Next-Generation Urbanism: ESG Strategies, Green Accounting, and the Future of Sustainable City Governance—A PRISMA-Guided Bibliometric Analysis

, ,

, ,

and

and

Abstract

1. Introduction

2. Literature Review

2.1. ESG Strategies and Urban Governance

2.2. Green Accounting and Environmental Governance

2.3. Sustainable Urbanism and Resilient Governance

3. Methodology

3.1. Data

3.2. Method

3.3. PRISMA Protocol

4. Results and Analysis

4.1. Network Analysis

4.2. Bibliometric Analysis

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

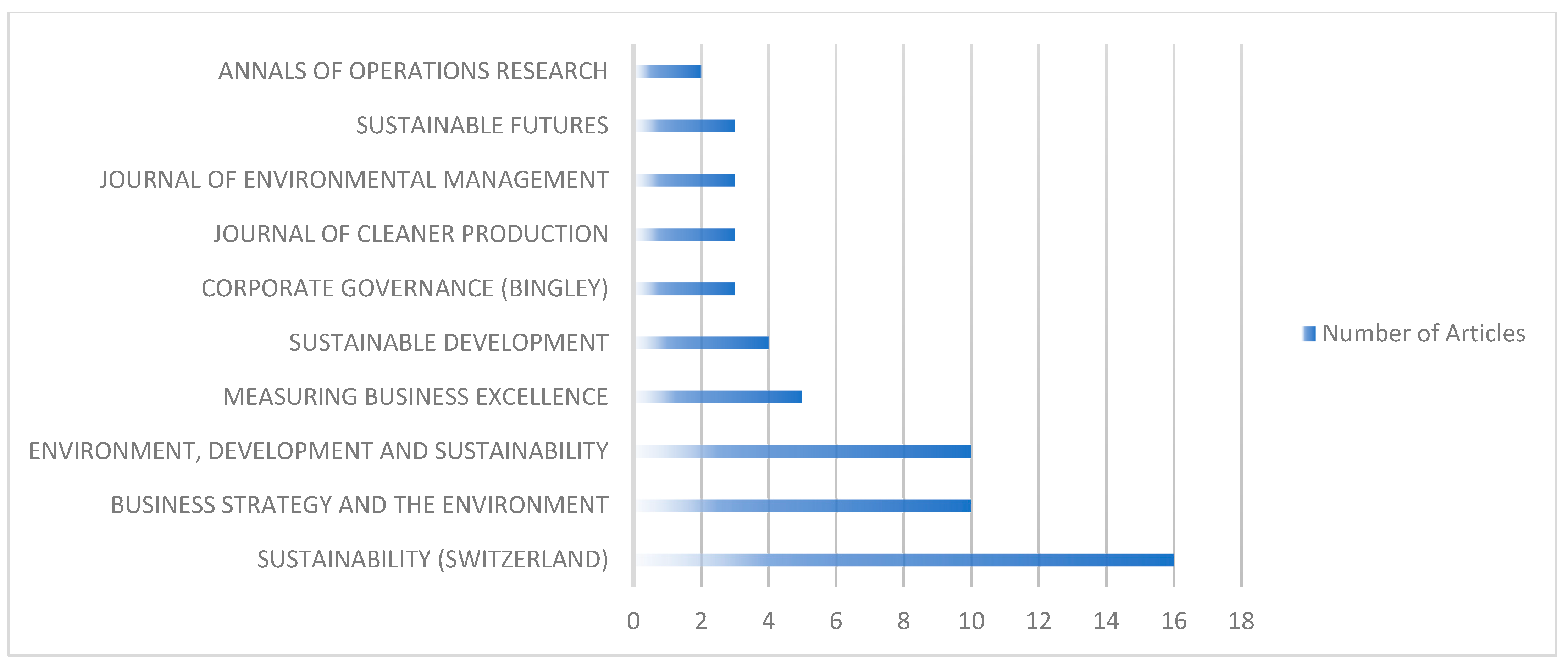

| SO | Rank | Freq | cumFreq | Zone |

|---|---|---|---|---|

| Sustainability (Switzerland) | 1 | 16 | 16 | Zone 1 |

| Business Strategy and The Environment | 2 | 10 | 26 | Zone 1 |

| Environment, Development and Sustainability | 3 | 10 | 36 | Zone 1 |

| Measuring Business Excellence | 4 | 5 | 41 | Zone 1 |

| Sustainable Development | 5 | 4 | 45 | Zone 1 |

| Corporate Governance (Bingley) | 6 | 3 | 48 | Zone 1 |

| Journal Of Cleaner Production | 7 | 3 | 51 | Zone 1 |

| Journal Of Environmental Management | 8 | 3 | 54 | Zone 1 |

| Sustainable Futures | 10 | 3 | 60 | Zone 2 |

| Annals Of Operations Research | 11 | 2 | 62 | Zone 2 |

| Cities | 12 | 2 | 64 | Zone 2 |

| Clean Technologies and Environmental Policy | 13 | 2 | 66 | Zone 2 |

| Cogent Business and Management | 14 | 2 | 68 | Zone 2 |

| Corporate Social Responsibility And Environmental Management | 15 | 2 | 70 | Zone 2 |

| Enhancing Sustainability Through Non-Financial Reporting | 16 | 2 | 72 | Zone 2 |

| Frontiers In Environmental Science | 17 | 2 | 74 | Zone 2 |

| Journal Of Environmental Planning And Management | 18 | 2 | 76 | Zone 2 |

