Abstract

This work, set in the context of the apparel industry, proposes an action-oriented disclosure tool to help solve the sustainability challenges of complex fast-fashion supply chains (SCs). In a search for effective disclosure, it focusses on actions towards sustainability instead of the measurements and indicators of its impacts. We applied qualitative and quantitative content analysis to the sustainability reporting of the world’s two largest fast-fashion companies in three phases. First, we searched for the challenges that the organisations report they are currently facing. Second, we introduced the United Nations’ Sustainable Development Goals (SDGs) framework to overcome the voluntary reporting drawback of ‘choosing what to disclose’, and revealed orphan issues. This broadened the scope from internal corporate challenges to issues impacting the ecosystems in which companies operate. Third, we analysed the reported sustainability actions and decomposed them into topics, instruments, and actors. The results showed that fast-fashion reporting has a broadly developed analysis base, but lacks action orientation. This has led us to propose the ‘Fast-Fashion Sustainability Scorecard’ as a universal disclosure framework that shifts the focus from (i) reporting towards action; (ii) financial performance towards sustainable value creation; and (iii) corporate boundaries towards value creation for the broader SC ecosystem.

1. Introduction

The textile and apparel industry, which ranks among the world’s most polluting sectors [1], has historically been among the first to enter less-developed countries due to its labour-intensive character [2]. This results in a highly globalised industry, with complex supply chains (SCs) shaped by the combination of transnational outsourcing and the relocation of activities by focal companies—those playing pivotal roles in the SC—with many SC actors (mainly upstream suppliers) located in developing countries [3,4]. Additionally, the characteristics of the fast-fashion business model—high volume, rapid lead times, and low prices [5]—adds criticality to the sustainability challenges associated with the sector [1]. Thus, fast-fashion SCs are potential vehicles for the development of upstream producers and the introduction of industrial improvements to local communities [2], but are also at risk of generating sustainability issues related to social and environmental breaches [6,7].

This situation, augmented by social pressures to enhance Corporate Social Responsibility (CSR), has forced fast-fashion companies to accelerate their search for sustainability—i.e., the confluence of the economic, social, and environmental dimensions, such that no dimension is compromised for the benefit of the others, as per Elkington’s triple bottom line (TBL) concept [8]. CSR is defined as “the responsibility of enterprises for their impacts on society” [9] (p. 6), and is particularly requested from:

- focal companies, due to their large size, global brands, media visibility, and reliance on demanding institutional investors based in developed countries; and/or

- industries with large economic, social, and environmental impacts [10,11,12].

This places retailers in fast-fashion SCs at the centre of the spotlight of social pressure.

The European Union (EU) points out that in order “to fully meet their corporate social responsibility, enterprises should have in place a process to integrate social, environmental, ethical, human rights, and consumer concerns into their business operations and core strategy in close collaboration with their stakeholders” [9] (p. 6). To this end, sustainability reporting is not only the most important accountability tool allowing stakeholders and companies to report their social and environmental risks and policies [13], but also a crucial one for decision makers balancing the TBL [14,15]. Therefore, CSR and sustainability reporting has grown considerably in the apparel and fast-fashion industry [15].

However, firms’ adoption of standards such as the Global Reporting Initiative (GRI) has increased alongside criticisms of the limitations of these standards in terms of actually enhancing sustainability in SCs [16]. Sustainability reporting has been broadly attacked as “greenwashing” [13,17], or corporate rhetoric lacking consistency between talk and action [18]. The primary interpretations for this apparent gap are paradoxical. On one hand, it has been argued that compliance with overly closed sustainability standards boils down to an annual “tick the box” ritual that ignores local and industry conditions [19]. On the other hand, standards that do not require firms to report concrete information about their actions and, thus, offer only vague assertions decoupled from business practices, have been criticised as too open [20].

All in all, the gap between sustainability reporting and sustainability practice is particularly worrisome in sectors that rely heavily on global SCs, as is the case in the fast-fashion industry. Furthermore, since apparel and fast-fashion SCs currently employ millions of workers—especially young women—worldwide, there is an urgent need to leverage their developing power for local producers, communities, and the environment, as well as reverse the negative impacts of their growth: that is, to create sustainable value within and beyond company and SC boundaries. This is the ultimate goal of this work, which relies on the potential of effective sustainability reporting. Specifically, we present a universal disclosure framework that aims to:

- Move beyond reporting towards action;

- Move beyond financial performance towards sustainable value creation; and

- Move beyond corporate boundaries towards value creation for the broader SC ecosystem.

By building on sustainable value creation and collective impact approaches, this integrative framework provides a common agenda for sustainability in the fast-fashion industry. To this end, we adopt the United Nations’ Sustainable Development Goals (SDGs) as the universally shared soft regulations that balance the three dimensions of TBL, uniting all countries, actors, and stakeholders—i.e., the broad SC ecosystem—around a common objective [21].

The article is structured as follows. We start by describing the structure of fast-fashion SCs and analysing the potential of the sustainable value creation and collective impact approaches to solve or leverage the sustainability challenges and opportunities of complex global SCs. We then discuss the limitations of mainstream reporting, and substantiate the potential utility of disclosure frameworks and practice-oriented and industry-relevant tools for sustainability. This discussion leads to our research objectives. In the Methods and Data Analysis section, we introduce the sample companies and their reporting instruments, and discuss the key concepts to be integrated into the proposed framework. We then explain the steps taken to carry out the content analysis. Subsequently, by building on the discussion of the findings, we present the ‘Fast-Fashion Sustainability Scorecard’ (SS) as the common agenda for sustainability in the fast-fashion industry. Finally, we outline the main conclusions and limitations of the study.

2. Literature Review

2.1. Complex SCs in the Fast-Fashion Industry

The fast-fashion industry, while endowed with enormous potential and responsibility related to the development of countries participating in its complex SCs, is also associated with high-risk activities along social and environmental dimensions. For example, workplaces and working conditions sometimes borderline human rights violations, and production methods often involve high levels of pollution and contamination [1,22,23].

The risk of fast-fashion activities is associated with the behaviour of both firms and customers [24]. Companies are compelled to adapt their processes and structures to survive in a market of immediate demands and cheap prices [25,26], which can involve endangering labour practices that violate human rights. Meanwhile, responsible environmental management requires the reduction of environmental impacts (e.g., boosting transportation emissions and reducing the use of water and water pollution) [26,27]. Customers support a SC ecosystem that encourages disposability, with the subsequent societal and environmental challenges [28].

Of the many definitions and formulas for fast-fashion [29], this paper follows the one proposed by Caro and Martínez-de-Albéniz [5], who describe fast-fashion as a specific business model that combines three elements: (i) quick responses; (ii) frequent assortment changes; and (iii) fashionable designs at affordable prices [5].

From the above, it follows that fast-fashion SCs tend to adopt the following structure, comprising two main types of actors and activities:

- Downstream activities: activities carried out by retailers acting as focal companies that are characterised by high competition (prices and speed), high volume, and high visibility.

- Upstream activities: activities carried out by suppliers following focal companies’ demands that are characterised by high dynamism (and pressure), high volume, labour intensiveness, social complexity, the geographical dispersion and fragmentation of production, high levels of pollution and contamination, and generally low profit margins.

The consequence of this dual structure is twofold. On one hand, the retailers (focal companies) lose direct control over upstream activities, while remaining fully responsible for their product/service lifecycles [11]. On the other hand, it results in frequent trade-off situations among the three dimensions of sustainability and the different actors of fast-fashion SCs, within and beyond corporate boundaries [24]. Using a case study of the fast-fashion retailer H&M, Shen [24] points out that these conflicts appear at each stage of the SC, “including material production, garment manufacturing, transportation/distribution, consumer education, and retailing” [24] (p. 6237). They may come from sourcing managers’ decisions to produce in countries with low levels of human well-being despite the higher carbon emissions [24], from product returns being part of the customer value strategy [30] or from the trade-offs between clean technology and technology investment [31], to cite only a few. Therefore, fast-fashion SCs’ focal companies will seek to manage the SCs and maximise the positive impacts of activities relating to the products they commercialise, while minimising (and ideally neutralising or even reversing) any negative effects for any related actor.

