Abstract

This study aimed to analyze the international literature on consumer behavior toward private label (PL) products, guided by the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analysis) method. We searched for peer-reviewed studies published until January 2021 in the Scopus and Web of Science databases using two main search terms, namely, “consumer behavior” and “private label,” which have several synonymous terms, such as “store brand,” “private brand,” and “own label.” A total of 44 eligible studies were selected for the analysis. We formulated research questions regarding the most studied categories of PL products, the non-health factors determining consumer behavior toward PL products, and the frequency of including health aspects in the choice of PL products. The following were analyzed in the studies included in the systematic literature review (SLR): general data and study design (authorship, year of publication, location, characteristics of the sample, and research category), research specifications (factors/variables, hypotheses, and measured parameters), and general findings (findings and practical recommendations). We found that most of the studies had analyzed dairy products as PL products, and the main non-health selection factors used were lower price and price–quality ratios. Health aspects were considered in only four of the analyzed studies, which focused on the evolution of PL products from low-cost products to sustainable brands with significant added value in terms of quality and health aspects.

1. Introduction

1.1. Health Aspects in Consumer Behavior

Consumer behavior is increasingly being influenced by health aspects [1,2]. Consumers are becoming more aware of the need to eat healthy foods to maintain good health [2]. As a result, the quality of products is now considered to be as important as their price. Some consumers are willing to pay a higher price for products that guarantee high quality [3]. This can be linked with a greater understanding of health and the impact of food on health [4].

Currently, researchers show increasing interest in studying consumer decision-making styles in order to understand how people make purchasing decisions in a competitive environment [5,6,7,8,9,10,11,12,13,14,15]. Consumer behavior is influenced by several factors in the cultural, social, personal, and psychological realms, which together determine the basic attitudes and views of consumers, and which are also an important element of marketing [16]. According to Kotler and Keller [17], consumer buying behavior can be defined as the behavior related to how individuals, groups, and organizations acquire and dispose of goods, services, ideas, or experiences to meet their needs and desires. From the viewpoint of marketers, consumer behavior can be understood by analyzing the reasons why consumers buy, the factors influencing consumer buying patterns, the changing determinants within the society, and others [18]. The purchase of PL products is a personal choice, and the growing popularity of such products has gained the attention of retail researchers [19,20]. In particular, the development of premium and value PLs has affected consumption behavior, the final demands of consumers, and the shares held by other brands (national or local) [21,22].

Today, an increasing number of consumers are making informed purchasing decisions, including with regard to the brands offered by retailers. Consumers choose food by considering factors such as quality and nutritional value [23]. It has been proven that the health information provided on the label raises consumer awareness, and that health claims also influence consumer preferences and increase the likelihood of purchasing the product [24]. Because information is effective if it succeeds in meeting the specific needs of the target audience, understanding consumers’ information-seeking and -processing behavior is crucial for making better marketing decisions [25].

1.2. Evolution of PL Products and Consumer Perceptions

PL products are goods sold under the brand name of a retailer (i.e., supermarket, hypermarket, discount store) [26], or a name used exclusively as a brand of the retailer [27]. Several terms for PLs can be found in the literature and have been used in market reports on retailer brands. The main terms used for PLs are “private labels” [28], “private brands” [29], “private label brands” [30], “store brands” [31], “own brands” [32], and “own labels” [33].

Initially, consumers’ brand consciousness and preference for national brands (NBs) were perceived to be barriers to purchasing PL products, as they were considered to be of low quality [34]. Over the years, PL products have evolved as a result of product development in retail chains and changes in consumer preferences [35]. Four generations of PL products have been distinguished [36,37]. The first generation included undifferentiated core products, defined as generic, no-name, brand-free, or unbranded. They were sold under generic names and offered at a very low, competitive price. The second generation of PL products were defined as products of own brands or “quasi-brands,” and sold under the name of the retail chain. They stood out for their packaging and slightly higher quality, although it was comparatively lower than the market leader. The third-generation PLs, also known as own brands, were characterized by their names, which were analogous to existing manufacturer brand products. Their price and quality are comparable to those of leading producer brands. The fourth-generation PLs, called extended own brands, include innovative and differentiated products. Their price and quality were the same or higher than those of the products of leading manufacturer brands [36].

Distributors rank their PL products, most often, as economy, premium, or standard, based on their quality and price [38]. Standard PL products are generally considered to be medium-quality or medium-price alternatives of NB products [39]. In contrast, premium PL products are top-quality-tier products. Compared with NB products, these products are rated higher for their quality. Finally, economy PL products are of a basic acceptable quality at the best price and are lower in quality than the products of NBs [20].

It has been shown that consumers no longer perceive PLs as inferior in quality to NBs [40], and they are considered to have comparable quality [41]. In 2005, more than 70% of consumers in the US and Europe rated the quality of PL products as at least as good as the products of large brands [34]. In a survey conducted in 2015 in Poland, consumers indicated that the strength of PLs is their good quality–price ratio (64% of responses), next to lower price (83%) [42]. These findings were supported by our studies conducted in 2020 and 2021 in three European countries: Poland, the UK [43], and Spain (Tenerife) [44]. In our studies, respondents from countries with varying levels of development of PL products agreed that the quality of these products is high as well as comparable to manufacturer brands. Customers had a sense of trust and security when they shopped for PL products, and also valued these products for the wide collection and availability of retailers’ products. They also stated that PL products had the appropriate price–quality [43,44].

Studies indicate that the quality of PL products can be compared with the products of NBs, and thus these products can be treated as equal and highly competitive. However, the retailers must offer products with high quality at an attractive price in order to encourage consumers to buy [45]. Currently, most large retailers have labels that are becoming increasingly popular and trusted by customers [46]. Consequently, consumers show more positive attitudes toward PL products due to the increase in their quality as well as brand reputation, which is in line with the perception of consumers who feel good about purchasing PL products [47].

1.3. Aim of the Study

Our study aimed to analyze the international literature on consumer behavior toward PL products, guided by the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analysis) method. This study is the continuation of our previous research, which focused on the evolution of PL products into sustainable PL products in national markets with large PL market shares [43] and in an autonomous community, using Tenerife as an example [44].

We attempted to find answers to the following questions:

- What PL product categories have been studied in terms of consumer behavior?

- What are the non-health factors considered by consumers when choosing PL products?

- How often are health factors considered by consumers when purchasing PL products?

2. Materials and Methods

2.1. Study Design

We performed a literature search based on the PRISMA guidelines [48,49], which are widely applied in many academic studies [50,51,52,53]. Our search focused on studies published until 15 January 2021 in the Scopus and Web of Science databases.

2.2. Inclusion/Exclusion Criteria

Our systematic literature review (SLR) analyzed the international literature on consumer behavior toward PL products, including studies on the determinants of consumers’ choice of PL products, such as price, perceived nutritional values, economic factors, intentions, attitudes toward PL products, and packaging.

The studies that met the following criteria were included in the analysis: those based on empirical research and those describing consumer behavior toward PL products. Peer-reviewed papers were also included. No time limits were applied in the search of articles. We excluded publications written in a language other than English, papers presenting theoretical models, doctoral dissertations, editorials, book chapters, short reports, and conference publications, as well as articles for which full texts were not available.

2.3. Search Strategy

Studies were retrieved through a systematic search of peer-reviewed journals from two databases: Scopus and Web of Science. The search was conducted between 4 and 20 February 2021 and included articles that were published between 2000 and 15 January 2021.

To identify studies focusing on consumer behavior toward PL products, particularly food products, we used a combination of key terms in the search. The first term used was “private label products,” in various combinations and forms, and the second was “consumer behavior or preferences.” We used a search string in which separate groups of words were combined and then applied to both databases (Table 1).

Table 1.

Databases and terms used in the study and the number of results obtained.

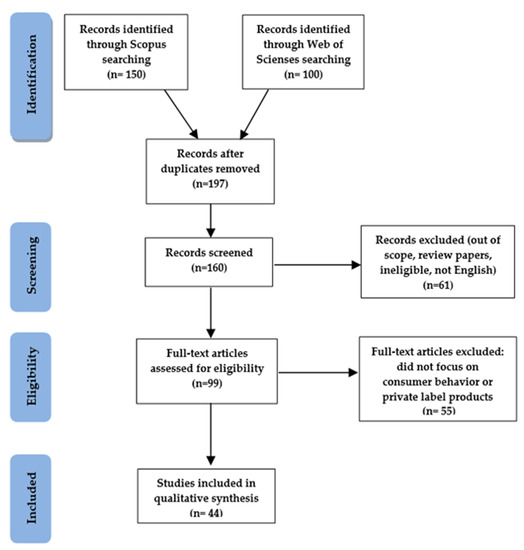

A total of 150 and 100 studies were identified, respectively, in the Scopus and Web of Science databases. After eliminating duplicates, there were 197 studies. Following the review of titles and abstracts, 160 studies remained. The number of articles was then reduced to 99, and their eligibility was analyzed in depth by assessing the full text. Studies that were not written in English, those that did not focus on PLs, own brands, or store brands, or studies that did not relate to consumer behavior were excluded.