| Journal Of Risk And Financial Management | 19 | 2 | 78 | Zone 2 |

| Meditari Accountancy Research | 20 | 2 | 80 | Zone 2 |

| Review Of Managerial Science | 21 | 2 | 82 | Zone 2 |

| Sn Business And Economics | 22 | 2 | 84 | Zone 2 |

| Technological Forecasting And Social Change | 23 | 2 | 86 | Zone 2 |

| Accounting For Carbon Neutrality: Corporate Accountability In The Hydrogen Economy | 24 | 1 | 87 | Zone 2 |

| Applied Sciences (Switzerland) | 25 | 1 | 88 | Zone 2 |

| Applied Soft Computing | 26 | 1 | 89 | Zone 2 |

| Benchmarking | 27 | 1 | 90 | Zone 2 |

| Biophysical Economy: Theory, Challenges, And Sustainability | 28 | 1 | 91 | Zone 2 |

| Business Ethics, The Environment And Responsibility | 29 | 1 | 92 | Zone 2 |

| Business Strategy And Development | 30 | 1 | 93 | Zone 2 |

| Carbon And Climate Law Review | 31 | 1 | 94 | Zone 2 |

| Cleaner Engineering And Technology | 32 | 1 | 95 | Zone 2 |

| Contributions To Finance And Accounting | 33 | 1 | 96 | Zone 2 |

| Convergence Of Industry 4.0 And Supply Chain Sustainability | 34 | 1 | 97 | Zone 2 |

| Discover Sustainability | 35 | 1 | 98 | Zone 2 |

| Economic Analysis And Policy | 36 | 1 | 99 | Zone 2 |

| Economics And Environment | 37 | 1 | 100 | Zone 2 |

| Ecosphere | 38 | 1 | 101 | Zone 2 |

| Edelweiss Applied Science And Technology | 39 | 1 | 102 | Zone 2 |

| Electronics (Switzerland) | 40 | 1 | 103 | Zone 2 |

| Enhancing Boardroom Diversity In Saudi Arabia | 41 | 1 | 104 | Zone 2 |

| Environmental And Sustainability Indicators | 42 | 1 | 105 | Zone 2 |

| Environmental Leadership In A Vuca Era: An Interdisciplinary Handbook | 43 | 1 | 106 | Zone 2 |

