The Impact of Smog Pollution on Audit Quality: Evidence from China

Abstract

1. Introduction

2. Literature Review and Hypotheses Development

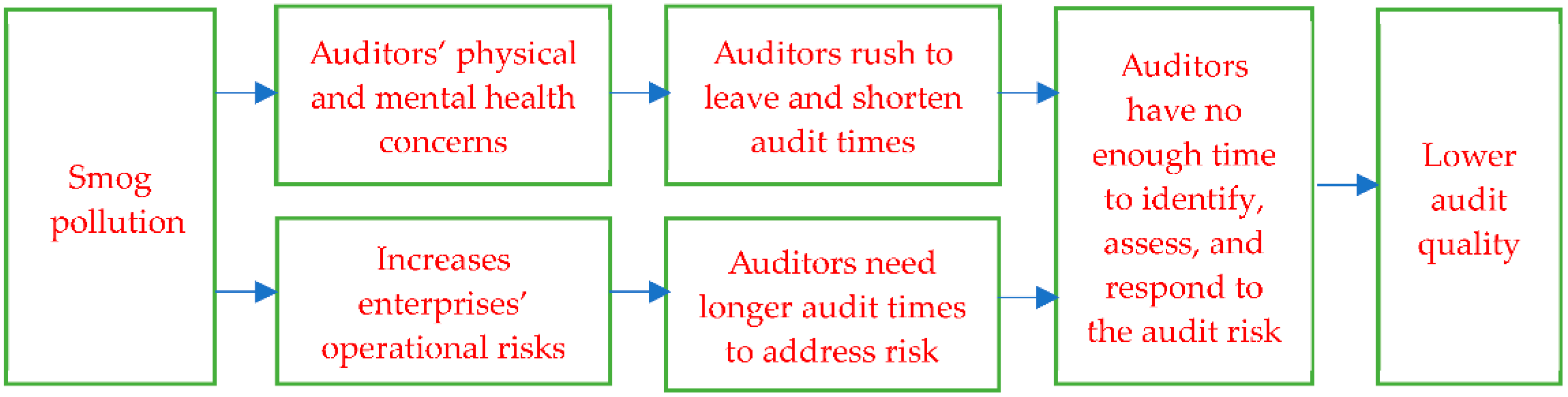

2.1. The Impact of Smog Pollution on Audit Quality

2.2. The Moderating Effect of Internal Controls

3. Methods

3.1. Data Source and Sample Selection

3.2. Variable Definition

3.3. Empirical Model

3.3.1. The Audit Time Mediation Effect Test between Smog Pollution and Audit Quality

3.3.2. The Internal Control Moderating Effect Test

4. Results

4.1. Descriptive Statistics

4.2. Pearson Correlation Coefficient Matrix

4.3. Regression Results

4.4. Further Analysis

4.5. Robustness Test

4.5.1. Using Extreme Weather

4.5.2. Replacement of the Smog Pollution Measurement Indicator

5. Summary and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Brunekreef, B.; Holgate, S.T. Air Pollution and Health. Lancet 2002, 360, 1233–1242. [Google Scholar] [CrossRef]

- Moretti, E.; Neidell, M. Pollution, Health, and Avoidance Behavior: Evidence from the Ports of los Angeles. J. Hum. Resour. 2011, 46, 154–175. [Google Scholar] [CrossRef]

- Lundberg, A. Psychiatric Aspects of Air Pollution. Otolaryngol. Head Neck Surg. 1996, 114, 227–231. [Google Scholar] [CrossRef]

- Yang, W.; Mu, L.; Shen, Y. Effect of Climate and Seasonality on Depressed Mood among Twitter Users. Appl. Geogr. 2015, 63, 184–191. [Google Scholar] [CrossRef]

- Levy, T.; Yagil, J. Air Pollution and Stock Returns in the US. J. Econ. Psychol. 2011, 32, 374–383. [Google Scholar] [CrossRef]

- Guo, M.; Wei, M.; Huang, L. Does Air Pollution Influence Investor Trading Behavior? Evidence from China. Emerg. Mark. Rev. 2021, 100822, in press. [Google Scholar] [CrossRef]

- Li, B.; Guo, P.; Zeng, Y. The Impact of Haze on the Availability of Company Debt Financing: Evidence for Sustainability of Chinese Listed Companies. Sustainability 2019, 11, 806. [Google Scholar] [CrossRef]

- Li, B.; Shi, S.; Zeng, Y. The Impact of Haze Pollution on Firm-Level TFP in China: Test of a Mediation Model of Labor Productivity. Sustainability 2020, 12, 8446. [Google Scholar] [CrossRef]

- Li, B.; He, M.; Gao, F.; Zeng, Y. The Impact of Air Pollution on Corporate Cash Holdings. Borsa Istanb. Rev. 2021, 21, S90–S98. [Google Scholar] [CrossRef]

- Tan, J.; Tan, Z.; Chan, K.C. Does Air Pollution Affect a Firm’s Cash Holdings? Pac. Basin Financ. J. 2021, 67, 101549. [Google Scholar] [CrossRef]

- Peng, M.; Zeng, Y.; Yang, D.C.; Li, B. The Role of Smog in Firm Valuation. Emerg. Mark. Financ. Trade 2021. [Google Scholar] [CrossRef]

