The Absolute Ruin Insurance Risk Model with a Threshold Dividend Strategy

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Integro-Differential Equations for and

- (1)

- For , as discussed in Albrecher et al. [23], and using the strong Markov property of the risk reserve process , we obtainwhere, is the high order infinitesimal of t when , i.e., .By Taylor expansion,

- (2)

- The above method is applied to when , and we haveBy Taylor expansion,

- (3)

- For , the same argument as in the proof of (10) givesBy Taylor expansion, we have (11). ☐

- (1)

- (2)

- For (18), when , we have

- (3)

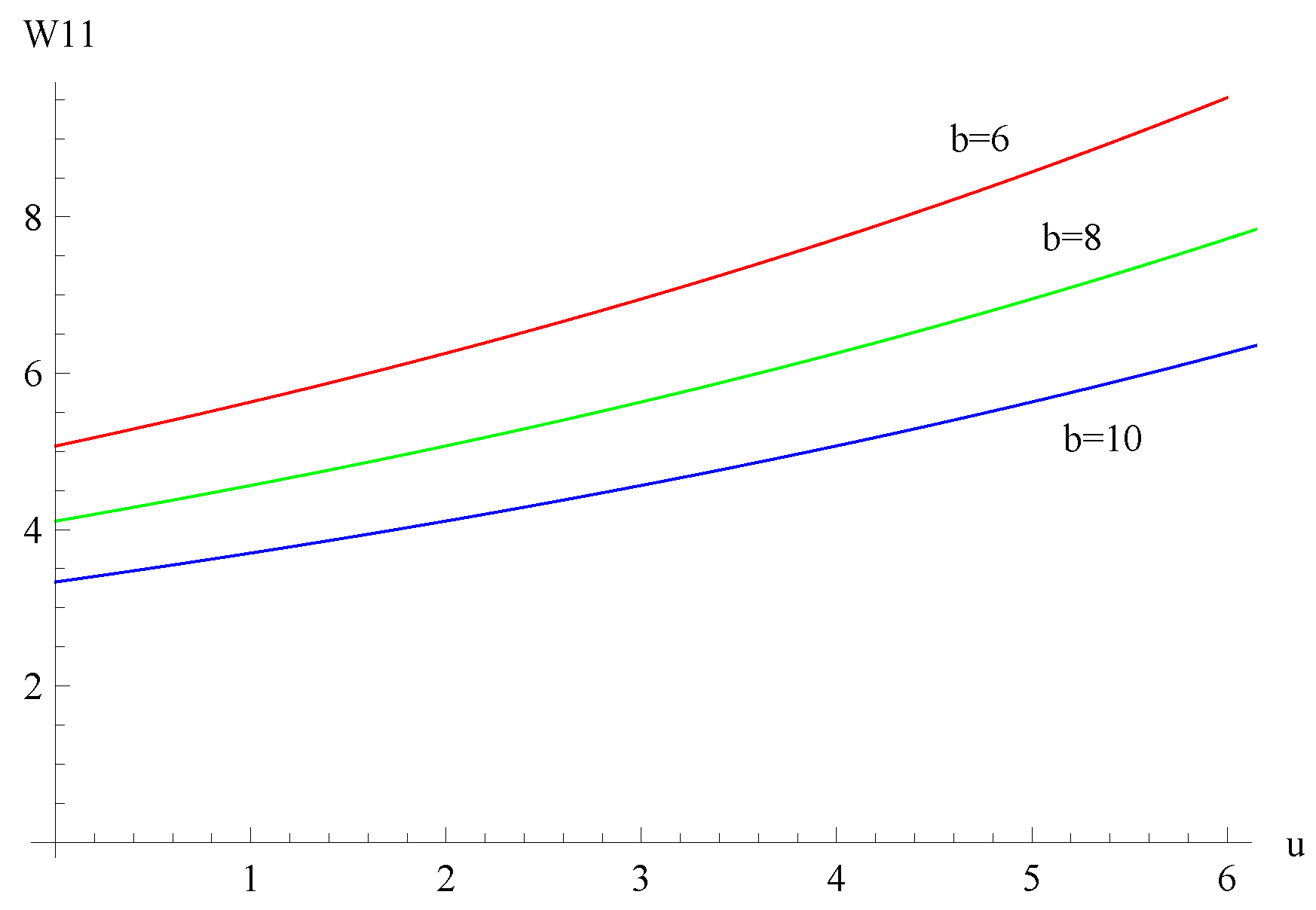

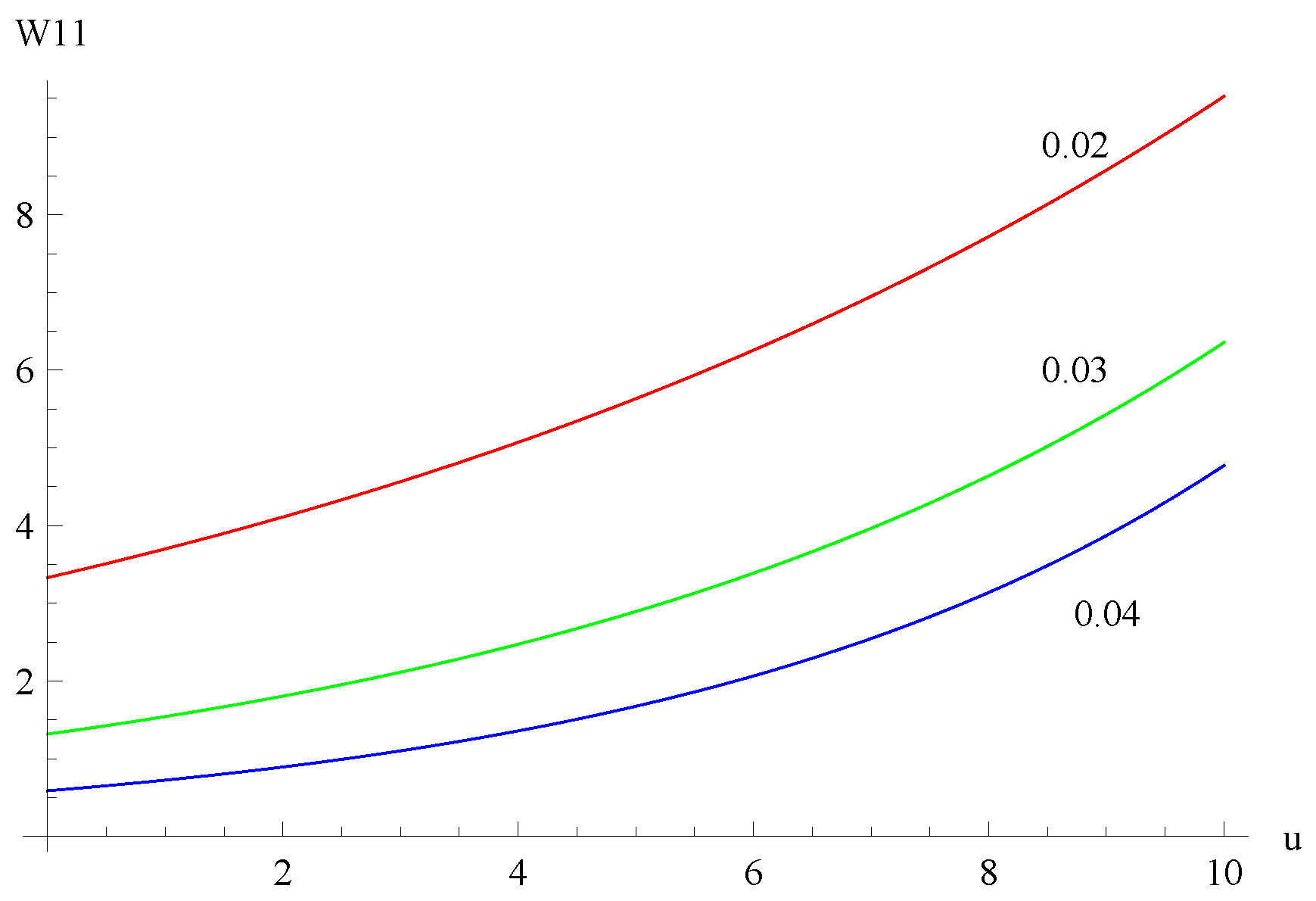

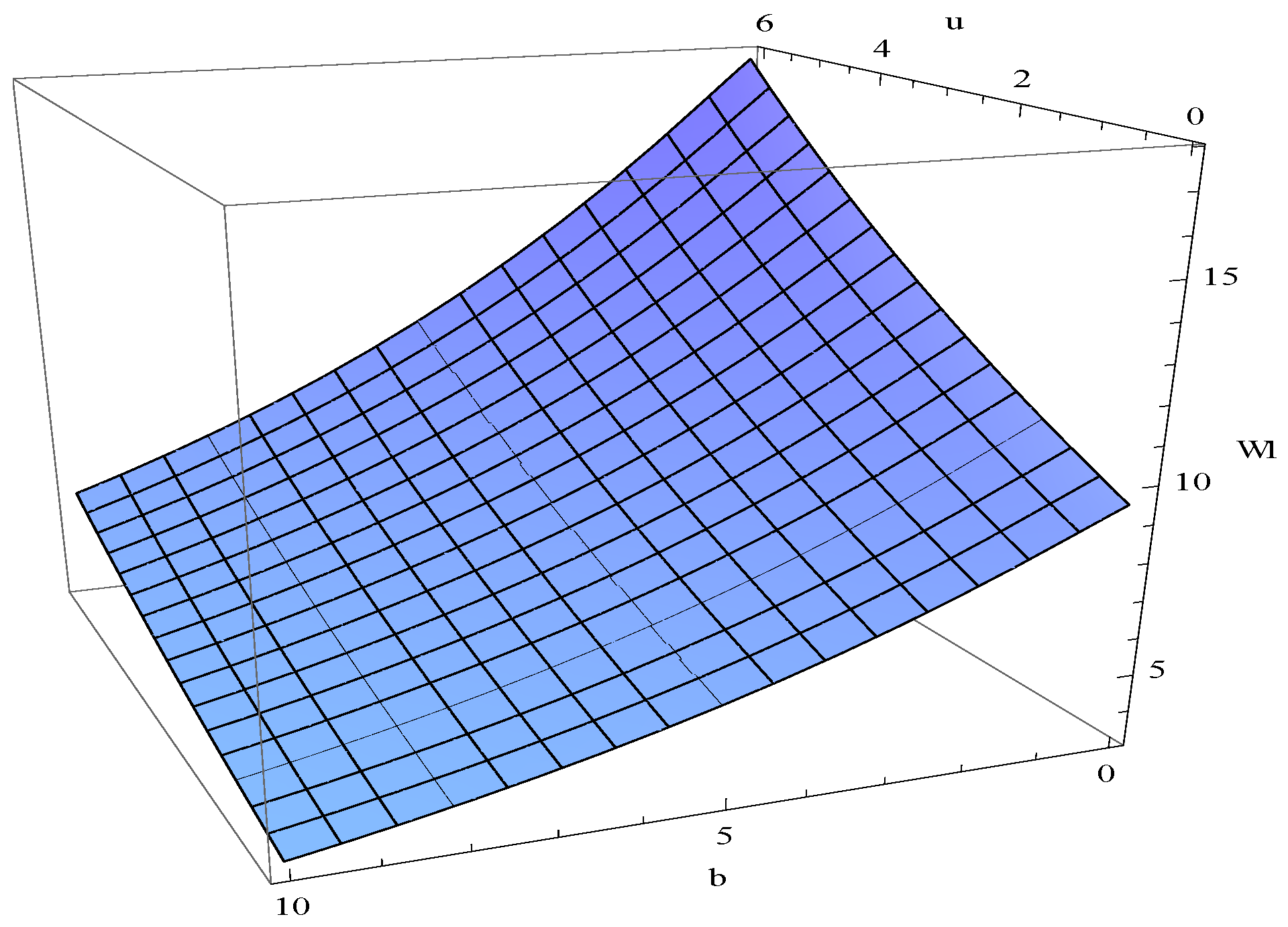

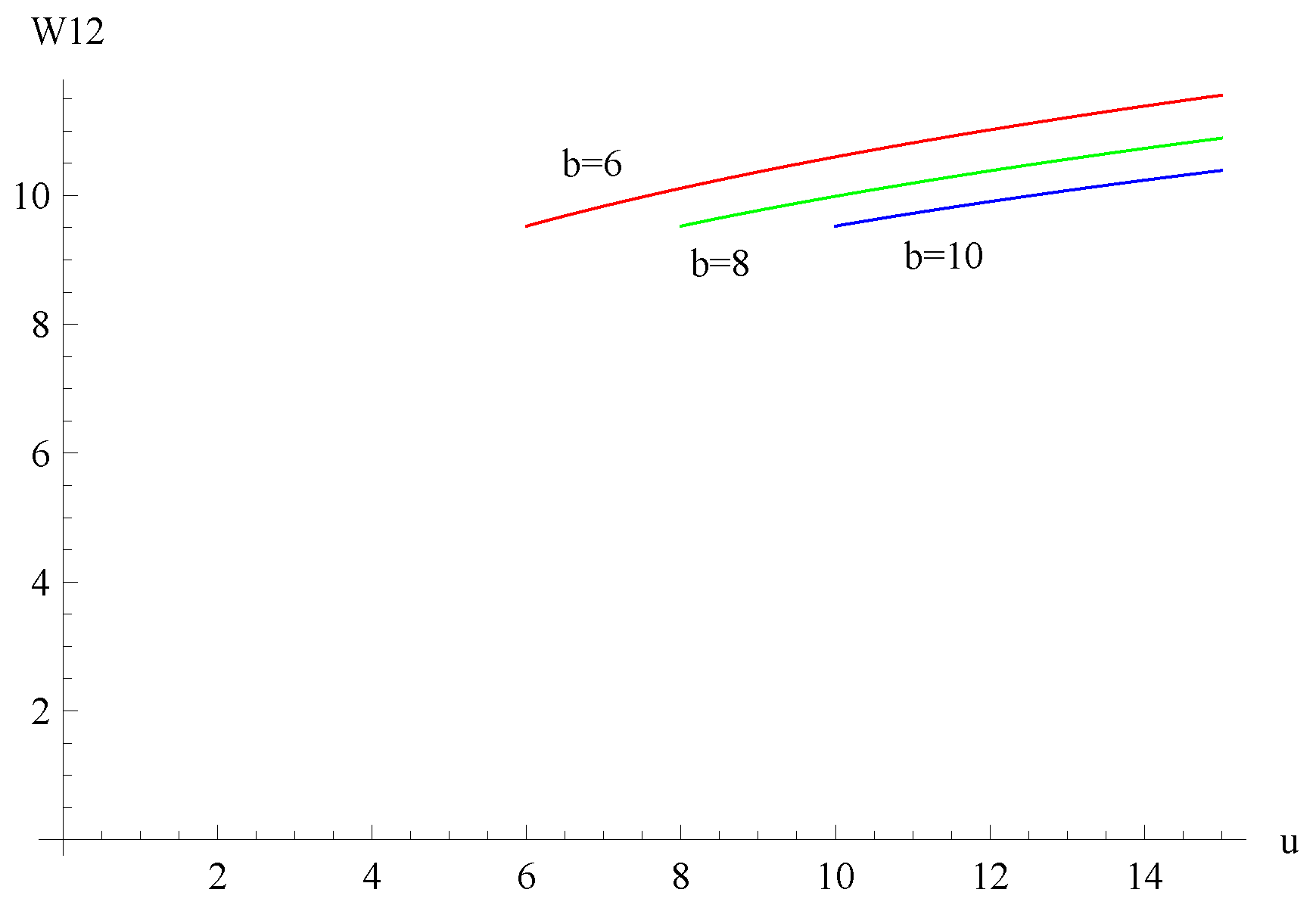

