Offset-Free Economic MPC Based on Modifier Adaptation: Investigation of Several Gradient-Estimation Techniques

Abstract

1. Introduction

2. Preliminaries

2.1. Plant and Cost Specifications

2.2. Nominal and Augmented Models

2.3. State and Disturbance Estimation

2.4. Output Modifiers

2.5. Target Calculation with Modifiers

2.6. Economic MPC with Modifiers

3. Gradient or Modifier Estimation

3.1. Basic Idea

3.2. Plant Gradient Estimation

3.2.1. Broyden’s Update for Plant Gradient Estimation

3.2.2. Linear Regression for Plant Gradient Estimation

3.3. Modifier Estimation

3.3.1. Broyden’s Update for Modifier Estimation

3.3.2. Linear Regression for Modifier Estimation

3.4. Role of Disturbance Model

3.4.1. Plant Gradient Estimation

- Using a linear disturbance model, as in (9), implies an equivalence between the nominal and augmented models for computing , as in (31), since the disturbances d would not appear in any of the derivatives involved, that is, , and . Hence, the disturbance variables are not involved in the gradient calculation.

- In contrast, using a nonlinear disturbance model, it would not be possible to discard the disturbance variables when calculating gradients. Moreover, a nonlinear disturbance model may be more challenging to implement; however, if implemented correctly, the first-order modifier terms might become superfluous (see [11] for an example).

