Abstract

Enterprise resource planning (ERP) systems have become the most important tool for integrating businesses and achieving the “once only” principle in data entry, which contributes to resource efficiency, the enhancement of numerous organizational processes and capabilities, and, ultimately, improved business performance. In this study, we examine the ERP system’s quality as the company’s dynamic capability, contributing to business performance according to the dynamic capability perspective. Thus, we incorporate theoretical mechanisms into the model of the ERP system’s dimensions as a function of financial and non-financial organizational performance. We hypothesized that companies with a better ERP system, with all three dimensions, information, system, and services, will achieve better non-financial and financial performance. The model was tested using primary data collected using a survey method in the environment of a developing country, where the digital transformation of companies is still at a lower level. Structural equation modeling was employed for data analysis, and the results suggest a positive relationship between ERP system quality and both types of organizational business performance. The results indicate that not all dimensions have the same effect. The quality of information and service is particularly important for business performance until the system’s technical characteristics have no significant effect.

1. Introduction

Data have become one of the most valuable organizational resources [1]. The accuracy and timeliness of data and information are important for corporate success [2]. Enterprise Resource Planning (ERP) systems are integrated solutions that manage most of an organization’s activities and cover most of its operations. In 2021, despite the COVID-19 pandemic (or possibly because of the pandemic), the worldwide ERP market was exhibiting a positive trend [3]. ERP systems are arranged modularly and include core modules such as finance, procurement, sales, human resources, and other modules unique to each firm based on the nature of the activity [2]. The ERP software package integrates and optimizes business management activities by utilizing standard business rules and a central repository for all business domains [4]. The ERP system stores processed data in a centralized database, which improves the flow of information between organizational departments [2]. EPR systems are regarded as one of the most important transformations in the past for maximizing organizational efficiency and productivity [5]. ERP benefits include revenue increase, cost reduction, market value improvement [6], productivity [7], decision-making quality [4], and other organizational processes. ERP systems enable transparent information flow within a company’s ecosystem, which improves supply chain efficiency [8].

The value of ERP for business is generally treated as the value of investing in information technology (IT) in general. The relationship between IT investment in general and business performance has been extensively analyzed, with varying results. There are numerous explanations for the impact of information technology on performance. First, some studies have confirmed a direct relationship between IT and business performance [9]. Second, the impact of IT is determined by analyzing the effect on business processes such as turnover ratios, inventory turnover, and customer service [10]. Then, certain analyses confirm that the firm’s overall performance is determined by combining these process measures. In other words, IT can directly affect a company’s business performance. Still, it can also have an indirect effect via measures of business processes, i.e., IT strengthens the individual functional capabilities of the company, resulting in improved business performance.

Hence, although the relationship between ERP and organizational performance has been studied for many years, both theorists and practitioners continue questioning the cost-effectiveness of investing in ERP. ERP can have a significant impact on enterprise performance, according to some studies [11,12], while cloud ERP has a relatively minor impact on enterprise performance, according to others [13]. Moreover, since ERP quality is commonly a multidimensional construct, the question arises as to whether each dimension of ERP quality contributes equally to organizational performance. Consequently, this study analyzes the relationship between ERP quality and organizational performance, considering the various dimensions of ERP quality.

In this way, the study’s results not only shed light on the relationship between ERP quality and organizational business performance but also highlight the significance of the ERP system’s dimensions. Therefore, the results indicate what needs to be considered regarding ERP to positively impact the organization’s financial and non-financial performance. In addition, this paper examines the impact of various ERP system quality dimensions on financial and non-financial performance.

2. Literature Review

ERP is a package of computer programs that help businesses integrate and improve their management procedures. ERP systems rely on standardized business rules and provide a central repository for all aspects of a company’s operations. An organization’s ERP systems necessitate a high level of coordination and a complex technological infrastructure. Large organizations worldwide have implemented ERP systems a long time ago, whereas small and medium-sized businesses, particularly in developing nations, lag [14]. ERP, as its name suggests, is an integrated system that satisfies the information demands of the entire organization by integrating data from several departments into a single system and database, allowing the “once only” principle to be realized. By integrating information flows and corporate processes, enterprise resource planning (ERP) solutions promote operational efficiency and process transformation [14].

