Abstract

Due to CO emissions, humans are encountering grave environmental crises (e.g., rising sea levels and the grim future of submerged cities). Governments have begun to offset emissions by constructing emission-trading schemes (carbon-offset markets). Investors naturally crave carbon-offset options to effectively control risk. However, the research and practice for these options are relatively limited. This paper contributes to the literature in this area. Specifically, according to carbon-emission allowances’ empirical distributions, we implement fractal Brownian motions and jump diffusions instead of traditional geometric Brownian motions. We contribute to extending the theoretical model based on carbon-offset option-pricing methods. We innovate the carbon-offset options of Asian styles. We authenticate the options’ stochastic differential equations and analytically price the options in the form of theorems. We verify the parameter sensitivity of pricing formulas by illustrations. We also elucidate the practical implications of an emission-trading scheme.

Keywords:

carbon offset; emission-trading scheme; carbon-offset investments; carbon-offset options; jump diffusions; fractal Brownian motions; stochastic differential equations MSC:

60H15; 91G20

1. Introduction

1.1. Alarming Global Warming and Carbon-Offset Options

We humans must accept the unquestionable fact that CO does cause global warming. Even climate scientists were astonished at observing record temperatures at the poles (e.g., 40 degrees above normal in Antarctica) on 20 March 2022. (Data source: The Irish Times, https://www.irishtimes.com/news/environment/scientists-astonished-by-heatwaves-at-north-and-south-poles-1.4831673, 20 March 2022).

The Intergovernmental Panel on Climate Change (IPCC) projects that the global sea level will rise 0.6 m to 1.1 m by 2100. (Data source: IPCC 2019 report, https://www.ipcc.ch/2019, 22 December 2021). The rising seas will then engulf numerous major cities (e.g., New York City by the year 2080 (Data source: JSTOR Daily, https://daily.jstor.org/new-york-city-underwater/, 6 October 2021) and Shanghai and Guangzhou by 2100 (Data source: JY International Cultural Communications, https://www.thatsmags.com/guangzhou/post/29864/shanghai-and-prd-at-risk-of-disappearing-under-rising-sea-levels, 1 November 2019)). More alarmingly, even such pessimistic projections have become too optimistic under accelerating global warming day by day.

Humans are eagerly trying to combat global warming by restraining CO consumption. Ref. [1] empirically confirms that economic growth increases CO emissions, and urges the reduction. Governments have composed carbon-offset securities to curb CO increments while preserving necessary economic growth. Promisingly, the European Union Emission-Trading System (EU ETS) was pioneered in 2005 as the first international emission-trading system and has successfully launched three phases of action. (Data source: EU ETS, https://ec.europa.eu/clima/eu-action/eu-emissions-trading-system-eu-ets/development-eu-ets-2005-2020_en#ecl-inpage-1020, 3 January 2022). Ref. [2] methodically concentrated on the EU ETS and contended that the public does care about climate.

In particular, investors have applauded European Union Allowances futures and European Union Allowances options as ground-breaking carbon-offset derivatives. However, the trading volume of such options is still scant, in the context of 33.31 billion option contracts being traded worldwide in 2021. (Data source: Statista Incorporation, https://www.statista.com/statistics/377025/global-futures-and-options-volume/, 9 March 2022).

1.2. Carbon-Offset-Option Literature

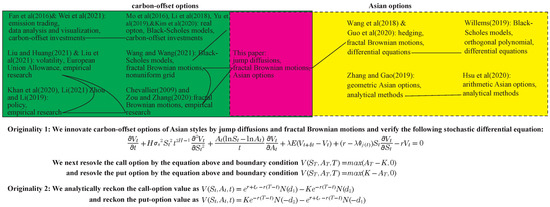

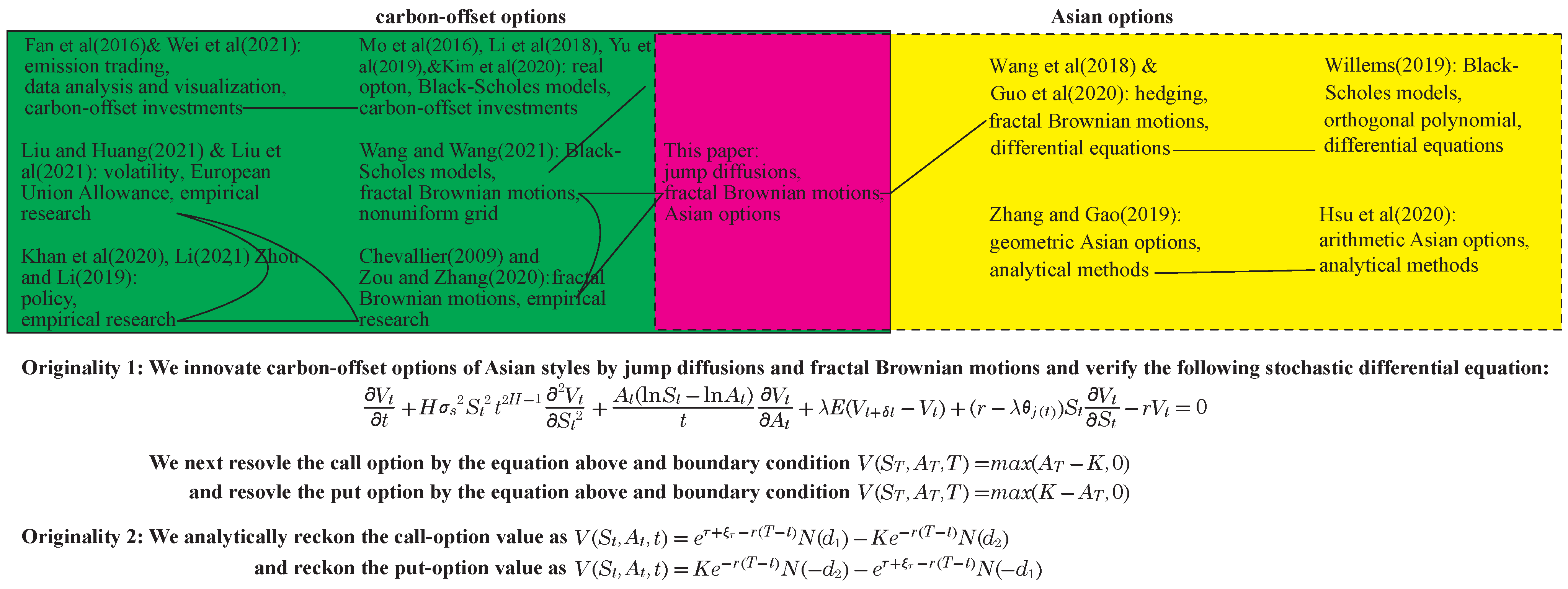

The literature on carbon-offset options is also relatively scant. We depict several key pieces of literature in the green rectangle under the name “carbon-offset options” in the top part of Figure 1. We categorize similar research into a group and register the main research methods. For instance, Refs. [2,3] have investigated emission trading, data analysis and visualization, and carbon-offset investments. We additionally connect different groups’ analogous methods using lines. For example, the group of [2,3] and the group of [4,5,6,7] have both contemplated carbon-offset investments. The group of [8,9] and the group of [1,10,11] have both conducted empirical research. We will further review the references later (especially in Section 2).

Figure 1.

The originality and several key pieces of literature [1,2,3,4,5,6,7,8,9,10,11,12,13,14,15,16,17,18,19].

Under a similar format, we also depict several key pieces of literature for Asian options in the yellow rectangle. For instance, the group of [12] and the group of [13,14] have both implemented differential equations. Refs. [15,16] applied analytical methods to derive pricing formulas.

As the intersection (in the pink shaded area) of the green rectangle and yellow rectangle, we depict this paper for Asian carbon-offset options based on jump diffusions and fractal Brownian motions in the top part of Figure 1. The group of [17], the group of [18,19], and the group of [13,14] have all harnessed fractal Brownian motions.

Moreover, we briefly present the originality in the bottom part of Figure 1.