| Environmental Science And Pollution Research | 44 | 1 | 107 | Zone 2 |

| Financial And Technological Innovation For Sustainability: Environmental, Social And Governance Performance | 45 | 1 | 108 | Zone 2 |

| Global Corporate Social Responsibility Initiatives For Reluctant Businesses | 46 | 1 | 109 | Zone 2 |

| Green Bonds And Sustainable Finance: The Evolution Of Portfolio Management In Conventional Markets | 47 | 1 | 110 | Zone 3 |

| Green Technologies And Sustainability | 48 | 1 | 111 | Zone 3 |

| Harnessing Blockchain-Digital Twin Fusion For Sustainable Investments | 49 | 1 | 112 | Zone 3 |

| Harnessing Technology For Knowledge Transfer In Accountancy, Auditing, And Finance | 50 | 1 | 113 | Zone 3 |

| Human Perspectives Of Industry 4.0 Organizations: Reviewing Sustainable Performance | 51 | 1 | 114 | Zone 3 |

| Indian Journal Of Corporate Governance | 52 | 1 | 115 | Zone 3 |

| Information Systems Frontiers | 53 | 1 | 116 | Zone 3 |

| International Journal Of E-Business Research | 54 | 1 | 117 | Zone 3 |

| International Journal Of Environmental Research And Public Health | 55 | 1 | 118 | Zone 3 |

| International Journal Of Financial Studies | 56 | 1 | 119 | Zone 3 |

| International Journal Of Green Energy | 57 | 1 | 120 | Zone 3 |

| International Journal Of Innovation Science | 58 | 1 | 121 | Zone 3 |

| International Journal Of Learning, Teaching And Educational Research | 59 | 1 | 122 | Zone 3 |

| International Journal Of Productivity And Performance Management | 60 | 1 | 123 | Zone 3 |

| Intersecting Environmental Social Governance And Ai For Business Sustainability | 61 | 1 | 124 | Zone 3 |

| Issues Of Sustainability In Ai And New-Age Thematic Investing | 62 | 1 | 125 | Zone 3 |

| Journal Of Business Research | 63 | 1 | 126 | Zone 3 |

| Journal Of Economic Surveys | 64 | 1 | 127 | Zone 3 |

| Journal Of Emerging Technologies In Accounting | 65 | 1 | 128 | Zone 3 |

| Journal Of Financial Reporting And Accounting | 66 | 1 | 129 | Zone 3 |

| Journal Of Innovation And Knowledge | 67 | 1 | 130 | Zone 3 |

| Journal Of Management In Engineering | 68 | 1 | 131 | Zone 3 |

| Journal Of Risk Research | 69 | 1 | 132 | Zone 3 |

| Journal Of Sustainable Tourism | 70 | 1 | 133 | Zone 3 |

| Journal Of The Knowledge Economy | 71 | 1 | 134 | Zone 3 |

| Lecture Notes In Networks And Systems | 72 | 1 | 135 | Zone 3 |

| Managerial And Decision Economics | 73 | 1 | 136 | Zone 3 |

| Multidisciplinary Reviews | 74 | 1 | 137 | Zone 3 |

| Multiple Criteria Decision-Making | 75 | 1 | 138 | Zone 3 |

| Principles Of Sustainable Business: Frameworks For Corporate Action On The Sdgs | 76 | 1 | 139 | Zone 3 |

| Proceedings Of The European Conference On Innovation And Entrepreneurship, Ecie | 77 | 1 | 140 | Zone 3 |

| Public Money And Management | 78 | 1 | 141 | Zone 3 |

| Qualitative Research In Accounting And Management | 79 | 1 | 142 | Zone 3 |

| Quality-Access To Success | 80 | 1 | 143 | Zone 3 |

| Resources | 81 | 1 | 144 | Zone 3 |

| Sidrea Series In Accounting And Business Administration | 82 | 1 | 145 | Zone 3 |