This study observes the quality of ERP systems through three dimensions [4,15]:

- ERP information quality;

- ERP system quality;

- ERP service quality.

The semantic quality of the outputs produced by the information system is what is meant when referring to ERP information quality. From the user’s perspective, information quality can be understood as the data responsive to the user’s needs and requirements [4].

ERP system quality reflects a computerized system capacity and information processing quality, including how well it meets technical requirements [4].

ERP service quality is the divergence between clients’ normative expectations and their perceived service performance provided by information system (IS) technical assistance [4,16].

Regarding ERP systems, the literature acknowledges the direct impact of ERP capabilities on business performance and the indirect impact via other organizational capabilities [8]. When businesses strive to align their strategic needs with the ERP system, the ERP system can contribute more to business performance [10]. ERP implies a change in the operational functioning of the organization and integrates processes and functions to create a more flawless, efficient, and transparent way of conducting business [17]. However, it is important to note that the ERP system should be chosen following the organizational process requirements, as failure to do so can result in significant resource waste.

3. Hypotheses Development

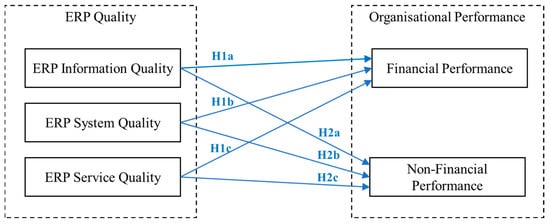

Figure 1 presents the research model and hypothesis, which are elaborated in the next two sections.

Figure 1.

Research model and hypothesis.

3.1. ERP Quality and Organizational Financial Performance

Adopting information technology can accomplish various organizational objectives and help organizations achieve superior financial outcomes relative to their competitors [14,18,19]. Implementing integrated IT solutions, such as ERP, can help the company achieve numerous financial benefits at the level of organizational units and departments and the entire enterprise.

The financial performance of an organization can be evaluated through several parameters that can be categorized into two major categories: financial parameters related to profitability and sales and financial parameters related to costs and savings. It is important to mention that the impact of ERP system implementation on financial performance is frequently not evident in the short term, but that these IT solutions’ medium- and long-term effects on a company’s operations become apparent [20,21]. Typically, only the costs of purchasing and implementing the system are visible in the short term. In contrast, the true impact of the ERP system on the organization’s financial performance is evident in the long term.

The relationship between ERP quality and organizational financial performance in terms of profitability and sales is most often observed through four parameters—return on investment (ROI), return on assets (ROA), return on sales (ROS) and stock returns.

The results of previous research show that ROI, ROA, ROS and stock returns had a downward trend in the short term after the ERP implementation, which was one of the main reasons why some organizations decided to stop the implementation of ERP systems and integrated business practices [14]. This is a very common case in small and medium-sized enterprises that enter the process of reengineering their business processes with insufficient resources, knowledge and/or experience [22]. However, companies that withstood the initial decline in profitability recorded significant improvements in the medium and long term of these financial parameters and achieved a significant competitive advantage over their competitors who did not implement the ERP system in their business [23]. Some companies have also noticed that ERP contributes to profitability by accurately calculating profit margins and price invoicing.

Still, the results are a little different regarding the ERP. Often, ROI and ROA calculations do not financially justify an ERP investment, especially if immediate returns are sought. Namely, the implementation of ERP does not give an immediate return [14], but the ROI and ROA are recorded during the combined period of implementation and the period after implementation [24].

When it comes to financial parameters related to costs and savings, the situation is different. ERP quality contributes to the reduction in various costs of the company, such as administrative costs, procurement costs, costs of storage and warehousing, etc. Some examples are mentioned below.

