1. Introduction

The models defined by stochastic differential equations (SDEs)

where

B is a standard Brownian motion,

g is a continuous function on

,

is nonrandom initial value, and

is a constant, include several well-known models such as Chan–Karolyi–Longstaff–Sanders (CKLS), Cox–Ingersoll–Ross (CIR), Ait–Sahalia (AS), Cox–Ingersoll–Ross variable-rate (CIR VR), and others used in many financial applications [

1,

2,

3,

4,

5,

6]. The positivity is a desirable property for many financial models, such as option pricing, stochastic volatility, and interest rate models. Thus, it is important to find conditions under which the solutions to Equation (

1) are positive. Preservation of positivity is a desirable modelling property, and in many cases the non-negativity of numerical approximations is needed for the scheme to be well defined. Therefore, many numerical methods have been developed to preserve the positivity of the approximate solution in the case of the positive true solution.

For an SDE to have a unique global solution (i.e., with no explosion in a finite time) for any given initial value, the coefficients of the equation are in general required to satisfy the linear growth and local Lipschitz conditions. These conditions are not satisfied in the models mentioned. The existence of positive solutions of SDEs corresponding to these models and implicit numerical schemes preserving the positivity were studied in [

1,

2,

3,

4,

5,

6].

An important research area in financial mathematics is the long memory phenomenon in financial data. Hence, since fractional Brownian motion (fBm)

introduces a memory element, there is much attention in recent years to models with fBm. Consider the FSDEs

with

. The stochastic integral in Equation (

2) is a pathwise Riemann–Stieltjes integral, but SDE (

2) cannot be treated directly since the functions

,

,

, do not satisfy the usual Lipschitz conditions.

For fractional CIR, CKLS, and AS models, the existence of a unique positive solution of Equation (

2) was obtained in [

7,

8,

9,

10,

11,

12,

13,

14]. The proof can be provided in several ways. One approach is based on the consideration of the conditions under which the equation

admits a unique positive solution, where

is a locally Lipschitz function with respect to the space variable

. This approach was used in [

7,

8,

9,

11,

14], where the inverse Lamperti transform was used to obtain conditions under which Equation (

1) admits a unique positive solution for fractional CIR, CKLS, and AS models. Unfortunately, we cannot apply the proof of positivity of the solution of (

3) given in [

14] (e.g., it is not applicable to the AS model).

Marie [

10] used the rough-path approach to find the existence of a unique positive solution of the fractional CKLS model.

A simulation of the fractional CIR process was given in [

11] by using the Euler approximation. In [

8,

14] an almost sure strongly convergent approximation of the considered SDE solution is constructed using the backward Euler scheme, which is positivity preserving.

In this paper, we consider the SDE

where

is a constant. This type of equation is obtained after the Lamperti transformation of the FSDE (

2). The purpose of the paper is finding sufficiently simple conditions when the solution of (

4) for

and

is positive. Moreover, using the backward Euler scheme, which preserves the positivity for (

4), we obtain an almost sure convergence rate for

X. Since the problem of the statistical estimation of the long-memory parameter

H is of great importance, we construct an estimate of the Hurst index

in the same way as for the diffusion coefficient satisfying the usual Lipschitz conditions (see [

15,

16]). This can be done since the solution of Equation (

2) is positive. More results on parameter estimations for the FSDEs can be found in the book [

17].

The paper is organized as follows. In

Section 2, we present the main results of the paper. In

Section 3, we prove the main auxiliary result on the existence and uniqueness of a positive solution for SDE (

4).

Section 4 contains proofs of the main theorems. In

Section 5, we consider fractional CKLS and AS models as examples. Finally, in

Appendix A, we recall the Love–Young inequality, the chain rule for Hölder-continuous functions, and some results for fBm.

2. Main Results

We are interested in conditions under which the SDE

has a unique positive solution. The stochastic integral in Equation (

5) is a pathwise Riemann–Stieltjes integral.