| Smart Cities | 83 | 1 | 146 | Zone 3 |

| Society And Business Review | 84 | 1 | 147 | Zone 3 |

| Socio-Economic Planning Sciences | 85 | 1 | 148 | Zone 3 |

| Soft Computing | 86 | 1 | 149 | Zone 3 |

| Sport, Business And Management: An International Journal | 87 | 1 | 150 | Zone 3 |

| Springer Proceedings In Business And Economics | 88 | 1 | 151 | Zone 3 |

| Springer Proceedings In Mathematics And Statistics | 89 | 1 | 152 | Zone 3 |

| Strategies And Approaches Of Corporate Social Responsibility Toward Multinational Enterprises | 90 | 1 | 153 | Zone 3 |

| Sustainability Accounting, Management And Policy Journal | 91 | 1 | 154 | Zone 3 |

| Sustainability And Climate Change | 92 | 1 | 155 | Zone 3 |

| Sustainability Appraisal: A Sourcebook And Reference Guide To International Experience | 93 | 1 | 156 | Zone 3 |

| Sustainability Reporting And Blockchain Technology | 94 | 1 | 157 | Zone 3 |

| Sustainable Development Goals Series | 95 | 1 | 158 | Zone 3 |

| Sustainable Finance | 96 | 1 | 159 | Zone 3 |

| Transportation Research Part E: Logistics And Transportation Review | 97 | 1 | 160 | Zone 3 |

| Urban Sustainability | 98 | 1 | 161 | Zone 3 |

| Utilities Policy | 99 | 1 | 162 | Zone 3 |

References

- Azunre, G.A.; Azerigyik, R.A.; Amponsah, O.; Kpeebi, Y. The jugaad urbanism-sustainable circular cities nexus: Insights from sub-Saharan Africa’s informal settlements. Habitat Int. 2025, 158, 103349. [Google Scholar] [CrossRef]

- Oktay, D. Sustainable urbanism and identity: A holistic perspective for future cities. Perspect. Arch. Urban. 2024, 1, 100016. [Google Scholar] [CrossRef]

- Sepehri, B.; Sharifi, A. X-minute cities as a growing notion of sustainable urbanism: A literature review. Cities 2025, 161, 105902. [Google Scholar] [CrossRef]

- Silva, R.H.; Zwarteveen, M.; Stead, D.; Bacchin, T.K. Bringing Ecological Urbanism and Urban Political Ecology to transformative visions of water sensitivity in cities. Cities 2024, 145, 104685. [Google Scholar] [CrossRef]

- Liu, M.; Xia, C.; Lan, H.; Gao, Z.; Yu, X.; Wang, L.; Liang, X.; Wu, Y. Driving toward sustainable cities: The interplay between Chinese emerging corporate ESG performance and climate finance in achieving low-carbon development. Urban Clim. 2024, 55, 101918. [Google Scholar] [CrossRef]

- Sharma, P.; Jain, J.K.; Kalla, P. A multi-criteria decision analysis (MCDA) approach for evaluating the performance of Indian cities’ sustainable infrastructure. Mater. Today Proc. 2023, 6, 355. [Google Scholar] [CrossRef]

- de Oliveira Alves, D.; de Oliveira, L.; Mühl, D.D. Commercial urban agriculture for sustainable cities. Cities 2024, 150, 105017. [Google Scholar] [CrossRef]

- Liu, Y.; Dong, K.; Wang, K.; Taghizadeh-Hesary, F. Moving towards sustainable city: Can China’s green finance policy lead to sustainable development of cities? Sustain. Cities Soc. 2024, 102, 105242. [Google Scholar] [CrossRef]

- Jun, X.; Ai, J.; Zheng, L.; Lu, M.; Wang, J. Impact of information technology and industrial development on corporate ESG practices: Evidence from a pilot program in China. Econ. Model. 2024, 139, 106806. [Google Scholar] [CrossRef]

