Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature

Abstract

:1. Introduction

- (i)

- What is the current state of CSR disclosure research in developing countries?

- (ii)

- What are the widely explored dimensions of CSR disclosure in developing countries?

- (iii)

- What are the underpinning theories of CSR disclosure research in developing countries?

- (iv)

- What are the measurements of CSR disclosure and its dimensions in developing countries?

- (v)

- What are the determinants of CSR disclosure in developing countries?

- (vi)

- What are the motivations of CSR disclosure in developing countries?

- (vii)

- What are the avenues for future research?

2. Methodology

2.1. Defining the Research Questions

2.2. Establishing the Scope and Boundaries of the Review

2.3. Identification, Screening, and Selection of studies

2.4. Analysis and Synthesis

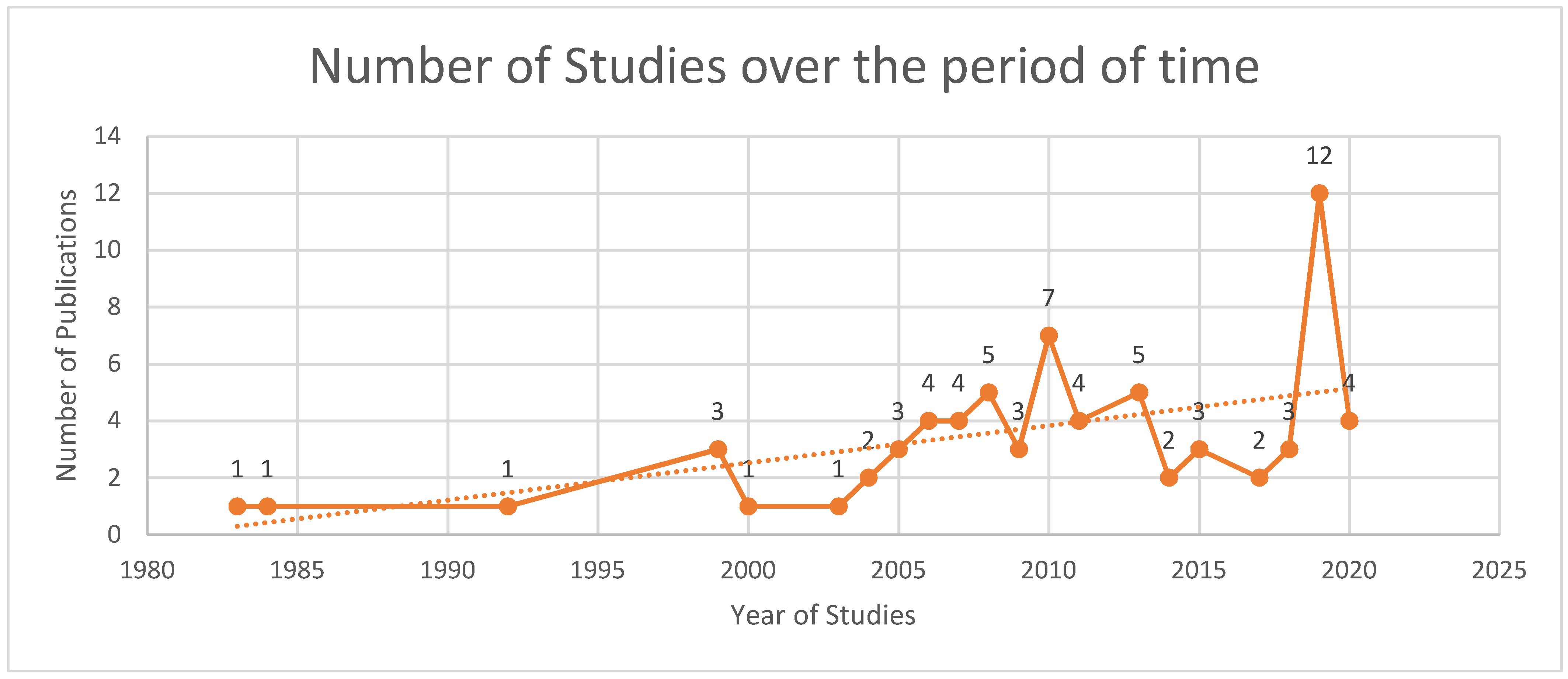

3. Review Results

3.1. Geographical Distribution of CSR Disclosure Studies

3.2. Theoretical Perspectives Used in CSR Disclosure Studies

3.3. CSR Disclosure and Its Dimensions

3.4. Measurement of CSR Disclosure and Its Dimensions

3.5. Drivers of CSR Disclosure

3.5.1. Internal Factors

3.5.2. External Environment

3.6. Motivations for CSR Disclosure

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Sr. # | Journal | Frequency | %Age |

|---|---|---|---|

| 1 | Journal of Business Ethics | 7 | 10% |

| 2 | Accounting, Auditing & Accountability Journal | 4 | 6% |

| 3 | Meditari Accountancy Research | 4 | 6% |

| 4 | Managerial Auditing Journal | 4 | 6% |

| 5 | Social Responsibility Journal | 4 | 6% |

| 6 | Corporate Social Responsibility and Environmental Management | 4 | 6% |

| 7 | International Journal of Islamic and Middle Eastern Finance and Management | 3 | 4% |

| 8 | Critical Perspectives on Accounting | 3 | 4% |

| 9 | Journal of Accounting in Emerging Economies | 2 | 3% |

| 10 | International Journal of Law and Management | 2 | 3% |

| 11 | The International Journal of Business in Society | 2 | 3% |

| 12 | Management Decision | 2 | 3% |

| 13 | Asian Review of Accounting | 2 | 3% |

| 14 | Accounting, Organizations and society | 2 | 3% |

| 15 | Pacific Accounting Review | 2 | 3% |

| 16 | Business Strategy and the Environment | 2 | 3% |

| 17 | Journal of Cleaner Production | 2 | 3% |

| 18 | International Journal of Law and Management | 1 | 1% |

| 19 | Critical Perspectives on International Business | 1 | 1% |

| 20 | Journal of Applied Accounting Research | 1 | 1% |

| 21 | Management Research Review | 1 | 1% |

| 22 | International Journal of Managerial Finance | 1 | 1% |

| 23 | Baltic Journal of Management | 1 | 1% |

| 24 | International Journal of Emerging Markets | 1 | 1% |

| 25 | International Journal of Accounting | 1 | 1% |

| 26 | The International Journal of Accounting | 1 | 1% |

| 27 | Journal of Accounting and Public Policy | 1 | 1% |

| 28 | Management & Accounting Review | 1 | 1% |

| 29 | Advances in International Accounting | 1 | 1% |

| 30 | Issues in Social and Environmental Accounting | 1 | 1% |

| 31 | The British Accounting Review | 1 | 1% |

| 32 | Business & Society | 1 | 1% |

| 33 | Qualitative Research in Accounting & Management | 1 | 1% |

| 34 | Corporate Governance | 1 | 1% |

| 35 | Corporate governance: an International Review | 1 | 1% |

| 36 | Gender in Management: An International Journal | 1 | 1% |

| 37 | Journal of Corporate Finance | 1 | 1% |

| Total | 71 | 100% |

References

- Wiseman, J. An evaluation of environmental disclosures made in corporate annual reports. Account. Organ. Soc. 1982, 7, 53–63. [Google Scholar] [CrossRef]