To state our main results, we assume that the following conditions on the function

f in (

5) are satisfied:

f is a locally Lipschitz on ;

There exist constants

and

such that

for all sufficiently small

;

The function

satisfies

the one-sided Lipschitz condition, that is, there exists a constant

such that

for all

.

Theorem 1. If a function f satisfies conditions –, then Equation (5) is well defined and has a unique positive solution of order for , where denotes the space of Hölder-continuous functions of order on . A strong approximation of the SDE that has locally Lipschitz drift for

is constructed by applying the backward Euler scheme in [

14] (see also [

1] for

). By using the backward Euler scheme, which preserves positivity for (

6), we obtain an almost sure convergence rate for

X.

A sequence of uniform partitions of the interval

we denote by

and let and

,

. We introduce the backward Euler approximation scheme for

YThe following assumption is needed for the positivity of the backward Euler approximation scheme to be preserved:

Let on , where the function satisfies condition . There exists such that and for .

Remark 1. Please note that under condition the function is strictly monotone on for small h. This follows from and the inequalitywhere . Thus, from the condition it follows that for each , the equation has a unique positive solution for . As a result, we see that the positivity is preserved by the backward Euler approximation scheme. For the simplicity of notation, we introduce the symbol . Let be a sequence of r.v.s, let be an a.s. nonnegative r.v., and let be a vanishing sequence. Then means that for all n. In particular, means that the sequence is a.s. bounded.

Theorem 2. Suppose that the function f in (5) is continuously differentiable on and satisfies condition and that there exists a constant such that the derivative is bounded above by K, that is, . If the sequence of uniform partitions π of the interval is such that , then for all and ,where Moreover,where X is the solution of Equation (5). For positive solutions of Equation (

5), we construct a strongly consistent and asymptotically normal estimator of the Hurst parameter

H from discrete observations of a single sample path.

For a real-valued process

, we define the second order increments along uniform partitions as

Theorem 3. Let X be a unique positive solution of SDE (5) with . Thenandwith known variance defined in Appendix, where 3. Auxiliary Results

As mentioned in Introduction, we are interested in conditions under which the SDE (

6) has a unique positive solution.

Proposition 1. Suppose that a function f satisfies conditions –. If , , and , then there exists a unique positive solution of Equation (6) such that , , where and . We easily to see that the same proof as in Proposition 1 [

8] remains valid for Proposition 1.

Applying Proposition 1 to the fractional AS model and Heston-3/2 volatility model, we obtain that the trajectories of these models are positive (see

Section 5). Our proof scheme gives no answer about the behavior of the trajectories of the CKLS model

with the initial value

and deterministic constants

,

, and

.

Now we will explain why we cannot give an answer about the behavior of the trajectories of the CKLS model. Consider the SDE

Suppose that the solution of the SDE (

11) is positive. Then by applying the chain rule (see

Appendix A.2) and the inverse Lamperti transform

we can prove that

X is a positive solution of (

10).

Unfortunately, it is easy to see that the function

does not satisfy condition

. So, we cannot apply Proposition 1 and say anything about the positivity of the solution of (

11).

