1. Introduction

Currently, numerous data structures are being utilized, and one of these is blockchain technology, which is a distributed and decentralized data structure. This technology allows for data to be shared through open access and peer-to-peer networks. However, transactions executed using blockchain technology must undergo verification and certification by the network’s community [

1]. The blockchain was first introduced to the financial industry as a cryptocurrency, with the main goal of replacing manual authentication with digital authentication [

2].

The use of blockchain technology can enhance the security, immutability, trust, transparency, and traceability of data, making it a subject of interest for professionals and academicians across various industries [

3]. As a result, investments in blockchain solutions from different industries are increasing over time, with an expected investment of around USD 176 billion. Blockchain technology has several capabilities, including promoting environmental, social, and economic sustainability in the manufacturing industry. Given the numerous benefits of utilizing blockchain technology in the manufacturing sector, investments in blockchain solutions for this industry are currently on the rise [

4].

Various studies have delved into the concept of business, describing it as a collaborative effort of individuals aimed at organizing the social and ethical aspects of communal life. To comprehend the ethical and social implications of modern organizations, it is crucial to examine their structural, economic, political, and social dimensions [

5]. Therefore, conducting business in an ethical manner is vital for organizations. At the micro level, business ethics involves human capabilities, motivations, and needs. The primary goal of an organization is to provide value to its stakeholders, thereby creating value for the organization [

6]. While profitability is an important aspect of business, it is not the sole objective. Organizations are expected to engage in social welfare activities that may impact their operational environment. A code of conduct is typically established and enforced within organizations, with business ethics serving as the guiding principle. Although such codes are often developed voluntarily, governments may also impose them through legislation [

7]. The practice of business ethics can greatly influence an organization’s public perception and therefore serve as a foundation for its success [

8].

In the current dynamic global market, it is imperative for organizations to establish and maintain a positive image while balancing environmental preservation, public welfare, and profits [

9]. Adapting strategies to changing societal values and globalization is essential for an organization’s successful operation, and developing partnerships with stakeholders is necessary for long-term sustainable development [

10]. Thus, organizations must embrace social responsibility to meet these requirements. Implementation and application of corporate social responsibility (CSR) are highly encouraged in the modern business environment, as they promote transparency in environmental protection and public welfare [

11]. Furthermore, following business ethics is also critical to promoting the positive image of banks among stakeholders [

12].

Social challenges, in particular, have a significant impact on organizational planning and practices, and addressing them is therefore crucial to achieving sustainability [

13]. For the banking sector, social sustainability is one of the major challenges, as it has role to play in engaging the community in which banks operate. Basically, social sustainability is a process of creating sustainable successful places that promote wellbeing by understanding what people need from the places they live and work [

14]. In addition, Woodcraft [

15] noted that a recent trend in the conversation about sustainable development is social sustainability. It has evolved over a few years in reaction to the predominance of technology and environmental concerns in urban development and the lack of progress in addressing social issues in cities including inequality, eviction, livability, and the growing demand for cheap housing. The social aspects of sustainability have been generally disregarded in discussions, policy, and practice around sustainable urbanism, despite the sustainable communities policy agenda having been adopted in the UK a decade ago. But things are starting to shift. Understanding and assessing the social effects of urban growth and regeneration are becoming more and more important both in the UK and elsewhere. A modest but expanding movement of city planners, architects, builders, housing organizations, and local governments promotes a more “social” method of creating and running cities. This is a part of a growing global interest in social sustainability, which is being used by governments, public institutions, decisionmakers, NGOs, and businesses to frame choices about housing, urban renewal, and development as part of a growing policy discourse on the resilience and sustainability of cities.

Furthermore, meeting society’s ethics and norms is also important for banks. The present study aims to investigate the impact of blockchain technology, corporate social responsibility (CSR), and business ethics on social sustainability in the context of UAE banks, while also examining the mediating role of corporate social responsibility (CSR) and business ethics, as the mediations are rarely tested simultaneously. The importance of sustainability in the success of global organizations cannot be overstated, as it is a critical challenge faced by organizations, encompassing social, environmental, and economic factors. It is important for the banking sector to focus on factors that can improve the social sustainability of banks. Improving the reputation of and trust in banks has long-term impact. Moreover, employee engagement is positively affected on a long-run basis. Therefore, it is key for banks to assess the impact of factors like blockchain technology, corporate social responsibility (CSR), and business ethics on social sustainability.