- Guthrie, J.; Parker, L.D. Corporate social reporting: A rebuttal of legitimacy theory. Account. Bus. Res. 1989, 19, 343–352. [Google Scholar] [CrossRef]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Fifka, M.S. Corporate Responsibility Reporting and its Determinants in Comparative Perspective—A Review of the Empirical Literature and a Meta-analysis. Bus. Strategy Environ. 2013, 22, 1–35. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Bus. Strategy Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Velte, P.; Stawinoga, M.; Lueg, R. Carbon performance and disclosure: A systematic review of governance-related determinants and financial consequences. J. Clean. Prod. 2020, 254, 120063. [Google Scholar] [CrossRef]

- Belal, A.R.; Momin, M. Corporate social reporting (CSR) in emerging economies: A review and future direction. Account. Emerg. Econ. 2009, 9, 119–143. [Google Scholar]

- Benlemlih, M.; Girerd-Potin, I. Corporate social responsibility and firm financial risk reduction: On the moderating role of the legal environment. J. Bus. Financ. Account. 2017, 44, 1137–1166. [Google Scholar] [CrossRef]

- Lagasio, V.; Cucari, N.; Åberg, C. How corporate social responsibility initiatives affect the choice of a bank: Empirical evidence of Italian context. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1348–1359. [Google Scholar] [CrossRef]

- Rodrigues, M.; Mendes, L. Mapping of the literature on social responsibility in the mining industry: A systematic literature review. J. Clean. Prod. 2018, 181, 88–101. [Google Scholar] [CrossRef]

- Velte, P. Environmental performance, carbon performance and earnings management: Empirical evidence for the European capital market. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 42–53. [Google Scholar] [CrossRef]

- Velte, P. Do CEO incentives and characteristics influence corporate social responsibility (CSR) and vice versa? A literature review. Soc. Responsib. J. 2019, 16, 1293–1323. [Google Scholar] [CrossRef]

- Zafar, M.B.; Sulaiman, A.A. Corporate social responsibility and Islamic banks: A systematic literature review. Manag. Rev. Q. 2019, 69, 159–206. [Google Scholar] [CrossRef] [Green Version]

- Broccardo, L.; Truant, E.; Zicari, A. Internal corporate sustainability drivers: What evidence from family firms? A literature review and research agenda. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1–18. [Google Scholar] [CrossRef] [Green Version]

- Denyer, D.; Tranfield, D. Producing a systematic review. In The Sage Handbook of Organizational Research Methods; SAGE: Los Angeles, CA, USA, 2009. [Google Scholar]

- Stumbitz, B.; Lewis, S.; Rouse, J. Maternity management in SMEs: A transdisciplinary review and research agenda. Int. J. Manag. Rev. 2018, 20, 500–522. [Google Scholar] [CrossRef]

- Zahoor, N.; Al-Tabbaa, O.; Khan, Z.; Wood, G. Collaboration and internationalization of SMEs: Insights and recommendations from a systematic review. Int. J. Manag. Rev. 2020, 22, 427–456. [Google Scholar] [CrossRef]

- Nijmeijer, K.J.; Fabbricotti, I.N.; Huijsman, R. Making franchising work: A framework based on a systematic review. Int. J. Manag. Rev. 2014, 16, 62–83. [Google Scholar] [CrossRef]

- Bailey, M.; Packer, H.; Schiller, L.; Tlusty, M.; Swartz, W. The role of corporate social responsibility in creating a Seussian world of seafood sustainability. Fish Fish. 2018, 19, 782–790. [Google Scholar] [CrossRef]

- Singh, D.; Ahuja, J. Corporate social reporting in India. Int. J. Account. 1983, 18, 151–169. [Google Scholar]

- Teoh, H.-Y.; Thong, G. Another look at corporate social responsibility and reporting: An empirical study in a developing country. Account. Organ. Soc. 1984, 9, 189–206. [Google Scholar] [CrossRef]

- Maheshwari, G. Corporate characteristics & social responsibility reporting. Asian Rev. Account. 1992, 1, 31–42. [Google Scholar]

- Williams, S.M. Voluntary environmental and social accounting disclosure practices in the Asia-Pacific region: An international empirical test of political economy theory. Int. J. Account. 1999, 34, 209–238. [Google Scholar] [CrossRef]

- De Villiers, C.J. Why do South African companies not report more environmental information when managers are so positive about this kind of reporting? Meditari Account. Res. 2003, 11, 11–23. [Google Scholar] [CrossRef] [Green Version]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Yusoff, H.; Lehman, G.; Nasir, N.M. Environmental engagements through the lens of disclosure practices: A Malaysian story. Asian Rev. Account. 2006, 14, 122–148. [Google Scholar] [CrossRef]

- Alsaeed, K. The association between firm-specific characteristics and disclosure: The case of Saudi Arabia. Manag. Audit. J. 2006, 21, 476–496. [Google Scholar] [CrossRef]

- Amran, A.; Devi, S.S. Corporate social reporting in Malaysia: A political theory perspective. Manag. Account. Rev. 2007, 6, 19–44. [Google Scholar]

- Kamla, R. Critically appreciating social accounting and reporting in the Arab MiddleEast: A postcolonial perspective. Adv. Int. Account. 2007, 20, 105–177. [Google Scholar] [CrossRef]

- Mirfazli, E. Corporate social responsibility (CSR) information disclosure by annual reports of public companies listed at Indonesia Stock Exchange (IDX). Int. J. Islamic Middle East. Financ. Manag. 2008, 1, 275–284. [Google Scholar] [CrossRef] [Green Version]

- Amran, A.; Devi, S.S. The impact of government and foreign affiliate influence on corporate social reporting: The case of Malaysia. Manag. Audit. J. 2008, 23, 386–404. [Google Scholar] [CrossRef]

- Wanderley, L.S.O.; Lucian, R.; Farache, F.; de Sousa Filho, J.M. CSR information disclosure on the web: A context-based approach analysing the influence of country of origin and industry sector. J. Bus. Ethics 2008, 82, 369–378. [Google Scholar] [CrossRef]

- Rizk, R.; Dixon, R.; Woodhead, A. Corporate social and environmental reporting: A survey of disclosure practices in Egypt. Soc. Responsib. J. 2008, 4, 306–323. [Google Scholar] [CrossRef]

- Mitchell, C.G.; Hill, T. Corporate social and environmental reporting and the impact of internal environmental policy in South Africa. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 48–60. [Google Scholar] [CrossRef]

- Sobhani, F.A.; Amran, A.; Zainuddin, Y. Revisiting the practices of corporate social and environmental disclosure in Bangladesh. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 167–183. [Google Scholar] [CrossRef]

- Hassan, A.; Harahap, S.S. Exploring corporate social responsibility disclosure: The case of Islamic banks. Int. J. Islamic Middle East. Financ. Manag. 2010, 3, 203–227. [Google Scholar] [CrossRef]

- Buniamin, S. The quantity and quality of environmental reporting in annual report of public listed companies in Malaysia. Issues Soc. Environ. Account. 2010, 4, 115–135. [Google Scholar] [CrossRef]

