Abstract

Purpose: The main purpose of this paper is to determine how particular audit firms deal with ISA 701 requirements and the society expectations towards reporting the materiality levels. Additionally, the aim of this paper is to range the assertions in terms of the frequency of their occurrence. Design/methodology/approach: The tested sample consisted of 317 companies listed on Warsaw (158 companies) or London (159 companies) stock exchange. The analysis was divided into companies from the following ten market indexes (WIGs): construction, IT, real estate, food, media, oil and gas, mining, energy, automotive and chemicals. The research was executed based on the analysis of annual consolidated financial statements (annual reports) and independent auditor reports that were published by in-scope entities for the latest twelve-months period available as at the date of the research (mostly periods ended on 31 December 2017 and 31 March 2018). All values were denominated to euro (EUR) with use of average exchange rates published by the National Bank of Poland. All performed analyses and developed charts were supported by Microsoft Power BI data analysis tool. Findings: The general conclusion, which may be drawn from this research, is that implementation of ISA 701 and materiality disclosure limited the audit expectation gap. Detailed observations are described throughout the paper and summarized in the conclusions section. Originality/value: This study extends the prior research by providing various dimensions of the analysed matters. It contributes to understanding of the audit expectation gap and investigates on methods of minimizing it.

“Capitalism without bankruptcy is like Christianity without hell”Frank Borman—American astronaut

1. Introduction

The International Auditing and Assurance Standards Board (IAASB) is a global independent standard-setting body that serves the public interest by setting high-quality international standards, which are generally accepted worldwide. The IAASB sets its standards in the public interest with advice from the IAASB Consultative Advisory Group (CAG) and under the oversight of the Public Interest Oversight Board. Changing expectations and public confidence in audits is one of the most significant environmental drivers that have shaped the IAASB’s strategy for 2020–2023 (IFAC 2019, p. 7).

There is decreasing confidence and declining trust in audits, arising from continuing high levels of reported poor results of external inspections and recent high profile corporate failures in some jurisdictions. Stakeholders’ expectations are also changing about what the standards should require the auditor to do, e.g., in relation to the detection and reporting of fraud, and the consideration of going concern issues.

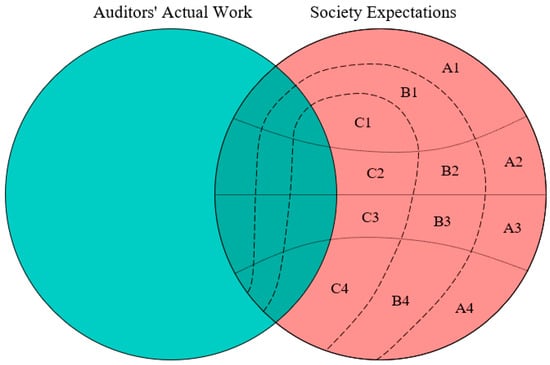

It has already been proved that public misperceptions are a major cause of the legal liability crisis facing the accounting profession. There is a concern that auditors and the public hold different beliefs about the auditors’ duties and responsibilities and the messages conveyed by audit reports (Koh and Woo 1998). This has been named as the “auditing expectation gap” which refers to the difference between (1) what the public and other financial statement users perceive auditors’ responsibilities to be and (2) what auditors believe their responsibilities entail (McEnroe and Martens 2001, pp. 345–58). This gap can be divided into three elements (ICAEW 2006):

These elements can be split down further into the following key areas:

- reporting (area ‘1’),

- assurance being provided (area ‘2’),

- regulation and liability (area ‘3’),

- audit independence (area ‘4’).

The auditing expectation gap is illustrated in Figure 1 below.

Figure 1.

Auditing expectation gap divided into three elements and four key areas. Source: own elaboration based on analysed literature.

In 2015, the IAASB issued amendments to its standards. The goal of this shift was to enhance the independent auditor’s reporting by making it more informative and insightful, and therefore valuable, to investors and other users of financial statements. The IAASB implemented a new International Standard on Auditing (ISA) 701, which introduced the auditor’s responsibility to report on Key Audit Matters (KAM). The standard is applicable to the audit of all listed entities for periods ending on or after 15 December 2016.

Communicating key audit matters is expected to assist the users of financial statements in understanding topics, which according to the auditor were of utmost importance in the audited period. Key audit matters are those matters that, in the auditor’s professional judgment, were of most significance in the audit of the financial statements of the current period (IAASB 2016a, ISA 701, para. 8). At the same time, ISA 701 does not define any number of key audit matters, which ought to be identified by the auditor. The standard requires that the auditor uses his professional judgement in order to prioritize what is to be communicated within the KAM section. An attempt to determine the degree of implementation of changes in auditors’ reporting for the largest companies (based on the example of the Polish market) was made in 2019 (Kutera 2019, pp. 79–94). The reports from the audit of the consolidated financial statements of the 30 largest companies listed on the Warsaw Stock Exchange for the years 2014–2016 were analyzed. The results of the analysis showed that the key audit matters mainly include estimating the impairment of assets (including deferred tax assets), revenue recognition and contingent liabilities disclosures.

Furthermore, in some jurisdictions, the auditor’s report may comprise additional information going beyond the requirements of the ISA including the determination of materiality (Deloitte 2016, p. 15). The concept of materiality has received a lot of attention in recent years as high-profile accounting scandals have plagued financial reporting. ISA requires that early in an audit engagement the auditor establishes a preliminary level of materiality. This monetary value is used to determine the extent of audit testing that is to be performed. It can be changed as the audit progresses and key financial statement numbers change (Kearns 2007). Under current standards neither the preliminary nor final materiality value must be disclosed. In Poland and United Kingdom, it is permitted to disclose such additional information and therefore audit firms can decide whether or not to present this information.

