid, M.; Elahi, E.; Iqbal, M.A. Access to output market by small farmers: The case of Punjab, Pakistan. J. Anim. Plant Sci. 2016, 26, 787–793. [Google Scholar]

- Chandio, A.A.; Jiang, Y.; Wei, F.; Guangshun, X. Effects of agricultural credit on wheat productivity of small farms in Sindh, Pakistan. Agric. Financ. Rev. 2018, 78, 592–610. [Google Scholar] [CrossRef]

- Government of Pakistan (GoP). Economic Survey of Pakistan. Economic Advisor Wing, Ministry of Finance, Islamabad, Pakistan. 2019. Available online: http://www.finance.gov.pk/survey/chapter_20/PES_2019_20.pdf (accessed on 11 September 2020).

- Sitko, N.J.; Jayne, T.S. Exploitative briefcase businessmen, parasites, and other myths and legends: Assembly traders and the performance of maize markets in eastern and southern Africa. World Dev. 2014, 54, 56–67. [Google Scholar] [CrossRef]

- Asad, M.; Mehdi, M.; Ashfaq, M.; Hassan, S.; Abid, M. Effect of Marketing Channel Choice on the Profitability of Citrus Farmers: Evidence form Punjab-Pakistan. Pak. J. Agric. Sci. 2019, 56, 1003–1011. [Google Scholar]

- Pokhrel, D.M.; Thapa, G.B. Are marketing intermediaries exploiting mountain farmers in Nepal? A study based on market price, marketing margin and income distribution analyses. Agric. Syst. 2007, 94, 151–164. [Google Scholar] [CrossRef]

- Khan, M.H. Agriculture in Pakistan: A Revisit. Pak. Dev. Rev. 2020, 59, 115–120. [Google Scholar] [CrossRef]

- Hassan, S.Z.; Jajja, M.S.S.; Asif, M.; Foster, G. Bringing more value to small farmers: A study of potato farmers in Pakistan. Manag. Decis. 2020. [Google Scholar] [CrossRef]

- Iqbal, M.A.; Abbas, A.; Ullah, R.; Ahmed, U.I.; Sher, A.; Akhtar, S. Effect of non-farm income on poverty and income inequality: Farm households evidence from Punjab Province Pakistan. Sarhad J. Agric. 2018, 34, 233–239. [Google Scholar] [CrossRef]

- Mariyono, J. Stepping up to market participation of smallholder agriculture in rural areas of Indonesia. Agric. Financ. Rev. 2019, 79, 255–270. [Google Scholar] [CrossRef]

- Sher, A.; Mazhar, S.; Zulfiqar, F.; Wang, D.; Li, X. Green entrepreneurial farming: A dream or reality? J. Clean. Prod. 2019, 220, 1131–1142. [Google Scholar] [CrossRef]

- Banerjee, A.V.; Duflo, E. Do firms want to borrow more? Testing credit constraints using a directed lending program. Rev. Econ. Stud. 2014, 81, 572–607. [Google Scholar]

- Pande, R.; Bernhardt, A.; Field, E.; Rigol, N. Household Matters: Revisiting the Returns to Capital among Female Micro-Entrepreneurs. NBER Working Paper No. 23358/2017. Available online: https://www.nber.org/system/files/working_papers/w23358/w23358.pdf (accessed on 11 September 2020).

- Rasheed, R.; Xia, L.C.; Ishaq, M.N.; Mukhtar, M.; Waseem, M. Determinants influencing the demand of microfinance in agriculture production and estimation of constraint factors: A case from south Region of Punjab Province, Pakistan. Int. J. Agric. Ext. Rural Dev. Stud. 2016, 3, 45–58. [Google Scholar]

- Qadri, H.M.-D. Theoretical, practical vis-à-vis legal development in Islamic banking: A case of Pakistan. In The Growth of Islamic Finance and Banking Innovation, Governance and Risk Mitigation; Routledge: Abingdon, UK, 2019; pp. 281–313. [Google Scholar]

