Multi-Faceted Collaborative Investment Models and Investment Benefit Assessment Under the New Type Power System

Abstract

1. Introduction

2. Literature Review

2.1. Multiple Investment Entities

2.2. Project Investment Benefit Evaluation

2.3. Research Progress on Comprehensive Decision-Making and Modeling of Energy Systems

3. Analysis of Diversified Investment Subjects and Investment Modes

3.1. Analysis of Multiple Investment Entities

3.2. Analysis of Multi-Subject Investment Mode

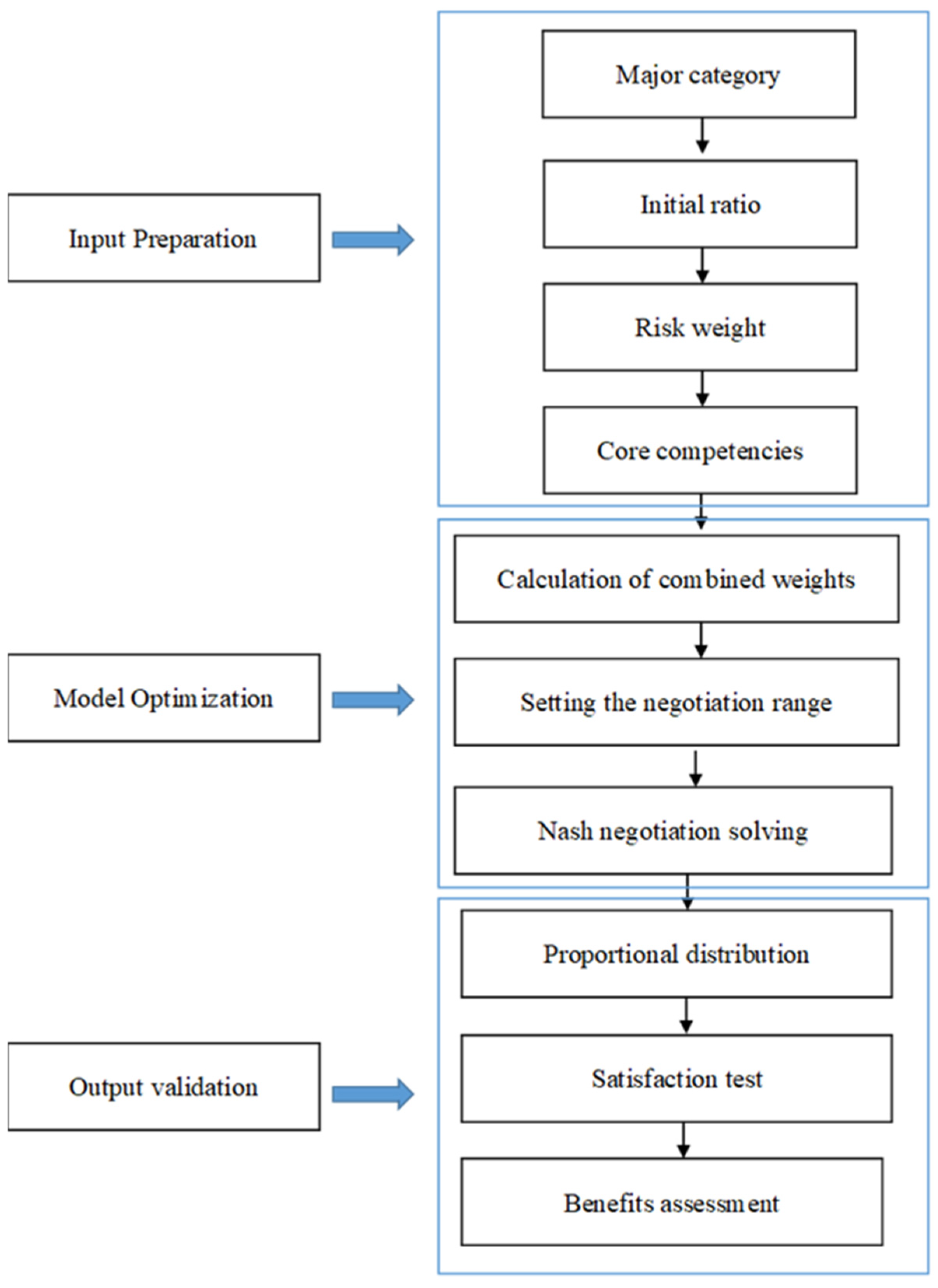

4. Calculation of Optimal Investment Proportion of Multiple Investment Entities

- (i).

