Is Pet Health Insurance Able to Improve Veterinary Care? Why Pet Health Insurance for Dogs and Cats Has Limits: An Ethical Consideration on Pet Health Insurance

{kind=link}

Abstract

:Simple Summary

Abstract

1. Introduction

- The animal’s welfare;

- Clinical problem-solving ability;

- Professionalism;

- Communication skills;

- Working in partnership.

“Some capabilities are considered essential while others are considered as valuable add-ons once the fundamentals are in place. It may be that our clients coming to see the vet that their first priority for their animal is its safety and physiological needs and that once they see those being met, they can then prioritize their own psychological needs”.

“(2) For the purposes of this Act, an animal’s needs shall be taken to include—

- (a)

- (b)

- (c)

- (d)

- (e)

“Care of the animal should take precedence over monetary aspects.[…] There was an expectation among some participants that out of a shared interest for the pet, the veterinarian would work with the client to find a solution if the client could not immediately afford veterinary care. […]Discussions of costs should be initiated upfront.Costs of veterinary care should be placed in a meaningful context.[…] Costs should be discussed within the context of their pet’s health and prognosis, stating, for instance, that “I want the information about cost in the context of what’s a reasonable prognosis.”Client suspicion should be addressed.[…] The most consistent suspicion arose from the conflict between the idea of veterinary medicine as a health-care profession versus a business.”

“Since the 2005 change in the law preventing veterinary surgeons from recommending particular insurance products, we have lost a very useful symbiotic relationship with the insurance industry”(GB) [17].

“[…] [Owners] will no longer have to worry whether or not they can afford the necessary veterinary attention. If an animal is insured by a caring owner for this laudable reason, it frees us to consider only the animal’s health and welfare and ensure we reach an accurate diagnosis and satisfactory conclusion […]”(GB) [4].

2. Methods

“The results are surprising, as various surveys have shown that many consumers are willing to spend significantly more money on meat if it has been produced according to higher animal welfare standards. The results of the present suggest that the observed reality of actual purchasing behavior is more differentiated and complex. The basic willingness to spend more money on such meat in the test for such meat is only pronounced to a limited extent. General statements on willingness to buy should therefore be viewed critically.”