- Qin, L.; Feng, Y.; Wang, R.; Wang, Y. Impact of the National Ecological Civilization Construction Demonstration Zone on corporate ESG: Evidence from China. Ecol. Indic. 2024, 166, 112463. [Google Scholar] [CrossRef]

- Wang, S.; Li, J. How do energy input and carbon emission constraints affect the ESG performance of manufacturing enterprises? Evidence from China. Sustain. Futures 2024, 8, 112463. [Google Scholar] [CrossRef]

- Oberrauch, L.; Kaiser, T.; Seeber, G. Measuring economic competence of youth with a short scale. J. Econ. Psychol. 2023, 97, 102633. [Google Scholar] [CrossRef]

- Ghosh, J.; Morgan, J. A Life in Development Economics and Political Economy: An interview with Jayati Ghosh. Real-World Econ. Rev. 2022, 101, 44–64. Available online: https://www.paecon.net/PAEReview/issue101/GhoshMorgan101.pdf (accessed on 13 May 2025).

- Tang, J.; Huang, K. Eco-cities of tomorrow: How green finance fuels urban energy efficiency—Insights from prefecture-level cities in China. Energy Inform. 2024, 7, 148. [Google Scholar] [CrossRef]

- Xue, S.; Jiang, Y.; Wei, Q. Green financial accounting and transition in the mining sector in emerging economies. Resour. Policy 2024, 89, 104683. [Google Scholar] [CrossRef]

- Sun, Y.; Shen, Y.; Tan, Q. The spillover effect of customers’ ESG performance on suppliers’ green innovation quality. China J. Account. Res. 2024, 17, 100362. [Google Scholar] [CrossRef]

- Saha, A.K.; Dunne, T.; Dixon, R. Carbon disclosure, performance and the green reputation of higher educational institutions in the UK. J. Account. Organ. Chang. 2021, 17, 604–632. [Google Scholar] [CrossRef]

- van der Heijden, J. Governance for Urban Sustainability and Resilience: Responding to Climate Change and the Relevance of the Built Environment; Edward Elgar Publishing Ltd: Cheltenham, UK, 2014; p. 229. [Google Scholar]

- Ragazou, K.; Sklavos, G. Circular economy as a footpath for regional development in European Union. In Proceedings of the International Virtual Conference on Social Sciences, Colombo, Sri Lanka, 31 July 2020. [Google Scholar] [CrossRef]

- Ragazou, K.; Passas, I.; Sklavos, G. Investigating the Strategic Role of Digital Transformation Path of SMEs in the Era of COVID-19: A Bibliometric Analysis Using R. Sustainability 2022, 14, 11295. [Google Scholar] [CrossRef]

- Zournatzidou, G.; Ragazou, K.; Sklavos, G.; Sariannidis, N. Examining the Impact of Environmental, Social, and Corporate Governance Factors on Long-Term Financial Stability of the European Financial Institutions: Dynamic Panel Data Models with Fixed Effects. Int. J. Financ. Stud. 2025, 13, 3. [Google Scholar] [CrossRef]

- Torres-Salinas, D.; Orduña-Malea, E.; Delgado-Vázquez, Á.; Gorraiz, J.; Arroyo-Machado, W. Foundations of Narrative Bibliometrics. J. Inf. 2024, 18, 101546. [Google Scholar] [CrossRef]

- Li, G.; Zhang, T.; Tsai, C.-Y.; Yao, L.; Lu, Y.; Tang, J. Review of the metaheuristic algorithms in applications: Visual analysis based on bibliometrics. Expert Syst. Appl. 2024, 255, 124857. [Google Scholar] [CrossRef]

- Hassan, W.; Duarte, A.E. Bibliometric analysis: A few suggestions. Curr. Probl. Cardiol. 2024, 49, 102640. [Google Scholar] [CrossRef] [PubMed]