The main purpose of this paper is to determine how particular audit firms deal with ISA 701 requirements and the society expectations towards reporting of the materiality levels. It compares and contrasts auditors’ extent of such reporting (both KAM and materiality section) separately with regard to entities listed on Warsaw and London stock exchange and separately for analysed market indexes. Additionally, the aim of this paper is to range the assertions in terms of the frequency of their occurrence.

This study extends the prior research by providing various dimensions of the analysed matters. The article consists of an introduction, three chapters, and a summary and conclusions. The first chapter was devoted to the review of literature on the auditing expectation gap. The second chapter presents the research methodology, while the third chapter presents the results of the research.

2. Literature Review

Business failures are connected with the financial situation and non-financial factors (Ptak-Chmielewska 2019). Financial scandals have not only resulted in the loss of trust in the capital market but have also caused a crisis of credibility of auditors (Whittington and Pany 2004). There is a need to increase the usefulness of the information provided by the statutory auditors upon examination of the financial statements (Szczepankiewicz 2011). Many regulators currently debate how to increase effectiveness of supervision of public companies (Szczepankiewicz 2012, p. 25). Public expectations should go much beyond the watchdog function. The public awaits an audit to assure as to discovery of all frauds and irregularities (Gupta 2005). Absolute objectivity cannot be guaranteed since “materiality” and “material significance” are auditors’ subjective concepts (Ojo 2006). A review of auditing literature shows how the auditing profession has responded to this problematic issue—including coining the phrase “audit expectation gap” (Lee et al. 2009). The expectation gap is the evolutionary development of audit responsibilities (Ebimobowei 2010, p. 129).

The audit expectation gap is a fundamental issue in every society in the world and that perception of users of financial statements as the responsibilities of auditors and the audit objective is the major cause of the gap. The gap can be addressed through (Schelluch and Gay 2006):

- emphasing the need to educate the public and reassure them about the exaggerated public outcries over isolated audit failures,

- codifying existing practices to legitimize them,

- attempting to control the audit expectation gap debate and repeatedly propounding the views of the profession,

- emphasing an awareness of the objective of the audit,

- readiness to extend the scope of an audit.

Audit definition is subject to challenges and changes according to social, economic and political developments (Jedidi and Richard 2009). Audit rules and regulations contain terms, like “reasonable”, “material”, and “professional scepticism” whose meanings vary in the minds of different auditors (Zikmund 2008). Independence is crucial to the reliability of auditors’ reports (Salehi 2009). The literature reveals that educating the public about the objects of audit and auditors’ responsibilities will help minimize the audit gap (Salehi and Rostami 2009).

The previous wording of the audit opinion no longer meets the expectations of the business community (Kutera 2018). The expanded audit report appeared to change users’ perceptions about the responsibilities of management and auditors that mean users found expanded reports more useful and understandable than short-form audit reports (Aljaaidi 2009, p. 52). The professional bodies should set up new standards and renew existing ones as one of the remedies to the expectations gap (Akinbuli 2010). A common response in order to reduce the gap is to set out more auditing and accounting standards (Saeidi 2012, p. 7032). Accelerated by waves of financial crises the authorities have introduced a variety of measures to enhance the effectiveness of companies supervision (Kiedrowska and Szczepankiewicz 2011).

The IAASB implemented new ISA 701, which introduced the auditor’s responsibility to report on KAM. Communicating KAMs is expected to assist the stakeholders in understanding the most important topics that occurred in the period presented in the financial statements. While determining key audit matters the auditor should consider i.a.:

- areas of higher risk of material misstatement or in which significant risks were identified (IAASB 2009e, ISA 315),

- financial statement areas, which involve substantial management judgment (e.g., accounting estimates),

- effects of significant events or transactions, which occurred during the audited period.

It must be noted that any matter giving rise to a qualified or adverse opinion (as per IAASB 2009d, ISA 705), or the existence of material uncertainty that may question the entity’s ability to continue as a going concern (IAASB 2016b, ISA 570) is by its nature a KAM. However, such matters should be reported in line with applicable ISAs and the auditor should not include them in the KAM section of the report. In case when the auditor does not determine any key audit matters, he shall:

- discuss this with the engagement quality control reviewer (if appointed),

- explain in the report that there are no KAM to be reported, including the rationale for such a conclusion (IAASB 2009c, ISA 230),

- communicate this with those charged with governance.

The audit committee helps in narrowing the audit expectation gap since it is independent and non-executive and it aims to settle disputes and to reinforce external and internal audit performance. If audit committees do not play their role not more than just window dressing, then the audit expectation gap will be widened (Shbeilat et al. 2017).

An external audit of financial statements provides reasonable assurance as to whether the audited financial statements as a whole are prepared, in all material respects, in accordance with an identifiable financial reporting framework. Thus, the auditor is only responsible to detect misstatements that are material to the financial statements as a whole (IAASB 2009a, ISA 200). Misstatements, including omissions, are considered to be material if they, individually or in the aggregate, could reasonably be expected to influence the economic decisions of users taken on the basis of the financial statements (IAASB 2009b, ISA 320, para. 2). This definition appears to be simple, however, the auditor has to distinguish between omissions and misstatements that would affect the users of financial statements and those that would not affect such users (Vorhies 2005). Additionally, there is a range of users, which makes such assessment more complex since materiality is likely to be unique to each user (Doxey 2013).

