1. Introduction

Companies that follow green trends and work on the development of green awareness to integrate it into their business policy are considered the companies of the future. The challenges faced by companies in modern business conditions are increasingly imposing the need to integrate the green concept into the business philosophy. Namely, in the 1980s, due to the disclosure of numerous environmental catastrophes, caused predominantly by making profits as the primary goal of the company, there was a significant increase in awareness of the negative effects of environmental degradation on both economic and social spheres. Therefore, the introduction of the practice of corporate self-regulation is becoming one of the most important paradigms on which modern companies want to improve sustainability by integrating elements of the environment into the business policy system. Building the company’s image through socially responsible business, which is in the function of sustainable economic development, imposes itself as one of the managerial postulates and is the key backbone of its survival in the XXI century [

1,

2,

3]. This mechanism is especially recognized in large corporations, which at one point realized that too much desire for profit leads to an imbalance between environmental goals and economic and environmental performance.

At the same time, it is an industry characterized by the current dynamic trend of increasing environmental awareness, which has resulted in the emergence of a new type of tourism, which is recognized as sustainable tourism. Current research documents the role and importance of awareness. In developed European countries 98% of European hoteliers believe that hotel activities have a negative effect on the environment [

4]. Sometimes, however, tourists disregard codes of conduct or are not aware of them. Policies are therefore needed to minimize harm in ecologically oriented tourism areas [

5]. Tourists need to abide by local regulations and avoid damaging the natural environment by exhibiting environmentally responsible behavior [

6]. Hoteliers tend to favor environmental issues, but their attitudes are generally independent of hotel characteristics [

7]. Sustainable tourism has become a response to the damage that mass tourism made to the ecological environment [

8]. It is important to mention that this type of tourism does not refer only to environmental sustainability, but also to cultural, social, and economic sustainability as well. For a short period of type, this type of tourism has taken a significant role in tourism trends in the global market [

9]. There are two main reasons for that. The first one refers to the fact that many important stakeholders in the tourism and hospitality industry have recognized the importance of this issue and have taken a number of measures in order to ensure sustainable development [

8], while the other reason refers to the fact that this type of tourists travels more frequently than the other [

10]. On the other hand, different goals of tourism companies include protecting the natural habitat and attracting and serving tourists at the same time. Competing goals are managed to prevent the area from becoming overexploited and at the same time integrate commercialized tourism as part of local development [

11].

Increasing environmental awareness, as well as changes in tourism demand, make hotels implement environmentally sustainable business practices that require the availability of reliable tools to assess the impact of the hotel on the environment, of which environmental management systems and environmental accounting are emphasized [

12]. So, accounting is needed to find routines, document, and systematically follow up on environmental issues. Accordingly, it is justified to introduce the category of environmental costs, and thus a new branch of accounting that would identify, generate, allocate and analyze these costs, and thus provide qualitative and quantitative information on material and energy flows. The concept of green accounting emphasizes the efficiency and effectiveness of resource use in the function of ensuring a sustainable economy that is encouraged by the promotion and development of value systems such as “clean” technology, i.e., healthy products and processes. More precisely, the green concept has emerged from the desire to achieve a socially responsible relationship with the company that will be in the function of achieving the goals of sustainable development.

Green accounting should answer the question of how environmentally efficient a company is in the process of environmental management through a cost-benefit approach. Efficiency evaluation is performed based on an assessment of future environmental activities (e.g., rational management of waste, energy, and resources) by identifying, analyzing, measuring all costs arising from environmental protection (so-called environmental costs), or based on forecasting certain benefits) that would arise on that basis, especially in the part of the expressed socially responsible attitude. It is a concept that has not yet entered the official normative framework, so it finds its support mainly in voluntary green accounting standards, which significantly lead to fragmentation of reporting. In order to bring green accounting to its full potential, the global accounting authority (International Federation of Accountants—IFAC) intends to implement green accounting standards as obligatory by 2023.

As the mentioned issue is relatively recent, the research work on this topic is very limited, especially in the use of the decision tree model (DT) in considering the relationship between demographic factors of employees in tourism, green concept, and environmental business, i.e., the importance of implementing green accounting to promote and encourage sustainable development in tourism. In that sense, this research will test hypotheses about the influence of socio-demographic factors on the level of knowledge and implementation of green accounting in Montenegro, and provide answers to certain research questions, which indicates the contribution of this research is multiple.

The main goal of this paper is to promote the socially responsible business of tourism companies in Montenegro and the importance of applying ISO standards reports on environmental costs, i.e., green accounting.

This research will generally contribute to raising awareness of the importance of the implementation of green accounting and sustainable development of tourism in Montenegro. Precisely, this work may be an incentive to pay more attention to this issue, both in Montenegro and in other countries in the region. Furthermore, if we take into account the fact that Chapter 27—Environment and Climate Change is one of the most demanding chapters, and also one of the prerequisites for Montenegro’s entry into the community of European countries, this research may serve economic policymakers in gaining additional insight into the perception of green concept by participants in the tourism industry. The contribution of this paper is also reflected in the fact that the DT method for the analysis of corporate social responsibility and green accounting implementation is being applied for the first time according to our knowledge.

The paper is structured into fourth key sections. The first part of the paper is an introduction, followed by a brief review of the literature. The second chapter describes hypotheses, data, and research methodology. The third and fourth chapter of the paper is devoted to research results and discussion, i.e., answers to research questions obtained using the DT model. After the results, the conclusion and the list of literature are presented.

1.1. Policy of Sustainable Development

It is important to mention UN policy in this area, especially the 17 Sustainable Development Goals and 169 targets into the “Transforming our worlds: the 2030 Agenda for Sustainable Development” called Agenda 2030, that have become relevant and crucial at the global level, encouraging the Member States around the world to integrate them into their strategic development policies. The United Nations Team in Montenegro in cooperation with the Government of Montenegro in 2017 discussed how the 2030 Agenda may be linked to the Government’s priority policies to meet defined goals. In that sense, in addition to the raised economic issues that are essential for the implementation of the policy of internal functioning of the EU market, which is regulated in Montenegro by opening a special chapter that deals with issues that focus on this paper, i.e., Chapter 20, somehow it seems that the 2030 Agenda, in particular, puts a priority on environmental sustainability, whose issues are treated separately through Chapters 14, 15, 21 and 27.

