Abstract

Recent research suggests that one of the main motivations for mergers and acquisitions is the attempt to acquire companies to incorporate intangible assets. Such assets provide important sources of sustainable competitive advantages and opportunities for growth. This article analyzes the strategies of engineering companies, as well as value creation in acquisition events of multinational companies, by using the study of the events method, providing an innovative way to be applied to this phenomenon. This method is used in our research to study the influence of the announcement of acquisitions on the abnormal accumulated returns of the acquiring companies, and is allowed to confirm that influence. In general, the average accumulated returns were positive and statistically significant in the three windows of the method, according to the significance tests used. The results validate the hypothesis that the events generate synergy gains for market players, emphasizing the importance of growth via acquisitions for the sector under analysis.

1. Introduction

Contemporary literature suggests that investment decisions are made based on several different reasons. One of the main reasons is the prospect of business growth. If a company decides to expand or diversify, there are two possible paths: internal growth or mergers and acquisitions (M&A). According to Singh and Montgomery [1], the process of internal growth takes more time and can be more costly than buying an already established business. Several different advantages can be attributed to growth through mergers and acquisitions. Regardless of the form chosen, the objectives of this growth process must be related to shareholder value creation, by increasing the company’s competitiveness.

Concerning the increasing competitiveness and synergy gains, it is very common to deal with intangible assets. After all, these assets provide their owners with important sources of differentiation and, therefore, a sustainable competitive advantage. Considering that, there are indications that incorporating companies is currently one of the main motivations for carrying out mergers and acquisitions.

Accordingly, it seems relevant to try to answer the following research problem: what is the relationship between the acquisition of companies and the creation of value and synergy gains for the acquiring company in a merger and acquisition’s event? In our paper, we answer this question by applying a model, innovative on its purposes of getting results for this research problem.

This article’s main purpose is to understand how consulting engineering companies develop their growth strategies in a complex and competitive global environment. This theme is particularly relevant from the perspective of a case study, by analyzing the evolution of the market share of the five largest companies in the world in consulting engineering and project management, and how it has expanded in the competitive market. The considered methodology allows obtaining very significant and robust results for the collected data. There is an increasingly common trend in globalization—that mergers and acquisitions by large companies, in various market segments, are becoming more common; this is due to a variety of reasons:, e.g., the expansion of company market shares, and the intention to expand and diversify the supply of services in a particular sector of the economy.

In general, the process of merger and acquisition is directly related to the increase in the market value of the company and, hence, to its profitability and strengthening of its capital structure. Thus, as it is a process of great impact to the largest companies, the approach of how incorporations and mergers contribute to the growth of company market values is particularly important.

This article aims to contribute toward filling the gaps in the research, on how consulting engineering companies develop their growth strategies in a complex and competitive global environment. Initially we presented the theoretical bases that grounded our research in all its stages, and then we explained our methodological option, which represents a strong add value in the analysis of such a phenomenon. To Triviños [2], the theoretical basis is indispensable, because it offers the researcher the possibility of understanding, explaining, and assigning meanings to the investigated fact, and avoids the formulation of personal opinions that do not have scientific support.

Our goal is to analyze if consulting engineering companies present different standards of value creation. To achieve this goal, an event study has been developed that seeks to verify the influence of M&A news on the accumulated abnormal returns and growth of these companies within their home countries, as well as abroad with cross-border operations (Bednarczyk et al. [3]. The event study is complemented by a significance test on the sample of cumulative abnormal returns to test the hypothesis that these accumulated returns are significantly different. The results suggest—unlike other empirical research—that merger and acquisition operations can be important tools for capturing synergy gains and creating value for consulting engineering firms.

According to Arikan [4], among all assets, intangibles are the greatest sources of sustainable competitive advantages, since they are more difficult to accumulate and take longer to do so. This author also states that activities of mergers and acquisitions serve as important mechanisms of accumulation of intangible assets for the acquiring companies. This opinion is shared by Gupta and Roos [5], who state that intangible resources are increasingly the main motivation for mergers and acquisitions among companies.

According to Weston et al. [6], most of the M&A movements (or waves) implemented in the United States occurred when the U.S. economy was experiencing high growth rates. In this context, the companies involved were looking for new investment opportunities, optimization of production processes, technological innovations, and efficiency in resource allocation. The first wave, covering the period from 1895 to 1904, consisted typically of horizontal merger and acquisition movements that had, as a practical result, a high concentration in various economic segments. The second wave began in 1922 and ended with the economic crisis of 1929. During this period, the processes of mergers and acquisitions were emphasized by the increase of innovations in the industries of transportation (motor vehicles), communication (domestic radios), and mass marketing (Markham and Stocking and Weston et al. [6]. In the 1960s, the third wave of mergers and acquisitions occurred. The horizontal operations of the early century and vertical operations of the 1920s gave rise to conglomerate mergers and acquisitions, according to Weston et al. [6]. The fourth wave occurred in the 1980s and had, as its main motivation, the increase of interest in publicly traded companies. Weston et al. [6] describe the existence of a confluence of forces: economic growth, including capital markets and increased international competition. For Weston et al. ([6], p. 194), the following wave comprised the 1990s. The economic recovery brought a new movement of acquisitions. In this period, the main motivations were technological changes (fiber optic and microwave communication and a significant increase in internet use), growth in global competition, deregulation of several markets, and macroeconomic and microeconomic changes. Gaughan [7] says that this new wave of mergers and acquisitions is motivated much more by strategic issues than by rapid financial gains. In addition, in contrast to the previous wave, most acquisitions are carried out with the use of equity capital. This was a strategy of consulting engineering companies.