Finally, 44 articles were selected for the analysis. Figure 1 presents a flow diagram describing the identification, screening, eligibility assessment, and inclusion of articles.

Figure 1.

Identification, screening, eligibility assessment, and inclusion of articles in the systematic review (PRISMA). Source: [48,49].

3. Results

All 44 studies included in the SLR were analyzed in three parts. The first part of the analysis focused on general information, including authorship, year of publication, research method used, country, sample population, product category, and the objective of the research (Table 2). The second part of the analysis focused on research specifications, which included the evaluation of factor/variables, hypotheses, and the types of data analysis used (Table 3). The third part of the analysis focused on key findings and practical implications of the studies (Table 4). In the Appendix A, in Table A1, we included the study objectives and research measures.

Table 2.

General details and design of the studies included in the systematic survey.

Table 3.

Research specifications of the studies included in the systematic survey.

Table 4.

General findings and managerial implications for the studies included in the systematic survey.

In all tables, studies are presented according to the year of their publication, starting with the most recent one (2021) and ending with the oldest (2000). To make the text analysis clearer in the tables, the retailer brand names are standardized by using the term “PL.” It also replaces other terms, such as store brand, private brand, private label brand, and own brand.

3.1. General Information

Table 2 presents general information pertaining to the studies included in the SLR.

The SLR included studies published between 2000 and 2021 as follows: seven studies from the period 2020–2021 [43,54,55,56,57,58,59], nine studies from the period 2018–2019 [16,60,61,62,63,64,65,66,67], 10 studies from the period 2015–2017 [38,68,69,70,71,72,73,74,75,76], six studies from the period 2010–2014 [29,77,78,79,80,81], and 12 studies from the period 2000–2009 [82,83,84,85,86,87,88,89,90,91,92,93]. The most frequently used research method was questionnaire survey (20 studies). The research sample consisted of between 200 [57,83] and 1272 respondents [61], but the average sample size was about 500. Other research methods used in the studies were experiments (six), in-depth interviews (six), blind sensory tests (four), scan panels (three), eye tracking (one), electroencephalography (two), and others (two). The studies included in the SLR had been conducted in cities located in Europe (31), America (eight), and Asia (six), as well as in Australia, New Zealand, and South Africa. The product categories mostly analyzed in terms of consumer behavior were dairy [29,43,54,60,63,79,80,81,82,88,93], cereals [16,43,54,55,56,58,68,69,73,76,80,85,88,92], sweets [16,43,54,60,63,79,80,81,82,85,88,90,91], frozen food [16,43,79,80,81,88], processed food [54,59,72,80,90], and cosmetics [16,38,60,70,74,75,76,79,81,87,90,91]. For example, in 2020, Slovak researchers conducted a series of studies on yogurts, which included a sensory comparison between PL products and products of NBs that are leading in the Slovak market [55,56,58]. Studies on nonfood product categories mainly chose cosmetics, especially shampoo, for the analysis of consumer behavior toward PL products [70,78,81,87,91].

3.2. Research Specifications

Table 3 presents the research specifications of the studies included in the SLR.

3.3. General Findings and Practical Implications

Table 4 presents the findings and conclusions from studies related to consumer behavior toward PL products, as well as managerial implications. The findings/conclusions mainly relate to how the studied factors, such as perceptions of quality, price, type of packaging, and risk of purchasing PL products, influence consumer behavior toward the PL products of retail chains. Practical recommendations are included in almost all the analyzed studies. Only one study did not provide any recommendations.

The main factors analyzed in the included studies were consumers’ perception of quality, price, store image, and the risk of PL products, and their attitude toward PL products in different forms. The other factors assessed were the risk of buying PL products in comparison to the products of NBs, the influence of the country of origin or packaging, and the effect of brand image and store chain on product choices. The results of the included studies were also supported by our studies conducted in Poland, the UK, and Spain (Canary Islands) on consumer behavior and the perception of PL products of retail chains in these countries. In all the three studies (the first two were carried out among Polish and British consumers [43], and the third one in Tenerife [44]), dairy products were rated highest in terms of the frequency of purchase of a given category of PL products.

Only four of the analyzed studies included health factors as determinants in the choice of purchasing PL products. The first study was performed in 2021, and proposes a new food labeling system with letter grades indicating the level of healthiness and recommended frequency of consumption of a product. Products were identified as healthier based on their Nutri-Score, and the healthiness of products, ranked across five categories, was evaluated differently. In addition, the study analyzed the impact of the Nutri-Score system on the perceived quality, perceived healthiness, and purchase intentions for NB and PL products. It also recommends that the Nutri-Score system can be introduced as the European nutrition label, and that it can be an effective option to manage the growing obesity epidemic [54].

In a second study from 2013, conducted in Germany, the researchers analyzed, through in-depth interviews, the four main motives for buying organic food: healthiness, hedonism, environmental friendliness, and food safety. The authors assumed that consumers have a belief that organic food has a higher nutritional value than nonorganic food, and has a higher degree of perceived healthiness compared to food from a brand without an organic label. The results confirmed that consumers perceived certified organic food to be significantly more healthy, hedonic, environmentally friendly, and safe compared to conventional or nonorganic food. This was also true in the case of organic PL products, which were ranked similarly to global organic brands by consumers. This indicates that consumers have positive perception toward organic PL products in terms of health aspects [29].

The third study analyzed the perceptions of manufacturer brands and PLs based on various choice factors. One of these factors was health, and respondents responded that PL products were comparable to the products of manufacturer brands, with a slight edge for manufacturer products, but this shows that consumers rate each brand equally, regardless of who owns it. This result could motivate retailers to further develop PL products, also taking into account the health aspects [84].

In the last study analyzed, which was conducted in 2006, the authors focused on the perceptions of purchase risk, comparing NBs and PLs for two nonfood products: shampoo and kitchen paper. The health aspects were discussed in the context of psychological risk during shopping, which was assessed by evaluating the level of fear caused by potential health harms. The results obtained were very similar, and supported the findings of other discussed studies that investigate the influence of health aspects on human health. The data showed that the greater the familiarity of consumers with PLs, the smaller the difference between PLs and NBs in terms of perceived risk, regardless of product category [87].

The studies included in the SLR used a variety of research methods. Quantitative research mainly used a survey questionnaire. Some studies conducted blind tests, in which consumers performed a sensory analysis of specific yogurt brands [55,56,58,68]. Most of the analyzed articles included research hypotheses (33), and a few included research questions [60,81,90], whereas some were devoid of both these research tools [43,54,68,71,74,80,85,88]. Only those research hypotheses that exclusively concerned PL products were taken for consideration in the analysis.

4. Discussion

We performed an SLR analysis on 44 studies related to consumer behavior toward PL products. The studies evaluated various factors determining the purchase of PL products, including perceived quality [54,55,56,59,65,69,72,73,82,83,85,88,89,91,92,93], packaging [55,56,69,73,86,93], price [29,38,59,63,64,69,70,71,72,73,74,75,77,78,82,83,86,88,89,90,91,92], health aspects [29,54,84,87], and brand loyalty [58,59,76,82,89]. Some of them also analyzed the frequency of the purchase of PL products [43,56,58,64,83,91].

The first research question concerned the product categories that were analyzed in the included studies. We found that the most analyzed food categories were dairy products, cereals, sweets, and frozen and processed food. These results reflect the value shares of product categories sold under PLs. For example, in western European countries, frozen foods (43%), chilled and fresh products (39%), and soft drinks (18.3%) have the highest value shares. As chilled and fresh foods, dairy products are frequently purchased by European consumers, and their value share ranges from as high as 55.4% in the UK to 42.1% in Spain and from 40.1% in the Netherlands to 21.8% in Italy [94]. In comparison, in the US, bakery products (36.6%), dairy products (33.1%), and delicatessen products (23.6%) had the highest share of sales in 2019 [95]. In Slovakia, dairy (40%) and durables (35%) were the most frequently purchased food categories, but the dairy category (46.6%) was dominant among products with the lowest income [16], and the sale shares of other categories were higher. Dairy products of PLs are therefore valued by consumers and selected by researchers for studies.

