Abstract

Sustainability has become a central concern globally, and efforts to enhance it are being made across various fields. In line with this trend, corporate sustainability reports have become more widely published. These reports provide both financial and non-financial information on a company’s sustainability. In this context, this study aims to, first, analyze the key keywords contained in CEO messages. Second, it examines whether the keywords emphasized by CEOs change in response to shifts in corporate risk under economic uncertainty. Finally, it identifies how the categories of words included in these messages are classified. To address these research questions, text analysis was selected as the methodology. Specifically, a qualitative research approach using text mining and CONCOR analysis was conducted on the text from sustainability report. According to the Term Frequency and Term Frequency-Inverse Document Frequency analyses, the most frequently occurring keywords were ESG, Sustainable, Society, Stakeholders, Growth, Environment, Effort, and Future. Centrality analysis identified the following keywords as having high centrality: Sustainable, ESG, Society, Environment, Growth, Effort, and Stakeholders. Finally, CONCOR analysis revealed four clusters: Eco-friendly Energy, ESG Management, Global Crisis, and Technological Competitiveness. This study is significant in that it analyzes the major keywords and their changes within unstructured text data using text mining and CONCOR analysis, and it suggests the possibility of future quantitative analysis of non-financial information using these keywords.

1. Introduction

In recent years, interest in corporate sustainability has grown both domestically and internationally, and capital market participants have made various efforts to assess it. Corporate sustainability can be evaluated using financial information, but non-financial information offers more comprehensive insights [1]. Financial information is readily available through business or development project reports and financial statements provided by disclosure systems, whereas non-financial information must be collected directly from diverse sources. Consequently, obtaining comprehensive and detailed non-financial information about companies is difficult. However, some companies have recently begun voluntarily providing such information through sustainability reports. In addition, the information efficiency of non-financial information is high [2,3]. These reports present information on each company’s sustainable management activities and performance data related to environmental, social, and governance (ESG) or corporate social responsibility (CSR) initiatives, while also communicating the company’s policy direction and views as non-financial information. Therefore, a company’s sustainability report can greatly assist capital market participants in predicting corporate value.

Sustainability reporting has evolved primarily in Europe. The EU implemented the Non-Financial Reporting Directive (NFRD) in 2014, followed by the development of various systems for sustainability disclosure. Beyond the NFRD, which provides guidelines for disclosing non-financial information, the EU revised its sustainability disclosure regulations to also include sustainability reporting from a financial perspective. As a result, it released a draft of the Corporate Sustainability Reporting Directive (CSRD) in 2021. The following year, it published a draft of the European Sustainability Reporting Standards (ESRS), which serve as the foundation for implementing the CSRD. In July 2023, the EU officially adopted the revised ESRS. According to the ESRS, sustainability reports must include ten standards covering general principles and general disclosure requirements for ESG topics. The general principles define the key concepts and standards applicable to sustainability reporting under the CSRD and require disclosure of material information affecting corporate sustainability. The general disclosure requirements mandate information on sustainability governance structures, risk and opportunity management, the relevance of sustainability to a company’s business model and strategy, and methods used to measure or progress in performance indicators and targets.

South Korea has also been working to align with this trend. For instance, in January 2021, the Financial Services Commission announced plans to make sustainability reporting mandatory. Under this plan, disclosure was voluntary until 2025, after which it would apply to companies listed on the securities market with total assets exceeding KRW 2 trillion, expanding to all Korea Composite Stock Price Index-listed companies by 2030. However, the mandatory implementation of ESG disclosure, originally scheduled for 2025, has been postponed by more than 1 year to 2026 or later.

Current sustainability reports voluntarily disclosed in South Korea are freely prepared by companies, which select their own initiatives without adhering to specific formats or guidelines, unlike business reports or corporate governance disclosures. As a result, the content and structure of sustainability reports vary significantly across companies. However, specific disclosure guidelines are expected in the future, increasing the likelihood that reports will adopt a standardized and more formulaic format. In addition, because sustainability report disclosure is currently not mandatory, the voluntary disclosure status and content of these reports can substantially affect corporate value.

Sustainability reports primarily contain financial and non-financial information regarding CSR, ESG, and future outlooks. CSR (Corporate Social Responsibility) refers to activities through which a company contributes to society by adhering to regulations and ethical conduct in its pursuit of profit, and it can be viewed as an integral part of the management process. Consequently, CSR cannot be measured simply and can lead to various outcomes [4,5]. Meanwhile, ESG has recently gained prominence alongside CSR. ESG aims to drive sustainable development through the implementation of environmental, social, and governance principles, and it is primarily utilized to measure a company’s non-financial performance in those specific areas. ESG and CSR are closely interconnected and provide investors with core information about a company [6,7].

Sustainability reports provide non-financial information related to a company’s sustainability, which is closely linked to individual corporate value. Corporate value assessments use estimates of current and future profits, drawing on both financial and non-financial information to predict future performance. In recent times, the types and volume of non-financial information used to assess corporate sustainability have increased considerably. Capital market participants are also actively utilizing this information. The growing reliance on non-financial information is closely tied to changes in the economic environment. In recent years, Economic Policy Uncertainty (EPU) has risen significantly, largely due to the impact of the COVID-19 pandemic [8].

COVID-19, first reported in China in 2019, spread worldwide, profoundly altering individual lifestyles and disrupting corporate management activities. Its spread led to the implementation of social distancing measures and border closures across the globe, changing personal living conditions and imposing significant constraints on corporate operations [8]. As the pandemic persisted, capital markets experienced severe turmoil, and market uncertainty increased sharply [9,10,11]. Consequently, demand for information on corporate sustainability grew, and the usefulness of such information increased substantially.

This study conducts text analysis on CEO messages, which constitute non-financial information disclosed in sustainability reports. Since CEOs hold the highest level of responsibility and authority within companies, their messages in these reports serve as signals of corporate prospects. Therefore, CEO messages can be regarded as key non-financial information useful for evaluating corporate sustainability.

Therefore, this study extracts CEO messages from sustainability reports published between 2021 and 2023 to analyze trends in the keywords contained within them. Through this, it aims to identify the primary non-financial information CEOs intend to convey and how this information has changed.

A CEO represents the company. As a key decision-maker responsible for corporate operations, the CEO plays a critical role in determining firm performance [12]. CEOs can communicate their messages through various channels, such as public disclosures, social media or letters. These messages allow for the identification of a company’s operational direction and key priorities; thus, analyzing them is of great importance [13].

