Abstract

This study examines the dynamic and distributional effects of financial technology (FinTech) and renewable energy (RE) on financial stability (FST) in BRICS economies from 2012 to 2022. Using a combination of Panel Autoregressive Distributed Lag (Panel ARDL) and Panel Quantile Regression (PQR) models, the analysis captures both short-run versus long-run adjustment mechanisms and heterogeneous effects across different levels of financial stability. The ARDL results reveal a dual effect of FinTech: while FinTech expansion initially increases short-run financial volatility, it enhances long-run stability as regulatory and institutional frameworks mature. Renewable energy consistently strengthens financial stability, with its impact intensifying in higher quantiles of the stability distribution. The quantile results further show that the stabilizing effects of FinTech, RE, institutional quality, and industrial development become stronger in more resilient financial systems. These findings highlight the need for BRICS policymakers to coordinate digital financial innovation with clean energy strategies under robust governance frameworks to promote a more stable, inclusive, and sustainable macro-financial environment.

1. Introduction

The 2008 global financial crisis, the COVID-19 pandemic, and recent geopolitical and energy-market tensions have exposed structural vulnerabilities in financial systems, particularly through energy-price volatility, inflationary pressures, and the transmission of credit risk. These shocks have highlighted the importance of macro-financial resilience mechanisms that can mitigate systemic risk. In response, two structural transformations, financial digitalization through FinTech and the transition toward renewable energy (RE), have emerged as central components of contemporary economic policy, with potential implications for financial stability. Both are reshaping the structures of contemporary economies, with potential implications for systemic stability [1,2,3]. FinTech restructures financial intermediation by increasing efficiency, transparency, and inclusion, while the development of renewable energy bolsters environmental sustainability and helps diversify economic activity. Despite their distinct domains, limited research has examined how these two dynamic processes may interact to influence financial stability (FST), particularly in developing economies where digital finance and energy transitions are accelerating within heterogeneous institutional environments [4,5]. From a macro-financial perspective, the digital transformation of finance and the energy transition are increasingly interconnected. FinTech facilitates the mobilization, allocation, and risk management of capital for large-scale renewable energy investments through digital payments, green lending platforms, and sustainable finance instruments. At the same time, renewable energy deployment can influence financial stability by reducing exposure to fossil-fuel price shocks, improving balance-of-payments dynamics, and lowering long-term inflationary pressures. When combined, these processes may enhance the capacity of financial systems to absorb shocks; however, rapid digitalization and capital-intensive energy transitions may also generate short-run volatility if regulatory and institutional frameworks lag behind.

Financial stability refers to the ability of the financial system to allocate resources efficiently, absorb shocks, and regain confidence in its institutions. Stability depends on striking a balance between innovation and caution. Technological innovations such as mobile banking, blockchain, and digital loans expand financial access while reducing transaction costs. However, they also bring increased risks: cyber risk, operational fragility, and market concentration are all new forms of vulnerability [6]. Similarly, demand for green projects reshapes investment patterns and channels credit into new arenas. Thus, carbon markets, as well as green bonds, have emerged to fill the gaps left by conventional emissions-trading mechanisms [6]. The overall result could be an improved long-run stability thanks to sustainable growth. But the same developments can also transmit high-frequency instability through speculative investment behavior and policy uncertainty [7]. As such, whether the growth of FinTech and renewables contributes to or undermines macro-finance stability remains a high-policy-relevance open question. However, these effects are unlikely to be uniform over time. Recent evidence suggests that FinTech innovations may initially trigger market turbulence, abrupt adjustments in credit allocation, and operational vulnerabilities due to rapid digital adoption and insufficient regulatory preparedness [8,9]. Only after a period of institutional learning and technological consolidation do FinTech systems begin to enhance efficiency, reduce information asymmetry, and stabilize financial intermediation. Therefore, a proper empirical assessment must account for this temporal pattern: short-run destabilization versus long-run stabilization. Our empirical strategy explicitly incorporates these transitional dynamics through the ARDL framework and quantile-based heterogeneity.

From a theoretical perspective, Joseph Schumpeter’s Innovation theory posits that technological change is the primary driver of economic development and that financial innovation facilitates rational behavior in saving, investment, and entrepreneurship [10]. This process is illustrated by FinTech democratizing financial services and raising capital for sustainable, productive industries, such as those related to renewable energy [11,12]. Endogenous growth theory assumes rationality about the effect of technological innovation, such as the introduction of new technologies in energy use [13]. Minsky’s Financial Instability Hypothesis posits that innovation, when it becomes excessive or inadequately regulated, can generate leverage and speculative behavior, ultimately leading to systemic risk [14].

The BRICS economies—Brazil, the Russian Federation, India, China, and South Africa offer an ideal setting in which to study the interaction between renewable energy and FinTech. The five countries combined represent a third of global GDP and form the most vibrant cluster of emerging markets currently undergoing simultaneous financial digitization and electrical energy transformation. Over the past decade, the vast majority of FinTech ecosystems in BRICS countries have been driven by open banking frameworks, innovation-friendly regulations, and digital payment networks [15]. China stands as a world leader in digital finance and green energy technologies. India and Brazil have made commendable progress in popularizing mobile payments. Meanwhile, Russia and South Africa are, in turn, incorporating digital platforms into their own banking and investing spheres. At the same time, these countries are at the forefront of deploying renewable energy because growing energy consumption, commitments to reduce carbon emissions, and a quest for sustainable growth models coincide [16,17]. But the rapid pace of financial innovation and divergent development of regulatory and institutional frameworks raise questions about potential trade-offs in stability. The interrelationship among FinTech, renewable energy, and financial stability has received little study. Previous studies have primarily investigated the factors that influence the development of financial facilities, the role of green finance in mitigating carbon emissions, and the impact of financial technology on credit availability [1,8].