- Huang, C.-L.; Kung, F.-H. Drivers of Environmental Disclosure and Stakeholder Expectation: Evidence from Taiwan. J. Bus. Ethics 2010, 96, 435–451. [Google Scholar] [CrossRef]

- Habib, K. The effect of corporate governance elements on corporate social responsibility (CSR) reporting: Empirical evidence from private commercial banks of Bangladesh. Int. J. Law Manag. 2010, 52, 82–109. [Google Scholar]

- Saleh, M.; Zulkifli, N.; Muhamad, R. Corporate social responsibility disclosure and its relation on institutional ownership: Evidence from public listed companies in Malaysia. Manag. Audit. J. 2010, 25, 591–613. [Google Scholar] [CrossRef] [Green Version]

- McGuinness, P.B.; Vieito, J.P.; Wang, M. The role of board gender and foreign ownership in the CSR performance of Chinese listed firms. J. Corp. Financ. 2017, 42, 75–99. [Google Scholar] [CrossRef] [Green Version]

- Mahadeo, J.D.; Oogarah-Hanuman, V.; Soobaroyen, T. A longitudinal study of corporate social disclosures in a developing economy. J. Bus. Ethics 2011, 104, 545–558. [Google Scholar] [CrossRef]

- Abd Rahman, N.H.W.; Zain, M.M.; Al-Haj, N.H.Y.Y. CSR disclosures and its determinants: Evidence from Malaysian government link companies. Soc. Responsib. J. 2011, 7, 181–201. [Google Scholar] [CrossRef]

- Abu Qa’dan, M.B.; Suwaidan, M.S. Board composition, ownership structure and corporate social responsibility disclosure: The case of Jordan. Soc. Responsib. J. 2019, 15, 28–46. [Google Scholar] [CrossRef]

- Haji, A.A. Corporate social responsibility disclosures over time: Evidence from Malaysia. Manag. Audit. J. 2013, 28, 647–676. [Google Scholar] [CrossRef]

- Khan, A.; Muttakin, M.B.; Siddiqui, J. Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. J. Bus. Ethics 2013, 114, 207–223. [Google Scholar] [CrossRef]

- Chiu, T.-K.; Wang, Y.-H. Determinants of Social Disclosure Quality in Taiwan: An Application of Stakeholder Theory. J. Bus. Ethics 2015, 129, 379–398. [Google Scholar] [CrossRef]

- Laidroo, L.; Sokolova, M. International banks’ CSR disclosures after the 2008 crisis. Balt. J. Manag. 2015, 10, 270–294. [Google Scholar] [CrossRef]

- Khan, I.; Khan, I.; Saeed, B.B. Does board diversity affect quality of corporate social responsibility disclosure? Evidence from Pakistan. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1371–1381. [Google Scholar] [CrossRef]

- Aboud, A.; Diab, A. The impact of social, environmental and corporate governance disclosures on firm value: Evidence from Egypt. J. Account. Emerg. Econ. 2018, 8, 442–458. [Google Scholar] [CrossRef] [Green Version]

- Sun, W.; Zhao, C.; Wang, Y.; Cho, C.H. Corporate social responsibility disclosure and catering to investor sentiment in China. Manag. Decis. 2018, 56, 1917–1935. [Google Scholar] [CrossRef]

- Orazalin, N. Corporate governance and corporate social responsibility (CSR) disclosure in an emerging economy: Evidence from commercial banks of Kazakhstan. Corp. Governance Int. J. Bus. Soc. 2019, 19, 490–507. [Google Scholar] [CrossRef]

- Ramananda, D.; Atahau, A.D.R. Corporate social disclosure through social media: An exploratory study. J. Appl. Account. Res. 2019, 21, 265–281. [Google Scholar] [CrossRef]

- Khan, I.; Khan, I.; Senturk, I. Board diversity and quality of CSR disclosure: Evidence from Pakistan. Corp. Gov. Int. J. Bus. Soc. 2019, 19, 1187–1203. [Google Scholar] [CrossRef]

- Daas, A.; Alaraj, R. The complementarity between corporate social responsibility disclosure and institutional investor in Jordan. Int. J. Islam. Middle East. Finance Manag. 2019, 12, 191–215. [Google Scholar] [CrossRef]

- Hamrouni, A.; Uyar, A.; Boussaada, R. Are corporate social responsibility disclosures relevant for lenders? Empirical evidence from France. Manag. Decis. 2019, 58, 267–279. [Google Scholar] [CrossRef]

- Sekhon, A.K.; Kathuria, L.M. Analysing the impact of corporate social responsibility on corporate financial performance: Evidence from top Indian firms. Corp. Gov. Int. J. Bus. Soc. 2019, 20, 143–157. [Google Scholar]

- Acar, M.; Temiz, H. Empirical analysis on corporate environmental performance and environmental disclosure in an emerging market context: Socio-political theories versus economics disclosure theories. Int. J. Emerg. Mark. 2020, 15, 1061–1082. [Google Scholar] [CrossRef]

- Sorour, M.K.; Shrives, P.J.; El-Sakhawy, A.A.; Soobaroyen, T. Exploring the evolving motives underlying corporate social responsibility (CSR) disclosures in developing countries: The case of “political CSR” reporting. Account. Audit. Account. J. 2020, 34, 1051–1079. [Google Scholar] [CrossRef]

- Bhatia, A.; Makkar, B. Stage of development of a country and CSR disclosure–the latent driving forces. Int. J. Law Manag. 2020, 62, 467–493. [Google Scholar] [CrossRef]

- Zamir, F.; Shailer, G.; Saeed, A. Do corporate social responsibility disclosures influence investment efficiency in the emerging markets of Asia? Int. J. Manag. Financ. 2020, 18, 28–48. [Google Scholar] [CrossRef]

- Maama, H. Institutional environment and environmental, social and governance accounting among banks in West Africa. Meditari Account. Res. 2020, 29, 1314–1336. [Google Scholar] [CrossRef]

- Ali, W.; Frynas, J.G. The role of normative CSR-promoting institutions in stimulating CSR disclosures in developing countries. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 373–390. [Google Scholar] [CrossRef]

- Belal, A.R.; Cooper, S. The absence of corporate social responsibility reporting in Bangladesh. Crit. Perspect. Account. 2011, 22, 654–667. [Google Scholar] [CrossRef] [Green Version]

- Belal, A.R.; Owen, D.L. The views of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh: An engagement-based study. Account. Audit. Account. J. 2007, 20, 472–494. [Google Scholar] [CrossRef] [Green Version]

- Chapple, W.; Moon, J. Corporate social responsibility (CSR) in Asia: A seven-country study of CSR web site reporting. Bus. Soc. 2005, 44, 415–441. [Google Scholar] [CrossRef] [Green Version]

- Choi, J.S. An investigation of the initial voluntary environmental disclosures made in Korean semi-annual financial reports. Pac. Account. Rev. 1998. [Google Scholar]

- De Villiers, M. Johannes. The decision by management to disclose environmental information: A research note based on interviews. Meditari Account. Res. 1999, 7, 3348. [Google Scholar]