3.4.2. Modifier Estimation

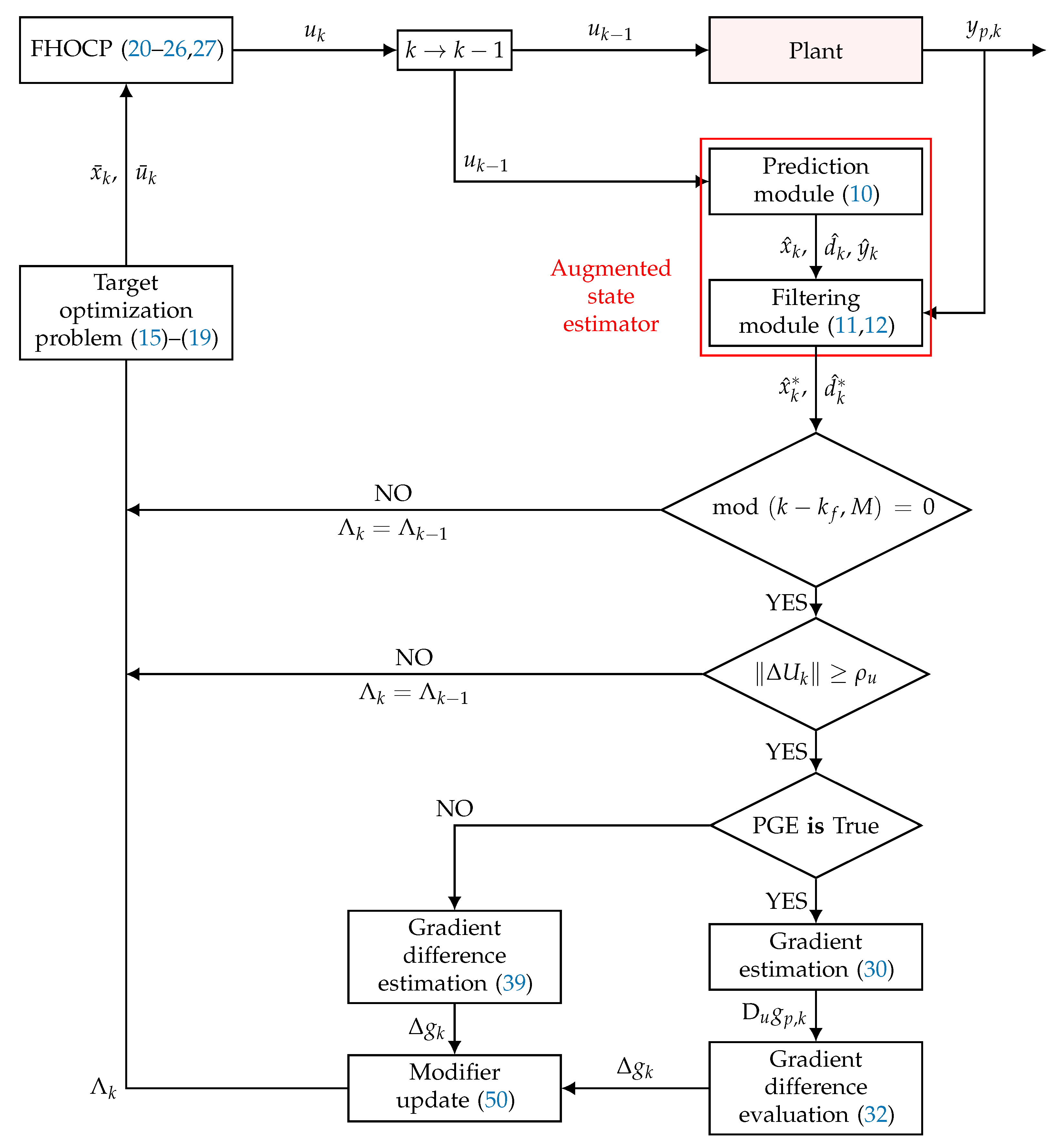

4. Offset-Free Economic MPC Algorithms

4.1. Algorithm Initialization

4.2. OF-eMPC Algorithm Using Broyden’s Update