5. Methodology

This study adopted a quantitative research approach and cross-sectional research design, keeping the study objectives in view. The model proposed in this study was tested within the banking sector of the UAE using a quantitative methodology to collect data from customers via field surveys. The study respondents were required to be over 18 years old, and the sampling method employed was purposive sampling, a type of nonprobability sampling [

55]. Purposive sampling was selected due to its cost effectiveness, simplicity, and ease of data collection, and is commonly used when identifying problems regarding a target market [

56]. This sampling approach is similar to that employed in a previous study by Abu Zayyad, Obeidat [

57], who also used the purposive sampling technique.

The study items were adapted from previous studies. The items of blockchain technology were adapted from Khan, Godil [

58]; the items of business ethics were adapted from Blanco-González, Del-Castillo-Feito [

59]; the items of CSR were adapted from Raza, Rather [

60]; and the items of social sustainability were adapted from DUONG and HA [

61]. These questionnaires were designed on a 5-point Likert scale ranging from 1 to 5. Overall, 416 questionnaires were distributed among employees of banks working in the UAE and 298 questionnaires were returned, with 262 deemed valid for data analysis, resulting in a usable response rate of 62.67%. The gathered data were assessed using SPSS for descriptive analysis and to obtain demographic details of the respondents and using PLS 3.3.9. This tool is more suitable when the proposed model is complex. In the present study, we tested two mediations. Thus, this tool was more suitable for analysis.

The characteristics of the respondents indicated that most of the respondents were male (67%) and married (56.7%). Additionally, 17% of the respondents held degrees below the bachelor’s level, 49% held a bachelor’s degree, and 33% held a master’s degree or higher. To assess common method variance (CMV), VIF was examined, as recommended by Kock [

62], and the results are presented in

Table 1, with all VIF values being less than 5.

Based on the VIF values in the

Table 1, it seems that BE (1.005) and CSR (1.002) have very low multicollinearity with the other variables in the model, while SS (1.460) has a slightly higher but still acceptable level of multicollinearity. This means that the coefficients estimated for BE (2.750) and CSR (2.717) are relatively stable and can be interpreted without much concern for multicollinearity, while some caution might be needed when interpreting the coefficient for SS. If higher VIF values are encountered (typically above 5 or 10), it is a stronger indication of problematic multicollinearity that might require further investigation.

Later, descriptive analysis of this study was conducted. The details are mentioned in

Table 2 of this study.

Table 2 provides a descriptive analysis of four variables: BCT (3.233), CSR (3.857), BE (2.887), and SS (4.074). This analysis summarizes key statistical characteristics of these variables based on a sample of 262 datapoints. In addition, the Mean (average) column shows the arithmetic mean (average) of each variable. It represents the central tendency of the data, indicating the typical or average value. In addition, Std. Dev (standard deviation) column provides the standard deviation of BCT (0.861), CSR (0.933), BE (1.031), and SS (0.884). The standard deviation is a measure of the spread or variability of the datapoints around the mean. It quantifies how much individual datapoints deviate from the mean.

6. Results and Analysis

To measure the validity and reliability of the instrument and the research framework, partial least squares structural equation modeling (PLS-SEM) was used. However, for the analysis of data, a statistical tool, SmartPLS version 3.2.9, was used. PLS-SEM is a variance-based approach that is used to estimate parameters [

63]. This study used PLS-SEM for several reasons, which are consistent with several past studies [

64].

On the other hand, the present study adopts a prediction orientation and has the goal of examining the causal relationship between the independent variable and the dependent variable of the model. In the end, the model of the present study is complex, containing a mediating analysis; therefore, this study preferred to use SmartPLS. On the other hand, there are a few benefits to using SmartPLS [

65]. It has a high level of statistical power. This means that it is more likely to examine the relationship among variables through PLS-SEM. Moreover, there is no sample size requirement in PLS-SEM [

66]. Therefore, this study preferred to use SmartPLS PLS-SEM.

