Since Hurricanes Katrina and Rita of 2005, risk awareness has grown among stakeholders of coastal Louisiana communities facing increasing flood risks from sea-level rise, intense storms and land subsidence. Like many other coastal regions, population growth along the Louisiana coast combined with limited land use planning has exacerbated these risks. For example, by the end of the 21st century, annual flood costs in the United States could increase from $2 billion to $7–$19 billion because of climate change, urbanization and urban emissions [

1]. The National Flood Insurance Program (NFIP), designed to provide affordable insurance to property owners in flood-prone areas, is running a $25 billion deficit in the wake of recent catastrophic storms [

2]. Efforts by the U.S. Congress in 2012 to increase policyholders’ premiums to more accurately cover the costs of property insurance in high risk regions were met with intense opposition from coastal stakeholders [

3,

4]. Given the inherent political and scientific challenges involved in setting and collecting higher premium rates for NFIP policyholders, the role to be played by local communities in formulating and implementing proactive planning to reduce overall exposure risks becomes even more important.

The Community Rating System (CRS) of the NFIP provides incentives to local communities to enact collective measures to mitigate flood risks. This analysis builds on the earlier work of several studies that examined contextual factors that may explain variation in CRS participation and helped shed light on the conditions under which local collective action may be more likely. This is especially relevant for researchers and stakeholders of Louisiana, where no previous study has examined CRS participation and given the historical ambivalence among counties and local communities concerning planning and land use management efforts [

5]. Although proactive planning could help Louisiana communities increase resiliency to large-scale disturbances, enacting such land use plans requires technical information, economic resources and political will. As a result, collective actions may be more difficult to formulate and implement in some communities.

The objectives of this study are to examine the CRS participation rates and performance of parishes (counties) in south Louisiana and to identify key factors associated with greater implementation of the CRS flood risk-reducing measures.

1.1. The Community Rating System

The CRS is a voluntary incentive program designed to encourage communities to implement structural and non-structural flood risk-reduction measures beyond minimum NFIP requirements. Participating communities are evaluated and given a score based on the number of planning milestones they have met. The CRS scores reflect a range of activities, including implementation of land-use controls, such as preservation of floodplain as open space, regulation of development in flood-risk areas and watersheds and development of a comprehensive floodplain management plan. These measures result in a discounted flood insurance rate for National Flood Insurance Program (NFIP) policyholders in that community. NFIP discounts flood insurance rates based on a point system that ranges from 5% to 45%, increasing in 5% increments, corresponding to the score, or total number of points received [

6,

7].

CRS communities vary in size and may include local municipalities and parishes. Each jurisdiction within a parish has the opportunity to participate in the CRS program and is not considered part of a county-wide CRS program. In other words, if decision makers of an incorporated municipality want CRS program discounts, they must enact their own separate CRS program, distinct from the county program. Thus, the county-level CRS programs cover residents and communities within the unincorporated areas of the county.

The CRS program seeks to further three broad goals: to reduce and avoid flood damage to insurable property; to strengthen and support insurance aspects of the NFIP; and to foster comprehensive floodplain management. Following reorganization in 2013, the program focuses on six core flood-loss reduction areas: reduction of liabilities to the NFIP fund; improvement of disaster resiliency and sustainability of communities; integration of a “Whole Community” approach to address emergency management; promotion of natural and beneficial functions of floodplains; increased understanding of risk; and adoption and enforcement of disaster-resistant building codes [

6]. The CRS encourages 19 activities or measures, organized into four categories: public information, mapping and regulations, flood damage reduction (structural and non-structural) and flood preparedness. Communities can also request that FEMA review other flood risk-reduction measures not listed in the program for additional CRS points.

Table 1 summarizes the types of planning and policy activities that are encouraged through the CRS program. The table shows the various activities under which communities can earn points through the CRS program, grouped into four categories (Series 300, 400, 500, 600). Each activity has a maximum number of points obtainable; however, most communities do not obtain the maximum amount of points. An average for all CRS communities in the program and an average for Louisiana communities are also included as a reference.

Table 1.

The Community Rating System (CRS) activities and credit point system [

6,

7].

Table 1.