- Guo, D.; Li, L.; Pang, G. Does the integration of digital and real economies promote urban green total factor productivity? Evidence from China. J. Environ. Manag. 2024, 370, 122934. [Google Scholar] [CrossRef] [PubMed]

- Galletta, S.; Mazzù, S.; Naciti, V.; Paltrinieri, A. A PRISMA systematic review of greenwashing in the banking industry: A call for action. Res. Int. Bus. Financ. 2024, 69, 102262. [Google Scholar] [CrossRef]

- Alabi, G. Bradford’s law and its application. Int. Libr. Rev. 1979, 11, 151–158. [Google Scholar] [CrossRef]

- Alvarado, R.U. Growth of Literature on Bradford’s Law. Investig. Bibl. 2016, 30, 51–72. [Google Scholar] [CrossRef]

- Rasoolimanesh, S.M.; Chee, S.Y.; Ragavan, N.A. Tourists’ perceptions of the sustainability of destination, satisfaction, and revisit intention. Tour. Recreat. Res. 2023, 50, 106–125. [Google Scholar] [CrossRef]

- Kumar, S.; Sharma, D.; Rao, S.; Lim, W.M.; Mangla, S.K. Past, present, and future of sustainable finance: Insights from big data analytics through machine learning of scholarly research. Ann. Oper. Res. 2021, 345, 1061–1104. [Google Scholar] [CrossRef]

- Zhang, D. Are firms motivated to greenwash by financial constraints? Evidence from global firms’ data. J. Int. Financ. Manag. Account. 2022, 33, 459–479. [Google Scholar] [CrossRef]

- McPherson, E.G. Accounting for benefits and costs of urban greenspace. Landsc. Urban Plan. 1992, 22, 41–51. [Google Scholar] [CrossRef]

- Hickmann, T. Locating Cities and Their Governments in Multi-Level Sustainability Governance. Politics Gov. 2021, 9, 211–220. [Google Scholar] [CrossRef]

- Fiorino, D.J. Sustainable cities and governance: What are the connections? In Elgar Companion to Sustainable Cities; Edward Elgar Publishing: Chechentenham, UK, 2014; pp. 413–433. [Google Scholar]

- Guo, Z.; He, Y. ESG and Urban Sustainable Development. Trans. Econ. Bus. Manag. Res. 2024, 5, 250–265. [Google Scholar] [CrossRef]

- Howard, K.W.F. Sustainable cities and the groundwater governance challenge. Environ. Earth Sci. 2014, 73, 2543–2554. [Google Scholar] [CrossRef]

- Evans, B.; Joas, M.; Sundback, S.; Theobald, K. Governing Sustainable Cities; Routledge: Abingdon, UK, 2013; pp. 1–146. [Google Scholar]

- May, T.; Marvin, S. The future of sustainable cities: Governance, policy and knowledge. Local Environ. 2017, 22, 1–7. [Google Scholar] [CrossRef]

- Alvarez-Risco, A.; Del-Aguila-Arcentales, S.; Rosen, M.A. Sustainable development goals and cities. In Building Sustainable Cities; Springer: Cham, Switzerland, 2020; pp. 313–330. [Google Scholar] [CrossRef]

- Conke, L.S.; Ferreira, T.L. Urban metabolism: Measuring the city’s contribution to sustainable development. Environ. Pollut. 2015, 202, 146–152. [Google Scholar] [CrossRef]