Namely, Chapter 27 is the last open and most demanding in terms of interconnection with the 2030 Agenda. It is dominantly focused on air quality measures and wastewater management, nature protection, but also climate change measures which are of crucial importance, having in mind the fact that, according to the obligations under the United Nations Framework Convention on Climate Change (UNFCCC) under the Paris Agreement, Montenegro has committed to reducing greenhouse gas emissions (GHG) up to 35% by 2030 compared to 1990 such a national contribution is needed to support the Paris Agreement, but also to align with the goals set within the Green Agreement for the Western Balkans, which was signed in 2020. It is extremely important to mention the fact that the tourism industry may have a huge potential to contribute directly or indirectly to the achievement of all sustainable development goals defined in the 2030 Agenda.

Thus, sustainable tourism development may strengthen economic growth and development, thus creating jobs and reducing the poverty and hunger; it may empower women and their engagement in business; it may contribute to the rural development as well as promotion of less developed areas, thus reducing inequalities. Additionally, the multicultural and intercultural dimension of tourism may significantly contribute to peace and justice, creating a base for tolerance and understanding; incomes from tourism may be invested in health and education thus improving their quality; it may foster sustainable industry, and infrastructure through different innovative initiatives based on the promotion of green infrastructure, smart and green destinations, etc. The role of tourism may be crucial in the creation of different programs regarding sustainable consumption and production, sustainable use of marine resources, conserving and preserving biodiversity. Additionally, through lowering energy consumption and usage of renewable energy sources, as well as a promotion of innovative energy solutions, tourism may have a leading role in a response to climate changes at the global level.

According to data Voluntary National Reviews (VNRs)

https://montenegro.un.org/sites/default/files/2020-04/_2019_Uzajamne%20veze%20-%20Pristupanje%20EU%20i%20Agenda%202030.pdf (accessed on 28 December 2021) in 2016 and 2017, which included 64 countries, tourism has been recognized as a sector with a high impact and potential to advance all sustainable development goals and 41 VNRs (64%) pointed out one or more direct references to the tourism industry, which highlights the fact that the governments of these countries are fully aware of the importance of tourism as one of the main driving forces for achievement of goals defined by the 2030 Agenda. Mentioned Voluntary National Reviews as well as analyzed MAPS countries roadmaps together with the “Chengdu Declaration on Tourism and the Sustainable Development Goals”

https://www1.undp.org/content/dam/undp/library/Sustainable%20Development/UNWTO_UNDP_Tourism%20and%20the%20SDGs.pdf pages 22–23 (accessed on 28 December 2021) that was adopted by Tourism Ministers during the 22nd UNWTO General Assembly in 2017, represent the excellent framework for strengthening the role and importance of tourism for successful implementation of the 2030 Agenda and full commitment of different stakeholders in the tourism industry to the achievement of sustainable development goals.

1.2. Literature Review

The Financial Stability Board in its report cites negative repercussions that economic inefficiency may cause, especially in the area of environmental management, i.e., it points out that the risks of climate change and a disorderly transition to a low carbon economy could destabilize the financial system and cause asset prices to fall sharply [

13]. For tourism businesses and organizations, the Social Responsibility System is of particular importance, which is owing to the dynamic development of this sector within the national economy, its social orientation on meeting the needs of people, and improving the quality of life [

14]. The issue of integrating the socially responsible business of tourism companies into business practice has been the subject of many authors [

7,

15,

16,

17,

18,

19,

20,

21]. Many of them generally state that a socially responsible attitude of the company, especially when it comes to its social dimension, may produce positive repercussions on the expectations of stakeholders [

22,

23], employee satisfaction [

24]. At the same time, research in this field indicates that one of the motives for introducing the concept of corporate social responsibility in the tourism industry is driven by the desire to achieve greater profit goals, but not to the detriment of society [

23,

24]. Thus, a tourism organization may be called socially responsible if it manages its business taking into account the negative and positive consequences of its activities in the field of environmental protection, economy, and social sphere [

25,

26].

Observed from the other perspective, there is a wide range of research studies that deal with the ecological attitude of tourists towards the environment [

6,

27,

28], where such behavior is recognized as environmentally responsible behavior [

29,

30,

31,

32]. Some research studies have confirmed the existence of a positive relationship between the green image of the hotel and tourists’ favorable behavior [

27] as well as the significant influence of the green image of the hotel on the level of guest satisfaction [

33]. Research on the performance of the Hilton hotel regarding environmental protection identified two most important factors for sustainable management practices and these are: human resources management and corporate social responsibility [

34]. Some authors point out that education in the field of life protection has an impact on the development of environmental awareness, i.e., environmentally responsible behavior of tourists [

35], while there are also some authors who believe that policy instruments play a crucial role in sustainable development [

36,

37,

38].

To ensure the efficiency of sustainable development, especially in the field of environmental protection, the concept of green accounting is increasingly being discussed, which should be institutionalized by deciding on the introduction of a green standard of financial reporting [

39,

40,

41]. As such, green accounting should improve the system of financial and non-financial reporting, through the identification, monitoring, and reporting of positive and negative activities related to the environment [

42]. The focus of green accounting is also the identification, systematization, allocation, and control of environmental costs [

43,

44]. Research conducted so far indicates that green accounting produces a significant impact on the financial position of the company [

45], i.e., that the company’s profitability is linked to the application of the green concept [

46].

When it comes to the implementation of green accounting in the tourism and hospitality industry, there are a few theoretic and research studies [

47,

48,

49]. Vejzagic et al. target some segments of this important issue such as measuring of eco-efficiency of tourist destination [

50], the relationship between the green reputation of the hotel and green accounting and harmonious culture [

51], environmental management in hospitality industry [

52], the relationship between sustainability management, financial reporting and business performance [

53], but, according to the findings of authors, there are no papers that discuss and analyze the influence of different socio-demographic factors on the familiarity of employees in the tourism and hospitality industry with green accounting, the level of their awareness about the importance of integration of green accounting in the business and similar areas.

2. Hypotheses, Materials, and Methods

Based on relevant literature and data obtained from the empirical research, i.e., surveys of employees in tourism companies in Montenegro, two hypotheses will be tested:

Hypothesis 1: The familiarity with the concept of green accounting is, of all socio-demographic factors, most significantly influenced by work on education, workplace, and level of education.

Hypothesis 2: The awareness of the importance of implementation of green accounting is, of all socio-demographic factors, most significantly influenced by work on education, workplace, and level of education.