1.3. Originality: Innovating and Pricing Carbon-Offset Options of Asian Styles by Jump Diffusions and Fractal Brownian Motions

Specifically in the area of carbon-offset options, this paper carries the following originality:

First, we innovate the options by justifying the jump-diffusion condition and fractal-Brownian-motion condition. Refs. [18,19] empirically discovered heavy tails, high peaks, and thus non-normal distributions for European carbon-offset futures. The discovery contradicts geometric Brownian motion properties (especially normal distributions). Therefore, we extend geometric Brownian motions into fractal Brownian motions. The COVID-19 pandemic, astronomical amounts of money worldwide and the liquidity effect, and regional conflicts can bring uncommon volatility and uncertainty to financial markets. For instance, Refs. [20,21] discerned uncommon volatility in stock markets and bond markets, respectively. The exceptional volatility can hardly be prescribed by geometric Brownian motion. Therefore, we append jump-diffusion models. Moreover, we envisage the options as Asian styles, because the existing carbon-offset options typically belong to European styles or American styles (see [17,22]). Asia (especially China and Japan) shoulders important roles in carbon offset. Meanwhile, the path dependence of Asian options avoids the risk of exceptional volatility for underlying asset prices on the maturity date, which is not considered in the existing research on carbon-offset options.

Second, we analytically price the options in the form of theorems. The approximate analytical pricing formula of options is more concise than pricing formulas containing series terms (as displayed by [23]).

1.4. Paper Structure

The rest of this paper is organized as follows: We review the theoretical background in Section 2. We instigate the options and gauge the stochastic differential equations in Section 3. We analytically price the options in Section 4. We elucidate the pricing by an example in Section 5. We conclude this paper in Section 6.

2. Literature Review: Asian Options and Carbon-Offset Options

2.1. Classic Option Pricing

Ref. [24] seminally lay the foundation of option pricing by assuming that the underlying asset follows a geometric Brownian motion. However, researchers later discovered the assumption’s weakness in practice. Ref. [25] compared and related thee major option-pricing methods. Ref. [26] stressed the discrepancy between the model of [24] and reality and modify the model.

To better delineate financial markets, researchers instigated the extensions. For instance, Ref. [27] (pp. 125–130) proposed jump-diffusion models, emphasizing uncommonly sizable stock-price jumps and prescribing that both continuous and jump processes command stock prices. Ref. [28] further enlightened the double exponential jump-diffusion models to overcome leptokurtic features (e.g., heavy tails) and volatility-smile features.

Specifically for jump diffusions, Ref. [29] (pp. 642–643) illuminated jump diffusions as follows:

where

- basically inscribes geometric Brownian motions (as delineated by [29] (pp. 323–324)).

- inscribes the jumps.

- Stochastic processes and are independent.

- For notations, we principally track the classic symbols of [29]. For stochastic processes (e.g., ), we interchangeably employ and by trailing the notation tradition (e.g., of [30] (p. 184) and of [31] (p. 199)).

Ref. [32] deployed (1) for Asian options.

The B-S model, based on the geometric Brownian motion (as displayed by [24]), assumes the log-normal property of the underlying asset price, and hardly describes random walks with skewness. For instance, Refs. [33,34] recognized the underlying asset peculiarity (e.g., heavy tails) and extended geometric Brownian motions into fractal Brownian motions. Scholars have further developed other diffusion processes for the fractal Brownian motion variant, for example, mixed fractal Brownian motion (see [35]) and sub-mixed fractal Brownian motion (see [36]). Consequently, scholars have gradually studied derivative prices jointly driven by jump diffusions and fractal Brownian motions (as displayed by [23]).

Specifically for fractal Brownian motions, Ref. [37] proposed a stochastic integral of fractal Brownian motions based on the Wick product. However, Ref. [38] first questioned the use of the Wick product and focused on the basic economic explanation beyond pure mathematical theories. Ref. [34] implemented the Wick product into the definition of portfolio value and the attribute of self-financing. Ref. [39] utilized properties of the fractal Taylor formula to develop the fractal Itô’s formula with the Hurst exponent . The method is different from the classic method of Wick product (as described by [37]). Ref. [13] presumed self-similar and long-term dependence characters for the assets, manipulated stochastic differential equations, and analytically assessed options. Ref. [40] utilized Itô’s lemma and analytically estimated the options by Malliavin calculus. Ref. [41] added approximative fractal stochastic volatility to the double Heston jump-diffusion model and deduced the option-pricing formula.

Moreover, researchers have exploited partial differential equations and analytically valued options. Ref. [42] applied partial differential equations, adopted Mellin transformation, and valued options using Volterra integral equations. Ref. [43] established monotonous transaction costs, fashioned partial differential equations, and analytically assessed options.

2.2. Pricing Asian Options

Ref. [29] (p. 626) defined that an Asian option is a kind of option whose value is determined by the average price of the underlying asset during the option life. Ref. [29] (p. 626) prescribed the call-option value and put-option value on maturity T as follows:

where

- K is the exercise price;

- is the asset’s geometric average price .

The analytical pricing formula of Asian options has been widely studied by scholars due to its concise form. Based on [24], Ref. [12] cogitated orthogonal polynomials, calculated series expansions for option prices, and established the series convergence. Ref. [13] explored the pricing formula of dual-asset Asian rainbow options under fractal Brownian motions based on differential equations. Ref. [14] targeted subdiffusive Brownian motions, executed hedging strategies, and analytically resolved option prices using partial differential equations. Ref. [15] experimented with double Heston models and evaluated first-order asymptotic expansions for the geometric Asian option price. Ref. [16] integrated Taylor-series expansions for deriving approximate analytical solutions for arithmetic Asian options.

2.3. Pricing Carbon-Offset Options

2.3.1. Underlying Assets’ Empirical Distributions and Limitations of Geometric Brownian

A great deal of empirical research analyzes the time series and empirical distribution characteristics of carbon underlying asset prices.

Carbon financial asset prices have random fluctuations and present fractal features such as non-normal distribution, peak, and thick tail. Ref. [18] focused on European carbon-offset futures and portrayed the returns using leptokurtic features (e.g., heavy tails) and nonzero-skewness features. Ref. [19] also characterized European carbon-offset futures using heavy tails, high peaks, and thus non-normal distributions, and deduced the characterization as the cause for multiple-fractal situations. Ref. [44] used the fractal market hypothesis and evolutionary computing to analyze carbon futures trading and short-term price prediction.

Carbon financial asset prices occasionally have exceptional fluctuations and jumping features. Ref. [45] empirically discovered that the time series of carbon-emission-allowance price presents jumps and is non-stationary. Ref. [46] confirmed the Markov property of the carbon allowance price under a non-linear market fundamental model. Ref. [47] applied the mechanism transformation jump-diffusion model with hidden Markov chains to capture the jump and fluctuation clustering characteristics of EUA price returns.

Because the leptokurtic features contradict geometric Brownian motion properties (especially normal distributions) from the existing empirical research, scholars have gradually channeled fractal Brownian motions for carbon-offset derivatives. Jumping and non-stationary features from carbon-trading markets also contradict geometric Brownian motion properties (especially continuous). Therefore, scholars have harnessed jump-diffusion processes for carbon-offset derivatives.

2.3.2. Carbon-Offset Option-Pricing Models

The main research on carbon-offset option pricing usually adopts the classic Black–Scholes model as the basis for construction. Ref. [22] attested that the carbon-emission permit price driven by geometric Brownian motion is a martingale process in stochastic, continuous, and infinite time models. Ref. [17] modulated the Black–Scholes model into a mixed fractal Black–Scholes model and direct power-penalty approaches and nonuniform grid-based modifications in the problem of American carbon-emission derivative pricing. Ref. [48] proposed the application of carbon-offset options evaluated through a geometric Brownian motion model with regime-switching for carbon management, together with the high volatility of the carbon price dynamic.

2.3.3. Exploring Real Options

Researchers have made promising progress in carbon-offset options. In addition, the research concentrates on real options. For instance, Ref. [4] constructed real options for wind power, tuned the main parameters, and dissected the relationship between the emission-trading scheme and low-carbon-energy investments in China. Ref. [6] aimed for defer-type real options and abandon-type real options, and executed two-dimensional binominal lattices in the pricing. Ref. [5] heeded carbon-price fluctuations and, accordingly, fashion real options, and enhanced investment performance. Ref. [7] was aware of fossil-energy prices and carbon-emission-allowance prices, and conceived real options for R&D investments.

2.3.4. Innovating Portfolio Selection

Considering the investment demand for carbon offsetting, scholars have proposed a multi-objective portfolio selection that takes into account both risks and returns. Investors can build constraints using the carbon-offset measure and operate portfolio selection and optimization (as experimented by [49]). Ref. [50] took the green innovation index as the third objective dimension of the portfolio-selection model.