- Song, Y.; Song, Y. Are Auditor’s Professional Judgments Influenced by Air Quality? China J. Account. Stud. 2018, 6, 555–582. [Google Scholar] [CrossRef]

- Chen, H.; Tan, X.; Cao, Q. Air pollution, Auditors’ Pessimistic Bias and Audit Quality: Evidence from China. Sustain. Account. Manag. 2021, 12, 74–104. [Google Scholar] [CrossRef]

- Defond, M.L.; Zhang, J. A Review of Archival Auditing Research. J. Account. Econ. 2014, 58, 275–326. [Google Scholar] [CrossRef]

- Watts, R.L.; Zimmerman, J.L. Agency Problems, Auditing, and the Theory of the Firm: Some Evidence. J. Law Econ. 1983, 26, 613–633. [Google Scholar] [CrossRef]

- Carcello, J.V.; Neal, T.L. Audit Committee Composition and Auditor Reporting. Account. Rev. 2000, 75, 453–467. [Google Scholar] [CrossRef]

- Palmrose, Z.V. Competitive Manuscript Co-Winner: An Analysis of Auditor Litigation and Audit Service Quality. Account. Rev. 1988, 63, 55–73. [Google Scholar]

- Teoh, S.H.; Wong, T.J. Perceived Auditor Quality and the Earnings Response Coefficient. Account. Rev. 1993, 68, 346–366. [Google Scholar]

- DeFond, M.L.; Francis, J.R. Audit Research after sarbanes-oxley. Aud. J. Pract. Theory 2005, 24, 5–30. [Google Scholar] [CrossRef]

- Gul, F.A.; Wu, D.; Yang, Z. Do Individual Auditors Affect Audit Quality? Evidence from Archival Data. Account. Rev. 2013, 88, 1993–2023. [Google Scholar] [CrossRef]

- Francis, J.R.; Yu, M.D. Big 4 Office Size and Audit Quality. Account. Rev. 2009, 84, 1521–1552. [Google Scholar] [CrossRef]

- Knechel, W.R.; Rouse, P.; Schelleman, C. A Modified Audit Production Framework: Evaluating the Relative Efficiency of Audit Engagements. Account. Rev. 2009, 84, 1607–1638. [Google Scholar] [CrossRef]

- Lobo, G.J.; Zhao, Y. Relation between Audit Effort and Financial Report Misstatements: Evidence from Quarterly and Annual Restatements. Account. Rev. 2013, 88, 1385–1412. [Google Scholar] [CrossRef]

- Francis, J.R. A Framework for Understanding and Researching Audit Quality. Audit. J. Pract. Theory 2011, 30, 125–152. [Google Scholar] [CrossRef]

- Zhang, Z.; Wang, J.; Chen, L.; Chen, X.; Sun, G.; Zhong, N.; Kan, H.; Lu, W. Impact of Haze and Air Pollution-Related Hazards on Hospital Admissions in Guangzhou, China. Environ. Sci. Pollut. Res. Int. 2014, 21, 4236–4244. [Google Scholar] [CrossRef] [PubMed]

- Gehring, U.; Gruzieva, O.; Agius, R.M.; Beelen, R.; Custovic, A.; Cyrys, J.; Eeftens, M.; Flexeder, C.; Fuertes, E.; Heinrich, J.; et al. Air Pollution Exposure and Lung Function in Children: The Escape Project. Environ. Health Perspect. 2013, 121, 1357–1364. [Google Scholar] [CrossRef] [PubMed]

- Wang, C.; Cai, J.; Chen, R.; Shi, J.; Yang, C.; Li, H.; Lin, Z.; Meng, X.; Liu, C.; Niu, Y.; et al. Personal Exposure to Fine Particulate Matter, Lung Function and Serum Club Cell Secretory Protein (Clara). Environ. Pollut. 2017, 225, 450–455. [Google Scholar] [CrossRef]

- Weiss, B. Behavior as an Early Indicator of Pesticide Toxicity. Toxicol. Ind. Health 1988, 4, 351–360. [Google Scholar] [CrossRef] [PubMed]

- Li, M.; Zhang, L.H. Haze in China: Current and Future Challenges. Environ. Pollut. 2014, 189, 85–86. [Google Scholar] [CrossRef]

- Cesaroni, G.; Forastiere, F.; Stafoggia, M.; Andersen, Z.J.; Badaloni, C.; Beelen, R.; Caracciolo, B.; de Faire, U.; Erbel, R.; Eriksen, K.T.; et al. Long Term Exposure to Ambient Air Pollution and Incidence of Acute Coronary Events: Prospective Cohort Study and Meta-Analysis in 11 European Cohorts from the Escape Project. BMJ 2014, 348, f7412. [Google Scholar] [CrossRef]

- Pascal, M.; Falq, G.; Wagner, V.; Chatignoux, E.; Corso, M.; Blanchard, M.; Host, S.; Pascal, L.; Larrieu, S. Short-Term Impacts of Particulate Matter (PM10, PM10−2.5, PM2.5) on Mortality in Nine French Cities. Atmos. Environ. 2014, 95, 175–184. [Google Scholar] [CrossRef]