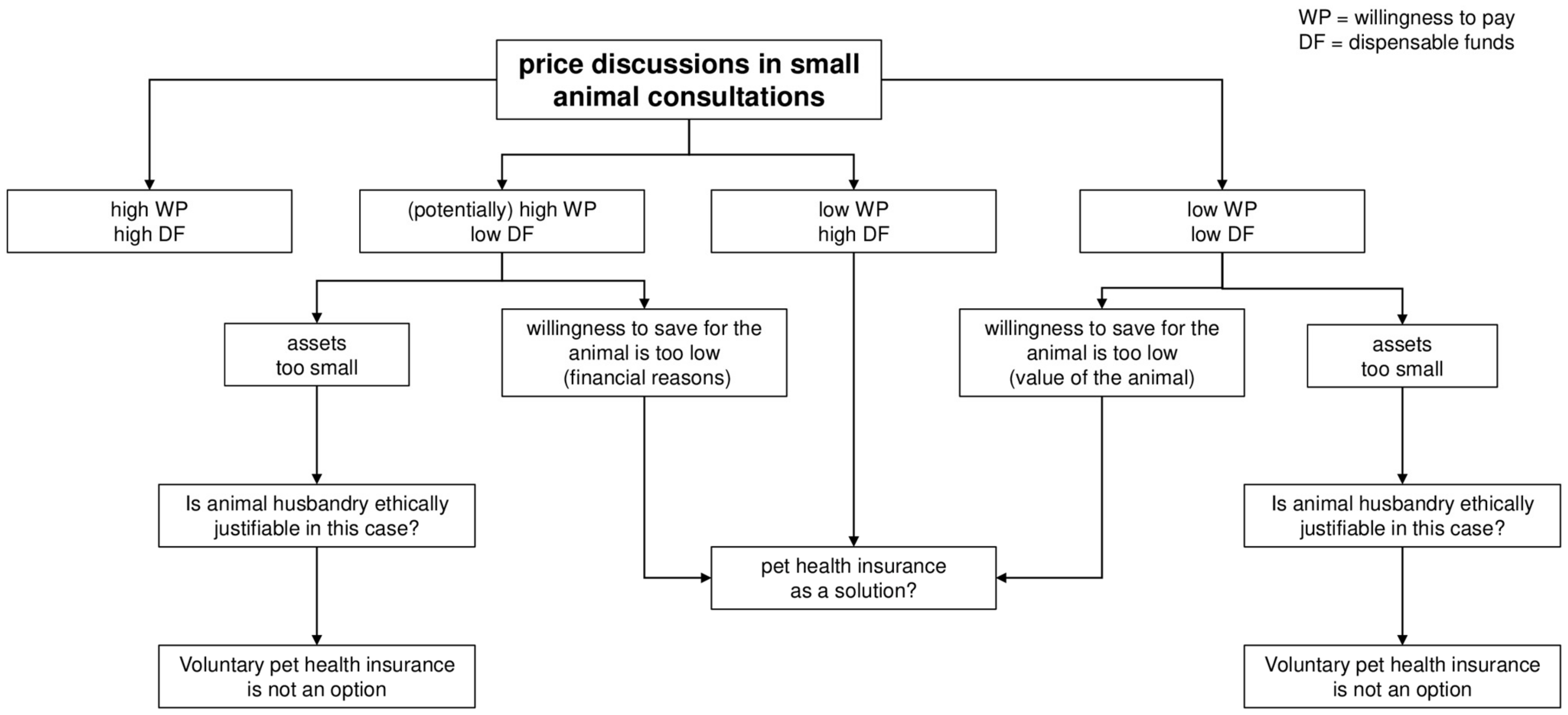

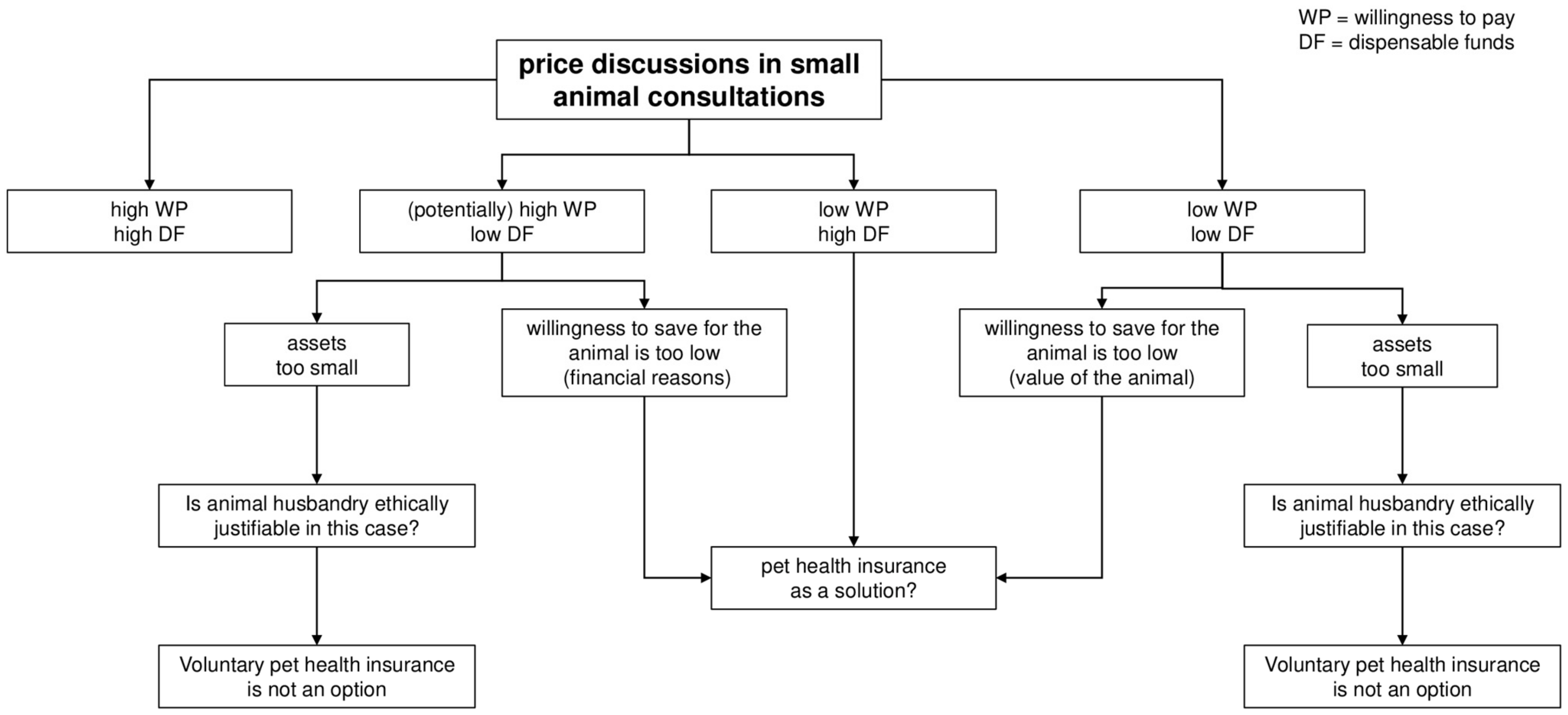

- High willingness to pay (WP) and high dispensable funds (DF);

- High WP and low DF;

- Low WP and high DF;

- Low WP and low DF.

3. Results

4. Conclusions

“The focus or, rather, the entire objective of veterinary activity should be on customer satisfaction, in which medical quality, although a very important part, is just one part.”

- Friendliness;

- Attention;

- Helpfulness;

- Telephone/personal availability;

- Speed;

- Reliability;

- Professional/social competence.

Further Perspectives and Conclusions for Practice

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| DF | Dispensable funds |

| NAPHIA | North American Pet Health Insurance Association |

| PHI | Pet health insurance |

| RCVS | Royal College of Veterinary Surgeons |

| UK | United Kingdom |

| WP | Willingness to pay |

References

- Kondrup, S.V.; Anhøj, K.P.; Rødsgaard-Rosenbeck, C.; Lund, T.B.; Nissen, M.H.; Sandøe, P. Veterinarian’s dilemma: A study of how Danish small animal practitioners handle financially limited clients. Vet. Rec. 2016, 179, 596. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Kipperman, B.S.; Kass, P.H.; Rishniw, M. Factors that influence small animal veterinarians’ opinions and actions regarding cost of care and effects of economic limitations on patient care and outcome and professional career satisfaction and burnout. J. Am. Vet. Assoc. 2017, 250, 785–794. [Google Scholar] [CrossRef] [PubMed]