2.3.5. Calibrating GARCH Models for the Volatility

The volatility prediction of underlying assets in the carbon-trading market has been another concern of researchers. Ref. [8] sampled European Union Allowances option prices on the European Energy Exchange, measured the volatility using GARCH models, and forecasted the future prices. Ref. [9] consumed the GARCH-MIDAS models for the volatility of European Union Allowances futures, contrasted the GARCH-MIDAS models and other GARCH models, and uncovered the outperformance of the GARCH-MIDAS models.

2.4. Appraising Key Literature

2.4.1. Urgency to Advance Carbon-Offset Options

Ref. [1] confirmed that economic growth increases CO emissions, and thus urged reduction. Ref. [10] reviewed Chinese research and the practice of carbon offset, underscoring the urgency for carbon-offset markets, and appraising the options. Ref. [11] empirically verified that options trading increases corporate investments and that the effect is stronger for corporations with higher information asymmetry difficulties.

2.4.2. Suitability for Jump Diffusions

In addition to global warming, the COVID-19 pandemic has unleashed crises of humanity, economy, and finance. With industry shutdown, loss of employment, and an unimaginable death toll of almost a million in the US alone by March 2022, the global economy is falling into recession. Moreover, the astronomical amount of money worldwide and the liquidity effect, and regional conflicts (e.g., the Russia–Ukraine war) can bring uncommon volatility and uncertainty to financial markets and put financial stability at great risk. For instance, Refs. [20,21] discerned uncommon volatility in stock markets and bond markets during the COVID-19 pandemic. In the carbon-emission trading market, Refs. [45,47] empirically discovered the jumping characteristics of carbon-emission allowance prices. Further research has claimed that the jump-diffusion model (JDM) proposed by [27] is the most suitable dynamic model for EUAs. Therefore, jump-diffusion models have surfaced as appropriate candidates.

2.4.3. Suitability for Fractal Brownian Motions

Refs. [18,19] empirically unearthed heavy tails, high peaks, and thus non-normal distributions for European carbon-offset futures and inferred the application of fractal Brownian motions. Ref. [17] unveiled fractal Black–Scholes models and affirmed the models’ effectiveness. Ref. [8] reasonably predicted carbon option prices with fractal Brownian motion considering the fractal characteristics of carbon-offset option prices.

3. Originating the Options and Verifying the Stochastic Differential Equation

3.1. Initiating Carbon-Offset Options of Asian Styles on the Basis of Jump Diffusions and Fractal Brownian Motions

We extend the geometric-Brownian-motion assumption of [24] (pp. 640–641), impose jumps for the underlying asset, and formulate the following fractal Brownian motions with jump diffusions for the asset (especially carbon-emission allowances):

where

- is the expectation (as documented by [29] (p. 323)).

- is the volatility (as documented by [29] (pp. 323–324)).

- On a probability space , we define as a fractal Brownian motion (as documented by [29] (pp. 329–330)) with the Hurst exponent with the following property:For , retreats to Brownian motions.

- We inherit the formulation of [27] (pp. 128–129) and establish as a Poisson process. is the expected jump numbers per unit time.

- We enrich the jump diffusions by erecting as the jump multitude. comes from the following log-normal distribution:The distribution is fixed by the variance and expectation as follows:We denote the expectation of as follows:

- At time t, if jumps with probability , assumes 1 (i.e., ) in time interval for sufficiently small . For term of (2), the underlying asset’s price changes by .Otherwise (i.e., does not jump at time t with probability ), assumes 0 (i.e., ) in time interval . For term of (2), the underlying asset’s price does not change. In summary, we reiterate in time interval as follows:

- Stochastic processes , , and are mutually independent at any time t.

- At last, we pursue [24] (pp. 640–641) and assume the following conditions:

- (a)

- continuous-time option trading,

- (b)

- no-arbitrage opportunity,

- (c)

- identical borrowing and lending interest rate r,

- (d)

- short-sales feasibility,

- (e)

- no dividend during the option life, and

- (f)

- frictionless markets in the form of no transaction cost or tax.

3.2. Verifying the Stochastic Differential Equation and Boundary Conditions

Traditionally for options based on geometric Brownian motions, Ref. [29] (p. 349) instructs the following stochastic differential equation for the option value :

Investors resolve a specific option by the boundary conditions for (7). For instance, the condition for European call options on maturity T with exercise price K is as follows:

Because we have already extended geometric Brownian motions into fractal Brownian motions and appended jump diffusions in (2), we correspondingly reckon the counterpart of (7) in this subsection. Of course, the counterpart is much more complicated.

The option value depends on , , and t as follows:

We then augment (7) in the following theorem:

Theorem 1.

Proof of Theorem 1.

- We exploit dynamic-hedging strategies (as outlined by [29] (pp. 422–423)) and build the following portfolio :where is the weight for . We trail [29] (pp. 422–423) and assign as follows:The value of changes from time t to time as follows:We consult [29] (p. 349) and rewrite the model above as follows:

- For the no-jump case as the simpler situation, we define the event as follows:With , we simplify (2) as follows:On the basis of (9) and (16), we operate fractal Itô’s lemma (as described by [39] (pp. 4814–4816)) to of (10) as follows:We substitute above into (14) as follows:We have already assigned of (13), so the term becomes 0 for (17). By (13)–(17), we develop as follows:For above, we then take the expectation or precisely conditional expectation on as follows:

- For the jump case, we define the event as follows:

- By the no-jump case and jump case, we manipulate total-expectation law (as described by [51] (p. 299)) for as follows:Because [51] (p. 44) posits for sufficiently small , so do we and thus infer as follows:By the zero item above, we advance and rearrange (22) as follows:Because [29] (p. 349 and 422–423) sketches the no-arbitrage opportunity and thus risk-free conditions for of (12) in time interval , earns interest-rate r as follows:

We then decipher the call option and put option by indicating the boundary conditions in the following theorems:

Theorem 2.

Proof of Theorem 2.

By Theorem 1, the call option satisfies (11). The boundary condition is that investors harness the option value on maturity T. □

Theorem 3.

Proof of Theorem 3.

By Theorem 1, the put option satisfies (11). The boundary condition is that investors harness the option value on maturity T. □

4. Pricing the Options

In the following theorems, we strive to analytically reveal the call-option value and put-option value.

Theorem 4.

For the carbon-offset options of (10) of Asian styles based on jump diffusions and fractal Brownian motions, the call-option value of Theorem 2 is approximately calculated as follows:

where

Proof of Theorem 4.

Overall, directly computing the term of Theorem 2 is difficult, so we approximate the term using the Taylor series, substitute variables three times, and reckon the option value in the following steps:

- For the first variable substitution, we substitute by x and substitute by as follows:Of course, x and depend on t. Due to the complex computation below, we suppress t for expression clarity. We total the partial derivatives by the substitution as follows:We transport and into (11) as follows:We focus on of for fixed t and introduce . We operate the following Taylor series with respect to and drop the cubic or higher-moment terms (as traditionally established by [52] (p. 10)):We then take the expectation of (27) as follows:By (3), (4), and (25), we recognize the expectation of as and recognize the variance of as . We gauge as follows:We substitute and into (28) as follows:By (25), we reexpress the boundary condition of Theorem 2 as follows:

- For the second variable substitution, we perform the following substitution in order to simplify (30):We calculate the following partial derivatives:

- For the third variable substitution, we follow [14] and introduce the following substitution:We will configure , , and later in this step. We presume . By (38), we reexpress the boundary condition (35) as follows:Moreover, by (38), we compute the following partial derivatives:We bring the partial derivatives above into (36) as follows:By (40), we demand the following equations:Equation (45) is a heat equation (as described by [53] (p. 254)). By (34) and (38), we usher in and (as dictated in Theorem 4) as follows:Ref. [53] (p. 254) crack the heat equation and we borrow their solution as follows:We take and calculate as follows:We take and calculate as follows:

- At last, we revert the three-round variable substitutions (25), (34), and (38) back to (10) as follows:We relocate (44) and (51) to (52) and obtain the pricing formula in Theorem 4 as follows:

Theorem 5.

For the carbon-offset options of (10) of Asian styles based on jump diffusions and fractal Brownian motions, the put-option value of Theorem 3 is approximately calculated as follows:

Proof of Theorem 5.

Overall, we follow the computations and steps of the proof of Theorem 4 as follows:

- For the first variable substitution, we exactly follow step 1 of the proof of Theorem 4.

- For the second variable substitution, we still perform (34) and rewrite the boundary condition of Theorem 3 as follows:We still designate (37).