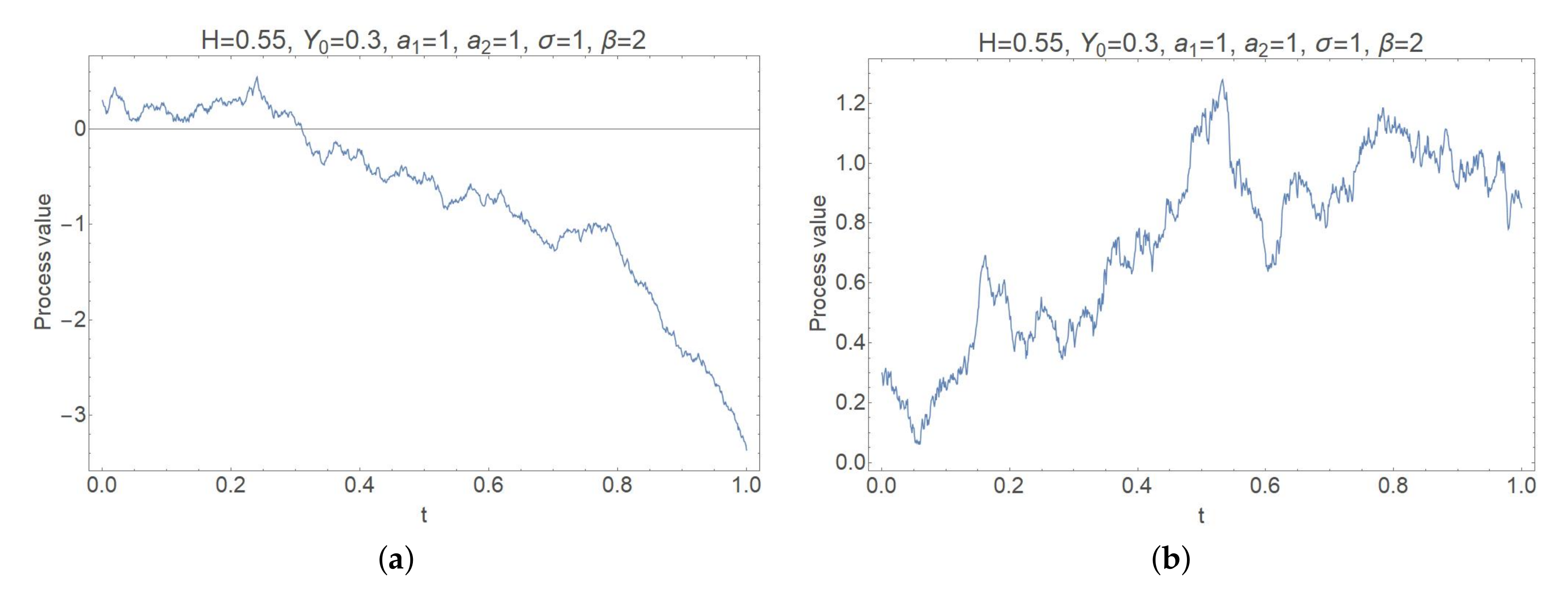

Computer modelling using

Wolfram Mathematica shows that the trajectories of the process

Y may have negative values for

(see

Figure 1).