- Sher, A.; Mazhar, S.; Abbas, A.; Iqbal, M.A.; Li, X. Linking Entrepreneurial Skills and Opportunity Recognition with Improved Food Distribution in the Context of the CPEC: A Case of Pakistan. Sustainability 2019, 11, 1838. [Google Scholar] [CrossRef]

- Aa, J.; Atkinson, J.; Kim, C.S. Smallholder Commercialization in Ethiopia: Market Orientation and Participation. Int. Food Res. J. 2016, 23, 1797–1807. [Google Scholar]

- Alhassan, H.; Abu, B.M.; Nkegbe, P.K. Access to Credit, Farm Productivity and Market Participation in Ghana: A Conditional Mixed Process Approach. Margin J. Appl. Econ. Res. 2020, 14, 226–246. [Google Scholar] [CrossRef]

- Mishra, S. Risks, farmers’ suicides and agrarian crisis in India: Is there a way out? Indian J. Agric. Econ. 2008, 63, 38–54. [Google Scholar]

- Oluwasola, O.; Osuntogun, D.A. Increasing agricultural household incomes through rural-urban linkages in Nigeria. African J. Agric. Res. 2008, 3, 566–573. [Google Scholar]

- Mariyono, J. Micro-credit as catalyst for improving rural livelihoods through agribusiness sector in Indonesia. J. Entrep. Emerg. Econ. 2019, 11, 98–121. [Google Scholar] [CrossRef]

- Linh, T.N.; Long, H.T.; Chi, L.V.; Tam, L.T.; Lebailly, P. Access to rural credit markets in developing countries, the case of Vietnam: A literature review. Sustainability 2019, 11, 1468. [Google Scholar] [CrossRef]

- Pham, T.T.T.; Lensink, R. Lending policies of informal, formal and semiformal lenders: Evidence from Vietnam. Econ. Transit. 2007, 15, 181–209. [Google Scholar] [CrossRef]

- Nagarajan, G.; Meyer, R.L.; Hushak, L.J. Demand For Agricultural Loans: A Theoretical And Econometric Analysis Of The Philippine Credit Market/La Demande De Prêts Agricoles: Une Analyse Théorique Et Économique Du Marché De Crédit Aux Philippines. Savings Dev. 1998, 349–363. Available online: www.jstor.org/stable/25830663 (accessed on 20 September 2020).

- Siamwalla, A.; Pinthong, C.; Poapongsakorn, N.; Satsanguan, P.; Nettayarak, P.; Mingmaneenakin, W.; Tubpun, Y. The Thai rural credit system: Public subsidies, private information, and segmented markets. World Bank Econ. Rev. 1990, 4, 271–295. [Google Scholar] [CrossRef]

- Akobundu, E.; Alwang, J.; Essel, A.; Norton, G.W.; Tegene, A. Does extension work? Impacts of a program to assist limited-resource farmers in Virginia. Rev. Agric. Econ. 2004, 26, 361–372. [Google Scholar] [CrossRef]

- Abdallah, W.; Goergen, M.; O’Sullivan, N. Endogeneity: How failure to correct for it can cause wrong inferences and some remedies. Br. J. Manag. 2015, 26, 791–804. [Google Scholar] [CrossRef]

- Sher, A.; Abbas, A.; Mazhar, S.; Azadi, H.; Lin, G. Fostering sustainable ventures: Drivers of sustainable start-up intentions among aspiring university students in Pakistan. J. Clean. Prod. 2020, 262, 121269. [Google Scholar] [CrossRef]

- Timmer, C.P. The Agricultural Transformation. In Handbook of Development Economice; Harvard University Press: Cambridge, MA, USA, 1988; pp. 275–331. [Google Scholar]

- Pinstrup-Andersen, P.; Shimokawa, S. Rural infrastructure and agricultural development. ABCDE 2007, 175. [Google Scholar] [CrossRef]

- Magruder, J.R. An assessment of experimental evidence on agricultural technology adoption in developing countries. Annu. Rev. Resour. Econ. 2018, 10, 299–316. [Google Scholar] [CrossRef]