The available studies in the literature on PLs refer not only to consumer research. For example, studies conducted in Poland have analyzed PLs as a source of competitive advantage for international retail chains. It was found that organic PL products are competitive in terms of price, assortment range, variety, retailer image, sustainability and process uniqueness, and product-related attributes. The sales of organic PL products with offers allow consumers to buy organic food at more affordable prices and adopt a nutritious and sustainable diet with a low environmental impact [96].

The second research question concerned the non-health factors considered when consumers choose PL products. Our review shows that price is the main factor determining consumers’ choice of PL products. The significant influence of an attractive, lower price is confirmed by previous studies and reports on consumer behavior toward PL products [94,97,98,99]. The IRI report published in 2018 indicated that the average price of PL products in Europe in 2017 was about 70% of the average price of manufacturer brands, and these differences influenced consumers’ perception of PL products as low-cost products [100]. Such an image influences consumers’ price sensitivity, acting as a tool for building consumer loyalty to a retail chain and PL products [31,101]. This also highlights that PL products in general, as well as premium PL products specifically, are products of good value for money of [102]. Another frequently studied factor influencing the choice of PL products is the perceived quality of these products in comparison to NB products [103]. Many studies have analyzed the consumers’ perception of the quality of PL products. In reports and surveys, consumers have indicated a significant improvement in the quality of PL products. Importantly, the quality of PL products directly influences consumer loyalty to PLs and has an indirect impact on store loyalty [104]. Studies show that the quality of PL products is almost the same as that of NB products, which makes PL products more competitive. However, the retailers are required to maintain high quality at an attractive price in order to encourage consumers to purchase PL products [45]. This is also supported by the fact that consumers’ perception of higher quality increases their willingness to purchase PL products [105]. Our research in Poland and the UK showed that the high quality of products available under PLs is a more important factor for determining the purchase decision among UK consumers compared to Polish consumers [43]. At the same time, in the UK, the development of PLs is closer to sustainable and premium PLs, and quality improvement has become a key factor influencing choice [39]. Additionally, as indicated by a study in Germany, quality improvement has a stronger effect on the growth of PL market share compared to the case of NBs [106].

Although health aspects play an increasingly important role in consumer behavior toward PL products, they are not considered to be the main factor determining the choice of PL products. The inclusion of health considerations in consumer behavior toward PL products represents a gap in knowledge or research identified in this literature review. In answering the third research question, only four articles included in our SLR focused on health aspects. At the same time, the literature indicates the growing consumer awareness of food and its impact on well-being and health [1,2,4]. For example, the available research refers to different product categories, such as bread, fruit snacks [107], ready-to-eat cereals, and organic and functional foods [25], as well as food in general [108]. Research focusing on the consumer side addresses issues such as their willingness to eat bread with health benefits [109], the use of nutrition and health information on labels to increase the demand for bakery products [110], and the pleasure of eating and healthy food behaviors [111]. One study analyzed the attitudes of consumers toward healthy foods, with particular reference to organic and functional products that may contribute to better strategic and tactical marketing decisions, and which may also be used by government agencies in designing public health programs [25]. In one study conducted in the UK, US, and Germany, the impact of product attributes regarding the nutritional and health values of products on consumer choices was analyzed. European consumers were found to be more health-conscious in terms of lifestyle and diet than American consumers, and more focused on the nutritional value of the product, nutrition claims, or food labeling systems, rather than just the price and visual issues of product packaging [112]. Another study explored the perceptions of health by identifying elderly adults’ beliefs about food and health-related aspects, and showed that, according to senior consumers, health is about personal well-being (life is enjoyable) or about preventing diseases (energy and autonomy) [108]. In some studies, the authors examined consumer behavior in terms of health aspects, and found that consumers analyzed marketing activities, in particular marketing communication. For example, one of the studies analyzed the impact of two types of advertising content—healthy eating and anti-obesity—on the demand for healthy and unhealthy food products and beverages. The results indicated that among overweight consumers, anti-obesity advertisements were more effective than advertisements promoting healthy eating in reducing the demand for unhealthy items and increasing the demand for healthy products [2]. Some studies analyzed healthcare consumer behavior in online communities [113], the effect of product health information on consumer liking and choice [24], and the impact of health-promoting campaigns on sales [114].

Research related to the importance of health factors from the producers’ side indicates that there is a need to produce innovative products. These include healthy snacks for immediate consumption which are unique in terms of nutritional value and lack additives [107]. The need for innovative products is also indicated in studies on organic and functional foods [25], cereal products [115], and probiotic foods [116].

Our literature review fills the gap in the literature on the importance of health factors in consumer choices using the example of PL products. It has not only revealed the individual factors that have been analyzed by studies over time for selected product categories, but also shows the significance of health factors in private labeling and the different ways in which studies have analyzed consumer behavior toward PL products. The attention paid to the health aspects of PL products points to the development of PLs, characterized by a similar level of quality and price compared to producer brands. This increases the competitive rivalry in the market, and at the same time, for retail chains, provides a competitive advantage in strengthening their position in the market. In this way, PLs have reached the fourth generation of their development, which implies that analogous methods of brand creation, brand positioning and, above all, brand quality are evaluated by consumers at the same, or an even higher level.

Our study has some limitations. One of them is related to the fact that we excluded theoretical publications, conference materials, books, dissertations, and the reports of market research agencies, and included only publications in English in the SLR. Further research is needed as PL products continue to evolve into sustainable products. It is important to understand the intentions of retail chains regarding the development of PL products in order to verify if they are in line with the growing consumer awareness of the health aspects of food and nutrition. This will help in developing products under retail chains’ PLs with a high nutritional value based on nutritional recommendations.

5. Conclusions

Our literature review revealed that many factors influence consumer behavior toward PL products. The main non-health factors are price, quality, packaging, and purchase frequency of PL products, and brand loyalty. The perception of health factors was not among the frequently analyzed selection criteria, which may be due to the evolution of PL products from low-cost products to the products of sustainable brands. This review showed the changing issues related to researchers’ perceptions of the PLs of retail chains. Studies conducted at the beginning of the 21st century mainly analyzed price and its influence on PL product purchases. This was followed by value for money, and research in recent years has been focusing on premium and value-added products among PLs. Consumers have started to perceive these products as high-quality, innovative products, with organic packaging and health benefits. For the further development of PLs, an appropriate approach by retail chain managers is essential. Our review has identified several practical recommendations for designing new products, improving the quality of existing products in terms of raw material quality, packaging, design, and labeling, as well as developing effective marketing strategies, and monitoring consumer behavior and preferences. At the same time, expanding the PL product range with health-oriented, organic, innovative, and targeted products increases the competitive advantage of retail chains. This may allow for the availability of PL products as products sold for health reasons, which will align with the recommendations for healthy eating, proper diet composition, and choosing the right food.

Author Contributions

Study conception and design: M.C. and H.G.-W.; methodology: M.C. and H.G.-W.; writing—original and draft preparation: M.C., H.G.-W. and R.Z.; writing—review and editing: M.C. and H.G.-W. All authors have read and agreed to the published version of the manuscript.

Funding

The Article Processing Charge was financed by the Polish Ministry of Science and Higher Education within funds of Institute of Human Nutrition, Warsaw University of Life Sciences (WULS) for scientific research.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are available at the Department of Food Market and Consumption research in the Institute of Human Nutrition Sciences, Warsaw University of Life Sciences, in Poland.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Objectives and measurement items of studies included in the SLR.

Table A1.