Moreover, this paper will answer four research questions: (a) RQ1—which tourism companies integrate corporate social responsibility into their business strategy? (b) RQ2—which companies from the tourism sector introduce the ISO 14001 standard related to the environmental management system? (c) RQ3—which companies in the tourism sector prepare reports on environmental costs? and (d) RQ4—which companies in the tourism sector have started to implement green accounting?

The research on the implementation of green accounting in tourism companies in Montenegro (

Appendix A) was conducted by surveying employees in the second half of 2021. A total of 115 employees in tourist companies (hotels, tourist organizations, restaurants, boarding houses, etc.) of different age groups, levels of education, work experience, etc., were surveyed on the knowledge and implementation of socially responsible business and environmental accounting. The survey is conceived in such a way that in the first part the respondents are segmented according to demographic and sociological factors, while the second part of the survey examines the implementation of environmental management systems, i.e., preparation for implementing green accounting in tourism companies.

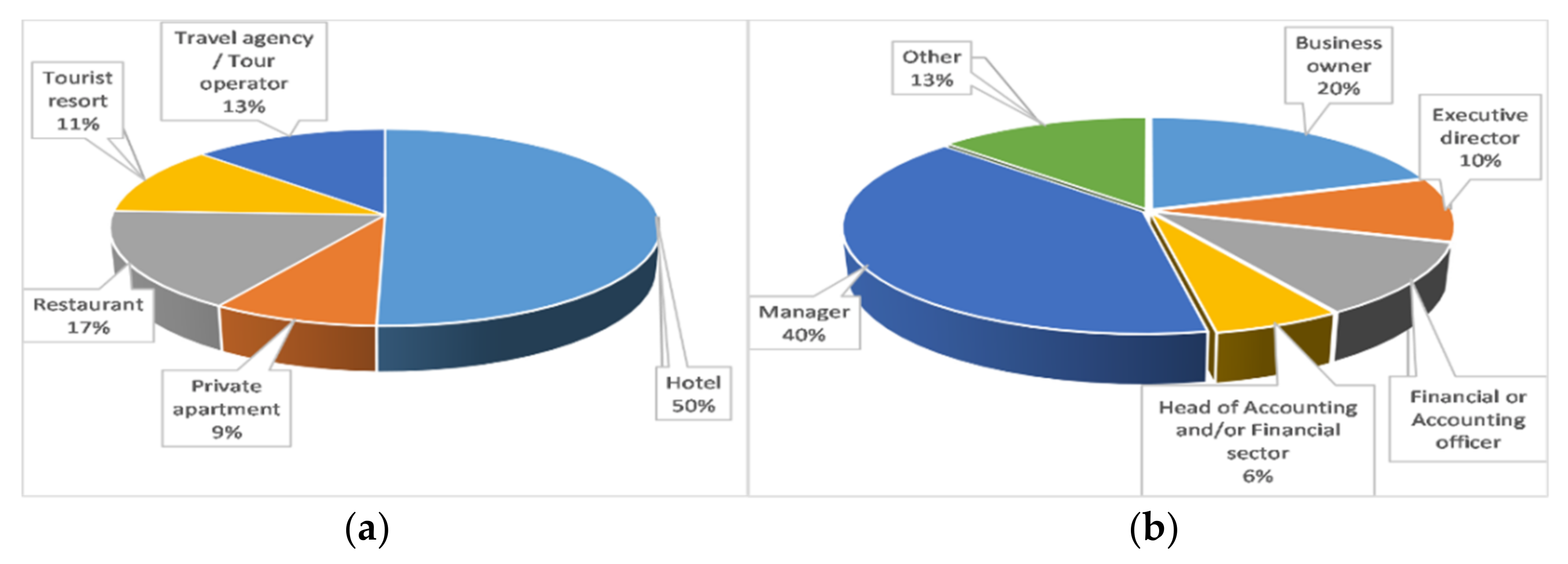

Descriptive statistics were used as the first step in data analysis, i.e., the collected data were described graphically. In the structure of the total number of respondents, respondents from hotel companies (50%) are dominant (

Figure 1a, left), with the most represented category of respondents in the position of manager (40%), or business owner (20%), which is significant from the aspect of the relevance of the answers received, i.e., their place and role in the management structure of the company (

Figure 1b, right).

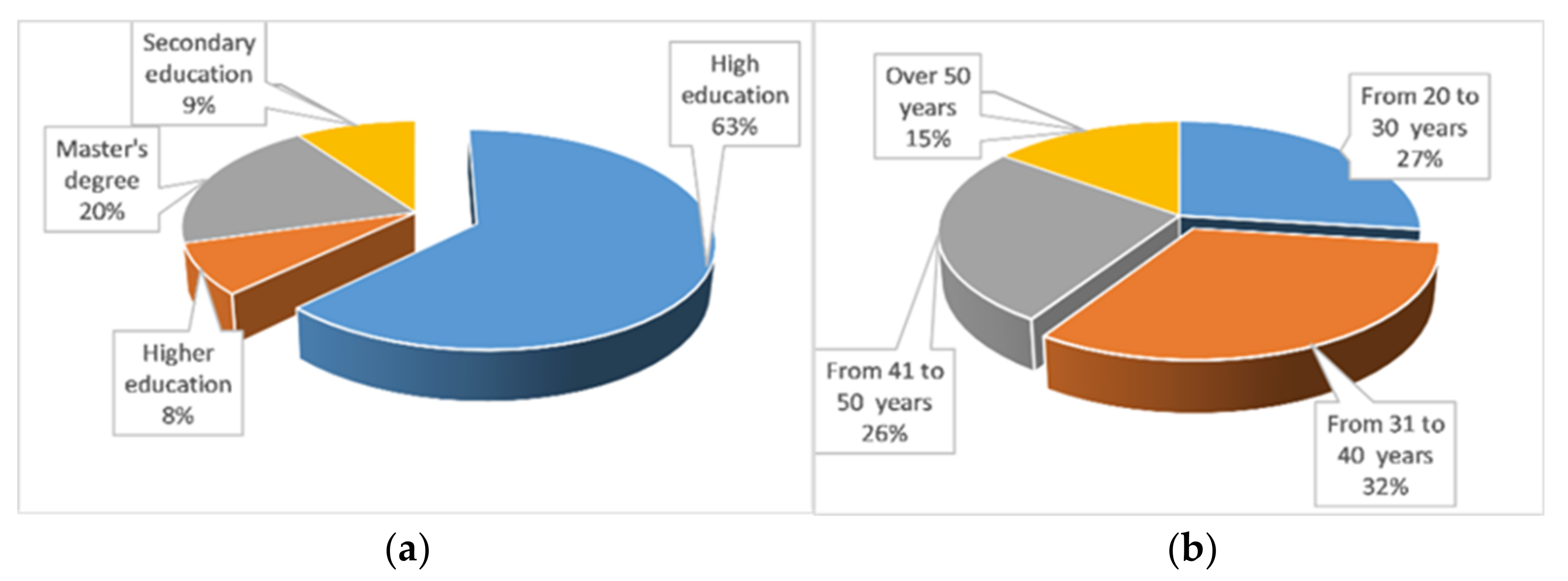

By further analysis of respondents, it may be concluded that this is the most highly educated staff, which is confirmed by the fact that the predominance of respondents with high education (63%) or master’s degree (20%) (