The situation in which (i) one individual company (focal company) is responsible for all the activities contributing to the product that the enterprise commercialises; and (ii) each individual company may belong to several SCs, leads us to explore sustainable value creation and collective impact approaches.

2.2. Fast-Fashion Industry Sustainable Value Creation and Collective Impact

The first element listed above relates to the asymmetry typical of fast-fashion SCs, in which the focal company is declared responsible for the whole set of activities and is assumed to be the strongest link (in terms of resources). This privileged position is a double-edged sword, since anything that happens in relation to a focal company’s products will be blamed on that enterprise. Who, then, is the weakest link? The answer to this question is not straightforward, and indicates that solving any SC challenge will benefit all of the ecosystem’s actors, which in turn get implicated in its solution. In this way, it demands a ‘sustainable value creation’ (‘co-creation’ or ‘shared value creation’) approach [32,33,34] where efforts are placed “on exploring how to create the value that benefits multiple stakeholders, including the environment and society, but not without sacrificing shareholders’ benefits.” [35] (p. 2). In line with Yang et al. [35], we put the focus on the entire SC. Therefore, in the context of fast-fashion, such sustainable value creation can be defined as the generation of value for all of the actors in the SC, the communities, and the environment in which the firm operates, without compromising the focal firm’s benefits.

The second element—that is, the fact that every company operating in the fast-fashion industry belongs to many different SCs—anticipates that different companies will share similar concerns, objectives, and actors. This gives meaning to our search for ‘collective impact’, which is defined as “the commitment of a group of important actors from different sectors [in our context: SCs] to a common agenda for solving a specific social problem” [36] (p. 36). We argue that there is no other way to reach the ambitious goal of sustainability. Even more, we can even expect synergetic effects of shared value and collective impact approaches: “to advance shared value efforts, therefore, businesses must foster and participate in multi-sector coalitions, and for that, they need a new framework. Governments, NGOs, companies, and community members all have essential roles to play, yet they work more often in opposition than in alignment.” [37] (p. 4).

2.3. From Sustainability Reporting to Effective Disclosure

Sustainability reporting standards seek to enhance SC sustainability, transparency, and value creation in practice. The Global Reporting Initiative (GRI), the most widely used sustainability reporting guidelines worldwide, states that “sustainability reporting helps organisations to set goals, measure performance, and manage change in order to make their operations more sustainable. A sustainability report conveys disclosures on an organisation’s impacts—be they positive or negative—on the environment, society, and the economy” [15] (p. 380). Modern sustainability reporting has evolved into Integrated Reporting (IR), which can be defined as “a concise communication about how an organization’s strategy, governance, performance, and prospects, in the context of its external environment, lead to the creation of value over the short, medium, and long term.” Its vision is to “align capital allocation and corporate behaviour to wider goals of financial stability and sustainable development.” [38]. Both GRI and IR adopt the United Nations’ Sustainable Development Goals (SDGs) as the universally shared soft regulations that balance the three dimensions of TBL, uniting all countries, actors and stakeholders—i.e., the broad SC ecosystem—around a common objective [21,38,39].

However, even the most recently developed IR initiatives are criticised for their inability to move beyond communication. IR has not yet shown its ability to effectively contribute to corporate sustainability [16], and this gap has led some researchers to brand the approach a failure [40].

Does this widespread scepticism concerning the potential of sustainability and integrated reporting mean that the effort to ensure its effectiveness is meaningless? The conventional assumption that CSR communication opposes CSR action, and that the talk–action gap hampers sustainability, has been challenged by the research tradition that regards communication as performative [41]. Christensen, Morsing, and Thyssen [42] argue that this gap has the potential to stimulate improvements in CSR. CSR statements reflect not only the current state of managerial practice, but also aspirations and visions for a (presumably) better future state. Schultz et al. [43] oppose the prevailing instrumental and political-normative views on CSR, and promote the communication view of CSR instead. This latter perspective argues that “CSR is a matter not only of legal liability, brand value, or social connectedness, but also of communicative connectedness between organisations, media, and stakeholders” [43] (p. 689). CSR derives from more than simply multiple social relations: it is communicatively constituted in complex and dynamic networks. Thus, responsibility is not achieved in corporate spheres separate from society, but rather, it is co-constructed in de-centralised networks where knowledge about the meaning and expectations of CSR is organised and negotiated.

We further argue that sustainability and integrated reporting is crippled by its origin in financial reporting, which is understood as a “detailed periodic account of a company’s activities, financial condition, and prospects that is made available to shareholders and investors” [44] (p. 178). Even in approaches integrating non-financial dimensions of performance, reporting is built on the concept of a company unilaterally producing and making information accessible about itself. In a networked society, however, revelations of new information about how companies consider ethical, social, and environmental impacts do not depend on views originating from instrumental corporate reports or consensual reporting standards, but rather, tend to emerge from the dialogue, conflict, or dissent of multiple voices. Along this line of thought, we integrate the concept of disclosure—that is, “the revelation of information that was previously secret or unknown” [44] (p. 178)—into the field of sustainability. Sustainability disclosure is effective to the extent that it reveals new information, regardless of origin, that provides incentives for action to the focal firm, other SC actors, stakeholders outside the SC, or stakeseekers—i.e., those beyond established stakeholders claiming to have a stake in a corporation’s decision making [45]. From this perspective, standards and frameworks are no longer considered just technical compliance tools; rather, they become agents of change, stimulating the questioning and constructive criticism of corporate practices [46].

2.4. Research Objectives

Thus, building on the sustainable value creation and collective impact approaches, and assuming that disclosure tools are agents of change, this paper argues that the complex problem of SC sustainability can only be tackled if a common agenda for the sector is co-constructed. Based on the discussion of CSR and sustainability literature, and on the insights from the previous experience of one of the authors as a practitioner in the fast-fashion industry, the ultimate purpose of the study—creating sustainable value through effective disclosure—is decoupled in a twofold objective:

Objective 1: To draw a comprehensive map of the sustainability challenges for fast-fashion SCs (Objective 1.a.) and analyse current fast-fashion industry actions in pursuit of sustainability (Objective 1.b.).

Objective 2: To propose a universal action-oriented tool for the fast-fashion industry that, with TBL disclosure, assists in creating sustainable value for the whole SC ecosystem.

This universal disclosure tool would constitute a common agenda towards sustainable value creation in the fast-fashion industry.

3. Methods and Data Analysis

This section begins with an introduction of the sample and the key elements and terms used in our analysis. Then, we explain the method of analysis and further develop the ad-hoc research design that we built on to reach our objectives.

3.1. Sample Description and Data Analysed

Acknowledging the role of focal companies as catalysts of sustainable value creation in global and complex SCs, this research focuses on the sustainability reports of the two leading fast-fashion retailers: Inditex and H&M [29]. This joint analysis represents a major study of the fast-fashion market.

3.1.1. Sample Selection: The Fast-Fashion Companies

Inditex is a fashion retailer that opened in 1963 as a small workshop making women’s clothing in A Coruña (Spain), where the company’s headquarters are still based. Today, Inditex operates in 88 countries (29 online) under eight commercial brands: Zara, Pull&Bear, Massimo Dutti, Bershka, Stradivarius, Oysho, Zara Home, and Uterqüe. In 2016, Inditex’s net sales were €23.3 billion [47].

Hennes & Mauritz AB (H&M), founded in 1947, is based in Sweden and currently operates in 64 markets (35 via e-commerce), offering fashion products from its seven brands: H&M, COS, Monki, Weekday, & Other Stories, Cheap Monday, and H&M Home. In 2016, it reported sales of 223 billion SEK (€23 billion), including value-added tax [48].