- The dominance of grid companies (Type A) in risk-taking (Section 3.1),

- (ii).

- The environmental/social weights mandated by China’s ‘dual-carbon’ goals.

4.1. Theoretical Basis for Optimizing the Investment Ratio of Multiple Investment Entities

4.2. Key Influencing Factors of Optimal Investment Ratio Measurement

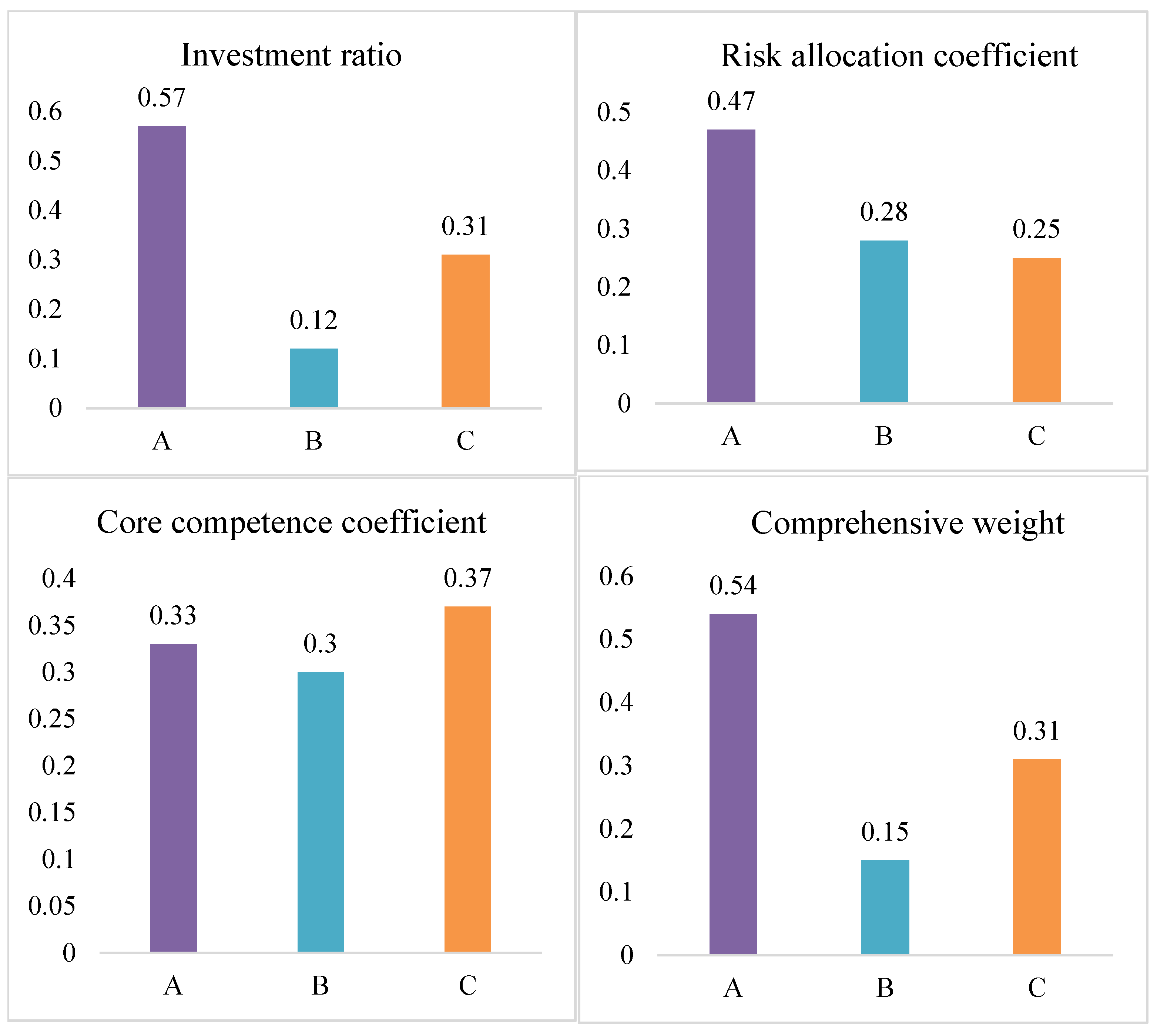

4.2.1. Initial Investment Ratio

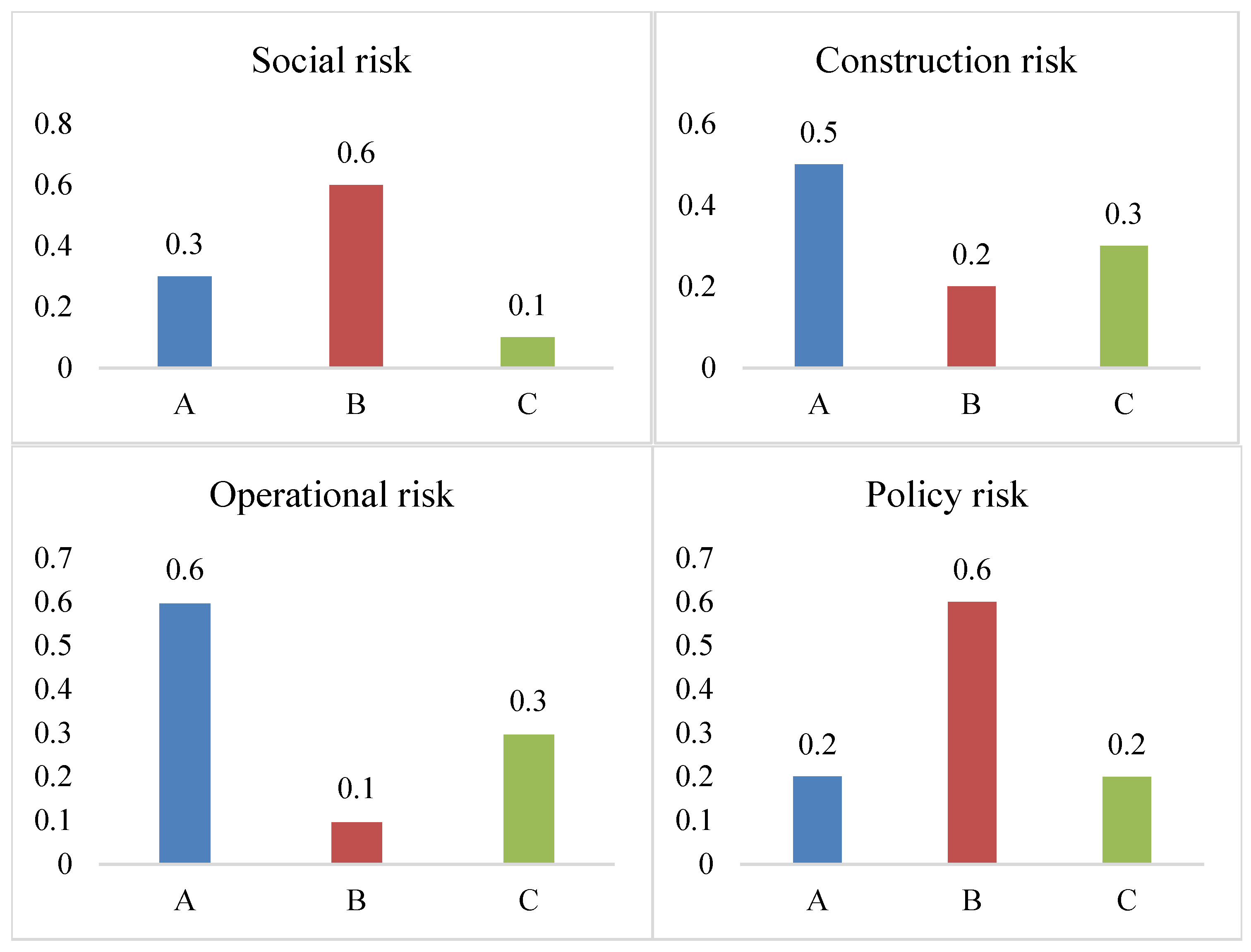

4.2.2. Risk Allocation Coefficient

4.2.3. Core Competence Coefficient

4.2.4. The Weight of Investment Entities