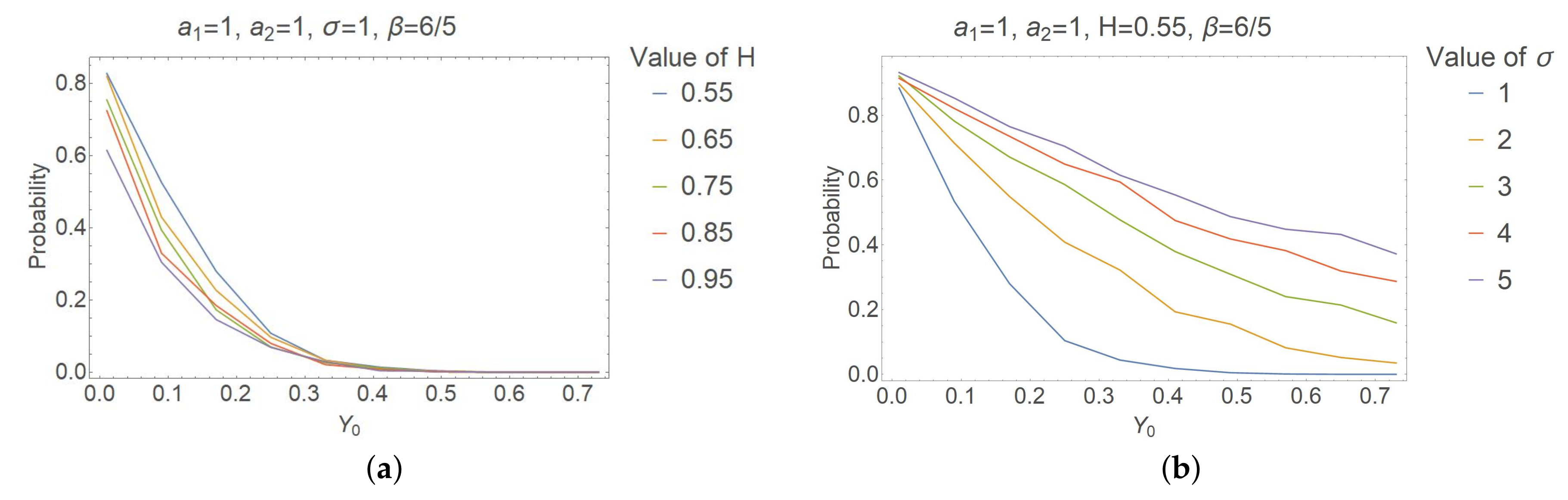

To investigate the probability of reaching the negative values by the process

Y when

, we simulate the “exact” solution by using the backward Euler approximation scheme for step size

and repeat this process

times counting the trajectories with negative values. We observe that the solution has a higher probability to reach the negative values for small initial values