While some prior studies have analyzed CEO messages, they remain limited [14,15,16,17,18,19,20]. Previous research has primarily focused on comparative analyses of specific industries (e.g., construction) or large global enterprises before and after the COVID-19 pandemic [21,22]. However, few studies have examined the long-term trends of CEO messages, and none have analyzed what specific messages CEOs prioritize during periods of high risk. This study contributes to the literature by analyzing the annual trends of CEO messages and identifying the keywords emphasized to respond to corporate risks.

Accordingly, to achieve the objectives of this study, the following research questions have been established: What are the key keywords contained in CEO messages? Do the keywords of CEOs messages have a trend in response to shifts under economic uncertainty? How are the categories of words in CEO messages classified?

2. Literature Review

The disclosure of non-financial information provides essential insights into a company. Non-financial information refers to data beyond the financial figures presented in financial statements, including items that can affect a company’s financial condition and business performance. Europe has long recognized the importance of non-financial information and emphasized the need for its disclosure. In 2014, the EU enacted the Directive on Non-Financial Information (Directive 2014/95/EU) regarding the disclosure of non-financial and diversity information by certain large undertakings and groups. Under this directive, companies subject to its provisions must publish a non-financial information report detailing their business model, adopted policies and outcomes, principal risks, and key performance indicators, while addressing environmental, social, employee, human rights, anti-corruption, and bribery themes [1].

Non-financial information is valuable for assessing corporate value and making relevant forecasts, highlighting its critical role in capital markets. Previous studies analyzing the role of non-financial information in capital markets support this view. Rezaee and Tuo [2] examined the value relevance of non-financial information and found it to be strongly associated with profit quality and future sustainability. Orens and Lybaert [3] analyzed how the use of non-financial information affected analysts’ forecast accuracy, revealing that analysts who utilized more forward-looking and internal structural information produced more accurate forecasts. These findings demonstrate a growing interest in non-financial information within capital markets. In other words, as capital market participants increasingly demand non-financial information, companies are expected to provide relevant disclosures.

The demand for non-financial information is also closely linked to EPU. Higher EPU increases risk in capital markets, prompting participants to rely on both financial and non-financial information in decision-making. The COVID-19 pandemic prolonged global economic uncertainty and affected corporate performance in a manner similar to the 2008 global financial crisis [8]. It also reduced the recoverability of accounts receivable, leading to declines in the fair value of stocks and bonds and impairments in asset values [9,10].

EPU has a significant impact on capital markets. Chiang [23] analyzed the relationship between market uncertainty and risk in G7 capital markets, reporting that higher EPU is associated with negative stock market returns and increased stock return volatility. Jin et al. [24] examined the effect of EPU on stock market crash risk, finding that higher uncertainty significantly increases this risk, particularly for companies with greater information asymmetry. Lu et al. [25] investigated the impact of EPU on default risk and reported that default risk rises significantly as economic policy uncertainty increases.

As such, when EPU rises, capital market participants place greater emphasis on non-financial information, leading investors to demand additional disclosures. Relevant previous studies support this relationship. Chahine et al. [26] analyzed the impact of policy uncertainty on financial analysts’ forecast errors and found that analysts’ accuracy declined as EPU increased. However, this decline was mitigated when more CSR-related non-financial information was disclosed, suggesting that non-financial disclosures can reduce forecast errors under conditions of high policy uncertainty. Similarly, Vural-Yavaş [27] examined the impact of EPU on ESG performance and found that higher EPU was associated with stronger ESG performance. This suggests that companies disclose more ESG information during periods of heightened uncertainty, which in turn improves performance in these areas. Finally, Assaf et al. [28] investigated the relationship between EPU and the disclosure of climate-related non-financial information, finding that higher uncertainty led companies to increase such disclosures to preserve legitimacy for their performance.

Among non-financial information, sustainability and CSR have recently received significant attention. The global need for sustainability reporting has grown alongside increasing demand for related information. Consequently, various countries have implemented regulations for sustainability report disclosure, and companies have increasingly provided these reports voluntarily.

Sustainability reports primarily present non-financial information related to CSR or ESG. Numerous studies have analyzed the characteristics of CSR- and ESG-related non-financial information in these reports. Stolowy and Paugam [29] conducted a comparative analysis of CSR and sustainability information between S&P 500 companies and those in the EuroStoxx 600 index, finding that the number of companies publishing CSR and sustainability reports increased substantially from 2002 to 2015. Additionally, EuroStoxx 600 companies demonstrated stronger CSR performance and published more CSR or sustainability reports compared with their S&P 500 counterparts. Eccles et al. [30] examined whether regional conditions (U.S. or Europe) and investor types influenced ESG indicator differences. They found that U.S. investors showed greater interest in governance than European investors but less interest in environmental issues. Stock investors exhibited broader interest in ESG information than bond investors, while sell-side analysts prioritized environmental information and money managers considered overall ESG indicators. Jackson et al. [31] analyzed how regulatory intensity affected CSR disclosure, showing that companies in countries with stronger disclosure pressure engaged in more CSR activities.

Sustainability reports largely focus on CSR or ESG information, enabling an assessment of perspective on company’s sustainability. Such non-financial information is valuable for predicting corporate performance and evaluating corporate value. Friede et al. [32] reviewed numerous empirical studies on the relationship between ESG standards and corporate financial performance (CFP), finding that ESG generally has a positive effect on CFP, with this effect becoming more stable over time. Broadstock et al. [33] examined ESG performance during the COVID-19 crisis, finding that higher ESG performance reduced financial risk.

In addition to CSR and ESG information, sustainability reports include CEO messages. As representatives of their organizations, CEOs possess the authority to determine overall organizational direction and specific operational details [34]. Therefore, CEO messages provide capital market participants with insights into a company’s policies and future outlook.

Research on CEO messages has been on a rising trend recently. As narrative expressions of personal perspectives, a CEO’s message exerts formal influence and carries social significance. Furthermore, it provides insights into the CEO’s perceptions and plays a useful role in assessing corporate value [13].

Theoretical frameworks related to CEO messages include Impression Management Theory, Legitimacy Theory, and Situational Crisis Communication Theory (SCCT). Impression Management Theory posits that companies communicate intentionally to project a positive image to stakeholders, focusing on how they are perceived by them. In this context, communication is utilized as a strategic tool. Barkemeyer et al. [35] conducted a sentiment analysis of CEO messages in sustainability reports, finding that CEOs tend to focus more on impression management than on narratives related to actual accountability.