Materiality disclosures are not mandatory in Polish statutory auditing. Several foreign studies have shown that materiality disclosures in the audit report could have beneficial effects, while other studies have raised concerns about potential drawbacks. Research from a users’ perspective seems to conclude that materiality should be disclosed, whilst research from the auditors’ perspective is still in its fledgling stages, although it seems that auditors are rather apprehensive about disclosing materiality. This lack of consensus with regards to materiality disclosures is part of a much larger audit reporting debate that has been going on for many decades (Baldacchino et al. 2017).

3. Research Methodology

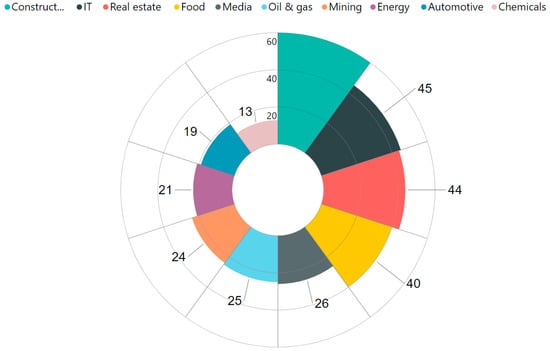

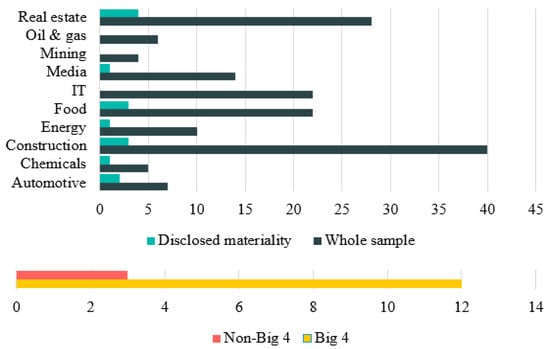

The tested sample, which was subject to the research, consisted of 317 companies listed on Warsaw (158 companies) or London (159 companies) stock exchange. The analysis was divided into companies from the following ten market indexes (WIGs): construction, IT, real estate, food, media, oil and gas, mining, energy, automotive and chemicals. The dispersion of the analyzed organizations in terms of represented WIG is illustrated in Figure 2 below.

Figure 2.

Tested sample by WIG. Source: own elaboration based on analyzed data.

The research was executed based on the analysis of:

- annual consolidated financial statements (annual reports)4,

- independent auditor reports,

published by in-scope entities for the latest twelve-months period available as at the date of the research (mostly these were twelve-months periods ended on 31 December 2017 and 31 March 2018). All values were denominated to euro (EUR) with the use of average exchange rates published by the National Bank of Poland.

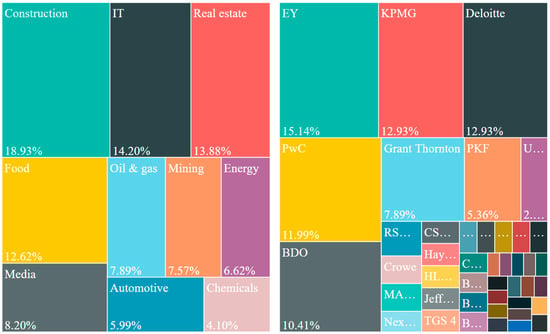

All enterprises within the tested sample were public interest entities (PIE) listed on Warsaw or London stock exchange. Analyzed companies listed on the Warsaw stock exchange (158 companies) represented the entire population of PIE operating within the tested WIGs. Firms from the United Kingdom were randomly selected from respective WIGs to “mirror” the Polish ventures. The structure of the tested sample in terms of WIGs and the auditors is presented in Figure 3 below.

Figure 3.

Structure of the tested sample in terms of WIGs and the auditors (in %). Source: own elaboration based on analyzed data.

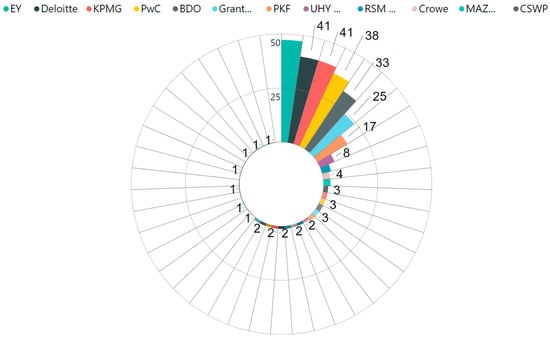

Analyzed corporations were subject to the obligatory audits of their financial statements. The coverage of the tested sample by auditors is demonstrated in Figure 4 below.

Figure 4.

Structure of the tested sample in terms of the auditors. Source: own elaboration based on analyzed data.

168 of tested companies (53%) entrusted their audits to so-called “Big 4” auditing firms while the remaining (149, i.e., 47%) selected 1 of 39 other audit service providers. In the tested sample, 20 auditors (47%) were represented by a single client.

Apart from the Big 4, the auditors with the biggest share in the tested sample were:

- BDO (33, i.e., 10%);

- Grant Thornton (25, i.e., 8%);

- PKF (17, i.e., 5%).

A combined simplified balance sheet and profit and loss for the tested sample is presented in Table 1 below.

Table 1.

Combined simplified balance sheet and profit and loss for the tested sample (in million EUR).