- Lu, F.; Xu, D.; Cheng, Y.; Dong, S.; Guo, C.; Jiang, X.; Zheng, X. Systematic Review and Meta-Analysis of the Adverse Health Effects of Ambient PM2.5 and PM10 Pollution in the Chinese Population. Environ. Res. 2015, 136, 196–204. [Google Scholar] [CrossRef] [PubMed]

- Chen, X.; Shao, S.; Tian, Z.; Xie, Z.; Yin, P. Impacts of Air Pollution and Its Spatial Spillover Effect on Public Health Based on China’s Big Data Sample. J. Clean. Prod. 2017, 142, 915–925. [Google Scholar] [CrossRef]

- Bullinger, M. Environmental Stress: Effects of Air Pollution on Mood, Neuropsychological Function and Physical State. Psychobiol. Stress 1990, 54, 241–250. [Google Scholar] [CrossRef]

- Cunsolo Willox, A.C.; Harper, S.L.; Ford, J.D.; Landman, K.; Houle, K.; Edge, V.L. ‘From this place and of this place:’ Climate Change, Sense of Place, and Health in Nunatsiavut, Canada. Soc. Sci. Med. 2012, 75, 538–547. [Google Scholar] [CrossRef] [PubMed]

- Neria, Y.; Shultz, J.M. Mental Health Effects of Hurricane Sandy: Characteristics, Potential Aftermath, and Response. JAMA 2012, 308, 2571–2572. [Google Scholar] [CrossRef] [PubMed]

- Evans, G.W.; Jacobs, S.V.; Dooley, D.; Catalano, R. The Interaction of Stressful Life Events and Chronic Strains on Community Mental Health. Am. J. Community Psychol. 1987, 15, 23–34. [Google Scholar] [CrossRef]

- Lim, Y.H.; Kim, H.; Kim, J.H.; Bae, S.; Park, H.Y.; Hong, Y.C. Air Pollution and Symptoms of Depression in Elderly Adults. Environ. Health Perspect. 2012, 120, 1023–1028. [Google Scholar] [CrossRef]

- Zivin, J.G.; Neidell, M. The Impact of Pollution on Worker Productivity. Am. Econ. Rev. 2012, 102, 3652–3673. [Google Scholar] [CrossRef]

- Chang, T.; Graff Zivin, J.; Gross, T.; Neidell, M. Particulate Pollution and the Productivity of Pear Packers. Am. Econ. J. Econ. Policy 2016, 8, 141–169. [Google Scholar] [CrossRef]

- Fu, S.; Zhang, P. Air Quality and Manufacturing Firm Productivity: Comprehensive Evidence from China. SSRN J. 2017. [Google Scholar] [CrossRef]

- Plaisier, I.; Beekman, A.T.F.; De Graaf, R.; Smit, J.H.; Van Dyck, R.; Penninx, B.W.J.H. Work Functioning in Persons with Depressive and Anxiety Disorders: The Role of Specific Psychopathological Characteristics. J. Affect. Disord. 2010, 125, 198–206. [Google Scholar] [CrossRef] [PubMed]

- Yu, L.; Ying, R.; Zhang, B. How Air Pollution Lowers the Domestic Value-added Ratio in Exports: An Empirical Study of China. Environ. Sci. Pollut. Res. 2021. ahead of print. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.; Lu, T.; Qiao, Y. The Effect of Air Pollution on Corporate Social Responsibility Performance in High Energy-consumption Industry: Evidence from Chinese Listed Companies. J. Clean. Prod. 2021, 280, 124345. [Google Scholar] [CrossRef]

- Bell, T.B.; Doogar, R.; Solomon, I. Audit Labor Usage and Fees under Business Risk Auditing. J. Account. Res. 2008, 46, 729–760. [Google Scholar] [CrossRef]

- Hermanson, H.M. An Analysis of the Demand for Reporting on Internal Control. Account. Horiz. 2000, 14, 325–341. [Google Scholar] [CrossRef]

- Doyle, J.T.; Ge, W.; Mcvay, S. Accruals Quality and Internal Control over Financial Reporting. Account. Rev. 2007, 82, 1141–1170. [Google Scholar] [CrossRef]

- Carter, M.E.; Lynch, L.J.; Zechman, S.L.C. Changes in Bonus Contracts in the Post-sarbanes–oxley Era. Rev. Account. Stud. 2009, 14, 480–506. [Google Scholar] [CrossRef]

- Feng, M.; Li, C.; McVay, S. Internal Control and Management Guidance. J. Account. Econ. 2009, 48, 190–209. [Google Scholar] [CrossRef]

- Cheng, Q.; Goh, B.W.; Kim, J.B. Internal Control and Operational Efficiency. Contemp. Account. Res. 2018, 35, 1102–1139. [Google Scholar] [CrossRef]

- Dechow, P.M.; Sloan, R.G.; Sweeney, A.P. Detecting Earnings Management. Account. Rev. 1995, 70, 193–225. [Google Scholar]

- Defond, M.L.; Wong, T.J.; Li, S. The Impact of Improved Auditor Independence on Audit Market Concentration in China. J. Account. Econ. 1999, 28, 269–305. [Google Scholar] [CrossRef]

- Chen, G.; Firth, M.; Gao, D.N.; Rui, O.M. Ownership Structure, Corporate Governance, and Fraud: Evidence from China. J. Corp. Financ. 2006, 12, 424–448. [Google Scholar] [CrossRef]