| Algorithm 1 Offset-free eMPC algorithm using Broyden’s update. |

|

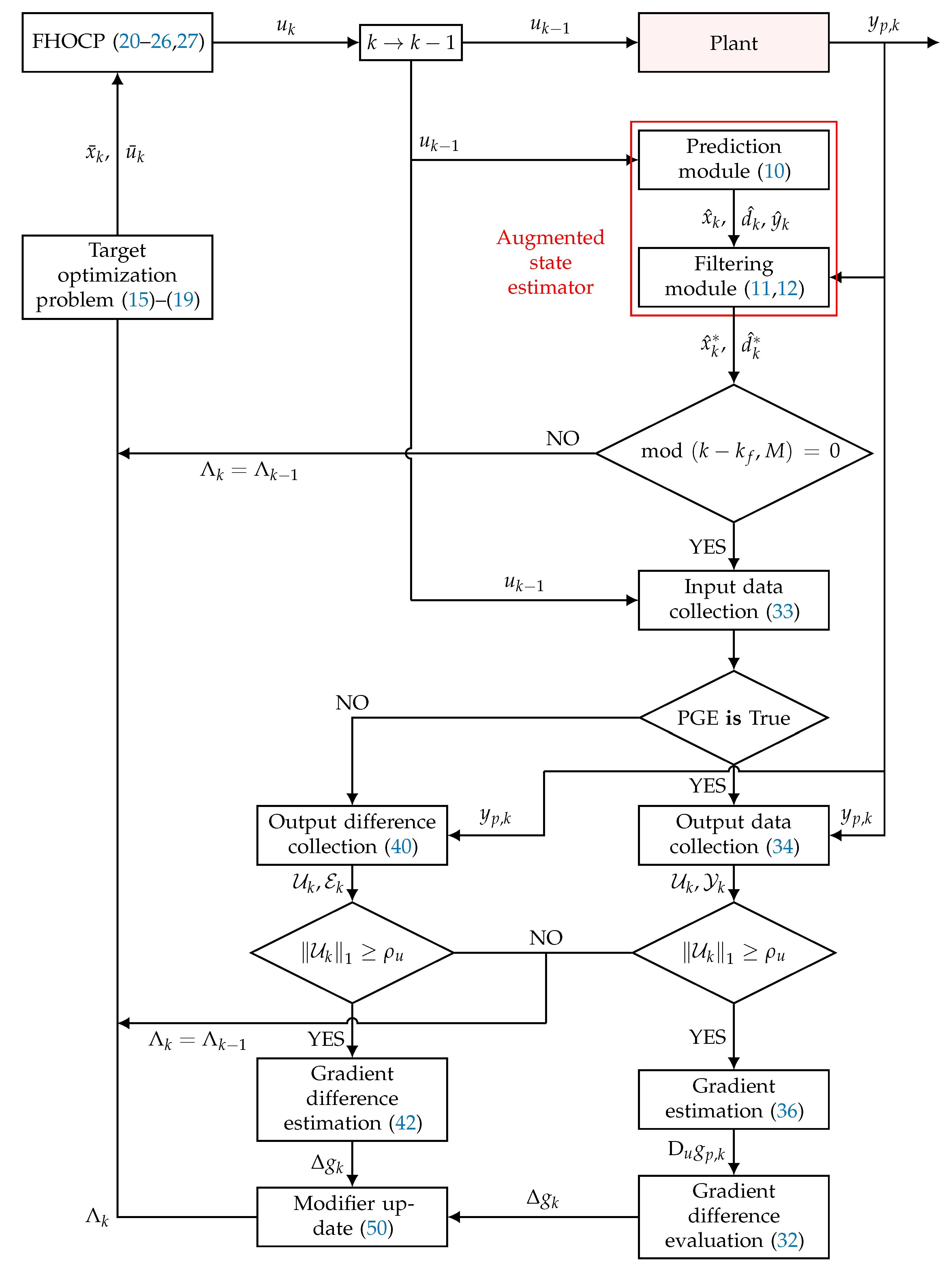

4.3. OF-eMPC Algorithm Using Linear Regression