The main reasons that lead companies to adopt a strategy of mergers and acquisitions are based on the firm’s theory. For Coase [8], the emergence of firms in an economy regulated by price mechanisms is related to maximizing the allocation of resources directly by the entrepreneur in a less costly way than in the market. Based on these premises, the size of companies would be limited, by not only transaction costs, but also administrative costs and the ability to manage the company. It becomes cheaper to acquire a product or service in the market than to invest to produce it.

In this article, when we analyze mergers and acquisitions within an event study approach, we have two main goals:

- (a)

- Investigating the influence of M&A strategies on the value market of the five largest engineering consulting of the world.

- (b)

- Identifying if the synthetic control method (SCM) (Abadie et al. [9]) constitutes a good metric to the analysis of M&A, by studying the events approach. Our approach contributes to the literature in at least two main respects. First, unlike existing literature that usually explores different event windows to check the robustness of the event studies analyses of M&A (Weston et al.; Hannan et al.; MacKinlay; Moeller et al. [6,10,11,12], we use SCM as a powerful alternative approach to the return market model MacKinlay [11]. Billmeier and Nannicini [13] highlight the transparent measurement of the counterfactual outcome of the treated unit as a great advantage of this method. To the best of our knowledge, Castro-Iragorri [14] was the first to address SCM on event studies literature. Within the SCM, we explore whether the M&A in time (T) leads to higher-growth on the stock return in the event window (T − i; T + i), compared to similar stocks that did not made M&A.

Our evidence finds similar impacts of the M&A strategies in both methods, highlighting the value of SCM as an instrument tool on M&A analysis. Second, our results show that acquires perform strong abnormal return in the M&A event window. This analysis is important toward understanding the role played by M&A in market value creation to firms. Moreover, we use a firm-level analysis; the focus on the biggest companies minimizes the bias of heterogeneity in the sample of events. The empirical results also reveal that the abnormal market return observed is at the upper limit established by the literature (Weston, Siu and Johnson, 2001) [6]. We believe that this evidence is related to the firm characteristics of acquires, which have a high degree of intangibility, intensive spends of R&D, and cross-border activities. All of them are important issues to determine the level of abnormal returns in M&A (Wilcox et al.; Bednarczyk et al. [3,15].

In order to evaluate the hypothesis of synergy gains, resulting from changes in the corporate structure of companies, Mulherin and Brooke [16] modeled acquisitions and diversity decisions based on the theory of events approach. Based on a sample of 1305 U.S. companies listed on Value Line’s Power Industry throughout the 1990s, and after initial cutoffs, 281 acquisition events and 268 divestiture episodes were modeled, based on daily return data from the listed companies. Gains in market value were evidenced after the announcement of both acquisitions and divestitures, indicating that the processes show optimal responses to changes in economic conditions linked to productive specialization (cost structure and synergy gains).

The analysis of event studies is used in Harris [17], to discuss the importance of cross-border acquisitions over foreign direct investment in the US. Several transmission channels are scored as value drivers for both acquirer and acquired firms in international transactions. These include reduction in transaction costs through the market mechanism, greater access to technology transfer, minimization of tariff costs associated with international business (complexity in regulatory policy in different countries), and imperfections in the capital market associated with exchange rate fluctuations (an exchange rate valorization in the currency of the acquiring company increases its bargaining power). The sample included companies acquired between 1970 and 1987, and were listed on the NYSE, considering 1114 domestic M&A and 159 cross-border acquisitions (company headquartered acquired outside the U.S.). The results indicated abnormal market gains for the target companies in cross-border acquisition events. The authors score additional gains in transactions involving R&D intensive firms, suggesting that technology transmission is a crucial factor for the M&A decision in international negotiations.

The technology diffusion element from cross-border acquisitions is also discussed in Bednarczyk et al. [3], from the energy and industry sectors in Central and Eastern Europe (CEE). The cross-border horizontal acquisitions (industry relatedness) reach higher wealth effects for both acquirers and targets firms. The results would be related to synergy gains by increasing efficiency and transfer technology.

In this context, we follow Gopalaswamy et al. [18], modeling the announcement of a merger and or acquisition as the event of analysis, taking the stock price as a regressor to be estimated in the econometric structure. Strong [19] highlights variations greater than a certain expected limit as the abnormal market return, being the same identified within the window of the event.

Sectorial specific analyses are also widely disseminated in the literature. The banking industry, for example, is a recurring theme in the analysis of the study of events. The popularity of this theme was mainly a result of the trend of creating financial conglomerates from the 1980s, in a number of countries, under the justification of reducing service costs and increasing operational flexibility based on economies of scale. Hannan and Wolken [10] conducted a pioneering study of 69 M&A episodes involving U.S.-listed companies, based on the market model, applying an estimation window in the interval between 90 and 16 days before the event announcement. The evidence points to a combined zero net effect to acquiring and acquired firms; the result of an abnormal positive return for shareholders of target banks, and negative for shareholders of bidder banks. Liargovas and Street [20] studied M&A events in the banking sector between 1996 and 2009 for institutions listed on the Athens Stock Exchange (Greece). The authors do not observe cumulative mean abnormal returns for both bidders and target firms. One of the key factors related to the result is the lack of improvement in operational performance as a result of M&As.