Based on the information provided in tested annual consolidated financial statements and independent auditor reports, there was a database created which contained:

- values of selected financial statements line items;

- detailed description of all KAMs reported;

- overall materiality levels and applied calculation methods.

Auditors of 317 companies, that were subjected to this test, identified a total of 793 unique KAMs. Based on their detailed descriptions they were then segmented into 36 categories (including category ‘none’) and finally mapped with a total of 2094 assertions from 7 types5.

All performed analyses and developed charts were supported by Microsoft Power BI data analysis tool. With regards to presented ‘sankey’ type of charts, that illustrate interconnections between auditors, KAMs, assertions, WIGs, overall materiality, benchmark and Overall Materiality Rule of Thumb (OM RoT), the weights of ribbons presented were defined as number/average value of KAMs/assertions/overall materiality respectively.

4. Presentation of Research Results

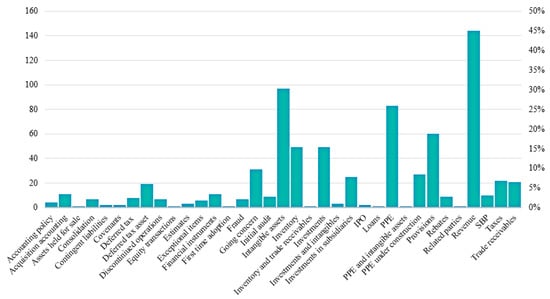

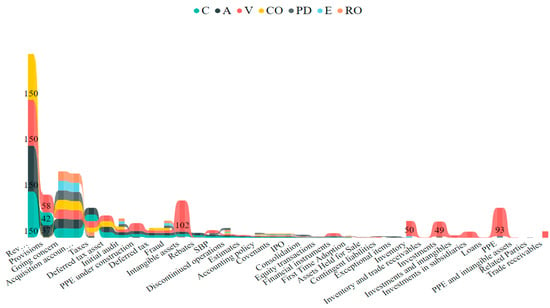

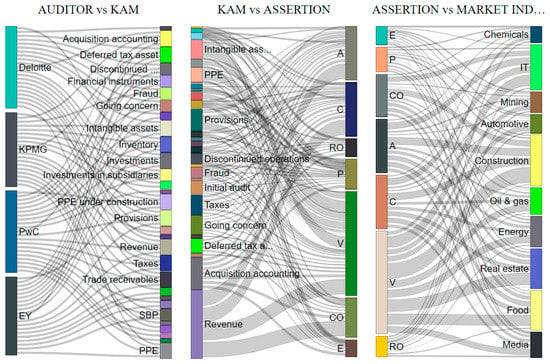

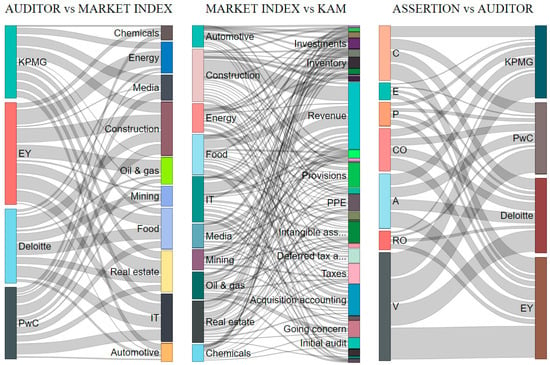

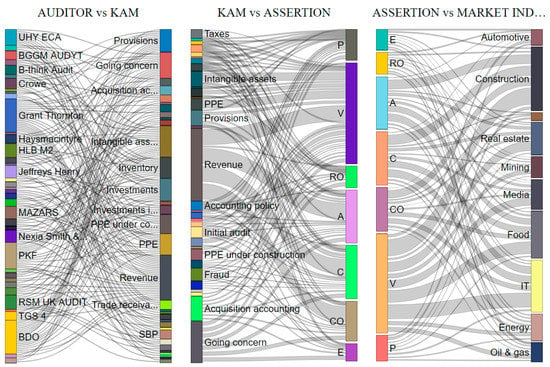

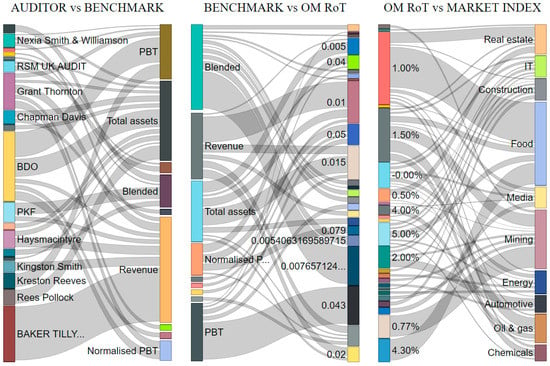

In Figure 5 and Figure 6, the KAMs’ number and frequency of use and KAMs’ mapping to assertions are presented, respectively. For the relationships between auditors, KAMs, assertions, and WIGs please refer to Figure 7 and Figure 8.

Figure 5.

KAM—number and frequency of use. Source: own elaboration based on analyzed data.

Figure 6.

KAM—mapping to assertions. Source: own elaboration based on analyzed data.

Figure 7.

Relationships between auditors, KAMs, assertions, and WIGs—for Big 4 auditing firms. Source: own elaboration based on analyzed data.

Figure 8.

Relationships between auditors, KAMs, assertions, and WIGs—for non-Big 4 auditing firms. Source: own elaboration based on analyzed data.