4.3. Multi-Subject Investment Proportion Optimization Model

5. Project Investment Benefit Analysis and Evaluation Model

5.1. Construction of Investment Benefit Evaluation Index System

5.2. Construction of Investment Benefit Analysis Model

5.2.1. Determining the Weight of Investment Benefit Analysis Index

5.2.2. Investment Benefit Analysis Model

6. Multi-Energy Complementary Energy System Project Investment Case Analysis

6.1. Project Introduction

6.2. Composition of Multiple Investment Entities of the Project

6.3. Comparative Analysis of Project Investment Costs Under Different Investment Modes

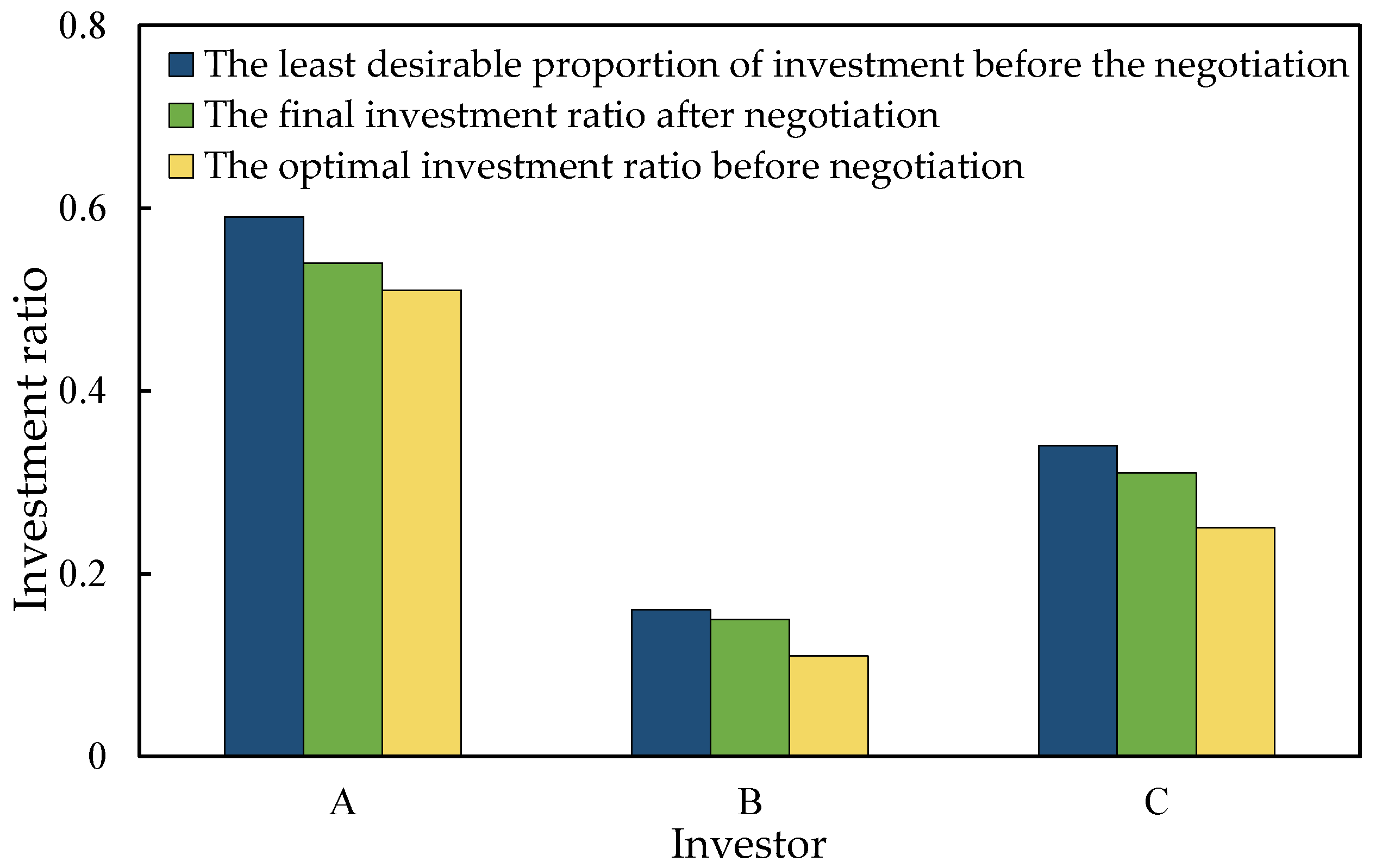

6.4. Optimization of the Investment Proportion of Multiple Investment Entities

6.5. Analysis of Project Alliance Stability and Investor Satisfaction

6.6. Analysis and Evaluation of Project Investment Benefit

7. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Jiang, T.; Yang, J.; Huang, S. Evolution and driving factors of CO2 emissions structure in China’s heating and power industries: The supply-side and demand-side dual perspectives. J. Clean. Prod. 2020, 264, 121507. [Google Scholar] [CrossRef]