Wilcox et al. [15] find evidence that M&A is an important growth strategy (market value) in the U.S. telecommunications industry, being the size of the company and the similarity in activities between the companies involved in the business catalyst—the process of market valuation. The authors attribute the effect to the lower risk involved for these M&A configurations, market consolidation (size), and already recognized expertise in the activity (know-how).

Khanal et al. [21] investigate the effect of M&A on the ethanol-based biofuel industries. The study starts from the hypothesis that M&E processes generate vertical integration (operational costs reduction), market-share gains, and enable the adoption of new technologies (productive specialization) for companies in the sector. Based on the market-adjusted equally weighted index and market-adjusted value-weighted index, the authors report gains in market value from M&A events for companies listed in the United States between 2010 and 2012.

In Table 1, we summarize some major contributions that used the events approach on this topic.

Table 1.

Literature review.

The paper is organized into the following sections: Section 2 presents the methodology for event studies. In Section 3, we present two approaches to the events study model: the market model approach and the synthetic control approach performance. In Section 4, we present an application of the model and the results and the discussion. Finally, Section 5 presents a discussion and our conclusions.

2. Methodology

The methodology of the study of events has been widely disseminated and used in the areas of economics, accounting, and finance. Among the events studied and their implications, we highlight the following two topics, among others: dividend announcements, and mergers and acquisitions. According to MacKinlay [11], the methodology of the study of events is pretty old, and has, over the years, been sophisticated. Moreover, according to MacKinlay [11], the research of Ball and Brown [22] and Fama et al. [23] introduced the methodology that is essentially used today. Brown and Warner [24,25], in their articles from 1980 and 1985, sought, from monthly and daily data of the stock prices of companies, to test the efficiency of several methodologies that were used to measure the performance of the prices of bonds. According to these authors, monthly data offer some advantages over the daily data.

The study of events is a widely used approach to capture market reaction from M&A processes based on stock prices listed on stock exchanges (Figure 1). The model starts from the assumption that the whole set of relevant information is quickly incorporated into the stock price (market efficiency). In this line, variations in the market return of the companies in the short term, soon after the edition of the event, are considered a proxy for the estimation of the gains of synergy and economies of scale, resulting from the productive restructuring of companies through inorganic growth.

Figure 1.

Event Studies Scheme.

In general, the methodology of the study of events involves the following:

- (i)

- Specifying the date of occurrence and the relevant fact: in this study, the event will be the exact date on which the conclusion of the merger and acquisition deal is formally announced.

- (ii)

- Specifying the pre-event and event windows: Mackinlay [11] points out that it is standard in the analysis to build a more extensive event window than just the date , considering that the announcements may have been made after the closing time of the stock market operations, or in the neighboring of non-business days (holidays and/or weekends). Keeping in mind that the market may capture relevant information before the relevant fact is announced, it is necessary to isolate the pre-event window, purging such noises from the estimation of pre-announcement returns.

- (iii)

- Specifying the selection criteria of relevant facts: it is necessary to define a criterion to evaluate only those mergers and acquisitions that were in fact important in market terms for the companies. Such criterion can be summarized by a set of characteristics (representativeness in terms of market share of the acquired company, monetary value of the negotiation, ratio between the size of the target company, and the acquiring company, selection of incorporated companies that were listed on the stock exchange, etc.).

Thus, the step to measure the abnormal market returns (measurement of synergy gains) consists in estimating the market returns of market players (incorporating companies) in the pre-event period (estimation window) and obtaining its sensitivity parameters in relation to the control variables.

Hypothesis 1.

Merger and acquisitions have a positive growth effect in consulting engineering companies.

The event study can be considered a methodology with very well-established properties to identify the effect of the M&A announcement on the market value for the shareholders of the companies involved in a short-term horizon. From a practical point of view, the empirical methodology was formally elaborated by Fama et al. [23], while the refinements later carried out with a view to overlapping violations of statistical hypotheses were summarized by Mackinlay [11]. The basic hypothesis of the event studies approach is that markets operate efficiently, so that the price of assets fully reflects the information availability in the market (Fama [26]).

Concerning the information absorption time, the efficient market hypothesis has three distinct forms: (i) weak form: where all the information contained in past prices is incorporated to current prices; (ii) semi-strong form: where the asset prices incorporate all of the public information available to the general public; (iii) strong form: where the asset prices incorporate all of the information available to at least one investor.

In other words, the efficiency of the markets in any version implies the fast adjustment of the prices of the assets, in front of new, available information that potentially affects the value of the company, being the analysis of short term ideal for the measurement of the gains of the market, resulting from changes in the foundations of the companies.

The conclusion of an M&A transaction is a relevant event that impacts the productive structure of the related companies. To this extent, M&A events containing at least one of the companies listed on the stock exchange must be published for the public. The analysis of this event is theoretically based on the premise of market efficiency in a semi-strong form, a condition under which the event study approach allows for strong inference of the parameters of interest and gains in market value arising from possible synergies in the corporate restructuring process.

The focus of the approach is to measure the cumulative mean abnormal returns in a window around the analyzed event, inferring the potential effect generated by an announcement (Kothari and Warner [27]). Most studies adopt daily data for a more accurate and informative measurement of the impact of the event, being the traditional method for measuring cumulative mean abnormal returns part of a market return model (MacKinlay [11]), estimated in a pre-event window.

