Abstract

Aviation is widely recognised as one of the most carbon-intensive modes of transport and among the most challenging sectors to decarbonise. The use of green hydrogen (H2) in airside operations can help reduce emissions from air transport. While the pace and scalability of technology development, including H2-powered and ground support equipment, will be key factors, other financial, regulatory, legal, organisational, behavioural, and societal issues must also be considered. This paper investigates the key opportunities and challenges of using H2 in the aviation industry through eleven semi-structured interviews and a virtual expert workshop (N = 37) with key aviation industry stakeholders and academia. The results indicate that, currently, decarbonisation of the aviation sector faces several challenges, including socio-technical, techno-economic, and socio-political challenges, with socio-technical challenges being the most prominent barrier. This study shows that decarbonisation will not occur until the UK government is ready to have all the required infrastructure and capacity in place. Governments can play a significant role in directing the necessary ‘push’ and ‘pull’ to develop and promote zero-carbon emission aircraft in the marketplace and ensure safe implementation.

1. Introduction

In 2018, aviation accounted for 7% of the UK’s total greenhouse gas emissions—an 88% increase since 1990—highlighting its growing environmental footprint. Without decisive action, this share could rise to 39% by 2050, as growth in air travel continues to outpace efficiency gains [1]. Although emissions temporarily fell by over 60% during the COVID-19 pandemic [2], passenger numbers have since rebounded to pre-pandemic levels, underscoring the urgent need for a sustained and systemic shift toward zero-emission aviation.

The UK aviation sector has set ambitious decarbonisation targets: a 15% reduction by 2030, 40% by 2040, and net-zero by 2050 [3]. Achieving these milestones requires a comprehensive overhaul—incorporating fuel efficiency improvements, widespread deployment of Sustainable Aviation Fuels (SAFs), and the commercialisation of electric and hydrogen-powered aircraft by the mid-2030s [4]. Yet, despite these commitments, the lack of a definitive roadmap reflects the scale of technological, regulatory, and infrastructural hurdles still to be addressed.

Decarbonising the aviation sector is widely acknowledged to be both technically challenging and financially demanding [5,6,7]. The UK government’s Hydrogen Strategy and the JET Zero initiative [8] aim to support this transition, aligning with similar efforts in countries like Germany, a European leader in hydrogen development [9]. Yet, aviation is a hard-to-abate sector, and the development and certification of zero-emission aircraft may take decades. As such, even with strong policy backing, current roadmaps risk delivering only partial decarbonisation, cutting emissions by just 50% by 2050.

Over half of the UK’s aviation emissions stem from international flights, emphasising the need for global coordination. While the UK has adopted the CORSIA framework launched by IATA in 2020 to offset emissions from international aviation, offsetting alone is insufficient for deep decarbonisation [10]. To meet its climate goals, the sector must not only overcome cost and technical barriers but also accelerate innovation timelines and invest in the infrastructure needed to make hydrogen and electric aviation viable at scale.

International aviation accounts for over half of the UK’s aviation emissions, reinforcing the necessity for global collaboration. The UK’s participation in CORSIA, launched by the International Air Transport Association in 2020, represents a step forward, but voluntary offsetting alone is insufficient for deep decarbonisation [10]. As one of Europe’s leaders in hydrogen strategy, the UK’s JET Zero initiative, launched in 2022, signals strong intent [8]. However, aviation remains a hard-to-abate sector, with long lead times for the development and certification of new technologies. Without accelerated action and cross-sectoral coordination, the current trajectory risks falling short, delivering only partial emissions cuts by mid-century.

Hydrogen (H2) is rapidly emerging as one of the most compelling solutions for decarbonising the aviation sector. As a clean and versatile energy carrier, hydrogen offers a strategic advantage by reducing reliance on fossil fuels, which remain heavily concentrated in geopolitically sensitive regions [11]. Unlike traditional fuels, hydrogen can be domestically produced using renewable energy sources, enhancing both energy security and supply resilience. Its growing appeal lies in its capacity to decarbonise hard-to-abate sectors—aviation being a prime example—where electrification alone is insufficient. Increasingly, countries such as the UK, Germany, Australia, Japan, and Chile, alongside global energy transition agencies and major industrial players, are positioning hydrogen at the centre of their climate strategies [12,13]. This widespread commitment underscores hydrogen’s potential not just as an alternative, but as a transformative force in the race to net zero.

Hydrogen (H2) has gained growing attention from both academics and policymakers as a promising energy carrier for decarbonising hard-to-abate sectors such as aviation, due to its potential environmental benefits and wide availability [14]. It is important to clarify, however, that H2 is not a primary energy source but an energy carrier, meaning it must be produced using another form of energy. This is particularly relevant given that over 90% of current global H2 supply is derived from fossil fuels, resulting in substantial carbon emissions depending on the production method [15]. Only a negligible portion comes from naturally occurring “white hydrogen” [16], which highlights the urgent need for scaling up green hydrogen, produced via electrolysis powered by renewable energy sources.

The environmental appeal of green hydrogen for aviation lies in its potential to achieve deep decarbonisation. When used as a propulsion fuel, green H2 offers significant climate impact reductions compared to conventional jet fuels [17]. Yet, a central constraint remains its cost, particularly the price of electricity, which is the dominant factor in the green H2 value chain [18]. Encouragingly, the IEA [19] forecasts that the rapid expansion of renewable energy capacity and anticipated electricity surpluses may reduce electricity costs by up to 10% in the coming decade, improving the long-term economic viability of green hydrogen projects.

Historically, the aviation and aerospace industries were early adopters of hydrogen technologies, with applications dating back to the 18th century, when hydrogen was first used in balloons, and later in various aerospace experiments [14,20]. Despite this long-standing interest, the full-scale viability of hydrogen propulsion for commercial aviation remains uncertain.

Much of the early research—from the 1980s to the early 2000s—focused on the engineering aspects of hydrogen propulsion systems, with limited attention paid to the broader infrastructure, economic, or regulatory implications [21]. While recent studies have renewed focus on the technical feasibility of hydrogen-powered aircraft, including fuel storage and propulsion systems [22,23,24], they often overlook the systemic challenges involved in deploying hydrogen across the aviation ecosystem.

Despite substantial research on the technical feasibility of hydrogen-powered aircraft—particularly in relation to propulsion systems and fuel cell technologies—the literature reveals a significant gap concerning the integration of hydrogen within airport inf restructure [25,26,27]. Recent literature underscores that H2-powered aviation is increasingly recognised as a critical policy and economic research priority in the pursuit of net-zero aviation transitions. Dua and Guzman [28] underscore the need for coordinated policy frameworks and economic strategies to support the integration of hydrogen technologies into the aviation sector. They emphasise the importance of aligning technological advancements with enabling policies to address implementation barriers. A more holistic approach is therefore needed to evaluate not only aircraft-level feasibility but also broader system-level requirements for a hydrogen-powered aviation future.

This paper aims to address this gap by providing a comprehensive overview of both the challenges and opportunities associated with H2 use in the aviation industry, grounded in empirical data. It goes beyond the existing literature by not only exploring infrastructural and operational barriers but also assessing the wider impact of H2 adoption on air transport demand and the overall aviation market. This approach offers a more integrated perspective, contributing valuable insights into the potential future landscape of hydrogen-powered aviation and its implications for the sector.

This paper presents findings from 11 semi-structured interviews and a virtual expert workshop involving 37 participants from the aviation industry, including airport operators, planners, power transmission and distribution network representatives, and academics.

The structure of this paper is as follows: Section 2 provides an overview of feasibility constraints as the analytical framework and evaluates existing barriers to aviation decarbonisation. Section 3 outlines the methodology, while Section 4 presents the findings. Section 5 discusses and concludes the study.

2. Materials and Methods

To delve into the perspectives of stakeholders within the aviation industry regarding the utilisation of H2 to fulfil air transport requirements and advance the decarbonization of the sector, we conducted eleven semi-structured interviews online between November and December 2021 with key stakeholders in the aviation industry. Online data collection became more noteworthy during the COVID-19 pandemic and has remained a popular approach for data collection due to its enhanced logistical efficiency and facilitation of diversity between participant groups to meet research needs [29].