Legitimacy Theory suggests that it is crucial for a company to not only possess inherent value but also be socially recognized, as this recognition is directly linked to survival. Therefore, companies strive to act in accordance with social norms and standards; failure to do so results in a legitimacy crisis. Based on this theory, Hooghiemstra [36] analyzed corporate social reporting behaviors. The study reported that corporate social reporting is increasing and is strategically intensified—particularly following major social events—to alter public perception of organizational legitimacy.

Finally, Situational Crisis Communication Theory (SCCT) [37] is a framework for identifying effective communication methods to minimize reputational damage when an organization faces a crisis. In SCCT, the severity of the crisis and the level of responsibility determine the intensity of the response. Liu et al. [38] analyzed CEO communication strategies under the crisis conditions caused by COVID-19. Based on an analysis of CEO letters from 152 multinational corporations, the study found that messages primarily acknowledged the current crisis while emphasizing organizational resilience, reporting that communication strategies and narrative topics play a vital role in crisis response.

Sustainability reports serve as a primary disclosure channel for non-financial information, with most companies placing CEO messages at the beginning of their reports. Several studies have analyzed the impact of CEO messages in sustainability reports on corporate financial indicators. Yook [39] examined the relationship between the characteristics of CEO messages and sustainability performance, finding that less convincing messages were associated with lower sustainability performance, while messages with more positive (optimistic) expressions and greater emphasis on future performance correlated with higher performance. Higher sentiment scores in CEO messages were also linked to higher corporate value (Tobin’s Q). Yoon and Byun [40] conducted a sentiment analysis of CEO messages and found that companies under greater environmental pressure—such as those highly sensitive to the business environment or closely connected to consumers—tended to limit emotional expressions in their messages. Na et al. [41] combined text analysis of CEO messages with the balanced scorecard (BSC) to examine their impact on corporate financial ratios. While a large portion of CEO messages consisted of positive words, sustainability-related words did not show a significant relationship with financial ratios, leading the authors to recommend institutional improvements for more responsible sustainability reporting.

Most previous studies have focused on the impact of CEO messages on corporate value or performance, but analyzing the linguistic characteristics of the messages themselves is also meaningful. Engineering News Record (ENR), a prominent American construction magazine, annually compiles and publishes rankings of the world’s leading construction companies based on their revenue since the 1970s. Choi and Cho [21] performed text analysis on CEO messages from 100 global by ENR rankings construction companies and identified representative keywords, including “management,” “value,” “employee,” “system,” “project,” “culture,” “new,” “occupational,” “practice,” and “basis.” Among these, “management,” “employee,” and “culture” were recognized as the most important keywords, while “rules and regulations” and “resources and equipment” were identified as central factors. Choi and Cho suggested that CEOs should carefully select words to build consensus with stakeholders and provide more detailed descriptions for items with low centrality. However, their study has limitations in generalizability, as it focused solely on the construction industry and analyzed messages from the pre-COVID-19 period; emphasized keywords may differ across industries and post-pandemic contexts.

Studies on CEO messages have been conducted worldwide. Specifically, the details are as follows: Hooghiemstra [14] compared the characteristics of CEO messages contained in letters to shareholders from U.S. and Japanese companies. The analysis revealed that U.S. CEOs tended to emphasize good news more than their Japanese counterparts, although no statistically significant difference was found between the letters from the two countries. Furthermore, regarding bad news, Japanese CEOs showed a stronger tendency to attribute such events to uncontrollable factors. These results demonstrate that the textual characteristics of CEO letters can vary due to cultural differences between countries.

Arvidsson [15] utilized text analysis to examine how CEOs of large Swedish corporations explained sustainability in their letters from 2008 to 2017. The findings indicated that these corporations aimed to maximize shareholder value through sustainable business practices, with CEO letters primarily focusing on enhancing the internal integration of sustainability. Additionally, Arvidsson and Sabelfeld [16] analyzed CEO letters from Swedish-based multinational corporations from 2008 to 2019. They reported that sustainability discourses in CEO letters reflect social and political events, as well as social activities over time, and gradually incorporate shifting sustainability demands from regulatory authorities and the social sphere.

Saglam et al. [17] analyzed 30 CEO letters issued by transportation companies listed on the NASDAQ and/or NYSE. Their study found that some CEOs merely conveyed the general content of the reports, while others used abstract language to define the organization’s approach to sustainability in specific letters.

Thepchalerma and Pinsuwanb [18] identified prominent themes in this year’s environmental reports by analyzing CEO messages from 18 sustainable airlines across various countries, as categorized by Sustainability Magazine and Alternative Airlines. The study reported that six major themes emerged: sustainability commitment, environmental initiatives, partnerships, challenges, future outlooks, and motivation. Furthermore, in the case of airlines, they emphasized a firm commitment to sustainability by mentioning topics such as fuel and waste, while predominantly maintaining an optimistic outlook.

In their study of 200 leading and lagging firms, Clatworthy et al. [19] examined how financial performance influences the linguistic style of CEO reports. Their findings indicate that leaders of underperforming organizations tend to prioritize reputation management and future-oriented optimism over detailing their actual financial standing.

An investigation into 159 Italian firms by Hammami [20] revealed that underperforming businesses often shows their annual reports by overusing optimistic terminology. By comparing the 20 highest and lowest-ranked companies, the study found a deliberate strategy among struggling entities to mask their poor results through an abundance of positive language.

COVID-19 brought changes to the economic environment and plays a role in macroeconomic factors that could reduce sustainability [11]. Therefore, the linguistic expressions in CEOs’ messages may have changed since the COVID-19 period, and words more closely related to future sustainability are likely to appear. However, few studies have analyzed linguistic characteristics specifically in the post-COVID-19 period. Park et al. [22] conducted a text analysis of messages from CEOs of Fortune Global 100 companies before and after COVID-19. Their analysis revealed that, compared with the pre-COVID-19 period, companies reported more frequently on social and environmental issues, while identifying sustainable management development, risk management, and competitive advantage as their main corporate strategies. In other words, they emphasized the need to strengthen CSR to respond to the crisis caused by COVID-19 and the importance of CSR as a communication tool.

