Drivers for the Acceptance of Green Housing Insurance from the Perspective of House Owners

Abstract

1. Introduction

2. Understanding the Acceptance of Green Housing Insurance Based on the Push–Pull Theory

2.1. The Influence of the Push–Pull Theory on Acceptance

2.2. Drivers of the Acceptance of Green Housing Insurance in the Push Dimension

2.2.1. Drivers from Green Housing Characteristics

2.2.2. Drivers from Insurance Function

2.3. Drivers of the Acceptance of Green Housing Insurance in the Pull Dimension

2.3.1. Drivers from Policy Incentives

2.3.2. Drivers from Social Stimulation

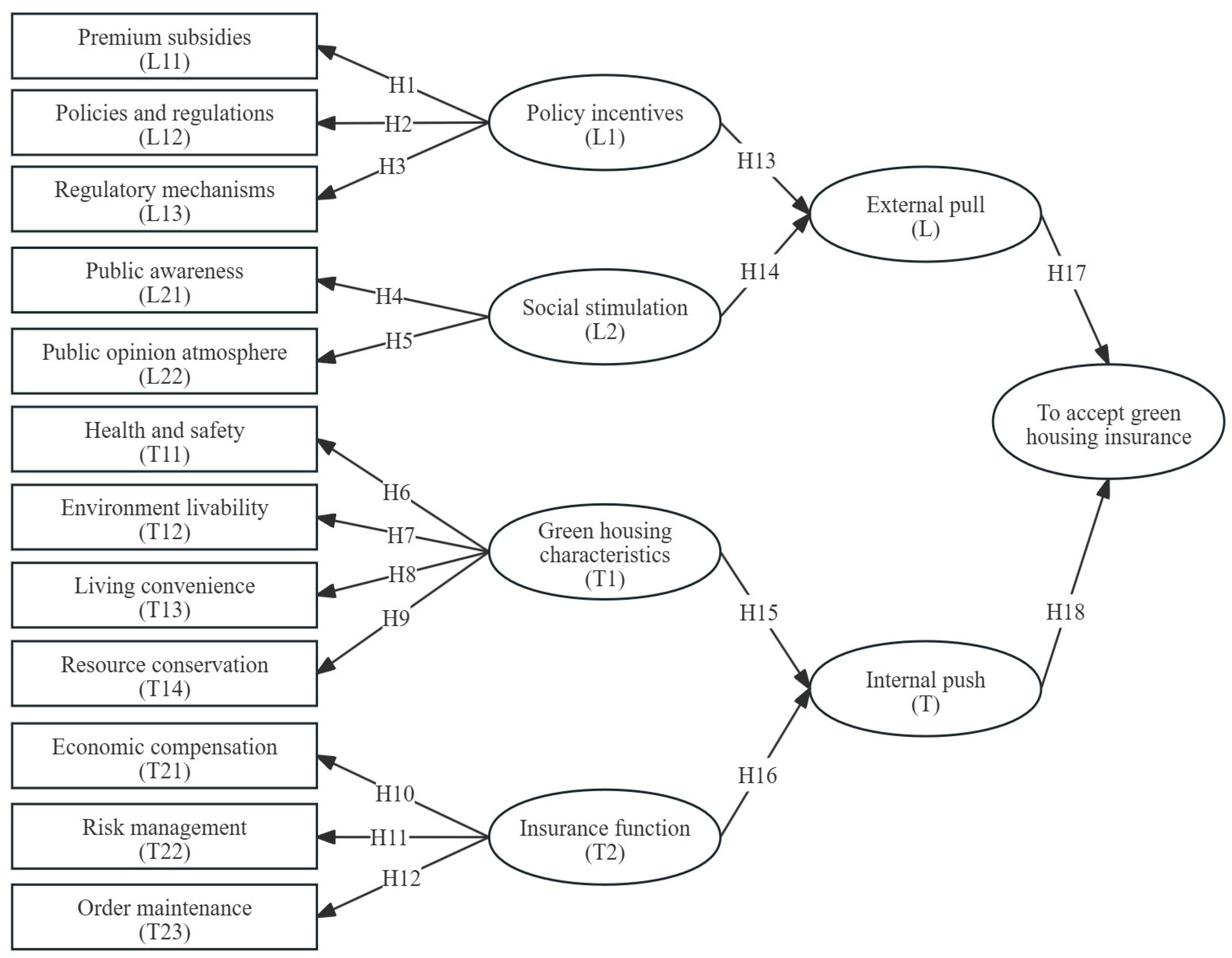

2.4. The Driver System for the Acceptance of Green Housing Insurance

3. Methods

3.1. Questionnaire Survey for Data Collection

3.2. Structural Equation Modeling (SEM) for Driver Analysis

4. Analysis of Drivers

4.1. Reliability and Validity Analysis of Survey Data

4.1.1. Reliability Analysis of Survey Data

4.1.2. Validity Analysis of Survey Data

4.2. Relationships Confirmation and Driver Analysis

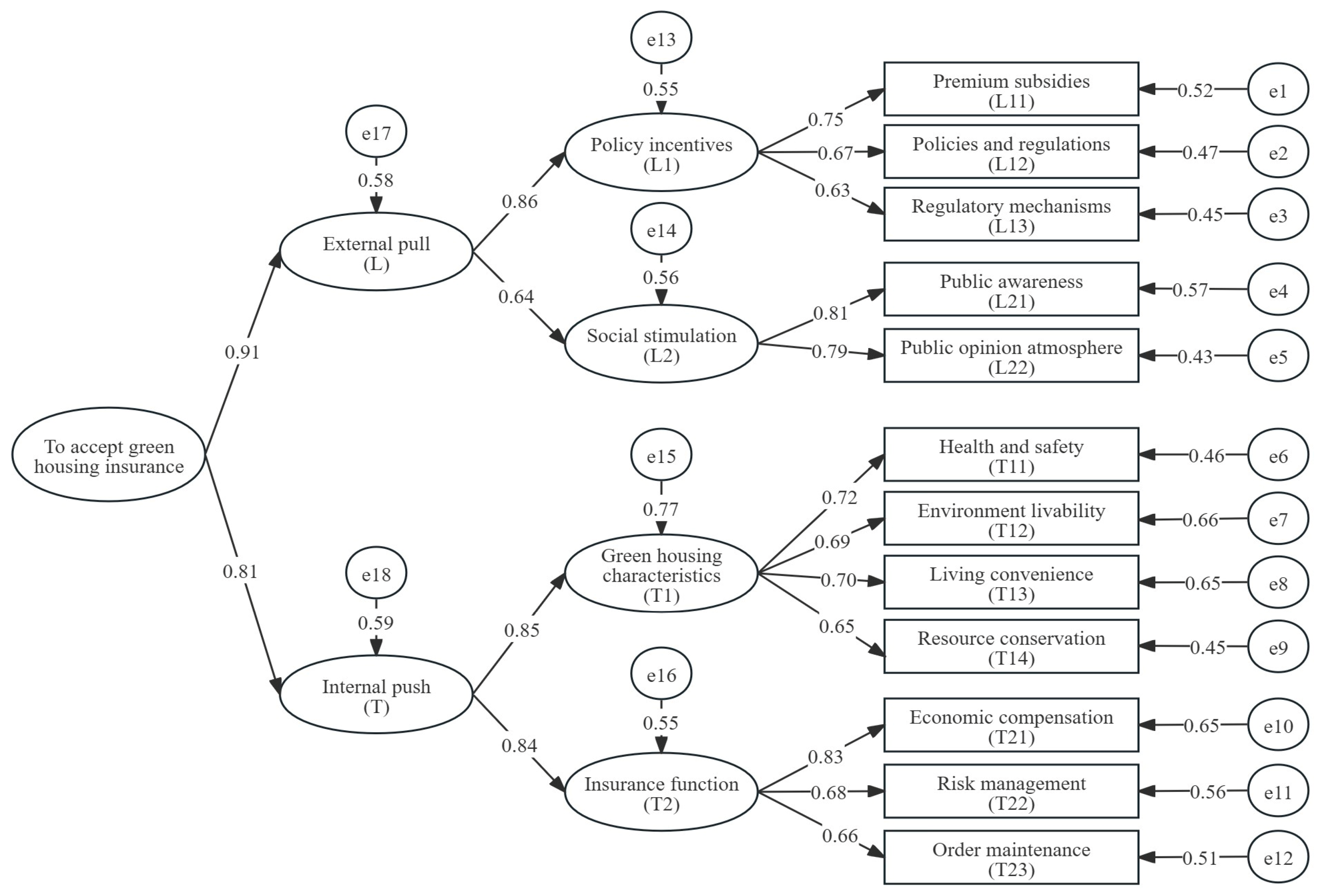

4.2.1. Initial Framework of the Model

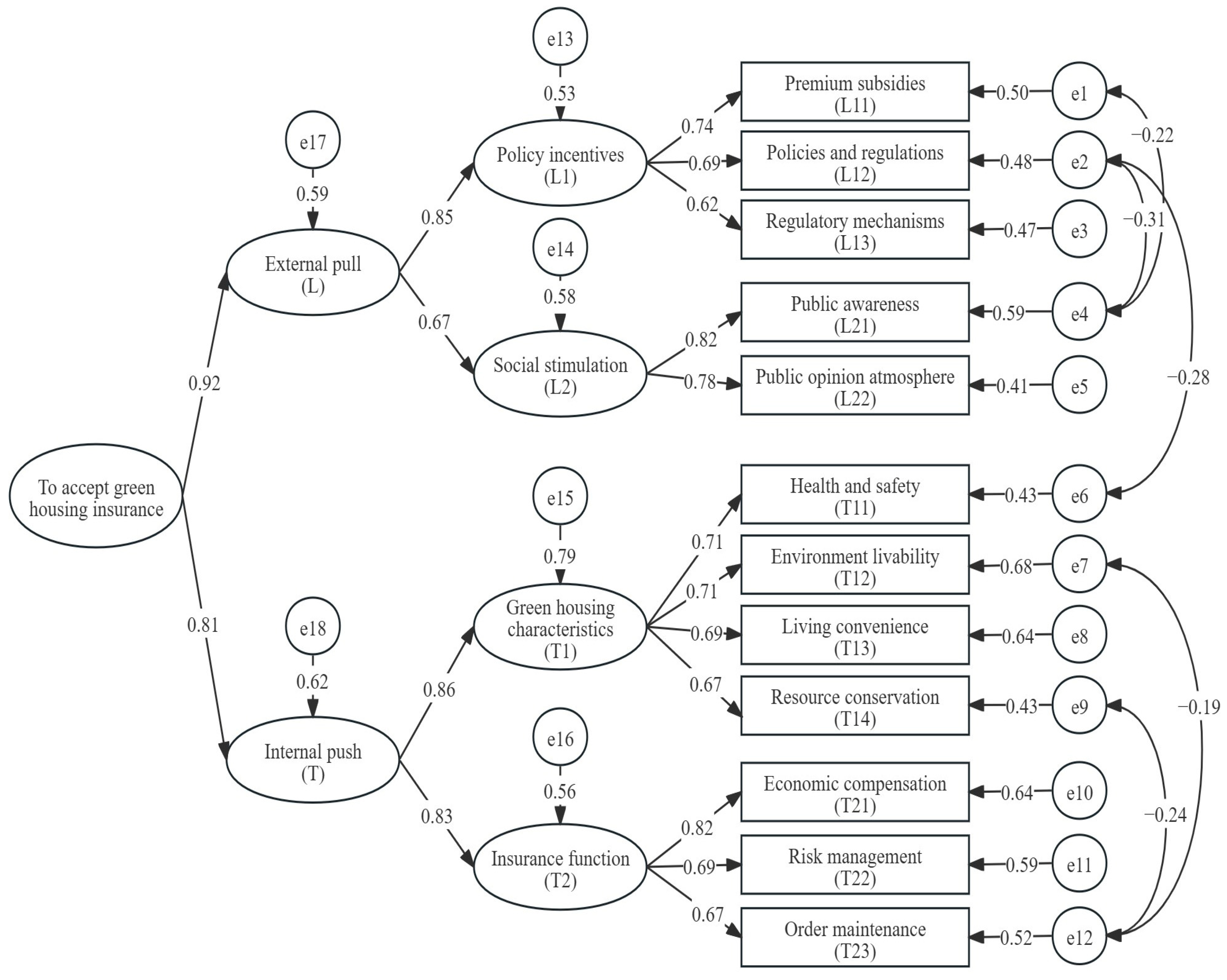

4.2.2. Model Test and Modification

4.2.3. Hypothesis Verification

4.2.4. Results Analysis

5. Discussion

5.1. Analysis of the Push–Pull Mechanism and Verification

5.1.1. Comprehensive Analysis of the Push–Pull Mechanism

5.1.2. Mechanistic Analysis from the Pull Dimension

5.1.3. Mechanistic Analysis from the Push Dimension

5.1.4. Verification for the Driver Mechanism

5.2. Policy Suggestions

5.2.1. General Strategy of “Pull-Dominant with Push–Pull Parallelism”