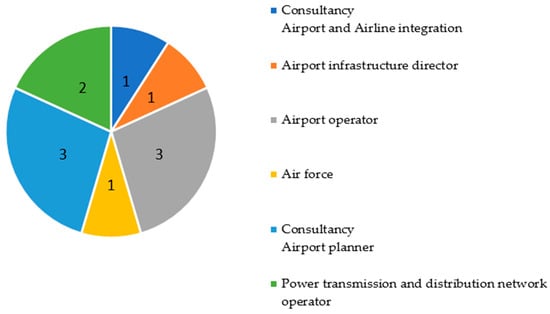

We selected our interviewees using a combination of purposive and snowball sampling methods. Our sample comprises actors who possess direct involvement and expertise within their respective domains, offering diverse perspectives crucial for understanding the complexities surrounding the integration of H2 technologies in the aviation sector. In total, our sample consisted of representatives from various sectors intimately involved in the aviation industry. This included three consultancy professionals specialising in airport planning, three individuals from airport operating companies, two experts from power transmission and distribution network operations, one consultant specialising in airport and airline integration, and one director with experience in the air force, as well as one director with experience in airport infrastructure management (Figure 1). Our sample comprised actors who possess direct involvement and expertise within their respective domains, offering diverse perspectives crucial for understanding the complexities surrounding the integration of H2 technologies in the aviation sector.

Figure 1.

Sectoral representation of interviewees (N = 11).

While our sample included a range of stakeholders across the aviation and energy sectors, we acknowledge the limited representation from commercial airlines and hydrogen producers, key actors in the implementation of hydrogen technologies. This limitation stems from the inherent challenges of engaging industry participants during the early stages of research. Although the number of expert semi-structured interviews conducted in this study is relatively small, it aligns with established practices in socio-technical energy transition research. In this field, qualitative methods such as semi-structured interviews and expert workshops are commonly employed to prioritise depth, diversity of perspectives, and stakeholder relevance over statistical generalizability [28,30,31,32]. The combined use of interviews (N = 11) and a virtual expert workshop (N = 37) reflects a robust approach for capturing both individual and collective.

The interview questions were formulated based on the research team’s extensive expertise in the aviation sector and decarbonisation, improved by a review of the literature on challenges pertinent to aviation decarbonisation and the utilisation of H2, encompassing both grey and academic sources. An interview guideline was structured to ensure consistency and facilitate comprehensive discussion across all interviews. Comprising 13 open-ended questions, the guideline centred on three key areas: (i) exploration of opportunities and barriers associated with H2 utilisation within the aviation sector, (ii) assessment of the impact of decarbonisation on air transport demand and the aviation market, and (iii) comprehension of the integration of H2 fuelling systems into airport infrastructure.

All interviews were audio-recorded and proceeded only with explicit consent from all interviewees. Following transcription, each interviewee was assigned a unique identifying code. The primary researcher reviewed each coded interview twice to ensure reliability. Subsequently, all coded transcripts were consolidated into a single file using descriptive coding software NVIVO 12 Plus, facilitating sorting and searching of transcripts based on keywords and content.

The insights gleaned from both the literature review and the semi-structured interviews were consolidated, considered, and validated during a virtual expert workshop held in January 2022, which saw the participation of 37 individuals. Among these participants were key stakeholders from the aviation industry, academia, and policymakers Fi. The primary objectives of the workshop were twofold: (i) to enrich the research agenda of the project pertaining to the implementation of green hydrogen in airside operations by incorporating input from a diverse array of stakeholders, and (ii) to elucidate the principal drivers and impediments associated with the development of low-carbon airport infrastructure, as perceived by experts in the field. All discussions during the workshop were accurately recorded, transcribed, and subsequently coded using NVIVO 12 Plus software.

Analytical Framework: Feasibility Constraints in the Aviation Sector

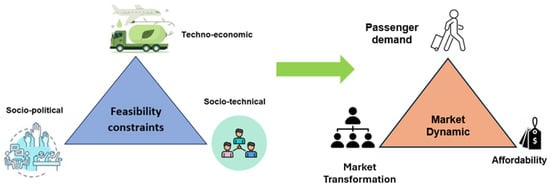

Feasibility constraints being faced in the global energy transition have been explored by ref. [33], and barriers facing to net-zero aviation sector have been investigated by Gordon et al. [34]. Drawing from existing research on barriers to decarbonisation of aviation [7,34], and insight on feasibility constraints from Mirzania et al. [32], we define feasibility constraints in the decarbonisation of aviation as the practical limitations and challenges that need to be addressed in transitioning towards greener and more sustainable practices within the aviation industry. These constraints encompass various aspects, including technical, economic, regulatory and policy, operational, and infrastructural considerations. In order to systematically understand feasibility constraints, these challenges can be categorised into three dimensions: socio-technical (technological feasibility, viability, and reliability), techno-economic (operational and infrastructure feasibility, and production costs), and socio-political (regulatory framework and policy support). As illustrated in Figure 2, these constraints directly shape key aspects of market dynamics—namely, passenger demand, market transformation, and affordability. Thus, decarbonisation pathways can be considered infeasible due to constraints in any of these dimensions [35].

Figure 2.

Aviation decarbonisation feasibility constraints framework.

According to the literature, one of the primary socio-technical barriers hindering the widespread adoption of H2 as a fuel is the necessity for substantial alterations to aircraft designs and refuelling systems to accommodate liquid H2 [21,36,37]. This requirement arises from the diverse propulsion technologies associated with H2, including H2 combustion engines and electrochemical conversion in fuel cells. These technologies necessitate modifications to aircraft structures to incorporate onboard H2 storage, impacting both the size and economics of flights [38]. Challenges related to the complexity of liquid hydrogen (LH2) refuelling and maintenance, as well as the need for innovative solutions for refuelling technologies, are highlighted by [21,27]. They may increase aircraft turnaround time and reduce utilisation. These challenges pose significant obstacles to achieving high LH2 aircraft performance and require addressing the vital interface with airport infrastructure. According to Verstraete [38], the fuselage of LH2-powered aircraft must be heavier and larger than conventional aircraft due to the need to house and withstand the hydrogen tank weight, impacting aerodynamic efficiency. Additionally, it has been noted by Verstraete [38] that storing LH2 above the passenger cabin increases energy consumption, further complicating aircraft design considerations.

Techno-economic barriers to the use of hydrogen in the aviation industry are primarily associated with high production costs. However, it is anticipated that scaling up hydrogen production and advancing the development of hydrogen-powered aircraft will lead to cost reductions over time. According to Chiaramonti et al. [39], H2 competes with conventional aviation fuels and sustainable aviation fuels (SAF) in terms of cost. Cerniauskas et al. [40] highlighted that carbon pricing mechanisms and government policies aimed at promoting renewable solutions, such as hydrogen development, are expected to influence the cost competitiveness of H2 solutions in the future. Creating a market for alternatives to fossil-based jet fuel, like H2, presents a substantial challenge. Currently, the majority of consumers have limited awareness and are hesitant to pay for these innovations [41].

Political challenges in the UK’s pursuit of the H2 strategy for the aviation industry encompass several key aspects. While there is a clear commitment from the UK government to support decarbonisation efforts within the aviation sector, there may be challenges in ensuring consistent and sustained political will over time. Political priorities and agendas may shift, potentially impacting the allocation of resources and support for H2 initiatives in the long term [42]. Furthermore, achieving net-zero emissions in the aviation sector requires coordination and cooperation not only domestically but also on a global scale. As the sector’s emissions are largely attributable to international flights, aligning policies and regulations with other countries poses a significant challenge. Negotiating international agreements and ensuring compliance with global standards for H2 adoption and infrastructure development may face political hurdles and require diplomatic effort [27,43].

In addition, while the establishment of the Jet Zero Council demonstrates a collaborative approach involving industry, government, and academia, maintaining effective coordination among diverse stakeholders with varying interests and priorities can be complex. Balancing the needs and perspectives of different stakeholders while driving forward decarbonisation initiatives may require adept political negotiation and consensus-building [8].