| Algorithm 2 Offset-free eMPC algorithm using linear regression |

|

4.4. Ill-Conditioning

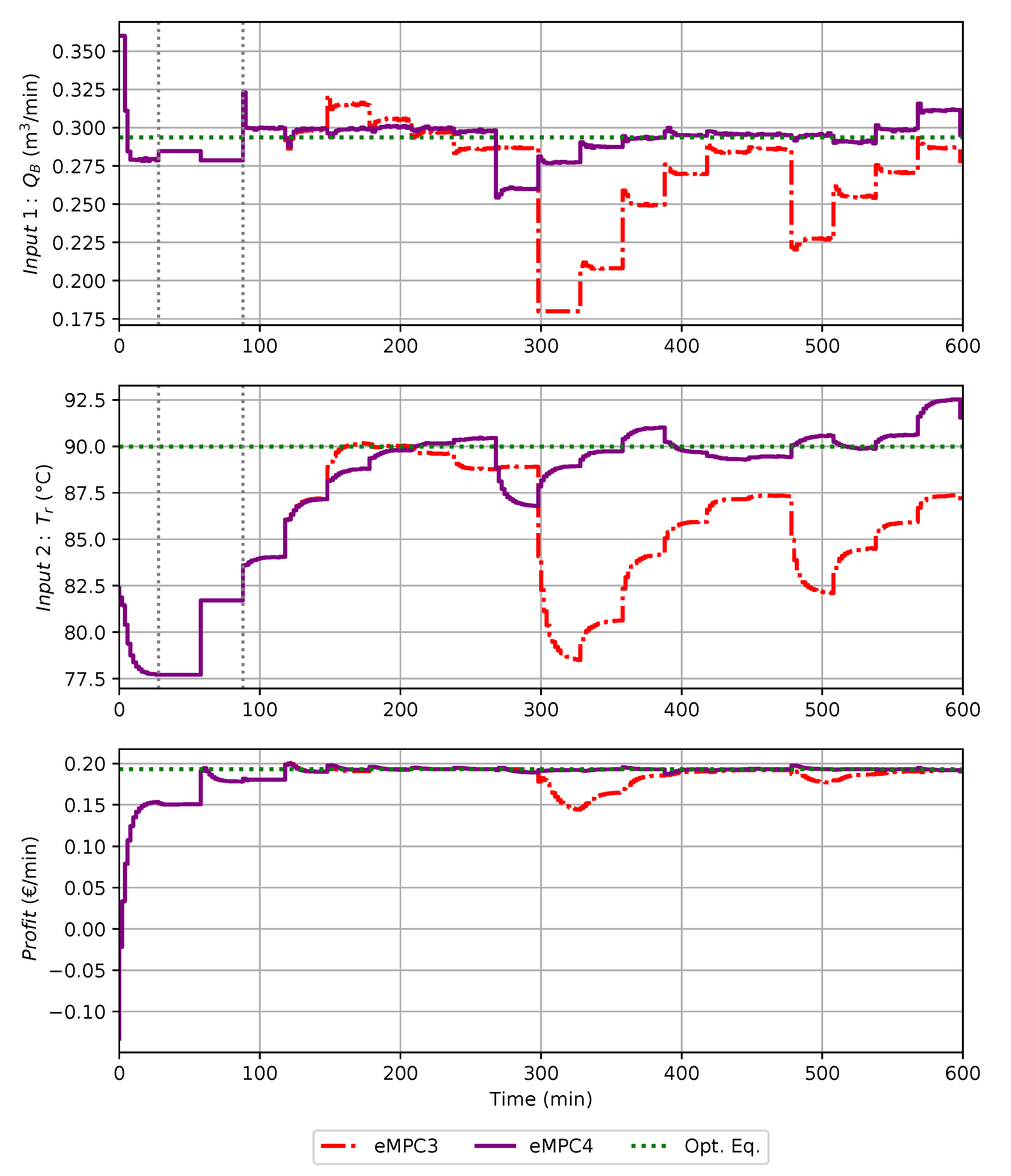

5. Simulation Results

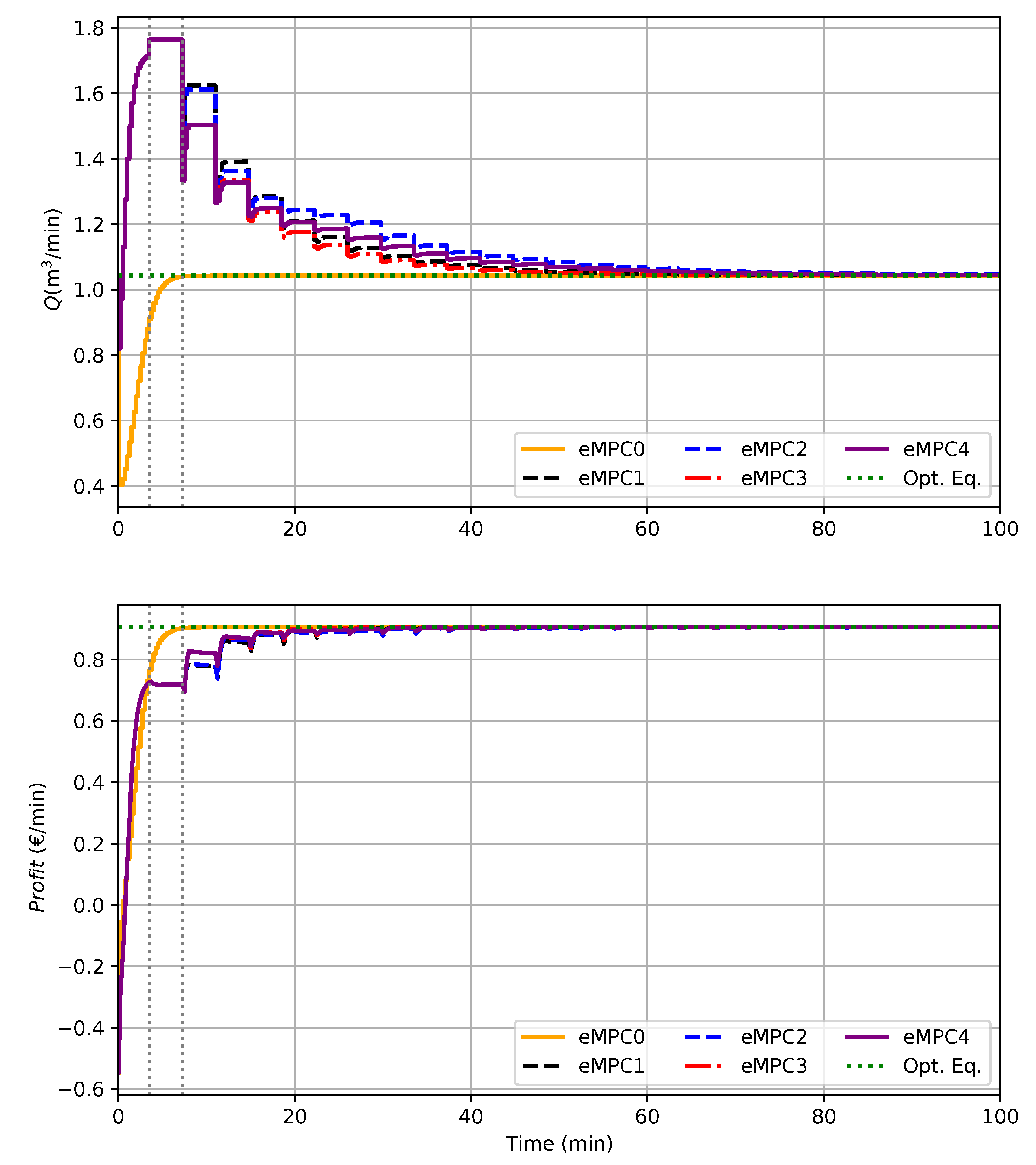