The research conducted by Park et al. [22] is significant in terms of analyzing CEOs’ messages before and after COVID-19. However, they focused only on large-scale global companies and analyzed differences between the pre- and post-COVID-19 periods. Each of the top 100 global companies has a different market status and faces diverse business environments. Furthermore, they did not analyze the time-series changes in messages during the COVID-19 period. The present study analyzes the overall content of CEOs’ messages by extracting those included in the sustainability reports of South Korean listed companies from 2021 to 2023.

3. Research Methodology

This study performs a text analysis of CEOs’ messages within sustainability reports published from 2021 to 2023. The Korea Investor’s Network for Disclosure System (KIND) of the Korea Exchange offers information on voluntarily disclosed sustainability reports. We collected sustainability reports from KIND and extracted the CEOs’ messages for analysis.

The number of sustainability reports disclosed on KIND was 21 in 2019, 38 in 2020, 80 in 2021, 142 in 2022, and 177 in 2023, showing a gradual upward trend. Before 2020, disclosure of sustainability reports was voluntary, resulting in low reporting frequency. However, the number of disclosures has increased in recent times, which is likely due to preparatory efforts for the mandatory disclosure requirement scheduled for 2026.

3.1. Research Procedures

This study was conducted following the procedures outlined below. In Phase 1, we collected 399 corporate sustainability reports from 2021 to 2023 as raw data. In Phase 2, the collected data were refined to make them suitable for analysis. Phase 3 involved the data analysis process, in which keyword frequency, Term Frequency-Inverse Document Frequency (TF-IDF) analysis, network analysis, social network analysis, and CONvergence of iteration CORrelation (CONCOR) analysis were performed.

3.2. Data Collection

We collected data for text analysis by extracting CEOs’ messages from sustainability reports attached to voluntary disclosure reports (sustainability report-related items) published on the electronic disclosure system. Sustainability reports disclose items related to corporate sustainability and are useful for exploring corporate management issues. Although sustainability reports have been disclosed since 2016, the annual number of disclosures was considerably low from 2016 to 2020. This period also corresponds to the early stages of social discussions on sustainability in South Korea. Therefore, we focus on reports published over the 3 years from 2021 to 2023 as the analysis sample. COVID-19 increased interest in corporate sustainability and had a significant impact on companies’ business environments. Accordingly, the analysis period was set from 2021 to 2023 to capture the effects of COVID-19.

The distribution of the sample is shown in Table 1. In total, we collected 399 sustainability reports: 80 in 2021, 142 in 2022, and 177 in 2023. Among these, two did not include CEOs’ messages, and seven were duplicates. Thus, a total of 390 CEOs’ messages were utilized for the final analysis.

Table 1.

Distribution of the Sample.

3.3. Data Refinement

The collected data were refined to make them suitable for analysis. In this study, we utilized TEXTOM (https://www.textom.co.kr), a web-based big data analysis program optimized for text mining [42]. The procedures were as follows. First, we performed a morphological analysis as the primary data preprocessing step, using MeCab-IMC within TEXTOM. The analysis with MeCab-IMC is based on a dictionary rather than relying on the original text’s spacing, providing highly consistent results.

Next, we removed irrelevant or meaningless stop words from the keywords refined in the first step. Using N-gram information to identify consecutively appearing keywords, compound words such as “Sustain-able” were merged into “Sustainable,” and synonyms and loanwords were corrected or consolidated. Finally, the researchers discussed the keywords to align them with the research objectives, reviewing the meaning of keywords with high co-occurrence frequencies within the original text and examining the contextual appropriateness of merging superordinate terms.

3.4. Data Analysis

The data analysis process was as follows. First, we estimated Term Frequency (TF) and TF-IDF from the refined data. TF measures how frequently a word appears within a document, while TF-IDF is a statistical measure indicating the importance of a specific word within a document relative to a collection of documents [43]. In this study, we calculated the top 50 TF and TF-IDF values for all keywords across the 3 years of data. The top 50 frequencies were visualized using a word cloud (Figure 1). Additionally, the top 50 frequencies for each year were analyzed separately and compared with the entire period.

Second, network analysis was conducted. The structural relationships among the top 50 keywords extracted by TEXTOM were numerically estimated, organized into a 1-Mode Matrix, and input into the UCINET 6 program to analyze overall network attributes and structures. UCINET 6, developed by Freeman, is traditionally the most frequently used package in Social Network Analysis and provides tools for visualization and indicator-based analysis [44].

Third, CONCOR analysis was performed. CONCOR analysis visualizes outcomes after confirming clusters grouped according to hierarchical levels derived from the dendrogram. In this study, we used the NetDraw program in UCINET 6 to visualize and derive clusters. Additionally, centrality analyses—degree centrality and eigenvector centrality—were examined to identify influential keywords. Degree centrality measures how extensively a node is connected to surrounding keywords by counting the number of edges directly linked to it. Eigenvector centrality assigns greater weight to nodes connected to other important nodes, measuring a keyword’s influence within the network. These approaches enabled the identification of keywords actively discussed in CEOs’ messages in sustainability reports.

4. Results

4.1. Results of Keyword Frequency and TF-IDF Analysis

We collected 390 CEOs’ messages from corporate sustainability reports published between 2021 and 2023. After refining, the keywords were organized for the entire 3-year period and for each individual year (2021, 2022, and 2023), and the top 50 words were extracted, as shown in Table 2. Figure 1 presents a word cloud visualizing the top 50 keywords for the entire 3-year period.

Table 2.

Keyword TF.

Figure 1.

TF Word Cloud.

Figure 1.

TF Word Cloud.

The most frequent words for the entire 3-year period, as well as for 2021, 2022, and 2023, were ESG, Sustainable, Society, Stakeholders, Growth, Environment, Effort, and Future. Comparing the 3-year period with each individual year reveals distinct patterns: COVID-19, which ranked 50th overall, rose to 11th place in 2021, fell to 36th in 2022, and did not appear among the top 50 keywords in 2023. This trend reflects the transition from the COVID-19 pandemic to its endemic phase in CEOs’ messages. In the 2021 analysis, keywords such as Finance, Crisis, and Competitiveness ranked highly compared with the overall 3-year period. In 2022, keywords such as Safety, Transparent, and Cooperation, which were not in the top 50 in 2021, appeared, and the ranks of Transparent and Cooperation further increased. The 2023 analysis revealed keywords such as Risk, System, Diverse, Evaluation, and Trust, which had not appeared in the overall 3-year rankings or in the previous 2 years.