Existing literature on aviation decarbonisation primarily focuses on technological innovations and solutions, often neglecting socio-economic and political challenges. This gap highlights the importance of a more comprehensive approach that incorporates socio-technical and socio-political factors. To address this, the present study applies a feasibility constraints framework—encompassing socio-technical, techno-economic, and socio-political dimensions—to analyse empirical data and systematically identify the multifaceted challenges faced in the aviation sector. This approach enables a more holistic understanding of the barriers to implementing hydrogen technologies and achieving meaningful decarbonisation in the industry [32].

3. Results

This section presents the primary insights derived from both semi-structured interviews and workshops conducted to assess experts’ viewpoints on the integration of hydrogen (H2) to meet air transport requirements. These insights are analysed within the context of feasibility constraints developed [32]. Our interview findings illustrate the primary barriers hindering the widespread adoption of H2 within the aviation sector, shedding light on the associated techno-economic, socio-technical, and political challenges and opportunities. Furthermore, the findings outline the potential impact of implementing H2 technologies on air transport demand and the broader aviation market landscape.

3.1. Key Opportunities of Using H2-Powered Aircraft

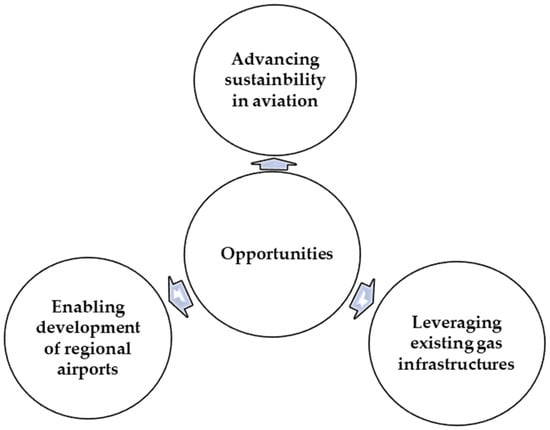

Most interviewees believe that using H2 can provide several opportunities across the aviation industry. Figure 3 summarises key opportunities of using H2-powered aircraft suggested by our interviewees.

Figure 3.

Key opportunities of using H2-powered aircraft.

The majority of our interviewees (seven out of eleven) identified green H2-powered aircraft as a potential alternative to significantly reduce the aviation industry’s environmental impact and make aviation more sustainable. Two interviewees highlighted the following:

“I think one of the major opportunities of use Hydrogen is that it reduces the carbon footprint and allows aviation to hit those carbon targets”(i9, airport planner consultant).

“In terms of the opportunities, the big one is it makes the aviation industry more sustainable. We truly believe aviation is a force for good, and we need no further than COVID-19 to show that. During COVID-19, the distribution of medical supplies around the world and vaccinations were all done by air transportation”(i5, airport operator).

H2 combustion emits no CO2 in flight [44]. Emissions of nitrogen oxide (NOx), which is potentially a more problematic greenhouse gas, can, however, be reduced between 50% and 80% with lean-mixture technology without sacrificing efficiency, and with fuel-cell propulsion systems, CO2 and NOx are eliminated.

Some of our interviewees highlighted that the emergence of zero-emission aircraft, H2-powered aircraft, can provide an opportunity for developing a regional airport that is currently not cost-effective. One of our interviewees stated:

“We foresee H2-powered aircraft leading to opportunities for smaller regional airports. So, project 9 or 19 seaters to be serving routes that currently can’t be served because of their cost level can potentially come into the market”(i2, airport operator).

In addition to these opportunities, our interviewees proposed that H2 offers the potential to leverage existing gas infrastructure. Several European countries are exploring the use of current gas pipelines for H2 transport, with pilot studies showing promising results. While studies indicate that H2 can reduce the fatigue life of pipelines, existing pipelines can still be repurposed for H2 if pressure levels are kept within reasonable limits and operational parameters are carefully managed [45]. Given H2’s compatibility with current gas systems, there is significant potential to repurpose existing infrastructure for hydrogen distribution and utilisation [46].

An airport and airline integration consultant expressed the following:

“A great advantage of hydrogen’s, it’s got a very high specific energy. Also, hydrogen can utilise existing infrastructure provided we know that like pipelines, but that we need to evolve the pipelines, and we need to update power stations, but we can reuse existing infrastructure and that that is far better than building a whole new one”(i3, airport and airline integration, consultant).

However, workshop participants highlighted that the potential for distributing H2 via existing gas pipeline infrastructure should be carefully examined in terms of purification, material compatibility, and emission losses.

According to [33], the expansion of H2 infrastructure will enable a variety of synergies with other energy offtakes at airports, such as ground support vehicles, airport heating, and electricity needs through fuel cells, which will aid in lowering the cost of H2 over other supply sources.

3.2. Constraints to the Use of H2 Across the Aviation Industry

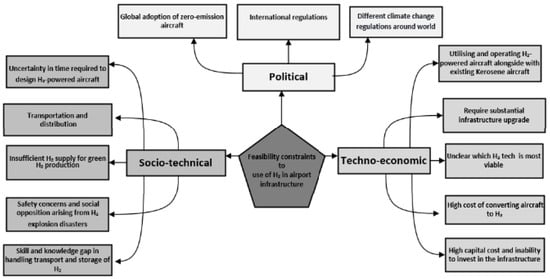

Despite all the opportunities, there are several socio-technical, techno-economic, and political constraints to implementing zero-carbon emission flight technologies across the aviation industry. Figure 4 provides a glimpse of all the identified constraints by our interviewees. The key challenges are discussed in more detail in the following sections.

Figure 4.

Key constraints faced in the use of H2 across the aviation industry.

3.2.1. Socio-Technical Constraints

As Figure 4 shows, socio-technical challenges are one of the most prominent obstacles in the adoption of H2-powered aircraft within the aviation sector. The subsequent sections delve deeper into these key socio-technical constraints for a comprehensive understanding.

Safety Concerns and Social Opposition Arising from H2 Explosion Disasters

Some of our interviewees suggested that there might be social opposition to adopting H2 aircraft due to past explosion disasters, such as the Hindenburg incident in 1937 This concern has also been noted by Baur et al. [47] and Iribarren et al. [48], who highlighted the primary public concern regarding H2 as the risk of H2 explosion. An airport planning consultant mentioned:

“There’s a history with the Hindenburg, blimp, those kinds of disasters that are still in people’s minds, certainly the older generation. However, I think technology has moved on significantly and is probably much safer now”(i3, airport and airline integration, consultant)

However, some workshop participants have challenged this perspective and emphasized that technologies have significantly improved in terms of safety compared to the past. The literature also indicates a positive overall willingness toward H2 solutions, with over 70% of the public expressing readiness to accept H2 as a solution [48,49]. Baur et al. [47] and Ricci et al. [49] highlighted that approximately 30% are even willing to pay an additional price or tax, if it is affordable, to support the developments.

However, it is recommended to increase efforts to raise public awareness regarding safety and qualifications for each H2 application as technology develops and is deployed. Creating public awareness through large demonstrations of climate impact and promoting the benefits of adopting zero-emission and H2-powered aircraft could play an important role in garnering public support. Our workshop participants suggested that displaying carbon emissions per trip on airline tickets would make passengers aware of their influence on the climate and their responsibility, thereby increasing their awareness of the benefits of zero-emission aircraft.

Insufficient Skills and Knowledge in Managing and Storing H2

Based on the responses from five interviewees, a notable technical impediment to the adoption of H2 across the aviation industry is the insufficient skills and knowledge regarding the management and storage of H2 within airport facilities. Two interviewees emphasised that while airports have some familiarity with battery usage and electrical systems, there remains a significant knowledge and skill gap in effectively handling H2. H2 is perceived as a volatile fuel source, leading to stability concerns and uncertainties compared to batteries.

“In terms of electricity, airports are much more comfortable with storage for the use of electricity than H2 because this skill is currently available in the airport industry. Still, handling H2 is a new skill which is the handling of gas such as Hydrogen. So, there is a skill gap that needs to be filled for Hydrogen”(i4, distribution network operator consultant).

“There’s still a lot of unknowns, so for hydrogen. Uh, there’s stability issues as it’s a quite a volatile fuel source. Whereas, on batteries we know and how is that going to work”(i8, airport operator).