Mandelker [28] conducts a pioneering study in the impact analysis of M&A processes from the measurement of cumulative mean abnormal returns. This author used monthly data from all common stocks traded on the New York Stock Exchange (NYSE) between February 1926 and June 1968 for market model estimates, considering as relevant mergers those consummated between November 1941 and August 1962 of NYSE-listed companies with relevant trading periods. The main contribution of this article is the empirical support to the hypothesis of market efficiency, with the prices of the shares involved in the event reflecting the economic gains (economies of scale, synergy, market share) of the acquisition, this being an important starting point for the literature, of the studies of events in the evaluation of M&A.

Hypothesis 2.

The method of Synthetic control strengthens the results observed through the market model.

From a methodological point of view, an important advance in the modeling of the counterfactual return (a measure of normal equity return in the absence of the M&A event) is observed in Castro-Iragorri [14], where the synthetic control method is used (Abadie et al. [9]) to adjust the market model in obtaining a synthetic portfolio. The author makes a comparison with the traditional market approach, observing a good adjustment of the market return model, both in the context of a diversified market index (S&P 500) and in the context of smaller markets (Colombia Index). However, the adoption of the synthetic control approach can be considered as a good robustness exercise for the results observed via the market model, an option that will be adopted in this article.

3. Market Model Approach

The market model was formally elaborated by Fama et al. [23], with important refinements being enhanced by Mackinlay [11]. Assume that the return on company i for the period t is estimated by the market model proposed by Mackinlay:

where is the return observed for the incorporating firm in period t, and the return of the market index m in period t, are the estimated sensitivity parameters, being the price share of the incorporating firm i in period t and a non-correlated error term, with expected value zero and constant variance matrix.

After obtaining the sensitivity parameters in the estimation window, it is necessary to calculate the difference in returns for the incorporating company in the window of events, comparing the market returns ( observed in the interval immediately before and after the event (three windows will be adopted), considering 2, 5, and 10 days before and after the event, respectively) to the counterfactual returns , measured from the interaction between the estimated parameters in the estimation window and the market return observed along the window.

Thus, the abnormal returns are given by:

Moreover, the accumulated abnormal returns along the window of events are given by:

Thus, the global inference test is based on the cumulative average abnormal returns (CAAR) containing all events in the sample. In formal terms, consider the existence of M&A events, then the CAAR is obtained as:

The estimated values for the CAAR passed a significance test in order to test the null hypothesis of the null estimated effect of M&A events on the companies’ market value. In case of rejection, then it is possible to infer the magnitude of the impact of the acquisitions on the average market value of the five largest consulting engineering companies.

4. Synthetic Control Approach

The central objective of the event study approach in our specific problem is to project the evolution of market returns of the companies involved in the business under the hypothesis of the non-existence of the M&A event. To achieve the predetermined objective, it is necessary to estimate the potential results of the companies mentioned along the event window from an appropriate counterfactual.

The market model adopts the temporal behavior of market indices as counterfactual for predicting the normal return associated with companies during the window of events. However, other models were also adopted by the literature in order to allow the comparison of results obtained with those observed by the market model, providing greater robustness in the analysis of the estimated effects. In this case, an alternative proposed by Castro-Iragorri [14] consists of adopting the synthetic control model proposed by Abadie et al. [9].

The method aimed to build the trajectory of the variable of interest (the market return of the companies in the window of events) in case the treatment (M&A event) did not occur. This counterfactual trajectory was obtained from a weighted average based on units of control (other companies that are listed in the same index as the acquiring company) that, theoretically, did not receive the treatment (did not perform M&A in the same period) and were not directly or indirectly affected by the event of interest.

In this context, our goal is to use a portfolio of companies in the control group to model the counterfactual trajectory of the company being treated (acquiring company) and estimate its normal returns during the event window. According to Castro-Iragorri [14], the synthetic portfolio results in a customized market index to project the market returns of the firms affected by the event. The participation of each company in the control group in the customized market index is obtained from the definition of relative weights that minimize the distance between the path of the observed variable of interest and its counterfactual trajectory.

Where is the return of the share of the acquiring company, and the vector with J shares of companies contained in the control group, the construction of the synthetic portfolio is obtained by solving the following optimization problem:

where denotes the estimation window, (where e the relative weight assigned to control unit j in the construction of the synthetic portfolio. Assume that , i.e., the relative weights are constant over time. Note that the impact of the treatment estimated by the synthetic control model is equivalent to the abnormal returns obtained by the market model:

where denotes the window of the event, and the relative weights that minimize the Equation (5)—for more details on the optimization process see Abadie et al. (2010) [9]. Thus, the synthetic control approach provides an alternative representation for abnormal market returns, obtained from a conditioned optimization on a set of shares listed in the local market of the analyzed company. The great theoretical advantage associated with this approach is that the relative weights for the construction of the counterfactual return are obtained by the similarity in the variations of the return of the shares in the control group, in relation to the fluctuations in the return of the company’s shares treated in the pre-treatment period (estimation window), and not by the market capitalization (main metric used to define the relative weights of the companies in a market index, such as the S&P 500), making obtaining of the potential results theoretically more efficient.

The transformation of abnormal returns into average accumulated returns (CAAR) and the hypotheses tests for significance adopted are the same discussed for the market model (Equations (3) and (4)).

5. Empirical Analysis

In this topic, we consider the impact of M&A on the market value of the acquiring companies. The market model and synthetic control model will be used to measure the abnormal returns from the date of the conclusion of the deal.

5.1. Sample

The sample of events consists of 21 M&A announcements made by the five largest consulting engineering companies between 2009 and 2019. We considered, as relevant facts, acquisitions in which the target companies had at least EUR 90 million in revenues in the year prior to the year of the announcement. The cutting point was justified by the high annual revenue of the acquiring companies at the time of the event (more than EUR 1000 billion in all cases). The dates of the events were obtained from companies on annual reports and cross-checked with information from the Crunchbase platform, a site specialized in financial information from private and public companies at the international level.