Examining TF-IDF, which reflects the importance of keywords within specific documents, the results for the entire 3-year period were nearly identical to the TF results. This suggests that keywords derived from frequency analysis can be interpreted as being significant even when considering TF-IDF weights. Among the top-ranked keywords, Growth and Global had relatively higher TF-IDF values, while Stakeholders and Strengthening had lower TF-IDF values.

4.2. Results of Network Visualization

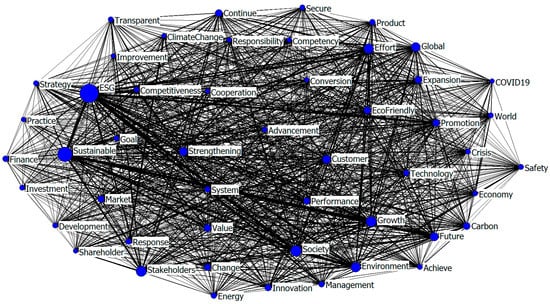

The network visualization reflecting the connection distribution and appearance frequency of the top 50 TF keywords is shown in Figure 2. The NetDraw function in UCINET 6 was used for visualization. When representing the 50 keywords as nodes, 2426 network ties were identified, with a density of 0.99 and an average network distance of 1.01. The average distance indicates that specific keywords were connected on average through 1.01 steps, showing that keywords within the network are closely connected.

Figure 2.

Results of network visualization.

Next, we conducted a centrality analysis (degree centrality and betweenness centrality) to identify keywords with high influence as key attributes of network nodes; the results are presented in Table 3. Degree centrality measures the number of connections a node has with other nodes within the network. Keywords such as ESG, Sustainable, Society, Stakeholders, Growth, Environment, and Effort exhibited high degree centrality, similar to their frequency rankings. Betweenness centrality identifies the most influential central nodes within a network. In this study, the keywords ranked as follows: Sustainable, ESG, Society, Environment, Growth, Effort, Strengthening, Stakeholders, Future, and Global. Keywords such as Sustainable, Environment, Effort, Strengthening, Future, Value, Response, Competitiveness, and Transparent generally appeared higher in betweenness centrality than in frequency rankings. Words that rank higher in betweenness centrality than in frequency can be considered to be more closely connected to other words or issues within the network.

Table 3.

Results of centrality analysis.

4.3. Results of CONCOR Analysis

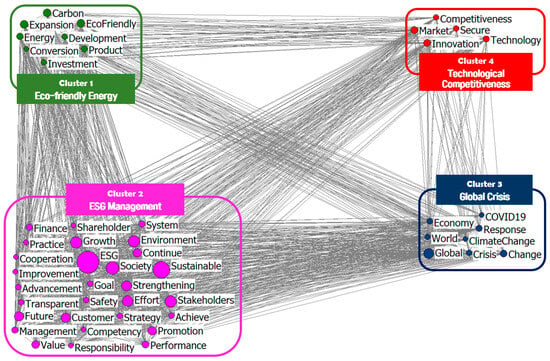

CONCOR analysis involves grouping highly associated keywords into clusters by considering the relationships between nodes in similar positions within the entire network structure. The CONCOR analysis results revealed a total of four clusters, which were named “Eco-friendly Energy (Cluster 1),” “ESG Management (Cluster 2),” “Global Crisis (Cluster 3),” and “Technological Competitiveness (Cluster 4)” (Figure 3).

Figure 3.

Results of CONCOR analysis.

Cluster 1 consists of eco-friendly energy-related words such as Carbon, Eco-friendly, and Energy. Cluster 2 includes keywords related to corporate management with a focus on ESG, such as Sustainable, Growth, Stakeholder, Strengthening, Customer, and Promotion. Cluster 3 contains mainly keywords related to crisis situations, such as COVID-19, and to response measures, such as Change and Response, as well as World and Global. Cluster 4 consists of keywords related to corporate competitiveness in the market, such as Market, Technology, Competitiveness, and Innovation.

5. Conclusions

This study performed text analysis on CEO messages contained in sustainability reports voluntarily published by South Korean listed companies from 2021 to 2023 to reveal trends in the main discourses related to corporate sustainability. In particular, by analyzing the linguistic features of non-financial information reflected in CEOs’ messages within the changed socioeconomic environment after COVID-19, this study aimed to identify trends in corporate communication regarding sustainability.

TF and TF-IDF analysis revealed main keywords such as ESG, Sustainable, Society, Stakeholders, Growth, Environment, Effort, and Future. Similar words also appeared prominently in the centrality analysis. The CONCOR analysis enabled the classification of four main clusters from CEOs messages: Eco-friendly Energy, ESG Management, Global Crisis, and Technological Competitiveness. These findings indicate that companies comprehensively addressed various sustainability-related issues through CEOs’ messages while actively incorporating them into both management strategy and communication. In general, sustainability-related keywords mainly covered corporate ESG activities and strategies, crisis response measures, and efforts to enhance corporate competitiveness, which can be interpreted as conveying corporate efforts to improve sustainability.

6. Discussion

6.1. Meaning of the Keywords

The frequency analysis of keyword for the three-year period (2021–2023), identifies ESG as the most prominent keyword across the entire timeframe. Notably, its cumulative frequency reached 2003, ranking first among all keywords. On an annual basis, it showed a distinct upward trend, increasing from 299 in 2021 to 716 in 2022 and 988 in 2023. This suggests that ESG has evolved beyond a single management activity to become a core strategic pillar overseeing overall corporate value enhancement.

The second-highest keyword, Sustainable, also recorded a cumulative frequency of 1470, growing approximately 2.6 times from 273 in 2021 to 707 in 2023. This reflects a corporate emphasis on long-term value creation and sustainable management over short-term performance. Furthermore, keywords such as Society (1042), Stakeholders (949), and Growth (940) indicate that CEO messages are expanding beyond environmental concerns to encompass social responsibility, stakeholder engagement, and the concept of growth integrated with sustainability.

According to the centrality analysis, the primary keywords derived in this study perform distinct roles and semantic functions within the network. First, in terms of Degree Centrality, “ESG” ranked first, showing the highest level of centrality. This signifies that ESG serves as a core cluster directly connected to numerous other keywords, positioned at the structural center of the discourse on corporate sustainability. These results suggest that ESG is not a single topic but a high-level concept that integrates various themes such as Sustainable, Society, Stakeholders, Growth, and Environment.