3.1.2. Inditex and H&M Sustainability and Integrated Reporting

Since sustainability reporting relies on companies’ willingness to share details of their performance and the initiatives used to achieve a balanced TBL, each company may use different mechanisms, “such as corporate web sites, reporting integrated with annual financial reporting, or stand-alone sustainability reports” [15] (p. 380). For example, since 2013, Inditex has followed an IR approach, including all sustainability information within its annual report, while H&M reports sustainability through a stand-alone document. Both communications include a materiality matrix. In sustainability and integrated reporting, materiality is “the principle that determines which relevant topics are sufficiently important that it is essential to report on them” [49] (p. 10), which considers the significance of their possible impacts from the reporting company’s point of view, as well as “the concerns expressed directly by stakeholders” [49] (p. 10). All of the identified issues (material issues) are positioned on the materiality matrix. Thus, the corpus of this study’s content analysis comprises the following:

- Annual report (Inditex; Supplementary Materials S1); and

- Sustainability report (H&M; Supplementary Materials S2).

We have analysed the latest reports available on the companies’ websites. The Inditex data belongs to its 2015 fiscal year (February 2015 to January 2016), and the H&M information belongs to its 2016 fiscal year (December 2015 to November 2016). The materiality matrices were included in each group’s report.

3.1.3. Sustainability Reporting Analysis—Key Elements

For the easier follow-up of the remaining of the paper, we explain the key elements from the sustainability and integrated reports, and the SDGs integrating our framework, before detailing the steps involved in pursuing our objectives.

- Reported Material Issues (RMIs): The points appearing on each company’s materiality matrix (i.e., the points that are sufficiently important to report).

- Common Material Issues (CMIs): The minimum number of material issues that summarise all of the RMIs in the fast-fashion retailers’ materiality matrices, and thus can be considered important for the broader fast-fashion ecosystem. It is possible for a CMI to relate to an RMI that appears in only one of the two matrices.

- Reported Actions towards Sustainability (RASs): The activities described in each company’s annual or sustainability report as having been implemented to tackle the RMIs.

- United Nations (UN) Sustainable Development Goals (SDGs) Framework: Since both Inditex and H&M have declared their alignment with, commitment, and contribution to the SDGs, we take them as the frame from which we have deductively derived the categories for the analysis of the materiality matrices. We chose the SDGs, as they represent a main framework toward new actions for those companies that aim to adopt new sustainability activities and practices (UN, 2015). Based on the descriptions of the 17 goals in the main document published by the UN [21], we set up the SDG framework (Table 1), which includes risk and opportunities around the SDGs. Those descriptions led us to define actions and practices that companies and other actors can adopt to contribute to SDGs, differentiating between risks (what need to be avoid) and opportunities (what should be developed/fostered). This produced 34 possible categories through which to frame the CMIs (Table 1).

Table 1. United Nations (UN) Sustainable Development Goals (SDGs) Framework.

Table 1. United Nations (UN) Sustainable Development Goals (SDGs) Framework.

3.2. Content Analysis and Research Process

Content analysis was chosen as the most appropriate method for the analysis of the data, which included corporate sustainability reports and their materiality matrices. Content analysis combines qualitative approaches, which require the interpretation of texts and documents, with quantitative analyses at levels determined by the researcher [50]. Content analysis can be broadly defined as “any methodological measurement applied to text (or other symbolic materials) for social science proposes” [50] (p. 546), and it is “the research method that is most commonly used to assess organizations’ social and environmental disclosures” [51] (p. 166). The content analysis process was supported by the specialised software NVivo 11 [52], which facilitated the desired research replicability and systematicity [53] and supported the quantitative data analysis.

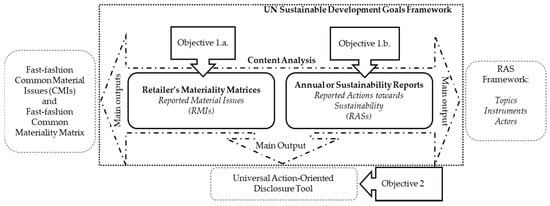

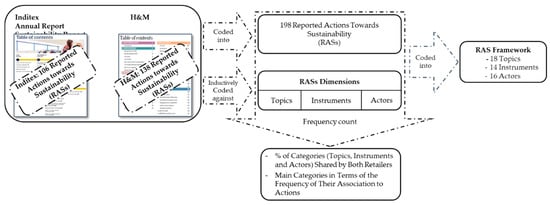

The ad-hoc research process (Figure 1) was designed to target the two sequential objectives of this study and included two separate codification processes. The first codification process (leading to Objective 1.a.) involved the analysis of the materiality matrices of the two fast-fashion retailers described in the previous subsection. The second codification process (leading to Objective 1.b.) involved the analysis of their annual or sustainability reports. We explain both codification processes below. Building on the results of the content analysis, an action-oriented disclosure tool (leading to Objective 2) is proposed.

Figure 1.

Research Process.

3.2.1. Objective 1.a. Retailer’s Materiality Matrices Analysis: Comprehensive Map of the Sustainability Challenges for Fast-Fashion SCs

- Subject of analysis: Inditex and H&M’s materiality matrices.

- Unit of analysis: RMIs.

- Content analysis process: We coded the RMIs in the materiality matrices of the two leading fast-fashion companies against the 34 SDGs categories in Table 1. Next, we grouped all of the RMIs into 27 CMIs, which are subsequently rated per their potential to impact SDGs and their relevance in the original materiality matrices. We finally performed cross-tabulation and frequency counts on the results from the previous analysis.

- Coding reliability: The first author performed the initial coding, and the results were discussed among the three researchers until agreement was reached for each coding. In the Results section, we illustrate with an example how the agreements were reached.

- Main outcome: CMIs and a fast-fashion common materiality matrix.

3.2.2. Objective 1.b. Annual and Sustainability Reports Analysis: Analysis of Current Fast-Fashion Industry Actions in Pursuit of Sustainability

- Subject of analysis: Inditex’s annual report and H&M’s sustainability report.

- Unit of analysis: RASs.

- Content analysis process: The annual or sustainability reports of the two retailers were analysed to identify significant RASs. We followed a qualitative codification process [54,55]. The reports were analysed carefully by following three levels of codification [56]. We did this analysis for each company separately. The first level of codification includes an inductive open coding analysis of first-order concepts, which includes the list of actions connected to sustainability reported by each company. The second level of codification includes second-order themes that joined the main similarities and differences between the two companies. Finally, the third level of codification resulted in three axial codes [56]. We finally performed cross-tabulation and frequency counts on the results from the previous analysis.

- Coding reliability: The first authors of this manuscript did the first two levels of coding, while the two main authors did the third level of codification by building the aggregate codes for the three final axial codes.

- Main outcome: Framework of RASs.

4. Results

This section describes in detail the process followed to achieve each objective, and the results of each phase.

4.1. Objective 1.a. Comprehensive Map of the Sustainability Challenges for Fast-Fashion SCs

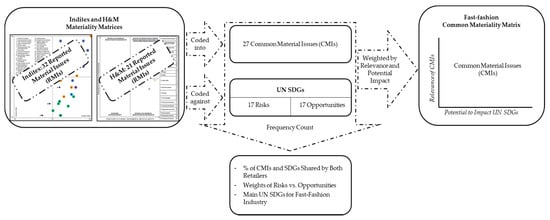

Figure 2 presents an outline of this phase.

Figure 2.

Materiality Matrices Content Analysis.

4.1.1. Materiality Matrices Coding

After coding all of the RMIs in the materiality matrices (32 from Inditex (Figure A1) and 21 from H&M (Figure A2)) against the 34 SDG categories (Table 1), we grouped them into 27 CMIs. The results are shown in Table 2, Column 1.