The closing price data of the five largest consulting engineering companies were obtained from the Yahoo Finance database, from the BatchGetSymbols package in the statistical software R. For the market model, the counterfactual returns were computed based on the stock indices related to the location in each of the acquiring companies that were traded. For the synthetic control model, the counterfactual returns were computed based on the set of the main individual shares that were traded on the stock exchange of the respective acquiring company. For the consulting engineering companies, Jacobs and AECOM were the companies that made up the S&P 500 index in August 2020. In the case of WSP and SNC, the controlling group was composed of the other companies that made up the S&P/TSX in August 2020, and the 100 largest shares that made up the AMX Composite Index in August 2020 formed the controlling group associated with Arcadis.

Table A1 (Appendix A) reports the main details related to the 21 events analyzed, discussing the extension of the estimation window adopted for calculating the coefficients associated with the market model and determining the relative weight of the individual shares of the respective control groups in the construction of the counterfactual return via synthetic control.

5.2. Results

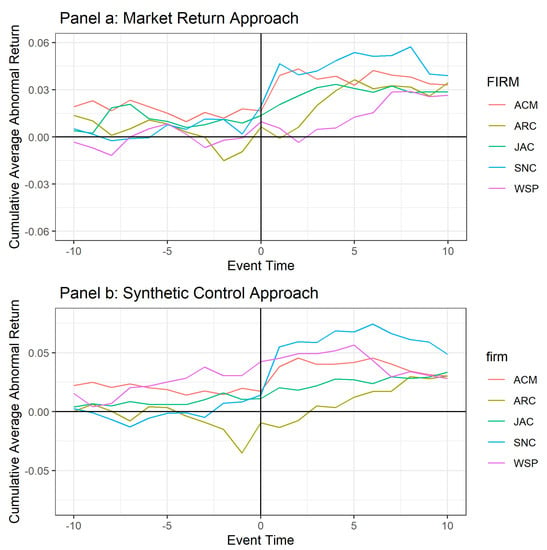

Figure 2 reports the cumulative average abnormal returns (in %) of the companies for the event window (−10 days, +10 days) based on the market model (Figure 2: Panel a) and the synthetic control model (Figure 2: Panel b). The results show that all companies present value creation from the M&A strategy. In both models, the SNC company reported the most positive average market reaction (3.90% in the market model and 4.87% based on the synthetic control model), while the WSP company presented the lowest cumulative average abnormal return (2.66% in the market model and 2.81% in the synthetic control approach).

Figure 2.

Dynamic of the cumulative average abnormal return by companies—event window (−10 days, +10 days). Notes: AECOM (ACM), Arcadis (ARC), Jacobs (JAC), SNC Lavalin (SNC), WSP Global (WSP).

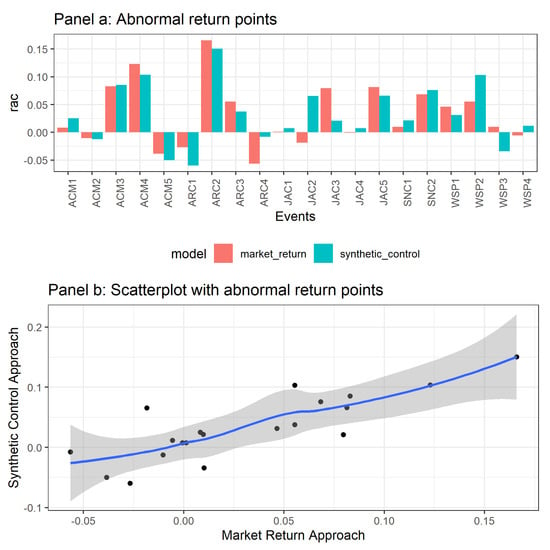

The estimated abnormal returns show a very similar pattern in both methodologies (Figure 3). The estimated effects (Figure 3: Panel a) differed slightly in magnitude between the market and synthetic control models through the analyzed events, being robustly equivalent to each other. The Scatterplot analysis (Figure 3: Panel b) confirms the strong correlation between the estimated effects, highlighting the robustness of the results obtained according to both methodologies. In this context, as in Castro-Iragorri (2019) [14], our evidence supports the quality of performance of the market model in the projection of returns obtained by companies from M&A processes.

Figure 3.

Abnormal return across the 20 events for the market return and synthetic control approaches—event window (−0 days, +10 days).