Objectives and measurement items of studies included in the SLR.

| Author, Year | Objective | Measurement Items |

|---|---|---|

| Temmerman, et al. (2021) [54] | To analyze the impact of the presence of the Nutri-Score and its five categories on consumers’ perceived healthiness perceptions and purchase intention. To analyze the impact of the Nutri-Score on perceived quality, perceived healthiness, and purchase intentions (national brands vs. PLs). | Study 1: 6 items in a 7-point semantic differential (SD) scale: PQ: 1 item; PH: 5 items 9 items on a 7-point Likert scale: PT: 5 items, PI: 4 items Study 2: 4 items on a 7-point SD scale: PH: 1 item; FNS: 3 items 20 items on a 7-point Likert scale: PI: 4 items; NK: 8 items; PhF: 5 items; Db: 3 items |

| Kadekova, et al. (2020) [55] | To analyze the impact of packaging on consumer purchasing decisions in the yoghurt segment. | Questionnaire: 17 items, scale of 1 to 5 Blind test: on a scale of 1 to 5, with 1 being the best rating and 5 the worst The first test: tasting yoghurts without knowing it The second test: already-known packaging |

| Czeczotko, et al. (2020) [43] | To analyze the behavior of British and Polish consumers towards PL products, i.e., the frequency of purchasing PLs, the motives for purchasing products offered under PLs, the consumers’ opinions on PL development, and the length of the period of purchasing PL products. | 36 items: PP: 5 items (single answer) FP: 8 items (5-point Likert scale) OCD: 6 items (5-point Likert scale) FPC: 10 items (5-point scale) SPL: 7 items (% scale) |

| Anitha and Krishnan (2020) [57] | To examine the impulse purchase behavior of PL products in modern retail outlets and the major factors influencing it. | 26 items, 5-point Likert scale |

| Košičiarová, et al. (2020) [58] | To analyze customer preferences in the context of loyalty to the brand of selected food products in the segment of yoghurts. | Questionnaire: 10 items (5-point Likert scale) Blind test: on a scale of 1 to 5, with 1 being the best rating and 5 the worst |

| Singh and Singhal (2020) [59] | To understand consumers’ attitudes and preferences, as well as behavior, focusing on 3 types of PLs. To investigate how the grocery retailers are motivated to market the PLs. | 23 items (5-point Likert scale) |

| Košičiarová, et al. (2020) [56] | To analyze the influence of packaging and marketing communication tools on consumer purchasing decisions in the dairy segment. | Questionnaire: 10 items (5-point Likert scale), Blind test: on a scale of 1 to 5, with 1 being the best and 5 the worst: -1st round–-5 items: color, flavor, fragrance, consistency, and the chocolate ratio -2nd round—7 items: color, flavor, fragrance, consistency, chocolate ratio, the attractiveness of the packaging, and grammage |

| Prediger, et al. (2019) [60] | To explain how store flyer features affect the store traffic and the consumers’ intentions to buy PLs. To analyze the moderating effect of consumers’ perceptions on the retailer’s assortment and the store. | Experiment: Factor 1: brand promoted on the cover page (+1 = NB, or −1 = PL) Factor 2: the page length of the store flyer (+1=20 pages, or −1=8 p.) Factor 3: use of an institutional slogan on the cover page (+1 = presence or −1 = absence) Online survey: 2 items (7-point Likert scale) |

| Gómez-Suárez, et al. (2019) [61] | To find out the extent to which smart shopping and its effect on consumer attitudes towards PLs and national brands is influenced by consumers’ cultural values. | Study 1: 18 items on a 9-point Likert scale—“guiding principle of my life” Study 2: 18 items on a 7-point Likert scale—smart shopper concept, attitude |

| Salazar-Ordóñez et al. (2018) [62] | To examine value for consumers of own-label or PLs. | 7-point Likert scale for 13 items: AE: 4 items; AR: 4 items; PV: 5 items |

| Liu et al. (2018) [63] | To examine consumers’ preference for national brands and PLs and their tendency to include brands as part of their self-concept. | Study 1: 12 items (7-point Likert scale) Study 2: 7-point scale Study 3: 3 items on an SD 7-point scale |

| Valaskova et al. (2018) [16] | To determine factors and variables that significantly influence and shape the consumer’s perception and attitude towards the purchase of PL products. | 6 items: 5-point Likert scale: choice from 10 categories of PLs |

| Vázquez- Casielles and Cachero-Martinez (2018) [64] | To analyze how the introduction of economy and premium PLs affects national brands and standard PLs for different customer segments. | 18 items: 5-point Likert scale |

| Garczarek-Bąk (2018) [65] | To investigate the factors affecting PL products’ possible purchase decisions for different retailers. To analyze how motivation, measured by total fixation duration using EEG asymmetry over the frontal hemisphere of the brain, predicts PL purchase. | PPE: 6-point scale, from 1 (poor) to 6 (high) PI: The Juster scale, from 0 (not at all) to 11 (for sure) QA: 8 items on a 6-point scale |

| Meliana (2018) [66] | To explain how PLs can create an attractive store image and become a shopping preference for consumers. | 8 items (5-point Likert scale) |

| Modica et al. (2018) [67] | To investigate the reactions of the EEG and the autonomic activities, as elicited by the cross-sensory interaction (sight and touch) across several different products. To investigate whether the brand (major brand or PL), familiarity (foreign or local brand), and hedonic value of products (comfort food or daily food) influence the reaction during their interaction with the products. | Each phase with eyes closed for 15 s and rating on the scale from −5 to +5: Experiment 1: VE, VTE; Experiment 2: TE, VE, VTE |

| Schouteten et al. (2017) [68] | To analyze the role of the research setting and brand information on the overall acceptance and sensory and emotional profiling of 5 strawberry yogurts. | 1. Emotional profiling—18 emotional terms: -8 positive terms (contented, friendly, good, happy, interested, pleasant, surprised, satisfied) -8 negative terms (bored, disappointed, discontented, disgust, dissatisfied, frustrated, stressed) -2 neutral terms (calm, steady) 2. Overall liking: 5-point scale (from 1 = slightly to 5 = extremely) 3. Sensory profiling: 12 sensory terms (aftertaste, creamy, dark color, firm, fruity, milky flavor, sour, liquid, homogeneous, smooth, sweet, and thick) |

| Jara et al. (2017) [69] | To analyze PL equity by considering two PL’s positioning strategies: those with high perceived added value (the organic store brands), as opposed to economic brands. | 11 items (5-point Likert scale) Respondents to look at an A3-sized image of a pack of four |

| Gomez-Suarez et al. (2016) [70] | To analyze the relationships between the different phases of the evaluation of PLs (attitude, preference, and purchase intention) in an international context. | 1 item: scale (0 = NB and 1 = SB) 8 items: 7-point Likert scale |

| Marques dos Santos et al. (2016) [71] | To explore brain-based differences in perception of national brands and PLs. To study the influence of price as a differentiating characteristic of national brands and PLs. | 15 explanatory variables (EVs): -12 items: type of brand (national and PLs), exhibited price (real market price and manipulated price), and the stage in the stimulus sequence (product, price, and decision) - 3 items: product, price, and decision for the overseas branded products |

| Thanasuta (2015) [72] | To investigate the relationship between consumer decision-making styles and actual purchases of PL products, using price consciousness, quality consciousness, brand consciousness, value consciousness, and risk perception. | 7-point Likert scale for 23 items: PLs purchase: 1 item; QC: 4 items QC: 4 items; BC: 4 items; VC: 6 items; RP: 4 items |

| Schnittka (2015) [38] | To identify the moderating impact of the store, category, and PL characteristics on consumers’ preferences for premium vs. economy PLs. | 7-point Likert scale: Study 1: 2 items Study 2a: 9 items Study 2b: 9 items |

| Monnot et al. (2015) [73] | To examine how eliminating overpackaging influences consumers’ perception of products sold under generic and mimic PL and purchase intention. | 1. 5-point Likert scale for 17 items: PS: 3 items; PQ: 3 items EC: 3 items; PE: 2 items; PI: 2 items; PEF: 2 items; PC: 2 items 2. OP: 4 items (5-point Likert scale) |

| Diallo et al. (2015) [74] | To investigate the role of image and consumer factors in influencing the choice of PLs between two retail chains (Carrefour and Extra). | 7-point Likert scale for 28 items: SIP: 9 items; SPI: 6 items; VP: 4 items A: 4 items; PI: 4 items; PL choice: 1 item |

| Zielke and Komor (2015) [75] | To extend cross-national research on price role orientations by focusing on culturally similar but economically different countries, relating differences to preferences for PLS and low-price store formats, and analyzing these effects for functional vs. hedonic and low- vs. high-price products. | 1. 7 items (7-point Lichtenstein’s scale) 2. 12 items (7-point Lichtenstein’s scale scale) |

| Fall-Diallo et al. (2015) [76] | To investigate how previous experience with PLs and marketing policy variables affect PL purchasing behavior in two specific periods (expansion and crisis). | Variables to each product and period: price, feature, display, loyalty (0 (no) or 1 (yes)) |

| Delgado-Ballester et al. (2014) [77] | To develop and test a conceptual model of the moderating effect of customers’ value consciousness on the relationship of store image with four dimensions of the perceived risk associated with the purchase of a PL over a manufacture brand, and the direct effect of those variables on the perceived unfairness of manufacture brand prices. | For each factor, a 10-point scale: SI: 7 items; FR: 3 items; FiR: 3 items; SR: 4 items; PR: 3 items; PU: 3 items; VC: 5 items |

| Bauer et al. (2013) [29] | To analyze if an organic labeled product generates positive consumer brand perceptions and, thus, influences consumers’ food buying intentions. To investigate how various types of brands’ benefit differently from organic labeling in the retail market. | Study 1: 12 German consumers using the laddering technique Study 2: 7-point Likert scale for 12 items: PH: 4 items; PHe: 4 items; EF: 4 items FS: 4 items Study 3: 7-point Likert scale for 2 items: PI: 1 item; WP: 1 item |