and that for large enough values of

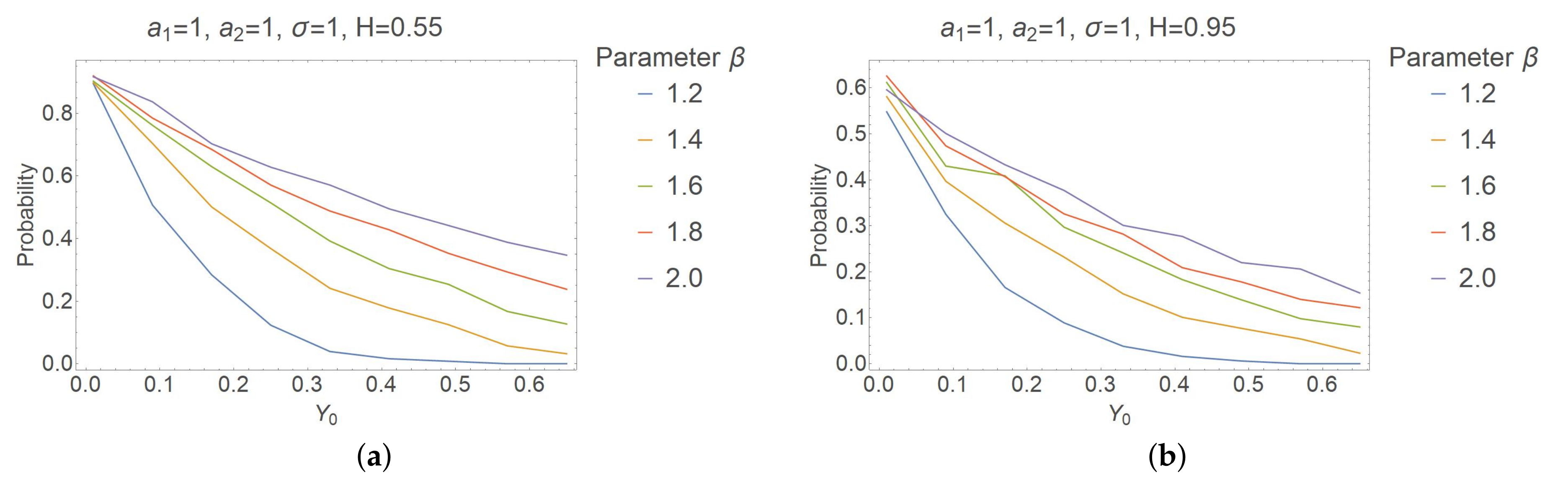

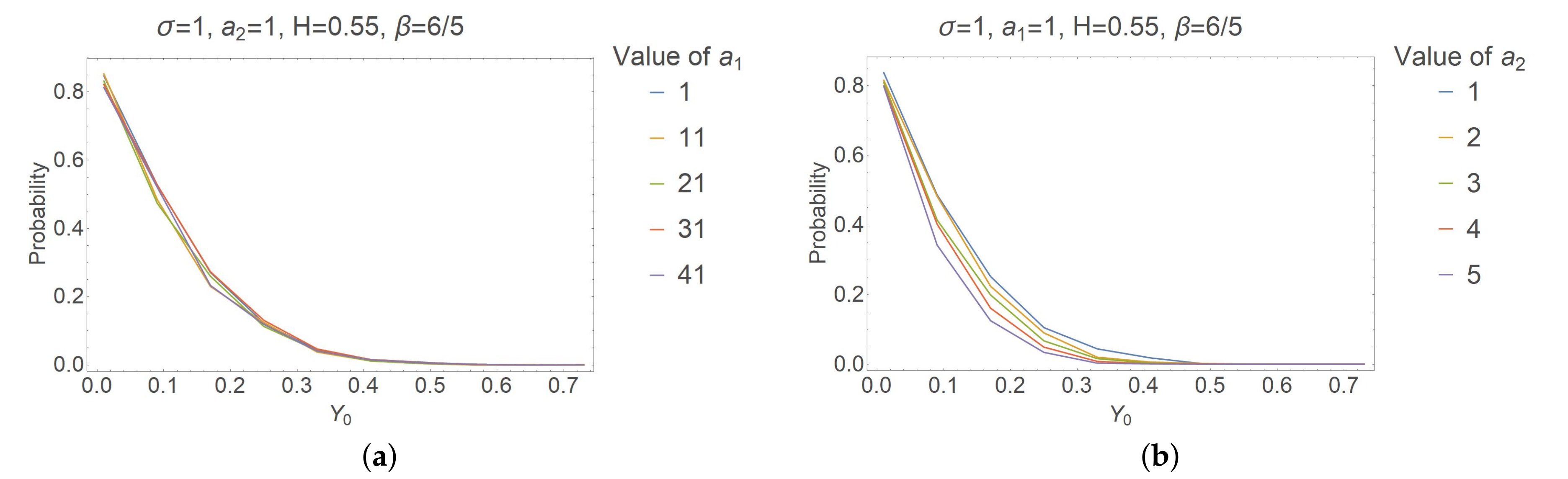

, this probability tends to zero. Additionally, the probability increases for greater values of the parameters

(see

Figure 2b and

Figure 3) and decreases for greater values of the parameters

(see

Figure 2a and

Figure 4b). The influence of

on the probability (see

Figure 4a) is not noticeable in comparison with other parameters.

Thus, we can only state that Equation (

10) has a solution

until the moment at which

Y becomes zero. On the other hand, we do know that the CKLS model driven by a standard Brownian motion (see [

6]) with

and the fractional CKLS model with

(see [

8]) have positive solutions.

6. Conclusions

In this paper, we gave sufficiently simple conditions under which the solution of SDE

has a unique positive solution. By applying the chain rule and the inverse Lamperti transform

, we proved that

X is a positive solution of equation

under certain conditions on the function

f.

Equation (

18) describes models, such as fractional Ait–Sahalia and Heston-

volatility, in which the positivity is important for many financial applications. Usually, we are not aware of an explicit expression for the solution, and therefore we considered computable discrete-time approximations, which can be used in Monte Carlo simulations. To approximate the solution of Equation (

17), we used an implicit Euler scheme, which preserves the positivity of the numerical scheme. By applying the inverse Lamperti transform to

Y we obtained an approximation scheme for the original SDE (

18). Moreover, we obtained the almost sure convergence rate for both processes.

Not all models defined by the stochastic differential Equation (

18) necessarily have positive trajectories. The paths of the fractional CKLS model are not necessarily positive, in contrast to the classical CKLS model driven by the standard Brownian motion with

or fractional CKLS model with

.

The statistical estimation of the long-memory parameter

H is of great importance, therefore, we constructed its estimate. For the first time, we obtained an estimate of the Hurst index for the solution of Equation (

18). Finally, the positivity of solution of (

18) allowed us to construct an estimate of the Hurst index, which is not only strongly consistent, but also asymptotically normal.

{kind=link}

{kind=link}

{kind=link}

{kind=link}