- De Villiers, C.; Barnard, P. Environmental reporting in South Africa from 1994 to 1999: A research note. Meditari Account. Res. 2000, 8, 15–23. [Google Scholar] [CrossRef] [Green Version]

- De Villiers, C.; Van Staden, C.J. Can less environmental disclosure have a legitimising effect? Evidence from Africa. Account. Organ. Soc. 2006, 31, 763–781. [Google Scholar] [CrossRef]

- Garas, S.; ElMassah, S. Corporate governance and corporate social responsibility disclosures: The case of GCC countries. Crit. Perspect. Int. Bus. 2018, 14, 2–26. [Google Scholar] [CrossRef]

- Giannarakis, G. The determinants influencing the extent of CSR disclosure. Int. J. Law Manag. 2014, 56, 393–416. [Google Scholar] [CrossRef]

- Gunawan, J. Corporate Social Disclosures by Indonesian Listed Companies: A Pilot Study. Soc. Responsib. J. 2007, 3, 26–34. [Google Scholar] [CrossRef]

- Islam, M.A.; Deegan, C. Motivations for an organisation within a developing country to report social responsibility information: From Bangladesh. Account. Audit. Account. J. 2008, 21, 850–874. [Google Scholar] [CrossRef] [Green Version]

- Issa, A.; Fang, H.-X. The impact of board gender diversity on corporate social responsibility in the Arab Gulf states. Gend. Manag. Int. J. 2019, 34, 577–605. [Google Scholar] [CrossRef]

- Katmon, N.; Mohamad, Z.Z.; Norwani, N.M.; Al Farooque, O. Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. J. Bus. Ethics 2019, 157, 447–481. [Google Scholar] [CrossRef]

- Kılıç, M.; Kuzey, C.; Uyar, A. The impact of ownership and board structure on Corporate Social Responsibility (CSR) reporting in the Turkish banking industry. Corp. Gov. Int. J. Bus. Soc. 2015, 15, 357–374. [Google Scholar]

- Pinkse, J.; Kolk, A. Challenges and trade-offs in corporate innovation for climate change. Bus. Strategy Environ. 2010, 19, 261–272. [Google Scholar] [CrossRef] [Green Version]

- Kuasirikun, N. Attitudes to the development and implementation of social and environmental accounting in Thailand. Crit. Perspect. Account. 2005, 16, 1035–1057. [Google Scholar] [CrossRef]

- Kuasirikun, N.; Sherer, M. Corporate social accounting disclosure in Thailand. Account. Audit. Account. J. 2004, 17, 629–660. [Google Scholar] [CrossRef]

- Liu, X.; Anbumozhi, V. Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 2009, 17, 593–600. [Google Scholar] [CrossRef]

- Matuszak, Ł.; Różańska, E.; Macuda, M. The impact of corporate governance characteristics on banks’ corporate social responsibility disclosure: Evidence from Poland. J. Account. Emerg. Econ. 2019, 9, 75–102. [Google Scholar] [CrossRef]

- Momin, M.A.; Parker, L.D. Motivations for corporate social responsibility reporting by MNC subsidiaries in an emerging country: The case of Bangladesh. Br. Account. Rev. 2013, 45, 215–228. [Google Scholar] [CrossRef]

- Muttakin, M.B.; Khan, A.; Subramaniam, N. Firm characteristics, board diversity and corporate social responsibility: Evidence from Bangladesh. Pac. Account. Rev. 2015, 27, 353–372. [Google Scholar] [CrossRef] [Green Version]

- Ntim, C.G.; Soobaroyen, T. Corporate governance and performance in socially responsible corporations: New empirical insights from a Neo-Institutional framework. Corp. Gov. Int. Rev. 2013, 21, 468–494. [Google Scholar] [CrossRef]

- Oh, W.Y.; Chang, Y.K.; Martynov, A. The effect of ownership structure on corporate social responsibility: Empirical evidence from Korea. J. Bus. Ethics 2011, 104, 283–297. [Google Scholar] [CrossRef]

- Rahaman, A.S.; Lawrence, S.; Roper, J. Social and environmental reporting at the VRA: Institutionalised legitimacy or legitimation crisis? Crit. Perspect. Account. 2004, 15, 35–56. [Google Scholar] [CrossRef]

- Ratanajongkol, S.; Davey, H.; Low, M. Corporate social reporting in Thailand: The news is all good and increasing. Qual. Res. Account. Manag. 2006, 3, 67–83. [Google Scholar] [CrossRef] [Green Version]

- Zeng, S.; Xu, X.; Dong, Z.; Tam, V.W. Towards corporate environmental information disclosure: An empirical study in China. J. Clean. Prod. 2010, 18, 1142–1148. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Jones, T.M. Corporate social responsibility revisited, redefined. Calif. Manag. Rev. 1980, 22, 59–67. [Google Scholar] [CrossRef]

- Dembińska, I. Doubts of the TSL Enterprises to Social Responsibility—An Empirical Study Based on the Results of Research. Eur. J. Serv. Manag. 2018, 27, 53–62. [Google Scholar] [CrossRef]

- Blasco, M.; Zølner, M. Corporate social responsibility in Mexico and France: Exploring the role of normative institutions. Bus. Soc. 2010, 49, 216–251. [Google Scholar] [CrossRef]

- Muthuri, J.N.; Gilbert, V. An institutional analysis of corporate social responsibility in Kenya. J. Bus. Ethics 2011, 98, 467–483. [Google Scholar] [CrossRef]

- Fernandez-Feijoo, B.; Romero, S.; Ruiz, S. Does board gender composition affect corporate social responsibility reporting. Int. J. Bus. Soc. Sci. 2012, 3, 31–38. [Google Scholar]

- Wang, H.; Qian, C. Corporate Philanthropy and Financial Performance: The Roles of Social Expectations and Political Access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Factors influencing social responsibility disclosure by Portuguese companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Chauvey, J.N.; Giordano-Spring, S.; Cho, C.H.; Patten, D.M. The normativity and legitimacy of CSR disclosure: Evidence from France. J. Bus. Ethics 2015, 130, 789–803. [Google Scholar] [CrossRef]

- Powell, W.W.; DiMaggio, P.J. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar]

- Siregar, S.V.; Bachtiar, Y. Corporate social reporting: Empirical evidence from Indonesia Stock Exchange. Int. J. Islamic Middle East. Financ. Manag. 2010, 3, 241–252. [Google Scholar] [CrossRef]

- Carter, D.A.; Simkins, B.J.; Simpson, W.G. Corporate governance, board diversity, and firm value. Financ. Rev. 2003, 38, 33–53. [Google Scholar] [CrossRef]

- Rao, K.K.; Tilt, C.A.; Lester, L.H. Corporate governance and environmental reporting: An Australian study. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 143–163. [Google Scholar]

- Sharma, E. A review of corporate social responsibility in developed and developing nations. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 712–720. [Google Scholar] [CrossRef]

- De Soto, J.H. Socialism, Economic Calculation and Entrepreneurship; Institute of Economic Affairs Monographs: London, UK, 2013. [Google Scholar]

- Foss, N.J.; Klein, P.G. Organizing Entrepreneurial Judgment: A New Approach to the Firm; Cambridge University Press: Cambridge, UK, 2012. [Google Scholar]