| Fall Diallo et al. (2013) [78] | To investigate how consumer and image factors, as well as store familiarity, influence PL purchase behavior. | 7-point Likert scale for 24 items: SIP: 4 items; SB PI: 4 items; VC: 4 items; A: 4 items; PIn: 4 items; PL choice: 4 items |

| Herstein et al. (2012) [79] | To investigate the association between 3 personality traits (individualism, materialism, and the “need for cognition”) and 2 characteristics of shoppers who buy PLs, and the importance they attach to the “brand dimensions”. | 5-point Likert scale: Study 1: 10 items (5 food and 5 non-food products) Study 2: 2 items Study 3: 33 items: VI: 4 items; HI: 4 items; M: 7 items; NC: 18 items |

| Wyma et al. (2012) [80] | To explore and describe consumers’ preferences for different PLs and national brands in a South African context. To determine and describe a possible relationship between consumers’ psychographic and demographic characteristics and their preferences for PLs/national brands. | 25 items, choose the brand which fits one’s preference 5-point Likert scale 8 items + living standard measure |

| Tifferet and Herstein (2010) [81] | To analyze whether individualism affects consumers’ preference for PLs vs. national brands; assess the effect of individualism on the perceived importance of brand image dimensions (country of origin, packaging design, and manufacturer reputation); and assess the degree of cross-cultural differences in individualism. | 5-point Likert scale: Study 1: 10 items Study 2: 30 items Study 3: 8 items |

| Glynn and Chen (2009) [82] | To examine the differences in the level category of risk perception and brand loyalty effects on consumer proneness towards buying PLs. | 5-point Likert scale for 16 items: PM: 2 items; QV: 3 items; S vs. E: 2 items PC: 3 items; PQP: 3 items; BL: 3 items PL purchase: buy NBs (1) or PLs (5) |

| Anchor and Kourilová (2009) [83] | To show how relatively little is known about the consumer perceptions of PLs in the newly emerging markets of Central and Eastern Europe. To investigate various aspects of consumer perceptions of Tesco PLs in the Czech Republic. | 3 items: 7-point semantic differential (SD) scale 2 brands x 4 items: 7-point SD scale |

| Kara et al. (2009) [84] | To examine consumers’ behavior with regard to PL purchasing by using a conceptual model, which incorporates factors such as brand, price and risk perceptions, involvement, experience, and familiarity, as well as psychographic and demographic factors. | 27 items (5-point Likert scale) |

| Albayrak and Aslan (2009) [85] | To identify the attitudes toward PL products and demographic features of PL consumers and of manufacturer brand consumers. To determine whether any differences exist between the two consumer groups. | 5-point Likert scale: 4 × 16 items |

| Cheng et al. (2007) [86] | To investigate the differences in the consumer perceptions of product quality, price, leadership, and personality brand among national brands, international and local PLs. | 2 products x 3 types of brand x 4 items for 1 product 7-point Likert scale: PQ: 3 items BL: 3 items PP: 1 item BP: 3 items |

| Mieres et al. (2006) [87] | To analyze the effects that a set of variables related to purchasing behavior have on the difference in perceived risk between PLs and national brands. | Each item for kitchen rolls and shampoo: A: 7-point Likert scale: PQ: 4 items; REA: 7 items; SSC: 5 items FSB: 4 items; EPC: 4 items B: 7-point Likert scale: FR: 4 items; FiR: 3 items; SR: 4 items PR: 4 items; PsR: 4 items; TR: 4 items |

| Akbay and Jones (2005) [88] | To determine whether purchase patterns are differ for two income groups, and whether these differences are consistent with economic theory. To analyze the relationship between income and shopping behavior. | A: 1. 9 items: % scales 2. 9 items: cents per ounce B: 1. 9 items: % scales 2. 9 items: cents per ounce C: 1. 18 items: the LA/AIDS model 2. 18 items: the LA/AIDS model D: 1. 8 items: the LA/AIDS model 2. 18 items: the LA/AIDS model 3. 18 items: the LA/AIDS model |

| Kurtulus et al. (2005) [89] | To construct a model to determine the effect of the psychographics of consumers on their tendency to purchase PLs. To analyze the role of consumer attitudes and behaviors in consumer preferences for PLs. | 5-point Likert scale: PC: 4 items; FC: 4 items QC: 4 items; SL: 4 items SM: 3 items; TL: 3 items BL: 3 items; T: 3 items |

| Semeijn et al. (2004) [90] | To investigate how store image and the perceived risk associated with product attributes affect the consumer evaluation of PLs. To determine the structural relationships between store image, the perceived risk associated with product attributes, and consumer attitude towards PLs. | Study 1: 11 items on a 7-point Likert scale Study 2: 7-point scale Study 3: 3 stores x 4 products 12 items: 7-point Likert scale |

| Veloutsou et al. (2004) [91] | To compare the importance of choice criteria when purchasing PLs and national brands, and the perceived characteristics of the products under PLs and manufacturer brands in two regions at different stages of PL development. To rate the change in the behavior towards PLs and supermarkets and product attributes (perceived quality, value for money, appealing packaging, perceived taste, and the importance of these values for PLs and national brands). | Study 1: 4 items on a 5-point Likert scale Study 2: average of the 5 categories of products; 5-point semantic differential scales (SEM) A: 4 items B: 5 items C: 5 items Study 3: 5 items on a 5-point SEM |

| Miquel et al. (2002) [92] | To model the decision process involved in a purchase when choosing PLs over national brands, and investigate why the same consumer may choose a store brand in one product category and not in another. | (1) 2 items: 5-point Likert scale (2) 2 items: 5-point Likert scale (3) 2 items: do not buy SB (0)/buy SB (1) |

| Vaidyanathan and Aggarwal (2000) [93] | To examine how a national brand’s extension to a PL product (through ingredient branding) affects the evaluation of national brands and PLs. | PA: 10 items on a 7-point SEM scale QP: 5 items on a 7-point quality scale VP: 6 items on a 7-point scale VC: 7 items on a 7-point value scale |

References

- Rana, J.; Paul, J. Consumer behavior and purchase intention for organic food: A review and research agenda. J. Retail. Consum. Serv. 2017, 38, 157–165. [Google Scholar] [CrossRef]

- Wang, R.; Liaukonyte, J.; Kaiser, H.M. Does Advertising Content Matter? Impacts of Healthy Eating and Anti-Obesity Advertising on Willingness to Pay by Consumer Body Mass Index. Agric. Resour. Econ. Rev. 2018, 47, 1–31. [Google Scholar] [CrossRef]

- Ali, T.; Ali, J. Factors affecting the consumers’ willingness to pay for health and wellness food products. J. Agric. Food Res. 2020, 2, 1–8. [Google Scholar] [CrossRef]

- Pindus, N.; Hafford, C. Food security and access to healthy foods in Indian country: Learning from the Food Distribution Program on Indian Reservations. J. Public Aff. 2019, 19, 1–8. [Google Scholar] [CrossRef]

- Bandara, W. Consumer Decision-Making Styles and Local Brand Biasness: Exploration in the Czech Republic. J. Compet. 2014, 6, 3–17. [Google Scholar]

- Antonić, B.; Jančíková, S.; Dordević, D.; Tremlová, B. Grape pomace valorization: A systematic review and meta-analysis. Foods 2020, 9, 1627. [Google Scholar] [CrossRef]

- Sproles, E.K.; Sproles, G.B. Consumer Decision-Making Styles as a Function of Individual Learning Styles. J. Consum. Aff. 1990, 24, 134–147. [Google Scholar] [CrossRef]

- Sprotles, G.B.; Kendall, E.L. A Methodology for Profiling Consumers’ Decision-Making Styles. J. Consum. Aff. 1986, 20, 267–279. [Google Scholar] [CrossRef]

- Hafstrom, J.L.; Chae, J.S.; Chung, Y.S. Consumer Decision-Making Styles: Comparison Between United States and Korean Young Consumers. J. Consum. Aff. 1992, 26, 146–158. [Google Scholar] [CrossRef]

- Walsh, G.; Mitchell, V.W.; Hennig-Thurau, T. German consumer decision-making styles. J. Consum. Aff. 2001, 35, 73–95. [Google Scholar] [CrossRef]

- Leo, C.; Bennett, R.; Härtel, C.E. Cross cultural differences in consumer decision making styles. Cross Cult. Manag. Int. J. 2005, 12, 32–62. [Google Scholar] [CrossRef]