Figure 2a, left), and that 58% said that continuously work on education, i.e., only 3% expressed a negative attitude regarding this issue. Observing the respondents through the prism of age, it may be noticed that young respondents are significantly present (32%, from 31 to 40 years and 27% from 20 to 30 years) (

Figure 2b, right). The presented results in terms of education and age are especially important for the tourism industry, which is heterogeneous, dynamic and which, due to its specificity, requires consistency in the implementation of new knowledge, skills, and competences of employees.

In the context of the previously mentioned statement about the younger population of respondents, it is logical to conclude that their working experience in terms of age is relatively modest, which is confirmed by the fact that the most represented respondents have working experience up to 10 (50%) or 20 years (31%). Furthermore, by analyzing the obtained results, it may be stated that over 90% of respondents are aware of the importance of corporate social responsibility of the company, and 94% of respondents stated that the company in which they work considers socially responsible business.

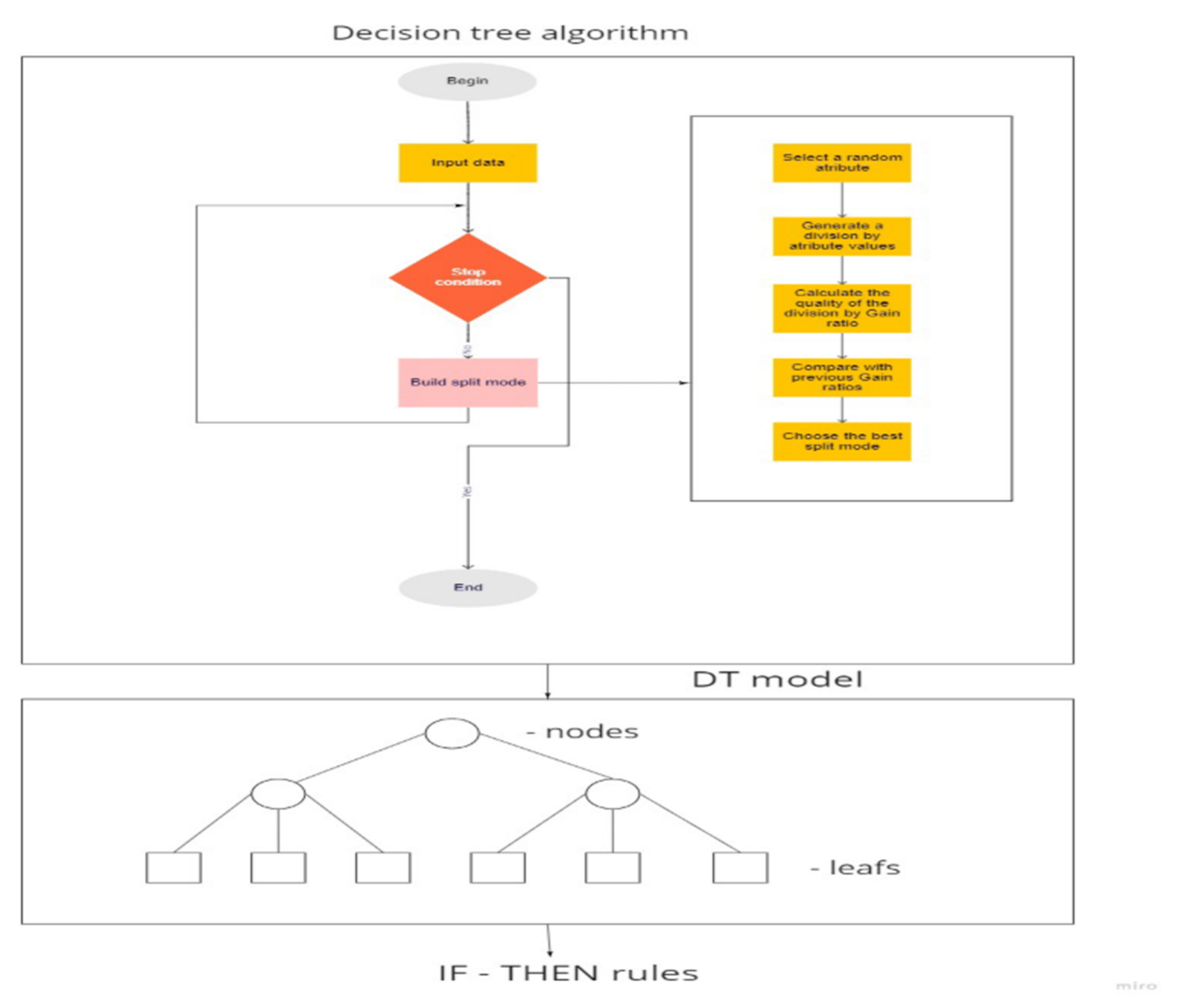

Classification “data mining” methods are increasingly used for the analysis of survey data, especially the method of machine learning, i.e., the Decision Tree (DT) method [

54,

55,

56,

57,

58]. In this context, in this research, the DT method was used, which identifies connections between dependent and independent variables through the so-called structure of the tree, i.e., nodes, branches, and leaves. Each node in the tree is associated with one of the independent variables, and each branch of the tree with a subset of the values of the corresponding independent variable. If the target variable is discrete (has a limited number of values), then the tree is considered a classification tree, and each leaf represents one value of the target variable (one class).

The DT algorithm also generates relative frequencies for each leaf, i.e., the probability of belonging to the class that this leaf represents (Rule accuracy). The tree induction process recursively divides the initial data set into subsets. The goal of each iteration is to get the best possible division. The separation method may differ depending on the DT algorithm itself, which defines the variable to be assigned to the node in the tree. Each branch of the tree that emerges from that node corresponds to one of the obtained subgroups. When a tree is generated on an entire data set with a categorical target variable, then the model allows classification because the initial data set is divided into classes (defined by the values of the target variable), and each class is assigned an appropriate classification rule to read from the tree. We emphasize that not all rules have the same meaning. More important are those rules whose leaf contains several examples of the class represented by that leaf.