5.2.2. Stimulate Premium Subsidies

5.2.3. Innovative Insurance Compensation Forms

5.2.4. Improve Relevant Policies and Regulations

5.2.5. Guide Public Awareness

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

- Pare 1: Background information (Please tick ✓ in the ☐ that applies to you)

- Living in a green housing: ☐ Yes ☐ No

- Living in which city:

- Gender: ☐ Male ☐ Female

- Age: ☐ Below 22 ☐ 22–30 ☐ 31–40 ☐ 41–50 ☐ 51–65 ☐ Over 65

- Educational background: ☐ College degree or below ☐ Bachelor’s degree ☐ Postgraduate degree or above

- Work institution: ☐ Government departments ☐ Construction industry ☐ Manufacturing enterprises ☐ Service industry ☐ Technology companies ☐ Educational institution ☐ Others

- Pare 2: Identification of the influencing degree of each driver on the acceptance of green housing insurance (Points present as 5—very important, 4—important, 3—common, 2—unimportant, and 1—negligible. Please tick ✓ in the ☐ that applies to you)

{kind=link}

{kind=link}

{kind=link}

| Code | Drivers | Importance of the Drivers | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| L11 | Premium subsidies | ☐ | ☐ | ☐ | ☐ | ☐ |

| L12 | Policies and regulations | ☐ | ☐ | ☐ | ☐ | ☐ |

| L13 | Regulatory mechanisms | ☐ | ☐ | ☐ | ☐ | ☐ |

| L21 | Public awareness | ☐ | ☐ | ☐ | ☐ | ☐ |

| L22 | Public opinion atmosphere | ☐ | ☐ | ☐ | ☐ | ☐ |

| T11 | Health and safety | ☐ | ☐ | ☐ | ☐ | ☐ |

| T12 | Environment livability | ☐ | ☐ | ☐ | ☐ | ☐ |

| T13 | Living convenience | ☐ | ☐ | ☐ | ☐ | ☐ |

| T14 | Resource conservation | ☐ | ☐ | ☐ | ☐ | ☐ |

| T21 | Economic compensation | ☐ | ☐ | ☐ | ☐ | ☐ |

| T22 | Risk management | ☐ | ☐ | ☐ | ☐ | ☐ |