- Fan, J.X.; Xiao, J.J. Consumer decision-making styles of young-adult Chinese. J. Consum. Aff. 1998, 32, 275–294. [Google Scholar] [CrossRef]

- Rezaei, S. Segmenting consumer decision-making styles (CDMS) toward marketing practice: A partial least squares (PLS) path modeling approach. J. Retail. Consum. Serv. 2015, 22, 1–15. [Google Scholar] [CrossRef]

- Shim, S.; Koh, A. Profiling Adolescent Consumer Decision-Making Styles: Effects of Socialization Agents and Social-Structural Variables. Cloth. Text. Res. J. 1991, 15, 50–59. [Google Scholar] [CrossRef]

- Hiu, A.S.Y.; Siu, N.Y.M.; Wang, C.C.L.; Chang, L.M.K. An Investigation of Decision-Making Styles of Consumers in China. J. Consum. Aff. 2001, 35, 326–345. [Google Scholar] [CrossRef]

- Valaskova, K.; Kliestikova, J.; Krizanova, A. Consumer Perception of Private Label Products: An Empirical Study. J. Compet. 2018, 10, 149–163. [Google Scholar]

- Kotler, P.; Keller, K.L. Marketing Management, 14th ed.; Pearson Education: London, UK, 2012; ISBN 9780132102926. [Google Scholar]

- Kumar, A.; Roy, S. Store Attribute and Retail Format Choice. Adv. Manag. 2013, 6, 27–33. [Google Scholar]

- Coelho, D.C.; Meneses, R.F.C.; Moreira, M.R.A. Factors Influencing Purchase Intention of Private Label Products: The Case of Smartphones. In Proceedings of the International Conference on Exploring Services Science, Porto, Portugal, 7–8 February 2013; João Falcão, C., Mehdi, S., Nóvoa, H., Eds.; Springer: Berlin/Heidelberg, Germany, 2013; Volume 7, pp. 939–945. [Google Scholar]

- Geyskens, I.; Gielens, K.; Gijsbrechts, E. Proliferating Private-Label Portfolios: How Introducing Economy and Premium Private Labels Influences Brand Choice. J. Mark. Res. 2010, 47, 791–807. [Google Scholar] [CrossRef]

- Steenkamp, J.B.E.M.; Geyskens, I. Manufacturer and retailer strategies to impact store brand share: Global integration, local adaptation, and worldwide learning. Mark. Sci. 2014, 33, 6–26. [Google Scholar] [CrossRef]

- Cristini, G.; Laurini, F. Growth factors of store brands in different store formats in Italy. Int. Rev. Retail. Distrib. Consum. Res. 2017, 27, 109–125. [Google Scholar] [CrossRef]

- Ali, B.J. Consumer attitudes towards healthy and organic food in the Kurdistan region of Iraq. Manag. Sci. Lett. 2021, 11, 2127–2134. [Google Scholar] [CrossRef]

- Roosen, J.; Marette, S.; Blanchemanche, S.; Verger, P. The effect of product health information on liking and choice. Food Qual. Prefer. 2007, 18, 759–770. [Google Scholar] [CrossRef]

- Annunziata, A.; Pascale, P. Consumer behaviour and attitudes towards healthy food products: Organic and functional foods. In Proceedings of the A Resilient European Food Industry in a Challenging World, Chania, Greece, 3–6 September 2009; pp. 1–14. [Google Scholar]

- Private Label Market (PLMA). Private Label Popular across Europe. Available online: https://www.plmainternational.com/industry-news/private-label-today (accessed on 15 October 2020).

- De Wulf, K.; Odekerken-Schröder, G.; Goedertier, F.; Van Ossel, G. Consumer perceptions of store brands versus national brands. J. Consum. Mark. 2005, 22, 223–232. [Google Scholar] [CrossRef]

- Amrouche, N.; Rhouma, T.B.; Zaccour, G. Branding Decisions for Retailers’ Private Labels. J. Mark. Channels 2014, 21, 100–115. [Google Scholar] [CrossRef]

- Bauer, H.H.; Heinrich, D.; Schäfer, D.B. The effects of organic labels on global, local, and private brands. More hype than substance? J. Bus. Res. 2013, 66, 1035–1043. [Google Scholar] [CrossRef]

- Calvo-Porral, C.; Lévy-Mangin, J.P. Private label brands: Major perspective of two customer-based brand equity models. Int. Rev. Retail. Distrib. Consum. Res. 2014, 24, 431–452. [Google Scholar] [CrossRef]

- Beristain, J.J.; Zorrilla, P. The relationship between store image and store brand equity: A conceptual framework and evidence from hypermarkets. J. Retail. Consum. Serv. 2011, 18, 562–574. [Google Scholar] [CrossRef]

- Collins-Dodd, C.; Lindley, T. Store brands and retail differentiation: The influence of store image and store brand attitude on store own brand perceptions. J. Retail. Consum. Serv. 2003, 10, 345–352. [Google Scholar] [CrossRef]

- Ibarra Consuegra, O.; Kitchen, P. Own labels in the United Kingdom: A source of competitive advantage in retail business. Pensam. Gestión 2006, 21, 114–161. [Google Scholar]

- Walsh, G.; Mitchell, V.W. Consumers’ intention to buy private label brands revisited. J. Gen. Manag. 2010, 36, 3–24. [Google Scholar] [CrossRef]

- Cyran, K. The perception of private labels of food products vs. the prospects for their development. Res. Pap. Wrocław Univ. Econ. 2016, 450, 114–124. [Google Scholar]

- Laaksonen, H.; Reynolds, J. Own brands in food retailing across Europe. J. Brand Manag. 1994, 2, 37–46. [Google Scholar] [CrossRef]

- Górska-Warsewicz, H.; Czeczotko, M.; Kudlińska-Chylak, A. Consumer Behaviours towards Private Labels. Handel Wewnętrzny 2018, 2, 54–64. [Google Scholar]

- Schnittka, O. Are they always promising? An empirical analysis of moderators influencing consumer preferences for economy and premium private labels. J. Retail. Consum. Serv. 2015, 24, 94–99. [Google Scholar] [CrossRef]

- Kumar, N.; Steenkamp, J. Private Label Strategy: How to Meet the Store Brand Challenge, 1st ed.; Harvard Business School Press: Boston, MA, USA, 2007. [Google Scholar]

- Helmig, B.; Huber, J.-A.; Leeflang, P. Explaining behavioural intentions toward co-branded products. J. Mark. Manag. 2007, 23, 285–304. [Google Scholar] [CrossRef]

- Kilian, T.; Walsh, G.; Buxel, H. Measurement of Attitude Toward Private Labels: A Replication and Extension. Eur. Retail Res. 2008, 22, 69–85. [Google Scholar]

- Kowalska, M. Development and significance of private label in Poland. Stud. Pract. WNEiZ 2015, 39, 353–365. [Google Scholar]

- Czeczotko, M.; Górska-Warsewicz, H.; Laskowski, W. Towards sustainable private labels-What is the consumer behavior relating to private labels in the UK and Poland? Sustainability 2020, 12, 6035. [Google Scholar] [CrossRef]

- Czeczotko, M.; Górska-Warsewicz, H.; Laskowski, W.; Rostecka, B. Towards sustainable private labels in an autonomous community during covid-19—Analysis of consumer behavior and perception on the example of Tenerife. Sustainability 2021, 13, 7467. [Google Scholar] [CrossRef]

- Retnawati, B.B.; Ardyan, E.; Farida, N. The important role of consumer conviction value in improving intention to buy private label product in Indonesia. Asia Pac. Manag. Rev. 2017, 23, 193–200. [Google Scholar] [CrossRef]

- Wang, J.J.; Torelli, C.J.; Lalwan, A.K. The interactive effect of power distance belief and consumers’ status on preference for national (vs. private-label) brands. J. Bus. Res. 2020, 107, 1–12. [Google Scholar] [CrossRef]

- Arnould, E.J.; Price, L.; Zinkhan, G.M. Consumers, 2nd ed.; McGraw-Hill/Irwin: Boston, MA, USA, 2004. [Google Scholar]

- Liberati, A.; Altman, D.G.; Tetzlaff, J.; Mulrow, C.; Gøtzsche, P.C.; Ioannidis, J.P.A.; Clarke, M.; Devereaux, P.J.; Kleijnen, J.; Moher, D. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: Explanation and elaboration. J. Clin. Epidemiol. 2009, 62, e1–e3. [Google Scholar] [CrossRef] [PubMed]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; Altman, D.; Antes, G.; Atkins, D.; Barbour, V.; Barrowman, N.; Berlin, J.A.; et al. Preferred reporting items for systematic reviews and meta-analyses: The PRISMA statement. PLoS Med. 2009, 6, e1000097. [Google Scholar] [CrossRef] [PubMed]