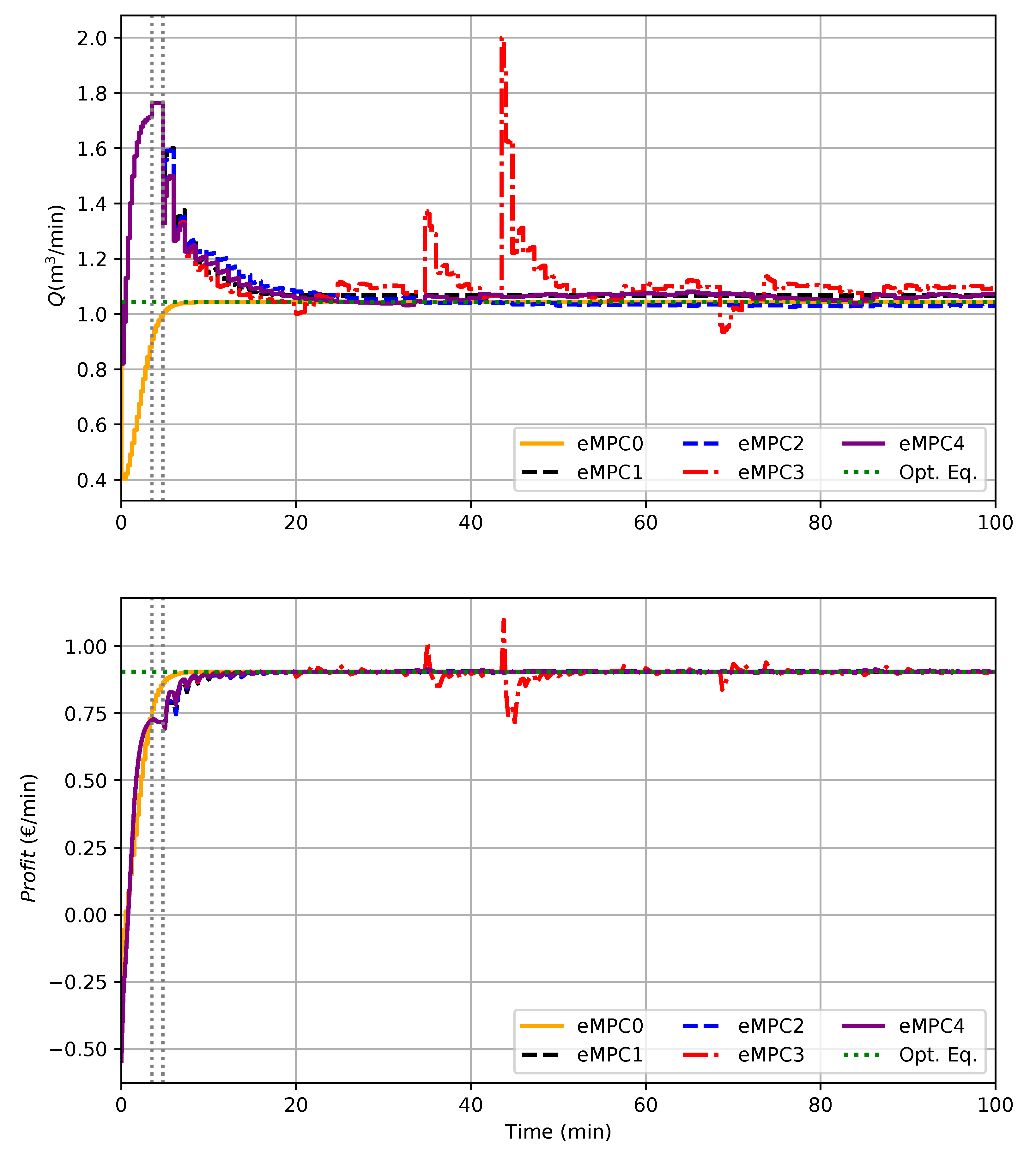

- eMPC0 assumes the plant gradients to be perfectly known, i.e., . This controller is not practically implementable but is used as reference.