- Harper, D.A. Foundations of Entrepreneurship and Economic Development; Routledge: Abingdon, UK, 2003. [Google Scholar]

- Espinosa, V.I.; William, H.W.; Haijiu, Z. Israel Kirzner on dynamic efficiency and economic development. Procesos Merc. Rev. Eur. Econ. Política 2020, 17, 283–310. [Google Scholar] [CrossRef]

- Ribeiro-Soriano, D.; Huarng, K.H. Innovation and entrepreneurship in knowledge industries. J. Bus. Res. 2013, 66, 1964–1969. [Google Scholar] [CrossRef]

- Hernández-Perlines, F.; Rung-Hoch, N. Sustainable entrepreneurial orientation in family firms. Sustainability 2017, 9, 1212. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z.; Wang, X.; Jia, M. Echoes of CEO entrepreneurial orientation: How and when CEO entrepreneurial orientation influences dual CSR activities. J. Bus. Ethics 2021, 169, 609–629. [Google Scholar] [CrossRef]

- Kim, Y. Environmental, sustainable behaviors and innovation of firms during the financial crisis. Bus. Strategy Environ. 2015, 24, 58–72. [Google Scholar] [CrossRef]

- Wang, H.; Choi, J.; Li, J. Too little or too much? Untangling the relationship between corporate philanthropy and firm financial performance. Organ. Sci. 2008, 19, 143–159. [Google Scholar] [CrossRef] [Green Version]

- Seifert, B.; Morris, S.A.; Bartkus, B.R. Having, giving, and getting: Slack resources, corporate philanthropy, and firm financial performance. Bus. Soc. 2004, 43, 135–161. [Google Scholar] [CrossRef]

- Godfrey, P.C. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Acad. Manag. Rev. 2005, 30, 777–798. [Google Scholar] [CrossRef] [Green Version]

| Study | Nature of Study | Country | Theory | Outcomes | ||

|---|---|---|---|---|---|---|

| Determinants | Motivations | Antecedents | Motivations | |||

| [20] Singh and Ahuja (1983) | ✓ | India | N/A | Firm size (+), industry (+), financial performance (+) | ||

| [21] Teoh and Thong (1984) | ✓ | Malaysia | N/A | Firm size related to commitment to social reporting (+), foreign ownership related to commitment to social reporting (+) | ||

| [22] Maheshwari (1992) | ✓ | ✓ | India | LT | Firm size (+), industry (+) profitability (+), governmental pressures (+), market forces (+), community involvement (−) | Enhanced corporate profitability and social responsibility (+), fair business practices (+) |

| [23] Williams (1999) | ✓ | Asian-pacific nations | PE | Culture, political, social system (+) | ||

| [24] De-Villiers (2003) | ✓ | South Africa | N/A | Absence of legal requirements (−), non-availability of data (−), lack of motivation for CSR disclosure (−) | ||

| [25] Haniffa and Cooke (2005) | ✓ | Malaysia | LT | Firm size (+), industry size (+), multiple listing (+), financial performance (+), culture proxied by Malay directors (+), governance structure (+) | ||

| [26] Yusoff et al. (2006) | ✓ | ✓ | Malaysia | AT, LT and ST | Firm size (+), industry (+), environmental performance (+), financial performance (+), environmental expenditures (+), financing for environmental equipment (+) | More visibility of corporate environmental performance (+), enhance motivation to develop environmental management system (+) |

| [27] Alsaeed (2006) | ✓ | Saudi-Arabia | N/A | Firm size (+), industry size (0), financial performance (0), firm age (0), creditors i.e., leverage (0), audit firm size (0), ownership dispersion (0) | ||

| [28] Amran and Devi (2007) | ✓ | Malaysia | PE | Influence of government proxied by govt. shareholdings (+), dependence on government (+) | ||

| [29] Kamla (2007) | ✓ | Middle East | N/A | Country specific factors (+) resulted in variation in themes of disclosure | ||

| [30] Mirfazil (2008) | ✓ | ✓ | Indonesia | LT | Firm size (0), industry (+), transparent information (+), environmental performance (+), regulatory pressure (+), environmental concerns (+), stakeholder’s concerns (+) | Adoption of the processes that are fulfilling the market demand (+), greater influence of firm’s operations on stakeholders as well as shareholders (+) |

| [31] Amran and Devi (2008) | ✓ | Malaysia | IT | Firm size (+), industry size (+), influence of government proxied by govt. shareholdings (+), dependence on govt. (+) | ||

| [32] Wanderley et al. (2008) | ✓ | Emerging Countries | N/A | Country (+) | ||

| [33] Rizk et al. (2008) | ✓ | Egypt | N/A | Industry size (+), ownership structure (+) | ||

| [34] Mitchell and and Hill (2009) | ✓ | South Africa | N/A | Industry size (+), absence of legal requirements (−), lack of motivation for disclosure (−), non-availability of data (−), cost of obtaining data (−) | ||

| [35] Sobhani et al. (2009) | ✓ | Bangladesh | N/A | Firm size (+), industry size (+), financial performance (+) | ||

| [36] Hassan and Harahap (2010) | ✓ | ✓ | Indonesia | ST | Firm size (o), board size (+), corporate governance (+), stakeholder’s concerns (+), environmental concerns (+), increased strategic social investments (+) | Enhance environmental protection using recyclable and environment friendly supplies (+); fair dealing with supply chain (+) |

| [37] Buniamin (2010) | ✓ | Malaysia | LT | Industry size (+) | ||

| [38] Huang and Kung (2010) | ✓ | Taiwan | ST | Firm size (+), financial performance (+), government. (+), creditors i.e., leverage (−), consumers (+), suppliers (−), competitors (+), employees (+), shareholding concentration (−) | ||

| [39] Khan (2010) | ✓ | Bangladesh | LT | Non-executive directors on board (+), foreign nationalities on board (+), women representation on board (0) | ||

| [40] Saleh et al. (2010) | ✓ | Malaysia | N/A | Firm size (+), financial performance (0), institutional ownership (+) | ||

| [41] McCuinness et al. (2017) | ✓ | China | CMT | Female CEO (+), female chairman of board (+), independent directors on board (0), CEO duality (0), board size (+), managerial size (+), managerial ownership (0), state ownership (−) | ||

| [42] Mahadeo et al. (2011) | ✓ | Mauritius | LT | Firm size (+), leverage (+) related to HR and ED | ||

| [43] Abd-Rahman et al. (2011) | ✓ | Malaysia | N/A | Firm size (+) | ||

| [44] Qadan and Suwaidan (2019) | ✓ | Jordan | AT | Board gender diversity (0), board size (+), board independence (−), CEO duality (−), director Age (−), ownership concentration (−), institutional ownership (−), foreign ownership (0) | Corporate accountability (+) | |

| [45] Haji (2013) | ✓ | Malaysia | LT | Managerial ownership (−), government ownership (+), | ||

| [46] Khan et al. (2013) | ✓ | Bangladesh | LT | Firm size (+), media visibility (+), managerial ownership (−), public ownership (+), foreign ownership (+) | ||