The number of correctly categorized examples relative to the total number of examples represents the accuracy of classification, while the number of misclassified examples relative to the total number of examples represents classification error. Important measures of classification accuracy are class precision (the number of accurately classified instances of one class in relation to all the instances that the model classified in that class), as well as class recall (the number of members of the class that the model correctly classified in relation to all members of that class) [

57].

The following chart illustrates the complex number of steps and procedures used in this research (

Figure 3).

3. Results

In order to test the hypotheses defined in this paper, the following DT models were generated:

- 1

DT1—Socio-demographic factors and respondents’ familiarity with green accounting

- 2

DT2—Socio-demographic factors and the implementation of green accounting in Montenegro

For dependent variables, one DT model is generated, which classifies the data according to the values of that variable. Each class is described by “if-then” rules through independent attributes.

In all DT models, the rules are read from root to leaves. Each leaf corresponds to an “if-then” rule. Leaves represent the values of the dependent variable. The most important are those leaves that have a thicker rectangle at the bottom, which means that the rules that correspond to them refer to a larger number of data, but the so-called “Victory margin”. The victory margin for a rule is higher if the color in the rectangle at the bottom of the corresponding list predominates, with each leaf (dependent variable) being assigned the corresponding color. It is impossible to expect an ideal classification where there would be the same color in each leaf. Accordingly, any accuracy greater than 50% in leaves is acceptable, but the rules that suit leaves with greater accuracy are more important, so they should be taken into account during the analysis of DT models (thicker rectangle and higher representation of appropriate color in the leaf).

The results of the models are shown in the following figures and tables.