- Gassen, J.; Skaife, H.A. Can Audit Reforms Affect the Information Role of Audits? Evidence from the German Market. Contemp. Account. Res. 2009, 26, 867–898. [Google Scholar] [CrossRef]

- DeFond, M.; Subramanyam, K. Restrictions to Accounting Choice: Evidence from Auditor Realignment; Working Paper; University of Southern California: Los Angeles, CA, USA, 1997. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

{kind=link}

| Variable Sign | Variable Name | Variable Description |

|---|---|---|

| Qualityi,t | Audit quality | The absolute value of discretionary accruals calculated using the modified Jones model [51]; multiplied by −100 to measure audit quality |

| Timei,t | Audit time | Measured by the number of days between the balance sheet date and the audit report date |

| ICi,t | Internal control | Measured by the internal control information disclosure index in the DIB Internal Control and Risk Management Database |

| PM2.5i,t | Smog pollution | The average of the PM2.5 concentration data in monthly air quality reports from November of the current year to April of the following year |

| Sizei,t | Firm size | The natural logarithm of total assets |

| Reci,t | Ratio of accounts receivable to total assets | Accounts receivable/total assets |

| Invi,t | Ratio of inventory to total assets | Inventory/total assets |

| Levi,t | Ratio of total liability to total assets | Total liability/total assets |

| Currenti,t | Current ratio | Current assets/current liability |

| Roai,t | Return on total assets | (total profit + financial expenses)/total assets |

| Lossi,t | Whether the firm experienced a loss in the current year | A dummy variable that takes 1 if the net profit is less than 0; otherwise, it is 0 |

| Btmi,t | Book-to-market ratio | |

| Growthi,t | Growth rate | Amount of increased revenue in current year /amount of revenue in previous year |

| Shrcr1i,t | Largest shareholder’s shareholding ratio | The largest shareholder’s shareholding ratio |

| Indirectori,t | Proportion of independent directors on the board of directors | Number of independent directors/number of board members |

| Duali,t | Whether the chairman is also the general manager | A dummy variable that takes 1 if the chairman is also the general manager; otherwise, it takes 0 |

| Soei,t | Whether the enterprise is a state-owned holding | A dummy variable that takes 1 if the enterprise is state-owned; otherwise, it takes 0 |

| Agei,t | Company’s listing age | The company’s listing age |

| AIi,t | Whether to issue additional shares | A dummy variable that takes 1 if stock is issued in the current year; otherwise, it takes 0 |

| Big_10i,t | Whether the enterprise’s annual audit is performed by a “top 10” accounting firm | A dummy variable that takes 1 if the accounting firm belongs to the “top 10;” otherwise, it takes 0 (The Chinese Institute of Certified Public Accountants publishes the top 100 accounting firms’ annual business income) |

| Switchi,t | Whether the company had an audit firm replacement in the current year | A dummy variable that takes 1 if the enterprise underwent audit firm replacement in the current year; otherwise, it takes 0 |

| L_opinioni,t | Type of audit opinion in the previous year | A dummy variable that takes 1 if a non-standard audit opinion was obtained in the previous year; otherwise, it takes 0 |

| Locai,t | Level of economic development at the company’s location | A dummy variable that takes 1 if the company is registered in Beijing, Shanghai, Tianjin, Guangzhou, or Shenzhen; otherwise, it takes 0 |