The Community Rating System (CRS) activities and credit point system [6,7].

| Series 300 | Public Information | Maximum Points | National Average | Louisiana Average |

| 310 | Elevation Certificates | 162 | 68 | 66 |

| 320 | Map Information Service | 140 | 140 | 140 |

| 330 | Outreach Projects | 380 | 99 | 80 |

| 340 | Hazard Disclosure | 81 | 14 | 15 |

| 350 | Flood Protection Information | 102 | 45 | 46 |

| 360 | Flood Protection Assistance | 71 | 47 | 51 |

| 370 | Flood Insurance Promotion * | 0 | 0 | 0 |

| | Total | 936 | 413 | 398 |

| Series 400 | Mapping and regulations | Maximum Points | National Average | Louisiana Average |

| 410 | Additional Flood Data | 1346 | 89 | 56 |

| 420 | Open Space Preservation | 900 | 182 | 93 |

| 430 | Higher Regulatory Standards | 2740 | 291 | 167 |

| 440 | Flood Data Maintenance | 239 | 97 | 82 |

| 450 | Stormwater Management | 670 | 111 | 71 |

| | Total | 5895 | 770 | 469 |

| Series 500 | Flood Damage Reduction | Maximum Points | National Average | Louisiana Average |

| 510 | Floodplain Management Planning | 359 | 129 | 135 |

| 520 | Acquisition and Relocation | 3200 | 237 | 121 |

| 530 | Flood Protection | 2800 | 79 | 68 |

| 540 | Drainage System Maintenance | 330 | 201 | 224 |

| | Total | 6689 | 646 | 548 |

| Series 600 | Flood Preparedness | Maximum Points | National Average | Louisiana Average |

| 610 | Flood Warning Program | 255 | 93 | 110 |

| 620 | Levee Safety | 900 | 93 | 0 |

| 630 | Dam Safety | 175 | 63 | 69 |

| | Total | 1330 | 249 | 179 |

1.1.1. Public Information Activities (300 Series)

Measures under this category include those that advise people about the flood hazard, encourage the purchase of flood insurance and provide information about ways to reduce flood damage. These activities also generate data needed by insurance agents for accurate flood insurance rating. They generally serve all members of the community.

1.1.2. Mapping and Regulations (400 Series)

This series credits programs that provide increased protection to new development. These activities include mapping areas not shown on the Flood Insurance Rate Maps (FIRMs), preserving open space, protecting natural floodplain functions, enforcing higher regulatory standards and managing stormwater. The credit is increased for growing communities.

1.1.3. Flood Damage Reduction Activities (500 Series)

These measures attempt to protect existing development, which is considered to be at risk within the participating jurisdiction. Credit is provided for a comprehensive floodplain management plan, relocating or retrofitting flood-prone structures and maintaining drainage systems.

1.1.4. Warning and Response (600 Series)

This series provides credit for measures that protect life and property during a flood, through flood warning and response programs. There is credit for the maintenance of levees and dams and also for programs that prepare for their potential failure.

Community class rankings in the CRS range from 1 to 10. A Class 1 community can receive the highest insurance rate discount of 45%. A Class 9 community can receive a 5% discount. A Class 10 community either has failed to receive a minimum number of points or has become inactive in the program and does not receive a discount. In order for a community to become a member of the CRS program, it must be in good standing with NFIP regulations (has adopted and enforced NFIP floodplain management regulations that conform to NFIP standards) and appoint a CRS coordinator to handle all application work. Further, the CRS requires that communities actually implement these plans and monitor activities annually as a condition for renewal. Each year, communities must re-certify under the CRS program to ensure that the community is still performing the tasks for which it has received CRS points. Furthermore, a new CRS class will not be enacted until the next point tier is reached. Therefore, a community with 1000 points will have the same CRS class of 8 as a community with 1498 points. CRS class changes occur in May and October of each year. If the community does not renew each year, its residents will lose any NFIP rate discounts [

8,

9]. It is noteworthy that residents living in the more flood-prone Special Flood Hazard Area (SFHA) are required to have flood insurance, and most purchase policies through the NFIP.