- Cao, Y.; Zhang, S. Facilitating the provision of load flexibility to the power system by data centers: A hybrid research method applied to China. Util. Policy 2023, 84, 101636. [Google Scholar] [CrossRef]

- Liu, X. Research on collaborative scheduling of internet data center and regional integrated energy system based on electricity-heat-water coupling. Energy 2024, 292, 130462. [Google Scholar] [CrossRef]

- Zhu, Z.; Wang, D.; Tang, B.; Zhao, X.; Gu, G.; Yang, P.; Lai, X. Co-optimization of distributed generation, flexible load, and energy storage for promoting renewable energy consumption and power balancing in distribution networks. Electr. Power Syst. Res. 2025, 238, 111124. [Google Scholar] [CrossRef]

- Aziz, S.; Chowdhury, S.A.; Alauddin, M. Investment risks and policy solutions for renewable electricity in Bangladesh. Energy Sustain. Dev. 2025, 85, 101605. [Google Scholar] [CrossRef]

- Liao, K.; Li, X.; Xie, H. Regional Difference decomposition and dynamic effect evaluation of Chinese local government investment efficiency-based on the perspective of economic and social efficiency. J. Quant. Technol. Econ. 2019, 36, 42–63. [Google Scholar] [CrossRef]

- Jin, S.; Xiong, R.; Peng, H.; Tang, S. ESG performance and private enterprise resilience: Evidence from Chinese financial markets. Int. Rev. Financ. Anal. 2025, 98, 103884. [Google Scholar] [CrossRef]

- Bridget, O.M.; Theophilus, A. Crowdfunding renewable energy investments: Investor perceptions and decision-making factors in an emerging market. Energy Res. Soc. Sci. 2024, 114, 103602. [Google Scholar] [CrossRef]

- Zhang, M.; Nie, J.; Su, B.; Liu, L. An option game model applicable to multi-agent cooperation investment in energy storage projects. Energy Econ. 2024, 131, 107397. [Google Scholar] [CrossRef]

- Yue, H.; Zhang, Y.; Guo, J.; Hu, Y.; Wei, C.; Jia, H.; Liu, D.; Xie, D. Analysis and construction of evaluation index system of inter-provincial electricity spot markets. Glob. Energy Interconnect. 2024, 7, 697–706. [Google Scholar] [CrossRef]

- Liu, Z.; Wu, J. Evaluation index system for carbon information disclosure quality in China’s electric power sector based on a mutual information and back propagation neural network model. Util. Policy 2024, 89, 101781. [Google Scholar] [CrossRef]

- Lyu, Y.; Luo, Y.; Jia, Z.; Fu, S.; Tang, Y.; Wang, Q.; Zeng, Y. Benefit evaluation of HVAC and HVDC for offshore wind power transmission system under the multidimensional index. Electr. Power Syst. Res. 2024, 237, 111018. [Google Scholar] [CrossRef]

- Xu, Y.; Du, R.; Pei, J. The investment risk evaluation for onshore and offshore wind power based on system dynamics method. Sustain. Energy Technol. Assess. 2023, 58, 103328. [Google Scholar] [CrossRef]

- Ji, Z.; Yu, X.; Li, W.; Niu, D. A multi-criteria decision-making framework for distributed generation projects investment considering the risk of electricity market trading. J. Clean. Prod. 2023, 416, 137837. [Google Scholar] [CrossRef]

- Choorikkat, S.; Lee, Y.; Hsu, H. Model for subsidizing industry and power company through gray-electricity taxation. Renew. Sustain. Energy Rev. 2025, 211, 115291. [Google Scholar] [CrossRef]

- Amiri-Pebdani, S.; Alinaghian, M.; Khosroshahi, H. A game theoretic approach for time-of-use pricing with considering renewable portfolio standard effects and investment in energy storage technologies under government interventions. Energy 2023, 282, 128721. [Google Scholar] [CrossRef]