- Batchelor, C.E.M.; McKeegan, D.E.F. Survey of the frequency and perceived stressfulness of ethical dilemmas encountered in UK veterinary practice. Vet. Rec. 2012, 170, 19. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bower, J. Pet health insurance. Vet. Rec. 1990, 127, 362–363. [Google Scholar] [PubMed]

- Royal College of Veterinary Surgeons. The Code of Professional Conduct for Veterinary Surgeons and Supporting Guidance. Available online: https://www.rcvs.org.uk/setting-standards/advice-and-guidance/code-of-professional-conduct-for-veterinary-surgeons/pdf/ (accessed on 14 May 2022).

- Berryman, J.C.; Howells, K.; Lloayd-Evans, M. Pet owner attitudes to pets and people: A psychological study. Vet. Rec. 1985, 117, 659–661. [Google Scholar] [CrossRef] [PubMed]

- Hughes, K.; Rhind, S.M.; Mossop, L.; Cobb, K.; Morley, E.; Kerrin, M.; Morton, C.; Cake, M. ‘Care about my animal, know your stuff and take me seriously’: United Kingdom and Australian clients’ views on the capabilities most important in their veterinarians. Vet. Rec. 2018, 183, 534. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Animal Welfare Act 2006. United Kingdom. Available online: https://www.legislation.gov.uk/ukpga/2006/45/contents (accessed on 17 January 2021).