| Industryi,t | Industry | Industry dummy variable |

| Yeari,t | Year | Year dummy variable |

| Variable | N | Mean | Std. Dev. | Min. | Median | Max. |

|---|---|---|---|---|---|---|

| Quality | 7744 | −9.227 | 19.661 | −133.757 | −2.883 | −0.061 |

| PM2.5 | 7744 | 63.173 | 21.234 | 29.166 | 59.912 | 122.263 |

| Time | 7744 | 135.655 | 18.346 | 64.000 | 127.000 | 148.000 |

| IC | 7744 | 35.895 | 6.072 | 18.070 | 36.541 | 47.885 |

| Size | 7744 | 22.208 | 1.260 | 19.903 | 22.048 | 26.069 |

| Rec | 7744 | 0.126 | 0.107 | 0.000 | 0.104 | 0.477 |

| Inv | 7744 | 0.150 | 0.147 | 0.000 | 0.110 | 0.747 |

| Lev | 7744 | 0.426 | 0.207 | 0.052 | 0.418 | 0.872 |

| Current | 7744 | 2.494 | 2.526 | 0.297 | 1.683 | 16.556 |

| Roa | 7744 | 0.044 | 0.050 | −0.159 | 0.042 | 0.192 |

| Loss | 7744 | 0.073 | 0.260 | 0.000 | 0.000 | 1.000 |

| Btm | 7744 | 0.825 | 0.867 | 0.083 | 0.530 | 4.854 |

| Growth | 7744 | 0.216 | 0.491 | −0.511 | 0.118 | 3.216 |

| Shrcr1 | 7744 | 0.361 | 0.152 | 0.092 | 0.342 | 0.750 |

| Indirector | 7744 | 0.376 | 0.053 | 0.333 | 0.364 | 0.571 |

| Dual | 7744 | 0.267 | 0.442 | 0.000 | 0.000 | 1.000 |

| Soe | 7744 | 0.342 | 0.474 | 0.000 | 0.000 | 1.000 |

| Age | 7744 | 10.209 | 7.000 | 1.000 | 8.000 | 24.000 |

| AI | 7744 | 0.178 | 0.382 | 0.000 | 0.000 | 1.000 |

| Big_10 | 7744 | 0.646 | 0.478 | 0.000 | 1.000 | 1.000 |

| Switch | 7744 | 0.143 | 0.350 | 0.000 | 0.000 | 1.000 |

| L_opinion | 7744 | 0.034 | 0.182 | 0.000 | 0.000 | 1.000 |

| Loca | 7744 | 0.379 | 0.485 | 0.000 | 0.000 | 1.000 |

| Variable | Quality (1) | Time (2) | Quality (3) | Quality (4) | Quality (5) |

|---|---|---|---|---|---|

| PM2.5 | −0.0416 ** | −0.0217 ** | −0.0404 ** | −0.0404 ** | |

| (−2.09) | (−2.06) | (−2.03) | (−2.03) | ||

| Time | 0.0575 *** | 0.0564 *** | −0.2190 * | ||

| (2.66) | (2.62) | (−1.81) | |||

| IC | −1.0290 ** | ||||

| (−2.41) | |||||

| Time × IC | 0.00776 ** | ||||

| (2.30) | |||||

| Size | −7.7750 *** | 0.8150 *** | −7.8560 *** | −7.8210 *** | −7.7480 *** |

| (−15.58) | (3.09) | (−15.75) | (−15.67) | (−15.34) | |

| Rec | 8.0900 * | 6.9960 *** | 7.4510 * | 7.6950 * | 7.9560 * |

| (1.91) | (3.13) | (1.76) | (1.82) | (1.88) | |

| Inv | 3.1610 | 0.1330 | 3.2610 | 3.1540 | 3.2560 |

| (0.94) | (0.07) | (0.97) | (0.94) | (0.97) | |

| Lev | 15.5900 *** | 0.7200 | 15.6600 *** | 15.5500 *** | 15.3600 *** |

| (4.63) | (0.41) | (4.66) | (4.62) | (4.56) | |

| Current | 0.1370 | 0.0481 | 0.1240 | 0.1340 | 0.1240 |

| (0.66) | (0.44) | (0.59) | (0.64) | (0.59) | |

| Roa | 12.1400 | −26.4000 *** | 13.5500 | 13.6300 | 13.9800 |

| (1.15) | (−4.72) | (1.28) | (1.29) | (1.32) | |

| Loss | −1.9480 | −1.3330 | −1.9450 | −1.8720 | −1.8480 |

| (−1.01) | (−1.31) | (−1.01) | (−0.97) | (−0.96) | |

| Btm | −9.1120 *** | 0.6080 | −9.2070 *** | −9.1460 *** | −9.1620 *** |

| (−11.97) | (1.51) | (−12.10) | (−12.01) | (−12.04) | |

| Growth | 0.3310 | −1.5060 *** | 0.4020 | 0.4160 | 0.3490 |

| (0.40) | (−3.41) | (0.48) | (0.50) | (0.42) | |

| Shrcr1 | −4.7090 * | −1.4100 | −4.7750 * | −4.6290 * | −4.6770 * |

| (−1.69) | (−0.96) | (−1.72) | (−1.67) | (−1.68) | |

| Indiretor | −32.7300 *** | −4.2120 | −31.7100 *** | −32.4900 *** | −32.1600 *** |

| (−4.41) | (−1.07) | (−4.28) | (−4.38) | (−4.33) | |

| Dual | −1.6490 * | 0.2350 | −1.5880 * | −1.6620 * | −1.7270 * |

| (−1.77) | (0.48) | (−1.71) | (−1.79) | (−1.85) | |

| Soe | −0.9390 | −2.9600 *** | −0.9970 | −0.7720 | −0.6700 |

| (−0.90) | (−5.36) | (−0.96) | (−0.74) | (−0.64) | |

| Age | 0.2170 *** | −0.0965 ** | 0.2300 *** | 0.2220 *** | 0.2180 *** |

| (2.91) | (−2.45) | (3.09) | (2.98) | (2.92) | |

| AI | 2.0300 * | 0.6690 | 2.0110 * | 1.9920 * | 1.9760 * |

| (1.86) | (1.16) | (1.84) | (1.82) | (1.81) | |

| Big_10 | −1.5250 * | 0.0240 | −1.3890 * | −1.5260 * | −1.5310 * |

| (−1.85) | (0.06) | (−1.69) | (−1.85) | (−1.86) | |

| Switch | 1.5220 | 0.3330 | 1.5380 | 1.5030 | 1.5320 |

| (1.36) | (0.57) | (1.38) | (1.35) | (1.37) | |

| L_opinion | 0.2620 | 2.5110 ** | 0.1030 | 0.1200 | 0.1290 |

| (0.12) | (2.18) | (0.05) | (0.05) | (0.06) | |

| Loca | −4.2710 *** | −0.0052 | −3.9830 *** | −4.2710 *** | −4.1990 *** |

| (−5.04) | (−0.01) | (−4.77) | (−5.04) | (−4.95) | |

| Cons | 187.6000 *** | 114.9000 ** | 178.3000 *** | 181.1000 *** | 216.0000 *** |