- eMPC1 uses the Broyden’s gradient update described in Section 3.2.1.

- eMPC2 estimates the plant gradient using linear regression as per Section 3.2.2. The number of data points in the regression is .

- eMPC3 uses the Broyden’s modifier update described in Section 3.3.1.

- eMPC4 estimates the modifiers using linear regression as per Section 3.3.2. The number of data points in the regression is also .

5.1. CSTR with Competitive Reactions

5.1.1. Model

5.1.2. Reactor Performance

5.2. Williams–Otto Reactor

5.2.1. Process

5.2.2. Model

5.2.3. Reactor Optimization

5.3. Final Considerations

- Estimate the plant gradients from measurements, compute the model gradients “analytically” from the model, and evaluate the modifiers as their differences, as per Section 3.2. This approach is very sensitive to truncation errors, as these errors affect the estimation of plant gradients but not of model gradients.

- Estimate the plant gradients from measurements, estimate the model gradients from the model using the same numerical scheme, and evaluate the modifiers as their differences. This is equivalent to estimating the modifiers directly from measurements (see Section 3.3). In this case, the truncation errors tend to cancel out upon computing the differences between plant and model gradients.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Rawlings, J.B.; Angeli, D.; Bates, C.N. Fundamentals of economic model predictive control. In Proceedings of the 51st IEEE Conference on Decision and Control, Maui, HI, USA, 10–13 December 2012; pp. 3851–3861. [Google Scholar]

- Morari, M.; Arkun, Y.; Stephanopoulos, G. Studies in the synthesis of control structures for chemical processes: Part I: Formulation of the problem. Process decomposition and the classification of the control tasks. Analysis of the optimizing control structures. AIChE J. 1980, 26, 220–232. [Google Scholar] [CrossRef]

- Engell, S. Feedback control for optimal process operation. J. Process Control 2007, 17, 203–219. [Google Scholar] [CrossRef]

- Ellis, M.; Christofides, P.D. On finite-time and infinite-time cost improvement of economic model predictive control for nonlinear systems. Automatica 2014, 50, 2561–2569. [Google Scholar] [CrossRef]

- Pannocchia, G.; Rawlings, J.B. Disturbance models for offset-free model-predictive control. AIChE J. 2003, 49, 426–437. [Google Scholar] [CrossRef]

- Muske, K.R.; Badgwell, T.A. Disturbance modeling for offset-free linear model predictive control. J. Process Control 2002, 12, 617–632. [Google Scholar] [CrossRef]

- Pannocchia, G. Offset-free tracking MPC: A tutorial review and comparison of different formulations. In Proceedings of the European Control Conference, Linz, Austria, 15–17 July 2015; pp. 527–532. [Google Scholar]

- Marchetti, A.G.; Chachuat, B.; Bonvin, D. Modifier-adaptation methodology for real-time optimization. Ind. Eng. Chem. Res. 2009, 48, 6022–6033. [Google Scholar] [CrossRef]

- Marchetti, A.G.; Chachuat, B.; Bonvin, D. A dual modifier-adaptation approach for real-time optimization. J. Process Control 2010, 20, 1027–1037. [Google Scholar] [CrossRef]

- Marchetti, A.; François, G.; Faulwasser, T.; Bonvin, D. Modifier adaptation for real-time optimization—Methods and applications. Processes 2016, 4, 55. [Google Scholar] [CrossRef]

- Vaccari, M.; Pannocchia, G. A Modifier-Adaptation Strategy towards Offset-Free Economic MPC. Processes 2016, 5, 2. [Google Scholar] [CrossRef]

- Faulwasser, T.; Pannocchia, G. Towards a unifying framework blending RTO and economic MPC. Ind. Eng. Chem. Res. 2019, 58, 13583–13598. [Google Scholar] [CrossRef]

- Vergara-Diertrich, J.; Ferramosca, A.; Mirasierra, V.; Normey-Rico, J.E.; Limon, D. A Modifier-Adaptation Approach to the One-Layer Economic MPC. IFAC-PapersOnLine 2020, 53, 6957–6962. [Google Scholar] [CrossRef]