One of the most frequently mentioned advantages of these systems is that they lead to the automation of repetitive tasks, which achieves significant savings in terms of labor costs that can be reallocated to other jobs and tasks [25]. Then, by establishing an integrated system, it is possible to create a better inventory planning and monitoring system, which reduces general, administrative and procurement costs [19]. In addition, it can be added that better financial planning leads to better resource management in general [25,26]. We hypothesize, based on the preceding discussion and theoretical assumptions, that the quality of the ERP system contributes to the financial performance of the company:

H1.

The quality of the ERP system positively affects the organization’s financial performance.

Following this preceding rationale and intending to test the impact of ERP system quality dimensions on financial business performance, the model assumes the following hypotheses:

H1a.

The ERP information quality positively affects the organization’s financial performance.

H1b.

The ERP system quality positively affects the organization’s financial performance.

H1c.

The ERP service quality positively affects the organization’s financial performance.

3.2. ERP Quality and Organizational Non-Financial Performance

From the very beginning of introducing ERP systems, organizations strive to increase their market agility, organizational structure, and business approach through these systems. In addition to the previously discussed effects of ERP quality on financial performance, there are numerous examples of ERP’s effects on non-financial performance.

Quantifying the realized benefits is one of the greatest challenges in determining the impact of ERP on the non-financial performance of an organization. The non-financial benefits of an ERP system can be divided based on the current and future benefits.

Current benefits may stem from issues such as process improvements, workflow and access to information [27]. Future benefits of an ERP system for an organization can be based on the customer service they can deliver to the end-user [19], which has higher quality and customer support.

Ref. [28] argue that non-financial benefits can be viewed through three key dimensions: (1) strategic, managerial, and operational benefits; (2) process benefits, customer benefits, financial and innovation benefits; (3) advantages in terms of IT and organizational infrastructure development.

When we consider the first dimension of non-financial benefits, we see that within this dimension fall several changes that the implementation of ERP systems brings. For example, the implementation of an ERP system can contribute to (1) changes in work patterns and changes in the focus of certain jobs; (2) building shared visions at the level of organizational units and the entire organization; (3) change in work focus and concentration on core work; (4) improved decision-making system [29].

Within the second dimension of non-financial benefits, researchers often state that ERP quality contributes to a reduced number of customer complaints by creating a platform for more interactive customer service. The organization can improve its service quality through this platform and provide customers with direct feedback [19]. One of the non-financial benefits often forgotten is the increased morale and employee satisfaction resulting from increased work efficiency and productivity [30]. In addition, it is possible to establish and/or facilitate the business learning process and enable employees to improve their skills, knowledge, and competencies. It is also important to emphasize that employees have more time to dedicate to clients and their problems, given that administrative and repetitive tasks are automated through the ERP system.

Finally, the third dimension of non-financial benefits includes the benefits of developing IT and organizational infrastructure. Through a well-implemented ERP system, organizations can empower their employees to be more proactive and provide a faster response to change to shorten the process cycle. In addition, IT infrastructure is the basis for establishing and maintaining ERP systems, and therefore, the continuous monitoring of IT innovations allows companies to build long-term sustainable competitive advantages [31].

All the non-financial benefits listed pertain to internal processes. In contrast, this study focuses on non-financial benefits, such as customer loyalty, image, reputation, and competitive advantage. Based on the preceding discussion and theoretical assumptions, we hypothesize that the quality of the ERP system contributes to the company’s non-financial performance:

H2.

The quality of the ERP system positively affects the organization’s non-financial performance.

However, to test the impact of dimensions of ERP system quality on non-financial business performance, the model assumes the following hypotheses:

H2a.

The ERP information quality positively affects the organization’s non-financial performance.

H2b.

The ERP system quality positively affects the organization’s non-financial performance.

H2c.

The ERP service quality positively affects the organization’s non-financial performance.

4. Methodology

4.1. Research Instrument

ERP quality, financial performance, and non-financial performance were investigated in this study. Three dimensions were utilized to evaluate ERP quality: ERP information quality, ERP system quality, and ERP service quality. The indicators for the ERP quality scale were taken from [4]. Each financial and non-financial performance is a one-dimensional construct measured by five indicators adopted from [32]. All items were measured on a 7-point Likert scale with 1 representing strong disagreement and 7 representing strong agreement. All measurements were adopted in English and translated into the local language by bilingual academics. Reverse translation ensured the translation’s accuracy.