Few studies have explored the confluence or symbiotic effects of digital financial transformation and renewable energy development on systemic stability in developing economies. Nguyen and Dang [18] analyzed 147 countries using quantile regression and concluded that renewable energy consumption tends to reduce financial stability, particularly in economies with already high financial resilience. This instability arises from the capital-intensive nature of renewable projects, which increases banks’ exposure and systemic risk. However, strong institutional quality can mitigate these negative effects by improving risk management and governance. Similarly, Imran et al. [19] examined South Asian economies using a panel ARDL model. They found heterogeneous outcomes: renewable energy enhances financial stability in India and Bangladesh, remains insignificant in Nepal, and negatively affects Pakistan due to high import dependence and fiscal burdens. In contrast, Kirikkaleli [20] demonstrated that in Ireland, renewable energy and financial stability are complementary, as financial soundness facilitates green investment and emission reduction. Moreover, the study [21] confirmed a bidirectional relationship, suggesting that stable financial systems attract renewable energy investment, which in turn supports long-term resilience. In addition, the relationship between renewable energy expansion and financial stability remains theoretically and empirically ambiguous. While renewable energy may reduce exposure to fossil-fuel price volatility and support long-term macroeconomic resilience, several studies highlight that large-scale RE deployment can generate short-run financial stress due to high capital intensity, policy uncertainty, and technology-related risks. Consequently, assuming a uniformly positive effect of RES on financial stability would be overly optimistic. The relationship must be empirically validated and tested for potential spuriousness, especially because RES may proxy for broader structural factors, such as institutional quality, environmental policy, or technological capabilities that themselves influence financial stability. By focusing attention on the BRICS bloc and adopting a macro-financial approach, this study bridges a key gap in current understanding. It deepens our understanding of how technology-driven structural changes and sustainability impact the resilience of financial systems.

Based on balanced panel data, this analysis covers the period 2012–2022 and integrates data from various indicators on RE, FinTech, and financial stability. This approach enables the evaluation of both direct and interactive effects of FinTech and renewable energy on macro-financial resilience, while also controlling for differences in structure and institutions among BRICS member countries. We begin our analysis with a question: how do the digitalization of finance and the transition to clean energy together create systemic risk in emerging economies? As financial FinTech expands, sensitive systems become increasingly linked and driven by data, offering potentially improved risk management but also exposing themselves to cyber threats and the spread of market crises. Similarly, the transition to renewable energy involves significant financial appropriations. Digital finance channels and green financing tools often facilitate these financial flows. The interdependent processes presented in these circumstances reveal whether FinTech and renewable energy are complementary, enabling a more stable financial system, or whether alternative forces of destabilization introduce new systemic risks. The results will have far-reaching implications for asset management, the development of green finance regimes, and the advancement of digital technology and environmental protection strategies in emerging countries. This study makes several significant contributions to the current literature on financial stability, financial technology, and RE within emerging economies. First, it offers a novel research perspective by jointly examining the interactive effects of FinTech and RE on banks’ z-score in the BRICS economies.

While prior studies have tended to analyze these dimensions separately, this paper provides the first comprehensive empirical evidence on how digital financial transformation and the clean energy transition interact to influence macro-financial resilience. Second, the study advances theoretical understanding by integrating Schumpeter’s innovation theory and Minsky’s financial instability hypothesis to explain the dual role of FinTech as both a stabilizing and destabilizing force. In parallel, it conceptualizes renewable energy as a long-run stabilizer that mitigates the cyclical volatility induced by rapid digitalization, offering a unified framework for technological and ecological transitions. Third, methodologically, the study employs both Panel Quantile Regression (PQR) and Panel Autoregressive Distributed Lag (ARDL) models to capture heterogeneous effects across quantiles and time horizons. This dual approach enables a more robust analysis of asymmetric short-run dynamics and long-run equilibrium relationships, while addressing cross-sectional dependence and structural heterogeneity among BRICS members. These techniques provide a more rigorous empirical framework capable of identifying nonlinear, time-varying, and quantile-specific interactions that conventional estimators would miss. Fourth, the empirical results reveal a nonlinear and asymmetric relationship: FinTech has short-term destabilizing effects that transform into long-term benefits as regulatory and institutional frameworks mature, while renewable energy gradually enhances systemic resilience by reducing dependence on volatile fossil fuel markets. Finally, the study provides valuable policy implications by demonstrating that institutional quality and governance effectiveness amplify the stabilizing effects of both FinTech and renewable energy. Hence, the findings underscore the importance of integrated policy design that aligns financial innovation, clean energy investment, and institutional reform to foster a more resilient, inclusive, and sustainable financial system in emerging economies. Following the introduction, the data and empirical techniques employed in the study are presented in Section 2. The experimental results are presented in Section 3. The study is concluded with policy implications in Section 4.