Table 2.

Fast-Fashion Common Material Issues (CMIs).

We take “Promote and Scale Innovation”, the first RMI in H&M’s materiality matrix, to illustrate this process. First, “Promote and Scale Innovation” was coded against all of the SDGs that it could potentially impact (i.e., the number of SDGs it could affect, as either risks or opportunities). As the three authors believe in the boundless contributions of promoting and scaling innovation to sustainable development, it was coded into the 17 SDG opportunities. However, we also consider that it could bring some associated risks. The most discussed risk was the potential of “Promote and Scale Innovation” to endanger the “Gender Equality Goal”. In line with the controversial debate where mixed evidence can be found in the literature (see for instance Cooper [57] and Hilbert [58]), the avoidance of labour practices and policies that foster all forms of discrimination against women that work at the company or across the company’s supply chain (Table 1) could not be ensured. We took a conservative approach to these discussions: if at least one (sound) reference could be provided in favour of an argument, it would be considered a possible scenario. Thus, “Promote and Scale Innovation” was coded into “Gender Equality Goal Risk”. Following this procedure, “Promote and Scale Innovation” was also coded into “Affordable and Clean Energy”; “Responsible Consumption and Production”, and “Climate Action” risks. Next, “Responsible Consumption and Production” was compared with similar RMIs that could be in a similar category (and hence conform a CMI). As no similar RMIs were found in the materiality matrices, we inductively developed the CMI “Innovation” that only contains the RMI “Promote and Scale Innovation”.

4.1.2. Building the Fast-Fashion Common Materiality Matrix

In a final step, we weighted the 27 CMIs to build the Fast-Fashion Common Materiality Matrix. Each CMI was rated according to (i) its relevance to the focal companies and stakeholders; and (ii) its potential to impact the SDGs:

- i.

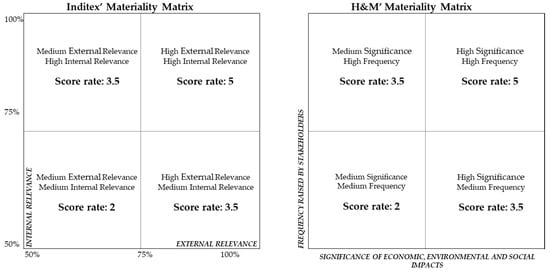

- The relevance to the focal companies and stakeholders was calculated based on the importance of each RMI that was condensed into each CMI in its original materiality matrix. Depending on the position of each RMI in the Inditex and H&M materiality matrices, we assigned a value, as shown in Figure 3.

Figure 3. Relevance of Reported Material Issues. Source: Own elaboration based on Inditex and H&M materiality matrices [47] (p. 161), [48] (p. 112).

Figure 3. Relevance of Reported Material Issues. Source: Own elaboration based on Inditex and H&M materiality matrices [47] (p. 161), [48] (p. 112).

The weighted final score per CMI appears in Table 3, Column 2. This final rate is determined by dividing the total score assigned to each CMI (i.e., the sum of the scores of the RMIs that conform the CMI) by the number of RMIs that it contains (i.e., two if the CMI is shared by the two retailers, and one otherwise).

Table 3.

Relevance of Common Material Issues and SDGs potentially impacted.

- ii.

- The potential to impact the SDGs appears in Table 3, Column 3, which shows the percentages of risks or opportunities possibly affected by each CMI.

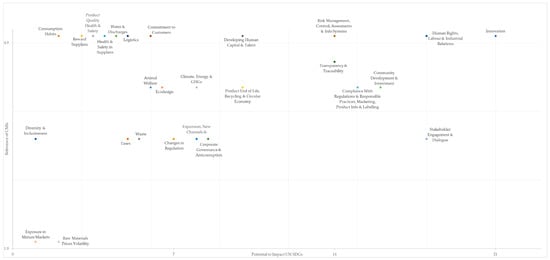

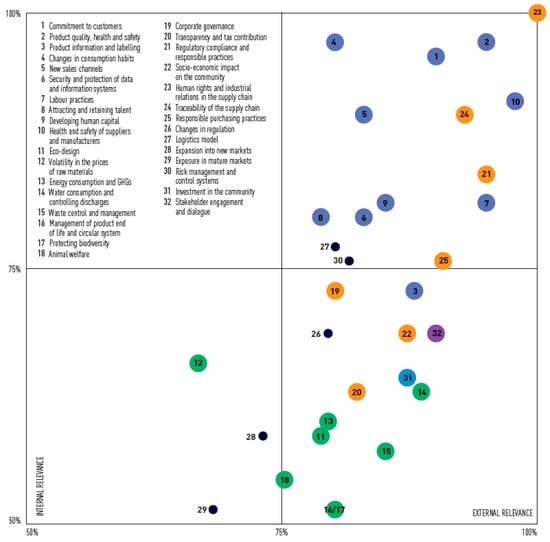

This process yielded the Fast-Fashion Common Materiality Matrix (Figure 4). The observations are the 27 CMIs within the matrix. The potential of each CMI to impact the SDGs (percentages in Table 3, Column 3) is shown by the <x> axis. Its relevance (coming from the Total Scores in Table 3, Column 2) is shown by the <y> axis. To facilitate the visualisation of all the observations, those with the same values on one axis have been moved to the closest possible position.

Figure 4.

Fast-Fashion Common Materiality Matrix.

Turning again to our empirical example of “Promote and Scale Innovation”, it appeared in the top right quadrant of the H&M materiality matrix, thus obtaining a score rate of 5 in Figure 3. This refers to the high significance of its impacts (as reported by H&M), and to being frequently raised by H&M’s stakeholders. As “Promote and Scale Innovation” is the unique RMI conforming to the CMI “Innovation”, the final score of “Innovation” is 5 (as shown in Table 3, Column 2). Regarding the SDGs it can impact, “Promote and Scale Innovation” was coded into the 17 SDG opportunities and four SDG risks (21 SDGs categories in total), which are directly translated into the CMI “Innovation”. The reading is that “Innovation” can potentially impact 61.7% (21) of the 100% (34) SDGs categories, as shown in Table 3, Column 3. The combination of the Final Score and the number of SDGs potentially impacted determined the position of “Innovation” in the Fast-Fashion Materiality Matrix (Figure 4).

4.1.3. Cross-Tabulation and Frequency Counts

Additionally, with the support of NVivo, we performed a quantitative evaluation of the above coding using cross-tabulations and frequency counts. Specifically, we analysed:

- the CMIs shared by the two retailers (i.e., the CMIs relating to a RMI in both materiality matrices);

- the connection between the SDGs and the CMIs; and

- the relation between risks and opportunities.

This step produced the following results:

Thus, our assumption concerning the need for a more universal disclosure framework is supported, and the SDGs appear to be an appropriate option.

- 3.

- Opportunities clearly surpass risks (72% vs. 28%). This reinforces, on one hand, the urgency of leveraging the industry development potential of the wider fast-fashion ecosystem, and on the other hand, indicates the need to go beyond voluntary reporting, which might be positively biased (Table 4, Columns 4 and 5).

Table 4. SDGs vs. Fast-Fashion RMIs and CMIs.

Furthermore, the top three SDG opportunities, as calculated through frequency counts (i.e., the goals into which the most individual RMIs were coded), were “Decent Work and Economic Growth” (Goal 8), “Responsible Consumption and Production” (Goal 12), and “Industry, Innovation and Infrastructure” (Goal 9). Remarkably, “Decent Work and Economic Growth” stood out as the industry’s most notable risk (Table 4, Column 6).

4.2. Objective 1.b.: Analysis of the Current Fast-Fashion Industry Actions in Pursuit of Sustainability

Figure 5 presents an outline of this phase.

Figure 5.

Annual and Sustainability Reports Content Analysis.