| [47] Chiu and Wang (2014) | ✓ | Taiwan | ST | Firm size (+), industry (+), listing in social investment funds (+), impact of global supply chain (+), international capital markets (+) | ||

| [48] Laidroo and Sokolova (2015) | ✓ | ✓ | Estonia | LT and ST | Firm size (+), firm value (+) shareholder’s contribution (+), political perspective (+), legal considerations (+), competitive pressures process standardization (+) | Increased demand of stakeholders’ information (+), improved public image (+) |

| [49] Khan et al. (2019) | ✓ | ✓ | Pakistan | N/A | Board gender diversity (+), board education diversity (0), board education background diversity (−), board tenure diversity (+), board age diversity (0), board nationality diversity (+), board ethnicity diversity (0), board size (0), board independence (0), board meeting (0), independent audit committee (+) | Good relations with the labor unions (+); positive firm value (+), and increased accountability (+) |

| [50] Aboud and Diab (2018) | ✓ | ✓ | Egypt | AT | Firm size (0), organizational performance (+), firm value (+), capital expenditure (+), cultural specificity (−), regulatory frameworks (+), shareholders’ conflicts (+), management decisions (+), negotiation (+) | Environment friendly engagement (+), financial stability (+) and positive firm value (+) |

| [51] Sun et al. (2018) | ✓ | ✓ | China | ST | Firm size (+), growth rate (0), regulatory pressures (+), stakeholder influence (+) | Recognition of firms’ investment capability (+), increased interaction/engagement with the investors (+) |

| [52] Orazalin (2019) | ✓ | ✓ | Kazakhstan | LT | Firm size (+), firm age (+), transparent information (+), interests of depositors and other stakeholders (+), societal pressure (−), independence of board (+) | Uncertainty avoidance (+), increased accountability and responsibility (+) |

| [53] Ramananda and Ataha (2019) | ✓ | ✓ | Indonesia | LT and ST | Firm size (+), firm performance (+), profitability (+), stakeholder’s interests (+), sustainability orientation (+), social media consideration (+), positive image (+) | Sustainable community and environmental development (+), proactive in engagement and increased accountability (+) |

| [54] Khan et al. (2019) | ✓ | ✓ | Pakistan and Turkey | RBV | Firm size (+), age of assets (+), board size (+), managerial ownership (+), legal regulatory guideline (+), environmental concerns (+), management decision making (+) | Sustainable utilisation of resources for environmental development (+), proactive engagement (+) |

| [55] Daas and Alaraj (2019) | ✓ | ✓ | Jordan | LT | Firm size (+), environmental concerns (+), steady growth (+) | Sustainable corporate growth (+), claims of internal initiatives (+) |

| [56] Hamrouni et al. (2019) | ✓ | ✓ | Tunisia | ST and AT | Firm size (0), profitability (+), regulatory pressures (+), eco-friendly practices (+), stakeholder pressure (+) | Recognition of firms’ investment capability (+), better management of portfolios (+) |

| [57] Sekhon and Kathuria (2019) | ✓ | ✓ | India | AT, LT and ST | Firm size (+), industry size (+), market regulatory pressure (+), level of competition (+), environmental concerns (+), social responsiveness (+) | Improved brand image and employee morale (+), increasing interest towards social responsibilities (+) |

| [58] Acar and Temiz (2019) | ✓ | ✓ | Turkey | LT and ST | Firm size (0), transparency of information (+), regulatory pressures (+), governmental pressures (+), environmental concerns (+), highly focusing on interests and demands of stakeholders (+) | More visibility of corporate environmental performance (+), enhance motivation to adopt more transparent processes (+) |

| [59] Souror et al. (2020) | ✓ | ✓ | Egypt | LT | Firm size (0), element of independence (+), investment capability (+), management of risk (+), political influence (+), societal expectations (+), regulatory pressure (+) | Fair business practices (+) |

| [60] Bhatia and Makkar (2020) | ✓ | ✓ | India | N/A | Firm size (+), industry (+), income inequality (−), environmental concerns (+), international listing (+), board independence (+) | Corporate accountability (+) |

| [61] Zamir et al. (2020) | ✓ | ✓ | Pakistan | LT | Firm size (+), investment sensitivity (−), firm value (+), regulatory pressure (+), environmental concerns (+), investment efficiency (+) | Corporate investment efficiency (+), positive firm value and increased accountability (+) |

| [62] Maama (2020) | ✓ | ✓ | South Africa | IT | Firm size (+), firm value (+), firm age (+), political perspective (+), influence of institutional environment (+) | Influence of governments (+), improved accounting practices (+) |

| [63] Ali and Frynas (2018) | ✓ | Pakistan | Institutional Theory | CSR Standard Setting Institutions (+), colloboration with NGOs (+), CSR forums and networks (+) | ||

| [5] Amran et al. (2014) | ✓ | Asian-pacific nations | LT & RBV | Board Size (0), board gender diversity (0), board independence (0), organizational CSR related vision and mission (+), CSR committee (+), Collaboration with NGOs (+) | ||

| [64] Belal and Cooper (2011) | ✓ | Bangladesh | PE | Lack of public awareness (−), lack of legal requirements (−), Lack of resources (−), departure from shareholder wealth maximization objective | ||

| [65] Belal and Owen (2007) | ✓ | Bangladesh | N/A | Economically powerful stakeholders (notable parent companies, international buyers, and investors demand) (+), weak institutions is reason of absence of disclosure (−), Enhancement of corporate image (+) | ||

| [66] Chapple and Moon (2005) | ✓ | Malaysia, Indonesia, Philipnines, South Korea, India, Singapore, Thailand | LT, ST | Country (+), internationalization (+), globalization (+) | ||

| [67] Choi (1998) | ✓ | South Korea | N/A | Size (+), industry (+), financial performance (0), auditing (+), Sales growth rate (+) | ||

| [68] De-Villiers and Johannes (1999) | ✓ | South Africa | N/A | Absence of legal requirements (−), non-availability of data (−), No motivation for disclosure (−) | ||

| [69] De-Villiers and Barnard (2000) | ✓ | South Africa | LT | Size (+), industry (+), fear of liability (−), listed companies (+) | ||

| [70] De-Villiers and Van Staden (2006) | ✓ | South Africa | LT | Industry (+), non-existance of need to legitimize corporate actions (−) | ||

| [71] Garas and ElMassah (2018) | ✓ | UAE | LT | Firm size (+), assets management (+), managerial ownership (−), market regulatorty pressure (+), societal concerns (+), separation of powers (+), independence of board (+) | ||

| [72] Giannarakis (2014) | ✓ | Greece | N/A | Firm size (0), information flow (−), consumer staple (−), stakeholders interests (+), policy regulators pressures (+) | ||

| [73] Gunawan (2007) | ✓ | India | LT, ST | Stakeholer influence (+), size (+), financial performance (0), firm age (0) | ||

| [74] Islam and Deegan (2008) | ✓ | Bangladesh | LT, ST, IT | Powerful stakeholders (e.g., international buyers, NGOs), demands and global expectations (+) | ||

| [75] Issa and Fang (2019) | ✓ | UAE | ST | Board gender diversity (0), Board independence (0), CEO duality (−), board size (+) | ||