Therefore, in order to prepare for the next generation of aviation, a holistic approach and new skillsets are required to fulfil the government targets of decarbonisation of the aviation industry.

Uncertainty Regarding Time Requirements to Design H2-Powered Aircraft

According to the literature, one of the primary barriers to the adoption of H2 in aviation is the necessity to modify aircraft design to accommodate LH2 as a fuel, as well as the integration of onboard H2 storage [21,36]. Our findings suggest that uncertainty regarding the time needed to redesign economically viable H2-powered aircraft could pose a challenge to their immediate adoption. Additionally, current limitations in H2 technology make it unsuitable for long-haul flights due to significant design changes required. An airport planner consultant highlighted:

“We don’t know how quickly the aircraft can be redesigned to meet new regulations, and the investment will be high for both the aircraft and the hydrogen infrastructure. That’s where conversion to hydrogen-powered aircraft becomes challenging as tourists are obviously used to paying a low cost for their flights“(i1, airport planner consultant).

Liquid H2-fuelled aircraft require less internal volume than those using gaseous hydrogen, offering greater design flexibility. However, this advantage is subject to design constraints: gaseous hydrogen demands heavy pressure vessels, whereas liquid hydrogen requires extensive insulation and potentially active cooling systems. If the fuel is stored in the fuselage rather than the wings—as is typical today—structural challenges arise. To maintain structural integrity against bending and vibrations caused by aerodynamic forces, the weight of the wings must be increased, since the beneficial inertia relief from fuel stored in the wings is lost [20,50]. Furthermore, the aircraft’s combustion chamber must be redesigned to efficiently burn hydrogen as a jet fuel. Compared to kerosene, hydrogen exhibits a faster flame speed, higher diffusivity, and a broader flammability range [20].

Operating H2-Powered Aircraft Alongside Existing Kerosene Aircraft

Integrating and operating H2-powered aircraft alongside existing kerosene-powered aircraft presents a significant socio-technical challenge. Additional safety measures are required to handle LH2 at extremely low temperatures [27], necessitating regulatory bodies to design new regulations enabling airport operators to manage a mixture of aircraft effectively and safely. The complexity is further highlighted by the need to accommodate various aircraft types, including H2, electric, drop-in sustainable aviation fuels (SAF), and traditional kerosene-powered aircraft. Arranging stands and coordinating arrival and departure schedules for each category poses logistical challenges. With the anticipated introduction of more aircraft with diverse propulsion systems, this complexity is expected to increase, demanding meticulous planning and coordination efforts from airport operators. An airport operator emphasised the magnitude of this challenge.

“It becomes challenging when you have a mixture of aircraft, so you could have aircraft that need hydrogen or aircraft that need electric or aircraft that need SAF or aircraft that need traditional kerosene. So, where do you locate that aircraft? When it comes on or that portfolio when they come on-site because today, you’d have a lot more choice in terms of putting and being and tactical around allocation stands. But in future you could undoubtedly have four or five other dimensions that need to be planned, as well as the actual arrival and departure times”(i5, airport operator).

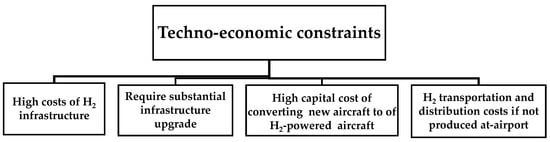

3.2.2. Techno-Economic Constraints

Several techno-economic constraints highlighted by our interviewees are outlined in Figure 5.

Figure 5.

Techno-economic challenges to the use of H2-powered aircraft in the aviation industry.

High Costs of H2 Infrastructure

The high capital costs of hydrogen infrastructure upgrades present a major barrier to airport readiness for H2-powered aviation. These costs cover the installation of refuelling stations, storage systems, and necessary modifications to existing facilities. The most significant challenge is the substantial upfront investment required.

According to FlyZero [43] liquid hydrogen requires about four times the volume of kerosene, demanding larger storage areas and cryogenic systems to maintain low temperatures. FlyZero [43] identifies three potential delivery methods: (1) road delivery by fuel tanker, (2) pipeline delivery with on-site liquefaction, and (3) on-site production via electrolysis and liquefaction. The third option is the least feasible due to high energy requirements and limited applicability to only small airports near renewable energy sources (Table 1).

Table 1.

Airport infrastructure options source [43].

Estimated infrastructure costs for hydrogen deployment vary significantly by airport size and infrastructure type. According to the FlyZero programme, more feasible options, such as hydrogen storage or liquefaction and storage, could cost up to GBP 1375 million for large airports, while smaller airports may still require GBP 325 million in investment. These figures highlight the importance of economies of scale. Without targeted funding and supportive policy, smaller and regional airports may struggle to participate in the hydrogen transition.

This challenge is further compounded by airports’ limited capacity to finance these necessary improvements, particularly given the prevailing economic downturn. The profound financial strains experienced by the aviation sector in the wake of the COVID-19 pandemic exacerbate this situation, amplifying the difficulty of securing funding for essential infrastructure enhancements. An airport planner consultant stated that:

“I believe one of the most significant challenges, particularly given the current economic climate, will be securing investment for infrastructure upgrades within the industry. This is especially pertinent considering the substantial financial impact the aviation sector has suffered over the past 18 months due to the COVID-19 pandemic”(i9, airport planner consultant).

High Capital for Designing and Operating Costs of H2-Powered Aircraft

Operating costs are a critical factor in the commercial aviation industry. H2-powered aircraft impact these costs in two main areas: the cost of the aircraft itself, including procurement and maintenance, and the cost of fuel. Both of these categories are associated with significant uncertainties. As a result, estimates of operating costs compared to similar kerosene-powered aircraft vary widely, ranging from a slight decrease to a potential increase of 50% or more depending on factors such as aircraft size, propulsion system, and technological assumptions [51,52].

To improve the efficiency of H2 combustion, aircraft engines must be redesigned to fully utilise H2’s unique properties [53]. A key techno-economic constraint, as highlighted by some interviewees, is the high cost associated with converting conventional aircraft to hydrogen-powered systems. This conversion involves redesigning the standard combustion chamber to efficiently burn H2 as jet fuel, a process that could increase manufacturing and maintenance costs by up to 25% [38,50].

Additionally, the long shelf life of existing aircraft poses another constraint. Since some aircraft are relatively new and expected to remain in service for the foreseeable future, transitioning them to H2-powered aircraft becomes more challenging due to the associated costs and support infrastructure requirements.

A Royal Air Force sustainability consultant expressed this challenge, stating the following:

“Going forward with our aircraft, given the fact that some of our aircraft are relatively still new, therefore their shelf life will carry on for the significant future and converting them to hydrogen will be a challenge because obviously it there tides up with support networks and the costs that go behind that”(i7, Royal air force sustainability consultant).

Furthermore, the high operational and running costs associated with H2-powered aircraft present a substantial techno-economic constraint for airports. The aircraft redesign requires changes to incorporate the H2 tanks that impact the aircraft’s length and weight, and consequently, the flight’s economics. This is particularly apparent for smaller aircraft with fewer seats, as charging fees based on weight or per passenger can significantly impact the airport’s business model and revenue generation. In addition, the varying passenger capacity of small aircraft affects the income level per flight, which can lead to fluctuations in revenue. Additionally, charging current taxes and airport visiting costs to small aircraft may result in disproportionately high airport costs, driving up seat prices and potentially making them less competitive. An airport operator emphasised:

“There is also an economic challenge, which is for us, as the airport is running and operation cost of hydrogen-powered aircraft. If you look at those smaller 19-seat aircraft and they are light, we charge on weight. And so, it impacts your business model it has nine or 19 seats. We charge per passenger, so the income level per flight will differ. And if we charge our current taxes and airport visiting costs to such small aircraft, the percentage of airport port costs will be too high. And we will drive up the seat price and make it competitive. So, there is also a challenge which needs to be overcome”(i2, airport operator).