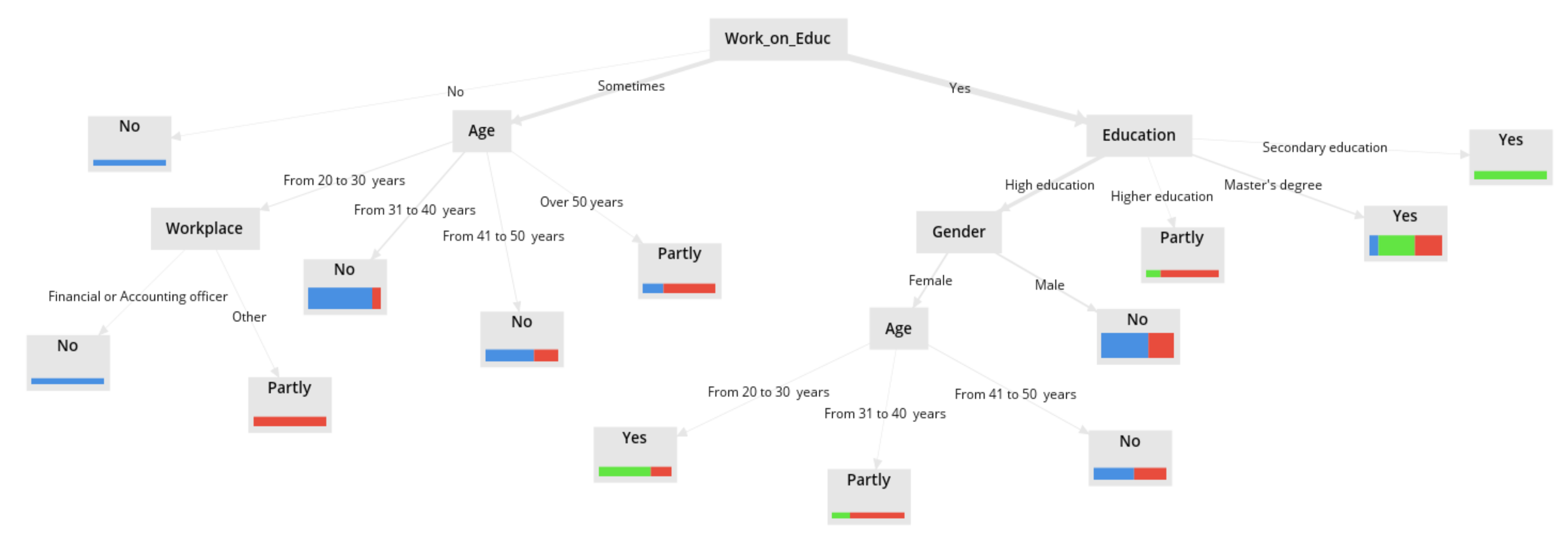

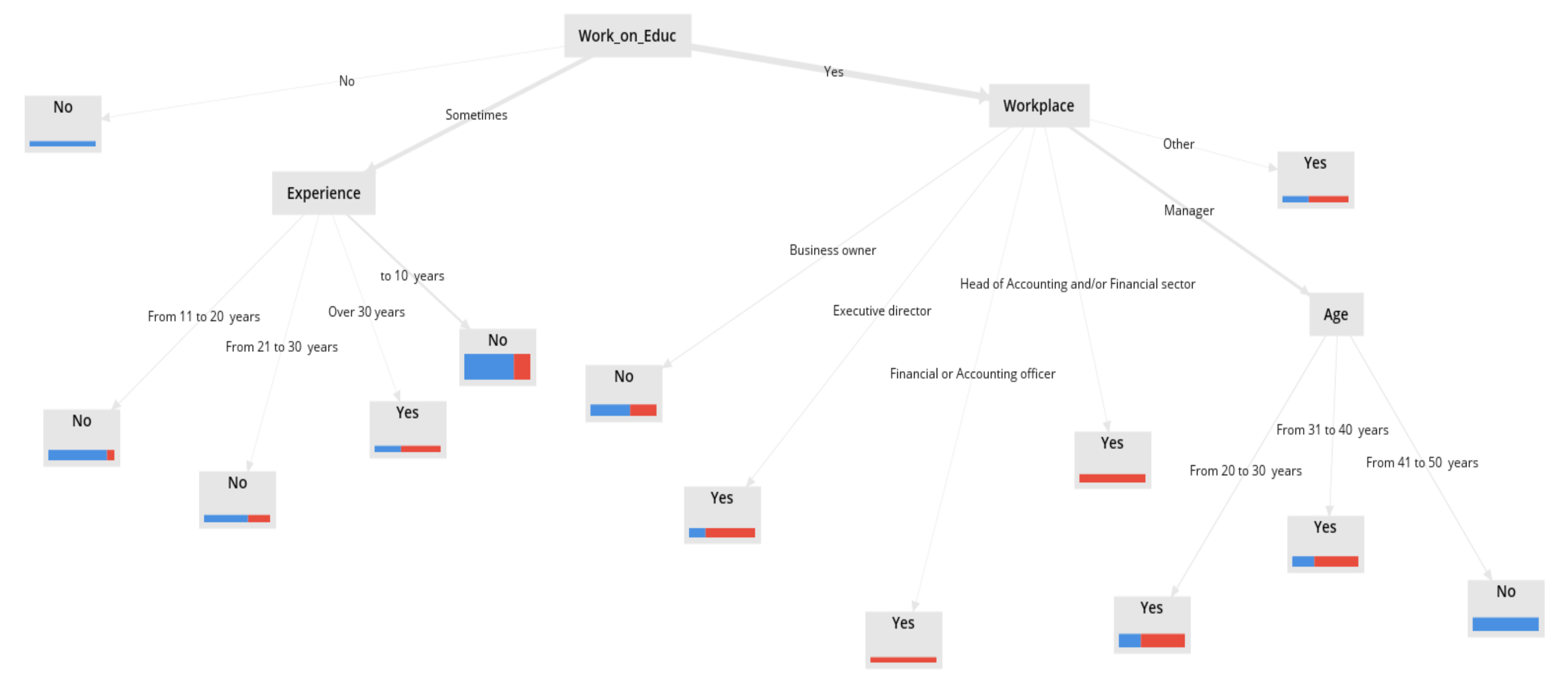

In

Figure 4, the leaves represent a dependent variable, i.e., the familiarity of respondents with green accounting. Partial familiarity is highlighted in red. Blue indicates that the respondent is unfamiliar with green accounting, while red indicates that he is familiar. Each leaf is assigned an if-then rule that is viewed from left to right (first rule—first leaf left, last rule, last leaf right).

Figure 4 shows that the thickness of the leaves is most pronounced in 4, 10, and 12. Additionally, it is interesting to look at leaves 3, 6, and 7. In these leaves, the number of examples (data) in the leaf makes an acceptable percentage of the class to which the leaf belongs and the probability of accuracy of the application of the rules is the same, i.e., more than 50%. By interpreting the rules relating to the leaves from

Figure 4, it may be concluded that employees in tourism aged 31 to 40 years, who occasionally work on their education are not familiar with green accounting (leaf 4), as well as the male population who has a bachelor’s degree (higher education) and who works on their education (leaf 10). Employees who are familiar with green accounting are those who have a master’s degree and who are continuously working on their education (leaf 12), as well as women aged 20 to 30 with a bachelor’s degree, who are also continuously working on their education (leaf 7). Respondents aged 20 to 30, as well as those over 50, who occasionally work on their education, are partially familiar with green accounting (leaf 3, 6).

The following table also shows the rules of the socio-demographic profile of the respondents, derived from this DT model, as well as the precision of the rules themselves (

Table 1).

Overall Accuracy in this model is 73.91% and is based on the Confusion Matrix (

Table 2).

The influence of sociodemographic and other factors on classification is calculated based on the Gain Ratio measure, as a measure used for the purity of division [

59,

60]. For the DT1 model, the greatest impact on the familiarity of respondents with the concept of green accounting has the work on education, then workplace and education and the least gender, which is shown in the following table (

Table 3).

The second tree, DT2, shows the impact of socio-demographic factors on the awareness of respondents about the importance of the implementation of green accounting in Montenegro.

In

Figure 5, the leaves represent a dependent variable, i.e., the respondents’ awareness of the importance of the implementation of green accounting in the company. Blue indicates that the respondent is not aware of how important the implementation of green accounting is, while red means that he is aware. The thickness of the leaves is most pronounced in leaf 5, and then partially in leaves 10 and 12. Additionally, leaves 2, 11, and then 7 and 9 may be observed. In these leaves, the probability of accuracy of the rules is higher than 50%, and it can be stated that employees in tourism with working experience up to 10 years, who occasionally work on their education, are not aware of the importance of the implementation of green accounting (leaf 5). Managers of tourism companies, who are continuously working on their education, aged 20 to 40, are aware of how important the implementation of green accounting in their companies is (leaves 10 and 11), while those aged 41 to 50 are not (leaf 12). Additionally, respondents who occasionally work on their education, with working experience of 11 to 20 years, are not aware of the importance of implementation of green accounting (leaf 2). Executive directors, i.e., heads of financial and/or accounting departments, who continuously work on their education, are also aware of the importance of implementation of green accounting in practice (leaves 7, 9).

The following table shows the rules as well as the precision of the rules themselves within the DT2 model (

Table 4).

Based on the Confusion Matrix, the overall classification accuracy in this model is 77.39% (

Table 5).

As with the previous model, and based on the Gain Ratio, the greatest impact on respondents’ awareness of the application of green accounting has worked on education. In this model, age has the least impact of all the attributes (

Table 6).

Thus, DT1 and DT2 showed that hypotheses 1 and 2 were not rejected, i.e., that socio-demographic factors have a significant impact on the familiarity of employees in tourism companies with green accounting, and on the awareness of owners and employees on the importance of its implementation.

Of all the observed attributes, the greatest influence in both models on the dependent variables has the training of employees after obtaining a certain education, i.e., work on education.

This result is justified, since continuous education, which is especially immanent to the accounting profession emphasizes innovations that are present in the accounting sphere, i.e., those innovations that the accounting community can get acquainted with and implement.

Table 3 and

Table 6 also show that both workplace and education (degree) have a significant impact on both dependent variables. This is because a higher level of education and a higher hierarchical level at work, or greater responsibility that the workplace brings with it, requires a higher level of knowledge, awareness, and understanding of the importance of each business concept, and thus green accounting.

Further, in order to get answers to the research questions, four more DT models were generated, as follows:

- (1)

DT3—Implementation of corporate social responsibility (CSR)

- (2)

DT4—Introduction of ISO 14001 standard

- (3)

DT5—Preparation of reports on environmental costs

- (4)

DT6—Implementation of green accounting in the tourism sector of Montenegro

For the DT3 tree, whose if-then rules are shown in

Table 7, it is important to analyze leaves 1, 5, and 7, because the number of examples (data) in the leaf makes an acceptable percentage of the class to which the leaf belongs. For all leaves in DT3, the “victory margin” is satisfactory. This further means that hotels in Montenegro, integrate CSR into their business policy (leaf/rule 1). On the other side, restaurants, regardless of whether their managers include or do not include a description related to environmental protection in their report, do not integrate CSR into their business policy (leaf/rule 5 and 7).