| (16.57) | (19.23) | (15.50) | (15.63) | (11.45) | |

| Industry | control | control | control | control | control |

| Year | control | control | control | control | control |

| N | 7744 | 7744 | 7744 | 7744 | 7744 |

| Adj R2 | 0.246 | 0.039 | 0.246 | 0.246 | 0.246 |

| Variable | Quality (1) | Quality (1) | Time (2) | Quality (3) | Quality (4) |

|---|---|---|---|---|---|

| Non-“Top 10” | “Top 10” | “Top 10” | “Top 10” | “Top 10” | |

| PM2.5 | 0.00198 | −0.0681 ** | −0.0323 ** | −0.0658 ** | |

| (0.16) | (−2.19) | (−2.40) | (−2.12) | ||

| Time | 0.0756 ** | 0.0733 ** | |||

| (2.31) | (2.24) | ||||

| Size | −4.2100 *** | −8.8410 *** | 0.6080 * | −8.9590 *** | −8.8860 *** |

| (−11.46) | (−12.34) | (1.96) | (−12.51) | (−12.40) | |

| Rec | 4.9680 * | 8.3930 | 10.6500 *** | 7.0830 | 7.6120 |

| (1.74) | (1.33) | (3.89) | (1.12) | (1.20) | |

| Inv | 2.6910 | 2.1080 | 3.8890 * | 2.1300 | 1.8230 |

| (1.25) | (0.40) | (1.72) | (0.41) | (0.35) | |

| Lev | −3.7870 * | 27.2100 *** | −1.2280 | 27.5400 *** | 27.3000 *** |

| (−1.69) | (5.39) | (−0.56) | (5.45) | (5.41) | |

| Current | −0.2490 * | 0.4550 | 0.1260 | 0.4340 | 0.4460 |

| (−1.75) | (1.48) | (0.94) | (1.41) | (1.45) | |

| Roa | −17.0400 ** | 23.3900 | −31.2400 *** | 25.5500 * | 25.6800 * |

| (−2.31) | (1.51) | (−4.67) | (1.65) | (1.66) | |

| Loss | −3.2600 ** | −1.7860 | −2.3650 * | −1.7020 | −1.6130 |

| (−2.56) | (−0.62) | (−1.88) | (−0.59) | (−0.56) | |

| Btm | −1.8840 *** | −12.3400 *** | 0.3380 | −12.4700 *** | −12.3700 *** |

| (−3.41) | (−11.21) | (0.71) | (−11.33) | (−11.23) | |

| Growth | −0.0380 | 0.2410 | −1.0980 ** | 0.2470 | 0.3220 |

| (−0.07) | (0.19) | (−2.01) | (0.20) | (0.25) | |

| Shrcr1 | 1.4560 | −8.0760 ** | −2.4690 | −8.0820 ** | −7.8950 * |

| (0.77) | (−1.96) | (−1.39) | (−1.96) | (−1.92) | |

| Indiretor | 5.2980 | −44.5500 *** | −4.3840 | −43.5900 *** | −44.2200 *** |

| (1.00) | (−4.13) | (−0.94) | (−4.05) | (−4.10) | |

| Dual | −1.7620 *** | −1.9700 | 0.2560 | −1.8980 | −1.9890 |

| (−2.76) | (−1.43) | (0.43) | (−1.38) | (−1.45) | |

| Soe | −0.3190 | −0.9770 | −2.7030 *** | −1.1540 | −0.7780 |

| (−0.47) | (−0.61) | (−3.92) | (−0.73) | (−0.49) | |

| Age | 0.00226 | 0.2900 *** | −0.0579 | 0.3120 *** | 0.2940 *** |

| (0.04) | (2.63) | (−1.21) | (2.83) | (2.66) | |

| AI | 0.6590 | 2.1540 | 1.0260 | 2.1090 | 2.0780 |

| (0.91) | (1.31) | (1.44) | (1.28) | (1.27) | |

| Switch | 0.1110 | 2.3380 | −0.0524 | 2.3820 | 2.3420 |

| (0.15) | (1.40) | (−0.07) | (1.42) | (1.40) | |

| L_opinion | 1.7240 | 0.2040 | 2.8470 ** | −0.0709 | −0.00417 |

| (1.18) | (0.06) | (2.02) | (−0.02) | (−0.00) | |

| Loca | 0.7830 | −6.9000 *** | −0.4460 | −6.3470 *** | −6.8670 *** |

| (1.33) | (−5.53) | (−0.82) | (−5.18) | (−5.50) | |

| Cons | 92.1300 *** | 214.5000 *** | 122.8000 *** | 201.8000 *** | 205.5000 *** |