In addition to the aforementioned techno-economic constraints, several interviewees have expressed uncertainty regarding the most viable and preferred technology between H2-fueled and electric-powered aircraft. This uncertainty could potentially serve as a barrier to the adoption of zero-carbon emission aircraft within the aviation industry. An airport infrastructure director emphasised:

“Currently, we don’t know if it’s going to be hydrogen or if the public will prefer electric-powered aircraft. So, that’s the risk right now as we don’t know which one will become the preferred mode of transport”(i11, airport infrastructure director).

Substantial Infrastructure Upgrade Requirement

The aviation industry continues to confront significant complications in employing H2 fuel for varied applications, as on a large scale, there is a shortage of suitable infrastructure [53]. Several interviewees have also highlighted that in order to integrate H2 systems into the airports, considerable infrastructure upgrades are required outside and inside airports, which ties in with significant capital cost requirements. This can potentially lead to several uncertainties around who should invest in infrastructure upgrades and what the future of the aviation industry will look like. Two interviewees mentioned:

“Hydrogen is still a great unknown. So, what infrastructure is needed for it? Because we do not know that today, but also who pays for what? What is the model going to? Because there is going to be quite a high infrastructure requirement if it goes, and when it so the uncertainty of what future?”(i5, airport operator)

“A lot of infrastructure changes are required for the integration of hydrogen, and that will cost a lot of money. Flying will become entirely different and just on cost alone unless or until we get those technologies up to where we want them and get them right”(i8, airport operator).

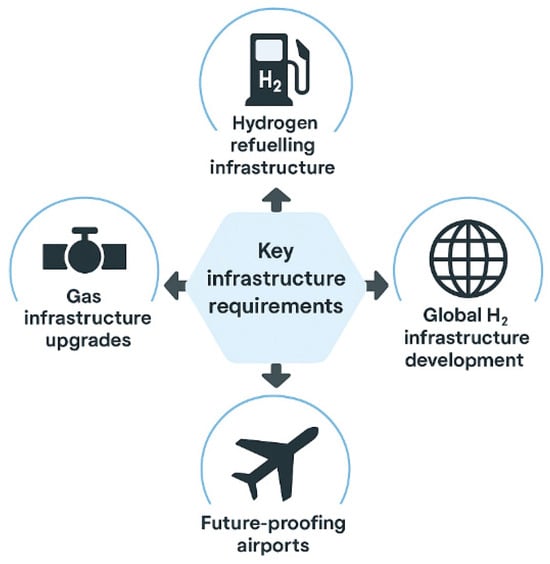

This study’s findings indicated that in order for H2-powered technology to be successfully integrated across the aviation industry, several key infrastructure upgrades are essential, which are summarised in Figure 6.

Figure 6.

Key infrastructure requirements based on interview results.

To accommodate the dispensing of H2 appropriately, new refuelling stations must be constructed, given that H2 is significantly more volatile than traditional kerosene. Due to the low volumetric density of LH2 and the potential for leakage during operation, LH2 refuelling tends to be slower than usual [54]. To ensure the economic viability of LH2 refuelling infrastructure at airports, it is essential that the scale of investment aligns with both the volume of hydrogen required and the specific needs of the airport. Larger airports, with higher hydrogen demands, necessitate proportionately greater investments in on-site infrastructure to support efficient refuelling operations.

A report developed by the World Economic Forum & McKinsey [55] highlights the substantial financial commitment needed for the transition to alternative, low-emission aircraft, estimating that between USD 700 billion and USD 1.7 trillion will be required across the value chain by 2050. Notably, 90% of this investment is projected to be allocated to off-airport infrastructure, including power generation and H2 liquefaction facilities.

Moreover, the report underscores that larger airports will require disproportionately higher investments in LH2 infrastructure compared to smaller ones [55]. However, some interviewees suggest that the size and scale of H2 fuelling systems at airports should be strategically determined based on the anticipated volume of H2 needed. For smaller volumes, more flexible delivery methods, such as tankers or modular systems, may be sufficient, offering a cost-effective solution without requiring extensive infrastructure. However, where there is a substantial demand for H2, it becomes necessary to invest in larger and more robust fuelling infrastructure to accommodate the scale effectively. Importantly, the decision to build and invest in H2 infrastructure should be driven by expected business needs and operational scale. This approach ensures that investments are sustainable over time, as installing high-cost infrastructure is only justifiable if the projected H2 requirements can offset the expenditure.

An airport operator elaborated:

“The size hydrogen fuelling systems, should depend on the hydrogen volume we could have. And then we can decide to have delivery through, tanker or some other smaller modular offerings, and where the scale wasn’t too much. Still, if we have a large scale of hydrogen requirements at an airport, we should probably look for more significant infrastructure. Also, we want to ensure that we’ve got an efficient and effective process, but we would only do it based on what we expected the business to be so that we wouldn’t put in massively expensive infrastructure. If actually, the scale of that operation wasn’t going to pay for it over time“(i5, airport operator).

In addition to establishing new refuelling stations, it is crucial to develop an optimal aircraft refuelling setup and standardised handling procedures to accommodate potentially longer refuelling periods. Safety concerns and procedural requirements during refuelling have the potential to impact the ability to conduct parallel operations during the turnaround process. Therefore, collaboration among relevant international authorities is essential to develop fuel infrastructures and safety regulations that ensure operational efficiency and adherence to safety standards [56].

To facilitate the adoption of H2-powered aircraft across the aviation industry, existing gas infrastructure, particularly the pipeline network, holds potential for reuse. However, it requires thorough evaluation and upgrading to meet H2 specifications. Traditional kerosene pipes may not suffice, necessitating alternative materials. Therefore, upgrading existing infrastructure, rather than constructing entirely new systems, is essential. This point is underscored by an airport and airline integration consultant:

“With hydrogen, we can use existing infrastructure. However, to meet hydrogen specifications existing gas infrastructure needs to be checked and upgraded because hydrogen is a much more volatile gas than traditional kerosene pipes. Traditional pipes might be too brittle or something, so we might need a different type of steel. It’s just upgrading as opposed to building a completely new infrastructure”(i3, airport and airline integration, consultant).

The findings from interviews underscore the necessity of future-proofing existing airports to accommodate new infrastructure and effectively manage operational changes. Implementing and developing new aircraft and infrastructure within airports entails significant operational adjustments, posing challenges for airport operators to navigate and enforce.

Another constraint highlighted in the interviews is that, despite the possibility of using existing gas infrastructure, significant upgrades or new constructions are necessary. Additionally, updated regulations and certifications from governments and regulatory bodies are required, posing a substantial challenge. Establishing suitable certifications and regulations to ensure the safe transit of H2 is essential. Moreover, achieving these upgrades and implementing new regulations within the desired timeframe is another major challenge. Therefore, to expedite the adoption and implementation of H2-powered aircraft, we need expedited certification of H2 aircraft and infrastructure. An airport planner consultant stated:

“So even though I mentioned that you can use existing gas infrastructure, but still, we have to build tracks or upgrade the pipeline network. In order to do this safely, that then leads to regulations need to be in place. And certifications for all of these, which all need to be updated by governments and regulatory bodies, so that’s a that’s a huge challenge. And I think the time scale that we want to achieve these things is another challenge”(i3, Airport and airline integration, consultant).

Furthermore, for global adoption of H2-powered aircraft, worldwide H2 infrastructure implementation is imperative to ensure uniformity in aircraft usage worldwide. An airport operator emphasised the importance of consistency in infrastructure and zero-emission aircraft across the globe, highlighting the need for standardised practices. To ensure smooth operations, it is essential that all airports adopt the same type of zero-emission infrastructure and aircraft, whether it is H2 or electricity. This consistency is crucial for maintaining a unified and efficient network worldwide. An airport operator stated that:

“We wouldn’t want one airport with hydrogen and another with electricity. So, we want the route between them to use the same aircraft. So, therefore, we require kind of a level of consistency in terms of infrastructure and zero-emission aircraft across the world”(i5, airport operator).

Workshop participants echoed this statement, stressing the importance of globally implemented infrastructures alongside consistent zero-emission aircraft and the incorporation of multiple H2 refuelling stations. They also anticipated that, initially, only a few airports may have H2 infrastructure, potentially leading to aircraft being stranded while awaiting H2 replenishment at airports lacking H2 refuelling authorisation. This could necessitate aircraft redirection, possibly leading to objections from airlines. Therefore, establishing worldwide H2 plants at or near major airports is crucial for refuelling purposes.