- For the third variable substitution, we still perform (38), obtain (42)–(44), and configure the following heat equationWe define and calculate as follows:We define and calculate as follows:

5. Illustrations

In this section, we postulate the following option parameters and dissect the parameter sensitivity by individually attuning one parameter:

where the Hurst exponent H is set in the parameter range of [39]. For default parameter assumptions, see [17] (p. 5) for setting the exercise price K and the interest-rate r. See ref. [22] (p. 455) for the setting range of the expectation and volatility of underlying asset prices.

At the beginning with time , we calculate the call-option value of Theorem 4 as follows:

We also calculate the put-option value of Theorem 5 as follows:

By (57) and the parameters above, we calculate the call-option value at time as follows:

By (58) and the parameters above, we calculate the put-option value at time as follows:

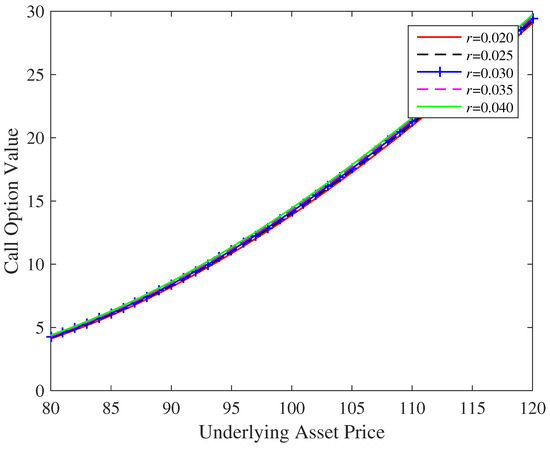

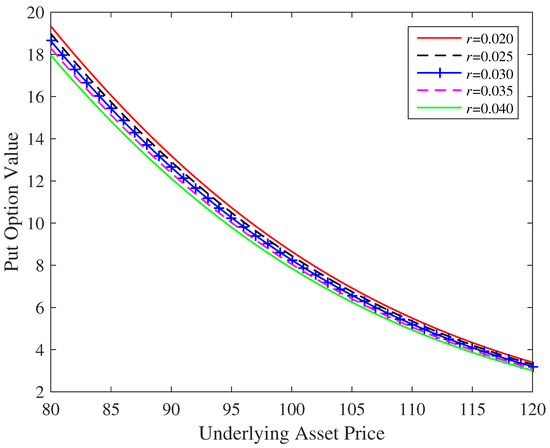

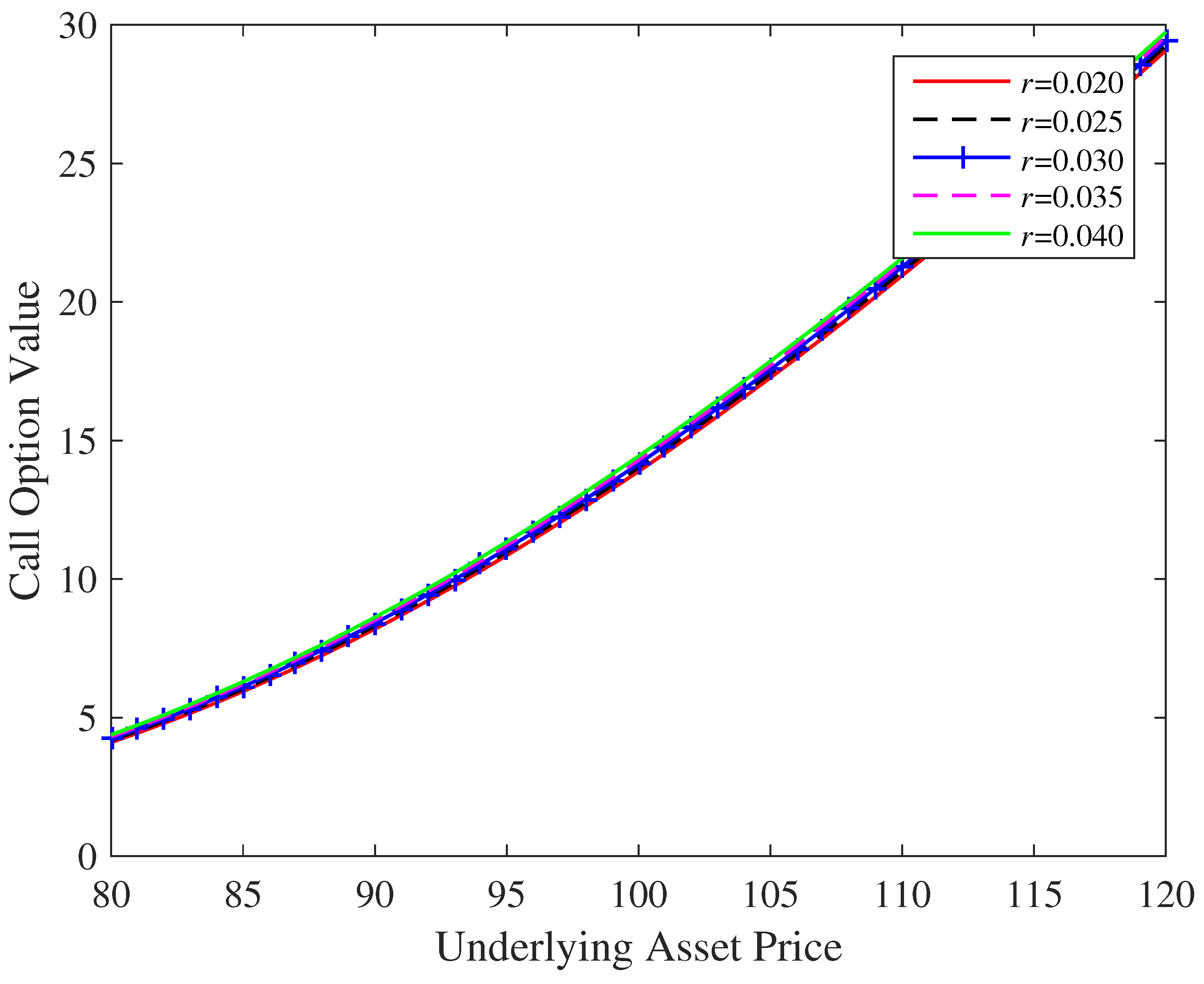

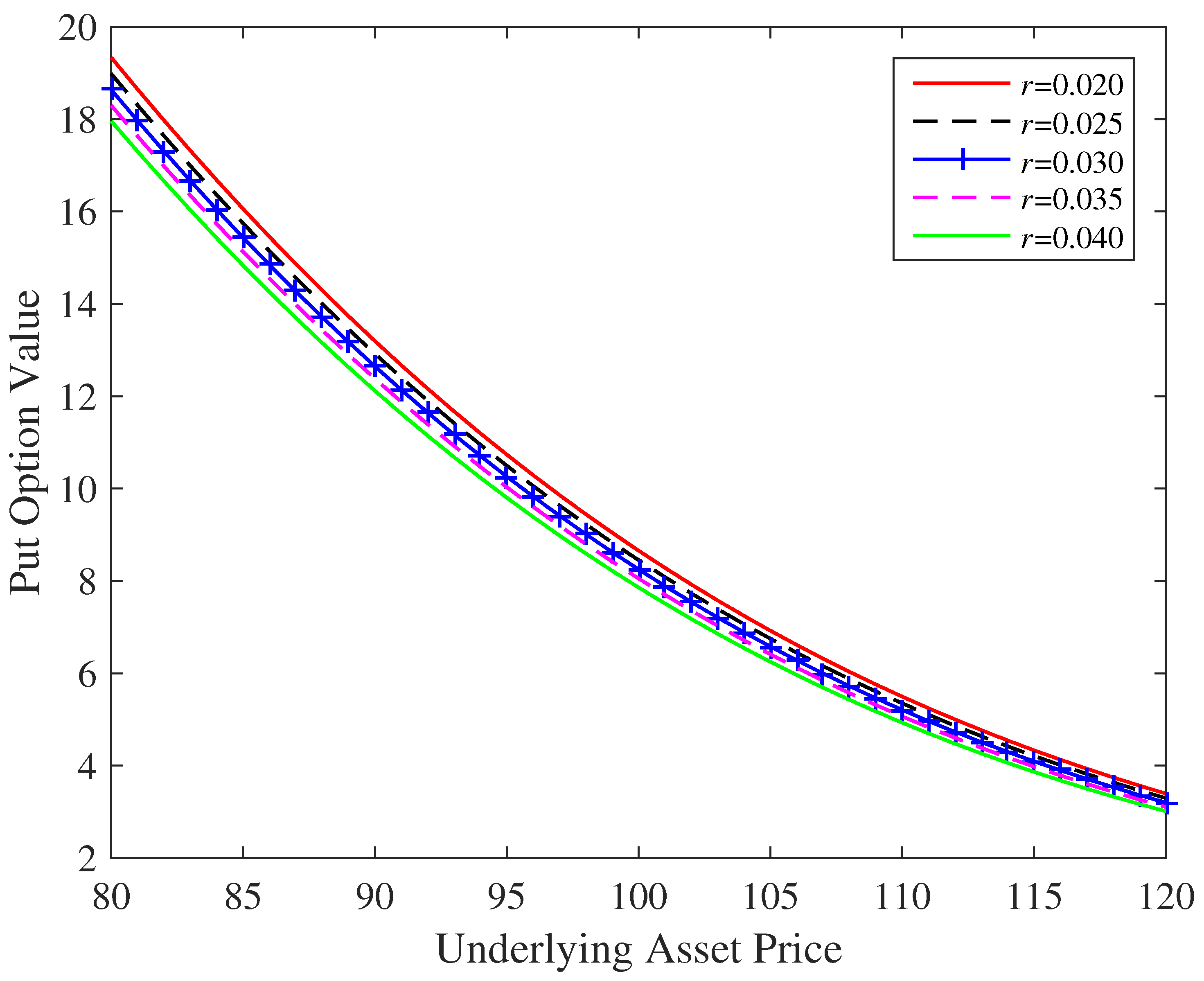

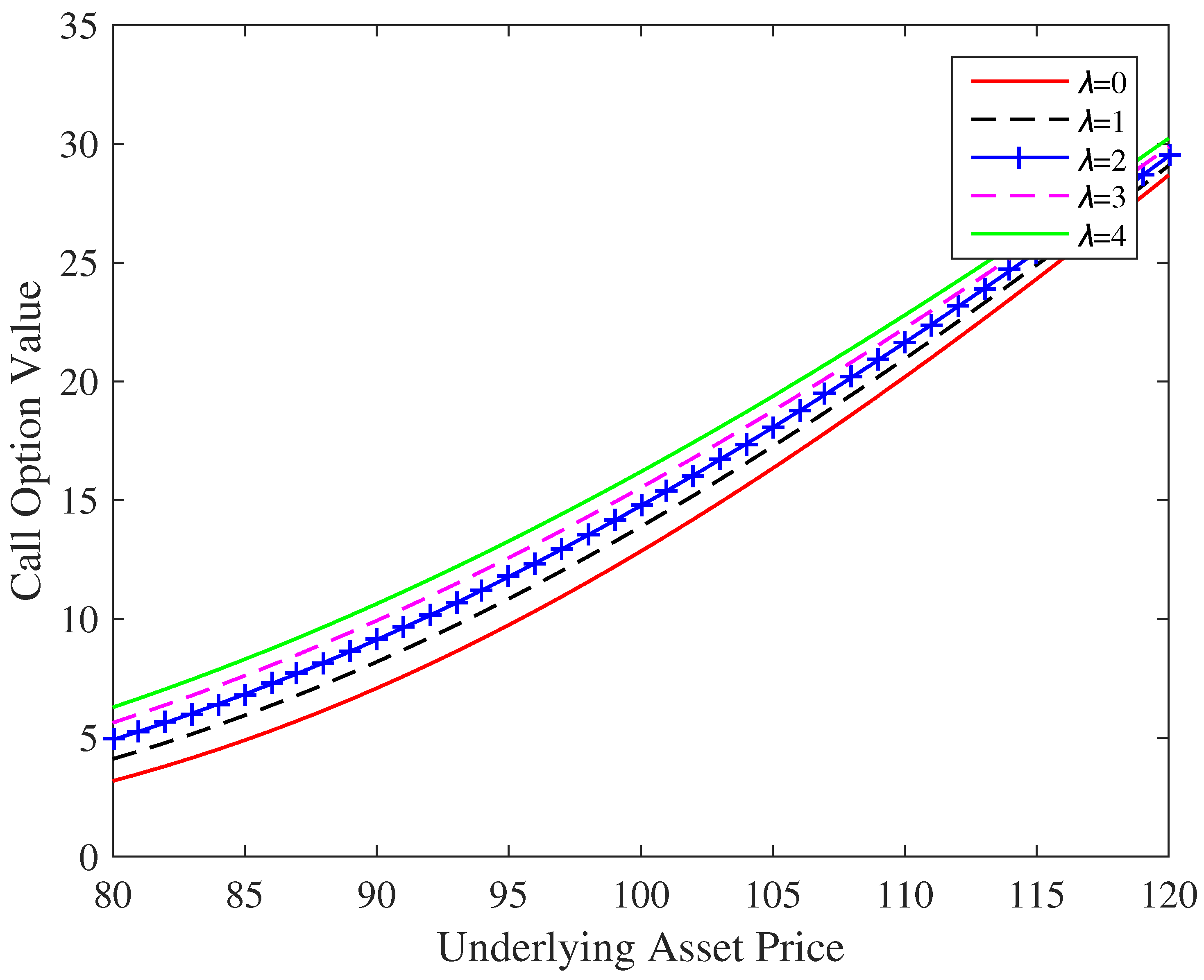

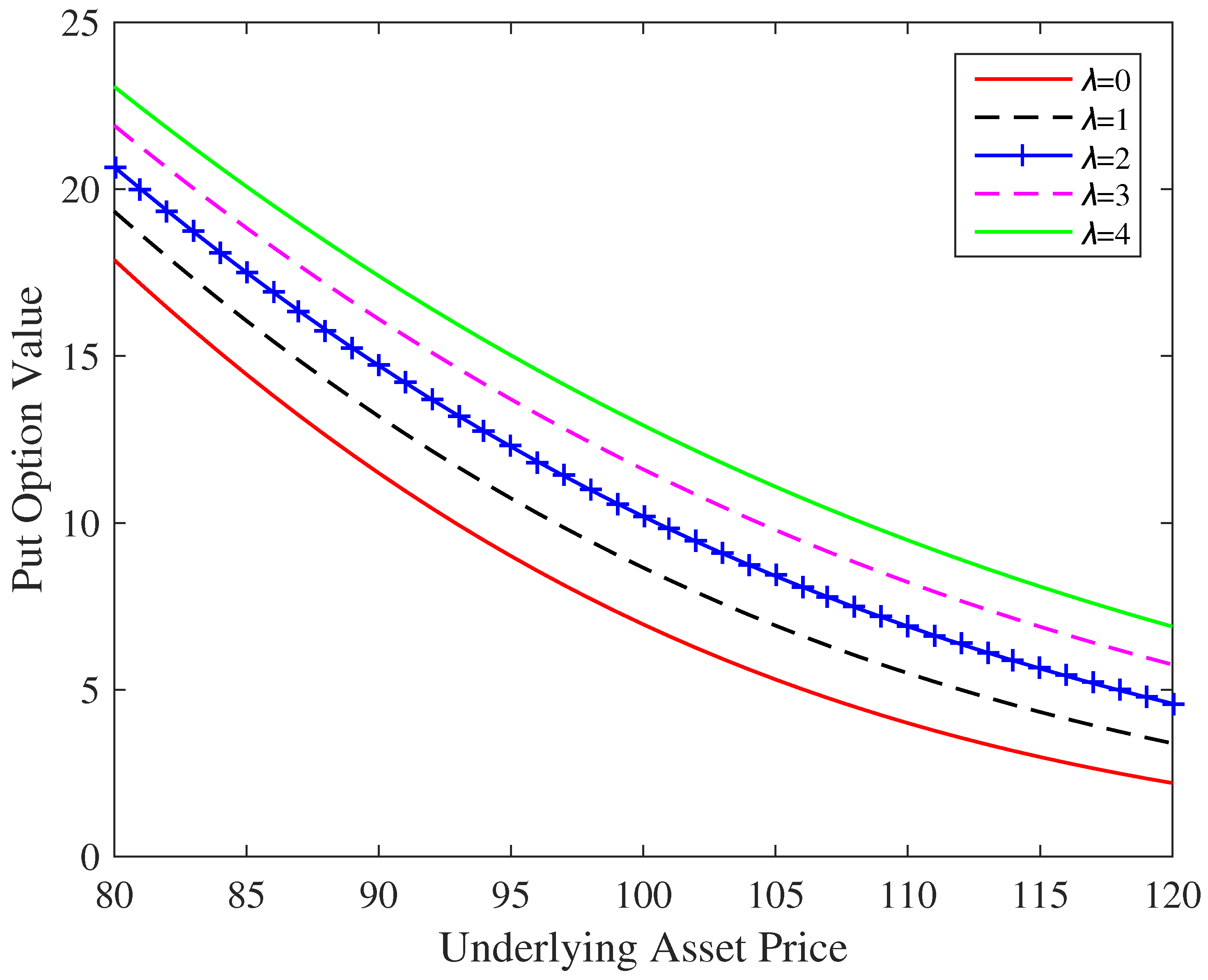

We then modify interest rate r by , , , , and but hold other parameters of (56) unchanged. We depict the effect on the call-option value in Figure 2. We illustrate the underlying asset price (2) at time in the horizon axis and the option value (57) at time in the vertical axis. We portray the value for by a solid red curve and the value for by a solid green curve. Under the same figure format, we depict the effect on the put-option value (58) at time in Figure 3.