- Ahmad, D.; Chani, M.I.; Afzal, M. Impact of Formal Credit on Agricultural Output: Empirical Evidence from Pakistan. Sarhad J. Agric. 2018, 34, 64–648. [Google Scholar] [CrossRef]

- Herrero, M.; Thornton, P.K.; Notenbaert, A.M.; Wood, S.; Msangi, S.; Freeman, H.A.; Bossio, D.; Dixon, J.; Peters, M.; van de Steeg, J. Smart investments in sustainable food production: Revisiting mixed crop-livestock systems. Science 2010, 327, 822–825. [Google Scholar] [CrossRef] [PubMed]

- Dobermann, A.; Nelson, R. Opportunities and Solutions for Sustainable Food Production; Sustainable Development Solution Network: Paris, France, 2013; pp. 1–10. [Google Scholar]

- Pawlak, K.; Kołodziejczak, M. The role of agriculture in ensuring food security in developing countries: Considerations in the context of the problem of sustainable food production. Sustainability 2020, 12, 5488. [Google Scholar] [CrossRef]

- Woolverton, A.; Neven, D. Understanding Smallholder Farmer Attitudes to Commercialization. The Case of Maize in Kenya; Food and Agriculture Organization of United Nations (FAO): Rome, Italy, 2014. [Google Scholar]

- Stephens, E.C.; Barrett, C.B. Incomplete credit markets and commodity marketing behaviour. J. Agric. Econ. 2011, 62, 1–24. [Google Scholar] [CrossRef]

- Coleman, J.S.; Fararo, T.J. Rational Choice Theory; Sage: New York, NY, USA, 1992; Available online: https://philpapers.org/rec/COLRCT/ (accessed on 13 September 2020).

- Boughton, D.; Mather, D.; Barrett, C.B.; Benfica, R.S.; Abdula, D.; Tschirley, D.; Cunguara, B. Market participation by rural households in a low-income country: An asset based approach applied to Mozambique. Faith Econ. 2007, 50, 64–101. [Google Scholar]

- Osmani, A.G.; Hossain, E. Market participation decision of smallholder farmers and its determinants in Bangladesh. Econ. Agric. 2015, 62, 163–179. [Google Scholar]

- North, D.C. A transaction cost theory of politics. J. Theor. Polit. 1990, 2, 355–367. [Google Scholar] [CrossRef]

- Romer, P. New goods, old theory, and the welfare costs of trade restrictions. J. Dev. Econ. 1994, 43, 5–38. [Google Scholar] [CrossRef]

- Barrett, C.B.; Swallow, B.M. Fractal poverty traps. World Dev. 2006, 34, 1–15. [Google Scholar] [CrossRef]

- Abdullah, D.Z.; Khan, S.A.; Jebran, K.; Ali, A. Agricultural credit in Pakistan: Past trends and future prospects. J. Appl. Environ. Biol. Sci. 2015, 5, 178–188. [Google Scholar]

- Bashir, M.; Saleem, A.; Ahmed, F. Akhuwat: Measuring Success for a Non-profit Organization. Asian J. Manag. Cases 2019, 16, 100–112. [Google Scholar] [CrossRef]

- Rehman, H.; Moazzam, A.; Ansari, N. Role of microfinance institutions in women empowerment: A case study of Akhuwat, Pakistan. South Asian Stud. 2015, 30, 107. [Google Scholar]

- McKenzie, D.; Rapoport, H. Network effects and the dynamics of migration and inequality: Theory and evidence from Mexico. J. Dev. Econ. 2007, 84, 1–24. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Inverse probability weighted estimation for general missing data problems. J. Econ. 2007, 141, 1281–1301. [Google Scholar] [CrossRef]

- Wooldridge, J.M. Econometric Analysis of cross Section and Panel Data; MIT Press: Cambridge, UK; London, UK, 2002; ISBN 9780262232197/0262232197. [Google Scholar]

- Wooldridge, J.M. Cluster-sample methods in applied econometrics. Am. Econ. Rev. 2003, 93, 133–138. [Google Scholar] [CrossRef]