- Jaczewska, J.; Tarkowski, M.; Puzdrakiewicz, K.; Połom, M. Urban densification and sustainable mobility in a post-socialist city. Reconstruction of the science and business district development in Gdańsk. Cities 2022, 127, 103739. [Google Scholar] [CrossRef]

| Study | Focus Area | Methodology | Scope | Key Contribution |

|---|---|---|---|---|

| Rasoolimanesh et al. (2023) | Sustainable tourism and SDGs | PRISMA + Thematic Review | 2010–2022 | Identifies sustainability indicators for tourism governance |

| Kumar et al. (2022) | Sustainable finance | Machine Learning + Bibliometric Analysis | 2000–2021 | Explores ESG–finance links using big data and clustering |

| Galletta et al. (2024) | Greenwashing in banking | PRISMA + SLR | 2000–2023 | Maps risks and controversies around ESG misreporting |

| This study | ESG, green accounting, urban governance | PRISMA + Biblioshiny + VOSviewer | 2014–2025 | First integrated mapping of ESG and accounting in sustainable urbanism |

| Description | Results |

|---|---|

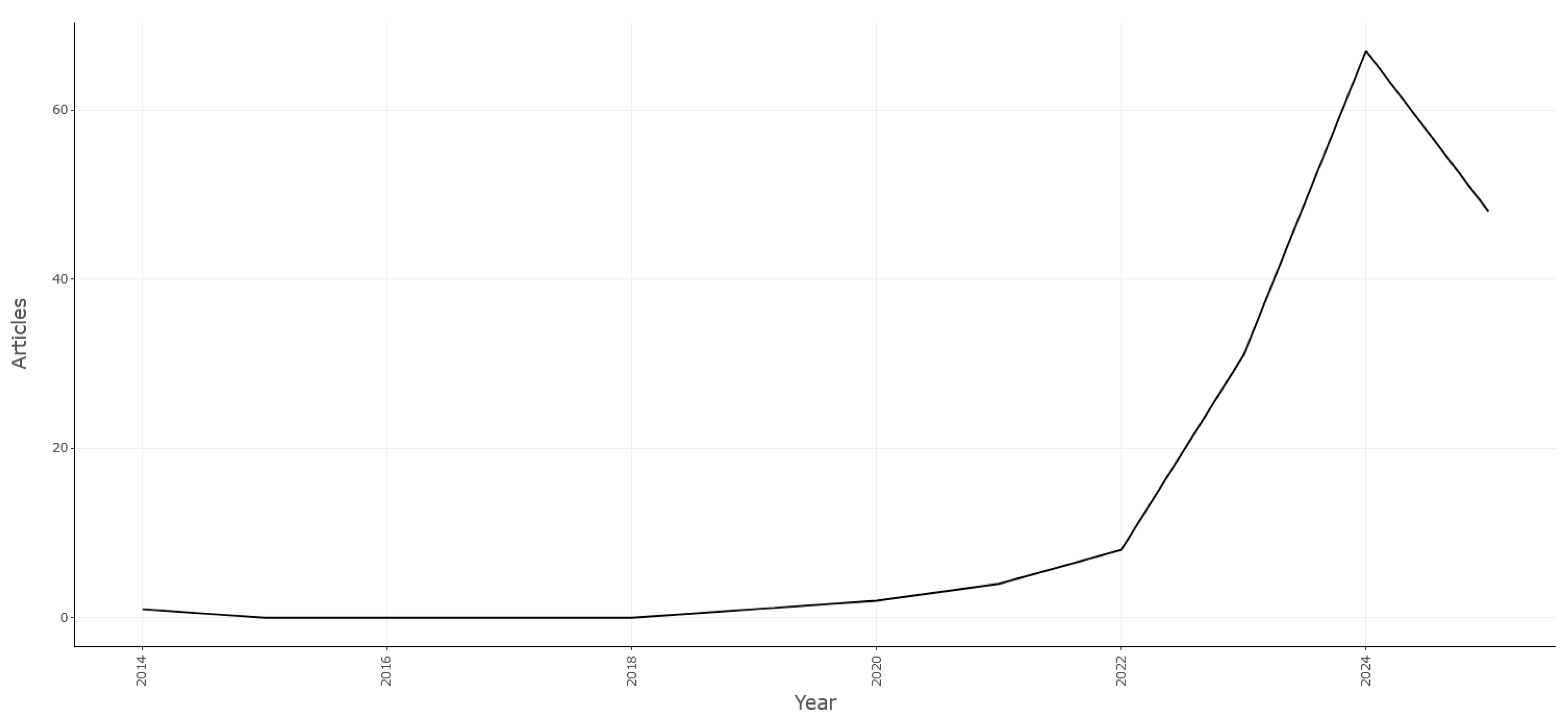

| Timespan | 2014–2025 |

| Total Documents | 130 |

| Sources (Journals, Books, etc.) | 99 |

| Annual Growth Rate (%) | 42.18% |

| Document Average Age | 1.21 years |

| Average Citations per Document | 10.86 |

| Total References | 16,835 |

| Author Keywords (DE) | 561 |

| Keywords Plus (ID) | 460 |

| Total Authors | 499 |

| Single-Authored Documents | 13 |

| Authors of Single-Authored Docs | 12 |

| Average Co-Authors per Document | 3.36 |

| International Co-Authorship (%) | 35.19% |

| Document Types | Articles (114), Reviews (19), Books (13), Chapters (12), Conference Papers (4) |

| Paper | Journal | Total Citations | TC/Year | Normalized TC |

|---|---|---|---|---|

| A systematic scoping review of sustainable tourism indicators in relation to sustainable development goals | Journal of Sustainable Tourism | 351 | 117 | 15.26 |