4.2. Data and Sample

This study included survey-based quantitative research. The context of the study is an economy in transition. The study was conducted in Bosnia and Herzegovina (BiH), where business digitization is lower. In BiH, 26% of companies (Eurostat data for 2021) have integrated internal processes, which is why BiH is positioned almost at the bottom of European countries regarding this indicator.

The respondents were senior-level managers familiar with good insight into the company’s organizational capabilities and performance. Therefore, based on two fundamental criteria—a sufficient level of knowledge and involvement with the concepts that are the subject of the analysis—company presidents and chief executive officers (CEOs) were identified as key respondents [33].

The sample included 217 companies with an average year of existence of 26.7 (sample demographics presented in Table 1). The companies are grouped according to the NACE classification, and most of them are from the manufacturing industry, which is followed by wholesale and retail trade. The information and communication industry comes next, which is followed by construction and other service activities. Regarding export activities, i.e., whether companies export their products outside the country, 35.5% of companies do not have export activities, while 58.5% export their products/services.

Table 1.

Sample demographics.

Following the recommendations for minimal sample sizes based on the model’s complexity and the measurement model’s basic characteristics, the sample size was established. In particular, Ref. [34] suggests a minimum sample size of 150 for models with seven or fewer components and no unidentified constructs (page 633). Five constructs were evaluated in our model, and none of them was nonidentified. In other words, a sample size of 217 is considered sufficient for this model.

4.3. Statistical Analysis

Data analysis was performed using a two-step approach [35]. The measures were first evaluated using confirmatory factor analysis (CFA). The theoretical model and hypotheses were evaluated using structural equation modeling (SEM) [36] using the Mplus software tool.

The degree of consistency between multiple latent construct variables is referred to as reliability. The composite reliability (CR) CFA reliability measure was used to evaluate reliability [34]. CR measures reliability and internal consistency in representing a latent construct by measurement variables. It evaluates whether the given indicators are adequate to represent the corresponding construct [37]. CR greater than 0.70 indicates that the measuring construct is reliable. Convergent validity refers to the extent to which two measures of the same concept are correlated, i.e., share a significant proportion of variance [36]. Convergent validity was determined by examining the value of each variable’s factor loading on the proposed construct [34] and by examining the average variance extracted (AVE), which is the average variance for the item loading on the construct. The value of standardized factor loadings should be greater than 0.50, and AVE greater than 0.5 indicates acceptable convergence [34]. Discriminant validity refers to the extent to which different constructs are distinct, i.e., that a single variable represents only one latent construct. It is checked by comparing the square root of the AVE value of the indicator with the values of the correlation of that with other constructs (the AVE value should be higher) [34]. This analysis confirmed the measurement model’s reliability and validity, allowing hypotheses to be tested. A conceptual model was evaluated using SEM, confirming that the model fits adequately into the data, and then, the path estimates were determined.

5. Results and Discussion

The data screening process showed that the data showed slight deviations from normal, and as a consequence, an estimate of the maximum probability was used [34].

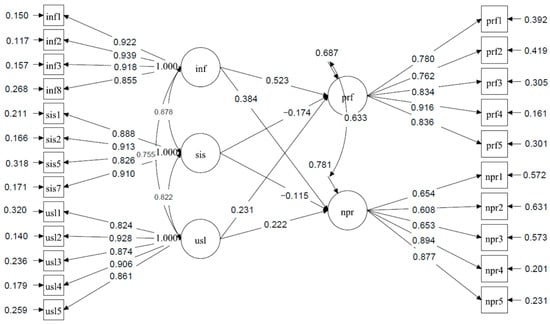

Using CFA, a model with five first-order dimensions was evaluated. Table 2 presents the indicators’ standardized loadings and t-values, showing that all the factor loadings are larger than 0.5, indicating a good fit. This conclusion was confirmed with the additional measures presented in Table 3: χ2[220] = 584.620 (p = 0.000), CFI = 0.924, and RMSEA = 0.087, SRMR = 0.061, TLI = 0.912.