- Santos, J.R.A. Cronbach’s alpha: A tool for assessing the reliability of scales. J. Ext. 1999, 37, 1–5. [Google Scholar]

- Hung Anh, N.; Bokelmann, W. Determinants of smallholders’ market preferences: The case of sustainable certified coffee farmers in Vietnam. Sustainability 2019, 11, 2897. [Google Scholar] [CrossRef]

- Kirimi, L.; Sitko, N.J.; Jayne, T.S.; Karin, F.; Muyanga, M.; Sheahan, M.; Flock, J.; Bor, G. A Farm Gate-To-Consumer Value Chain Analysis of Kenya’s Maize Marketing System; MSU International Development Working Paper N0. 111; Department of Agricultural, Food, and Resource Economics Department of Economics, Michigan State University: East Lansing, MI, USA, 2011. [Google Scholar]

- Arinloye, D.-D.A.A.; Pascucci, S.; Linnemann, A.R.; Coulibaly, O.N.; Hagelaar, G.; Omta, O.S.W.F. Marketing channel selection by smallholder farmers. J. Food Prod. Mark. 2015, 21, 337–357. [Google Scholar] [CrossRef]

- Feder, G.; Lau, L.J.; Lin, J.Y.; Luo, X. The relationship between credit and productivity in Chinese agriculture: A microeconomic model of disequilibrium. Am. J. Agric. Econ. 1990, 72, 1151–1157. [Google Scholar] [CrossRef]

- Blarel, B.; Hazell, P.; Place, F.; Quiggin, J. The economics of farm fragmentation: Evidence from Ghana and Rwanda. World Bank Econ. Rev. 1992, 6, 233–254. [Google Scholar] [CrossRef]

- Jaleta, M.; Gebremedhin, B.; Hoekstra, D. Smallholder Commercialization: Processes, Determinants and Impact; Discussion Paper 18; International Livestock Research Institute (ILRI): Nairobi, Kenya, 2009; pp. 1–55. [Google Scholar]

- Von Braun, J.; Kennedy, E.T. Agricultural Commercialization, Economic Development, and Nutrition; International Food Policy Research Institute (IFPRI): Washington, DC, USA, 1994; pp. 44–57. [Google Scholar]

- Sedem, E.D.; William, A.; Gideon, D.-A. Effect of access to agriculture credit on farm income in the Talensi district of northern Ghana. Russ. J. Agric. Socio-Econ. Sci. 2016, 7, 40–46. [Google Scholar]

- Bashir, M.K.; Mehmood, Y.; Hassan, S. Impact of agricultural credit on productivity of wheat crop: Evidence from Lahore, Punjab, Pakistan. Pakistan J. Agric. Sci. 2010, 47, 405–409. [Google Scholar]

- Ogundeji, A.A.; Donkor, E.; Motsoari, C.; Onakuse, S. Impact of access to credit on farm income: Policy implications for rural agricultural development in Lesotho. Agrekon 2018, 57, 152–166. [Google Scholar] [CrossRef]

- Shah, M.K.; Khan, H.; Khan, Z. Impact of agricultural credit on farm productivity and income of farmers in mountainous agriculture in northern Pakistan: A case study of selected villages in district Chitral. Sarhad J. Agric. 2008, 24, 713–718. [Google Scholar]

- Agbodji, A.E.; Johnson, A.A. Agricultural Credit and Its Impact on the Productivity of Certain Cereals in Togo. Emerg. Mark. Financ. Trade 2019, 1–17. [Google Scholar] [CrossRef]

- Khandker, S.R.; Samad, H.A.; Khan, Z.H. Income and employment effects of micro-credit programmes: Village-level evidence from Bangladesh. J. Dev. Stud. 1998, 35, 96–124. [Google Scholar] [CrossRef]

- Hussain, A.; Taqi, M. Impact of agricultural credit on agricultural productivity in Pakistan: An empirical analysis. Int. J. Adv. Res. Manag. Soc. Sci. 2014, 3, 125–139. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).