| Past, present, and future of sustainable finance: insights from big data analytics through machine learning of scholarly research | Annals of Operations Research | 172 | 172 | 39.13 |

| The Social Dimensions of Corporate Sustainability: An Integrative Framework Including COVID-19 Insights | Sustainability | 90 | 15 | 1.62 |

| Navigating Sustainability: Unveiling the Interconnected Dynamics of ESG factors and SDGs in BRICS-11 | Sustainable Development | 69 | 34.5 | 12.53 |

| Sustainability reporting in smart cities: Multidimensional performance measures | Cities | 49 | 9.8 | 1.92 |

| Author | Articles | Fractionalized Contribution |

|---|---|---|

| Kumar S | 3 | 0.73 |

| Paridhi | 3 | 0.87 |

| Saini N | 3 | 0.87 |

| Lee S | 3 | 0.67 |

| Wang G | 3 | 0.60 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sklavos, G.; Zournatzidou, G.; Ragazou, K.; Spinthiropoulos, K.; Sariannidis, N. Next-Generation Urbanism: ESG Strategies, Green Accounting, and the Future of Sustainable City Governance—A PRISMA-Guided Bibliometric Analysis. Urban Sci. 2025, 9, 261. https://doi.org/10.3390/urbansci9070261

Sklavos G, Zournatzidou G, Ragazou K, Spinthiropoulos K, Sariannidis N. Next-Generation Urbanism: ESG Strategies, Green Accounting, and the Future of Sustainable City Governance—A PRISMA-Guided Bibliometric Analysis. Urban Science. 2025; 9(7):261. https://doi.org/10.3390/urbansci9070261

Chicago/Turabian StyleSklavos, George, Georgia Zournatzidou, Konstantina Ragazou, Konstantinos Spinthiropoulos, and Nikolaos Sariannidis. 2025. "Next-Generation Urbanism: ESG Strategies, Green Accounting, and the Future of Sustainable City Governance—A PRISMA-Guided Bibliometric Analysis" Urban Science 9, no. 7: 261. https://doi.org/10.3390/urbansci9070261

APA StyleSklavos, G., Zournatzidou, G., Ragazou, K., Spinthiropoulos, K., & Sariannidis, N. (2025). Next-Generation Urbanism: ESG Strategies, Green Accounting, and the Future of Sustainable City Governance—A PRISMA-Guided Bibliometric Analysis. Urban Science, 9(7), 261. https://doi.org/10.3390/urbansci9070261