- for five businesses (1.6% of the tested sample) no KAMs were reported by the auditors,

- revenue is the most vastly used as a KAM category (45.3% of auditors’ reports contained this KAM),

- the following 9 KAMs referred to all seven assertions: accounting policy, acquisition accounting, covenants, discontinued operations, first time adoption, fraud, going concern, initial audit and initial public offering (IPO),

- the valuation was the most frequently appearing assertion (745 items from a total of 2094, 35.6%);

- there is no clear differentiation in terms of presented patterns between Big 4 and non-Big 4 audit firms.

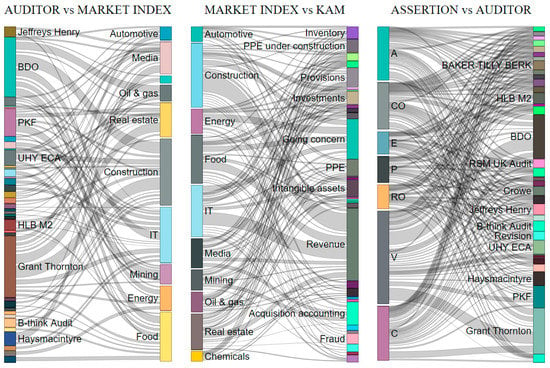

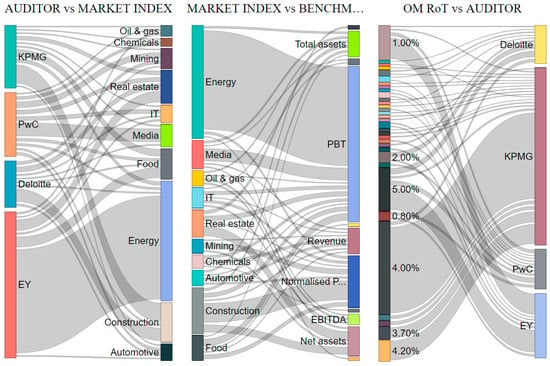

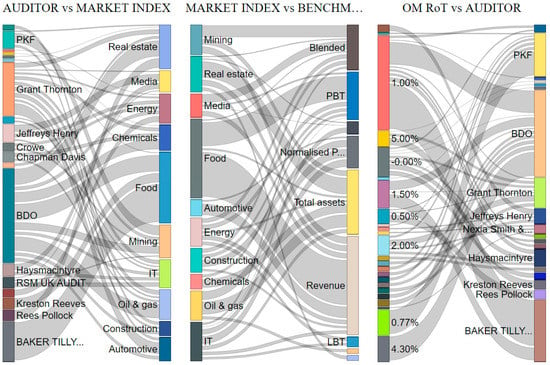

In Figure 9, the companies listed on the Warsaw stock exchange for which materiality levels were disclosed by auditors are presented. For the relationships between auditors, benchmarks, OM RoT, and WIGs please refer to Figure 10 and Figure 11.

Figure 9.

Companies listed on the Warsaw stock exchange for which materiality levels were disclosed by auditors—by WIG and non-Big/Big 4 auditors. Source: own elaboration based on analyzed data.

Figure 10.

Relationships between auditors, benchmarks, OM RoT and WIGs—for Big 4 auditing firms. Source: own elaboration based on analyzed data.

Figure 11.

Relationships between auditors, benchmarks, OM RoT and WIGs—for non-Big 4 auditing firms. Source: own elaboration based on analyzed data.

All auditors of companies listed on the London stock exchange reported on the materiality levels, which they utilized for audit purposes. The information was fairly comprehensive and included: benchmark, OM RoT, overall materiality level, and de minimis materiality level. Some auditors provided also additional details about haircut and performance materiality.

As presented in Figure 9, this statistic was substantially lower for entities listed on the Warsaw stock exchange. Materiality levels were reported for 15 PIEs, which represented 9.5% of the whole population of companies operating within 10 specific industries (the Polish tested sample). It was observed that 80% of all reported materiality levels were announced by Big 4 auditors (by PwC in 11 out of 12 cases).

- coverage of sectors by Big 4 representatives was fairly even, with the exception of the energy, which was dominated by EY,

- specialization of auditors may be observed (Baker Tilly’s portfolio comprises mostly of food WIG) but no concentration over any particular auditor is visible within any sector,

- the most broadly used OM RoT was 4%, which was applied primarily:

- ■

- by KPMG,

- ■

- for normalized PBT,

- ■

- in construction WIG;

- relatively, among Big 4, EY has the least differentiated benchmarks, with PBT being the main variable used to determine materiality,

- among Big 4, profit before tax (PBT) was the most commonly used benchmark, followed by normalized PBT, while among non-Big 4 it was revenue and total assets respectively,

- there was no other clear differentiation in terms of presented patterns between Big 4 and non-Big 4 audit firms.