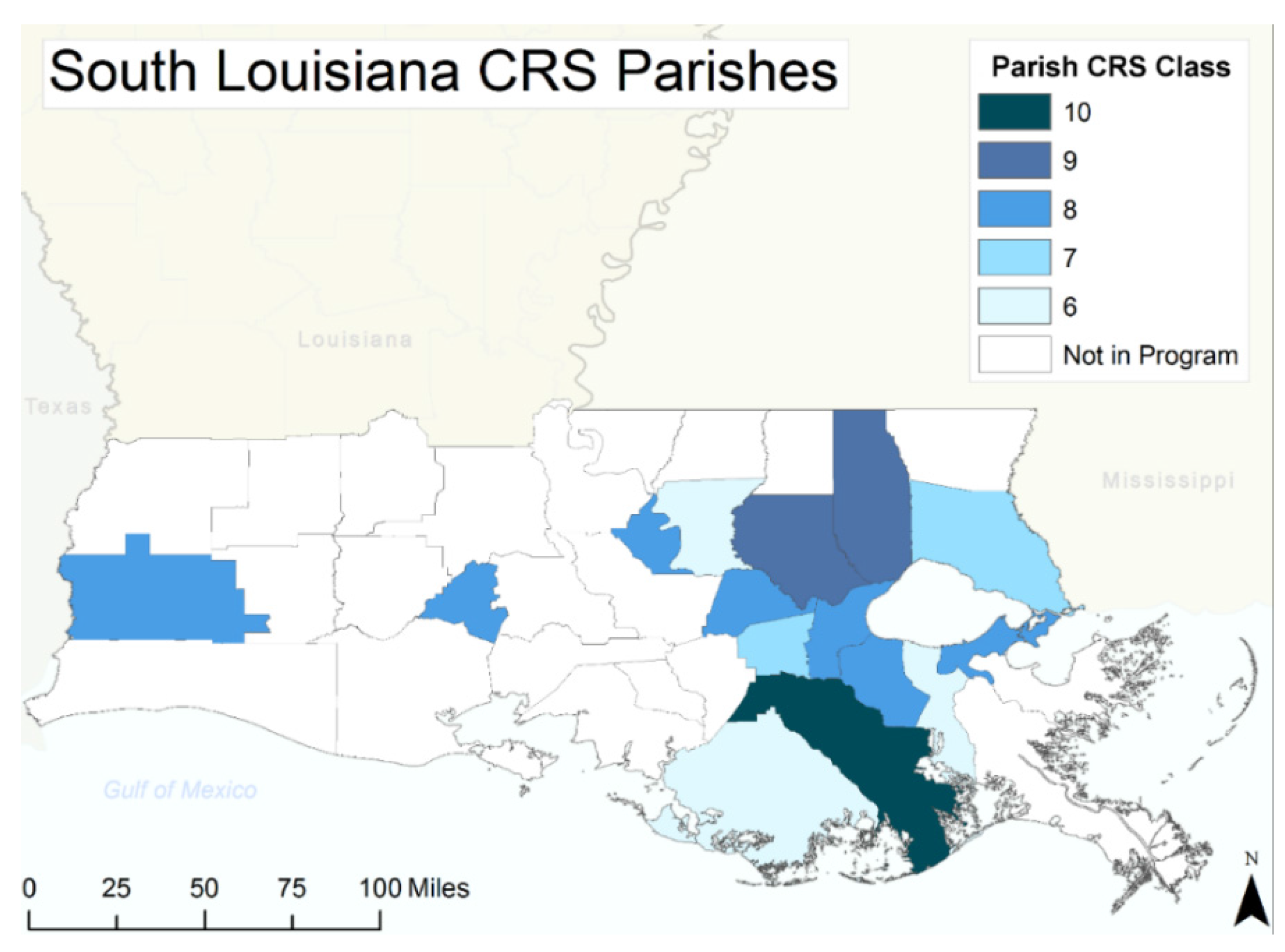

Table 2 displays the NFIP insurance premium reductions associated with the total CRS points and the number of Louisiana parishes in each of the rate-reduction categories.

Table 2.

The CRS points and classification system [

6]. SFHA, Special Flood Hazard Area.

Table 2.

The CRS points and classification system [6]. SFHA, Special Flood Hazard Area.

| Credit Points (Score) | Class | Premium Reduction | Number of Louisiana Parishes |

|---|

| (SFHA) | Non-SFHA |

|---|

| 4500+ | 1 | 45% | 10% | 0 |

| 4000–4499 | 2 | 40% | 10% | 0 |

| 3500–3999 | 3 | 35% | 10% | 0 |

| 3000–3499 | 4 | 30% | 10% | 0 |

| 2500–2999 | 5 | 25% | 10% | 0 |

| 2000–2499 | 6 | 20% | 10% | 3 |

| 1500–1999 | 7 | 15% | 5% | 2 |

| 1000–1499 | 8 | 10% | 5% | 8 |

| 500–999 | 9 | 5% | 5% | 2 |

| 0–499 | 10 | 0% | 0% | 1 |

As of October 2015, the CRS program had 1368 participating communities in the United States, or approximately 5% of the total NFIP communities present. Roseville, California, is the only Class 1 ranked community in the United States [

10]. Louisiana currently has 46 communities participating in the program. Of those 46, 16 are parishes and 30 are municipalities of varying size and population [

11].