Based on the Confusion Matrix (

Table A1 in

Appendix B), the overall accuracy of classification in the DT3 model is 97.39%, while the greatest impact on the integration of CRS into business strategy and company policy is the type of tourism company, i.e., a type of company and the smallest education and preparation for the implementation of green accounting (

Table A2 in

Appendix B).

Therefore, the type of company, but also the attitude of the employees that the incentive for environmental management is based on the pressure of stakeholders, have the most significant impact on the application of CSR. In general, not all companies have the same level of awareness of corporate social responsibility, which was ultimately confirmed by the above research. It is logical that large companies, especially companies that have the influence of foreign capital and have a slightly different business philosophy compared to the domicile Montenegrin, have a more developed level of knowledge about the benefits of corporate social responsibility and green concept in sustainable development. As respondents from smaller or micro-tourism companies, who are particularly exposed to the challenges of market survival, also took part in the research, the issue related to environmental protection was not set as a priority among them. On the other hand, to leave the impression of a socially responsible company, employees are often subjected to pressure to promote this approach in a certain way in public. For the DT4 tree, leaves/rules 3, 6, 10 and 14 are important (

Table 8).

For all leaves in the DT4 algorithm, the “victory margin” is satisfactory, i.e., more than 50%. This further means that tourism companies in Montenegro that use information about environmental protection, especially when calculating the costs and effects of environmental protection, as well as those that take care of waste, have not yet officially introduced the application of ISO 14001 (rule 3). Tourism companies that use information related to environmental protection, especially when budgeting, have introduced the ISO 14001 standard (rule 6). Respondents who did not know whether their companies had introduced the ISO 14001 standard belong to companies that do not use environmental protection information and think that the incentive for environmental management is based on pressures from stakeholders such as regulators, investors, the community, environmental organizations, etc., (rule 14). Moreover, respondents who belong to the companies that care most about waste, and who also do not know whether their companies use the information on environmental protection, or whether the Management Report describes the aspect related to environmental protection, were not informed about whether their company introduced the ISO 14001 standard (rule 10).

Based on the Confusion Matrix (

Table A3 in

Appendix B), the total Overall Accuracy in the DT4 model is 79.13%.

The use of information related to environmental protection has the greatest impact on the introduction or non-introduction of the ISO standard. On the other hand, the attitude of employees in terms of pressures and incentives for environmental management has the least impact. (

Table A4 in

Appendix B)

In model DT5, (

Table 9), it is valid to consider rules 1, 3, and 14, based on which it may be concluded that those tourism companies that use environmental protection information when calculating costs and effects, do not create a report on environmental costs (rule 1), as nor those companies that do not consider information related to environmental protection (rule 14). On the other hand, companies that use information related to environmental protection in alternative business decisions and that believe that the incentive for environmental management is based on the pressure of stakeholders are preparing a report on environmental costs.

The overall Accuracy in the DT5 model, based on the Confusion Matrix, is 89.57% (

Table A5 in

Appendix B), while as in the previous model, environmental protection information has the greatest impact on the Environmental Expenditure Report, while as with the previous model, the attitude of employees regarding pressures and incentives for environmental management has the least impact (

Table A6 in

Appendix B).

The last algorithm should provide an answer to the research question of which are the tourism companies that implement green accounting in Montenegro. Based on the importance of the rules and the “margin of victory”, the analysis should focus on the leaves (rules) number 1, 2, and 13 described in

Table 10.

DT6 shows us that respondents who do not know whether their company includes an environmental description in the Management Report also do not know whether their company implements green accounting (rule 1). Companies that do not include a description of environmental protection in the Management Report, but which use information related to environmental protection when calculating costs and effects arising from environmental protection activities, do not implement green accounting (rule 2). Finally, only those tourism companies that include an environmental description in the Management Report and whose respondents (owners and/r employees) believe that environmental management incentives are based on stakeholder pressures implement the concept of green accounting.

The overall accuracy of classification in this model, based on Confusion Matrix is 81.74% (

Table A7 in

Appendix B).

The greatest impact on the implementation of green accounting in tourism companies in Montenegro has the inclusion of a detailed description of environmental aspects in the Management Report, then the use of information related to environmental protection, and the smallest is the type of company (

Table A8 in

Appendix B). We believe that this result is a consequence of the current legislation (Law on Accounting of Montenegro), according to which the management report, among other things, must contain information on investments to protect the environment.

Finally, it should be emphasized that there is a positive but very small correlation between the familiarity of respondents with green accounting and their awareness of the importance of implementing the green concept with the introduction of ISO standards on the one hand, but also with corporate social responsibility (

Table 11).

4. Discussion

The results of the DT1 and DT2 models confirmed that, above all, work on education as well as education itself, plays a significant role in awareness of the importance of the environmental concept and green accounting, which has been previously confirmed in the literature. Specifically, several other authors point out that sociodemographic factors, especially education has an important impact on the development of environmental awareness. For example, Hsieh and Jeon concluded that hotels first have to discover barriers for environmental practices implementation, and then develop methods for their resolving, organizing workshops, conferences and exchange data of best environmental practices, etc., [

61]. Wang and Wang consider that sustainable development of hotels is based on “greening” their businesses, dealing with lifelong learning [

21]. For sustainable tourism, training of personnel with educational programs is extremely important, so that employees serve more consciously and in teamwork [

47]. In relation to educational levels and environmental concerns, being more highly educated is presumed to enable people to become better informed about environmental and social issues [

62]. There is some empirical support that educated people to show more environmental concern than people with lower education levels [

63,

64]. However, other researchers have found no relationship between educational level and environmental concern [

65,

66].

The results of the DT3 model show that tourism companies, especially hotels in Montenegro, integrate CSR into their business policy, while some other companies, for example, restaurants, do not integrate CSR. More precisely, the implementation of CSR mostly depends on the type of tourist company. For example, hotel companies in Spain, in order to achieve a sustainable competitive advantage, implement CSR, taking significant efforts to decrease environmental pollution and energy consumption, and use new technologies and recycled materials [

19]. On the other hand, Bohdanowicz points out that hotels in Spain and Poland recognize the need for environmental protection and that they are activated in many activities, but this is not their main priority [

20]. Some studies indicate that environmental responsibility is higher for those hotels with defined environmental policies, which are in foreign ownership, which are part of hotel chains, and which achieve high financial performance [

67].