3. Explicit Expressions for Exponential Claims to and Numerical Examples

4. The Gerber-Shiu Expected Discounted Penalty Function

5. The Laplace Transform of Absolute Ruin Time

6. The Time to Reach the Dividend Barrier

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Cai, J. On the time value of absolute ruin with debit interest. Adv. Appl. Probab. 2007, 39, 343–359. [Google Scholar] [CrossRef]

- Wang, C.W.; Yin, C.C. Dividend payments in the classical risk model under absolute ruin with debit interest. Appl. Stoch. Model. Bus. 2009, 25, 247–262. [Google Scholar] [CrossRef]

- Wang, C.W.; Yin, C.C.; Li, E.Q. On the classical risk model with credit and debit interests under absolute ruin. Stat. Probab. Lett. 2010, 80, 427–436. [Google Scholar] [CrossRef]

- Yuan, H.L.; Hu, Y.J.; Qin, Q.Q. Absolute ruin problems for the risk process with interest and a constant dividend barrier. Wuhan Univ. J. Nat. Sci. 2011, 16, 199–205. [Google Scholar] [CrossRef]

- Peng, D.; Liu, D.H.; Hou, Z.T. Absolute ruin problems in a compound Poisson risk model with constant dividend barrier and liquid reserves. Adv. Differ. Equ. 2016, 2016. [Google Scholar] [CrossRef]

- Wang, C.W.; Du, X.G.; Chen, Q.Y. On the compound Poisson risk model with debit interest and a threshold dividend strategy. In Proceedings of the Information Computing and Applications: Second International Conference ICICA, Qinhuangdao, China, 28–31 October 2011; Volume 243, pp. 596–603. [Google Scholar]

- Li, S.M.; Lu, Y. Moments of the dividend payments and related problems in a Markov-modulated risk model. N. Am. Actuar. J. 2007, 11, 65–76. [Google Scholar] [CrossRef]