| T23 | Order maintenance | ☐ | ☐ | ☐ | ☐ | ☐ |

Appendix B

- Pare 1: Background information (Please tick ✓ in the ☐ that applies to you)

- Profession: ☐ Department directors of insurance companies ☐ Department directors of property management companies ☐ Staffs of local construction authorities ☐ Others institutions (including design organization, consultant firms and research institutions)

- Working years: ☐ Below 5 years ☐ 5–10 years ☐ 11–20 years ☐ Over 20 years

- Pare 2: Identification of the influencing degree of each driver on the acceptance of green housing insurance (Points present as 5—very important, 4—important, 3—common, 2—unimportant, and 1—negligible. Please tick ✓ in the ☐ that applies to you)

| Code | Drivers | Importance of the Drivers | ||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| L11 | Premium subsidies | ☐ | ☐ | ☐ | ☐ | ☐ |

| L12 | Policies and regulations | ☐ | ☐ | ☐ | ☐ | ☐ |

| L13 | Regulatory mechanisms | ☐ | ☐ | ☐ | ☐ | ☐ |

| L21 | Public awareness | ☐ | ☐ | ☐ | ☐ | ☐ |

| L22 | Public opinion atmosphere | ☐ | ☐ | ☐ | ☐ | ☐ |

| T11 | Health and safety | ☐ | ☐ | ☐ | ☐ | ☐ |

| T12 | Environment livability | ☐ | ☐ | ☐ | ☐ | ☐ |

| T13 | Living convenience | ☐ | ☐ | ☐ | ☐ | ☐ |

| T14 | Resource conservation | ☐ | ☐ | ☐ | ☐ | ☐ |

| T21 | Economic compensation | ☐ | ☐ | ☐ | ☐ | ☐ |

| T22 | Risk management | ☐ | ☐ | ☐ | ☐ | ☐ |

| T23 | Order maintenance | ☐ | ☐ | ☐ | ☐ | ☐ |

References

- Jiang, Y.; Zhang, Y.; Yeganeh, A.; Zhao, D. Resilience of Green Building Supply Chain: Capabilities, Risks and Influence Mechanism. J. Green Build. 2024, 19, 41–69. [Google Scholar] [CrossRef]