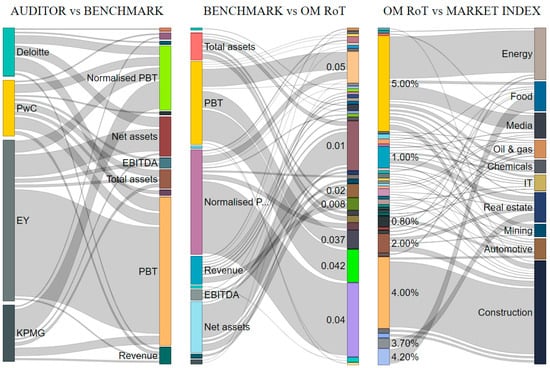

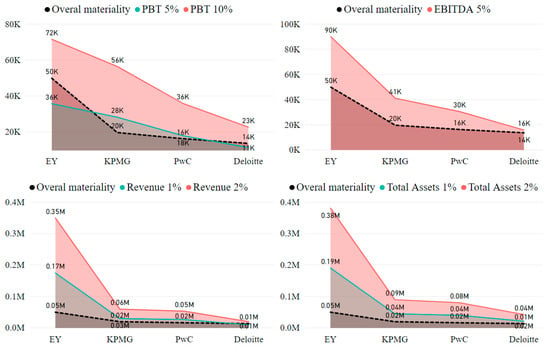

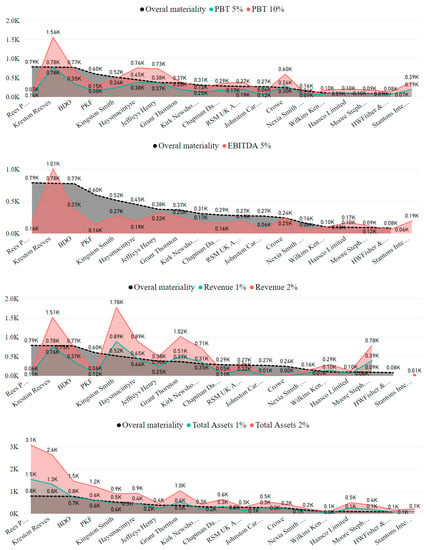

The exact level of the OM is not imposed on auditors by any governing body. Its calculation is at the auditor’s discretion. The auditor’s determination of materiality is a matter of professional judgment and is affected by the auditor’s perception of the financial information needs of users of the financial statements (ISA 320, para. 4). Determining a percentage to be applied to a chosen benchmark involves the exercise of professional judgment. There is a relationship between the percentage and the chosen benchmark, such that a percentage applied to profit before tax from continuing operations will normally be higher than a percentage applied to total revenue. For example, the auditor may consider five percent of profit before tax from continuing operations to be appropriate for a profit-oriented entity in the manufacturing industry, while the auditor may consider one percent of total revenue or total expenses to be appropriate for a not-for-profit entity (ISA 320, para. A7). The Figure below presents the OM used by Big 4 auditors in relation to those thresholds.

As presented in Figure 12, on average:

Figure 12.

Overall materiality used by Big 4 auditors in relation to the percentage mentioned in ISA 320 and literature. Source: own elaboration based on analyzed data.

- for PBT, KPMG is 28.6% and PwC is 12.5% below the bottom threshold of 5% PBT, which means that they are even more detailed and conservative than as per the example presented in ISA 320, EY keeps it almost in the middle between the lower and upper limits, while Deloitte maintains its OM 27.3% over this base,

- for EBITDA, Deloitte stands out from the competition by getting close to the upper limit of the threshold, while the remainders keep it in the middle of the scale,

- for revenue, all Big 4 auditors except for Deloitte set up their OM below 1% revenue as per the example presented in ISA 320,

- finally, the situation for total assets is akin to the one for the revenue.

The Figure 13 below presents the OM used by non-Big 4 auditors in relation to those thresholds.

Figure 13.

Overall materiality used by non-Big 4 auditors in relation to the percentage mentioned in ISA 320 and literature. Source: own elaboration based on analyzed data.

For non-Big 4 auditors it may be observed that the levels of the overall materiality, which they apply, are in general at higher stakes and in many cases, they exceed the upper thresholds as per examples presented in ISA 320.

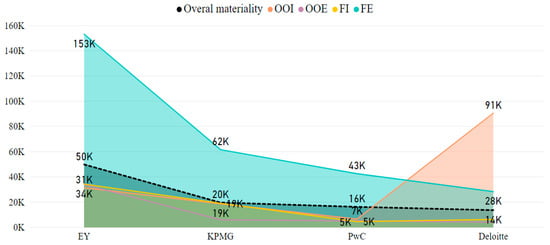

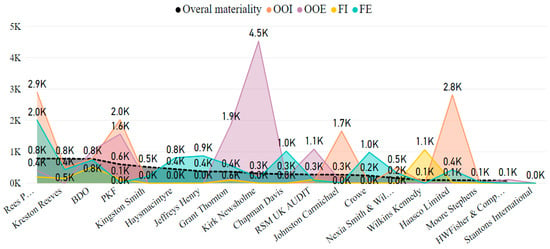

On Figure 14 and Figure 15 there are presented other operating income (OOI), other operating expenses (OOE), financial income (FI), and financial expenses (FE) which in some cases on average were below the OM and therefore were not audited, while they seem meaningful and vivid to the business.

Figure 14.

Average values of operating income (OOI), other operating expenses (OOE), financial income (FI), and financial expenses (FE) in relation to the OM—for Big 4 auditing firms. Source: own elaboration based on analyzed data.

Figure 15.

Average values of OOI, OOE, FI, and FE in relation to the OM—for non-Big 4 auditing firms. Source: own elaboration based on analyzed data.

As presented in Figure 14, Big 4 representatives on average do not audit OOI (except for Deloitte), OOE, and FI. The same dependencies, but for non-Big 4 auditors, are demonstrated in Figure 15, however the situation in this view is more diversified and varies by auditor. Nonetheless, it seems that there is no common approach on the market and in many cases OOI, FI, and FE are not subject to the audit of the financial statement.