The measurement model was examined using PLS-SEM, which involved assessing the reliability and validity of the data collected, given the use of reflective measurement items. To ensure reliability and validity, item loading was examined, with a threshold of 0.70 or higher, as recommended by Sarstedt, Ringle [

67]. In this study, all loadings exceeded the recommended threshold and were thus retained for further analysis.

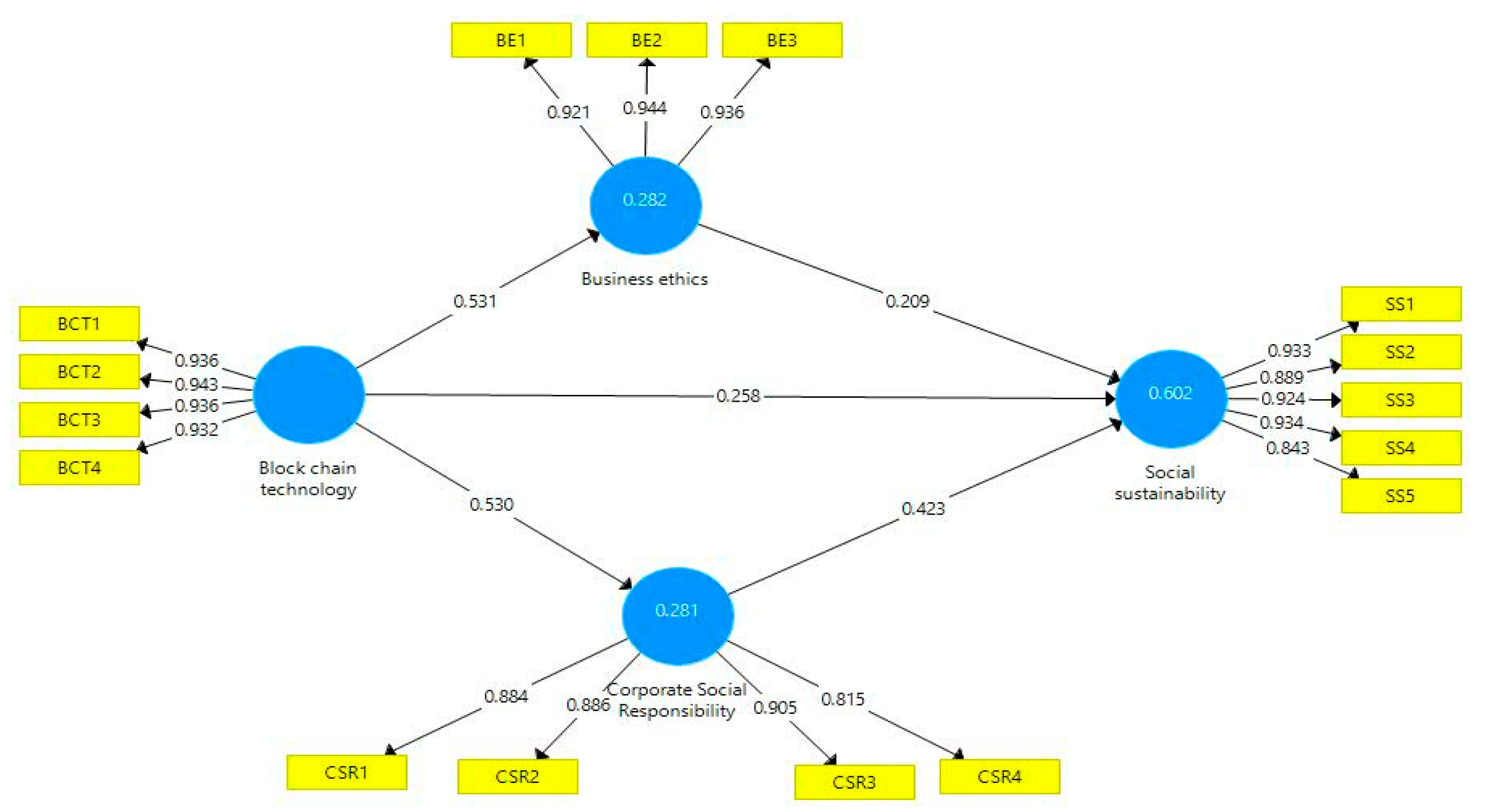

In conducting this study using PLS-SEM, the measurement model was examined, particularly the reflective measurement items. As such, the reliability and validity of the collected data were evaluated based on the loading of items. Sarstedt, Ringle [