2. Data and Methodology

2.1. Data

This study aims to examine the impact of FinTech and RE on the financial stability of the BRICS economies. The report utilizes balanced panel data sets. The period from 2012 to 2022 encompasses all BRICS economies: Brazil, the Russian Federation, India, China, and South Africa. The dependent variable, the financial stability Z-score (FST), is denoted Z-score and captures the soundness and robustness of a bank system using simple metrics; higher values indicate lower insolvency risk for banks. The main independent variable is Renewable energy (RE), measured as the share of renewable energy sources in total final energy consumption rather than absolute energy use. This indicator captures the structural composition of the energy mix and is more relevant for macro-financial analysis, as it reflects long-term energy diversification rather than scale effects. The other main variables are the financial technology (FINT) index, which depicts the degree of FinTech penetration in a financial system. Other control variables include Gross Domestic Product (GDP) which measures the size of total economic activity; Industrial Value Added (IND), representing how much industry sector contributes to Volumes; Institutional Quality (INS), measuring quality and effectiveness in establishment frameworks for governance of public organizations, respectively; Return On Assets (ROA) and Return On Equity (ROE) to reflect the profitability performance of banks with two different flavors interplayed against each other; and Interest Rate (INTRS), which reflects both borrowing cost as well as general monetary policy attitude. The sources of data include macroeconomic indicators from the World Bank’s World Development Indicators (WDI), financial statistics from the International Monetary Fund (IMF) and national financial authorities, energy databases, and information on FinTech indicators. The choice of the BRICS economies stems from their increasing influence in international finance, rapid financial digitalization, and growing interest in renewable energy technologies.

2.2. Definition Techniques

2.2.1. Panel Quantile Regression (PQR)

This paper introduces a new estimation and inference method for panel data, known as Panel Quantile Regression (PQR). It is an extension of traditional mean-based panel regression, just as ordinary least squares (OLS) and maximum likelihood techniques [22,23]. With panel quantile regression, we can estimate the entire conditional distribution of y given its independent variables, x, and how this distribution changes across different quantiles [24,25]. In practice, this means that panel quantile regression is not limited to analysis at a single point in the distribution but can also be used (e.g., in one-way variance analysis). This approach, as proposed by [26], enables the study of diverse relationships among variables at various points along the outcome spectrum. In addition, PQR can assess the statistical significance of various points in the distribution of x while also observing those of y. A financial and macroeconomic study finds that PQR is far better suited than methods that assume a normal distribution. PQR analyses also acknowledge the non-linearity often observed in these fields of inquiry. Studies designed to illustrate panel quantile regression typically conclude with a case in which the researcher tests effects at different points along the outcome distribution.

2.2.2. Panel Autoregressive Distributed Lag (Panel ARDL)

To capture the temporal pattern highlighted in the literature, where FinTech expansion may generate short-run market turbulence but enhances stability once regulatory and institutional structures mature, we rely on the Panel ARDL framework. This model separates immediate adjustments from long-run equilibrium effects, allowing us to observe whether FinTech shocks are destabilizing in the short run and stabilizing in the long run, as theory predicts. The autoregressive distributed lag (ARDL) model enables us to account for mixed-order variables, including I(0) and I(1), as developed by [27]. Panel ARDL Estimation can be carried out using methods that accommodate cross-sectional dependence heterogeneity [28], such as the Pooled Mean Group (PMG) or Mean Group (MG) approach [29,30]. In financial and energy economics, Panel ARDL is frequently employed to explore how economic, technological, and institutional factors jointly influence stability or sustainability over time. Consequently, given the critique that the RES share may induce spurious correlations with financial stability, we conducted several pre-estimation diagnostic procedures, including unit root testing and cross-sectional dependence assessment, to ensure that the inclusion of RES does not violate stationarity conditions. Moreover, RES is conceptually meaningful because it captures structural changes in the real economy that influence credit markets, sovereign risk, and macro-financial stability. The empirical specification, therefore, treats RES as a long-run structural determinant while allowing its short-run effects to vary, precisely to test whether its role is stabilizing or destabilizing. Therefore, our empirical interpretation distinguishes carefully between short-run and long-run dynamics. The ARDL framework is particularly suited for detecting these transitional effects, while PQR allows us to capture nonlinear and distribution-dependent responses. Consistent with recent evidence from advanced economies, this study does not assume a monotonic or universally stabilizing effect of renewable energy expansion. Instead, it considers that excessive or poorly coordinated renewable energy deployment may cause short-term instability. The use of Panel ARDL and Panel Quantile Regression explicitly captures these nonlinear and asymmetric dynamics by differentiating short-term adjustment costs from potential long-term equilibrium effects across various levels of financial stability.

2.2.3. Robustness Checks

Several robustness procedures were conducted to validate the empirical results. First, alternative specifications of the FinTech index and renewable energy share were tested, and the direction and significance of coefficients remained stable. Second, we re-estimated the PQR model using bootstrap standard errors, confirming the consistency of quantile-specific effects. Third, the ARDL results were checked using both MG and PMG estimators, which produced qualitatively similar long-run coefficients. Finally, we assessed multicollinearity and cross-sectional dependence; the results confirmed that the findings are not driven by model instability or correlated shocks across BRICS economies.