- Taemthong, W.; Chaisaard, N. An Analysis of Green Building Costs Using a Minimum Cost Concept. J. Green Build. 2019, 14, 53–78. [Google Scholar] [CrossRef]

- Wang, Y.; Chen, D.; Tian, P. Research on the Impact Path of the Sustainable Development of Green Buildings: Evidence from China. Sustainability 2022, 14, 13628. [Google Scholar] [CrossRef]

- Qian, Y.; Yu, M.; Wang, T.; Yuan, R.; Feng, Z.; Zhao, X. Evolutionary Game and Simulation of Green Housing Market Subject Behavior in China. Comput. Intell. Neurosci. 2022, 2022, 7153270. [Google Scholar] [CrossRef]

- Yang, Y.X.O.; Chew, B.C.; Loo, H.S.; Tan, L.H. Green Commercial Building Insurance in Malaysia. In Proceedings of the 5th International Conference on Education, Concept, and Application of Green Technology, Semarang, Indonesia, 5–6 October 2016. [Google Scholar]

- Taghizadeh-Hesary, F.; Yoshino, N. Sustainable Solutions for Green Financing and Investment in Renewable Energy Projects. Energies 2020, 13, 788. [Google Scholar] [CrossRef]

- Li, S.; Zheng, X.; Zeng, Q. Can Green Finance Drive the Development of the Green Building Industry?—Based on the Evolutionary Game Theory. Sustainability 2023, 15, 13134. [Google Scholar] [CrossRef]

- Eling, M. Is the insurance industry sustainable? J. Risk Financ. 2024, 25, 684–703. [Google Scholar] [CrossRef]

- Stricker, L.; Pugnetti, C.; Wagner, J.; Zeier Röschmann, A. Green Insurance: A Roadmap for Executive Management. J. Risk Financ. Manag. 2022, 15, 221. [Google Scholar] [CrossRef]

- Sun, M.; Han, C.; Nie, Q.; Xu, J.; Zhang, F.; Zhao, Q. Understanding building energy efficiency with administrative and emerging urban big data by deep learning in Glasgow. Energy Build. 2022, 273, 112331. [Google Scholar] [CrossRef]

- Wang, S.; Chen, S.; Nah, K. Exploring the Mechanisms Influencing Users’ Willingness to Pay for Green Real Estate Projects in Asia Based on Technology Acceptance Modeling Theory. Buildings 2024, 14, 349. [Google Scholar] [CrossRef]

- Grierson, D. Unfinished Business at the Urban Laboratory-Paolo Soleri, Arcology, and Arcosanti. Open House Int. 2016, 41, 63–72. [Google Scholar] [CrossRef]

- Yang, R.J.; Zou, P.X.; Wang, J. Modelling stakeholder-associated risk networks in green building projects. Int. J. Proj. Manag. 2016, 34, 66–81. [Google Scholar] [CrossRef]

- Jiang, Y.; Xing, Y.; Zhao, D.; Jiao, R. Resale of Green Housing Compensates for Its Premium Pricing: An Empirical Study of China. J. Green Build. 2021, 16, 45–61. [Google Scholar] [CrossRef]

- Chen, Y.; Jones, C.A.; Dunse, N.A.; Li, E.; Liu, Y. Housing Prices and the Characteristics of Nearby Green Space: Does Landscape Pattern Index Matter? Evidence from Metropolitan Area. Land 2023, 12, 496. [Google Scholar] [CrossRef]

- Hu, Y.; Du, S.; Wang, Y.; Yang, X. How Does Green Insurance Affect Green Innovation? Evidence from China. Sustainability 2023, 15, 12194. [Google Scholar] [CrossRef]

- Zona, R.; Roll, K.; Law, Z. Sustainable/green insurance products. In Casualty Actuarial Society E-Forum; Casualty Actuarial Society: Arlington, VA, USA, 2014. [Google Scholar]

- Yanghua, H.; Jingbo, C.; Shen, L. Green Technology Innovation under China’s New Development Concept: The Effects of Policy-Push and Demand-Pull on Renewable Energy Innovation. Soc. Sci. China 2023, 44, 158–180. [Google Scholar] [CrossRef]

- Nipane, A.P.; Awasthi, A. Interconnection Between Human’s Psychological Elements and Their Influential Mediums and Channels Are Potential Accelerators to Comprehend People’s Inclination Towards Autonomous Vehicles. EasyChair 2021, 5522. Available online: https://easychair.org/publications/preprint/CXWP (accessed on 7 April 2025).

- Alexandrovna, P.Y.; Galimovna, S.K. The migration theory’s process of formation and development in the globalizing world. Opción Rev. Cienc. Humanas Soc. 2018, 87, 18. [Google Scholar]

- Tolman, E.C. Behavior and Psychological Man: Essays in Motivation and Learning; University of California Press: Berkeley, CA, USA, 2023. [Google Scholar]

- Sha, C.; Che, T.; Xu, T.; Yang, Z. Antecedents of users’ switching intention to Central Bank Digital Currency: A push-pull-mooring model perspective. Electron. Commer. Res. Appl. 2024, 68, 101467. [Google Scholar] [CrossRef]

- Morales-Alonso, G.; Blanco-Serrano, J.A.; Núñez Guerrero, Y.; Grijalvo, M.; Blanco Jimenez, F.J. Theory of planned behavior and GEM framework—How can cognitive traits for entrepreneurship be used by incubators and accelerators? Eur. J. Innov. Manag. 2022, 27, 922–943. [Google Scholar] [CrossRef]

- Ganiyu, B.O. Strategy to Enhance Sustainability in Affordable Housing Construction in South Africa. Ph.D. Thesis, Cape Peninsula University of Technology, Cape Town, South Africa, 2016. [Google Scholar]

- GB/T 50378—2019; Assessment Standard for Green Building. China Architecture and Building Press: Beijing, China, 2019.