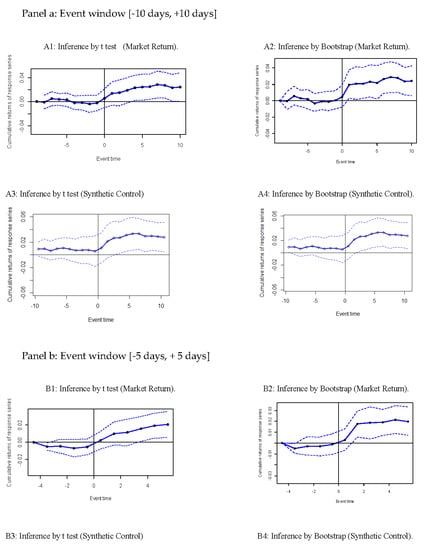

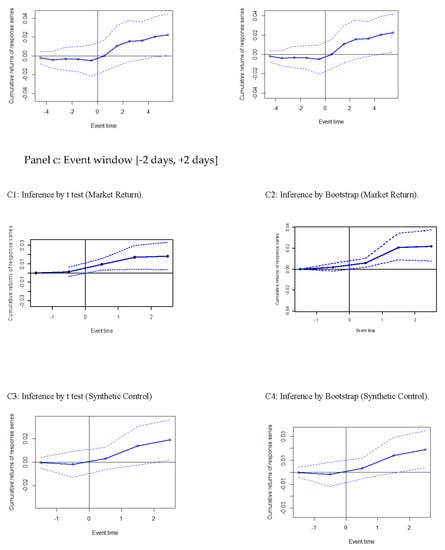

Table 2 and Figure 3 report the statistical tests to infer the market reaction to the announcement of the conclusion of the M&As processes under analysis, according to the three estimation windows ((−10 days, +10 days), (−5 days, + 5 days), (−2 days, + 2 days)). The statistical significance of the cumulative average abnormal return (CAAR) estimator was tested based on the classic t-student inference test and the non-parametric test built from 100,000 bootstrap re-samples.

Table 2.

Significance test on the sample of cumulative average abnormal return, according to the event windows 1.

Overall, our results indicate the positive impact of M&A announcements on market value by the five largest consulting engineering companies between 2009 and 2019 in the three estimation windows. The market reaction to the announcements ranged from 2.094% (market return approach) to 2.782% (synthetic control approach) in our main analysis (10-day window before and after the event), both being statistically significant at a 5% significance level. Companies showed significant and positive abnormal market returns when considering the (−5 days, +5 days) and (−2 days, +2 days) windows, with estimated effects ranging from 1.870% to 2.242% in all estimates, confirming investor perceptions of value generation for acquiring companies.

From a theoretical point of view, another important observation is the fact that the cumulative abnormal average return does not present significance from the statistical point of view in the days before the M&A announcement in any of our 12 specifications (Figure 4). Conversely, a positive and statistically significant market reaction is observed in all specifications, reaffirming the impact of the event on the market value of the companies.

Figure 4.

Accumulated abnormal returns of analyzed events. Note: The blue dotted lines represent a 95% confidence interval for the accumulated abnormal return. The vertical line indicates the moment when the event was announced.

Our results are in line with the evidence available in the literature and are at the upper threshold of estimates of M&A impact on the market value of acquiring companies. Weston et al. [6] consider that, in normal situations, the accumulated abnormal returns range from −2% (value destruction) to 2% (value creation) in the case of acquiring companies; however, Moeller et al. [12] suggest that negative returns are more common in the acquisition of public companies, which is not verified in the transactions under analysis.

The acquiring companies in our sample are characterized by intensive R&D and capillarity in their production structure, with assets and production of goods and services in multiple countries—factors also associated with value creation through M&A (in this case company expertize) is considered an important factor for the absorption of the transmission channels resulting from the synergy gains from M&A. International activity, on the other hand, potentializes the gains resulting from cross-border acquisitions, through technology transfer, exchange rate variation, and economies of scale, when potentializing the market for companies (Bednarczyk et al. [3]). This factor is especially relevant, since all companies operate in at least forty different countries, taking into account that twelve of the events analyzed characterized acquisitions made outside the country of origin of the acquiring company.

Another point associated with the market reaction is the size of the acquiring companies (market capitalization), which affects abnormal returns through two congruent effects. The first effect is summarized by the positive relationship between company size and bargaining power in the M&A negotiation process. The second effect concerns the perception of investors about the uncertainty (risk) of the business produced, which tends to be minimized when the acquiring company already presents market consolidation (Wilcox et al. [15]).

6. Conclusions

Companies in various sectors have different strategies and skills when it comes to generating and capturing opportunities to create market value. We conducted an empirical study on the role of mergers and acquisitions on the market returns of the world’s leading consulting engineering companies, assessing the importance of this mechanism in generating market value for them. We found important evidence that companies’ inorganic growth strategies had a positive impact on their market returns, based on a sample of the twenty-one major M&A events that occurred between 2009 and 2019. The positive market reaction to the announcement of M&A events indicates that the acquisition process generates opportunities for the diffusion of technology, the increase of effective market demand, and capturing revenue synergies. This can be important information for companies, since they can consider the existence of abnormal market reactions in the decision process in takeover bids (positive externality generated).

The event study model shows interesting results, reaching the objectives intended by its implementation. In addition, the synthetic control method strengthens the results achieved in the classic model.

Our methodology is theoretically very relevant for consulting engineering companies, and its practical application in companies is currently the subject of our research. A study is currently being applied in these companies, and practical results are expected after its implementation period.

This study offers a number of implications in several dimensions, making it possible for companies to easily achieve improved performance and growth, based on a cooperative approach.

Considering the range of the approach of our article, we recognize that further investigations can be carried out to understand the mechanisms of transmission of M&A announcements on market returns of other companies in the sector, analyzing whether there is financial contagion on the market returns of other companies. Bera et al. [29] find that the effects of risk factors on average returns vary over time scales due to their coefficient magnitudes and statistical significance, based on the multi-stage wavelet approach, for the period July 1963 to February 2018. This would be a relevant contribution to the construction and management of portfolio and risk management associated with the sector.

In addition, it would be interesting to consider a sample with a larger number of players in the consulting engineering sector, to build cross-section regressions and infer the contribution of corporate and financial factors on the creation of market value for the acquiring companies, in order to understand the role of the heterogeneities present in the sector on the abnormal market returns in M&A events.