3. The Results and Discussion

3.1. Descriptive Statistics

The descriptive statistics show substantial variability in BRICS economies (Table 1). Although a value of 15.68 for FST exists, moderate changes in the standard deviation (SD) of approximately 5.33 are expected. FinTech exhibits a mean of 0.91 and a range of −0.27 to 2.01, underscoring varying levels of adoption of digital finance technologies, with China and India as the leading countries. GDP and IND highlight the structural asymmetries in production and income between China and other countries of the bloc. Among all the statistical results, the INR average of 3.40 suggests that the interest rate is moderately high, with slightly higher kurtosis at 5.16. Institutional governance indicators, with a lower value of −0.21, confirm the need for quality institutions to provide support and stability for innovation. The ROA and ROE of bank performance undergo significant changes. Although most variables exhibit moderate skewness and kurtosis, the Jarque–Bera test indicates that several variables (GDP, RE, ROE, and INR) deviate from normality at the 5% level. This supports our use of quantile-based estimation methods that do not rely on normality assumptions.

Table 1.

Descriptive statistics.

3.2. CSD Test

The results of the CSD tests [28,31,32] show p-values of 0.00, indicating strong statistical significance (Table 2). This confirms the presence of CSD among the BRICS economies, meaning that financial stability, FinTech, and renewable energy indicators are interconnected across countries. Consequently, shocks or policy changes in one BRICS member are likely to influence others, justifying the use of econometric techniques that account for such interdependence, such as Panel ARDL and Panel Quantile Regression models.

Table 2.

CSD test.

3.3. Unit Test Root

Table 3 presents the first-generation Fisher–ADF and second-generation CIPS panel unit root tests. The Fisher–ADF statistics show that all variables, except renewable energy (RE), are non-stationary at levels but become stationary after first differencing, confirming their integration order of I(1). In contrast, RE is stationary in levels, and is therefore classified as I(0). The second-generation CIPS results, which account for cross-sectional dependence, support these findings: all variables have CIPS statistics below the 5% critical value (–2.52) in first differences, while RE is stationary in levels. Overall, the panel contains a mix of I(0) and I(1) variables, validating the use of the Panel ARDL approach for further analysis.

Table 3.

Unit test root results.

3.4. The Effect Results Using the Panel ARDL

In the panel ARDL model reported in Table 4, the focus of interpretation and discussion is on both the short and long run. The results from the ARDL model provide valuable insights into the short- and long-run dynamics linking financial technology (FinTech) and RE, considering micro- and macro-variable determinants of financial stability in the BRICS economies. The model exhibits high explanatory power, with R2 = 0.95 and Adjusted R2 = 0.93, indicating that approximately 93% of the variation in financial stability is explained by the included variables. The Durbin–Watson statistic (2.45) confirms the absence of serial correlation, and the significant F-statistic of approximately 53.16 indicates a strong joint significance of the regressors. The significant coefficient for the lagged dependent variable, lagged FS, is 0.6, suggesting strong persistence in financial stability. This suggests that shocks to stability tend to be partially sustained over time and to converge with the long-run equilibrium.

Table 4.

The Panel ARDL results.

The most remarkable conclusion pertains to the development of FinTech and its impact on financial stability. The current size of FinTech has significant negative short-run implications for financial stability (−6.22 at 5%), while its lagged value carries the opposite effect and is slightly larger (6.73). This pattern of movement in time suggests that, in the short term, a proliferation of FinTech products may trigger sharp adjustments and market turbulence. However, the positive coefficient of the lagged term indicates that, after an initial period of adaptation, a mature financial system emerges, characterized by efficiency, inclusivity, and risk aversion. Economically speaking, this type of cycle suggests that while FinTech innovation may, due to the reshaping of the financial system, temporarily increase both complexity and volatility in financial markets, once regulatory frameworks and technological infrastructures are established, In the BRICS context, these findings align with the digital transformation paths of countries such as China and India, where improvements followed the initial proliferation of FinTech platforms, leading to increased financial inclusion, expanded credit channels, and enhanced supervisory capacity. Thus, the model reflects the nonlinear and transitional effects of FinTech at the beginning, which are disruptive, and thereafter stabilize as digital systems solidify.

In addition to Table 3, the RE coefficient shows a similar pattern in short-term adjustments. The current coefficient only shows positive values (0.44, p < 0.01). It means that using renewable energy in the short term to break the cycle of resource constraints, such as dependence on coal or oil, can improve financial stability and reduce volatility. The overall interpretation suggests that renewable energy indeed serves as a structural stabilizer for financial systems, particularly during economic transitions toward sustainable growth models. However, evidence from advanced economies, particularly in Europe, shows that an accelerated, unbalanced deployment of renewable energy sources can destabilize energy systems and the broader economy. The rapid expansion of intermittent renewable technologies, combined with insufficient grid flexibility, storage capacity, and policy coordination, has increased energy price volatility, fiscal burdens, and supply insecurity in several European countries. These imbalances have, in some cases, translated into macroeconomic pressures and financial stress, challenging the assumption that renewable energy expansion is unambiguously stabilizing. These results aligned with [19,20]. Estimates of economic growth coefficients indicate a positive short-run effect of 0.15, followed by a lagged negative effect of about −0.16. This cyclical pattern suggests that periods of rapid economic expansion positively affect stability by boosting profitability and reducing default risk; however, this effect tends to diminish as credit extension accelerates in subsequent periods. The result reflects the procyclical nature of financial stability, where strong growth initially increases stability [33,34]. The industrial value-added variable has a positive current coefficient of 0.62, indicating that industrial expansion reinforces financial stability by generating sound income flows from production and employment [35,36]. The interest rate coefficient is −0.10 and is statistically insignificant, indicating that monetary policy’s impact on short-term stability is minimal. This may indicate the presence of offsetting channels: on the one hand, raising interest rates will lower inflationary pressures, but on the other hand, they will increase borrowing costs and potential default risk. The institutional governance coefficient of 5.48 is highly significant and substantial in magnitude, confirming the enormous importance of institutional quality to systemic stability [37]. Profitability indicators also offer banks insights. The coefficient of Return on Assets is negative about −3.33, indicating that higher short-term profitability does not necessarily lead to greater systemic stability. In contrast, the Return on Equity is positive about 0.3, suggesting that well-capitalized banks with efficient equity deployment contribute to financial system stability.