- She, Y.; Wu, S.; Wang, Y.; Zhu, Y.; Jiao, L. Habitat Safety Evaluation of Sustainable Housing from the Perspective of Households. J. Green Build. 2023, 18, 189–216. [Google Scholar] [CrossRef]

- Tong, L. China Catastrophe Insurance: A Boost to Green Insurance Development under ESG Concept. Acad. J. Bus. Manag. 2022, 4, 11–19. [Google Scholar] [CrossRef]

- Alabady, H.S.; Abu Ghazaleh, S.N. Green building insurance. JL Pol’y Glob. 2017, 66, 137. [Google Scholar]

- Du, C.; Lou, W.; Qiao, Y.; Zhang, Y. Public Rental Housing and Long-Term Settlement Intention of the Migrants in China: The Mediating Effect of Identity. Buildings 2024, 14, 2774. [Google Scholar] [CrossRef]

- Hu, H.; Geertman, S.; Hooimeijer, P. The willingness to pay for green apartments: The case of Nanjing, China. Urban Stud. 2014, 51, 3459–3478. [Google Scholar] [CrossRef]

- Fang, X.; Lv, Y. Housing prices and green innovation: Evidence from Chinese enterprises. Manag. Decis. 2023, 61, 3519–3544. [Google Scholar] [CrossRef]

- Li, S.; Zhao, T.; Zhang, G.; Zhou, Y.; Qu, S.; Sun, X.; Li, J.; Zhang, S. Willingness to pay for earthquake insurance for rural houses and its influencing factors in Xinjiang, China. Int. J. Disaster Risk Reduct. 2024, 103, 104340. [Google Scholar] [CrossRef]

- Westland, J.C. Structural equation models. Stud. Syst. Decis. Control 2015, 22, 152. [Google Scholar]

- Orogun, B.; Issa, M.H. Evaluating the Health and Safety Maturity of Sustainable Building Projects Using a Sustainable Health and Safety Maturity Model. J. Green Build. 2023, 18, 57–78. [Google Scholar] [CrossRef]

- Siswadi, Y.; Jufrizen, J.; Saripuddin, J.; Farisi, S.; Sari, M. Organizational Culture and Organizational Citizenship Behavior: The Mediating Role of Learning Organizations and Organizational Commitment. J. Ris. Bisnis Dan Manaj. 2023, 16, 73–82. [Google Scholar] [CrossRef]

- Guenther, P.; Guenther, M.; Ringle, C.M.; Zaefarian, G.; Cartwright, S. Improving PLS-SEM use for business marketing research. Ind. Mark. Manag. 2023, 111, 127–142. [Google Scholar] [CrossRef]

- Yin, J.; Qiu, X. AI technology and online purchase intention: Structural equation model based on perceived value. Sustainability 2021, 13, 5671. [Google Scholar] [CrossRef]

- Kineber, A.F.; Massoud, M.M.; Hamed, M.M.; Alhammadi, Y.; Al-Mhdawi, M.K.S. Impact of Overcoming BIM Implementation Barriers on Sustainable Building Project Success: A PLS-SEM Approach. Buildings 2023, 13, 178. [Google Scholar] [CrossRef]

- Li, C.; Zhang, Y.; Xu, Y. Factors Influencing the Adoption of Blockchain in the Construction Industry: A Hybrid Approach Using PLS-SEM and fsQCA. Buildings 2022, 12, 1349. [Google Scholar] [CrossRef]

- Wang, C.; Wood, L.C.; Teo, L.T. Tropical Vertical Greenery Systems: Irrigation Systems, Biophysical Characteristics, and Influential Criteria. J. Green Build. 2016, 11, 57–90. [Google Scholar] [CrossRef]

- Kalkbrenner, M.T. Alpha, Omega, and H Internal Consistency Reliability Estimates: Reviewing These Options and When to Use Them. Couns. Outcome Res. Eval. 2021, 14, 77–88. [Google Scholar] [CrossRef]

- Rajput, S. Methods of reliability and validity. In An SPSS Guide for Tourism, Hospitality and Events Researchers; Routledge: London, UK, 2020; pp. 243–264. [Google Scholar]

- Alhammadi, Y.; Radzi, A.R.; Alias, A.R.; Rahman, R.A. Modeling Workplace Well-Being Factors in Infrastructure Construction Projects: PLS-SEM Approach. Buildings 2024, 14, 2289. [Google Scholar] [CrossRef]

- Fan, L.; Xiong, Y.; Peng, Y. Assessing Accessible Travel Satisfaction in Old Communities: A SEM Study. Buildings 2024, 14, 1273. [Google Scholar] [CrossRef]

- Cheung, G.W.; Cooper-Thomas, H.D.; Lau, R.S.; Wang, L.C. Reporting reliability, convergent and discriminant validity with structural equation modeling: A review and best-practice recommendations. Asia Pac. J. Manag. 2023, 41, 745–783. [Google Scholar] [CrossRef]

- Bolukbas, N.; Gol, G. Surgical Anxiety Questionnaire: Turkish validity and reliability. Psychol. Health Med. 2024, 29, 1652–1663. [Google Scholar] [CrossRef]