In contrast, Betweenness Centrality analysis showed that “Sustainable” recorded the highest value. This indicates that “Sustainable” acts as a mediator connecting different keyword clusters within the network. In other words, the keyword “Sustainability” functions as a vital link that diffuses the concept of ESG into specific domains such as Environment, Society, and Growth. This finding demonstrates that sustainability is utilized as a platform to connect various strategic discourses, moving beyond a mere increase in corporate value.

As previously mentioned, understanding the meaning of keywords is significantly important. Arvidsson [15] also noted that how CEOs communicate narratives related to sustainability is crucial, emphasizing the importance of identifying the messages they intend to convey. This is because such insights can be effectively utilized when drafting policies and regulations for sustainable development.

6.2. Comparing the Trends of the Keywords

An examination of the annual changes in keyword rankings reveals that ‘ESG’ and ‘Sustainable’ maintained the first and second positions, respectively, from 2021 to 2023, exhibiting the most stable trends. Conversely, ‘Stakeholders’ rose from 7th place in 2021 (172 instances) to 4th in 2022 (337 instances) and finally reached 3rd place in 2023 (440 instances). This provides quantitative evidence of the increasing emphasis on stakeholder-oriented management in corporate communications. While ‘Society’ consistently increased (264 in 2021, 359 in 2022, 419 in 2023) and remained in the top tier, it was surpassed by ‘Stakeholders’ in 2023, falling to 4th place. This suggests that discussions on social value are being integrated into or, in some cases, replaced by stakeholder-centric narratives.

Meanwhile, ‘Growth’ showed continuous growth (217 in 2021, 321 in 2022, 402 in 2023), but its rate of increase was relatively lower than that of ‘ESG’ and ‘Sustainable’. This indicates a strengthening trend where growth is emphasized in conjunction with keywords like ESG, Environment, and Sustainable rather than as an independent concept. In fact, ‘Environment’ more than doubled from 185 instances in 2021 to 391 in 2023, demonstrating that environmental issues have become a core element of CEO messages.

Combining the frequency and centrality analyses clarifies the trend of the ESG keyword. ‘ESG’ not only maintained the highest frequency over the three-year period but also ranked first in Degree Centrality, confirming its role as the absolute central keyword in both quantitative and structural aspects. This implies that ESG is consistently emphasized in CEO messages and functions as the central axis for organizing various discourses. On the other hand, while ‘Sustainable’ maintained the second-highest frequency, it recorded the highest Betweenness Centrality. This suggests that over time, sustainability has evolved beyond being a key term to performing a structural role in connecting and expanding the discourse on ESG. Specifically, its links with keywords related to Growth, Future, and Strategy show that companies are utilizing sustainability as a logic for long-term value creation.

Additionally, ‘Environment’ ranked 6th in Degree Centrality and 4th in Betweenness Centrality, confirming its role as an important connecting element. This means that environment is not an isolated topic but is discussed integratively by being combined with keywords such as Society, Effort, and Eco-friendly. ‘Growth’ ranked 5th in both Degree and Betweenness Centrality, interpreted as playing a role in combination rather than acting as a mediator between keywords.

Overall, these keyword trends demonstrate that the significance of a keyword depends on its position and role within the network rather than simple frequency. Specifically, ESG functions as a central hub, Sustainable as a key mediator, and Society and Environment as the main axes for discourse expansion. This suggests that recent corporate ESG communication is evolving into a more integrated and relationship-oriented structure.

6.3. Contribution and Limitation

The theoretical implications of this study are as follows. First, this study extends Impression Management Theory from quantitative and structural perspectives. While existing research has interpreted CEO messages primarily as strategic expressions to project a positive image to stakeholders [13,35], this study confirms that “ESG” and “Sustainable” function as central and mediating keywords within these messages. This suggests that impression management is being executed at the level of the overall structural design of the message.

Second, this study empirically demonstrates that CEO messages serve as a primary vehicle for securing corporate social legitimacy. Legitimacy Theory emphasizes that companies ensure survival by aligning with social norms and expectations [36]. The finding that keywords such as “Society,” “Stakeholders,” and “Environment” are strongly linked to “ESG” suggests that CEO messages are actively utilized to communicate social legitimacy. In particular, the strengthening structural centrality of keywords related to stakeholders and social responsibility shows that companies are moving beyond simple information disclosure to actively reconstruct their values and roles to meet social expectations. This implies that firms consistently emphasize values and responsibilities that align with social norms.

Finally, this study provides evidence that Situational Crisis Communication Theory (SCCT) can be extended from crisis-specific contexts to routine management communication. The result—where COVID-19-related keywords were positioned at the periphery of the network while “ESG” and “Sustainable” maintained consistent centrality—extends the work of Liu et al. [38]. This suggests that CEO messages are utilized as strategic communication tools to consistently convey organizational accountability and resilience, not only during crisis responses but also in general operations.

Overall, this study provides evidence that CEO messages are not merely descriptive texts but function as complex strategic discourses where impression management, legitimacy seeking, and crisis response converge. This offers a perspective to integrally understand the functions of CEO communication, which existing theories have previously explained in isolation.

This study also provides significant practical implications for senior leaders, CEOs, and policymakers. The primary contribution of this research is the quantitative verification of the intensification of ESG discourse by directly comparing three-year keyword frequency data from CEO messages in sustainability reports. Specifically, through keywords showing clear upward trends—such as ESG (299 → 716 → 988), Sustainable (273 → 490 → 707), and Stakeholders (172 → 337 → 440)—the study clearly demonstrates that the focus of corporate communication is shifting toward the environment, society, and stakeholders.

Furthermore, keywords such as risk management, social responsibility, and technological innovation have become more prominent, indicating that the content of CEO messages is becoming increasingly structured and strategic. While these keywords were present in previous periods, they appear to have been further emphasized following global crises such as COVID-19.

This study offers several contributions. First, by performing a text analysis of CEO messages, this research demonstrates that Situational Crisis Communication Theory (SCCT) can be extended beyond crisis situations to serve as a strategic communication tool in ordinary. In other words, this study enhances understanding of corporate communication strategies. Second, this research is significant in that it bridges Impression Management Theory with longitudinal discourse. This indicates that corporations engage in strategic communication to enhance their image, and the findings show that CEO messages function as one such communication channels. Finally, this study provides evidence that Legitimacy Theory can be applied differentially over time. The results that CEO messages trend and topics shift over time implies that legitimacy strategies operate by time-series dynamically, even concerning the information provided through text.