5. Summary and Conclusions

Investors expect that after auditors inspect financial statements of public companies, they are complete, accurate and reliable in every significant aspect. Furthermore, as mentioned in chapter 1, investors expect that based on the auditor’s reporting they will be capable of evaluating whether to invest in the entity or not. The aim of introducing ISA 701 was to further build up this confidence by ensuring that auditors, apart from “crunching numbers”, also identify and pay special attention to the matters, which were the most noteworthy in the audited period and required dedicated treatment.

The performed research is the continuation of the market-wide studies conducted in this field after the implementation of the standards related to reporting on Key Audit Matters. The analysis depicted in this paper explores and re-discovers the landscape of auditing services provided to public companies in relation to the examination of their financial statements.

The general conclusion, which may be drawn from this research, is that implementation of ISA 701 and materiality disclosure limited the audit expectation gap. The study illustrates that:

- among Big 4, profit before tax (PBT) was the most commonly used benchmark, followed by normalized PBT, while among non-Big 4 it was revenue and total assets respectively,

- there were identified the following Key Audit Matters which are related with all assertions: going concern, business combination accounting, fraud risk, first-year audit and discontinued operations,

- under the current approach, some financial statement items, such as other operating expenses, are not audited at all, it should be noted that this particular category is quite capacious and can easily hide undesirable “surprises”,

- although many individual Key Audit Matters were identified by auditors, they were fairly little differentiated, key categories, applied to most of the companies, were the same as benchmarks used for calculation of overall materiality,

- valuation stands out as the assertion, which is of utmost significance to the auditors, what clearly drives the way in which audit procedures are designed and performed,

- the extent of caution applied by non-Big 4 auditors, expressed by the level of overall materiality and its relation to relevant guidelines, is, in general, lower than the one exercised by their Big 4 colleagues, this means that audits performed by lesser firms may be less diligent than the ones conducted by market leaders.

The above indicates that, in general, and on average, some audits are truly commodity-like and focus only on revenues, total assets, and valuation, while other areas are not thoroughly investigated. This is especially true with regard to audit engagements performed by smaller players.

On one hand, being a commodity service is in line with the substance and the nature of the audit, which is a standardized service. On the other hand, regulators and market makers do their best to strengthen the confidence of business transactions by improving the value, which auditors create and provide to investors. In order to achieve that goal, it is necessary to re-imagine the way in which audit services are designed and delivered.

Presented results also underline the necessity to continue the discussion on the involvement of advanced tools and techniques, e.g., data analytics and visualization, machine learning (ML), blockchain, robotic process automation (RPA), and artificial intelligence (AI), to facilitate the implementation of such concepts in audit services. This idea is to be further explored in the detailed studies, which are planned to be performed following this paper. Academicians, practitioners, and regulators shall have an important insight into the current subject matter from this work. Future researchers shall also get a good base of scholarly work from this study. The proposed direction of further research is to extend the scope of the audit by including public companies listed on another European stock exchange, followed by an analysis for the next 12-month reporting periods.

Author Contributions

Conceptualization, Methodology, Software, Validation, Formal Analysis, Investigation, Resources, Data Curation, Writing-Original Draft Preparation, Writing-Review & Editing, Visualization, Supervision, Project Administration, T.I. and B.I.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Akinbuli, Sylvester F. 2010. The effect of audit expectation gap on the work of auditors, the profession and users of financial information. The Nigerian Accountants 43: 37–40. [Google Scholar]

- Aljaaidi, Khaled. 2009. Reviewing the Audit Expectation Gap Literature from 1974 to 2007. International Postgraduate Business Journal (IPBJ) 1: 41–75. [Google Scholar]

- Baldacchino, Peter J., Norbert Tabone, and Ryan Demanuele. 2017. Materiality Disclosures in Statutory Auditing: A Maltese Perspective. Journal of Accounting, Finance and Auditing Studies 3: 116–57. [Google Scholar]

- Deloitte. 2016. Benchmarking the New Auditor’s Report. Key Audit Matters and Other Additional Information. Available online: https://www2.deloitte.com/content/dam/Deloitte/ch/Documents/audit/ch-en-audit-benchmarking-auditors-report.pdf (accessed on 15 March 2019).

- Doxey, Marcus M. 2013. The Effect of Increased Audit Disclosure on Investors’ Perceptions of Management, Auditors, and Financial Reporting: An Experimental Investigation. Lexington: University of Kentucky, Available online: http://uknowledge.uky.edu/accountancy_etds/2 (accessed on 22 March 2019).

- Ebimobowei, Appah. 2010. An evaluation of audit expectation gap: Issues and challenges. International Journal of Economic Development Research and Investment 1: 129–41. [Google Scholar]

- Gupta, Kamal. 2005. Contemporary Auditing, 6th ed. New Delhi: Tata McGraw Hill. [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2009a. ISA 200 Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2009b. ISA 320 Materiality in Planning and Performing and Audit. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2009c. ISA 230 Audit Documentation. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2009d. ISA 705 Modifications to the Opinion in the Independent Auditor’s Report. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2009e. ISA 315 Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2016a. ISA 701 Communicating Key Audit Matters in the Independent Auditor’s Report. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- International Auditing and Assurance Standards Board (IAASB). 2016b. ISA 570 (Revised) Going Concern. New York: The International Federation of Accountants (IFAC). [Google Scholar]

- Institute of Chartered Accountants in England and Wales (ICAEW). 2006. Expectation Gaps. London: Audit and Assurance Faculty, Available online: https://www.icaew.com/-/media/corporate/files/technical/audit-andassurance/audit-quality/audit-quality-forum/expectation-gaps.ashx (accessed on 22 March 2019).