- Shrestha, N. Factor analysis as a tool for survey analysis. Am. J. Appl. Math. Stat. 2021, 9, 4–11. [Google Scholar] [CrossRef]

- Awang, Z. Research Methodology and Data Analysis, 2nd ed.; UiTM Press: Shah Alam, Malaysia, 2012. [Google Scholar]

- Cribbie, R.A.; Fiksenbaum, L.; Keselman, H.J.; Wilcox, R.R. Effect of non-normality on test statistics for one-way independent groups designs. Br. J. Math. Stat. Psychol. 2012, 65, 56–73. [Google Scholar] [CrossRef] [PubMed]

- Henseler, J.; Sarstedt, M. Goodness-of-fit indices for partial least squares path modeling. Comput. Stat. 2012, 28, 565–580. [Google Scholar] [CrossRef]

- Paunova, R.; Ramponi, C.; Kandilarova, S.; Todeva-Radneva, A.; Latypova, A.; Stoyanov, D.; Kherif, F. Degeneracy and disordered brain networks in psychiatric patients using multivariate structural covariance analyzes. Front. Psychiatry 2023, 14, 1272933. [Google Scholar] [CrossRef]

- Shin, D.S.; Jeong, B.Y. Older Female Farmers and Modeling of Occupational Hazards, Wellbeing, and Sleep-Related Problems on Musculoskeletal Pains. Int. J. Environ. Res. Public Health 2022, 19, 7274. [Google Scholar] [CrossRef]

- Trafimow, D.; Rice, S.; MacDonald, J.A. An investigation of the accuracy of standardized path coefficients. J. Gen. Psychol. 2011, 138, 201–214. [Google Scholar] [CrossRef]

- Kaewanuchit, C.; Sawangdee, Y. A Path Analysis of Mental Health Among Thai Immigrant Employees in Pranakron Si Ayutthaya Province. J. Immigr. Minor Health 2016, 18, 871–877. [Google Scholar] [CrossRef]

- Pandove, D.; Goel, S.; Rani, R. General correlation coefficient based agglomerative clustering. Clust. Comput. 2018, 22, 553–583. [Google Scholar] [CrossRef]

- Ghali, Z.Z. Effect of utilitarian and hedonic values on consumer willingness to buy and to pay for organic olive oil in Tunisia. Br. Food J. 2020, 122, 1013–1026. [Google Scholar] [CrossRef]

- She, Y.; Shen, L.; Jiao, L.; Zuo, J.; Tam, V.W.Y.; Yan, H. Constraints to achieve infrastructure sustainability for mountainous townships in China. Habitat Int. 2018, 73, 65–78. [Google Scholar] [CrossRef]

- Phillips, D. Quality of Life: Concept, Policy and Practice; Routledge: London, UK, 2006. [Google Scholar]

- Cai, J.; De Janvry, A.; Sadoulet, E. Subsidy policies and insurance demand. Am. Econ. Rev. 2020, 110, 2422–2453. [Google Scholar] [CrossRef]

- Ma, S.-C.; Fan, Y.; Feng, L. An evaluation of government incentives for new energy vehicles in China focusing on vehicle purchasing restrictions. Energy Policy 2017, 110, 609–618. [Google Scholar] [CrossRef]

- Xian, Y.; Wang, Q.; Fan, W.; Da, Y.; Fan, J.-L. The impact of different incentive policies on new energy vehicle demand in China’s gigantic cities. Energy Policy 2022, 168, 113137. [Google Scholar] [CrossRef]

- Chawla, Y.; Kowalska-Pyzalska, A. Public awareness and consumer acceptance of smart meters among Polish social media users. Energies 2019, 12, 2759. [Google Scholar] [CrossRef]

- Lippmann, W. Public Opinion; Routledge: London, UK, 2017. [Google Scholar]

- Wang, Y.; Feng, Y.; Han, K.; Zheng, Z.; Dai, P. Analysis of the Temporal and Spatial Patterns of Residential Prices in Qingdao and Its Driving Factors. Buildings 2025, 15, 195. [Google Scholar] [CrossRef]

- Tseng, M.-L.; Li, S.-X.; Lin, C.-W.R.; Chiu, A.S.F. Validating green building social sustainability indicators in China using the fuzzy delphi method. J. Ind. Prod. Eng. 2022, 40, 35–53. [Google Scholar] [CrossRef]

- Oluwagbemiga Paul, A.; Uduma-Olugu, N. Exploring the symbiotic relationship between smart technologies and thermal comfort in urban environments. Soc. Sci. Humanit. Open 2024, 10, 100943. [Google Scholar] [CrossRef]

- Xiao, Y.; Olshansky, R.; Zhang, Y.; Johnson, L.A.; Song, Y. Financing rapid community reconstruction after catastrophic disaster: Lessons from the 2008 Wenchuan earthquake in China. Nat. Hazards 2019, 104, 5–30. [Google Scholar] [CrossRef]

- Ingram, J.D. The changing role of liability insurance: Contract of indemnity or source of compensation? FDCC Q. 2001, 51, 269. [Google Scholar]

- Wang, A.; Wang, C.; Chu, Z. Research on the Path of Green Finance to Help Green Building Development Under the Background of “Double Carbon”. In Novel Technology and Whole-Process Management in Prefabricated Building, 5th International Prefabricated Building Seminar on Frontier Technology and Talent Training, Chongqin, China, 21–22 September2023; Springer: Singapore, 2023; pp. 589–599. [Google Scholar]

- Feng, L.; Sun, Z. The Impact of Green Finance Pilot Policy on Carbon Intensity in Chinese Cities—Based on the Synthetic Control Method. Sustainability 2023, 15, 11571. [Google Scholar] [CrossRef]