Table 2.

Indicators’ standardized loadings and t-values.

Table 3.

Reliability and validity of the measurement model.

Reliability, convergent, and discriminant validity were evaluated (Table 3). All CR values are greater than 0.7, which confirms the reliability of the measurement model. All items measuring constructs in the model had a high (0.609) and significant factor load (p = 0.000). In addition, AVE values are greater than 0.5, confirming acceptable convergence. Finally, all square roots of AVE values are greater than all correlations between that construct and all other constructs, confirming discriminant validity.

The SEM results supported four of six proposed hypotheses (Table 4).

Table 4.

Hypotheses testing.

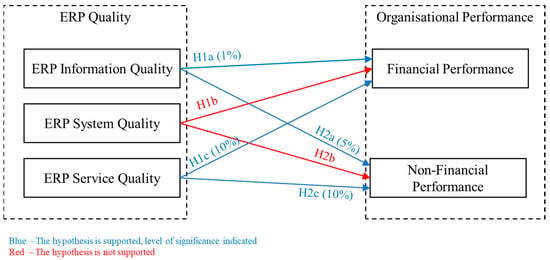

A positive relationship between ERP information quality (INF) and financial business performance (PRF) was established, confirming H1a (β = 0.523, p < 0.01).

Because the estimated structural path between ERP system quality (SYS) and financial performance (PRF) did not yield significant results, we can conclude that hypothesis H1b cannot be supported (β = −0.174, p > 0.1).

It was hypothesized in H1c that there is a positive correlation between the ERP service quality (SRV) and the business’s financial performance (PRF). The findings confirm that the relationship is significant (β = 0.231, p < 0.1), supporting hypothesis H1c.

Hypothesis H2 proposed a positive relationship between ERP system quality and non-financial business performance.

The results revealed that hypothesis H2a is supported by the data (β = 0.384, p < 0.05), confirming the positive impact of ERP information quality (INF) on non-financial organizational performance (NPR).

We can conclude that hypothesis H2b cannot be supported because the estimated structural path connecting ERP system quality (SYS) and non-financial performance (NPR) did not yield significant results (β = −0.115, p > 0.1).

Finally, it was hypothesized in H2c that there is a positive correlation between ERP service quality (SRV) and non-financial performance (NPR), and the results confirm that the relationship is significant (β = 0.222, p < 0.1).

Figure 2 presents the path estimation result presenting the β estimates for the latent variables, and factor loadings for the individual indicators, while Figure 3 presents the conclusion of the research model.

Figure 2.

Path estimation results.

Figure 3.

Research model with the results of hypothesis testing.

This study’s findings shed light on the relationship between ERP system quality dimensions and financial and non-financial business performance. The primary findings indicate that the ERP system’s quality directly impacts financial and non-financial business performance. Regarding the quality dimensions of the ERP system, it is interesting that the quality of information and service contributes to financial and non-financial performance. In other words, if the data in the system correspond to the users’ needs and requirements, and if the company’s technical support meets the users’ normative expectations, the results will be reflected in the company’s business performance. In other words, the system’s technical characteristics do not contribute to the enhancement of business results.

In light of the above discussion, this study concludes that the system itself and its features are not a priority when it comes to business, but rather what the ERP system does for business: namely, provides access to the right information at the right time and that there is adequate support to use the system.

6. Conclusions

This study investigates the relationship between ERP system quality and financial and non-financial organizational performance, considering the impact of distinct dimensions of ERP system quality. The research was conducted in a developing market with a low income. The results indicate that ERP information quality is crucial for financial and non-financial organizational performance. This result is consistent with past research that verified the direct effect of ERP systems on business performance. The underlying rationale is that the quality of ERP systems can be applied to all company departments and greatly impacts their efficiency [38].