- Papasavvas, A.; de Avila Ferreira, T.; Marchetti, A.G.; Bonvin, D. Analysis of output modifier adaptation for real-time optimization. Comput. Chem. Eng. 2019, 121, 285–293. [Google Scholar] [CrossRef]

- Marchetti, A.G.; Faulwasser, T.; Bonvin, D. A feasible-side globally convergent modifier-adaptation scheme. J. Process Control 2017, 54, 38–46. [Google Scholar] [CrossRef]

- Schneider, R.; Milosavljevic, P.; Bonvin, D. Accelerated and adaptive modifier-adaptation schemes for the real-time optimization of uncertain systems. J. Process Control 2019, 83, 129–135. [Google Scholar] [CrossRef]

- Mirasierra, V.; Vergara-Diertrich, J.; Limon, D. Real-Time Optimization of Periodic Systems: A Modifier-Adaptation Approach. IFAC-PapersOnLine 2020, 53, 1690–1695. [Google Scholar] [CrossRef]

- Papasavvas, A.; Francois, G. Internal Modifier Adaptation for the Optimization of Large-Scale Plants with Inaccurate Models. Ind. Eng. Chem. Res. 2019, 58, 13568–13582. [Google Scholar] [CrossRef]

- Gao, W.; Wenzel, S.; Engell, S. Modifier adaptation with quadratic approximation in iterative optimizing control. In Proceedings of the European Control Conference, Linz, Austria, 15–17 July 2015; pp. 2527–2532. [Google Scholar]

- Costello, S.; François, G.; Bonvin, D. A Directional Modifier-Adaptation Algorithm for Real-Time Optimization. J. Process Control 2016, 39, 64–76. [Google Scholar] [CrossRef]

- Pannocchia, G. An economic MPC formulation with offset-free asymptotic performance. IFAC-PapersOnLine 2018, 51, 393–398. [Google Scholar] [CrossRef]

- François, G.; Bonvin, D. Use of transient measurements for the optimization of steady-state performance via modifier adaptation. Ind. Eng. Chem. Res. 2013, 53, 5148–5159. [Google Scholar] [CrossRef]

- de Avila Ferreira, T.; François, G.; Marchetti, A.G.; Bonvin, D. Use of transient measurements for static real-time optimization. IFAC-PapersOnLine 2017, 50, 5737–5742. [Google Scholar] [CrossRef]

- Hernández, R.; Engell, S. Economics Optimizing Control with Model Mismatch Based on Modifier Adaptation. IFAC-PapersOnLine 2019, 52, 46–51. [Google Scholar] [CrossRef]

- Vaccari, M.; Pannocchia, G. Implementation of an economic MPC with robustly optimal steady-state behavior. IFAC-PapersOnLine 2018, 51, 92–97. [Google Scholar] [CrossRef]

- Singhal, M.; Marchetti, A.G.; Faulwasser, T.; Bonvin, D. Active directional modifier adaptation for real-time optimization. Comput. Chem. Eng. 2018, 115, 246–261. [Google Scholar] [CrossRef]

- Marchetti, A.; de Avila Ferreira, T.; Costello, S.; Bonvin, D. Modifier adaptation as a feedback control scheme. Ind. Eng. Chem. Res. 2020, 59, 2261–2274. [Google Scholar] [CrossRef]

- Singhal, M.; Marchetti, A.G.; Faulwasser, T.; Bonvin, D. A note on efficient computation of privileged directions in modifier adaptation. Comput. Chem. Eng. 2020, 132, 106524. [Google Scholar] [CrossRef]

- Jeong, D.H.; Lee, C.J.; Lee, J.M. Experimental gradient estimation of multivariable systems with correlation by various regression methods and its application to modifier adaptation. J. Process Control 2018, 70, 65–79. [Google Scholar] [CrossRef]

- Navia, D.; Briceño, L.; Gutiérrez, G.; De Prada, C. Modifier-Adaptation Methodology for Real-Time Optimization Reformulated as a Nested Optimization Problem. Ind. Eng. Chem. Res. 2015, 54, 12054–12071. [Google Scholar] [CrossRef]

- Oliveira-Silva, E.; de Prada, C.; Navia, D. Dynamic optimization integrating modifier adaptation using transient measurements. Comput. Chem. Eng. 2021, 149, 107282. [Google Scholar] [CrossRef]