4.2.1. Annual and Sustainability Reports Coding

In this phase, we first conducted a qualitative content analysis of the Inditex annual report and the H&M sustainability report to identify the fast-fashion retailers’ main RASs. We identified 106 RASs from Inditex and 138 from H&M, and we condensed these into 198 primary RASs. Then, we interpreted and inductively coded these RASs into three core axial codes (RAS dimensions):

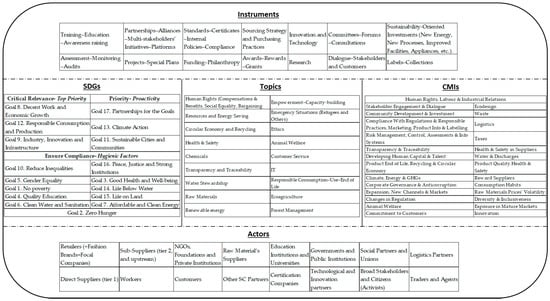

- Topics: The broad questions the RAS seeks to tackle.

- Instruments: Strategies, policies, and practices through which the RASs are implemented in practice.

- Actors involved: Each player (from the wider fast-fashion ecosystem) participating in the execution of the RASs.

4.2.2. Building RAS Framework

These three dimensions conform the “Reported Actions Towards Sustainability Framework” (Table 5). It shows 18 main topics and 14 instruments through which the actions towards sustainability are implemented in practice, with the active participation of 16 actor groups.

Table 5.

Reported Actions Towards Sustainability Framework.

4.2.3. Cross-Tabulation and Frequency Counts

Additionally, we carried out a quantitative evaluation of the above analysis. This involved:

- Comparing the results of the two companies’ reports; and

- Performing frequency counts of the three RSA dimensions over the coded actions. Although we are aware of the flaws associated with frequency measurements, which we will briefly underline in the limitations section, we consider this indicator relevant and appropriate for our analysis under the rationale of communication as performative, and that talk is a precursor to action [42]. It will follow that the more times something is reported, the closer it becomes to action (and the opposite holds true). Thus, it fits our goal of pushing sustainability reporting into action, and helping reveal orphan issues that are key for sustainable value creation.

From this evaluation, we outline the following findings:

- 1.

- The three dimensions indicate a high level of coincidence between the two studied retailers (72% of the topics, 100% of the instruments, and 87.5% of the actors are shared by the two companies’ RASs) (Table 6, Column 2). These results may suggest, on one hand, that the RSAs may constitute the skeleton of the action-oriented disclosure framework we seek. However, on the other hand, it might also suggest a possibility of orphan issues not being tackled by fast-fashion retailers due to their complexity or difficulty.

Table 6. Quantitative Evaluation of the Reported Actions towards Sustainability (RASs)—Topics, Instruments, and Actors.

- 2.

- The most frequently coded elements from each category (Table 6, Column 3) reveal that there is still an important gap between reporting and action, and that filling this gap may introduce trade-offs within the core business of fast-fashion.

- Topics. Of the 198 actions under analysis, only 1% dealt with Responsible Consumption and End of Life; 5.5% addressed Raw Materials Sustainability; and a rather low 6% had to do with Traceability and Transparency, a key aspect in complex textile SCs. The analysis also showed that the highest proportion of actions (35%) related to human rights (Compensations and Benefits, Social Equality, Bargaining Power, etc.), which was likely due to the seriousness of these topics, as well as related social pressure and media impact. The concern here is whether tackling only ‘tip-of-the-iceberg’ topics will truly solve sustainability issues in practice.

- Instruments. The analysis showed that most efforts go towards Training, Education, and Awareness Campaigns (28%) and Assessment and Monitoring (17%). Although these areas are needed as instruments of transversal support, they will not transform the industry in the short term. On the other hand, Sustainable Sourcing Strategies and Sustainability-Oriented Investments—approaches that could have more immediate and durable impacts—attracted only 5% and 2.5% of the actions reported, respectively.

- Actors. The frequency count showed that the core group of actors actively involved in the execution of the RASs was limited, for a high percentage of the actions, to retailers, suppliers (direct and indirect), workers, and NGOs. The positive reading of this result leaves room for hope, suggesting that solving sustainability issues is not impossible, but rather that many SC actors, stakeholders, and other stakeseekers have not yet begun to proactively collaborate on a solution. This interpretation supports our initial assumption concerning the urgency of building a shared disclosure framework capable of uniting the wider ecosystem’s actors around a common goal.

5. Action-Oriented Disclosure Tool Proposal

The results described in the previous section clearly reinforce the second objective of this paper:

Objective 2: To propose a universal action-oriented tool for the fast-fashion industry that assists TBL disclosure in creating sustainable value for the whole SC ecosystem.

Thus, building on the results of the content analysis and in combination with our discussion of the academic literature and the insights and experience of the fast-fashion practitioner, we worked towards constructing a disclosure tool that could ensure that:

- The CMIs were complemented with the absent material issues, i.e., those issues not currently being reported, but found to be key for the wider fast-fashion industry ecosystem.

- The RASs were contrasted with the SDGs and the CMIs to ensure that they:

- Targeted the relevant topics.

- Leveraged the most effective instruments.

- The key actors actively involved in the implementation of the RASs were shortlisted in order to identify and push all of the relevant ecosystem actors towards a common goal.

Our action-oriented disclosure tool aims to facilitate the revelation of information on sustainability actions to help SC actors, stakeholders, and stakeseekers understand how sustainability is managed in practice in complex SCs in the fast-fashion industry, as well as to promote actions towards improving such practices.

Weighing its pros and cons, we decided to root our tool in the architecture of the Balanced Score Card (BSC) and the Sustainability Balanced Score Card (SBSC) [59,60,61]. The rational was to leverage its benefits as an interactive system for integrated sustainability management [59,61] that “helps significantly to overcome the shortcomings of the often parallel approaches of environmental, social, and economic management systems implemented in the past” [59] (p. 283). We overcome its main critique of not contributing to sustainable development [62] with our focus on actions and the direct link to the SDGs.

To adapt the SBSC architecture to our objective, we moved the traditional business unit focus to a system level that analyses the fast-fashion SC’s wider ecosystem, thus taking a multiple stakeholders’ view [63]. Consequently, in order to not contradict the founders of the original BSC [61], we removed the word ‘balanced’ from our disclosure tool and named it the Fast-Fashion Sustainability Scorecard.

Our Fast-Fashion Sustainability Scorecard (Figure 6) is an action-oriented disclosure framework comprising the five analysed elements that were revealed to be key to fast-fashion sustainability:

Figure 6.

Fast-Fashion Sustainability Scorecard.

- SDGs: The universal framework containing the broader and widely accepted sustainability goals. The 17 goals are grouped into three levels of urgency (Critical Relevance, Priority, and Ensure Compliance) inspired by previous BSC and SBSC architectures [59,63] according to their relevance to the fast-fashion industry (extracted from our previous analysis; see Table 3). By forcing companies to report on all goals (to at least a minimum compliance level), we avoid the possibility of orphan issues or easy-to-solve problem biases.

- CMIs: The concrete issues already reported by fast-fashion retailers. By disclosing the CMIs in a common framework that relates them to the other categories in the Sustainability Scorecard, we make it difficult for disclosing companies to leave any issue unaddressed and prevent retailers from reporting on accessory issues.

- RAS Topics: The particular questions retailers report that they are already actively tackling. By disclosing these in a common framework and relating them to the other categories in the Sustainability Scorecard, we make it difficult for disclosing companies to act on irrelevant questions and easier for them to compare and team up with peers in the sector.

- RAS Instruments: The strategies, policies, and practices that retailers report that they are already using to cover their RMIs. Publicly disclosing these makes it more difficult for companies to communicate only green-washing practices or other mechanisms that are far from action. Such disclosure also facilitates a sector-wide comparison and analysis to identify the most useful instruments.