However, our research indicates that the system itself and its features have little effect on performance; rather, it is the timeliness and accuracy of the information provided by ERP, as well as the availability of technical support for the operation of ERP, that influences performance. This implies that if the information provided by the ERP system is accurate, timely, and easily understood, and if used in the decision-making process, the results will be evident in both financial and non-financial organizational performance. Then, the quality of ERP service impacts the enhancement of organizational performance. In other words, if employees in the IT department are always available to all company employees for all ERP-related issues, if they provide accurate information, improve the quality of work, resolve employee issues, and deliver what they promise, this will result in improved organizational performance. However, the results indicate that the quality of the ERP system itself has no significant effect on organizational performance. This practically means that if the ERP system always functions as needed, it reacts quickly enough and is stable. Its simplicity does not significantly impact the financial and non-financial performance of the organization. This conclusion confirms the widespread notion that data and information are the foundation of modern business success and the most valuable resource for enterprises [1].

Theoretically, the findings contribute to the ongoing discussion regarding the importance of ERP systems to an organization’s business performance. This study examines, to the best of our knowledge for the first time, the effects of individual ERP system quality dimensions on an organization’s financial and non-financial performance. On this basis, the significance of individual ERP quality dimensions was evaluated. Specifically, the study confirmed that the IT department’s information and services quality is more important than the system’s quality. In terms of the study’s practical implications, the findings highlight the significance of ERP information quality and ERP service quality for the organization’s financial and non-financial performance. Now, more than ever, businesses are attempting to improve their cost-effectiveness and overall performance [13]. Therefore, company managers and executives should be aware of the general benefits of ERP and the individual dimensions of ERP system quality assessment. Managers should also ensure that the IT department is always accessible to all employees to resolve any ERP-related issues.

When interpreting the presented results, it should be kept in mind that the managers were the respondents, since they are most called upon to evaluate the company’s business performance. In this regard, the interpretation that the system itself does not represent an antecedent of a successful business might be different if the operational level employees evaluated the ERP quality. In other words, a multilevel approach to testing the proposed model would significantly contribute to improving the obtained results. In addition, the model was tested in a business environment with a low level of business digitization (economy in transition), so repeating the research in a developed country would certainly contribute to a better understanding of the observed effects of ERP system dimensions on the company’s financial and non-financial performance.

Author Contributions

Conceptualization, A.B. and L.T.; methodology, A.B.; software, A.B.; validation, L.T., E.K. and M.P.-B.; formal analysis, A.B.; investigation, A.B.; data curation, A.B.; writing—original draft preparation, A.B., L.T. and E.K.; writing—review and editing, M.P.-B.; visualization, M.P.-B.; supervision, L.T. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Data available on request due to privacy restrictions.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Dubey, R.; Gunasekaran, A.; Childe, S.J.; Bryde, D.J.; Giannakis, M.; Foropon, C.; Roubaud, D.; Hazen, B.T. Big data analytics and artificial intelligence pathway to operational performance under the effects of entrepreneurial orientation and environmental dynamism: A study of manufacturing organisations. Int. J. Prod. Econ. 2020, 226, 107599. [Google Scholar] [CrossRef]

- Barna, L.-E.; Ionescu, B.; Ionescu-Feleagă, L. The relationship between the implementation of erp systems and the financial and non-financial reporting of organizations. Sustainability 2021, 13, 11566. [Google Scholar] [CrossRef]

- Zerbino, P.; Aloini, D.; Dulmin, R.; Mininno, V. Why enterprise resource planning initiatives do succeed in the long run: A case-based causal network. PLoS ONE 2021, 16, e0260798. [Google Scholar] [CrossRef] [PubMed]

- Ouiddad, A.; Okar, C.; Chroqui, R.; Beqqali Hassani, I. Assessing the impact of enterprise resource planning on decision-making quality: An empirical study. Kybernetes 2020, 50, 1144–1162. [Google Scholar] [CrossRef]