1.2. CRS Activities and Community Resilience

Historically, Louisiana communities have been slow to adopt planning measures [

12], despite the potential benefits in terms of reducing exposure to flood risks. As a largely rural state, many parishes lack the resources to implement and maintain parish-wide measures, such as open-space preservation or floodplain management. Furthermore, since stakeholders of many smaller and more rural communities do not feel the pressure to implement growth management strategies, they may not recognize the benefits or relevance of planning in terms of disaster prevention and/or flood reduction [

13,

14]. However, smarter growth strategies and other land use planning measures may lessen the vulnerability (and increase the resiliency) of a community [

15,

16]. Common examples of smarter growth strategies include growth restrictions in flood-prone areas and tighter building codes and regulations [

17]. However, as pressure for more development and housing grows, pressure to develop in floodplains increases, and therefore, more individual properties are exposed to risk [

18,

19,

20].

In 2007, the United States Federal Emergency Management Agency (FEMA) ranked Florida, California, Texas, Louisiana and New Jersey respectively as highest risk for flooding based on a composite risk score derived from floodplain area, per capita housing and number of housing. Researchers found that “non-structural” methods, such as those measured by the CRS rating, were more than twice as effective as “structural” measures, such as dams, at reducing the level of damage from flooding [

11,

18]. Furthermore, while structural measures directly reduce flooding risk to property and communities, they can encourage development in flood-prone areas that are now protected by these measures [

2]. Therefore, the types of measures encouraged by the CRS program, such as open space preservation, stormwater management and flood information disclosure, address an obvious need.

In England, the Netherlands and Germany, strong flood mapping tools drive planning decisions, as flood management efforts focus increasingly on non-structural methods. However, these tools still run the risk of remaining just that: tools. These programs still see resistance between central and local governments, individuals and professional planners [

21,

22,

23]. Furthermore, even with increasing flooding events, research suggests individuals and organizations tend to minimize flooding events as recent as 10 years prior and see those events as isolated incidents, which are unlikely to occur again [

18].

The CRS program with its incentives to individual NFIP policyholders, prescription of collective risk-reducing measures and annual evaluation of participating jurisdictions is an important resource for local decision makers seeking to reduce flood exposure risks. Previous research has shown that the CRS program does in fact promote discount-seeking activities [

24,

25]. The CRS program also introduces more interactions between local policy makers and citizens through the creation of specific risk assessments, information sharing and other educational outreach activities. Related research also shows that mitigation measures can be affected at the individual level through public information activities and hazard information disclosure, a large part of the CRS-creditable activities [

26]. As such, the program may enhance public understanding of flood risks. According to Jennifer Gerbasi, the CRS coordinator for Terrebonne parish who was interviewed for this study, the CRS program promotes greater levels of trust in local officials for residents and encourages community-based decision making to reduce flood exposure risks [

27].

Participation in the CRS program may encourage and support several key attributes of more resilient communities, as identified by resilience theorists. For example, Adger [

28] and colleagues identified as a key attribute of resilience the ability to withstand repeated disturbances, like large-scale storms and floods, while still maintaining “essential structures, processes and feedbacks” within the system. The constituent members of resilient communities are able to “self-organize” to carry out essential functions in the aftermath of disturbances and are able to learn from their experiences and to adapt to reduce future exposure risks [

28,

29,

30,

31,

32]. Researchers have observed that the process of recovering from major disturbances presents opportunities for expanded learning environments with greater stakeholder input into collective decisions and consideration of data from multiple sources to gain a more holistic understanding of the risks [

33,

34,

35]. As a result, the public may become more involved, aware and informed of potential risks, and the political will to take collective action may increase.

Despite the opportunity to learn and adapt following large disturbances, lack of available information on flooding, inundation, land use and growth patterns can present challenges for community stakeholders to participate in informed decision making and for decision makers to formulate and implement proactive disaster management planning [

36]. Furthermore, some communities in Louisiana have historically avoided land use planning, as a result of strong private property rights. Prior to Hurricane Katrina in 2005, Louisiana was among the states least likely to limit private property rights regarding planning and development and had not updated state-wide planning mandates put into place in 1927 [

5,

11]. While Hurricane Katrina spurred planning initiatives with the Louisiana Speaks program, Louisiana still lacks large-scale or state-wide planning efforts, with the Coastal Master Plan as the largest current planning effort.