- Zhao, J.; Zhang, C.; Wu, Y.; Zhu, J. Dual driving forces for corporate environmental responsibility performance: The synergistic effects of government environmental regulation and market multi-agent green supervision. Sci. Total Environ. 2024, 949, 174790. [Google Scholar] [CrossRef]

- Cui, Y.; Wang, W.; Wang, Q.; Li, Q. Characteristics and optimization strategies of multi-subject governance network structure for land consolidation. J. Rural. Stud. 2024, 112, 103470. [Google Scholar] [CrossRef]

- Zhang, C.; Jin, X.; Xie, G. Method to extract critical characteristics of power grid projects adapting to new situations and construction of index system. Energy Rep. 2022, 8, 533–539. [Google Scholar] [CrossRef]

- He, C.; Zhou, S.; Zhang, M.; Hou, J. Research and application of project post-evaluation based on company ESG investment concept. Reform Openning 2022, 37, 64–72. [Google Scholar] [CrossRef]

- Song, X.; Yang, Q.; Wan, J. The Principle and Method of Economic Efficiency Evaluation of Project Capital Rationing. Chin. J. Manag. Sci. 2002, 19, 46–49. [Google Scholar] [CrossRef]

- Liao, H.; Yuan, N. Evaluation index and evaluation method of project investment decision. Stat. Decis. 2021, 37, 181–185. [Google Scholar] [CrossRef]

- Zou, H. Post-evaluation of government investment projects: Logical orientation, system inspection and legal regulation. Adm. Trib. 2022, 29, 147–154. [Google Scholar] [CrossRef]

- Xue, J.; Dai, X.; Xiao, L.; Wang, Q.; Li, M.C. Multi-objective carbon-energy portfolio optimization under investment horizon heterogeneity. Res. Int. Bus. Financ. 2025, 79, 103036. [Google Scholar] [CrossRef]

- Koutsandreas, D.; Keppo, I. Harnessing machine learning algorithms to unveil energy efficiency investment archetypes. Energy Rep. 2024, 12, 3180–3195. [Google Scholar] [CrossRef]

- Cheng, F.; Huang, P.; Zou, T.; Zhang, M.; Peng, P.; Lu, W. Evolutionary game-theoretical approaches for long-term strategic bidding among diverse stakeholders in large-scale and local power markets: Basic concept, modelling review, and future vision. Int. J. Electr. Power Energy Syst. 2025, 166, 110589. [Google Scholar] [CrossRef]

- Zheng, H.; Wu, Z. Enhancing economic and environmental performance of energy communities: A multi-objective optimization approach with mountain gazelle optimizer. Sustain. Comput. Inform. Syst. 2025, 46, 101098. [Google Scholar] [CrossRef]

- Ruan, Y.; Wang, W.; Abubakar, M.; Ahmad, N. Global economic resilience: Developing green growth strategies, renewable energy integration, and environmental economics for sustainability. Renew. Energy 2025, 251, 123341. [Google Scholar] [CrossRef]

- Lilliu, F.; Recupero, D.R. A cooperative game-theory approach for incentive systems in local energy communities. Sustain. Energy Grids Netw. 2024, 38, 101391. [Google Scholar] [CrossRef]

- Lokeshgupta, B.; Sivasubramani, S. Cooperative game theory approach for multi-objective home energy management with renewable energy integration. IET Smart Grid 2019, 2, 34–41. [Google Scholar] [CrossRef]

- Malik, S.; Duffy, M.; Thakur, S.; Hayes, B.; Breslin, J. A priority-based approach for peer-to-peer energy trading using cooperative game theory in local energy community. Int. J. Electr. Power Energy Syst. 2022, 137, 107865. [Google Scholar] [CrossRef]

- Han, L.; Morstyn, T.; McCulloch, M. Incentivizing prosumer coalitions with energy management using cooperative game theory. IEEE Trans. Power Syst. 2018, 34, 303–313. [Google Scholar] [CrossRef]

- Harsanyi, J.C. Chapter 19 Game and decision theoretic models in ethics. Handb. Game Theory Econ. Appl. 1992, 1, 669–707. [Google Scholar] [CrossRef]