- Raoof, R.; Basheer, M.F.; Javeria, S.; Ghulam Hassan, S.; Jabeen, S. Enterprise resource planning, entrepreneurial orientation, and the performance of SMEs in a South Asian economy: The mediating role of organizational excellence. Cogent Bus. Manag. 2021, 8, 1973236. [Google Scholar] [CrossRef]

- Cañizares, S.M.S.; Ángel, M.; Muñoz, A.; Guzmán, T.L. The relationship between benefits of ERP systems implementation and its impacts on firm performance of SCM. J. Enterp. Inf. Manag. 2009, 22, 722–752. [Google Scholar]

- Beheshti, H.M.; Beheshti, C.M. Improving productivity and firm performance with enterprise resource planning. Enterp. Inf. Syst. 2010, 4, 445–472. [Google Scholar] [CrossRef]

- Ruivo, P.; Johansson, B.; Sarker, S.; Oliveira, T. The relationship between ERP capabilities, use, and value. Comput. Ind. 2020, 117, 103209. [Google Scholar] [CrossRef]

- Alghorbany, A.; Che-Ahmad, A.; Abdulmalik, S.O. IT investment and corporate performance: Evidence from Malaysia. Cogent Bus. Manag. 2022, 9, 2055906. [Google Scholar] [CrossRef]

- Velcu, O. Exploring the effects of ERP systems on organizational performance: Evidence from Finnish companies. Ind. Manag. Data Syst. 2007, 107, 1316–1334. [Google Scholar] [CrossRef]

- Elsayed, N.; Ammar, S.; Mardini, G.H. The impact of ERP utilisation experience and segmental reporting on corporate performance in the UK context. Enterp. Inf. Syst. 2021, 15, 61–86. [Google Scholar] [CrossRef]

- Gupta, S.; Meissonier, R.; Drave, V.A.; Roubaud, D. Examining the impact of Cloud ERP on sustainable performance: A dynamic capability view. Int. J. Inf. Manag. 2020, 51, 102028. [Google Scholar] [CrossRef]

- Jayeola, O.; Sidek, S.; Abdul-Samad, Z.; Hasbullah, N.N.; Anwar, S.; An, N.B.; Nga, V.T.; Al-Kasasbeh, O.; Ray, S. The Mediating and Moderating Effects of Top Management Support on the Cloud ERP Implementation–Financial Performance Relationship. Sustainability 2022, 14, 5688. [Google Scholar] [CrossRef]

- Galy, E.; Sauceda, M.J. Post-implementation practices of ERP systems and their relationship to financial performance. Inf. Manag. 2014, 51, 310–319. [Google Scholar] [CrossRef]

- Gorla, N.; Somers, T.M.; Wong, B. Organizational impact of system quality, information quality, and service quality. J. Strateg. Inf. Syst. 2010, 19, 207–228. [Google Scholar] [CrossRef]

- Hsu, P.F.; Yen, H.J.R.; Chung, J.C. Assessing ERP post-implementation success at the individual level: Revisiting the role of service quality. Inf. Manag. 2015, 52, 925–942. [Google Scholar] [CrossRef]

- Al-Dhaafri, H.; Alosani, M. Integration of TQM and ERP to enhance organizational performance and excellence: Empirical evidence from public sector using SEM. World J. Entrep. Manag. Sustain. Dev. 2021, 17, 822–845. [Google Scholar] [CrossRef]

- Putra, D.G.; Rahayu, R.; Putri, A. The Influence of Enterprise Resource Planning (ERP) Implementation System on Company Performance Mediated by Organizational Capabilities. J. Account. Invest. 2021, 22, 221–241. [Google Scholar] [CrossRef]

- Fernandez, D.; Zainol, Z.; Ahmad, H. The impacts of ERP systems on public sector organizations. Procedia Comput. Sci. 2017, 111, 31–36. [Google Scholar] [CrossRef]

- Sislian, L.; Jaegler, A. ERP implementation effects on sustainable maritime balanced scorecard: Evidence from major European ports. Supply Chain Forum 2020, 21, 237–245. [Google Scholar] [CrossRef]