67] recommended a loading value of at least 0.70 for ensuring reliability and validity. The results, as shown in

Figure 2 and

Table 3, indicate that all loading values are above 0.70, thus supporting the retention of these items for further analysis. Furthermore, Fornell and Larcker [

68] suggested that the average variance extracted (AVE) should be at least 0.50 to explain the variance of a study. The AVE values, as presented in

Table 4, all exceed 0.50, further supporting this study’s validity. Finally, composite reliability (CR) was used to examine this study’s reliability, with CR values exceeding 0.70 being deemed acceptable.

The present study also evaluated discriminant validity, which refers to the extent to which one variable exhibits empirical difference from other variables. Two approaches were used to assess discriminant validity: Fornell and Larcker [

68] and the HTMT approach. As shown in

Table 5, the diagonal values of the matrix, which represent the square root of AVE, are greater than the remaining values, indicating good discriminant validity according to the Fornell and Larcker approach. Furthermore, all values in the matrix are less than 0.90, as per the criteria of the HTMT (see

Table 6) approach and criteria suggested by Henseler, Ringle [

69], confirming good discriminant validity.

After assessing the discriminant validity, CR, AVE, and factor loading, the measurement model of this study was found to be satisfactory. The next step in using PLS-SEM is to evaluate the structural model [

70], which involves testing the relationship between variables in the study. The level of significance for this study was set at 5%. The estimated values of path coefficients were then used to empirically support the direct and indirect hypotheses. The hypotheses of this study were accepted or rejected on the basis of

t- (more than 1.67) and

p-values.