Author Contributions

Methodology, P.d.M.N.; Supervision, J.A.F.; Validation, C.d.S.; Writing—original draft, M.A.J. All authors have read and agreed to the published version of the manuscript.

Funding

This research was supported by Iscte—University Institute of Lisbon through the Business Research Unit—BRU.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Description of the main mergers and acquisitions (M&A) events of the five largest engineering companies between 2009 and 2019.

Table A1.

Description of the main mergers and acquisitions (M&A) events of the five largest engineering companies between 2009 and 2019.

| Event (Acquiring—Target) | Date of Event | Estimation Window (Window Extension) (Distance from the Event)] | Control Group (Market Return Approach) | Control Group (Synthetic Control Approach) | Highlights |

|---|---|---|---|---|---|

| Arcadis—EC Harris | 18 October 2011 | 18 June 2010–18 June 2011 (257 observations) (4 months) | AMX Composite Index | The 100 largest stocks in AMX Composite Index | |

| Arcadis—DLS | 11 April 2012 | 18 June 2010–18 June 2011 (257 observations) (~10 months) | AMX Composite Index | The 100 largest stocks in AMX Composite Index | The same estimation window was adopted for the event (Arcadis—EC Harris), because of proximity between both acquisitions |

| Arcadis—Calisson | 21 August 2014 | 3 May 2013–3 May 2014 (254 observations) (~3 months) | AMX Composite Index | The 100 largest stocks in AMX Composite Index | |

| Arcadis—Hyder | 17 November 2014 | 3 May 2013–3 May 2014 (254 observations) (~6 months) | AMX Composite Index | The 100 largest stocks in AMX Composite Index | The same estimation window was adopted for the event (Arcadis—Calisson), because of proximity between both acquisitions |

| WSP—Focus | 10 April 2014 | 31 January 2013–31 January 2014 (250 observations) (~3 months) | S&P/TSX Composite Index | The 250 companies in S&P/TSX at august 2020. | Date of Hearing: 13 March 2014 |

| WSP—Parsons Brinckenhoff | 31 October 2014 | 31 January 2013–31 January 2014 (250 observations) (~9 months) | S&P/TSX Composite Index | The 250 companies in S&P/TSX at August 2020. | Date of Hearing: 9 September, 2014. The same estimation window of the event (WSP—Hyder) was adopted, because of proximity between both acquisitions |

| WSP—OPUS | 15 August 2017 | 15 May 2016–15 May 2017 (250 observations) (3 months) | S&P/TSX Composite Index | The 250 companies in S&P/TSX at August 2020. | |

| WSP—Louis Berger | 31 December 2018 | 31 October 2017–21 July 2018 (181 observations) (5 months) | S&P/TSX Composite Index | The 250 companies in S&P/TSX at August 2020. | Date of hearing: 31 July, 2008. The window became relatively less extensive due to the date of the previous event and the market rumors of the current event. |

| AECOM—Tishman Construction Group | 14 July 2010 | 1 March 2009–31 March 2010 (273 observations) (~4 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | |

| AECOM—Davis Langdon and McNeil Technologies | 5 August 2010 | 1 March 2009–31 March 2010 (273 observations) (~5 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | The same window was adopted for the estimation of the event (WSP—Tishman), because of proximity between both acquisitions. |

| AECOM—URS | 11 July 2014 | 30 April 2013–30 April 2014 (251 observations) (~3 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | |

| AECOM—Hunt | 28 July 2014 | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | The same window was adopted for the estimation of the event (WSP—URS), because of proximity between both acquisitions. | |

| AECOM—Shimmick | 6 July 2017 | 30 April 2017–30 April 2017 (252 observations) (~3 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | |

| JACOBS—Sinclair | 12 December 2013 | 12 August 2012–12 September 2013 (271 observations) (3 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | |

| JACOBS—Blue Canopy Group | 31 August 2017 | 15 May 2016–15 May 2017 (251 observations) (~4 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | |

| JACOBS—CH2M | 15 December 2017 | 15 May 2016–15 May 2017 (251 observations) (7 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | The same estimation window was adopted for the event (JACOBS—Blue Canopy Group), because the proximity between both acquisitions. |

| JACOBS—KeyW | 22 April 2019 | 22 March 2018–22 February 2019 (230 observations) (2 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | The date 22 March, 2018, was adopted as the initial period, to guarantee the distance of 3 months in relation to the date of the event (JACOBS—CH2M), which will occur on 15 December, 2017. To incorporate additional information to the window, a distance of only two months in relation to the event was used. |

| JACOBS—JWG | 20 August 2019 | 22 March 2018–22 February 2019 (230 observations) (~6 months) | NYSE Composite Index | The 500 companies in S&P 500 at August 2020. | The same estimation window was adopted for the event (JACOBS—KeyW), because of proximity between both acquisitions. |

| SNC—Kentz | 23 June 2014 | 23 March 2013–23 March 2014 (250 observations) (3 months) | S&P/TSX Composite Index | The 250 companies in S&P/TSX at August 2020. | |

| SNC—WS Atkins | 3 July 2017 | 3 April 2016–3 April 2017 (251 observations) (3 months) | S&P/TSX Composite Index | The 250 companies in S&P/TSX at August 2020. | Date of Hearing: 20 April 2007. |

References

- Singh, H.; Montgomery, C.A. Corporate acquisitions strategies and economic performance. Strateg. Manag. J. 1987, 8, 377–386. [Google Scholar] [CrossRef]