| [76] Katmon et al. (2019) | ✓ | Malaysia | AT and Resource Dependency Theory | board gender diversity (0), board education diversity (+), board education backgrough diversity (0), board tenure diversity (+), board age diversity (−), board nationality diversity (−), board ethnicity diversity (0), board size (0), board independence (+), board meeting (+), independent audit committee (0) | ||

| [77] Kiliç et al. 2015 | ✓ | Turkey | LT, ST | Board gender diversity (+), board independence (+), board size (0), ownership diffusion (+), company size (+) | ||

| [78] Kolk et al. (2010) | ✓ | China | LT | Nationality (+) | ||

| [79] Kuasirikun (2005) | ✓ | Thailand | N/A | Latent positive attitudes (+), towards social accounting that may result in CSR disclosure | ||

| [80] Kuasirikun and Sherer (2004) | ✓ | Thailand | LT, ST, IT | Country (+) | ||

| [81] Liu and Anbumozhi (2009) | ✓ | China | ST | Government pressure (+), size (+), financial performance (+), geographical location within country (+) | ||

| [82] Matuszak et al. (2019) | ✓ | Poland | N/A | Firm size (+), board size (+), managerial ownership (+), board leadership (+), legal regulatory guideline (+), public welfare (+), shareholder’s interests (+) | ||

| [83] Momin and Parker (2013) | ✓ | Bangladesh | LT, IT | External environment of MNCs (informal norms and beliefs, very low expectations for CSR reporting, lax formal reporting regulation, low level of legal implementation), is a major hurdle for CSR reporting Management culture of parent company (+), and enhance corporate Image (+), are the main reasons for MNCs CSR reporting. | ||

| [84] Muttakin et al. 2015 | ✓ | Bangladesh | AT, LT, ST, and Sinaling Theory | Board gender diversity (−), board independence (+), CEO duality (+), foreign director (+), firm size (+), profitability (+), family ownership (−) | ||

| [85] Ntim and Soobaroyen 2013 | ✓ | South Africa | Neo Institutional Theory | Board gender diversity (+), board size (0), independent directors (+), CEO duality (0), government ownership (+), institutional ownership (0), block ownership (−), CSR committee (+) | ||

| [86] Oh et al. (2011) | ✓ | Korea | AT | Institutional ownership (+), and foreign ownership (+) | ||

| [87] Rahaman et al. (2004) | ✓ | Ghana | IT | Institutional pressures from World Bank regulatory requirements (+) | ||

| [88] Ratanajongkol et al. (2006) | ✓ | Thailand | LT, PE | Stakeholder Influence (+), size (0), industry (+) | ||

| [89] Zeng et al. (2010) | ✓ | China | N/A | Size (+), industry (+) | ||

| Sr. No | Country | Frequency | %Age |

|---|---|---|---|

| 1 | Malaysia | 10 | 14.085% |

| 2 | Bangladesh | 8 | 11.268% |

| 3 | South Africa | 7 | 9.859% |

| 4 | India | 5 | 7.042% |

| 5 | China | 5 | 7.042% |

| 6 | Egypt | 3 | 4.225% |

| 7 | Indonesia | 3 | 4.225% |

| 8 | Pakistan | 3 | 4.225% |

| 9 | Thailand | 3 | 4.225% |

| 10 | UAE | 2 | 2.817% |

| 11 | Jordan | 2 | 2.817% |

| 12 | Turkey | 2 | 2.817% |

| 13 | Asian-pacific nations | 2 | 2.817% |

| 14 | Taiwan | 2 | 2.817% |

| 15 | Greece | 1 | 1.408% |

| 16 | Poland | 1 | 1.408% |

| 17 | Korea | 1 | 1.408% |

| 18 | Kazakhstan | 1 | 1.408% |

| 19 | Pakistan and Turkey | 1 | 1.408% |

| 20 | Estonia | 1 | 1.408% |

| 21 | Tunisia | 1 | 1.408% |

| 22 | Saudi-Arabia | 1 | 1.408% |

| 23 | Middle-East | 1 | 1.408% |

| 24 | Emerging Countries | 1 | 1.408% |

| 25 | Mauritius | 1 | 1.408% |

| 26 | Ghana | 1 | 1.408% |

| 27 | Malaysia, Indonesia, Philippines, South Korea, India, Singapore, Thailand | 1 | 1.408% |

| 28 | South Korea | 1 | 1.408% |

| Total | 71 | 100% |

| Sr. No | Theory/Theories | Frequency | %Age |

|---|---|---|---|

| 1 | Legitimacy Theory | 16 | 22.54% |

| 2 | Legitimacy Theory and Stakeholder Theory | 7 | 9.86% |

| 3 | Stakeholder Theory | 6 | 8.45% |

| 4 | Institutional Theory | 5 | 7.04% |

| 5 | Agency Theory | 3 | 4.23% |

| 6 | Political Economy Theory | 3 | 4.23% |

| 7 | Agency Theory, Legitimacy Theory and Stakeholder Theory | 3 | 4.23% |

| 8 | Resource Based View Theory | 2 | 2.82% |

| 9 | Miscellaneous theories | 2 | 2.82% |

| 10 | Resource Based View Theory and other theories | 1 | 1.41% |

| 11 | Agency Theory and Stakeholder Theory | 1 | 1.41% |

| 12 | Critical Mass Theory | 1 | 1.41% |

| 13 | Agency Theory and Resource Dependency Theory | 1 | 1.41% |

| 14 | Legitimacy and Institutional Theory | 1 | 1.41% |

| 15 | Not Applied | 19 | 26.76% |

| Total | 71 | 100% |

| Sr. No | Disclosure Dimensions | Frequency | Percentage |

|---|---|---|---|

| 1 | Environmental Disclosure | 29 | 25.00% |

| 2 | Human Resource Disclosure | 12 | 10.34% |

| 3 | Product and Consumer Disclosure | 3 | 2.59% |

| 4 | General Disclosure | 2 | 1.72% |

| 5 | Community Involvement Disclosure | 15 | 12.93% |

| 6 | CSR Disclosure | 55 | 47.41% |

| Total | 116 | 100% |

| Determinants of CSR/Environmental Disclosure | Sig +ve | Insignificant | Sig −ve | Grand Total |