The Green H2 Supply Chain Issues

Ensuring sufficient infrastructure at airports alone will not resolve all the challenges associated with hydrogen aviation. A deeper, systemic issue lies within the current energy supply chain. Several interviewees emphasised a critical shortage in the hydrogen supply chain, particularly in the production of green hydrogen needed to meet the demands of the aviation sector. This shortage is not a minor obstacle; it constitutes a fundamental barrier to the widespread adoption of hydrogen as a viable aviation fuel. The lack of sufficient renewable energy to produce green hydrogen has been repeatedly highlighted [57].

Several interviewees raised critical concerns about hydrogen supply, citing insufficient production capacity, the dominance of grey hydrogen, and the urgent need to scale up green hydrogen infrastructure.

One consultant noted, “even if everyone wanted it today, there just isn’t enough [hydrogen] generated” (i3), while another highlighted, “we produce grey hydrogen… but it’s a dirty one” (i1).

Interviewees’ concerns about the current hydrogen supply align with the literature, highlighting substantial industry hurdles, particularly the insufficient production capacity and heavy reliance on grey hydrogen. The IEA’s Global Hydrogen Review 2024 confirms that low-emission hydrogen production remains far below what is needed for large-scale aviation decarbonisation, projecting that even by 2030, production may only reach 50 million metric tons—still inadequate to meet rising demand.

To address renewable energy shortages for low-emission hydrogen production, some workshop participants proposed leveraging nuclear power. However, water scarcity presents a significant barrier to pink hydrogen production, as both reactor cooling and electrolysis require substantial water resources—a concern particularly acute in water-scarce regions [58]. This issue was echoed by an airport operator, who emphasised the challenge of balancing hydrogen production with water availability.

“Another factor we must consider here is that the shortage of water resource for some parts of the world is a huge issue. And now, with global warming, we see some of the glaciers melting. God help us with that a little bit, but water supply is certainly something that can’t be ruled out”(i8, airport operator).

However, this concern may not be universally applicable and could be overstated in some contexts. For instance, in the UK, freshwater “non-revenue” leakage amounts to around 3 billion litres per day, representing roughly one-third of total potable water production. In energy terms, redirecting just 10% of this lost water could theoretically produce enough hydrogen to fully meet the UK’s aviation fuel demand if the fleet were converted to H2 propulsion [59,60].

H2 Transportation and Distribution Costs if Not Produced At-Airport

Another techno-economic challenge that could hinder the use of H2-powered aircraft across the aviation industry, especially for regional and smaller airports, is the high distribution cost. According to our participants, currently, small airfields are among the most expensive because the cost of transporting fuel is high. While larger players benefit from contracts that mitigate these costs, it is not anticipated that H2 will be significantly cheaper than kerosene. One interviewee highlighted that if the distribution cost issue is addressed, it would help envision future airports operating with H2-powered aircraft.

An airport operator mentioned:

“One of the challenges, if you look at hydrogen has to do with the distribution costs. And currently, we are the most expensive airfields in the [……], and because the kerosene has to be transported from [……], which is expensive for us. And, of course, the bigger players do not suffer that much because they have contracts. But in every discussion with new airlines, we emphasis this important point, as hydrogen will not be significantly cheaper than kerosene. So, if you can rule out the distribution elements, we see future airports where we operate with our hydrogen aircraft”(i2, airport operator).

H2 can be transported from its production site to the airport’s on-site storage facility via various means such as truck, ship, rail, or pipeline, with the chosen mode depending on the type of H2 storage [61]. While many large airports currently utilise hydrant refuelling systems for supplying kerosene to aircraft, the adoption of cryogenically insulated hydrant refuelling systems for LH2 could potentially reduce liquid-handling costs and alleviate congestion at airports in the future [21]. Regarding H2 transportation, the pipeline network responsible for H2 supply must be constructed with materials capable of withstanding H2 penetration and resisting embrittlement [53]. Additionally, while distribution across the network typically results in a 3% loss of H2, this loss may be minimised if the production facility is located nearby. Some workshop participants suggested that investigating the electrolysis of saltwater to produce H2 could be advantageous for airports situated near the coast.

3.3. Socio-Political Constraints

In addition to socio-technical and techno-economic constraints, several socio-political factors have been identified as significant barriers to the global adoption of zero-emission aircraft and the decarbonisation of the aviation industry (Figure 7).

Figure 7.

Key socio-political barriers to H2-powered aircraft across the aviation industry.

According to several interviewees, international rules and regulations present significant obstacles to decarbonising the aviation industry. For example, France’s Transport Code, updated in 2021, prohibits certain domestic flights where a rail alternative exists with a journey time of less than two and a half hours [62]. Similarly, Austria’s Climate Act [63] includes comparable restrictions, prioritising rail travel over short-haul flights when feasible. These regulations mandate that, where a viable train option exists, air travel for that route is not permitted. Some in the aviation industry argue that blocking short flights could hinder progress toward making aviation more sustainable, as expressed by a consultant specialising in airport and airline integration:

“In Europe, they’ve got a law which says in France and Austria, if there is an alternative option where you can take a train, you cannot fly that route. However, short-haul flights are the first place where aviation will become clean. So, by implementing these rules, blocking short flights means you’re hindering aviation’s ability to get clean”(i3, Airport and airline integration, consultant).

While such regulations may initially pose a barrier to the decarbonisation of short-haul flights, it is essential to note that short-haul flights only account for 24% of all flights, contributing to 3.8% of carbon emissions [64]. Therefore, focusing on decarbonising long-haul flights is crucial, as they constitute 6% of all flights and they contribute 47.6% to emissions [65].

It has been underscored by some of our interviewees that different countries have varying national climate change regulations and targets. Consequently, uncertainty surrounds the timing of the global transition and the commitment of airlines to this shift, as well as the pace at which they are willing to make changes. An airport planner consultant highlighted the potential barrier posed by divergent rules and regulations across countries regarding fuel types and management practices:

“We’ve all got different rules and regulations and that could become barrier going forward if one country has certain rules and regulations on certain types of fuel and how that’s managed and how that set up compared or lack of availability of that compared to another country, and that could then become a barrier. Also, I think it’s about how globally Governments and industry can influence those governments to make sure that it’s an aligned and it’s, uh, one global agenda. It sounds simple, however, that is the hardware. We can’t even get everyone to agree on the same entry and exit requirements”(i9, airport planner consultant).

Another political and regulatory constraint highlighted by several interviewees is the lack of a global commitment to decarbonisation, which contributes to the slow adoption of zero-emission aircraft. Achieving global and coordinated adoption of zero-carbon emission aircraft is crucial for fully decarbonising the aviation industry, but it presents significant challenges. A globally coordinated effort to deploy H2 technology would accelerate, streamline, and reduce the cost of transitioning to sustainable energy. Governments can play a significant role in guiding the necessary “push” and “pull” factors to develop and promote zero-carbon emission aircraft in the marketplace, ensuring their safe implementation [42]. Thus, governments should offer incentives to facilitate global investment in next-generation aircraft. An airport operator emphasised this point as well:

“Because of legacy systems, that change is so costly and challenging to do. That’s why things haven’t necessarily moved as fast as we would have liked within aviation. Also, we have to take into consideration that this is not just a local change; these airlines are global, so it’s a global change that needs to happen together. And that’s one of the big challenges, I believe”(i5, airport operator).

3.4. Implications of H2-Powered Aircraft on Market Dynamics

Experts in this study suggest that the aviation industry is unlikely to see significant shifts in demand for air transport solely based on changes to aircraft fuel. They argue that most travelers are largely indifferent to the type of fuel used in the aircraft and are unlikely to base their travel decisions on whether it is powered by electricity or H2. However, they anticipate a potential decrease in demand due to higher ticket prices resulting from necessary infrastructure upgrades and associated transition costs.

An airport operator commented:

“I don’t think people will be influenced by what’s driving the airplane. They’d be more concerned about will it get there? You know the majority of the population won’t be looking at whether it’s electric or Hydrogen”(i8, an airport operator).