- Actors Involved: The players already reported as participating in the execution of the RASs. By shortlisting these actors, we call out all actors in the wider fast-fashion ecosystem and empower relevant partners to pursue a common goal.

The Fast-Fashion Sustainability Scorecard, which was conceived as a public and interactive tool, constitutes the co-constructed common agenda to foster sustainable value creation in the industry. Its main contributions are detailed in the following section.

6. Discussion and Final Conclusions

Current sustainability and integrated reporting frameworks have sought to develop common standards and measurement tools to allow companies to communicate their performance regarding material issues in relation to a range of indicators [15,64]. However, these tools’ potential for practice has yet to be fulfilled. Our ‘Fast-Fashion Sustainability Scorecard’ addresses the call of the communication view of CSR to construct an action-oriented, networked disclosure approach capable of enacting sustainable transformation in and beyond global and/or complex SCs [43].

Within the fast-fashion industry, too much time and effort and too many resources have been devoted to identifying impacts that are nearly identical for all industry actors and are universally clustered around the SDGs. With respect to the disclosure of relevant information that was “previously secret or unknown” [44] (p. 178), it is necessary to discontinue this expenditure and instead invest in solutions, which are currently very weak and fail to point to core business activities. Only by focussing our efforts on building and disclosing concrete actions towards sustainable supply chains, can we exploit sustainability-related challenges and opportunities. Those concrete actions can be contrasted and discussed among stakeholders and eventually become best practices. However, many of the actions that retailers report thus far are vague, uncertain, and projected too far into the future.

We agree on the potential of standards and frameworks as agents of change that stimulate the constructive criticism of corporate practices, but argue that in order to achieve effective sustainability disclosure with an impact beyond investors and organisations’ financial performance, it is more relevant to share timely and detailed information on how companies are tackling key industry-specific concerns. We apply the main lessons learnt from previous experience, our content analysis, and the literature to propose a new approach that does not change the universal framework for the impacts (SDGs). On the contrary: it explores concrete ways to manage the SDGs and compel companies to disclose them in ways that reveal and communicate how risks and opportunities are being tackled, which in turn allows these risks to be minimised and industry opportunities to be exploited. In sum, by focusing on actions instead of impacts and relating actions to SDGs and SC and non-SC actors, this paper builds a universal disclosure framework—the ‘Fast-Fashion Sustainability Scorecard’—which allows for interactive, timely, and dynamic information sharing, and offers several contributions that are discussed below in line with previous relevant literature.

It specifically covers the challenges of the fast-fashion industry (Figure 6), allowing for comparability and synergetic actions alongside contributions to the impact of SDGs. Fritz et al. defended a similar approach for the electronics and automotive industry. Their work suggested a list of 36 industry-specific-SDG related aspects that allow companies “to prioritise, measure, and monitor their own sustainability performance over time, as well as the one of their entire SC and to address stakeholders’ expectations” [64] (p. 600). The originality of our study is that, after identifying SDG-related aspects for the fast-fashion industry, we applied the same logic to the reported actions towards sustainability, thus helping disclosure take a step forward, towards practice. This orientation to immediate action distinguishes our research from Turker and Altuntas’ analysis of fast-fashion corporate reports, whose comprehensive conceptual map of Sustainable Supply Chain Management approaches remains at a theoretical level [27].

- It focusses on immediate solutions and actions, including the topics, instruments (strategies, policies, and practices), and actors needed to deploy them. For example, rather than publishing, with a lapse of one and a half years, the percentage of CO2 reductions coming from stores (impacts), the proposed ‘Fast-Fashion Sustainability Scorecard’ facilitates the identification and exchange of solutions to tackle concerns related to “climate, energy and greenhouse gases (GHG)” (instruments). In this way, we hope to contribute to the need for a “greater emphasis in disclosures related to what apparel brands are doing to find better ways of doing things”, as pointed out by Kozlowski et al. [15] (p. 392).

- It integrates the focal company with other relevant actors in the SC and beyond. For instance, it smoothens the process used to detect and team up with key partners within or outside the SC for each activity or issue to be tackled. This would have a direct contribution to sustainability, as anticipated in the works of Li et al. [26] and Hansen and Schaltegger [63]. In the first study, the authors verified collaborations between suppliers, industries, and NGOs as true enablers of SC sustainability. In the second, Li et al. point out that “collaboration among all stakeholders will normally guarantee an increase in the level of sustainable performance in the global marketplace.” [26] (p. 834).

- In trying to avoid the reporting company being the one that decides “which kind of information to disclose and how to deepen the narrative” [13] (p. 5), our scorecard facilitates the revelation of new information on the gap between sustainability goals and material issues, on one hand, and sustainability actions and instruments, on the other. In other words, it helps to identify orphan material issues so that they can be appropriately addressed. For instance, our analysis reveals a big gap between the potential of innovation in terms of sustainability and the number of actions reported on it. As shown in Figure 4, innovation is revealed as the most material issue in the Fast-Fashion Common Materiality Matrix. However, Table 6 reveals that only 3.54% of the analysed RASs turn to Innovation (under the ‘Innovation and Technology’ instrument) as the instrument for action. This opens up the floor for stakeholders’ demands to focal companies to align their sustainability investments (and disclosure) with the real needs and potential of the broader SC ecosystem. Additionally, following Fritz et al. [64] (p. 600), if the scorecard is pushed by SC actors different from the focal firm, “the risk to report only on good performance aspects would be even better addressed”.

- If retailers allow the scorecard to be interactive, all of the actors related to a particular goal or action can report on and monitor it in almost real-time. As pointed out by Yang et al. [35], fostering SC actors to exchange information would create sustainable value and improve business operations. In this way, the scorecard can also be used to control involuntary disclosure—“what stakeholders and stakeseekers disclose about an organisation” [65] (p. 30)—in two ways. The scorecard can firstly prevent the dissemination of inaccurate or false information from outside a company, and secondly, facilitate an awareness of and reactions to key concerns from other companies and related actors, stakeholders, and stakeseekers. Companies can use our scorecard as a hedging tool against false declarations, and as an opportunity pool for proactively integrating and canalizing external information from stakeholders and stakeseekers.

- It supports the social enforcement, thereby overcoming the critique of lack of normative enforcement that exists in current reporting norms [40]. When reporting on particular and tangible issues that people can understand and see, everyone becomes capable of auditing the degree of execution of an action and claiming responsibility. A simple but clear example is that, although customers might not be able to measure the CO2 in a store, they can report on (and act against) retailers irrationally using the air-conditioning system on shop floors at 15 °C in summer time.

- Finally, our scorecard broadens the grounds for finding best practices, by focussing not on CMIs, but rather on uncovering as many different actions (topics, instruments, and operative actors) as possible. The aim is to compel companies to ‘compete’ in the TBL, thereby adding goals such as ‘I want the best partners for sustainability’ or ‘I want the most comfortable climatisation systems for the workers in the factories’ to already existing goals, such as ‘I want the best IT system’ or ‘I want the highest turnover growth’.

- Businesses and SCs can use the ‘Fast-Fashion Sustainability Scorecard’ to understand and design corporate actions to help alleviate poverty, address climate change, protect human rights, or prevent worker exploitation, thereby encouraging the implementation and commitment of new actions, tools, and actors. UN Global Compact has called for the use of instruments that increase SDG adoption and implementation. The present scorecard addresses this call by aligning CMIs currently reported in fast-fashion with the 17 SDGs, and then examining sustainability-oriented business practices (i.e., real actions in cooperation with SC actors and stakeholders). As described before, our proposed ‘Fast-Fashion Sustainability Scorecard’ aims to transform compliance tools into agents of change [46].