3.5. The Panel QR Results

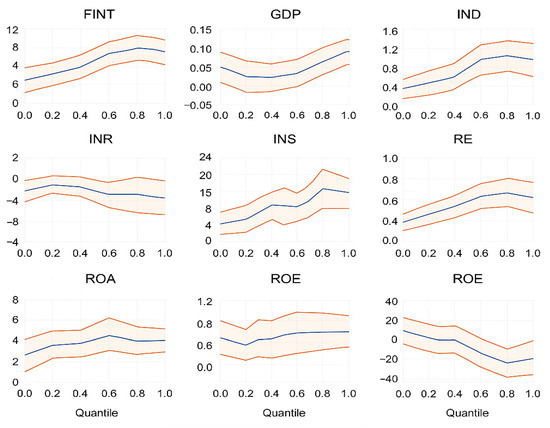

This section employs a panel QR, as shown in Table 4. The data estimates from the quantile process showed that the impacts of financial technology and renewable energy on financial stability varied across BRICS nations (Figure 1). The associated coefficient for these two variables increases smoothly from the lower quartile to the upper quartile, indicating that their contribution to financial stability strengthens as a resilient financial system emerges. In the case of FINT, the estimated coefficient for the lower quantile (0.1) is approximately 1.8, indicating a weak but positive effect in less stable environments. However, as breakdowns in stability increase, FINT’s effect becomes very marked, reaching approximately 4.5 at the median quantile (0.5) and approaching 9.0 at the upper quantile (0.9). This rising pattern demonstrates that the spread of FinTech innovation plays a crucial role in stabilizing mature financial systems by enhancing operational efficiency, promoting credit allocation, and managing risks. The findings also reveal that institutional strength influences the benefits of FinTech. Developing countries, such as China and India, with more comprehensive regulations and technical frameworks than their neighbors, Brazil and Russia, are likely to enjoy the most substantial stabilizing effects from the digital age. RE exhibits a similar, though less steep, upward trajectory across quantiles, indicating that its contribution to financial stability is gradual and continuous. At the lower quantile (0.1), it is approximately 0.25, indicating that when the economy remains in its early stage of energy transition, relying heavily on fossil fuels, a significant renewable resource allocation has only a modest impact; therefore, this effect is small. At the median quantile (0.5), the coefficient is approximately 0.55, indicating that as RE deployment becomes more intensive, these benefits are realized through regulation, with improved energy security, savings, and reduced injury from oil price downturns. At the upper quantile (0.9), the coefficient approaches 0.9, indicating that renewable energy expansion significantly enhances system resilience once clean energy becomes a substantial part of the energy mix. From a macroeconomic perspective, partial profits generated through renewables will mitigate the impact on the balance of payments. This is critically important for energy-importing economies, such as India or South Africa; in this case, the development of RE directly moderates the macroeconomic vulnerability associated with external energy price shocks. The industrial value added, regulation quality, and ROE exhibit a positive effect, while ROA and INT indicate an adverse effect across different quantiles, confirming the panel ARDL results.

Figure 1.

Quantile process estimates of Financial Stability Determinants (FST). In the quantile regression plots, the blue line denotes the estimated marginal effect of the explanatory variable across quantiles, whereas the red lines indicate the associated confidence bands, illustrating the statistical uncertainty of the estimates.

Table 5 presents the Panel Quantile Regression estimates and highlights the heterogeneous effects of FinTech, renewable energy, and the control variables across the financial stability distribution. The effect of FinTech (FINT) increases monotonically from Q0.10 (1.80) to Q0.90 (9.00), suggesting that FinTech contributes only modestly to stability in less resilient financial systems but becomes a strong stabilizing force in more mature and robust ones. This supports the argument that digital financial innovations yield greater benefits when regulatory and technological infrastructures are well established. Renewable energy (RE) shows a similar but more gradual upward pattern, moving from 0.25 at the lower quantile to 0.90 at the upper quantile. This implies that the stabilizing effects of renewable energy expand as economies progress further in their energy transition. In lower-stability environments, RE investments only marginally reduce systemic risk, but in higher-stability contexts, they significantly enhance resilience by improving energy security and reducing exposure to fossil-fuel price shocks.

Table 5.

Panel Quantile Regression (PQR) results across quantiles.