- Huu, N.V.; Hoang, V.Q.; Ngoc, T.M. Central limit theorem for functional of jump Markov processes. Vietnam J. Math. 2005, 33, 443–461. [Google Scholar]

- Luo, S.Z.; Taksar, M. On absolute ruin minimization under a diffusion approximation model. Insur. Math. Econ. 2011, 48, 123–133. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, J.; Gao, Q. Asymptotics for the infinite-time absolute ruin probabilities in time-dependent renewal risk models. Sci. Sin. Math. 2013, 43, 173–184. [Google Scholar] [CrossRef]

- Yang, Y.; Wang, K.Y.; Liu, J. Asymptotics and uniform asymptotics for finite-time and infinite-time absolute ruin probabilities in a dependent compound renewal risk model. J. Math. Anal. Appl. 2013, 398, 352–361. [Google Scholar] [CrossRef]

- Yu, W.G. Some results on absolute ruin in the perturbed insurance risk model with investment and debit interests. Econ. Model. 2013, 31, 625–634. [Google Scholar] [CrossRef]

- Cai, J.; Yang, H.L. On the decomposition of the absolute ruin probability in a perturbed compound Poisson surplus process with debit interest. Ann. Oper. Res. 2014, 212, 61–77. [Google Scholar] [CrossRef]

- Zhu, J.X. Optimal dividend control for a generalized risk model with investment incomes and debit interest. Scand. Actua. J. 2013, 2013, 140–162. [Google Scholar] [CrossRef]

- Zhu, J.X. Singular optimal dividend control for the regime-switching Cramér-Lundberg model with credit and debit interest. J. Comput. Appl. Math. 2014, 257, 212–239. [Google Scholar] [CrossRef]