- Hu, Q.; Xue, J.; Liu, R.; Qiping Shen, G.; Xiong, F. Green building policies in China: A policy review and analysis. Energy Build. 2023, 278, 112641. [Google Scholar] [CrossRef]

- Bungau, C.C.; Bungau, T.; Prada, I.F.; Prada, M.F. Green Buildings as a Necessity for Sustainable Environment Development: Dilemmas and Challenges. Sustainability 2022, 14, 13121. [Google Scholar] [CrossRef]

- Abdel Hay bin Omera, A. The use of green building materials in enhancing sustainable architecture. Int. J. Adv. Res. Plan. Sustain. Dev. 2024, 6, 51–70. [Google Scholar] [CrossRef]

- Lee, W.Y.; Fung, D.W.H. Current deficiencies and reinforcement of institutional pillars for reform in the green insurance market: A systematic review. Eur. J. Sustain. Dev. Res. 2023, 7, 13634. [Google Scholar] [CrossRef]

- Shao, L.; Yang, J.; Zhang, M. Subsidy scheme or price discount scheme? Mass adoption of electric vehicles under different market structures. Eur. J. Oper. Res. 2017, 262, 1181–1195. [Google Scholar] [CrossRef]

- Adetoyese, L.; Ngozi Samuel, U.; Munachi Chikodili, U.; Portia, O. Role and effectiveness of advance payment guarantees in construction contracts. World J. Adv. Sci. Technol. 2024, 6, 88–102. [Google Scholar] [CrossRef]

- Zhang, W.; Zhao, D. China Pilot Zone for Green Financial Reform and Innovation. In Green Finance in China; Contributions to Finance and Accounting; Springer: Berlin/Heidelberg, Germany, 2024; pp. 71–93. [Google Scholar]

- Roberts, R.L. The Relationship Between Rewards, Recognition and Motivation at an Insurance Company in the Western Cape. Ph.D. Thesis, University of the Western Cape, Cape Town, South Africa, 2005. [Google Scholar]

- Yu, E.P.-y.; Luu, B.V.; Chen, C.H. Greenwashing in environmental, social and governance disclosures. Res. Int. Bus. Financ. 2020, 52, 101192. [Google Scholar] [CrossRef]

- Dongguan Green Building Association China. Policy Promotion of the Coordinated Development of Green Building Industry and Green Finance and the Launch Ceremony of the Energy Conservation Publicity Month in the Construction Field of Dongguan in 2024. Available online: https://mp.weixin.qq.com/s?__biz=MzIxNjQ3Mzk1NA==&mid=2247645263&idx=1&sn=c27a02ee8b539ecf49d85a61b4022113&chksm=962acbe34099d408917162425d81531c3efc02efd820363eb2625f1c8543914858c11a7e77ad&scene=27 (accessed on 23 March 2025).

- Pugnetti, C.; Gebert, T.; Hürster, M.; Huizenga, E.; Moor, M.; Stricker, L.; Winistörfer, H.; Zeier Röschmann, A. Leading the Green Insurance Revolution; ZHAW School of Management and Law: Winterthur, Switzerland, 2022. [Google Scholar]

- Ministry of Housing and Urban–Rural Development; National Development and Reform Commission; Ministry of Education; Ministry of Industry and Information Technology; People’s Bank of China; China Banking and Insurance Regulatory Commission. The Green Building Creation Action Plan. Available online: https://www.gov.cn/zhengce/zhengceku/2020-07/24/content_5529745.htm (accessed on 24 January 2025).

| Objective Layers | First-Level Drivers | Second-Level Drivers | Third-Level Drivers | |||

|---|---|---|---|---|---|---|

| Dimensions | Code | Drivers | Code | Drivers | Code | |

| Driver system for the acceptance of green housing insurance | Pull | L | Policy incentives | L1 | Premium subsidies | L11 |

| Policies and regulations | L12 | |||||

| Regulatory mechanisms | L13 | |||||

| Social stimulation | L2 | Public awareness | L21 | |||

| Public opinion atmosphere | L22 | |||||

| Push | T | Green housing characteristics | T1 | Health and safety | T11 | |

| Environment livability | T12 | |||||

| Living convenience | T13 | |||||

| Resource conservation | T14 | |||||

| Insurance function | T2 | Economic compensation | T21 | |||

| Risk management | T22 | |||||

| Order maintenance | T23 | |||||

| Basic Information | Category | Survey Methods | Frequency of Valid Respondents | Ratio (%) | Basic Information | Category | Frequency of Valid Respondents | Ratio (%) |

|---|---|---|---|---|---|---|---|---|

| Profession | Owners of green housing | Distributed on-site and website | 240 | 80.81 | Age | 22–30 | 36 | 15.00 |

| 31–50 | 180 | 75.00 | ||||||

| 51–65 | 24 | 10.00 | ||||||

| Total | 240 | 100 | ||||||

| Department directors of property management companies | Distributed on-site and website | 13 | 4.37 | Working years | 5–10 years | 15 | 26.32 | |

| Department directors of insurance companies | Face-to-face, telephone and email | 31 | 10.44 | |||||

| 11–20 years | 28 | 49.12 | ||||||

| Staff of local construction authorities | Face-to-face, telephone and email | 7 | 2.36 | |||||

| Over 20 years | 14 | 24.56 | ||||||

| Others institutions including design organizations, consultant firms and research institutions | Website and telephone | 6 | 2.02 | |||||