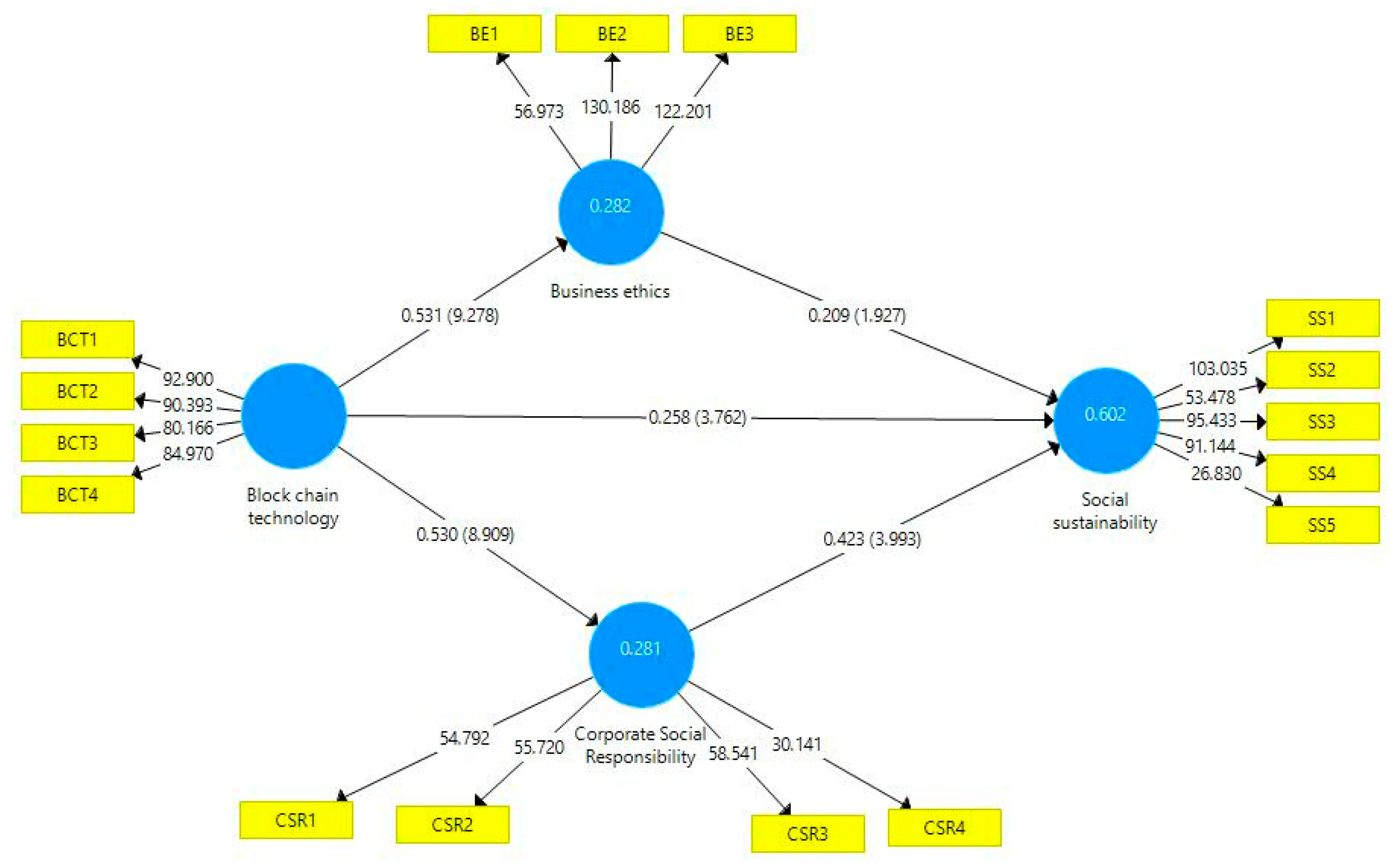

The findings of this study indicate that H1 is supported (see

Table 7), as blockchain technology has a significant effect on business ethics (beta = 0.531,

t = 9.278). Similarly, blockchain technology has a significant positive effect on CSR (beta = 0.530,

t = 8.909), supporting H2. Furthermore, H3 is supported, as blockchain technology has a significant positive effect on social sustainability (beta = 0.258,

t = 3.762). Additionally, H4 is supported, as business ethics have a positive effect on social sustainability (beta = 0.209,

t = 1.927). Finally, H5 is significant, as CSR has a positive relationship with social sustainability (beta = 0.423,

t = 3.993).

Moreover, this study examined the mediating hypotheses. The results in

Table 8 indicate that CSR significantly mediates the relationship between blockchain technology and social sustainability, supporting H6. Furthermore, H7 is also supported, as business ethics significantly mediate the relationship between blockchain technology and social sustainability. Overall, the findings of this study suggest that blockchain technology can have a positive impact on business ethics, CSR, and social sustainability, with business ethics and CSR mediating the relationship between blockchain technology and social sustainability.

This study also examined the value of R square, which measures the amount of variance in the dependent variable explained by the independent variables [

71]. Chin [

72] suggested that an R square value of 0.19 is considered weak, 0.33 is considered moderate, and 0.67 is considered strong.

The R-squared values used for this study involved four variables: BE (business ethics), CSR (corporate social responsibility), SS (social sustainability), and BCT (blockchain technology). The R-squared value for BE is 0.282 (

Figure 3), indicating that approximately 28.2% of the variance in the dependent variable is explained by the independent variable BE (business ethics). The R-squared value for CSR is 0.281, indicating that approximately 28.1% of the variance in the dependent variable is explained by the independent variable CSR (corporate social responsibility). The R-squared value for SS is 0.602, indicating that approximately 60.2% of the variance in the dependent variable is explained by the independent variable SS (social sustainability). R-squared (R

2) is a statistical measure that represents the proportion of variance in the dependent variable that is explained by the independent variables in a regression model. It ranges from 0 to 1, where 0 indicates that the model does not explain any of the variance, and 1 indicates that the model explains all of the variance.