South Korea is currently preparing for the mandatory disclosure of sustainability reports. In this context, this study suggests the possibility of quantitative analysis for non-financial information by extracting structural patterns inherent in unstructured text data through text mining and CONCOR analysis. Consequently, the findings of this study can serve as a guideline for the policy-making process regarding disclosure standards.

However, this study has several limitations. First, as the analysis is based on keyword frequency, it is difficult to conclude that a high frequency necessarily implies a positive impact on corporate value or a deliberate strategic application in every instance. Additionally, since the scope was limited to CEO messages, the study did not conduct a linked analysis with the full text of sustainability reports or actual ESG performance indicators.

Furthermore, while this study focused on analyzing the textual characteristics and trends of CEO messages, sophisticated statistical analyses were not performed. Although the frequency, centrality, and trends of such text can influence ESG/CSR ratings, corporate value, or the cost of capital, deriving direct quantitative indicators from CEO messages for such analysis remains challenging. Therefore, the absence of rigorous statistical testing remains a limitation of this research.

Finally, because the analysis was restricted to voluntarily disclosed sustainability reports, there may be limitations regarding the representativeness of the sample. Detailed comparative analyses based on industry sectors or firm sizes were not conducted. Moreover, there is a possibility that some contextual nuances may have been overlooked during the qualitative interpretation of the CEO messages.

6.4. Future Works

Future research needs to move beyond simple keyword frequency analysis to conduct more in-depth investigations into the structural relationships of ESG discourse, utilizing methods such as year-over-year growth rate comparisons or co-occurrence analysis. For instance, performing a network analysis among keywords that frequently appear alongside ESG—such as Stakeholders, Environment, and Growth—would allow for a more sophisticated understanding of the specific contexts in which companies utilize ESG narratives. Additionally, follow-up studies are required to verify the alignment between corporate discourse and actual practice by integrating the full text of sustainability reports with empirical ESG performance data.

Furthermore, while this study analyzed CEO messages within South Korean sustainability reports, it did not conduct a comparative analysis with CEO messages from other countries due to challenges in data collection and inherent linguistic differences. Therefore, comparative research on CEO messages across different countries that reflects diverse cultural and linguistic characteristics remains a task for future study.

Future research could attempt more sophisticated interpretations through comparative analysis by industry and company size or clearly suggest practical implications by analyzing the causal relationship between CEOs’ messages and CFP or ESG evaluation results. Detailed sentiment and semantic network analyses using AI-based natural language processing techniques could also be significant as future research.

Author Contributions

Conceptualization, Y.S.; formal analysis, Y.S. and H.L.; methodology, H.L.; visualization, H.L.; writing—original draft, Y.S. and H.L.; writing—review and editing, Y.S. and H.L. All authors have read and agreed to the published version of the manuscript.

Funding

This study was supported by research fund from Chosun University, 2025.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors on request.

Conflicts of Interest

The authors declare no conflicts of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| ESG | Environmental, Social, and Governance |

| CSR | Corporate Social Responsibility |

| NFRD | Non-Financial Reporting Directive |

| CSRD | Corporate Sustainability Reporting Directive |

| ESRS | European Sustainability Reporting Standards |

| EPU | Economic Policy Uncertainty |

| CFP | Corporate Financial Performance |

| KIND | Korea Investor’s Network for Disclosure System |

| TF-IDF | Term Frequency-Inverse Document Frequency |

| CONCOR | CONvergence of iteration CORrelation |

References

- Kim, S. Interpretation and Implications of EU Legislation on the Disclosure of Non-financial Information—with a Focus on Directive 2014/95/EU. J. Bus. Adm. Law 2022, 33, 1–42. Available online: https://kiss.kstudy.com/Detail/Ar?key=4002896 (accessed on 12 January 2026).

- Rezaee, Z.; Tuo, L. Voluntary disclosure of non-financial information and its association with sustainability performance. Adv. Account. 2017, 39, 47–59. [Google Scholar] [CrossRef]

- Orens, R.; Lybaert, N. Does the financial analysts’ usage of non-financial information influence the analysts’ forecast accuracy? Some evidence from the Belgian sell-side financial analyst. Int. J. Account. 2007, 42, 237–271. [Google Scholar] [CrossRef]

- Janowski, A. CSR in Management Sciences: Is It “a Road to Nowhere”? Economies 2021, 9, 198. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What We Know and Don’t Know About Corporate Social Responsibility: A Review and Research Agenda: A Review and Research Agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research Progress and Future Prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Rau, P.R.; Yu, T. A survey on ESG: Investors, institutions and firms. China Financ. Rev. Int. 2024, 14, 3–33. [Google Scholar] [CrossRef]

- Korea Institute for International Economic Policy. COVID-19 Crisis and Shifts in the Corporate Competitive Landscape: Comparisons with Previous Economic Crises. 2022. Available online: https://www.kiep.go.kr/gallery.es?act=view&mid=a10101020000&bid=0001&list_no=10812&cg_code=C03&act=view&list_no=10812&cg_code=C03&act=view&list_no=10812&cg_code=C03 (accessed on 28 October 2025).

- Gofran, R.; Liasidou, S.; Gregoriou, A. The impact of COVID-19 on the liquidity of the European Tourism industry. Curr. Issues Tour. 2022, 26, 2235–2249. [Google Scholar] [CrossRef]

- Gubareva, M. The impact of COVID-19 on liquidity of emerging market bonds. Financ. Res. Lett. 2021, 41, 101826. [Google Scholar] [CrossRef]

- Shin, Y.; Choi, B. The Changes in the Economic Environment and Corporate Information Asymmetry—Focusing on the COVID-19 Pandemic. Sustainability 2025, 17, 3858. [Google Scholar] [CrossRef]

- Ansoff, H.I. Strategies for diversification. Harv. Bus. Rev. 1957, 35, 113–124. [Google Scholar]

- Amernic, J.; Craig, R.; Tourish, D. Measuring and Assessing Tone at the Top Using Annual Report CEO Letters; The Institute of Chartered Accountants of Scotland: Edinburgh, UK, 2010. [Google Scholar]

- Hooghiemstra, R. Letters to the shareholders: A content analysis comparison of letters written by CEOs in the United States and Japan. Int. J. Account. 2010, 45, 275–300. [Google Scholar] [CrossRef]