- Animal Welfare Act 1972/07/24. Germany. Current Version of 2020/06/19. Available online: https://www.gesetze-im-internet.de/tierschg/BJNR012770972.html (accessed on 17 January 2021).

- Rowena, V. Epilepsy beyond seizures: A review of the impact of epilepsy and its comorbidities on health-related quality of life in dogs. Vet. Rec. 2015, 177, 306–315. [Google Scholar]

- Williams, V. Conflicts of interest affecting the role of veterinarians in animal welfare. Aust. N. Z. Counc. Care Anim. Res. Teach. 2002, 15, 1–3. [Google Scholar]

- Coe, J.B.; Adams, C.L.; Bonnett, B.N. A focus group study of veterinarians’ and pet owners perceptions of the monetary aspects of veterinary care. J. Am. Vet. Assoc. 2007, 231, 1510–1518. [Google Scholar] [CrossRef] [PubMed]

- Kersebohm, J.C.; Lorenz, T.; Becher, A.; Doherr, M.G. Factors related to work and life satisfaction of veterinary practicioners in Germany. Vet. Rec. Open 2017, 4, e000229. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Moses, L.; Malowney, M.J.; Wesley Boyd, J. Ethical conflict and moral distress in veterinary practice: A survey of North American veterinarians. J. Vet. Intern. Med. 2018, 32, 2115–2122. [Google Scholar] [CrossRef] [PubMed]

- Fiedermutz, K.L. Situationsanalyse der Tierkrankenversicherungen für Hunde und Katzen in Deutschland aus der Sicht von Versicherungsunternehmen, Tierärzten und Tierhalten (Situation Analysis of Veterinary Health Insurance for Dogs and Cats in Germany from the Perspective of Insurance Companies, Veterinarians and Pet Owners); Mensch und Buch Verlag: Berlin, Germany, 2020. [Google Scholar]

- North American Pet Health Insurance Association (NAPHIA). Press Kit, “Driving Growth of Pet Health Insurance”; Research Report 2016; NAPHIA: Kansas City, MO, USA, 2016. [Google Scholar]

- King, R. Uptake of pet insurance. Vet. Rec. 2011, 168, 624. [Google Scholar] [CrossRef] [PubMed]

- Zühlsdorf, S.; Gauly, K. Wie Wichtig Ist Verbrauchern das Thema Tierschutz? Präferenzen, Verantwortlichkeiten, Handlungskompetenzen und Politikoptionen (How Important Is the Issue of Animal Welfare to Consumers? Preferences, Responsibilities, Action Competencies and Policy Options). Ein Gemeinsames Projekt der Zühlsdorf + Partner Marketingberatung und des Lehrstuhls “Marketing für Lebensmittel und Agrarprodukte“ der Universität Göttingen im Auftrag des Verbraucherzentrale Bundesverbandes e.V. (vzbv) (A Joint Project of Zühlsdorf + Partner Marketingberatung and the Chair of “Marketing for Food and Agricultural Products” at the University of Göttingen on Behalf of the Federation of German Consumer Organisations). Göttingen. 2016. Available online: https://www.vzbv.de/sites/default/files/downloads/Tierschutz-Umfrage-Ergebnisbericht-vzbv-2016-01.pdf (accessed on 15 May 2022).

- Enneking, U. Kaufbereitschaft bei Verpackten Schweinefleischprodukten im Lebensmitteleinzelhandel (Willingness to Buy Packaged Pork Products in the Food Retail Sector). Osnabrück. 2018. Available online: https://www.hs-osnabrueck.de/fileadmin/HSOS/Homepages/Personalhomepages/Personalhomepages-AuL/Enneking/Tierwohlstudie-HS-Osnabrueck_Teil-Realdaten_17-Jan-2019.pdf (accessed on 15 May 2022).