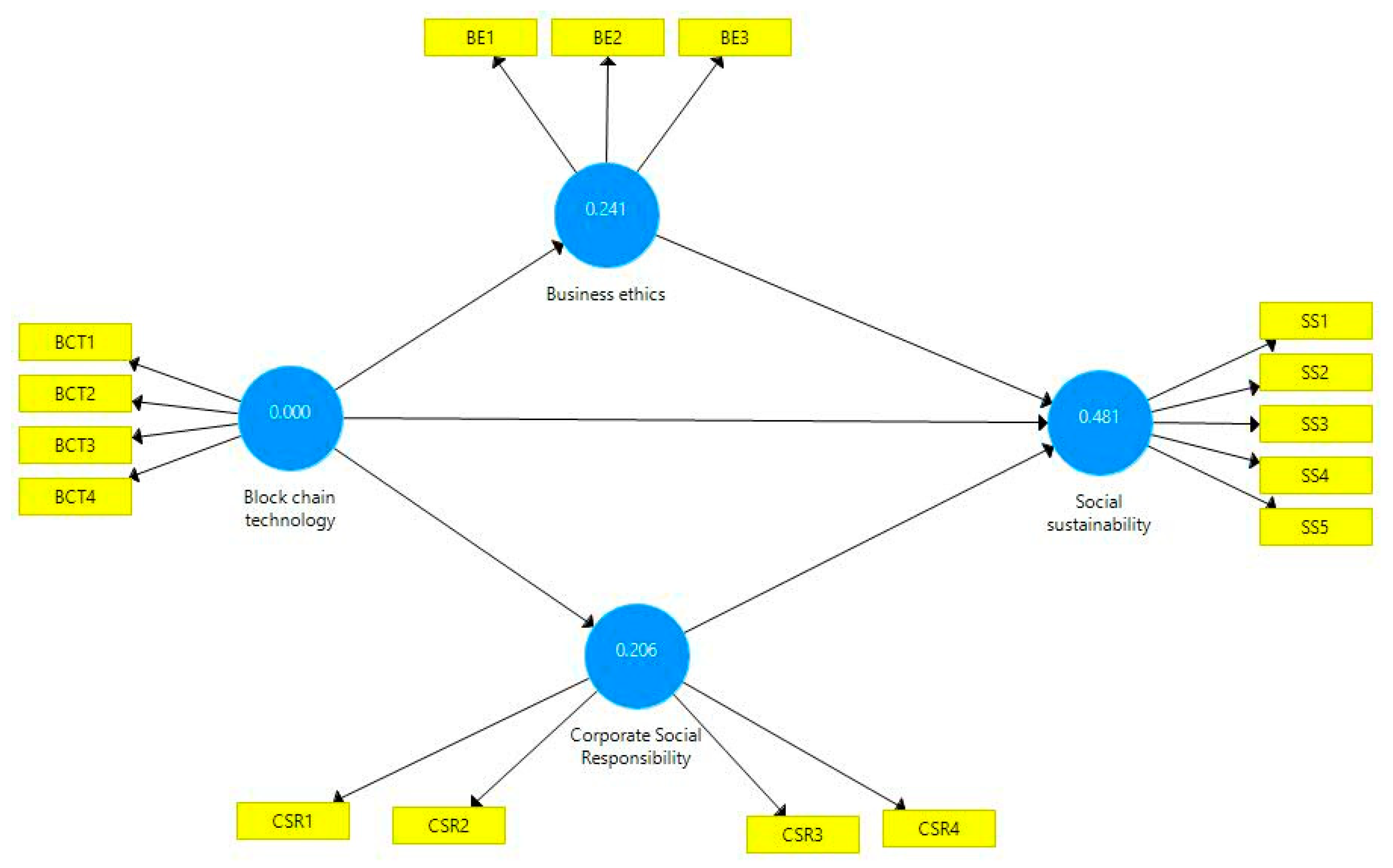

Finally, the predictive relevance of this study was examined. Hair, Risher [

71] explained that the predictive relevance of this study is established if the Q square values are greater than zero. Based on the values of Q square (

Figure 4), this criterion was achieved.