- Triviños, A.N.S. Introduction to Social Science Research; Atlas: São Paulo, Brazil, 2012. [Google Scholar]

- Bednarczyk, T.P.; Schierec, D.; Walter, H.N. Cross-border acquisitions and shareholder wealth: Evidence from the energy and industry in Central and Eastern Europe. J. East Eur. Manag. Stud. 2010, 15, 106–127. [Google Scholar] [CrossRef]

- Arikan, A.M. Does it pay-off to capture intangible assets through mergers and acquisitions? Acad. Manag. Proc. 2002, 2002, R1–R6. [Google Scholar] [CrossRef]

- Gupta, O.; Roos, G. Mergers and acquisitions through an intellectual capital perspective. J. Intellect. Cap. 2001, 2, 297–309. [Google Scholar] [CrossRef]

- Weston, J.F.; Siu, J.A.; Johnson, B.A. Takeovers, Restructuring & Corporate Governance, 3rd ed.; Prentice-Hall: Upper Saddle River, NJ, USA, 2001. [Google Scholar]

- Gaughan, P.A. Mergers, Acquisitions, and Corporate Restructurings, 3rd ed.; John Wiley & Sons: New York, NY, USA, 2002. [Google Scholar]

- Coase, R.H. The nature of the firm. Economica 1937, 4, 386–405. [Google Scholar] [CrossRef]

- Abadie, A.; Diamond, A.; Hainmueller, J. Synthetic Control Methods for Comparative Case Studies: Estimating the Effect of California’s Tobacco Control Program. J. Am. Stat. Assoc. 2010, 105, 490–505. [Google Scholar] [CrossRef]

- Hannan, T.H.; Wolken, J.D. Returns to bidders and targets in the acquisition process: Evidence from the banking industry. J. Financ. Serv. Res. 1989, 3, 5–16. [Google Scholar] [CrossRef]

- Mackinlay, A.C. Event studies in economics and finance. J. Econ. Lit. 1997, 35, 13–39. [Google Scholar]

- Moeller, S.B.; Schlingemann, F.P.; Stulz, R.M. Firm size and the gains from acquisitions. J. Financ. Econ. 2004, 73, 201–228. [Google Scholar] [CrossRef]

- Billmeier, A.; Nannicini, T. Assessing Economic Liberalization Episodes: A Synthetic Control Approach. Rev. Econ. Stat. 2013, 95, 983–1001. [Google Scholar] [CrossRef]

- Iragorri, C.C. Does the market model provide a good counterfactual for event studies in finance? Financ. Mark. Portf. Manag. 2019, 33, 71–91. [Google Scholar] [CrossRef]

- Wilcox, H.D.; Chang, K.-C.; Grover, V. Valuation of mergers and acquisitions in the telecommunications industry: A study on diversification and firm size. Elsevier Inf. Manag. 2001, 38, 459–471. [Google Scholar] [CrossRef]

- Mulherin, J.H.; Boone, A.L. Comparing acquisitions and divestitures. J. Corp. Financ. 2000, 6, 117–139. [Google Scholar] [CrossRef]

- Harris, R.S.; Ravenscraft, D. The Role of Acquisitions in Foreign Direct Investment: Evidence from the U.S. Stock Market. J. Financ. 1991, 46, 825–844. [Google Scholar] [CrossRef]

- Gopalaswamy, A.K.; Acharya, D.; Malik, J. Stock Price Reaction to Merger Announcements: An Empirical note on Indian Markets. Invest. Manag. Financ. Innov. 2008, 5, 95–103. [Google Scholar]

- Strong, N. Modelling Abnormal Returns: A Review Article. J. Bus. Financ. Account. 1992, 19, 533–553. [Google Scholar] [CrossRef]

- Liargovas, P.; Repousis, S. The Impact of Mergers and Acquisitions on the Performance of the Greek Banking Sector: An Event Study Approach. Int. J. Econ. Financ. 2011, 3, 89–100. [Google Scholar] [CrossRef]

- KhanaL, A.R.; Mishra, A.K.; Mottaleb, K.A. Impact of mergers and acquisitions on stock prices: The US ethanol-based biofuel industry. Biomass Bioenergy 2014, 61, 138–145. [Google Scholar] [CrossRef]

- Ball, R.; Brown, P. An empirical evaluation of accounting numbers. J. Account. Res. 1968, 6, 159–178. [Google Scholar] [CrossRef]

- Fama, E.F.; Fisher, L.; Jensen, M.C.; Roll, R. The adjustment of stock prices to new information. Int. Econ. Rev. 1969, 10, 1–21. [Google Scholar] [CrossRef]

- Brown, S.J.; Warner, J.B. Measuring security price performance. J. Financ. Econ. 1980, 8, 205–258. [Google Scholar] [CrossRef]

- Brown, S.J.; Warner, J.B. Using daily stock returns. J. Financ. Econ. 1985, 14, 3–31. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Kothari, S.P.; Warner, J.B. Econometrics of Event Studies. In Handbook of Corporate Finance; Espen Eckbo, B., Ed.; Elsevier: Amsterdam, The Netherlands, 2007; Volume 1, pp. 3–36. [Google Scholar]

- Mandelker, G. Risk and Return: The Case of Merging Firms. J. Financ. Econ. 1974, 1, 303–335. [Google Scholar] [CrossRef]

- Bera, A.; Uyar, U.; Uyar, S. Analysis of the five-factor asset pricing model with wavelet multiscaling approach. Q. Rev. Econ. Financ. 2020, 76, 414–423. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).