Figure 2.

Modifying interest rate r and observing the effect on the call-option value.

Figure 3.

Modifying interest rate r and observing the effect on the put-option value.

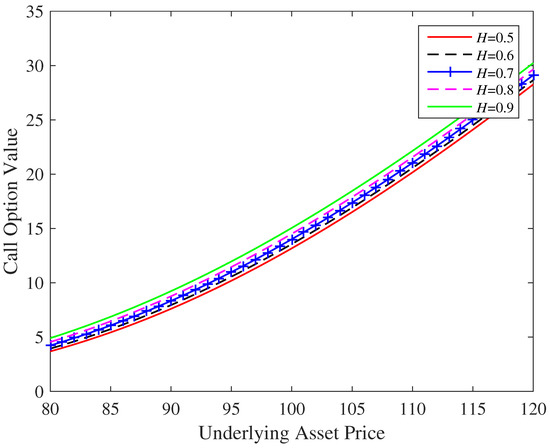

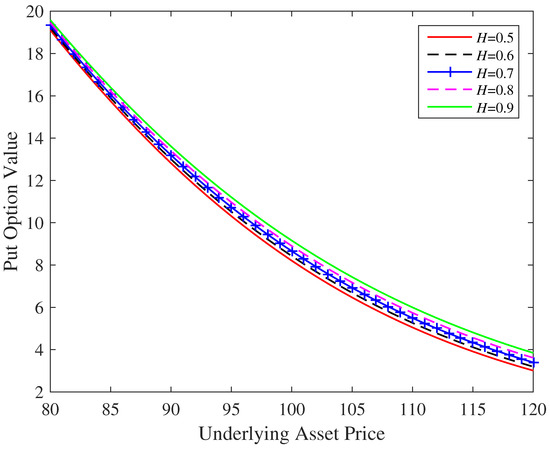

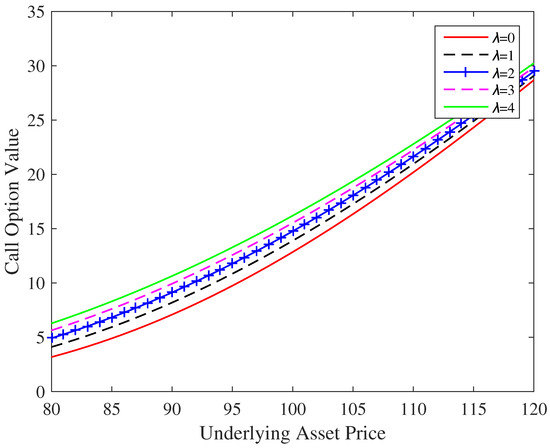

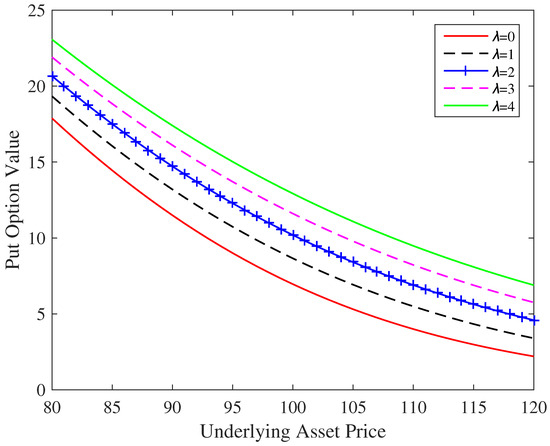

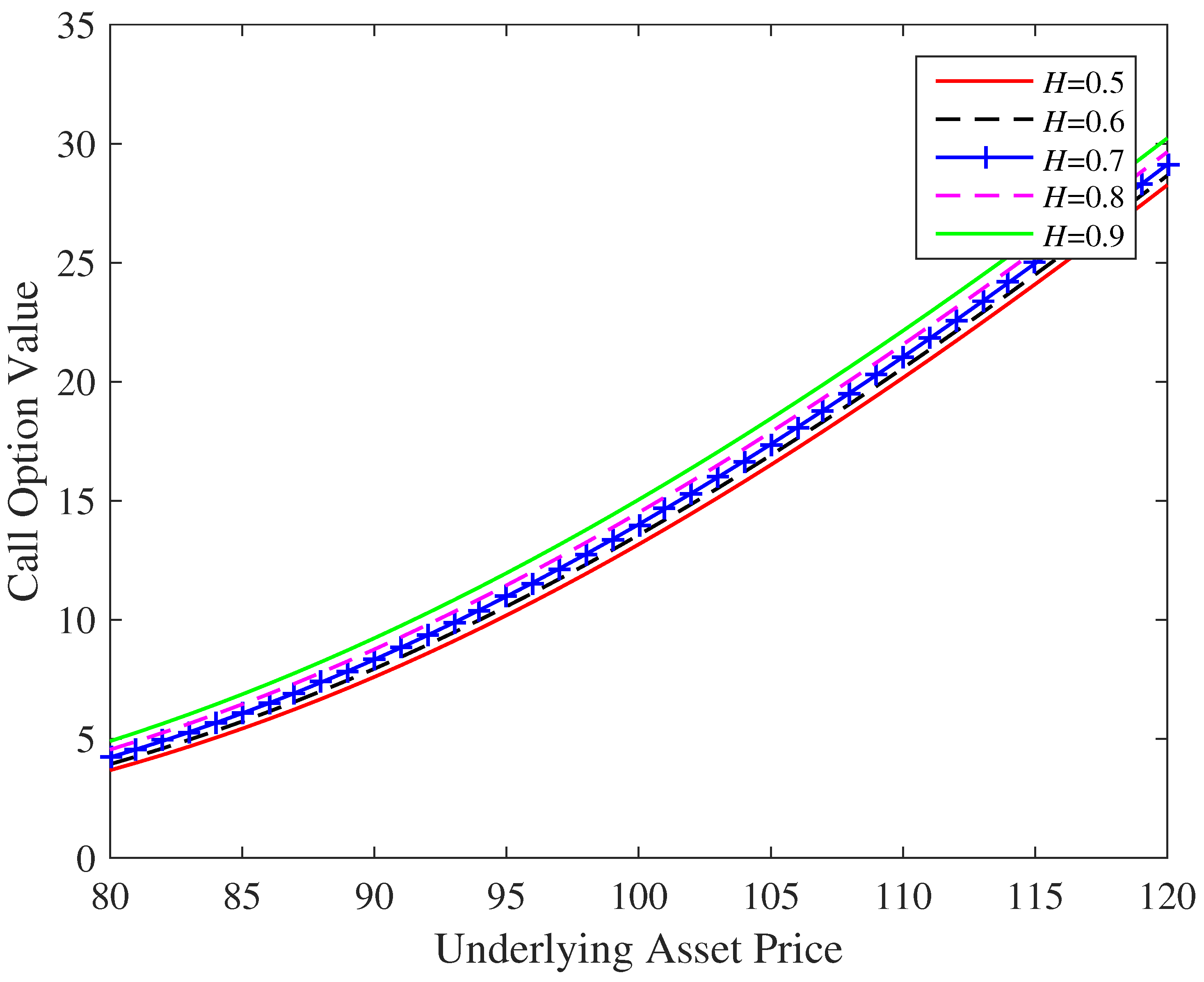

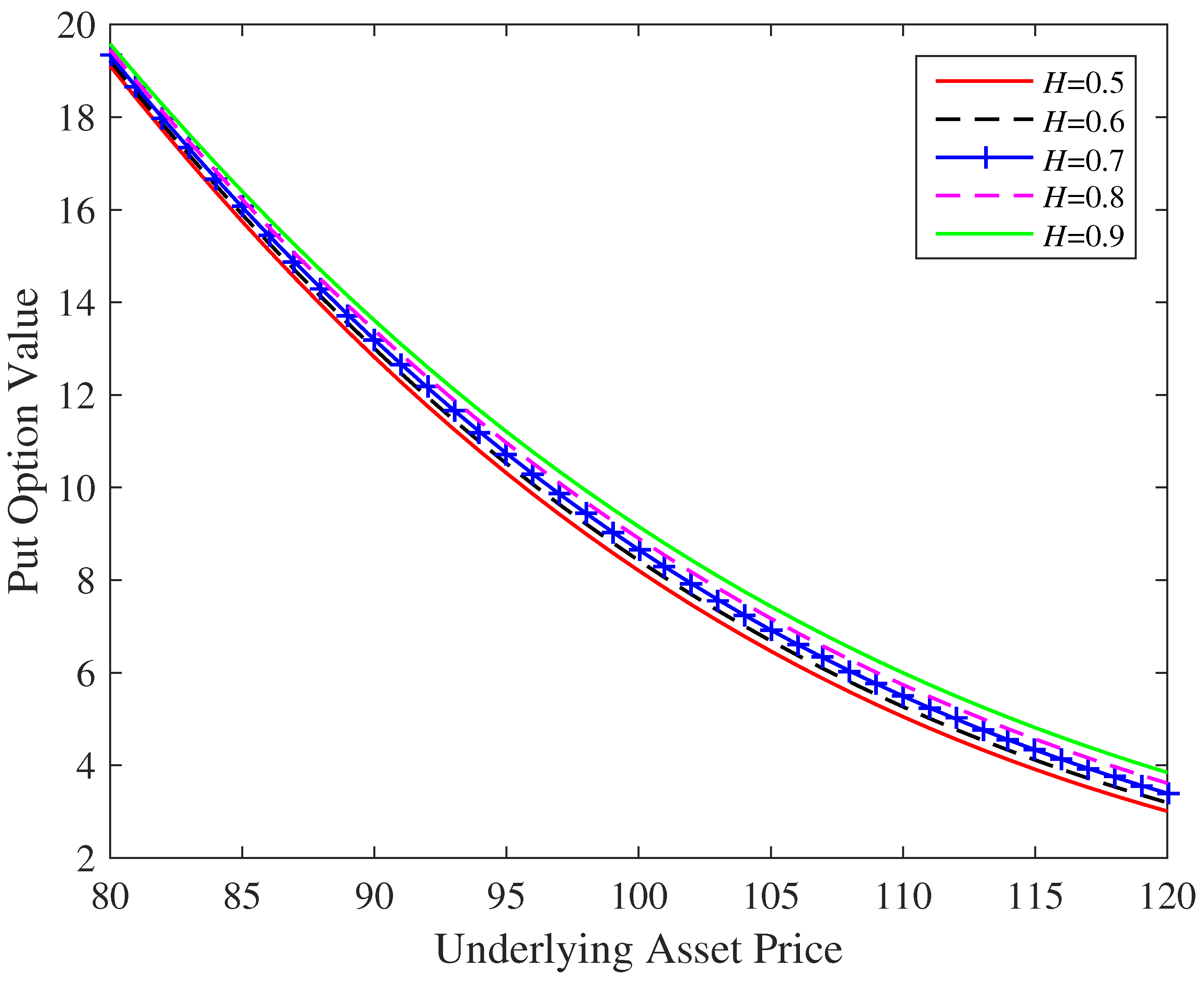

Under the same figure format, we also modify Hurst exponent H and depict the effect on the call-option value and on the put-option value in Figure 4 and Figure 5. Furthermore, we modify expected jump numbers and depict the effect on the call-option value and on the put-option value in Figure 6 and Figure 7.

Figure 4.

Modifying Hurst exponent H and observing the effect on the call-option value.

Figure 5.

Modifying Hurst exponent H and observing the effect on the put-option value.

Figure 6.

Modifying expected jump numbers and observing the effect on the call-option value.

Figure 7.

Modifying expected jump numbers and observing the effect on the put-option value.

We have deposited the data and codes for this paper at Harvard Dataverse https://doi.org/10.7910/DVN/O4VXBD.

6. Conclusions

6.1. Future Directions

In future studies, we can design the terms of carbon-offset option contracts based on underlying assets such as the carbon-emission allowance or the carbon-neutral index, including the contract type, expiration date, strike price, and other terms of the carbon-offset option, to provide a reference for launching carbon options in the carbon-emission trading market. In addition, we can also analyze the time series of the underlying asset price of carbon-offset options based on the historical data from the carbon-emission trading market, estimate the volatility of carbon-offset options through the GARCH model, and then use our pricing model to calculate the initial price of carbon-offset option contracts.

6.2. Concluding Remarks

Our Asian-style carbon-offset option-pricing model considers the fractal and jump characteristics of carbon financial underlying assets and provides a theoretical reference for pricing. With the implementation of the double carbon policy, the carbon-emission trading market can explore carbon-offset option financial derivatives, improve market activity, and enrich the trading variety system.

Author Contributions

Conceptualization, Y.Q.; methodology, Y.W.; software, Y.W.; validation, Y.Q. and Y.W.; formal analysis, Y.Q.; data curation, Y.W.; writing—original draft preparation, Y.Q. and Y.W.; writing—review and editing, Y.Q.; supervision, Y.Q. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data and codes that support the illustrations of this study are available from Harvard Dataverse. These data were obtained from the following resources available in the public domain: https://doi.org/10.7910/DVN/O4VXBD. The data were accessed on 16 March 2022.