This study’s main limitations concern its reliance on the analysis of contents voluntarily disseminated by companies (i.e., the materiality matrices and corporate reports). However, we believe that this methodological limitation should not negate the significance and potential utility of the proposed framework to foster sustainability in practice. On one hand, it could be argued that stakeholders’ views are indirectly reflected in the materiality matrix; on the other hand, our scorecard can help stakeseekers [45] uncover new information and position concrete new topics, actions, and instruments within the corporate agenda. In fact, voluntary reports are only the starting point for the ‘Fast-Fashion Sustainability Scorecard’ as a collaborative disclosure mechanism that aims to uncover the hidden and out-of-date information that is commonly used in traditional reporting.

Common to qualitative analysis that form the basis of coding processes, we acknowledge the potential limitation of the researcher’s previous experience, knowledge, and mindset leading the results [7,66], and tried to overcome it by discussing the findings of each step of the content analysis among the three authors of the paper.

Another methodological limitation involves the analysis focussed on frequencies, which could cause a bias towards simplicity and is short in regard to assessing the different magnitude of the discussed RSAs. To address this limitation, it would be desirable to critically analyse the importance of actions in relation to companies’ core business, main impacts, and performance, as well as compare the efforts and feasibility (in terms of resources) that each action would imply.

It is necessary to underline that, except for the SDGs, the list of entries under the four key elements of the ‘Fast-Fashion Sustainability Scorecard’ in Figure 6 is by no means exclusive. Even in the context of the content analysis of the two main fast-fashion retailers, this list may still be too restrictive. Thus, the lists appearing under the categories of CMIs, Topics, Instruments, and Actors aim to serve as a starting point for a dynamic tool co-constructed by the wider pool of fast-fashion ecosystem actors.

Regarding the validity of our scorecard, it would be desirable to expand the testing by replicating it in other sectors and/or through real case studies with primary data. Given the importance of collective impact, reinforced by the complete lack of any reported actions involving only one SC partner or stakeholder, a deep analysis of industry collaboration would truly complement this research.

Finally, given the nature and goals of the ‘Fast-Fashion Sustainability Scorecard’, research on digital and technological solutions supporting the framework’s potential is also needed.

Supplementary Materials

The following are available online at www.mdpi.com/2071-1050/9/12/2256/s1, S1: Inditex Annual Report 2015, S2: H&M Sustainability Report 2016.

Acknowledgments

We gratefully acknowledge the funding of this research by the University of Deusto through a FPI scholarship granted to the first author. The authors would like to show their gratitude to John Dumay and three anonymous reviewers for their enlightening comments and feedback on a previous version of this article.

Author Contributions

Sofia Garcia-Torres and Marta Rey-Garcia conceived and designed the research. Sofia Garcia-Torres, Marta Rey-Garcia and Laura Albareda-Vivo provided bibliographic material. Sofia Garcia-Torres performed the empirical analysis, which results and critical interpretation were discussed by Sofia Garcia-Torres, Marta Rey-Garcia and Laura Albareda-Vivo. Sofia Garcia-Torres wrote the paper and Marta Rey-Garcia and Laura Albareda-Vivo substantively revised it.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

Inditex’ Materiality Matrix.

Figure A2.

H&M’s Materiality Matrix.

References

- Shen, B.; Li, Q.; Dong, C.; Perry, P. Sustainability Issues in Textile and Apparel Supply Chains. Sustainability 2017, 9. [Google Scholar] [CrossRef]

- Gereffi, G.; Korzeniewicz, M. Commodity Chains and Global Capitalism; ABC-CLIO: Santa Barbara, CA, USA, 1994; ISBN 0-275-94573-1. [Google Scholar]

- Choi, T.Y.; Dooley, K.J.; Rungtusanatham, M. Supply networks and complex adaptive systems: Control versus emergence. J. Oper. Manag. 2001, 19, 351–366. [Google Scholar] [CrossRef]

- Tachizawa, E.M.; Wong, C.Y. Towards a theory of multi-tier sustainable supply chains: A systematic literature review. Supply Chain Manag. 2014, 19, 643–653. [Google Scholar] [CrossRef]

- Caro, F.; Martínez-de-Albéniz, V. Fast Fashion: Business Model Overview and Research Opportunities. In Retail Supply Chain Management: Quantitative Models and Empirical Studies; Agrawal, N., Smith, A.S., Eds.; Springer: Boston, MA, USA, 2015; pp. 237–264. ISBN 978-1-4899-7562-1. [Google Scholar]

- Krause, D.R.; Vachon, S.; Klassen, R.D. Special topic forum on Sustainable Supply Chain Management: Introduction and reflections on the role of purchasing management. J. Supply Chain Manag. 2009, 45, 18–25. [Google Scholar] [CrossRef]

- Seuring, S.; Müller, M. From a literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals with Forks: Triple Bottom Line 21st Century; Capstone Publishing Ltd.: Oxford, UK, 1997. [Google Scholar]

- European Commision. Corporate Social Responsibility: A New Definition, a New Agenda for Action 2011; European Commision: Brussels, Belgium, 2011. [Google Scholar]

- European Commision. Next Steps for a Sustainable European Future European Action for Sustainability 2016; European Commision: Brussels, Belgium, 2016. [Google Scholar]

- Ras, P.J.; Vermeulen, W.J.V.; Saalmink, S.L. Greening global product chains: Bridging barriers in the north-south cooperation. An exploratory study of possibilities for improvement in the product chains of table grape and wine connecting South Africa and The Netherlands. Prog. Ind. Ecol. 2007, 4, 401–417. [Google Scholar] [CrossRef]

- White, C.L.; Nielsen, A.E.; Valentini, C. CSR research in the apparel industry: A quantitative and qualitative review of existing literature. Corp. Soc. Responsib. Environ. Manag. 2017. [Google Scholar] [CrossRef]

- Truant, E.; Corazza, L.; Scagnelli, S.D. Sustainability and risk disclosure: An exploratory study on sustainability reports. Sustainability 2017, 9. [Google Scholar] [CrossRef]

- Integrated Reporting. The International <IR> Framework 2013; The International Integrated Reporting Council: London, UK, 2013; Available online: http://integratedreporting.org/wp-content/uploads/2013/12/13-12-08-THE-INTERNATIONAL-IR-FRAMEWORK-2-1.pdf (accessed on 5 December 2017).

- Kozlowski, A.; Searcy, C.; Bardecki, M. Corporate sustainability reporting in the apparel industry an analysis of indicators disclosed. Int. J. Product. Perform. Manag. 2015, 64, 377–397. [Google Scholar] [CrossRef]

- Stacchezzini, R.; Melloni, G.; Lai, A. Sustainability management and reporting: The role of integrated reporting for communicating corporate sustainability management. J. Clean. Prod. 2016, 136 Pt A, 102–110. [Google Scholar] [CrossRef]

- Kim, D.; Kim, S. Sustainable Supply Chain Based on News Articles and Sustainability Reports: Text Mining with Leximancer and DICTION. Sustainability 2017, 9. [Google Scholar] [CrossRef]

- Castelló, I.; Lozano, J.M. Searching for New Forms of Legitimacy through Corporate Responsibility Rhetoric. J. Bus. Ethics 2011, 100, 11–29. [Google Scholar] [CrossRef]

- Rasche, A. The limits of corporate responsibility standards. Bus. Ethics 2010, 19, 280–291. [Google Scholar] [CrossRef]

- Sethi, S.P.; Schepers, D.H. United Nations Global Compact: The Promise-Performance Gap. J. Bus. Ethics 2014, 122, 193–208. [Google Scholar] [CrossRef]

- UN General Assembly. Transforming Our World: The 2030 Agenda for Sustainable Development; UN General Assembly: New York, NY, USA, 2015. [Google Scholar]

- Arrigo, E. Corporate responsibility management in fast fashion companies: The Gap Inc. case. J. Fash. Mark. Manag. 2013, 17, 175–189. [Google Scholar] [CrossRef]