An airport planner consultant said:

“That could result in increasing ticket prices, and travel or flying could then become something that only the rich can afford. I’m not saying this is the case, but it all depends on how much the infrastructure costs”(i9, airport planner consultant).

In addition, it has also been anticipated that the market share of the existing airlines would experience some significant changes. Some interviewees suggested that the decarbonisation across the aviation industry might result in small airlines going out of business, as some low-cost carriers cannot keep up with the cost of the transition.

An airport operator underlined:

“The markets may never bear the cost burden. The inefficiencies that come with these things right now. Because the cost would outweigh the profit, some don’t make it financially, and it will, uh, put current mid-sized airlines and regional carriage out of business if they don’t have a feeder line”(i2, airport operator).

It has also been predicated by some interviewees that there will be several start-ups across the airline industry to start the revolution of decarbonisation of aviation, which will be followed by established firms taking over these small firms. A distribution network operator consultant mentioned:

“I think there will be several start-ups, to start the revolution of Decarbonisation of Aviation, which will be followed by bigger firms taking over some of these smaller firms and taking their technology over there, but at the moment. But, because of disruption due to the pandemic, the aviation sector is pretty much open for new entrants because we see a lot of established firms going out of business, so this might be a good opportunity for new entrants as well”(i4, distribution network operator consultant).

4. Discussion

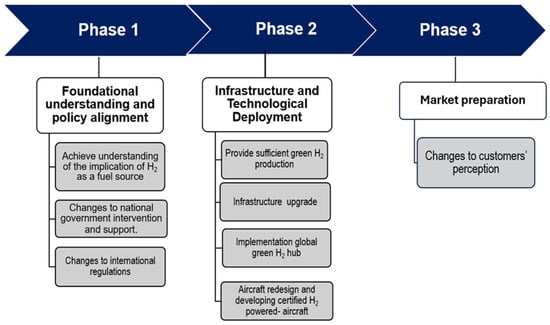

The findings of this research reveal that the current endeavour to decarbonise the aviation industry through H2 faces several constraints of socio-technical, techno-economic, political, and regulatory nature, with socio-technical challenges emerging as the most prominent barrier. Drawing from the insights gathered from both semi-structured interviews and expert workshops, this paper identifies key transformations necessary across the aviation sector to streamline and expedite the adoption of H2-powered aircraft (Figure 8).

Figure 8.

Top changes required to facilitate and accelerate decarbonisation.

As illustrated in Figure 8, a key catalyst for accelerating the adoption of H2-powered aircraft and achieving decarbonisation in the aviation sector is first establishing a clear understanding of the implications of hydrogen as a fuel source, supported by robust policy alignment. This foundational phase should be followed by infrastructure development and technological deployment. Finally, market preparation—including addressing customer perception and acceptance—will be essential to enable widespread adoption.

Nonetheless, this paper underscores that several unresolved concerns and queries persist among aviation industry experts regarding H2 infrastructure. For instance, a central question revolves around who bears the responsibility for financing this infrastructure upgrade—is it to be shouldered by aviation passengers or funded by the public through taxes, akin to the decarbonisation of electricity? However, several experts suggest that governments should establish a suitable framework to oversee and implement an infrastructure upgrade scheme.

Furthermore, our participants contend that the most crucial change needed to accelerate decarbonisation in aviation is enhanced government intervention and support. For instance, the UK government should introduce support schemes and incentives to stimulate investment in grid infrastructure upgrades. This point was also emphasised in a report published by hydrogeninaviation [66], which recommends that the government should provide the necessary support and incentives to help the sector overcome the challenges of transition costs and invest in new infrastructure.

This study identified a significant socio-technical barrier to the adoption of H2-powered aircraft: the UK’s insufficient renewable energy resources needed to produce green H2 at a scale that meets the aviation industry’s fuel demands. Although renewable energy capacity and water availability might be sufficient to support H2-powered aircraft on a global level [64], the UK’s limited renewable energy resources in certain regions may necessitate the import of H2 for specific airports. To accelerate decarbonisation through H2, the UK government must go beyond current strategies and ensure an adequate supply of clean H2 to meet all aviation fuel requirements. One effective approach could be to establish partnerships with other countries to import H2 for production needs. However, the UK’s H2 strategy remains heavily focused on domestic production, overlooking the potential benefits of international collaboration [67]. This is in stark contrast to countries like Germany, which aims to meet 50–70% of its H2 demand through imports by 2030 [68].

Given the recent geopolitical developments, such as the Ukraine conflict, the UK has even more reason to prioritise energy security and enhance its internal capacity to meet domestic H2 demand. Germany’s strategy of emphasising international partnerships has shown the potential to improve H2 supply security [68]. To expedite the decarbonisation of the aviation industry through H2, participants underscored the necessity for worldwide governmental collaboration to establish international regulatory standards for H2 infrastructure.

Accordingly, both global and UK-level strategies must be developed to cultivate a robust H2 market and encourage the entry of new players and private investors through regulatory flexibility. One effective approach could be the promotion of incentive schemes or the provision of discounts to aviation industry entities that adopt green technology. A precedent for such an initiative can be seen in the support provided for Sustainable Aviation Fuels (mainly biofuels) (SAF) by the Heathrow Airport. The Heathrow Airport has taken a proactive role in promoting SAF by offering financial incentives to airlines that use the fuel, effectively reducing their operational costs and encouraging broader adoption [69]. These incentives not only make alternative drop-in fuels more economically viable for airlines but also help to signal a market demand, which can drive further investment in SAF production and infrastructure. A similar model could be applied to H2, where airports, in collaboration with the government, could offer financial incentives such as reduced landing fees, tax breaks, or subsidies for airlines and aviation companies that commit to using green H2. Such measures would lower the financial barriers associated with the transition to H2-powered aircraft and stimulate the development of the necessary infrastructure, such as refuelling stations and H2 production facilities. Therefore, adopting a dual approach encompassing both internal capacity development and fostering international partnerships, akin to Germany’s strategy, can render the UK’s H2 economy more competitive and secure.

Several participants have emphasised the imperative for the UK aviation industry to attain a comprehensive understanding of the implications of H2 as a fuel source to expedite its adoption. Consequently, a holistic approach is deemed necessary, along with the cultivation of new skill sets to equip the next generation of aviation professionals and fulfil government targets for decarbonising the aviation sector. Airports should assume responsibility for educating the public about the future of aviation in their catchment area. One way is stakeholder consultations, which are crucial since they are the individuals who provide informed opinions about whether an airport should expand or not. Creating public awareness through large demonstrations of climate impact and promoting the benefits of adopting zero-emission aircraft can play a significant role in engaging the public.

Although the UK government has supported several innovation and demonstration projects, including H2GEAR, HyFlyer I and II, and FlyZero, ZeroAvia, CH2i, further advancements are necessary to facilitate the widespread adoption of H2-powered aircraft [70,71,72,73,74,75,76]. One critical area requiring acceleration is the development and certification of H2-powered aircraft. This process involves several stages, progressing through the Certification Readiness Levels (CRL). It starts with experimental design and safety regulator familiarisation (CRL 1), followed by in-house prototype certification trials and roadmap identification (CRL 5). The next steps involve testing and demonstrating the new prototype in an operational environment (CRL 9) and ensuring system compliance with regulatory standards and qualification requirements [77]. This development cycle is inherently complex and time-consuming [51], and must account for potential prototype failures, fatigue testing, and the stringent requirements of engine certification [76]. However, it has been argued that a newly built or redesigned aircraft cannot yet be fully tested or proven airworthy, as flight tests are not available at this stage.

The timeline for developing certified H2-powered aircraft is crucial, as it directly impacts the ability to overcome one of the key techno-economic barriers: uncertainty regarding the time and costs associated with redesigning aircraft to make them economically viable for H2 propulsion. Without clear timelines and delivery dates for certified H2-powered aircraft, it becomes difficult for stakeholders, including airlines, manufacturers, and regulators, to commit to the necessary investments and operational changes.