| Total | - | 297 | 100 | Total | 57 | 100 |

| Driver Variables | Cronbach’s Alpha |

|---|---|

| Premium subsidies | 0.896 |

| Policies and regulations | 0.900 |

| Regulatory mechanisms | 0.898 |

| Public awareness | 0.901 |

| Public opinion atmosphere | 0.898 |

| Health and safety | 0.891 |

| Environment livability | 0.888 |

| Living convenience | 0.895 |

| Resource conservation | 0.891 |

| Economic compensation | 0.900 |

| Risk management | 0.897 |

| Order maintenance | 0.902 |

| Overall scale variables | 0.904 |

| Index Name | GOF Measures | Initial SEM | Recommended Levels | Evaluation |

|---|---|---|---|---|

| Absolute fit index | X2/df | 1.973 | 1.00–3.00 | Acceptable |

| Goodness-of-fit index (GFI) | 0.945 | >0.9 | Acceptable | |

| Adjusted goodness-of-fit index (AGFI) | 0.904 | >0.9 | Acceptable | |

| Root mean square residual (RMR) | 0.032 | <0.05 | Acceptable | |

| Root mean square error of approximation (RMSEA) | 0.042 | <0.05 | Acceptable | |

| Comparative fit index | Normed fit index (NFI) | 0.903 | >0.9 | Acceptable |

| Comparative fit index (CFI) | 0.904 | >0.9 | Acceptable | |

| Relative fit index (RFI) | 0.922 | >0.9 | Acceptable | |

| Parsimony fit index | Akaike information criterion (AIC) | 96.426 | Smaller is better | Acceptable |

| Consistent akaike information criterion (CAIC) | 187.339 | Smaller is better | Acceptable |

| Path Relationship | Standardized Path Coefficients | S.E. | C.R. | p | ||

|---|---|---|---|---|---|---|

| L | ← | Accept green housing insurance | 0.916 | |||

| T | ← | Accept green housing insurance | 0.806 | 0.122 | 9.609 | *** |

| T1 | ← | Push dimension | 0.862 | 0.110 | 7.789 | *** |

| T2 | ← | Push dimension | 0.826 | 0.121 | 10.278 | *** |

| L1 | ← | Pull dimension | 0.845 | |||

| L2 | ← | Pull dimension | 0.674 | 0.124 | 10.254 | *** |

| L11 | ← | Policy incentives | 0.744 | |||

| L12 | ← | Policy incentives | 0.691 | 0.113 | 13.201 | *** |

| L13 | ← | Policy incentives | 0.618 | 0.168 | 9.433 | *** |

| L21 | ← | Social stimulation | 0.822 | |||

| L22 | ← | Social stimulation | 0.780 | 0.085 | 7.671 | *** |

| T11 | ← | Green housing characteristics | 0.714 | |||

| T12 | ← | Green housing characteristics | 0.708 | 0.073 | 10.271 | *** |

| T13 | ← | Green housing characteristics | 0.694 | 0.087 | 10.385 | *** |

| T14 | ← | Green housing characteristics | 0.670 | 0.112 | 9.178 | *** |

| T21 | ← | Insurance function | 0.823 | |||

| T22 | ← | Insurance function | 0.690 | 0.096 | 9.661 | *** |

| T23 | ← | Insurance function | 0.668 | 0.082 | 10.048 | *** |

| First-Level Drivers | Standardized Path Coefficients | Relative Importance Weights | Ranking |

|---|---|---|---|

| L | 0.916 | 0.532 | 1 |

| T | 0.806 | 0.468 | 2 |

| Second-Level Drivers | Standardized Path Coefficients | Relative Importance Weights | Ranking |

|---|---|---|---|

| L1 | 0.845 | 0.449 | 1 |

| L2 | 0.674 | 0.359 | 4 |

| T1 | 0.862 | 0.403 | 2 |

| T2 | 0.826 | 0.387 | 3 |

| Second-Level Drivers | Third-Level Drivers | Standardized Path Coefficients | Relative Importance Weights | Ranking in All | Ranking Within Each Dimension |

|---|---|---|---|---|---|

| L1 (0.449) | L11 | 0.744 | 0.334 | 1 | 1 |

| L12 | 0.691 | 0.311 | 3 | 2 | |

| L13 | 0.618 | 0.278 | 9 | 3 | |

| L2 (0.359) | L21 | 0.822 | 0.295 | 4 | 1 |

| L22 | 0.780 | 0.280 | 7 | 2 | |

| T1 (0.403) | T11 | 0.714 | 0.288 | 5 | 1 |

| T12 | 0.708 | 0.286 | 6 | 2 | |

| T13 | 0.694 | 0.280 | 7 | 3 | |

| T14 | 0.670 | 0.270 | 10 | 4 | |

| T2 (0.387) | T21 | 0.823 | 0.318 | 2 | 1 |

| T22 | 0.690 | 0.267 | 11 | 2 | |

| T23 | 0.668 | 0.258 | 12 | 3 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

She, Y.; Pu, N.; Wang, Y.; Li, J.; Peng, X.; Lv, Q.; Ma, M. Drivers for the Acceptance of Green Housing Insurance from the Perspective of House Owners. Buildings 2025, 15, 1241. https://doi.org/10.3390/buildings15081241

She Y, Pu N, Wang Y, Li J, Peng X, Lv Q, Ma M. Drivers for the Acceptance of Green Housing Insurance from the Perspective of House Owners. Buildings. 2025; 15(8):1241. https://doi.org/10.3390/buildings15081241

Chicago/Turabian StyleShe, Yujuan, Nan Pu, Ying Wang, Jiahao Li, Xinyi Peng, Qiguang Lv, and Mingxue Ma. 2025. "Drivers for the Acceptance of Green Housing Insurance from the Perspective of House Owners" Buildings 15, no. 8: 1241. https://doi.org/10.3390/buildings15081241

APA StyleShe, Y., Pu, N., Wang, Y., Li, J., Peng, X., Lv, Q., & Ma, M. (2025). Drivers for the Acceptance of Green Housing Insurance from the Perspective of House Owners. Buildings, 15(8), 1241. https://doi.org/10.3390/buildings15081241