Acknowledgments

We would very much like to thank four anonymous referees for their highly constructive comments. Yue Qi thanks Ralph E. Steuer at the University of Georgia, USA, for his constant support.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Khan, M.K.; Khan, M.I.; Rehan, M. The relationship between energy consumption, economic growth and carbon dioxide emissions in Pakistan. Financ. Innov. 2020, 6, 1. [Google Scholar] [CrossRef]

- Wei, Y.; Gong, P.; Zhang, J.; Wang, L. Exploring public opinions on climate change policy in “Big Data Era”—A case study of the European Union Emission Trading System (EU-ETS) based on Twitter. Energy Policy 2021, 158, 112559. [Google Scholar] [CrossRef]

- Fan, Y.; Wu, J.; Xia, Y.; Liu, J. How will a nationwide carbon market affect regional economies and efficiency of CO2 emission reduction in China? China Econ. Rev. 2016, 38, 151–166. [Google Scholar] [CrossRef]

- Mo, J.; Agnolucci, P.; Jiang, M.; Fan, Y. The impact of Chinese carbon emission trading scheme (ETS) on low carbon energy (LCE) investment. Energy Policy 2016, 89, 271–283. [Google Scholar] [CrossRef]

- Li, Y.; Wu, M.; Li, Z. A Real Options Analysis for Renewable Energy Investment Decisions under China Carbon Trading Market. Energies 2018, 11, 1817. [Google Scholar] [CrossRef]

- Yu, S.; Li, Z.; Wei, Y.; Liu, L. A real option model for geothermal heating investment decision making: Considering carbon trading and resource taxes. Energy 2019, 189, 116252. [Google Scholar] [CrossRef]

- Kim, K.; Lee, D.; An, D. Real Option Valuation of the R&D Investment in Renewable Energy Considering the Effects of the Carbon Emission Trading Market: A Korean Case. Energies 2020, 13, 622. [Google Scholar]

- Liu, Z.; Huang, S. Carbon option price forecasting based on modified fractional Brownian motion optimized by GARCH model in carbon emission trading. N. Am. J. Econ. Financ. 2021, 55, 101307. [Google Scholar] [CrossRef]

- Liu, J.; Zhang, Z.; Yan, L.; Wen, F. Forecasting the volatility of EUA futures with economic policy uncertainty using the GARCH-MIDAS model. Financ. Innov. 2021, 7, 76. [Google Scholar] [CrossRef]

- Zhou, K.; Li, Y. Carbon finance and carbon market in China: Progress and challenges. J. Clean. Prod. 2019, 214, 536–549. [Google Scholar] [CrossRef]

- Li, K. The effect of option trading. Financ. Innov. 2021, 7, 65. [Google Scholar] [CrossRef]

- Willems, S. Asian option pricing with orthogonal polynomials. Quant. Financ. 2019, 19, 605–618. [Google Scholar] [CrossRef]

- Wang, L.; Zhang, R.; Yang, L.; Su, Y.; Ma, F. Pricing geometric Asian rainbow options under fractional Brownian motion. Phys. A Stat. Mech. Its Appl. 2018, 494, 8–16. [Google Scholar] [CrossRef]