- Vaccari, M.; Pelagagge, F.; Dominique, B.; Pannocchia, G. Estimation technique for offset-free economic MPC based on modifier adaptation. IFAC-PapersOnLine 2020, 53, 11251–11256. [Google Scholar] [CrossRef]

- Maeder, U.; Borrelli, F.; Morari, M. Linear offset-free model predictive control. Automatica 2009, 45, 2214–2222. [Google Scholar] [CrossRef]

- Morari, M.; Maeder, U. Nonlinear offset-free model predictive control. Automatica 2012, 48, 2059–2067. [Google Scholar] [CrossRef]

- Pannocchia, G.; Gabiccini, M.; Artoni, A. Offset-free MPC explained: Novelties, subtleties, and applications. IFAC-PapersOnLine 2015, 48, 342–351. [Google Scholar] [CrossRef]

- Rawlings, J.B.; Allan, D.A. Moving horizon estimation. Encycl. Syst. Control 2020, 1–7. [Google Scholar] [CrossRef]

- Angeli, D.; Amrit, R.; Rawlings, J.B. On average performance and stability of economic model predictive control. IEEE Trans. Autom. Control 2012, 57, 1615–1626. [Google Scholar] [CrossRef]

- Vaccari, M.; Pannocchia, G. A performance monitoring algorithm for sustained optimal operation with economic MPC. In Proceedings of the 2019 18th European Control Conference (ECC), Naples, Italy, 25–28 June 2019; pp. 3353–3358. [Google Scholar]

- Roberts, P.D. Broyden derivative approximation in ISOPE optimising and optimal control algorithms. In Proceedings of the 11th IFAC Workshop on Control Applications of Optimisation, Saint Petersburg, Russia, 3–6 July 2000; pp. 283–288. [Google Scholar]

- Rodger, E.A.; Chachuat, B. Design methodology of modifier adaptation for on-line optimization of uncertain processes. In Proceedings of the IFAC World Congress, Milan, Italy, 28 August–2 September 2011; pp. 4113–4118. [Google Scholar]

- Dennis, J.E., Jr.; Schnabel, R.B. Numerical Methods for Unconstrained Optimization and Nonlinear Equations; SIAM: Philadelphia, PA, USA, 1996; Volume 16. [Google Scholar]

- Kelley, C.T. Iterative Methods for Optimization; SIAM: Philadelphia, PA, USA, 1999. [Google Scholar]

- Marchetti, A.G. A new dual modifier-adaptation approach for iterative process optimization with inaccurate models. Comput. Chem. Eng. 2013, 59, 89–100. [Google Scholar] [CrossRef]

- Williams, T.J.; Otto, R.E. A generalized chemical processing model for the investigation of computer control. Trans. Am. Inst. Electr. Eng. Part I Commun. Electron. 1960, 79, 458–473. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Value | Unit |

|---|---|---|

| 11,111 | ||

| 10 | ||

| 10 | ||

| V | ||

| Parameter | Value | Unit |

|---|---|---|

| 12,438.5 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vaccari, M.; Bonvin, D.; Pelagagge, F.; Pannocchia, G. Offset-Free Economic MPC Based on Modifier Adaptation: Investigation of Several Gradient-Estimation Techniques. Processes 2021, 9, 901. https://doi.org/10.3390/pr9050901

Vaccari M, Bonvin D, Pelagagge F, Pannocchia G. Offset-Free Economic MPC Based on Modifier Adaptation: Investigation of Several Gradient-Estimation Techniques. Processes. 2021; 9(5):901. https://doi.org/10.3390/pr9050901

Chicago/Turabian StyleVaccari, Marco, Dominique Bonvin, Federico Pelagagge, and Gabriele Pannocchia. 2021. "Offset-Free Economic MPC Based on Modifier Adaptation: Investigation of Several Gradient-Estimation Techniques" Processes 9, no. 5: 901. https://doi.org/10.3390/pr9050901

APA StyleVaccari, M., Bonvin, D., Pelagagge, F., & Pannocchia, G. (2021). Offset-Free Economic MPC Based on Modifier Adaptation: Investigation of Several Gradient-Estimation Techniques. Processes, 9(5), 901. https://doi.org/10.3390/pr9050901