|---|---|---|---|---|

| Firms Characteristics | ||||

| Firm size | 33 | 1 | 7 | 41 |

| Industry | 18 | 0 | 1 | 19 |

| Financial performance | 11 | 2 | 2 | 15 |

| Firm age | 3 | 1 | 1 | 5 |

| Firm value | 4 | 0 | 0 | 4 |

| Leverage | 1 | 1 | 1 | 3 |

| Transparent information | 3 | 0 | 0 | 3 |

| Audit firm size | 1 | 0 | 1 | 2 |

| Managers/accountants positive attitude | 2 | 0 | 0 | 2 |

| Asset management | 1 | 0 | 0 | 1 |

| Capital expenditure | 1 | 0 | 0 | 1 |

| Employees’ information | 1 | 0 | 0 | 1 |

| Fear of liability | 0 | 0 | 1 | 1 |

| Investment capability | 1 | 0 | 0 | 1 |

| Lack of resources | 0 | 0 | 1 | 1 |

| Non availability of data | 0 | 0 | 1 | 1 |

| Non-existence of need to legitimize corporate actions | 0 | 0 | 1 | 1 |

| Corporate Environmental Policies and Concerns | ||||

| Environmental concerns | 7 | 0 | 0 | 7 |

| Environmental performance | 2 | 0 | 0 | 2 |

| Institutional environment | 2 | 0 | 0 | 2 |

| Sustainability orientation | 2 | 0 | 0 | 2 |

| Eco friendly practices | 1 | 0 | 0 | 1 |

| Environmental expenditure | 1 | 0 | 0 | 1 |

| Financing for environmental equipment | 1 | 0 | 0 | 1 |

| GRI adoption | 1 | 0 | 0 | 1 |

| Governance Characteristics | ||||

| Board size | 6 | 0 | 5 | 11 |

| Board independence | 5 | 1 | 4 | 10 |

| Stakeholders’ interest/concern | 10 | 0 | 0 | 10 |

| Board gender diversity | 4 | 1 | 4 | 9 |

| CEO duality | 1 | 2 | 2 | 5 |

| Board age diversity | 0 | 2 | 1 | 3 |

| Board education | 1 | 0 | 1 | 2 |

| Board meetings | 1 | 0 | 1 | 2 |

| CSR committee | 2 | 0 | 0 | 2 |

| Independent audit committee | 1 | 0 | 1 | 2 |

| Long term tenure of directors | 2 | 0 | 0 | 2 |

| Foreign directors on board | 1 | 0 | 0 | 1 |

| Vision and mission | 1 | 0 | 0 | 1 |

| Owners and Shareholders | ||||

| Managerial ownership | 2 | 3 | 1 | 6 |

| Disperse ownership | 3 | 0 | 1 | 4 |

| Foreign ownership | 3 | 0 | 1 | 4 |

| Government ownership | 3 | 1 | 0 | 4 |

| Institutional ownership | 2 | 1 | 1 | 4 |

| Shareholder contribution | 3 | 1 | 0 | 4 |

| Public ownership | 1 | 0 | 0 | 1 |

| Determinants of CSR /Environmental Disclosure | Sig +ve | Insignificant | Sig −ve | Grand Total |

|---|---|---|---|---|

| Political and Legal Factors | ||||

| Regulatory pressure | 15 | 0 | 0 | 15 |

| Absence of legal requirements | 0 | 2 | 3 | 5 |

| Political development/pressure | 3 | 0 | 0 | 3 |

| Government pressure | 2 | 0 | 0 | 2 |

| Dependence on government | 1 | 0 | 0 | 1 |

| Low level of legal implementation | 0 | 0 | 1 | 1 |

| Media visibility/pressure | 1 | 0 | 0 | 1 |

| Political system | 1 | 0 | 0 | 1 |

| Weak institutions of the country | 0 | 0 | 1 | 1 |

| Global Issue | ||||

| International buyer pressure | 2 | 0 | 0 | 2 |

| Global supply chain | 1 | 0 | 0 | 1 |

| Globalization | 1 | 0 | 0 | 1 |

| Pressure from regulatory bodies e.g., World Bank | 1 | 0 | 0 | 1 |

| International NGOs | 1 | 0 | 0 | 1 |

| Normative Institution (CSR Promoting Institutions) | ||||

| Collaboration with NGOs | 2 | 0 | 0 | 2 |

| CSR forums and networks | 1 | 0 | 0 | 1 |

| CSR standard setting institutions | 1 | 0 | 0 | 1 |

| Social Cultural Factors | ||||

| Country specific factors | 4 | 0 | 0 | 4 |

| Public pressure | 2 | 2 | 0 | 4 |

| Cultural factor | 2 | 0 | 0 | 2 |

| Cultural specificity | 0 | 1 | 0 | 1 |

| Income inequality | 0 | 1 | 0 | 1 |

| Lack of public awareness | 0 | 0 | 1 | 1 |

| Public welfare | 1 | 0 | 0 | 1 |

| Social media concerns | 1 | 0 | 0 | 1 |

| Low public expectations for CSR reporting | 0 | 0 | 1 | 1 |

| Industry Level Factors | ||||

| Level of competition | 2 | 0 | 0 | 2 |

| Capital market | 1 | 0 | 0 | 1 |

| Customer concerns | 1 | 0 | 0 | 1 |

| Market forces | 1 | 0 | 0 | 1 |

| Multiple listing | 1 | 0 | 0 | 1 |

| Overseas listing | 1 | 0 | 0 | 1 |

| Stock market listing | 1 | 0 | 0 | 1 |

| Suppliers | 0 | 1 | 0 | 1 |

| Systematic risk | 1 | 0 | 0 | 1 |

| Motivations of CSR Disclosure | F | %Age |

|---|---|---|

| Corporate Accountability | ||

| Demonstrate corporate accountability | 4 | 5.56% |

| Improve accounting practices | 1 | 1.39% |

| Total | 5 | |

| Corporate Reputation | ||

| Showcase corporate environmental performance | 3 | 4.17% |

| Improve public image | 2 | 2.78% |

| Exhibit environment friendly engagement | 1 | 1.39% |

| Improve environmental management systems | 1 | 1.39% |

| Promote fair business practices | 1 | 1.39% |

| Total | 8 | |

| Financial Performance | ||

| Drive corporate performance | 1 | 1.39% |

| Promote positive firm value | 3 | 4.17% |

| Contribute to sustainable corporate growth | 1 | 1.39% |

| Improve financial stability | 1 | 1.39% |

| Eliminate uncertainty in reporting practices | 1 | 1.39% |

| Enhance corporate profitability and social responsibility | 1 | 1.39% |

| Total | 8 | |

| Investment Opportunities | ||

| Recognize firms’ investment potential | 2 | 2.78% |

| Secure more opportunities for institutional investments | 1 | 1.39% |

| Demonstrate corporate investment efficiency | 1 | 1.39% |

| Total | 4 | |

| Management of key Stakeholders | ||

| Increase interaction/engagement with investors/ stakeholders | 4 | 5.56% |

| Demonstrate good relations with the labor unions | 1 | 1.39% |

| Respond to increased stakeholders’ demand for information | 1 | 1.39% |

| Influence on governments | 1 | 1.39% |

| Reduce political costs | 1 | 1.39% |

| Improve employee morale | 1 | 1.39% |

| Align firm’s operations with stakeholders | 1 | 1.39% |

| Total | 10 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ali, W.; Wilson, J.; Husnain, M. Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature. Sustainability 2022, 14, 3474. https://doi.org/10.3390/su14063474

Ali W, Wilson J, Husnain M. Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature. Sustainability. 2022; 14(6):3474. https://doi.org/10.3390/su14063474

Chicago/Turabian StyleAli, Waris, Jeffrey Wilson, and Muhammad Husnain. 2022. "Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature" Sustainability 14, no. 6: 3474. https://doi.org/10.3390/su14063474

APA StyleAli, W., Wilson, J., & Husnain, M. (2022). Determinants/Motivations of Corporate Social Responsibility Disclosure in Developing Economies: A Survey of the Extant Literature. Sustainability, 14(6), 3474. https://doi.org/10.3390/su14063474