- Górska-Warsewicz, H.; Kulykovets, O. Hotel brand loyalty—A systematic literature review. Sustainability 2020, 12, 4810. [Google Scholar] [CrossRef]

- Głąbska, D.; Guzek, D.; Groele, B.; Gutkowska, K. Fruit and vegetable intake and mental health in adults: A systematic review. Nutrients 2020, 12, 115. [Google Scholar] [CrossRef]

- Del Prete, M.; Samoggia, A. Chocolate consumption and purchasing behaviour review: Research issues and insights for future research. Sustainability 2020, 12, 5586. [Google Scholar] [CrossRef]

- Górska-Warsewicz, H.; Dębski, M.; Fabuš, M.; Kováč, M. Green brand equity—Empirical experience from a systematic literature review. Sustainability 2021, 13, 11130. [Google Scholar] [CrossRef]

- De Temmerman, J.; Heeremans, E.; Slabbinck, H.; Vermeir, I. The impact of the Nutri-Score nutrition label on perceived healthiness and purchase intentions. Appetite 2021, 157, 1–11. [Google Scholar] [CrossRef]

- Kadekova, Z.; Kosiciarová, I.; Vavrecka, V.; Dzupina, M. The impact of packaging on consumer behavior in the private label market—The case of Slovak consumers under 25 years of age. Innov. Mark. 2020, 16, 62–73. [Google Scholar] [CrossRef]

- Košičiarová, I.; Kádeková, Z.; Kubicová, Ľ.; Predanocyová, K.; Rybanská, J.; Džupina, M.; Bulanda, I. Rational and irrational behavior of slovak consumers in the private label market. Potravin. Slovak J. Food Sci. 2020, 14, 402–411. [Google Scholar] [CrossRef]

- Anitha, V.; Krishnan, A.R. Situational factors ascendant impulse purchase behavior of private label brands with special reference to modern trade retail outlets in Chennai. Int. J. Manag. 2020, 11, 178–187. [Google Scholar]

- Košičiarová, I.; Kádeková, Z.; Holotová, M.; Kubicová, L.; Predanocyová, K. Consumer preferences in the content of loyalty to the yoghurt brand. Agris Online Pap. Econ. Inform. 2020, 12, 37–48. [Google Scholar] [CrossRef]

- Singh, A.; Singhal, R.K. Emerging third generation private label brands: Retailers’ and consumers’ perspectives towards leading Indian retail chains. Int. J. Bus. Emerg. Mark. 2020, 12, 179–203. [Google Scholar] [CrossRef]

- Prediger, M.; Huertas-Garcia, R.; Gázquez-Abad, J.C. Store flyer design and the intentions to visit the store and buy: The moderating role of perceived variety and perceived store image. J. Retail. Consum. Serv. 2019, 51, 202–211. [Google Scholar] [CrossRef]

- Gómez-Suárez, M.; Quinõnes, M.; Yaguë, M.J. How individual value structures shape smart shopping experience and brand choices: An international perspective. Eur. J. Int. Manag. 2019, 13, 515–532. [Google Scholar]

- Salazar-Ordóñez, M.; Schuberth, F.; Cabrera, E.R.; Arriaza, M.; Rodríguez-Entrena, M. The effects of person-related and environmental factors on consumers’ decision-making in agri-food markets: The case of olive oils. Food Res. Int. 2018, 112, 412–424. [Google Scholar] [CrossRef] [PubMed]

- Liu, R.L.; Sprott, D.E.; Spangenberg, E.R.; Czellar, S.; Voss, K.E. Consumer preference for national vs. private brands: The influence of brand engagement and self-concept threat. J. Retail. Consum. Serv. 2018, 41, 90–100. [Google Scholar] [CrossRef]

- Vázquez-Casielles, R.; Cachero-Martínez, S. Multi-tiered private labels portfolio strategies: Effects on consumer behavior. J. Mark. Channels 2018, 25, 36–46. [Google Scholar] [CrossRef]

- Garczarek-Bąk, U. Explicit and Implicit Factors That Determine Private Labels’ Possible Purchase: Eyetracking and EEG Research. Int. J. Manag. Econ. 2018, 54, 36–49. [Google Scholar] [CrossRef]

- Meliana, V. Private Label Brand as Better Competitive Advantage for Local Retailers. Bus. Manag. Res. 2019, 74, 170–173. [Google Scholar]

- Modica, E.; Cartocci, G.; Rossi, D.; Martinez Levy, A.C.; Cherubino, P.; Maglione, A.G.; Di Flumeri, G.; Mancini, M.; Montanari, M.; Perrotta, D.; et al. Neurophysiological responses to different product experiences. Comput. Intell. Neurosci. 2018, 2018, 9616301. [Google Scholar] [CrossRef] [PubMed]

- Schouteten, J.J.; De Steur, H.; Sas, B.; De Bourdeaudhuij, I.; Gellynck, X. The effect of the research setting on the emotional and sensory profiling under blind, expected, and informed conditions: A study on premium and private label yogurt products. J. Dairy Sci. 2017, 100, 169–186. [Google Scholar] [CrossRef] [PubMed]

- Jara, M.; Cliquet, G.; Robert, I. A comparison between economic and organic store brands: Packaging as a key factor of store brand equity. Int. J. Retail Distrib. Manag. 2017, 45, 1298–1316. [Google Scholar] [CrossRef]

- Gómez-Suárez, M.; Quinones, M.; Yagúe, M.J. Store brand evaluative process in an international context. Int. J. Retail Distrib. Manag. 2016, 44, 754–771. [Google Scholar] [CrossRef]

- Marques dos Santos, J.P.; Martins, M.; Ferreira, H.A.; Ramalho, J.; Seixas, D. Neural imprints of national brands versus own-label brands. J. Prod. Brand Manag. 2016, 25, 184–195. [Google Scholar] [CrossRef]

- Thanasuta, K. Thai consumers’ purchase decisions and private label brands. Int. J. Emerg. Mark. 2015, 10, 102–121. [Google Scholar] [CrossRef]

- Monnot, E.; Parguel, B.; Reniou, F. Consumer responses to elimination of overpackaging on private label products. Int. J. Retail Distrib. Manag. 2015, 43, 329–349. [Google Scholar] [CrossRef]

- Diallo, M.F.; Burt, S.; Sparks, L. The influence of image and consumer factors on store brand choice in the brazilian market: Evidence from two retail chains. Eur. Bus. Rev. 2015, 27, 495–512. [Google Scholar] [CrossRef]

- Zielke, S.; Komor, M. Cross-national differences in price–role orientation and their impact on retail markets. J. Acad. Mark. Sci. 2015, 43, 159–180. [Google Scholar] [CrossRef]

- Fall-Diallo, M.; Kaswengi, J.; Gázquez-Abad, J.C. The Role of Previous Experience and Marketing Policy on Consumer Behaviour Towards Different Private Label Categories. In Advances in National Brand and Private Label Marketing; Springer: Cham, Switzerland, 2015; pp. 193–201. [Google Scholar]

- Delgado-Ballester, E.; Hernandez-Espallardo, M.; Rodriguez-Orejuela, A. Store image influences in consumers’ perceptions of store brands: The moderating role of value consciousness. Eur. J. Mark. 2014, 48, 1850–1869. [Google Scholar] [CrossRef]

- Fall Diallo, M.; Chandon, J.L.; Cliquet, G.; Philippe, J. Factors influencing consumer behaviour towards store brands: Evidence from the French market. Int. J. Retail Distrib. Manag. 2013, 41, 422–441. [Google Scholar] [CrossRef]

- Herstein, R.; Tifferet, S.; Abrantes, J.L.; Lymperopoulos, C.; Albayrak, T.; Caber, M. The effect of personality traits on private brand consumer tendencies: A cross-cultural study of Mediterranean countries. Cross Cult. Manag. 2012, 19, 196–214. [Google Scholar] [CrossRef]

- Wyma, L.; Van der Merwe, D.; Bosman, M.J.C.; Erasmus, A.C.; Strydom, H.; Steyn, F. Consumers’ preferences for private and national brand food products. Int. J. Consum. Stud. 2012, 36, 432–439. [Google Scholar] [CrossRef]

- Tifferet, S.; Herstein, R. The effect of individualism on private brand perception: A cross-cultural investigation. J. Consum. Mark. 2010, 27, 313–323. [Google Scholar] [CrossRef]