| (11.05) | (13.07) | (17.27) | (12.01) | (12.17) | |

| Industry | control | control | control | control | control |

| Year | control | control | control | control | control |

| N | 2743 | 5001 | 5001 | 5001 | 5001 |

| Adj R2 | 0.416 | 0.250 | 0.043 | 0.250 | 0.250 |

| Variable | Quality (1) | Time (2) | Quality (3) | Quality (4) | Quality (5) |

|---|---|---|---|---|---|

| Extrweather | −5.6050 ** | −2.6840 ** | −5.4540 ** | −5.4690 ** | |

| (−2.29) | (−2.08) | (−2.23) | (−2.23) | ||

| Time | 0.0575 *** | 0.0563 *** | −0.2190 * | ||

| (2.66) | (2.61) | (−1.80) | |||

| IC | −1.0280 ** | ||||

| (−2.41) | |||||

| Time × IC | 0.00775 ** | ||||

| (2.29) | |||||

| Size | −7.7710 *** | 0.8150 *** | −7.8560 *** | −7.8170 *** | −7.7430 *** |

| (−15.58) | (3.09) | (−15.75) | (−15.66) | (−15.33) | |

| Rec | 8.1430 * | 7.0120 *** | 7.4510 * | 7.7480 * | 8.0130 * |

| (1.92) | (3.13) | (1.76) | (1.83) | (1.89) | |

| Inv | 3.1710 | 0.1420 | 3.2610 | 3.1630 | 3.2670 |

| (0.94) | (0.08) | (0.97) | (0.94) | (0.97) | |

| Lev | 15.5800 *** | 0.7180 | 15.6600 *** | 15.5400 *** | 15.3400 *** |

| (4.63) | (0.40) | (4.66) | (4.62) | (4.55) | |

| Current | 0.1370 | 0.0479 | 0.1240 | 0.1340 | 0.1240 |

| (0.66) | (0.44) | (0.59) | (0.65) | (0.60) | |

| Roa | 12.2100 | −26.3700 *** | 13.5500 | 13.7000 | 14.0600 |

| (1.15) | (−4.72) | (1.28) | (1.29) | (1.33) | |

| Loss | −1.9500 | −1.3380 | −1.9450 | −1.8750 | −1.8520 |

| (−1.01) | (−1.32) | (−1.01) | (−0.97) | (−0.96) | |

| Btm | −9.1220 *** | 0.6010 | −9.2070 *** | −9.1560 *** | −9.1720 *** |

| (−11.98) | (1.50) | (−12.10) | (−12.03) | (−12.05) | |

| Growth | 0.3240 | −1.5100 *** | 0.4020 | 0.4090 | 0.3420 |

| (0.39) | (−3.42) | (0.48) | (0.49) | (0.41) | |

| Shrcr1 | −4.6610 * | −1.3940 | −4.7750 * | −4.5830 * | −4.6300 * |

| (−1.68) | (−0.95) | (−1.72) | (−1.65) | (−1.67) | |

| Indiretor | −32.9000 *** | −4.2630 | −31.7100 *** | −32.6600 *** | −32.3300 *** |

| (−4.43) | (−1.09) | (−4.28) | (−4.40) | (−4.35) | |

| Dual | −1.6600 * | 0.2330 | −1.5880 * | −1.6730 * | −1.7400* |

| (−1.79) | (0.47) | (−1.71) | (−1.80) | (−1.87) | |

| Soe | −0.9190 | −2.9600 *** | −0.9970 | −0.7520 | −0.6480 |

| (−0.88) | (−5.36) | (−0.96) | (−0.72) | (−0.62) | |

| Age | 0.2170 *** | −0.0958 ** | 0.2300 *** | 0.2230 *** | 0.2180 *** |

| (2.92) | (−2.44) | (3.09) | (2.99) | (2.93) | |

| AI | 2.0260 * | 0.6670 | 2.0110 * | 1.9880 * | 1.9710 * |

| (1.85) | (1.16) | (1.84) | (1.82) | (1.80) | |

| Big_10 | −1.5140 * | 0.0353 | −1.3890 * | −1.5160 * | −1.5210 * |

| (−1.84) | (0.08) | (−1.69) | (−1.84) | (−1.85) | |

| Switch | 1.4950 | 0.3220 | 1.5380 | 1.4770 | 1.5050 |

| (1.34) | (0.55) | (1.38) | (1.32) | (1.35) | |

| L_opinion | 0.2640 | 2.5120 ** | 0.1030 | 0.1220 | 0.1280 |

| (0.12) | (2.18) | (0.05) | (0.06) | (0.06) | |

| Loca | −4.3890 *** | −0.0492 | −3.9830 *** | −4.3860 *** | −4.3150 *** |

| (−5.13) | (−0.11) | (−4.77) | (−5.13) | (−5.05) | |

| Cons | 186.9000 *** | 114.5000 *** | 178.3000 *** | 180.4000 *** | 215.3000 *** |