The control variables also display meaningful heterogeneity. GDP exhibits a rising positive effect across quantiles, indicating that economic expansion reinforces financial stability more strongly when the financial system is already robust. Industrial value added (IND) is consistently positive and increasing, reflecting the role of industrial development in providing stable cash flows, employment, and productive capacity—factors that support macro-financial resilience. Institutional quality (INS) is strongly positive across all quantiles. It becomes particularly influential at the upper end of the distribution, underscoring the importance of governance structures in amplifying the stabilizing effects of both FinTech and renewable energy. Profitability indicators exhibit asymmetric behavior: ROE strengthens financial stability across all quantiles and becomes more influential at higher levels. At the same time, ROA displays a consistently negative effect, echoing the ARDL results that short-term asset-driven profitability may reflect risk-taking behavior. The interest rate (INTRS) shows mild negative effects at all quantiles, suggesting that monetary tightening slightly reduces stability, though the magnitude is small. Overall, the PQR findings reinforce the nonlinear, quantile-specific nature of financial stability determinants and complement the ARDL results by illustrating how FinTech, renewable energy, and structural factors exert differentiated impacts across financial system conditions.

Beyond FinTech and renewable energy, the PQR results reveal heterogeneous effects of the control variables across the financial stability distribution. GDP shows a positive, increasing impact across the lower to upper quantiles, indicating that economic expansion contributes more strongly to financial resilience in already stable systems. Industrial value added (IND) shows a consistently positive effect across all quantiles, aligning with ARDL findings and suggesting that structural production capacity remains a key stabilizing factor. Institutional quality (INS) becomes more influential in higher quantiles, reinforcing the view that strong governance enhances systemic robustness, particularly in financially mature economies. Profitability indicators exhibit asymmetry: ROE shows a rising positive effect across quantiles, while ROA remains negative across the distribution, echoing the short-run ARDL interpretation that asset-based profitability may entail higher risk exposure. Interest rates (INTRS) show a mild negative effect across all quantiles, with the magnitude remaining small, consistent with limited short-run monetary transmission in BRICS. These results confirm the heterogeneous and nonlinear architecture of financial stability determinants and complement the ARDL findings by illustrating how structural, institutional, and profitability dynamics vary across different states of financial resilience.

The heterogeneous effects identified in this study are consistent with an emerging body of recent global and regional evidence. For instance, several cross-country studies confirm that FinTech adoption produces nonlinear stability responses, initially raising short-term operational and credit risks while improving long-run intermediation efficiency [38,39]. Similar patterns have been documented in Europe and the MENA region, where FinTech-enabled credit expansion improved inclusion but required stronger supervisory oversight to preserve stability [2]. Parallel findings emerge in renewable-energy finance: recent analyses show that steady increases in renewable capacity reinforce macro-financial resilience by reducing energy-price volatility and sovereign risk, though the magnitude depends on institutional governance and capital-market depth [40,41]. Country-specific work from emerging Asia and Latin America also supports the view that the interaction between clean-energy investment and financial-system quality determines whether renewable energy exerts stabilizing or destabilizing effects [19]. Collectively, this new evidence is aligned with the results observed for BRICS economies, reinforcing the conclusion that technological innovation and energy transition strengthen financial stability when supported by sound institutions, effective regulatory capacity, and sustainable investment frameworks [42].

4. Conclusions and Policy Implications

This study provides empirical evolutionary evidence on the dynamic and asymmetric impacts of financial technology and renewable energy on financial stability in BRICS economies from 2012 to 2022. Using a mix of PQR and panel ARDL models, the findings suggest that FinTech and renewable energy jointly strengthen the structural foundations of economic development, and their effects complement one another across different time horizons. The PQR estimates suggest that as the distribution of financial stability becomes richer. The ARDL results, meanwhile, make explicit both the short-run adjustment dynamics and the long-run equilibrium relationships among technological, structural, and institutional determinants of stability. From a policy perspective, these findings have several implications. Pilot regulatory programs and supervisory technologies can help manage innovation-induced volatility, while also accelerating the safe implementation of digital finance. The second implication is that to maintain macroeconomic and financial stability and achieve sustainable development, policy support for clean energy must be consistent with the financial sector’s strategy through means such as issuing green bonds, implementing carbon pricing, and establishing climate disclosure standards. By enticing private capital into innovation investment, such as through FinTech financing platforms, the funding side can diversify and thus improve the resilience of sustainable finance. In the short term, reducing adjustment costs and protecting against digital and energy shocks are crucial. On the other hand, policy objectives in the longer run should aim to shape a comprehensive system where economic innovation is in tune with environmental sustainability, alongside other dimensions such as quality upgrading and institutional reform. This study has several limitations. Although the PQR and Panel ARDL approaches address heterogeneity and dynamics, time-varying effects cannot be entirely excluded. Third, the dataset ends in 2022 and does not reflect more recent shocks. Finally, using aggregate national data may mask significant differences within a country. Future work could address these issues by employing instrumental-variable quantile methods and finer-grained datasets. Although our findings point to a stabilizing long-run effect, RES may also reflect deeper structural characteristics of BRICS economies. Future research could incorporate alternative measures of the energy transition, apply instrumental-variable quantile regressions, and explore potential endogeneity between RES expansion and financial stability.

Author Contributions

Methodology, S.A.R.S.; Software, S.A.R.S.; Validation, K.S.M.; Writing—original draft, S.B.A.; Writing—review & editing, K.S.M. All authors have read and agreed to the published version of the manuscript.

Funding

The authors extend their appreciation to the Deanship of Scientific Research at King Khalid University for funding this work through large group Research Project under grant number RGP2/570/46.

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors on request.