To effectively decarbonise the aviation sector, it is crucial that the UK government continues to support innovation and technology development through more demonstration projects. While the feasibility of achieving decarbonisation at both large and small airports remains uncertain, the majority of experts argue that the military is likely to be the first to achieve zero-carbon status. This is primarily due to their substantial financial resources and strong political backing. Additionally, cargo flights, with their significant heavy-lift requirements, present a unique opportunity to serve as testing grounds for emerging decarbonisation technologies.

However, it is not enough to focus solely on national initiatives or specific sectors within aviation. For true progress, international aviation rules and regulations must be standardised. The current fragmented regulatory landscape poses a significant barrier to the global decarbonisation of aviation [77]. Harmonised international regulations would not only facilitate the widespread adoption of H2 infrastructure and technology but would also ensure that H2 hubs can be implemented consistently across airports worldwide [78].

The argument for standardised global rules is compelling: without them, the industry risks creating isolated pockets of progress rather than achieving a cohesive global strategy. Decarbonisation cannot be effectively realised if airports and airlines operate under a patchwork of inconsistent regulations. Therefore, the UK’s national efforts must be complemented by active participation in the creation of international frameworks that enable the aviation industry to decarbonise on a global scale. This dual approach, national innovation coupled with international regulatory alignment, is essential for achieving meaningful and sustainable progress in aviation decarbonisation.

This study provides important qualitative insights into the socio-technical, socio-political, and infrastructural constraints shaping green hydrogen deployment in the aviation sector. However, it does not include quantitative modelling or detailed deployment scenario simulations. Addressing these gaps presents valuable opportunities for future research.

Future studies could focus on translating UK policy frameworks (e.g., Jet Zero, UK Hydrogen Strategy) into concrete deployment scenarios and aligning them with realistic technological timelines. This may involve pathway analyses and comparative evaluations with international strategies, such as Germany’s import-oriented hydrogen approach. Such work would offer a more actionable roadmap for stakeholders and strengthen policy coherence across infrastructure, technology, and governance domains.

Building on the conceptual framework developed in this study, future research should incorporate economic and environmental modelling—for example, comparing the costs of green hydrogen with Sustainable Aviation Fuels (SAF), and assessing their respective carbon savings. These analyses will help bridge the gap between systemic feasibility and market transformation by addressing key factors such as affordability, passenger demand, and infrastructure scalability. An integrated approach will enhance the policy relevance and practical applicability of the findings, supporting evidence-based decision-making in the transition toward low-carbon transport systems.

Additionally, future work should examine the regulatory and certification challenges associated with hydrogen aviation. This includes a detailed analysis of certification readiness levels (CRLs), the roles of key agencies such as the Civil Aviation Authority (CAA) and the European Union Aviation Safety Agency (EASA), and realistic timelines for technology certification. Investigating precedents from SAF certification and assessing the implications of certification bottlenecks for investment planning will be critical. A clearer understanding of these regulatory pathways and milestones will enable more robust planning and de-risking, ultimately supporting the scale-up of hydrogen technologies in aviation.

5. Conclusions

In conclusion, while the transition to H2-powered aircraft presents several significant barriers, there are also substantial opportunities and potential solutions. Overcoming socio-technical, techno-economic, and socio-political challenges through collaboration, investment, and regulatory alignment is essential for the successful decarbonisation of the aviation industry.

This paper identifies socio-technical barriers as among the most significant obstacles. These include safety concerns, skills shortages, and resource limitations. Despite technological advancements, public perception challenges persist, necessitating awareness campaigns. The lack of expertise in managing H2 and uncertainties in aircraft redesign further complicated adoption. Addressing supply shortages and operational complexities is crucial for integrating H2 aircraft effectively. Collaboration and public engagement are vital for overcoming these barriers and realising the potential of H2 technology in aviation.

Significant techno-economic challenges that must be addressed include the high capital costs for infrastructure upgrades, which are particularly burdensome in the context of ongoing economic pressures such as inflation, and the lingering effects of the COVID-19 pandemic. Converting conventional aircraft to H2-powered ones involves substantial redesign and costs and regulatory efforts, complicated by the long lifespan of existing aircraft. Significant infrastructure upgrades are necessary to support H2 systems within airports, requiring considerable investment, logistical planning, and certification compliance. This includes ensuring that safety regulations, certifications, and consistent global infrastructure standards are in place. Additionally, the high costs of H2 transportation and distribution, especially for smaller airports, present further economic challenges.

Socio-political interferences are to be considered, as, for example, those implemented by the French government by prohibiting domestic flights when viable train alternatives exist [79]. However, the number of flights affected remains relatively low. Divergent national climate regulations and the lack of global commitment to decarbonisation further complicate the transition. Achieving a coordinated global effort is crucial but challenging, requiring aligned regulations and incentives to facilitate investment in next-generation aircraft. Governments must play a pivotal role in guiding and promoting zero-carbon emission technologies to ensure safe and widespread implementation.

To achieve decarbonisation across the aviation industry, the UK government should implement the following recommendations, categorised by timeframe, to effectively address barriers and support the sector’s transition:

Short-term:

- Provide financial support for airports to facilitate near-term decarbonisation efforts.

- Develop policy support for renewable energy capacity dedicated to green hydrogen production.

- Offer incentives to encourage early investment in zero-emission aircraft and supporting technologies.

Medium-term:

- Implement support schemes for grid infrastructure upgrades, enabling integration of renewables and electrification.

- Establish a national framework to deliver infrastructure upgrade programmes, including fuelling, charging, and storage systems.

- Sustain investment incentives for zero-emission aircraft development to ensure long-term technology maturation and adoption.

Long-term:

- Accelerate and harmonise international certification pathways for zero-emission aircraft to streamline market entry.

Author Contributions

P.M.: conceptualisation, methodology, software, validation, formal analysis, investigation, resources, data curation, writing—original draft preparation, and visualisation. N.B.-O.: conceptualisation, writing—review and editing, project administration, and funding acquisition. H.R.: writing—review and editing, funding acquisition, and support in data curation. G.G.: conceptualisation, writing—review and editing, and funding acquisition. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the UK Department for Transport (DfT) and the Connected Places Catapult through the Transport Research and Innovation Grants (TRIG) programme as part of the Zero Emission Flight Infrastructure (ZEFI) initiative, under the project “Low Carbon Energy Demand Scenarios for Aviation (LOCESA)” in 2021 and the article processing charge (APC) was kindly waived by the journal Sustainability.

Institutional Review Board Statement

This study was conducted in accordance with the Declaration of Helsinki and approved by the Ethics Committee of Cranfield University through the CURES ethics service (protocol code CURES/14685/2021, approved in 2021.

Informed Consent Statement

Informed consent was obtained from all participants involved in the study.

Data Availability Statement

The data supporting this study are available from the authors upon request.

Acknowledgments

We would like to thank all participants who contributed to the interviews and workshops. Their valuable insights and support were essential to the development of this paper.

Conflicts of Interest

The authors declare no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| CORSIA | Carbon Offsetting and Reduction Scheme for International Aviation |

| H2 | Hydrogen |

| IATA | International Air Transport Association |

| IEA | International Energy Agency |

| IRENA | International Renewable Energy Agency |

| LH2 | Liquified Hydrogen |

| NOx | Nitrogen Oxide |

| SAFs | Sustainable Aviation Fuels |

References

- Howard, M.; Harris, P.; Mcclintock, W.; Milne, K.; Cole, J. The Case for the UK to Accelerate Zero Carbon Emission Air Travel. 2022. Available online: https://www.ati.org.uk/wp-content/uploads/2022/03/FZO-CST-PPL-0041-Case-for-the-UK-to-Accelerate-Zero-Carbon-Emission-Air-Travel.pdf (accessed on 3 June 2025).

- Climate Change Committee. The Sixth Carbon Budget—Aviation; Climate Change Committee: London, UK, 2020; p. 56. Available online: https://www.theccc.org.uk/publications (accessed on 6 March 2022).

- Sustainable Aviation. UK Aviation Industry Strengthens Commitment to Achieving Net Zero and Launches First Interim Decarbonisation Targets. Available online: https://www.sustainableaviation.co.uk/news/uk-aviation-industry-strengthens-commitment-to-achieving-net-zero-and-launches-first-interim-decarbonisation-targets/ (accessed on 18 August 2022).