- Guo, Z.; Wang, X.; Zhang, Y. Option pricing of geometric Asian options in a subdiffusive Brownian motion regime. AIMS Math. 2020, 5, 5332–5343. [Google Scholar] [CrossRef]

- Zhang, S.; Gao, X. An asymptotic expansion method for geometric Asian options pricing under the double Heston model. Chaos Solitons Fractals 2019, 127, 1–9. [Google Scholar] [CrossRef]

- Hsu, C.C.; Lin, C.G.; Kuo, T.J. Pricing of Arithmetic Asian Options under Stochastic Volatility Dynamics: Overcoming the Risks of High-Frequency Trading. Mathematics 2020, 8, 2251. [Google Scholar] [CrossRef]

- Wang, Y.; Wang, J. Pricing of American Carbon Emission Derivatives and Numerical Method under the Mixed Fractional Brownian Motion. Discret. Dyn. Nat. Soc. 2021, 2021, 6612284. [Google Scholar] [CrossRef]

- Chevallier, J. Carbon futures and macroeconomic risk factors: A view from the EU ETS. Energy Econ. 2009, 31, 614–625. [Google Scholar] [CrossRef]

- Zou, S.; Zhang, T. Multifractal detrended cross-correlation analysis of the relation between price and volume in European carbon futures markets. Phys. A Stat. Mech. Its Appl. 2020, 537, 122310. [Google Scholar] [CrossRef]

- Kusumahadi, T.A.; Permana, F.C. Impact of COVID-19 on global stock market volatility. J. Econ. Integr. 2021, 36, 20–45. [Google Scholar] [CrossRef]

- Zaremba, A.; Kizys, R.; Aharon, D.Y. Volatility in international sovereign bond markets: The role of government policy responses to the COVID-19 pandemic. Financ. Res. Lett. 2021, 43, 102011. [Google Scholar] [CrossRef] [PubMed]

- Chesney, M.; Taschini, L. The Endogenous Price Dynamics of Emission Allowances and an Application to CO2 Option Pricing. Appl. Math. Financ. 2012, 19, 447–475. [Google Scholar] [CrossRef]

- Kim, K.H.; Kim, N.U.; Ju, D.C.; Ri, J.H. Efficient hedging currency options in fractional Brownian motion model with jumps. Phys. A Stat. Mech. Its Appl. 2020, 539, 122868. [Google Scholar] [CrossRef]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Lee, C.; Chen, Y.; Lee, J. Alternative methods to derive option pricing models: Review and comparison. Rev. Quant. Financ. Account. 2015, 47, 417–451. [Google Scholar] [CrossRef]

- Lin, X.; Wang, M.; Lai, C. A modification term for Black-Scholes model based on discrepancy calibrated with real market data. Data Sci. Financ. Econ. 2021, 1, 313–326. [Google Scholar] [CrossRef]

- Merton, R.C. Option pricing when underlying stock returns are discontinuous. J. Financ. Econ. 1976, 3, 125–144. [Google Scholar] [CrossRef]

- Kou, S.G. A jump-diffusion model for option pricing. Manag. Sci. 2002, 48, 1086–1101. [Google Scholar] [CrossRef]

- Hull, J.C. Options, Futures, and Other Derivatives, 11th ed.; Pearson Education Limited: Harlow, UK, 2022. [Google Scholar]

- Arguin, L. A First Course in Stochastic Calculus; American Mathematical Society: Providence, RI, USA, 2022. [Google Scholar]

- Brémaud, P. Probability Theory and Stochastic Processes; Springer Nature: Cham, Switzerland, 2020. [Google Scholar]

- Kirkby, J.L.; Nguyen, D. Efficient Asian option pricing under regime switching jump diffusions and stochastic volatility models. Ann. Financ. 2020, 16, 307–351. [Google Scholar] [CrossRef]

- Mandelbrot, B.B.; Van Ness, J.W. Fractional Brownian Motions, Fractional Noises and Applications. SIAM Rev. 1968, 10, 422–437. [Google Scholar] [CrossRef]

- Hu, Y.; Øksendal, B. Fractional white noise calculus and applications to finance. Infin. Dimens. Anal. Quantum Probab. Relat. Top. 2003, 6, 1–32. [Google Scholar] [CrossRef]

- Li, Z.; Wang, X.T. Valuation of bid and ask prices for European options under mixed fractional Brownian motion. AIMS Math. 2021, 6, 7199–7214. [Google Scholar] [CrossRef]

- Wang, X.; Wang, J.; Guo, Z. Pricing equity warrants under the sub-mixed fractional Brownian motion regime with stochastic interest rate. AIMS Math. 2022, 7, 16612–16631. [Google Scholar] [CrossRef]

- Duncan, T.E.; Hu, Y.; Pasik-Duncan, B. Stochastic calculus for fractional Brownian motion I. Theory. SIAM J. Control Optim. 2000, 38, 582–612. [Google Scholar] [CrossRef]

- Sottinen, T.; Valkeila, E. On arbitrage and replication in the fractional Black-Scholes pricing model. Stat. Decis. 2003, 21, 137–151. [Google Scholar] [CrossRef]

- Lv, L.; Ren, F.Y.; Qiu, W.Y. The application of fractional derivatives in stochastic models driven by fractional Brownian motion. Phys. A Stat. Mech. Its Appl. 2010, 389, 4809–4818. [Google Scholar]

- Han, Y.; Li, Z.; Liu, C. Option pricing under the fractional stochastic volatility model. ANZIAM J. 2021, 63, 123–142. [Google Scholar]

- Chang, Y.; Wang, Y.; Zhang, S. Option Pricing under Double Heston Jump-Diffusion Model with Approximative Fractional Stochastic Volatility. Mathematics 2021, 9, 126. [Google Scholar] [CrossRef]

- Guardasoni, C.; Rodrigo, M.R.; Sanfelici, S. A Mellin transform approach to barrier option pricing. IMA J. Manag. Math. 2020, 31, 49–67. [Google Scholar] [CrossRef]

- Pan, D.; Zhou, S.; Zhang, Y.; Han, M. Asian option pricing with monotonous transaction costs under fractional Brownian motion. J. Appl. Math. 2013, 2013, 352021. [Google Scholar] [CrossRef]

- Lamphiere, M.; Blackledge, J.; Kearney, D. Carbon Futures Trading and Short-Term Price Prediction: An Analysis Using the Fractal Market Hypothesis and Evolutionary Computing. Mathematics 2021, 9, 1005. [Google Scholar] [CrossRef]

- Daskalakis, G.; Psychoyios, D.; Markellos, R.N. Modeling CO2 emission allowance prices and derivatives: Evidence from the European trading scheme. J. Bank. Financ. 2009, 33, 1230–1241. [Google Scholar] [CrossRef]

- Hintermann, B. Allowance price drivers in the first phase of the EU ETS. J. Environ. Econ. Manag. 2010, 59, 43–56. [Google Scholar] [CrossRef]

- Li, C.Y.; Chen, S.N.; Lin, S.K. Pricing derivatives with modeling CO2 emission allowance using a regime-switching jump diffusion model: With regime-switching risk premium. Eur. J. Financ. 2016, 22, 887–908. [Google Scholar] [CrossRef]

- Liu, Y.; Tian, L.; Sun, H.; Zhang, X.; Kong, C. Option pricing of carbon asset and its application in digital decision-making of carbon asset. Appl. Energy 2022, 310, 118375. [Google Scholar] [CrossRef]

- Qi, Y. Parametrically computing efficient frontiers of portfolio selection and reporting and utilizing the piecewise-segment structure. J. Oper. Res. Soc. 2020, 71, 1675–1690. [Google Scholar] [CrossRef]

- Li, M.; Liao, K.; Qi, Y.; Liu, T. Constructing Multiple-Objective Portfolio Selection for Green Innovation and Dominating Green Innovation Indexes. Complexity 2022, 2022, 8263720. [Google Scholar] [CrossRef]

- Øksendal, B. Stochastic Differential Equations: An Introduction with Applications, 5th ed.; Springer: Berlin/Heidelberg, Germany, 2000. [Google Scholar]

- Campbell, J.Y. Financial Decisions and Markets: A Course in Asset Pricing, 1st ed.; Princeton University Press: Princeton, NJ, USA, 2018. [Google Scholar]

- Karatzas, I.; Shreve, S.E. Brownian Motion and Stochastic Calculus, 2nd ed.; Springer Science + Business Media: New York, NY, USA, 1991. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).