- Arvidsson, S. CEO talk of sustainability in CEO letters: Towards the inclusion of a sustainability embeddedness and value-creation perspective. Sustain. Account. Manag. Policy J. 2023, 14, 26–61. [Google Scholar] [CrossRef]

- Arivdsson, S.; Sabelfeld, S. Adaptive framing of sustainability in CEO letters. Account. Audit. Account. J. 2023, 36, 161–199. [Google Scholar] [CrossRef]

- Saglam, B.B.; Solak-Fiskin, C.; Akgul, E.F. Conveying the sustainability message through CEO letters: An investigation on selected transportation companies. World Rev. Intermodal Transp. Res. 2023, 11, 436–454. [Google Scholar] [CrossRef]

- Thepchalerm, T.; Pinsuwan, S. CEO voices on sustainable aviation: An analysis of environmental communication in the airline industry. Green Technol. Sustain. 2025, 3, 100194. [Google Scholar] [CrossRef]

- Clatworthy, M.; Jones, M.J. The effect of thematic structure on the variability of annual report readability. Account. Audit. Account. J. 2001, 14, 311–326. [Google Scholar] [CrossRef]

- Hammami, H. Accounting narratives’ characteristics and firm performance in the MD&As of listed Italian companies. Int. J. Account. Financ. 2011, 3, 72–86. [Google Scholar] [CrossRef]

- Choi, Y.G.; Cho, K.T. Analysis of safety management characteristics using network analysis of CEO messages in the construction industry. Sustainability 2020, 12, 5771. [Google Scholar] [CrossRef]

- Park, H.; Kim, T.; Cho, K. Changes in Management Trends in 100 Global Companies before and after COVID-19: A Topic Modeling Approach. Sustainability 2024, 16, 2342. [Google Scholar] [CrossRef]

- Chiang, T.C. Economic policy uncertainty, risk and stock returns: Evidence from G7 stock markets. Financ. Res. Lett. 2019, 29, 41–49. [Google Scholar] [CrossRef]

- Jin, X.; Chen, Z.; Yang, X. Economic policy uncertainty and stock price crash risk. Account. Financ. 2019, 58, 1291–1318. [Google Scholar] [CrossRef]

- Lu, C.; Yang, M.; Xia, X. Economic policy uncertainty and default risk: Evidence from China. Econ. Anal. Policy 2023, 79, 821–836. [Google Scholar] [CrossRef]

- Chahine, S.; Daher, M.; Saade, S. Doing good in periods of high uncertainty: Economic policy uncertainty, corporate social responsibility, and analyst forecast error. J. Financ. Stab. 2021, 56, 100919. [Google Scholar] [CrossRef]

- Vural-Yavaş, Ç. Economic policy uncertainty, stakeholder engagement, and environmental, social, and governance practices: The moderating effect of competition. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 82–102. [Google Scholar] [CrossRef]

- Assaf, C.; Benlemlih, M.; El Ouadghiri, I.; Peillex, J. Does policy uncertainty affect non-financial disclosure? Evidence from climate change-related information. Int. J. Financ. Econ. 2024, 29, 4613–4629. [Google Scholar] [CrossRef]

- Stolowy, H.; Paugam, L. The expansion of non-financial reporting: An exploratory study. Account. Bus. Res. 2018, 48, 525–548. [Google Scholar] [CrossRef]

- Eccles, R.G.; Serafeim, G.; Krzus, M.P. Market interest in nonfinancial information. J. Appl. Corp. Financ. 2011, 23, 113–127. [Google Scholar] [CrossRef]

- Jackson, G.; Bartosch, J.; Avetisyan, E.; Kinderman, D.; Knudsen, J.S. Mandatory non-financial disclosure and its influence on CSR: An international comparison. J. Bus. Ethics 2020, 162, 323–342. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Broadstock, D.C.; Chan, K.; Cheng, L.T.; Wang, X. The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Financ. Res. Lett. 2021, 38, 101716. [Google Scholar] [CrossRef]

- Resick, C.J.; Whitman, D.S.; Weingarden, S.M.; Hiller, N.J. The bright-side and the dark-side of CEO personality: Examining core self-evaluations, narcissism, transformational leadership, and strategic influence. J. Appl. Psychol. 2009, 94, 1365. [Google Scholar] [CrossRef]

- Barkemeyer, R.; Comyns, B.; Figge, F.; Napolitano, G. CEO statements in sustainability reports: Substantive information or background noise? Account. Forum 2014, 38, 241–257. [Google Scholar] [CrossRef]

- Hooghiemstra, R. Corporate communication and impression management–new perspectives why companies engage in corporate social reporting. J. Bus. Ethics 2000, 27, 55–68. [Google Scholar] [CrossRef]

- Coombs, W.T. Protecting organization reputations during a crisis: The development and application of situational crisis communication theory. Corp. Reput. Rev. 2007, 10, 163–176. [Google Scholar] [CrossRef]

- Liu, J.; Hong, C.; Yook, B. CEO as “chief crisis officer” under COVID-19: A content analysis of CEO open letters using structural topic modeling. In Strategic Communication and the Global Pandemic; Routledge: Abingdon, UK, 2025. [Google Scholar] [CrossRef]

- Yook, K. The Effect of CEO Narcissism on the CSR Performance: Mediating Role of Board Composition. J. Ind. Econ. Bus. 2018, 31, 2131–2159. [Google Scholar] [CrossRef]

- Yoon, T.; Byun, H. A Sentiment Analysis of CEO Message in Sustainability Report. J. Public Relat. 2023, 27, 153–181. [Google Scholar] [CrossRef]

- Na, H.J.; Lee, K.C.; Choi, S.U.; Kim, S.T. Exploring CEO messages in sustainability management reports: Applying sentiment mining and sustainability balanced scorecard methods. Sustainability 2020, 12, 590. [Google Scholar] [CrossRef]

- Lee, H.; Shin, Y. A Study on MBTI Perceptions in South Korea: Big Data Analysis from the Perspective of Applying MBTI to Contribute to the Sustainable Growth of Communities. Sustainability 2024, 16, 4152. [Google Scholar] [CrossRef]

- Qaiser, S.; Ali, R. Text mining: Use of TF-IDF to examine the relevance of words to documents. Int. J. Comput. Appl. 2018, 181, 25–29. [Google Scholar] [CrossRef]

- Kim, D. Analysis of Research Trends in Elderly Housing Keyword Network Analysis. J. Korean Hous. Assoc. 2024, 35, 79–90. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2026 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license.