- Berentzen, W. Die Deutschen und Ihre Hunde; Wilhelm Goldmann Verlag in der Verlagsgruppe Bertelsmann GmbH: München, Germany, 1999. [Google Scholar]

- Why Are Dogs Called Man’s Best Friend? For Dog People. Available online: https://www.rover.com/blog/dogs-called-mans-best-friend/ (accessed on 17 January 2021).

- Hens, K. Ethical Responsibilities Towards Dogs: An Inquiry into the Dog-Human Relationship. J. Agric. Environ. Ethics 2009, 22, 3–14. [Google Scholar] [CrossRef] [Green Version]

- Market Study 2018—Consumer and Vehicle Financing in Germany. GfK SE. Consumer Panels. Conducted on Behalf of the Bankenfachverband e.V. (German Association of Credit Banks). 2018. Available online: https://ssl.bfach.de/bankenfachverband.php/cat/246/aid/4471/title/Marktstudie_Konsum-_und_Kfz-Finanzierung_2018 (accessed on 17 January 2021).

- AVMA Pet Ownership and Demographics Sourcebook; 2017–2018 Edition; Veterinary Economics Division, American Veterinary Medical Association: Schamburg, IL, USA, 2018; ISBN 978-1-882691-52-4.

- Bir, C.; Ortez, M.; Olynk Widmar, N.J.; Wolf, C.A.; Hansen, C.; Ouedraogo, F.B. Familiarity and Use of Veterinary Services by US Resident Dog and Cat Owners. Animals 2020, 10, 483. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bentlage, G. Kommunikations Skills—Erfolgreiche Gesprächsführung in der Tierärztlichen Praxis (Communication Skills—Successful Conversation in Veterinary Practice); Schattauer GmbH: Stuttgart, Germany, 2016. [Google Scholar]

- Carnegie, D. How to Win Friends and Influence People; Pocket Books: New York, NY, USA, 2010. [Google Scholar]

- Küper, A.M.; Merle, R. Being Nice Is Not Enough–Exploring Relationship-Centered Veterinary Care with Structural Equation Modeling. A Quantitative Study on German Pet Owners’ Perceptions. Front. Vet. Sci. 2019, 6, 56. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wagner, F. Risikoausgleich. In Definition im Gabler Wirtschaftslexikon; Springer: Berlin/Heidelberg, Germany, 2018. [Google Scholar]

- Becker, M.; Kunzmann, P.; Volk, H.A. Verpflichtende Tierkrankenversicherung für Hunde und Katzen—Eine bessere Alternative zur freiwilligen TKV? Prakt. Tierarzt 2022, 103, 140–151. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Becker, M.; Volk, H.; Kunzmann, P. Is Pet Health Insurance Able to Improve Veterinary Care? Why Pet Health Insurance for Dogs and Cats Has Limits: An Ethical Consideration on Pet Health Insurance. Animals 2022, 12, 1728. https://doi.org/10.3390/ani12131728

Becker M, Volk H, Kunzmann P. Is Pet Health Insurance Able to Improve Veterinary Care? Why Pet Health Insurance for Dogs and Cats Has Limits: An Ethical Consideration on Pet Health Insurance. Animals. 2022; 12(13):1728. https://doi.org/10.3390/ani12131728

Chicago/Turabian StyleBecker, Michelle, Holger Volk, and Peter Kunzmann. 2022. "Is Pet Health Insurance Able to Improve Veterinary Care? Why Pet Health Insurance for Dogs and Cats Has Limits: An Ethical Consideration on Pet Health Insurance" Animals 12, no. 13: 1728. https://doi.org/10.3390/ani12131728

APA StyleBecker, M., Volk, H., & Kunzmann, P. (2022). Is Pet Health Insurance Able to Improve Veterinary Care? Why Pet Health Insurance for Dogs and Cats Has Limits: An Ethical Consideration on Pet Health Insurance. Animals, 12(13), 1728. https://doi.org/10.3390/ani12131728