- Gereffi, G. International trade and industrial upgrading in the apparel commodity chain. J. Int. Econ. 1999, 48, 37–70. [Google Scholar] [CrossRef]

- Shen, B. Sustainable fashion supply chain: Lessons from H & M. Sustainability 2014, 6, 6236–6249. [Google Scholar] [CrossRef]

- Choi, T.-M.; Chiu, C.-H.; Govindan, K.; Yue, X. Sustainable fashion supply chain management: The European scenario. Eur. Manag. J. 2014, 32, 821–822. [Google Scholar] [CrossRef]

- Li, Y.; Zhao, X.; Shi, D.; Li, X. Governance of sustainable supply chains in the fast fashion industry. Eur. Manag. J. 2014, 32, 823–836. [Google Scholar] [CrossRef]

- Turker, D.; Altuntas, C. Sustainable supply chain management in the fast fashion industry: An analysis of corporate reports. Eur. Manag. J. 2014, 32, 837–849. [Google Scholar] [CrossRef]

- Joy, A.; Sherry, J.F., Jr.; Venkatesh, A.; Wang, J.; Chan, R. Fast fashion, sustainability, and the ethical appeal of luxury brands. Fash. Theory 2012, 16, 273–295. [Google Scholar] [CrossRef]

- Runfola, A.; Guercini, S. Fast fashion companies coping with internationalization: Driving the change or changing the model? J. Fash. Mark. Manag. 2013, 17, 190–205. [Google Scholar] [CrossRef]

- Shen, B.; Li, Q. Impacts of returning unsold products in retail outsourcing fashion supply chain: A sustainability analysis. Sustainability 2015, 7, 1172–1185. [Google Scholar] [CrossRef]

- Shen, B.; Ding, X.; Chen, L.; Chan, H.L. Low carbon supply chain with energy consumption constraints: Case studies from China’s textile industry and simple analytical model. Supply Chain Manag. 2017, 22, 258–269. [Google Scholar] [CrossRef]

- Hart, S.L.; Milstein, M.B.; Caggiano, J. Creating sustainable value. Acad. Manag. Exec. 2003, 17, 56–69. [Google Scholar] [CrossRef]

- Prahalad, C.K.; Ramaswamy, V. Co-creation experiences: The next practice in value creation. J. Interact. Mark. 2004, 18, 5–14. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating shared value. Harv. Bus. Rev. 2011, 89, 1–17. [Google Scholar]

- Yang, Y.; Han, H.; Lee, K.P. An Exploratory Study of the Mechanism of Sustainable Value Creation in the Luxury Fashion Industry. Sustainability 2017. [Google Scholar] [CrossRef]

- Kania, J.; Kramer, M. Collective Impact. Stanf. Soc. Innov. Rev. 2011, 9, 36–41. [Google Scholar]

- Kramer, M.R.; Pfitzer, M.W. The ecosystem of shared value. Harv. Bus. Rev. 2016, 94, 80–89. [Google Scholar]

- Integrated Reporting. Available online: http://www.webcitation.org/6uPaastj9 (accessed on 22 October 2017).

- Global Reporting Initiative. Available online: http://www.webcitation.org/6uPaibAHS (accessed on 22 October 2017).

- Flower, J. The international integrated reporting council: A story of failure. Crit. Perspect. Account. 2015, 27, 1–17. [Google Scholar] [CrossRef]

- Dumay, J.; Guthrie, J.; Farneti, F. GRI sustainability reporting guidelines for public and third sector organizations: A critical review. Public Manag. Rev. 2010, 12, 531–548. [Google Scholar] [CrossRef]

- Christensen, L.T.; Morsing, M.; Thyssen, O. CSR as aspirational talk. Organization 2013, 20, 372–393. [Google Scholar] [CrossRef]

- Schultz, F.; Castelló, I.; Morsing, M. The construction of corporate social responsibility in network societies: A communication view. J. Bus. Ethics 2013, 115, 681–692. [Google Scholar] [CrossRef]

- Dumay, J. A critical reflection on the future of intellectual capital: From reporting to disclosure. J. Intellect. Cap. 2016, 17, 168–184. [Google Scholar] [CrossRef]

- Holzer, B. Turning stakeseekers into stakeholders: A political coalition perspective on the politics of stakeholder influence. Bus. Soc. 2008, 47, 50–67. [Google Scholar] [CrossRef]

- Christensen, L.T.; Morsing, M.; Thyssen, O. License to Critique: A Communication Perspective on Sustainability Standards. Bus. Ethics Q. 2017, 27, 239–262. [Google Scholar] [CrossRef]

- Inditex. Available online: https://www.inditex.com/en/home (accessed on 22 October 2017).

- H&M. Available online: http://www2.hm.com/en_gb/index.html (accessed on 22 October 2017).

- Global Reporting Initiative (GRI). GRI 101: Foundation 2016; GRI: Amsterdam, The Netherlands, 2016. [Google Scholar]

- Seuring, S.; Gold, S. Conducting content-analysis based literature reviews in supply chain management. Supply Chain Manag. 2012, 17, 544–555. [Google Scholar] [CrossRef]

- Vourvachis, P.; Woodward, T. Content analysis in social and environmental reporting research: Trends and challenges. J. Appl. Account. Res. 2015, 16, 166–195. [Google Scholar] [CrossRef]

- Nvivo. Available online: https://www.qsrinternational.com (accessed on 22 October 2017).

- Bryman, A.; Bell, E. Business Research Methods; Oxford University Press: Oxford, UK, 2011. [Google Scholar]

- Saldaña, J. The Coding Manual for Qualitative Researchers; SAGE: Thousand Oaks, CA, USA, 2012. [Google Scholar]

- Corbin, J.M.; Strauss, A. Grounded theory research: Procedures, canons, and evaluative criteria. Qual. Sociol. 1990, 13, 3–21. [Google Scholar] [CrossRef]

- Gioia, D.A.; Corley, K.G.; Hamilton, A.L. Seeking Qualitative Rigor in Inductive Research: Notes on the Gioia Methodology. Organ. Res. Methods 2013, 16, 15–31. [Google Scholar] [CrossRef]

- Cooper, J. The digital divide: The special case of gender. J. Comput. Assist. Learn. 2006, 22, 320–334. [Google Scholar] [CrossRef]

- Hilbert, M. Digital gender divide or technologically empowered women in developing countries? A typical case of lies, damned lies, and statistics. Women’s Stud. Int. Forum. 2011, 34, 479–489. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard—Linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. Sustainability Balanced Scorecards and their Architectures: Irrelevant or Misunderstood? J. Bus. Ethics 2017. [Google Scholar] [CrossRef]

- Kaplan, R.S. Conceptual Foundations of the Balanced Scorecard. In Handbooks of Management Accounting Research; Elsevier: Amsterdam, The Netherlands, 2008; Volume 3, ISBN 9780080554501. [Google Scholar]

- Hahn, T.; Figge, F. Why Architecture Does Not Matter: On the Fallacy of Sustainability Balanced Scorecards. J. Bus. Ethics 2016. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. The Sustainability Balanced Scorecard: A Systematic Review of Architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Fritz, M.M.C.; Schöggl, J.-P.; Baumgartner, R.J. Selected sustainability aspects for supply chain data exchange: Towards a supply chain-wide sustainability assessment. J. Clean. Prod. 2017, 141, 587–607. [Google Scholar] [CrossRef]

- Dumay, J.; Guthrie, J. Involuntary disclosure of intellectual capital: Is it relevant? J. Intellect. Cap. 2017, 18, 29–44. [Google Scholar] [CrossRef]

- Köksal, D.; Strähle, J.; Müller, M.; Freise, M. Social sustainable supply chain management in the textile and apparel industry-a literature review. Sustainability 2017. [Google Scholar] [CrossRef]

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).