- Wieder, B.; Booth, P.; Matolcsy, Z.P.; Ossimitz, M.L. The impact of ERP systems on firm and business process performance. J. Enterp. Inf. Manag. 2006, 19, 13–29. [Google Scholar] [CrossRef]

- Bazhair, A.; Sandhu, K. Factors for the Acceptance of Enterprise Resource Planning (ERP) Systems and Financial Performance. J. Econ. Bus. Manag. 2015, 3, 1–10. [Google Scholar] [CrossRef]

- Pattanayak, S.; Roy, S. Synergizing Business Process Reengineering with Enterprise Resource Planning System in Capital Goods Industry. Procedia—Soc. Behav. Sci. 2015, 189, 471–487. [Google Scholar] [CrossRef][Green Version]

- Hendricks, K.B.; Singhal, V.R.; Stratman, J.K. The impact of enterprise systems on corporate performance: A study of ERP, SCM, and CRM system implementations. J. Oper. Manag. 2007, 25, 65–82. [Google Scholar] [CrossRef]

- Lorenc, A.; Szkoda, M. Customer logistic service in the automotive industry with the use of the SAP ERP system. In Proceedings of the 2015 4th International Conference on Advanced Logistics and Transport (ICALT), Valenciennes, France, 20–22 May 2015; pp. 18–23. [Google Scholar] [CrossRef]

- Nicolaou, A.I.; Bhattacharya, S. Organizational performance effects of ERP systems usage: The impact of post-implementation changes. Int. J. Account. Inf. Syst. 2006, 7, 18–35. [Google Scholar] [CrossRef]

- Elgohary, E. The Role of ERP Capabilities in Achieving Competitive Advantage: An Empirical Study on Dakahlia Governorate Companies, Egypt. Electron. J. Inf. Syst. Dev. Ctries. 2019, 85, e12085. [Google Scholar] [CrossRef]

- Eckartz, S.; Daneva, M.; Wieringa, R.; van Hillergersberg, J. A Conceptual Framework for ERP Benefit Classification: A Literature Review; University of Twente: Enschede, The Netherlands, 2009; p. 16. [Google Scholar]

- De Loo, I.; Bots, J.; Louwrink, E.; Meeuwsen, D.; Van Moorsel, P.; Rozel, C. The effects of ERP-implementations on the non-financial performance of small and medium-sized enterprises in the Netherlands. Electron. J. Inf. Syst. Eval. 2013, 16, 101–113. [Google Scholar]

- HassabElnaby, H.R.; Hwang, W.; Vonderembse, M.A. The impact of ERP implementation on organizational capabilities and firm performance. Benchmarking 2012, 19, 618–633. [Google Scholar] [CrossRef]

- Gupta, S.; Qian, X.; Bhushan, B.; Luo, Z. Role of cloud ERP and big data on firm performance: A dynamic capability view theory perspective. Manag. Decis. 2019, 57, 1857–1882. [Google Scholar] [CrossRef]

- Chen, J.-S.; Tsou, H.T.; Huang, A.Y.-H. Service Delivery Innovation. J. Serv. Res. 2009, 12, 36–55. [Google Scholar] [CrossRef]

- Campbell, D.T. The Informant in Quantitative Research Author. Am. J. Sociol. 1955, 60, 339–342. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 8th ed.; Cengage: Andover, Hampshire, UK, 2019. [Google Scholar]

- Anderson, J.C.; Gerbing, D.W. Structural equation modeling in practice: A review and recommended two-step approach. Psychol. Bull. 1988, 103, 411. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Anderson, J.C. An approach for confirmatory measure- ment and structural equation modeling of organizational properties. Manag. Sci. 1987, 3, 525–541. [Google Scholar] [CrossRef]

- Kocaaga, A.S.; Ervural, B.C.; Demirel, O.F. Analysis of the Relationship between Enterprise Resource Planning Implementation and Firm Performance: Evidence from Turkish SMEs. In Proceedings of the International Symposium for Production Research; Springer: Cham, Switzerland, 2018; pp. 724–736. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).