- Glynn, M.S.; Chen, S. Consumer-factors moderating private label brand success: Further empirical results. Int. J. Retail Distrib. Manag. 2009, 37, 896–914. [Google Scholar] [CrossRef]

- Anchor, J.R.; Kouřilová, T. Consumer perceptions of own brands: International differences. J. Consum. Mark. 2009, 26, 439–451. [Google Scholar] [CrossRef]

- Kara, A.; Rojas-Méndez, J.I.; Kucukemiroglu, O.; Harcar, T. Consumer preferences of store brands: Role of prior experiences and value consciousness. J. Target. Meas. Anal. Mark. 2009, 17, 127–137. [Google Scholar] [CrossRef][Green Version]

- Albayrak, M.; Aslan, Z. A comparative study of consumer preferences for manufacturer or private labelled food products. Afr. J. Bus. Manag. 2009, 3, 764–772. [Google Scholar]

- Ming-Sung Cheng, J.; Shui-Lien Chen, L.; Shih-Tse Wang, E.; Ying-Chao Lin, J. Do consumers perceive differences among national brands, international private labels and local private labels? The case of Taiwan. J. Prod. Brand Manag. 2007, 16, 368–376. [Google Scholar] [CrossRef]

- Mieres, C.G.; Martín, A.M.D.; Gutiérrez, J.A.T. Antecedents of the difference in perceived risk between store brands and national brands. Eur. J. Mark. 2006, 40, 61–82. [Google Scholar] [CrossRef]

- Akbay, C.; Jones, E. Food consumption behavior of socioeconomic groups for private labels and national brands. Food Qual. Prefer. 2005, 16, 621–631. [Google Scholar] [CrossRef]

- Kurtuluş, K.; Kurtuluş, S.; Yeniçeri, T.; Yaraş, E. The role of psychographics in explaining store brand buying behavior. Bogazici J. 2005, 19, 99–113. [Google Scholar] [CrossRef]

- Semeijn, J.; van Riel, A.C.R.; Ambrosini, A.B. Consumer evaluations of store brands: Effects of store image and product attributes. J. Retail. Consum. Serv. 2004, 11, 247–258. [Google Scholar] [CrossRef]

- Veloutsou, C.; Gioulistanis, E.; Moutinho, L. Own labels choice criteria and perceived characteristics in Greece and Scotland: Factors influencing the willingness to buy. J. Prod. Brand Manag. 2004, 13, 228–241. [Google Scholar] [CrossRef]

- Miquel, S.; Caplliure, E.M.; Aldas-Manzano, J. The effect of personal involvement on the decision to buy store brands. J. Prod. Brand Manag. 2002, 11, 6–18. [Google Scholar] [CrossRef]

- Vaidyanathan, R.; Aggarwal, P. Strategic brand alliances: Implications of ingredient branding for national and private label brands. J. Prod. Brand Manag. 2000, 9, 214–228. [Google Scholar] [CrossRef]

- Eales, T. Private Label in Western Economies. Available online: https://www.iriworldwide.com/en-GB/News/Media-Coverage/Private-label-in-Europe-Tailor-your-growth-strategy-per-country,-says-IRI (accessed on 20 May 2021).

- Statistica.com. Sales Share of Private Labels Food in USA in 2019, by Category. Available online: Statistica.com/statistics/1100038/sale-share-of-private-label-food-us-by-category/ (accessed on 25 May 2020).

- Górska-Warsewicz, H.; Żakowska-Biemans, S.; Czeczotko, M.; Świątkowska, M.; Stangierska, D.; Świstak, E.; Bobola, A.; Szlachciuk, J.; Krajewski, K. Organic Private Labels as Sources of Competitive Advantage—The Case of International Retailers Operating on the Polish Market. Sustainability 2018, 10, 2338. [Google Scholar] [CrossRef]

- The Rise and Rise Again of Private Label. 2018. Available online: http://www.nielsen.com/us/en/insights/reports/2018/the-riseand-rise-again-of-private-label.html (accessed on 9 June 2019).

- Nielsen the State of Private Label Around the World. Available online: https://www.nielsen.com/wp-content/uploads/sites/3/2019/04/state-of-private-label-around-the-world-nov-2014.pdf (accessed on 5 October 2020).

- IRI Share of Private-Label-Price-Level-in-Europe-2018-by-Country. 2019. Available online: https://www.statista.com/statistics/383455/private-label-price-level-by-european-countries/ (accessed on 22 May 2020).

- Abotorabi, O. Private Label in Western Economies IRI Special Report. Available online: https://www.iriworldwide.com/site/IRI/media/IRI-Clients/International/IRI-PL-Report_July-2018.pdf (accessed on 12 May 2020).

- Ipek, I.; Aşkin, N.; Ilter, B. Private label usage and store loyalty: The moderating impact of shopping value. J. Retail. Consum. Serv. 2016, 31, 72–79. [Google Scholar] [CrossRef]

- Nenycz-Thiel, M.; Romaniuk, J. Understanding premium private labels: A consumer categorisation approach. J. Retail. Consum. Serv. 2016, 29, 22–30. [Google Scholar] [CrossRef]

- Peter, J. Boyle and E. Scott Lathrop the value of private label brands to U.S. consumers: An objective and subjective assessment. J. Retail. Consum. Serv. 2007, 20, 80–86. [Google Scholar]

- do Vale, R.C.; Verga Matos, P.; Caiado, J. The impact of private labels on consumer store loyalty: An integrative perspective. J. Retail. Consum. Serv. 2016, 28, 179–188. [Google Scholar] [CrossRef]

- Wanjiku, M. Consumer Perception towards Private Label Brands of Four Key Supermarkets in Kenya; University of Nairobi: Nairobi, Kenya, 2015; pp. 1–55. [Google Scholar]

- Olbrich, R.; Jansen, H.C.; Hundt, M. Effects of pricing strategies and product quality on private label and national brand performance. J. Retail. Consum. Serv. 2017, 34, 294–301. [Google Scholar] [CrossRef]

- Ciurzyńska, A.; Cieśluk, P.; Barwińska, M.; Marczak, W.; Ordyniak, A.; Lenart, A.; Janowicz, M. Eating Habits and Sustainable Food Production in the Development of Innovative “Healthy” Snacks (Running Title: Innovative and “Healthy” Snacks). Sustainability 2019, 11, 2800. [Google Scholar] [CrossRef]

- Lesakova, D. Health perception and food choice factors in predicting healthy consumption among elderly. Acta Univ. Agric. Silvic. Mendel. Brun. 2018, 66, 1527–1534. [Google Scholar] [CrossRef]

- Sajdakowska, M.; Gębski, J.; Żakowska-Biemans, S.; Jeżewska-Zychowicz, M. Willingness to eat bread with health benefits: Habits, taste and health in bread choice. Public Health 2019, 167, 78–87. [Google Scholar] [CrossRef]

- Borowska, A.; Rejman, K. The Use of Nutrition and Health Information on the Bakery Market to Increase the Demand for its Products (in Polish). Med. Sport. Pract. 2009, 10, 79–87. [Google Scholar]

- Giboreau, A.; Fleury, H. A new research platform to contribute to the pleasure of eating and healthy food behaviors through academic and applied Food and Hospitality research. Food Qual. Prefer. 2009, 20, 533–536. [Google Scholar] [CrossRef]

- Ghvanidze, S.; Velikova, N.; Dodd, T.; Oldewage-Theron, W. A discrete choice experiment of the impact of consumers’ environmental values, ethical concerns, and health consciousness on food choices. Br. Food J. 2017, 119, 863–881. [Google Scholar] [CrossRef]

- Gheorghe, I.-R.; Liao, M.-N. Investigating Romanian Healthcare Consumer Behaviour in Online Communities: Qualitative Research on Negative eWOM. Procedia—Soc. Behav. Sci. 2012, 62, 268–274. [Google Scholar] [CrossRef]

- Levy, A.S.; Stokes, R.C. Effects of a health promotion advertising campaign on sales of ready-to-eat cereals. Public Health Rep. 1987, 102, 398. [Google Scholar]

- Dean, M.; Shepherd, R.; Arvola, A.; Vassallo, M.; Winkelmann, M.; Claupein, E.; Lähteenmäki, L.; Raats, M.M.; Saba, A. Consumer perceptions of healthy cereal products and production methods. J. Cereal Sci. 2007, 46, 188–196. [Google Scholar] [CrossRef]

- Mattila-Sandholm, T.; Myllärinen, P.; Crittenden, R.; Mogensen, G.; Fondén, R.; Saarela, M. Technological challenges for future probiotic foods. Int. Dairy J. 2002, 12, 173–182. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).