- The International Federation of Accountants (IFAC). 2019. Proposed Strategy for 2020–2023 and Work Plan for 2020–2021. p. 7. Available online: http://www.ifac.org/publications-resources/proposed-strategy-2020-2023-and-work-plan-2020-2021 (accessed on 8 March 2019).

- Jedidi, Imen, and Chrystelle Richard. 2009. The Social Construction of the Audit Expectation Gap: The Market of Excuses. Strasbourg: La place de la dimension europeenne dans la Comptabillite controle Audit. [Google Scholar]

- Kearns, Francis. 2007. Materiality & the Audit Report: It’s Time for Disclosure. Available online: https://scholarworks.rit.edu/other/640 (accessed on 1 March 2019).

- Kiedrowska, Maria, and Elżbieta Izabela Szczepankiewicz. 2011. Internal Control in the Concept of Integrated Enterprise Risk Management (ERM) System in Insurance Undertakings. Finanse, Rynki Finansowe, Ubezpieczenia 640: 695–706. [Google Scholar]

- Chye Koh, Hian, and E-Sah Woo. 1998. The expectation gap in auditing. Managerial Auditing Journal 13: 147–54. [Google Scholar] [CrossRef]

- Kutera, Małgorzata. 2018. Nowy raport biegłego rewidenta—Implementacja przy audycie spółek WIG-20. Prace Naukowe Uniwersytetu Ekonomicznego We Wrocławiu 503: 281–92. [Google Scholar] [CrossRef]

- Kutera, Małgorzata. 2019. Kluczowe kwestie badania—Nowy element w raportowaniu biegłych rewidentów. Zeszyty Teoretyczne Rachunkowości 101: 79–94. [Google Scholar] [CrossRef]

- Lee, Teck Heang, Azham Md. Ali, and Juergen Dieter Gloeck. 2009. The Audit Expectation Gap in Malaysia: An Investigation into its Causes and Remedies. South African Journal of Accountability and Auditing Research 9: 57–88. [Google Scholar]

- McEnroe, John, and Stanley C. Martens. 2001. Auditors’ and Investors’ Perceptions of the “Expectation Gap”. Accounting Horizons 15: 345–58. [Google Scholar] [CrossRef]

- Ojo, Marianne. 2006. Eliminating the Audit Expectations Gap: Myth or Reality? Available online: https://mpra.ub.uni-muenchen.de/232/1/MPRA_paper_232.pdf (accessed on 15 March 2019).

- Ptak-Chmielewska, Aneta. 2019. Predicting Micro-Enterprise Failures Using Data Mining Techniques. Journal of Risk and Financial Management 12: 6. [Google Scholar] [CrossRef]

- Saeidi, Fatemeh. 2012. Audit expectations gap and corporate fraud: Empirical evidence from Iran. African Journal of Business Management 6: 7031–41. [Google Scholar]

- Salehi, Mahdi. 2009. Audit Independence and Expectation Gap: Empirical Evidences from Iran. Journal of Economics and Finance 1: 165. [Google Scholar] [CrossRef]

- Salehi, Mahdi, and Vahab Rostami. 2009. Audit Expectation Gap: International Evidence. International Journal of Academic Research 1: 140–46. [Google Scholar]

- Schelluch, Peter, and Grant Gay. 2006. Assurance provided by auditors’ reports on prospective financial information: Implications for the expectation Gap. Accounting and Finance 46: 653–76. [Google Scholar] [CrossRef]

- Shbeilat, Mohammad, Waleed Abdel-Qader, and Donald Ross. 2017. The Audit Expectation gap: Does Accountability Matter? International Journal of Management and Applied Science 3: 75–84. [Google Scholar]

- Szczepankiewicz, Elżbieta Izabela. 2011. The Role of the Audit Committee, the Internal Auditor and the Statutory Auditor as the Bodies Supporting Effective Corporate Governance in Banks. Finanse, Rynki Finansowe, Ubezpieczenia 640: 885–97. [Google Scholar]

- Szczepankiewicz, Elżbieta Izabela. 2012. The role and tasks of the Internal Audit and Audit Committee as bodies supporting effective Corporate Governance in Insurance Sector Institutions in Poland. Oeconomia Copernicana 4: 23–39. [Google Scholar] [CrossRef]

- Vorhies, James Brady. 2005. The New Importance of Materiality: CPAs Can Use This Familiar Concept to Identify Key Control Exceptions. Journal of Accountancy 199: 53. [Google Scholar]

- Whittington, Ray O., and Kurt Pany. 2004. Principles of Auditing and Other Assurance Services, 14th ed. New York: McGraw-Hill Education. [Google Scholar]

- Zikmund, Paul E. 2008. Reducing the Expectation Gap. CPA Journal 78: 12. [Google Scholar]

| 1 | Referring to what society expects of auditors and what can reasonably be expected of auditors to accomplish. |

| 2 | The gap between the responsibilities that society reasonably expects auditors to perform and auditors’ actual responsibilities under statute. |

| 3 | The difference between the expected standard of performance of auditors and the actual performance of responsibilities by auditors. |

| 4 | The research was executed based on the analysis of the annual consolidated financial statements or standalone financial statements in situations where there was no capital group. The tested sample consisted of 317 financial statements (both consolidated and standalone). |

| 5 | The following types of assertions were defined and analysed: C—completeness; A—accuracy; V—valuation; CO—cut-off; PD—presentation and disclosures; E—existence; RO—rights and obligations. |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).