Acknowledgments

The authors extend their appreciation to the Deanship of Scientific Research at King Khalid University for funding this work through large group Research Project under grant number RGP2/570/46.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Curea, M.; Huian, M.C.; Zecca, F.; Balu, F.O.; Mironiuc, M. Green Goals, Financial Gains: SDG 7 “Affordable and Clean Energy” and Bank Profitability in Romania. Energies 2025, 18, 3252. [Google Scholar] [CrossRef]

- Afzal, A.M.; Abu Khalaf, B.; Al-Naimi, M.S.; Samara, E. The Impact of Fintech on the Stability of Middle Eastern and North African (MENA) Banks. Risks 2025, 13, 106. [Google Scholar] [CrossRef]

- Meero, A. Islamic vs. Conventional Banking in the Age of FinTech and AI: Evolving Business Models, Efficiency, and Stability (2020–2024). Int. J. Financ. Stud. 2025, 13, 148. [Google Scholar] [CrossRef]

- Dai, B.; Zhang, J.; Hussain, N. Policy pathways through FinTech and green finance for low-carbon energy transition in BRICS nations. Energy Strategy Rev. 2025, 57, 101603. [Google Scholar] [CrossRef]

- Sun, Y.; Li, T.; Mehmood, U. Balancing acts: Assessing the roles of renewable energy, economic complexity, Fintech, green finance, green growth, and economic performance in G-20 countries amidst sustainability efforts. Appl. Energy 2025, 378, 124846. [Google Scholar] [CrossRef]

- Bruno, E.; Pistolesi, F.; Teti, E. Cybersecurity policy, ESG and operational risk: A Virtuous relationship to improve banks’ performance. Int. Rev. Econ. Finance 2025, 99, 104053. [Google Scholar] [CrossRef]

- Wang, J.; Huang, X.; Gu, Q.; Song, Z.; Sun, R. How does fintech affect bank risk? A perspective based on financialized transfer of government implicit debt risk. Econ. Model. 2023, 128, 106498. [Google Scholar] [CrossRef]

- Kakar, S.K.; Wang, J.; Arshed, N.; Le Hien, T.T.; Akhter, S.; Abdullahi, N.M. The impact of circular economy, sustainable infrastructure, and green FinTech on biodiversity in Europe: A holistic approach. Technol. Soc. 2025, 81, 102841. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Abakah, E.J.A.; Shao, X.; Le, T.-L.; Gyamfi, M.N. Financial technology stocks, green financial assets, and energy markets: A quantile causality and dependence analysis. Energy Econ. 2023, 118, 106498. [Google Scholar] [CrossRef]

- Cevik, S. Is Schumpeter right? Fintech and economic growth. Econ. Innov. New Technol. 2025, 34, 1095–1106. [Google Scholar] [CrossRef]

- Esquivias, M.A.; Sugiharti, L.; Rohmawati, H.; Rojas, O.; Sethi, N. Nexus between Technological Innovation, Renewable Energy, and Human Capital on the Environmental Sustainability in Emerging Asian Economies: A Panel Quantile Regression Approach. Energies 2022, 15, 2451. [Google Scholar] [CrossRef]

- Mohd Suki, N.; Mohd Suki, N.; Afshan, S.; Sharif, A.; Ariff Kasim, M.; Rosmaini Mohd Hanafi, S. How does green technology innovation affect green growth in ASEAN-6 countries? Evidence from advance panel estimations. Gondwana Res. 2022, 111, 165–173. [Google Scholar] [CrossRef]

- Jangid, H.; Bal, D.P.; Rao, N.V.M. Role of FinTech and technological innovation towards energy, growth, and environment nexus in G20 economies. Sci. Rep. 2025, 15, 20057. [Google Scholar] [CrossRef]

- Keen, S. Emergent Macroeconomics: Deriving Minsky’s Financial Instability Hypothesis Directly from Macroeconomic Definitions. Rev. Polit. Econ. 2020, 32, 342–370. [Google Scholar] [CrossRef]

- Udeagha, M.C.; Ngepah, N. The drivers of environmental sustainability in BRICS economies: Do green finance and fintech matter? World Dev. Sustain. 2023, 3, 100096. [Google Scholar] [CrossRef]

- Jahanger, A.; Awan, A.; Anwar, A.; Adebayo, T.S. Greening the Brazil, Russia, India, China and South Africa (BRICS) economies: Assessing the impact of electricity consumption, natural resources, and renewable energy on environmental footprint. In Natural Resources Forum; Blackwell Publishing Ltd.: Oxford, UK, 2023. [Google Scholar] [CrossRef]

- Radulescu, M.; Si Mohammed, K.; Kumar, P.; Baldan, C.; Dascalu, N.M. Dynamic effects of energy transition on environmental sustainability: Fresh findings from the BRICS+1. Energy Rep. 2024, 12, 2441–2451. [Google Scholar] [CrossRef]

- Nguyen, Q.K.; Dang, V.C. Renewable energy consumption, carbon dioxide emission and financial stability: Does institutional quality matter? Appl. Econ. 2024, 56, 8820–8837. [Google Scholar] [CrossRef]

- Imran, M.; Khan, M.K.; Alam, S.; Wahab, S.; Tufail, M.; Jijian, Z. The implications of the ecological footprint and renewable energy usage on the financial stability of South Asian countries. Financ. Innov. 2024, 10, 102. [Google Scholar] [CrossRef]

- Kirikkaleli, D.; Sofuoğlu, E. Does financial stability matter for environmental degradation? Geol. J. 2023, 58, 3268–3277. [Google Scholar] [CrossRef]