- Yu, H.; Xu, F.; Chen, C.; Chen, Y.; Zhang, W.; Yang, L.; Lin, Z. Asymmetric Nash bargaining-based community-centric energy sharing strategy for numerous prosumers. Energy 2025, 316, 134468. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| The Investment Subject | Investment Role | Industry Background |

|---|---|---|

| Individual creditors | Commercial banks, securities companies, industrial funds, etc. | The return on investment through borrowing benefits can alleviate the capital pressure of investment planning and share certain risks of financial and market operations. |

| Government sector | Local government investment platform, city investment, state investment, etc. | It has the advantage of approving projects, franchising rights, providing funds and policy support, and buying shares with funds. |

| Specialized corporation | Power grid enterprises | With talent, technology, management, and other advantages in the power industry, with capital, technology shares in the distribution company. |

| Power generation group | With distributed power investment, operation, and other technical advantages, with capital and technology investment, improve the project’s distributed power investment and operation efficiency. | |

| Social capital | Activating capital can improve the vitality of project investment and operation. | |

| Energy public service corporation | It has technical advantages in the construction, operation, and maintenance of energy supply equipment and other aspects of the industry and invests in capital and technology. While coordinating the coordinated operation of cold, hot, and electricity sources in the distribution network, value-added services such as integrated energy services, energy conservation and efficiency, and intelligent electricity consumption can be developed. |

| Investment Pattern | Operation Mode | Paraphrase |

|---|---|---|

| Independent investment | Independent operation | Independently undertake project investment, construction, and operation. |

| Co-investment | Direct operation | Participate in the investment, construction, and operation of the project. |

| Entrusted operation | Only participate in the operation of the project, not participate in the investment and construction of the project. | |

| Lease operation | Only participate in the investment and construction of the project, not participate in the operation of the project. |

| Destination Layer | Criterion Layer | Scheme Layer |

|---|---|---|

| Investment benefits (B) | Economic benefits of investment (B1) | Total project investment cost (B11) Annual operation and maintenance cost of the project (B12) Annual operating income of the project (B13) Net present value (B14) Payback period (B15) Internal rate of return (B16) |

| Environmental benefits of investment (B2) | Energy saving and emission reduction (B21) Renewable energy consumption increased proportionally (B22) | |

| Social benefits of investment (B3) | The rate of technology update (B31) Policy intensity (B32) Multi-energy complementary operation mode (B33) |

| Investment Benefits | Economic Benefits of Investment | Environmental Benefits of Investment | Social Benefits of Investment | Weight |

|---|---|---|---|---|

| Economic benefits of investment | 1.00 | 3.00 | 3.00 | 0.5936 |

| Environmental benefits of investment | 0.33 | 1.00 | 2.00 | 0.2493 |

| Social benefits of investment | 0.33 | 0.50 | 1.00 | 0.1571 |

| CR = 0.0516 < 0.1, which has consistency. | ||||

| Criterion Layer | Weight | Scheme Layer | Weight |

|---|---|---|---|

| Economic benefits of investment (B1) | W1 = 0.5936 | Total project investment cost (B11) Annual operation and maintenance cost of the project (B12) Annual operating income of the project (B13) Net present value (B14) Payback period (B15) Internal rate of return (B16) | W11 = 0.1390 W12 = 0.0675 W13 = 0.2021 W14 = 0.1494 W15 = 0.1236 W16 = 0.3183 |

| Environmental benefits of investment (B2) | W2 = 0.2493 | Energy saving and emission reduction (B21) Renewable energy consumption increased proportionally (B22) | W21 = 0.7249 W22 = 0.2751 |

| Social benefits of investment (B3) | W3 = 0.1571 | The rate of technology update (B31) Policy intensity (B32) Multi-energy complementary operation mode (B33) | W31 = 0.2217 W32 = 0.5489 W33 = 0.2294 |

| Parameter Index | Data | Unit |

|---|---|---|

| 35 kV gathering station | 2 × 10 | MVA |

| Storage capacity | 5/10 | MW/MWh |

| Micro gas turbine | 300 | kW |

| Electric boiler | 2160 | kW |

| Gas boiler | 4 | t/h |

| Annual electricity supply | 35,000 | MW |

| Annual heat supply | 21 × 104 | GJ |

| Total project investment | 8444.35 | ten thousand yuan |

| Equipment lifetime | 20 | year |

| Annual operation and maintenance costs | 2592.3 | ten thousand yuan |

| Average tariff | 0.72 | yuan/kWh |

| Heat selling price | 34.6 | yuan/GJ |

| Parameter | Meaning | Value and Unit |

|---|---|---|

| The part of the investment that is not related to substation capacity. | 150,000 yuan | |