- Bi, X.C.; Zhang, S.G. Minimizing the risk of absolute ruin under a diffusion approximation model with reinsurance and investment. J. Syst. Sci. Complex. 2015, 28, 144–155. [Google Scholar] [CrossRef]

- Liu, J.J.; Yang, Y. Infinite-time absolute ruin in dependent renewal risk models with constant force of interest. Stoch. Models. 2017, 33, 97–115. [Google Scholar] [CrossRef]

- Zeng, Y.; Li, Z. Optimal time-consistent investment and reinsurance policies for mean-variance insurers. Insur. Math. Econ. 2011, 49, 145–154. [Google Scholar] [CrossRef]

- Zeng, Y.; Li, D.; Chen, Z.; Yang, Z. Ambiguity aversion and optimal derivative-based pension investment with stochastic income and volatility. J. Econ. Dyn. Control. 2018, 88, 70–103. [Google Scholar] [CrossRef]

- Peng, J.Y.; Wang, D.C. Asymptotics for ruin probabilities of a non-standard renewal risk model with dependence structures and exponential Lévy process investment returns. J. Ind. Manag. Optim. 2017, 13, 155–185. [Google Scholar]

- Peng, J.Y.; Wang, D.C. Uniform asymptotics for ruin probabilities in a dependent renewal risk model with stochastic return on investments. Stochastics. 2018, 90, 432–471. [Google Scholar] [CrossRef]

- Avram, F.; Perez, J.; Yamazaki, K. Spectrally negative Lévy processes with Parisian reflection below and classical reflection above. Stoch. Proc. Appl. 2018, 128, 255–290. [Google Scholar] [CrossRef]

- Albrecher, H.; Claramunt, M.; Marmol, M. On the distribution of dividend payments in a Sparre Andersen model with generalized Erlang(n) interclaim times. Insur. Math. Econ. 2005, 37, 324–334. [Google Scholar] [CrossRef]

- Wan, N. Dividend payments with a threshold strategy in the compound Poisson risk model perturbed by diffusion. Insur. Math. Econ. 2007, 40, 509–532. [Google Scholar] [CrossRef]

- Paulsen, J.; Gjessing, H.K. Ruin theory with stochastic economic environment. Adv. Appl. Probab. 1997, 29, 965–985. [Google Scholar] [CrossRef]

- Cai, J.; Yang, H.L. Ruin in the perturbed compound Poisson risk process under interest force. Adv. Appl. Probab. 2005, 37, 819–835. [Google Scholar] [CrossRef]

- Salter, L.J. Confluent Hypergeometric Functions; Cambridge University Press: London, UK, 1960. [Google Scholar]

- Seaborn, J.B. Hypergeometric Functions and Their Applications; Springer: New York, NY, USA, 1991. [Google Scholar]

- Cai, J.; Dickson, D.C.M. On the expected discounted penalty function at ruin of a surplus process with interest. Insur. Math. Econ. 2002, 30, 389–404. [Google Scholar] [CrossRef]

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, W.; Huang, Y.; Cui, C. The Absolute Ruin Insurance Risk Model with a Threshold Dividend Strategy. Symmetry 2018, 10, 377. https://doi.org/10.3390/sym10090377

Yu W, Huang Y, Cui C. The Absolute Ruin Insurance Risk Model with a Threshold Dividend Strategy. Symmetry. 2018; 10(9):377. https://doi.org/10.3390/sym10090377

Chicago/Turabian StyleYu, Wenguang, Yujuan Huang, and Chaoran Cui. 2018. "The Absolute Ruin Insurance Risk Model with a Threshold Dividend Strategy" Symmetry 10, no. 9: 377. https://doi.org/10.3390/sym10090377

APA StyleYu, W., Huang, Y., & Cui, C. (2018). The Absolute Ruin Insurance Risk Model with a Threshold Dividend Strategy. Symmetry, 10(9), 377. https://doi.org/10.3390/sym10090377