| (16.57) | (19.23) | (15.50) | (15.63) | (11.42) | |

| Industry | control | control | control | control | control |

| Year | control | control | control | control | control |

| N | 7744 | 7744 | 7744 | 7744 | 7744 |

| Adj R2 | 0.246 | 0.039 | 0.246 | 0.246 | 0.247 |

| Variable | Quality (1) | Time (2) | Quality (3) | Quality (4) | Quality(5) |

|---|---|---|---|---|---|

| AQI | −0.6330 ** | −0.3130 * | −0.6150 ** | −0.6150 ** | |

| (−2.09) | (−1.95) | (−2.03) | (−2.03) | ||

| Time | 0.0575 *** | 0.0565 *** | −0.2190 * | ||

| (2.66) | (2.62) | (−1.80) | |||

| IC | −1.0280 ** | ||||

| (−2.41) | |||||

| Time × IC | 0.00775 ** | ||||

| (2.29) | |||||

| Size | −7.7880 *** | 0.8070 *** | −7.8560 *** | −7.8330 *** | −7.7610 *** |

| (−15.61) | (3.07) | (−15.75) | (−15.70) | (−15.37) | |

| Rec | 8.0920 * | 6.9910 *** | 7.4510 * | 7.6970 * | 7.9580 * |

| (1.91) | (3.12) | (1.76) | (1.82) | (1.88) | |

| Inv | 3.1900 | 0.1510 | 3.2610 | 3.1820 | 3.2840 |

| (0.95) | (0.08) | (0.97) | (0.94) | (0.97) | |

| Lev | 15.6500 *** | 0.7530 | 15.6600 *** | 15.6100 *** | 15.4200 *** |

| (4.65) | (0.42) | (4.66) | (4.64) | (4.58) | |

| Current | 0.1360 | 0.0476 | 0.1240 | 0.1330 | 0.1230 |

| (0.65) | (0.43) | (0.59) | (0.64) | (0.59) | |

| Roa | 12.080 | −26.4400 *** | 13.5500 | 13.5700 | 13.9200 |

| (1.14) | (−4.73) | (1.28) | (1.28) | (1.31) | |

| Loss | −1.9660 | −1.3440 | −1.9450 | −1.8900 | −1.8660 |

| (−1.02) | (−1.32) | (−1.01) | (−0.98) | (−0.97) | |

| Btm | −9.11600 *** | 0.6050 | −9.2070 *** | −9.1500 *** | −9.1660 *** |

| (−11.97) | (1.50) | (−12.10) | (−12.02) | (−12.04) | |

| Growth | 0.3240 | −1.5100 *** | 0.4020 | 0.4090 | 0.3430 |

| (0.39) | (−3.42) | (0.48) | (0.49) | (0.41) | |

| Shrcr1 | −4.6790 * | −1.3990 | −4.7750 * | −4.6000 * | −4.6470 * |

| (−1.68) | (−0.95) | (−1.72) | (−1.65) | (−1.67) | |

| Indiretor | −32.7700 *** | −4.2130 | −31.7100 *** | −32.5400 *** | −32.2000 *** |

| (−4.41) | (−1.07) | (−4.28) | (−4.38) | (−4.34) | |

| Dual | −1.6680 * | 0.2270 | −1.5880 * | −1.6810 * | −1.7460 * |

| (−1.79) | (0.46) | (−1.71) | (−1.81) | (−1.87) | |

| Soe | −0.9290 | −2.9610 *** | −0.9970 | −0.7620 | −0.6600 |

| (−0.89) | (−5.36) | (−0.96) | (−0.73) | (−0.63) | |

| Age | 0.2180 *** | −0.0956 ** | 0.2300 *** | 0.2230 *** | 0.2190 *** |

| (2.93) | (−2.43) | (3.09) | (3.00) | (2.94) | |

| AI | 2.037 * | 0.6730 | 2.0110 * | 1.9990 * | 1.9820 * |

| (1.86) | (1.16) | (1.84) | (1.83) | (1.81) | |

| Big_10 | −1.5270 * | 0.0266 | −1.3890 * | −1.5290 * | −1.5330 * |

| (−1.86) | (0.06) | (−1.69) | (−1.86) | (−1.86) | |

| Switch | 1.5260 | 0.3360 | 1.5380 | 1.5070 | 1.5360 |

| (1.37) | (0.57) | (1.38) | (1.35) | (1.38) | |

| L_opinion | 0.2840 | 2.5220 ** | 0.1030 | 0.1420 | 0.1500 |

| (0.13) | (2.19) | (0.05) | (0.06) | (0.07) | |

| Loca | −4.2920 *** | −0.00746 | −3.9830 *** | −4.2910 *** | −4.2190 *** |

| (−5.05) | (−0.02) | (−4.77) | (−5.06) | (−4.97) | |

| Cons | 188.4000 *** | 115.3000 *** | 178.3000 *** | 181.9000 *** | 216.8000 *** |

| (16.57) | (19.20) | (15.50) | (15.63) | (11.47) | |

| Industry | control | control | control | control | control |

| Year | control | control | control | control | control |

| N | 7744 | 7744 | 7744 | 7744 | 7744 |

| Adj R2 | 0.246 | 0.039 | 0.246 | 0.246 | 0.246 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, B.; Zhou, Y.; Zhang, T.; Liu, Y. The Impact of Smog Pollution on Audit Quality: Evidence from China. Atmosphere 2021, 12, 1015. https://doi.org/10.3390/atmos12081015

Li B, Zhou Y, Zhang T, Liu Y. The Impact of Smog Pollution on Audit Quality: Evidence from China. Atmosphere. 2021; 12(8):1015. https://doi.org/10.3390/atmos12081015

Chicago/Turabian StyleLi, Bin, Ying Zhou, Tingyu Zhang, and Yang Liu. 2021. "The Impact of Smog Pollution on Audit Quality: Evidence from China" Atmosphere 12, no. 8: 1015. https://doi.org/10.3390/atmos12081015

APA StyleLi, B., Zhou, Y., Zhang, T., & Liu, Y. (2021). The Impact of Smog Pollution on Audit Quality: Evidence from China. Atmosphere, 12(8), 1015. https://doi.org/10.3390/atmos12081015