7. Discussion

The results of this research were determined using structural equation modeling. The findings of H1 showed that use of blockchain technology is positively related to the ethical conduct of business operations. Moreover, the findings of existing studies support this relationship. Weking, Mandalenakis [

73] also highlighted that blockchain technology helps firms in improving the fair working of their business. Meanwhile, Mathivathanan, Mathiyazhagan [

74] pointed out that blockchain technology should be integrated in business management for it to work transparently. Demirkan, Demirkan [

75] also asserted the use of blockchain technology for the advanced working of firms. The findings of H2 confirmed that blockchain technology has a positive impact on the CSR. Moreover, the findings of existing studies support this relationship. Nuseir [

76] highlighted that blockchain technology can be fairly used to advance the fair working of corporations. Schneider, Leyer [

77] pointed out that the role of blockchain technology is critical to organizational functioning. Hooper and Holtbrügge [

78] also emphasized the use of blockchain technology for the operational improvement of businesses.

The outcomes of H3 showed that blockchain technology has a positive impact on social sustainability. Moreover, the findings of existing studies support this relationship. Wang, Li [

79] highlighted that newly emerging of technologies can be fairly used for organizational advancement. In accordance, Nuryyev, Wang [

80] pointed out that social sustainability can be achieved with the fair use of technology. Qasim and Kharbat [

81] reported that many international firms use blockchain technology for the reliable functioning of organizations. The findings of H4 showed that business ethics has a positive impact on social sustainability. Moreover, the findings of existing studies support this relationship. Bai, Cordeiro [

82] asserted that ethical management is required for the improvement in a business’ impact on society. Tönnissen and Teuteberg [

83] asserted that only ethically functioning organizations can achieve the goals of CSR. Tan and Sundarakani [

84] asserted that employees of firms should be motivated to work ethically.

The findings of H5 confirmed that CSR has a positive impact on social sustainability. Moreover, the findings of existing studies support for this relationship. Rijanto [

85] reported that CSR is an important factor in organizational sustainability. Khalil, Khawaja [

86] also recommended CSR practices for advancing the work of firms in any market. Mercuri, della Corte [

87] pointed out the sustainability of firms can be achieved by their advanced working through social sustainability. The outcomes of H6 showed that business ethics mediate the relationship between blockchain technology and social sustainability. Moreover, the findings of existing studies support this relationship. Jensen, Hedman [

88] highlighted that an ethical management body can use technology for organizational sustainability. Liu, Wu [

89] reported the importance of technology in the ethical working of organizations to improve the transparency in work. Frizzo-Barker, Chow-White [

90] emphasized the use of technology to modernize business practices and improve people’s understanding. The outcomes of H7 showed that CSR mediates the relationship between blockchain technology and social sustainability. Moreover, the findings of existing studies support this relationship. de Villiers, Kuruppu [

91] pointed out that blockchain technology is helpful in achieving the goals of CSR. Meanwhile, Ronaghi and Mosakhani [

42] pointed out the use of technology in the advancement of working practices.

Enhancing social sustainability is of great significance in improving the quality of society. To this end, this study was undertaken to evaluate diverse factors that can bolster social sustainability. To achieve this objective, data were obtained from bank staff employed in the United Arab Emirates. The research findings suggest that the adoption of blockchain technology by UAE banks plays a pivotal role in enhancing their corporate social responsibility. This is because there are fewer chances of fraud and corruption. Also, all the processes of banks become more transparent. These conclusions are consistent with other work [

44]. Furthermore, the results suggest that CSR plays a pivotal role in cultivating a favorable image among stakeholders, which in turn contributes to enhancing social sustainability. One of the plausible reasons is that it promotes the ethical practices of banks. Moreover, effective CSR can engage stakeholders for a longer period. These findings are consistent with those presented in another study [

53]. Additionally, it is recommended that banks under investigation adhere to ethical business practices, since such practices have a positive impact on social sustainability. These findings concur with the outcomes of an earlier study [

49]. Overall, the results of this study provide evidence of the mediating role of both CSR and business ethics in augmenting social sustainability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}