| Coefficient of linear relationship between investment and substation capacity. | 50 yuan | |

| The coefficient of the investment is independent of the cross-sectional area of the conductor. | 20,000 yuan | |

| Coefficient of the linear relationship between investment and cross-sectional area of wire. | 100 | |

| Annualized coefficient. | 5% | |

| Coefficient of operation and maintenance cost. | 8% | |

| The overall loss rate of the incremental distribution network. | 4% | |

| Power generation ratio | 1.5 |

| Time Frame | Price/(Yuan/(kW·h)) | ||

| Sell Electricity | Purchasing Electricity | ||

| During peak demand | 8:00—12:00 17:00—21:00 | 1.0902 | 0.8722 |

| At ordinary times | 12:00—17:00 21:00—24:00 | 0.6541 | 0.5232 |

| During low demand | 0:00—8:00 | 0.3180 | 0.2544 |

| Types of Investment | Direct Operation (Cooperative) | Independent Operation | ||

|---|---|---|---|---|

| Cost/104 Yuan | Proportion/% | Cost/104 Yuan | Proportion/% | |

| Power purchase cost | 1648.89 | 53.88 | 2317.50 | 58.54 |

| Gas purchase cost | 933.82 | 30.52 | 702.62 | 17.75 |

| Distribution network construction costs | 38.57 | 1.26 | 75.02 | 1.89 |

| Energy conversion equipment costs | 52.95 | 1.73 | 0 | 0 |

| Energy storage construction cost | 385.91 | 12.61 | 864.00 | 21.82 |

| Total | 3060.14 | 100 | 3959.14 | 100 |

| Investor | Innovation Ability | Core Technology | Collaborative Ability |

|---|---|---|---|

| A | 0.2 | 0.6 | 0.2 |

| B | 0.2 | 0.1 | 0.6 |

| C | 0.6 | 0.3 | 0.2 |

| Investor | Negotiation Basis | Degree of Satisfaction | Deviation Value |

|---|---|---|---|

| A | 5.000 | 19.421 | 14.421 |

| B | 2.000 | 2.1866 | 0.1866 |

| C | 2.5000 | 3.1837 | 0.6837 |

| Primary Index | Secondary Index | Three-Level Index | Data | Unit |

|---|---|---|---|---|

| Investment benefits (B) | Economic benefits of investment (B1) | Total project investment cost (B11) Annual operation and maintenance cost of the project (B12) Annual operating income of the project (B13) Net present value (B14) Payback period (B15) Internal rate of return (B16) | 8444.353 2592.302 3403.6 1666.041 10.409 6.91 | 104 yuan 104 yuan 104 yuan 104 yuan year % |

| Environmental benefits of investment (B2) | Energy saving and emission reduction (B21) Renewable energy consumption increased in proportion (B22) | 20,916 23 | t % | |

| Social benefits of investment (B3) | The rate of technology update (B31) Policy intensity (B32) Multi-energy complementary operation mode (B33) | 4 8 8 | % minute minute |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, P.; Lan, L.; Qian, Y.; Guo, M.; Zhao, W. Multi-Faceted Collaborative Investment Models and Investment Benefit Assessment Under the New Type Power System. Energies 2025, 18, 4031. https://doi.org/10.3390/en18154031

Chen P, Lan L, Qian Y, Guo M, Zhao W. Multi-Faceted Collaborative Investment Models and Investment Benefit Assessment Under the New Type Power System. Energies. 2025; 18(15):4031. https://doi.org/10.3390/en18154031

Chicago/Turabian StyleChen, Peng, Li Lan, Yanyuan Qian, Mingxing Guo, and Wenhui Zhao. 2025. "Multi-Faceted Collaborative Investment Models and Investment Benefit Assessment Under the New Type Power System" Energies 18, no. 15: 4031. https://doi.org/10.3390/en18154031

APA StyleChen, P., Lan, L., Qian, Y., Guo, M., & Zhao, W. (2025). Multi-Faceted Collaborative Investment Models and Investment Benefit Assessment Under the New Type Power System. Energies, 18(15), 4031. https://doi.org/10.3390/en18154031