- Alsagr, N. Financial efficiency and its impact on renewable energy investment: Empirical evidence from advanced and emerging economies. J. Clean. Prod. 2023, 401, 136738. [Google Scholar] [CrossRef]

- Cho, J.S.; Kim, T.H.; Shin, Y. Quantile cointegration in the autoregressive distributed-lag modeling framework. J. Econom. 2015, 188, 281–300. [Google Scholar] [CrossRef]

- Sim, N.; Zhou, H. Oil prices, US stock return, and the dependence between their quantiles. J. Bank. Financ. 2015, 55, 1–8. [Google Scholar] [CrossRef]

- Shahzad, U.; Tiwari, S.; Si Mohammed, K.; Zenchenko, S. Asymmetric nexus between renewable energy, economic progress, and ecological issues: Testing the LCC hypothesis in the context of sustainability perspective. Gondwana Res. 2024, 129, 465–475. [Google Scholar] [CrossRef]

- Voumik, L.C.; Islam, M.d.A.; Ray, S.; Mohamed Yusop, N.Y.; Ridzuan, A.R. CO2 Emissions from Renewable and Non-Renewable Electricity Generation Sources in the G7 Countries: Static and Dynamic Panel Assessment. Energies 2023, 16, 1044. [Google Scholar] [CrossRef]

- Koenker, R.; Bassett, G. Regression Quantiles. Econometrica 1978, 46, 33–50. [Google Scholar] [CrossRef]

- Shin, Y.; Yu, B.; Greenwood-Nimmo, M. Modelling Asymmetric Cointegration and Dynamic Multipliers in a Nonlinear ARDL Framework. In Festschrift in Honor of Peter Schmidt; Sickles, R., Horrace, W., Eds.; Springer: New York, NY, USA, 2014. [Google Scholar] [CrossRef]

- Pesaran, M.H. General Diagnostic Tests for Cross Section Dependence in Panels; Working Paper No. 0435; University of Cambridge: Cambridge, UK, 2004. [Google Scholar]

- Sadik-Zada, E.R.; Ferrari, M. Environmental policy stringency, technical progress and pollution haven hypothesis. Sustainability 2020, 12, 3880. [Google Scholar] [CrossRef]

- Anser, M.K.; Syed, Q.R.; Lean, H.H.; Alola, A.A.; Ahmad, M. Do Economic Policy Uncertainty and Geopolitical Risk Lead to Environmental Degradation? Evidence from Emerging Economies. Sustainability 2021, 13, 5866. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Ullah, A.; Yamagata, T. A bias-adjusted LM test of error cross-section independence. Econom. J. 2008, 11, 105–127. [Google Scholar] [CrossRef]

- Breusch, T.S.; Pagan, A.R. The Lagrange Multiplier Test and its Applications to Model Specification in Econometrics. Rev. Econ. Stud. 1980, 47, 239. [Google Scholar] [CrossRef]

- Adedoyin, F.F.; Erum, N.; Ozturk, I. Does higher innovation intensity matter for abating the climate crisis in the presence of economic complexities? Evidence from a Global Panel Data. Technol. Forecast. Soc. Change 2022, 181, 121762. [Google Scholar] [CrossRef]

- Algaeed, A.H.; Algethami, B.S. Monetary volatility and the dynamics of economic growth: An empirical analysis of an oil-based economy, 1970–2018. OPEC Energy Rev. 2023, 47, 3–18. [Google Scholar] [CrossRef]

- Kumar, B.; Kumar, J.; Amjad, A.Q.; Kumar, L.; Sassanelli, C. Sustainable aviation finance: Integration of environmental impact mitigation and green investment strategies. Res. Transp. Bus. Manag. 2025, 61, 101410. [Google Scholar] [CrossRef]

- Fedajev, A.; Mitić, P.; Kojić, M.; Radulescu, M. Driving industrial and economic growth in Central and Eastern Europe: The role of electricity infrastructure and renewable energy. Util. Policy 2023, 85, 101683. [Google Scholar] [CrossRef]

- Huang, L.; Lu, F. The Cost of Russian Sanctions on the Global Equity Markets. SSRN Electron. J. 2022. [Google Scholar] [CrossRef]

- Koranteng, B.; You, K. Fintech and financial stability: Evidence from spatial analysis for 25 countries. J. Int. Financ. Mark. Inst. Money 2024, 93, 102002. [Google Scholar] [CrossRef]

- Anestiawati, C.A.; Amanda, C.; Khantinyano, H.; Agatha, A. Bank FinTech and credit risk: Comparison of selected emerging and developed countries. Stud. Econ. Financ. 2025. [Google Scholar] [CrossRef]

- Razi, U.; Karim, S.; Cheong, C.W.H. From turbulence to resilience: A bibliometric insight into the complex interactions between energy price volatility and green finance. Energy 2024, 304, 131992. [Google Scholar] [CrossRef]

- Kassi, D.F.; Sun, G.; Ding, N. Does governance quality moderate the finance-renewable energy-growth nexus? Evidence from five major regions in the world. Environ. Sci. Pollut. Res. 2020, 27, 12152–12180. [Google Scholar] [CrossRef]

- Mirza, N.; Umar, M.; Lobont, O.-R.; Safi, A. ESG lending, technology investment and banking performance in BRICS: Navigating sustainability and financial stability. China Financ. Rev. Int. 2025, 15, 324–336. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.