Thus, the CRS program has an important role to play in Louisiana as community stakeholders work to reduce flood exposure risks. What factors may explain variation in parish-level measures for floodplain management and hazard mitigation evaluated under the CRS program? We turn to recent related research that considers the preconditions and attributes of more resilient communities, and the specific influences on CRS participation in particular, to select variables to include in our analysis.

1.3. Factors Associated with Disaster Resilience

In recent years, researchers have attempted to identify the most suitable indicators to assess disaster resilience. For example, in 2010, Cutter and colleagues [

30] introduced the Baseline Resilience Indicator for Communities (BRIC), which is an aggregation of five sub-indexes measuring socioeconomic, institutional, infrastructural and other community capacities and attributes. Furthermore, in 2010, Sherrieb and others [

8] reduced 88 variables to a smaller group of 17 variables representing two components, including social capital and economic development, as indicators of resilience. In 2015, we applied the Resilience Inference Measurement (RIM) model to measure resilience in the 52 counties of the U.S. Gulf Coast region and identified key predictors for the ability of a county to withstand exposure and damages from storms and still maintain or increase in population over time [

37]. Specific factors associated with greater resilience were found to be higher elevation and greater socioeconomic resources.

Several studies have examined influences on community and household-level disaster planning. First, experience with recent floods has been found to be associated with greater community interest in and acceptance of collective planning efforts [

38]. Regarding household-level measures to mitigate damages associated with floods, a survey of Tennessee residents found that individuals living in communities that experienced floods within the last year were more likely to purchase flood insurance policies [

39]. The heightened awareness of flood impacts appears to have influenced residents to take action to protect their property from future floods. It is noteworthy that since 1973, the NFIP has required all properties located within the Special Flood Hazard Area to have flood insurance. However, in the Tennessee study, four years after the flood event, the number of household policies purchased through the NFIP declined, indicating a possible short-term bias in residents’ risk perceptions. Similarly, Browne and Hoyt [

40] found that insurance purchases are highly correlated to the level of flood losses experienced during the previous year. Others showed that proximity to flood hazards increased the likelihood that residents will purchase flood insurance [

41].

Other potential influences on parish-level adaptive planning in general are the capacities and resources of the parish government. Since planning occurs at the sub-federal and sub-state level [

42,

43], the resources available to local policy makers may help shape planning activities and outcomes. County and local governments play an important role both in educating residents about flood risks and developing proactive disaster planning to mitigate future damages [

44]. Larger county governments with more resources and staff may be better able to implement adaptive planning measures. Furthermore, stakeholders of wealthier communities have more assets to protect and inherently have a greater stake in how those assets are protected and, thus, may be likely to support more planning [

10].

Finally, recent studies examining specific influences on CRS participation and implementation of risk-reducing measures point to the importance of hydrological conditions, the socioeconomic attributes of residents and government capacity. Our study builds most directly on the work of Landry and Li (2012) in which they examined the CRS participation of 100 counties in North Carolina from 1991 to 1996 [

45]. They tested the influence of factors, including recent floods, local government capacity, socioeconomic conditions and the number of CRS participating communities within a county on CRS participation. They found that more floodplain management activities among counties with recent flood experience, greater hydrological risk and more local jurisdictions within the county also participating in the CRS program led to higher CRS scores. Sadiq and Noonan (2015) examined CRS activities throughout the nation and how they may be affected by flood risk, local government capacity and the socioeconomic attributes of residents, among other factors. They found that more hazard mitigation planning was associated with wealthier, better-educated residents [

25]. Similarly, other studies have found that wealthier home owners may invest more in the protection of their property, be less willing to relocate and may be more supportive of local hazard mitigation efforts [

44]. In a recent study of Florida counties’ CRS scores, Brody and colleagues found that higher scores were associated with higher socioeconomic capital, recent flood experience and less land area located in a flood plain. Previous research also suggests that the greater amount of floodplain in a county may deter local CRS flood mitigation efforts; the costs of implementing mitigation measures may not outweigh the discount in insurance premiums [

24].

These studies suggest that socioeconomic attributes of residents, county government capacity, physical factors, such as elevation, and experience with recent flood events may influence the level of CRS planning. Thus, we include indicators of these conditions and attributes of the parishes (counties) within the south Louisiana study area.

{kind=link}

{kind=link}