Analyzing the results of the DT4 model, it is noticed that tourism companies that use information related to environmental protection, especially when budgeting, have introduced the ISO standard related to the green concept. Ienciu showed that certification of the environmental management system according to ISO 14001 contributes to a higher level of voluntary reporting of environmental performance [

68]. Companies that have successfully implemented the ISO standard have achieved certain benefits not only in terms of increasing profitability, but also in terms of increasing business efficiency, better image, and improving environmental awareness through proactive action in the direction of environmental protection [

69].

The results of the DT5 model indicate that a small number of tourism companies prepare an environmental cost report, i.e., these reports are disclosed by companies that use information related to environmental protection in alternative business decisions and believe that the incentive for environmental management is based on the pressure of stakeholders. As with the previous model, the algorithm of the DT6 model indicates that there is also a small number of tourism companies that implement green accounting, i.e., that this concept is implemented by companies that include a detailed description of environmental protection in the Management Report.

Similar to Montenegro, hotels in Croatia are far behind the global competition in the area of sustainability reporting and their sustainability reports mainly miss relevant information [

70]. The statement that the hotel industry needs reliable and universal tools for reporting and comparing environmental performance is indicated by some authors who also emphasize that all sectors of the hotel industry have to participate in this process, as well as scientists and legislators [

4]. Buyukipekci indicates that 5-star hotels are quite sensitive in terms of sustainable tourism because they have to take environmental costs into consideration, as well as some of the 4-star hotels [

47]. Jankovic and Perisic offer recommendations for the initial development of environmental accounting practices for hotels and their departments [

49]. Jankovic et al. argue for the importance of developing relevant cost management systems and also describe the model for the implementation of environmental accounting in hotel organizations [

48].

5. Conclusions

Growing awareness, especially in the corporate world, about the importance of environmental cost management, has led to the birth of the green concept as a new business philosophy. Although green accounting has only recently begun to enter the international accounting framework institutionally, the available scientific literature indicates that this is a concept that, through socially responsible business, began to occupy the attention of researchers two decades ago. Specifically, the concept originally began to attract the attention of the large corporate community and over time became an integral part of their business concept. In this regard, this research tried to examine the extent to which the green concept is present in the tourism industry, i.e., in the strategic branch of development of the Montenegrin economy.

This study has empirical, methodological, and practical contributions. Namely, the results supplemented the lack of empirical findings for the Montenegrin tourism sector. Methodologically, for the first time according to the available literature for the analysis of this type, the DT method is applied, which makes it more efficient and accurate than standard statistical analyzes. The results of the research obtained using the DT model led to various conclusions regarding the knowledge and importance of the application of green accounting in tourism in Montenegro. The models showed that socio-demographic factors have a significant impact, both on the information of tourism employees about what green accounting is, and on their understanding of the importance of implementation of green accounting in practice. The models showed that understanding the green concept and understanding the importance of its implementation depends to a large extent on the additional education of tourism employees. Additionally, the DT model showed that most tourism companies in Montenegro (hotels, private apartments, resorts, as well as travel agencies/tour operators) include CSR in their business strategy and policy. Furthermore, it may be concluded that tourism companies that use information related to environmental protection, especially when budgeting, have introduced the ISO standard related to the green concept. In Montenegro, especially large companies (banks, telecommunications sector) with the influence of foreign capital have a proactive environmental strategy thanks to the incorporation of ISO 14001 standard. At the same time, almost the entire health care system (private and public sector), as well as large retail chains and larger hotel complexes, have adopted an integrated management system as one of the important tools for continuous and proactive business improvement, The algorithm also showed that companies belonging to the tourism sector generally do not prepare a report on environmental costs, while green accounting is applied by those tourism companies that include a detailed description of environmental protection in the Management Report and in which the general opinion is that environmental management incentives are based at stakeholder pressures.

The results and validity of the model (good classification performance) confirmed that the DT method is effective for the analysis of this type of research. The advantage of the DT method is that it provides clear rules, easy to interpret, which can be used to conduct an in-depth analysis of survey data. Furthermore, this method works successfully with the categorical data that most often appear in this type of survey. This paper contributes to the existing literature from the methodological aspect because it confirms the advantages of DT methods for the analysis of this kind.

Bearing in mind that this is the first research not only in Montenegro but also in the region that analyzes and discusses this extremely important issue, its results may be very useful for many stakeholders in tourism in the hospitality industry. This is extremely important for Montenegro which is the first and still the only ecological country in the world. The topic is especially important due to the climate challenges faced at the global level, but also due to the fact that Montenegro is in the process of joining the European Union, and that Chapter 27—Environment and Climate Change is one of the most crucial in the process of EU integrations. Except the practical, the authors of the paper believe that this research may give an important theoretical contribution, filling the gap in the literature that exists in this field, especially regarding Montenegro and countries in the region. It is also strongly believed that the results of this research will contribute to raising awareness about the importance of not only implementation of green accounting, but sustainable development in general and future discussion of this topic, which may give the additional contribution to facing challenging of climate changes not only nationally, but globally as well.

The limitations permeated through this paper relate to the insufficient research base, which limits better comparative experiences, both in terms of available literature and in the implementation of green accounting in the tourism industry. At the same time, it should not be overlooked that the online research conducted during the COVID pandemic can also be considered limiting in terms of the relevance of the responses because there is a possibility that implementation of some other method of data collection such as interview would provide us deeper inside into the analyzed topic and somehow different insights. Moreover, the focus of this research was predominantly on respondents coming from the coastal region of Montenegro, which can also be considered a limitation since Montenegrin tourism offer includes the central and the northern region as well especially in terms of eco, rural, medical, sports, cultural and other types of tourism. From a methodological point of view, one of the limitations of this research is that the treatment of DT models can be complex because it requires knowledge and skills in the field of machine learning.

Future research could go in the direction of expanding the research work by the inclusion of respondents from the central and north part of Montenegro, as well as analyzing the comparative experiences of countries in the region, not only those that give priority to summer/coastal but also other types of tourism. Additionally, considering the fact that the concept of green accounting is very broad, the future research could be focused on the analysis of green accounting at the level of management, i.e., cost accounting, which is important especially in determining the more realistic cost price, but also in obtaining more relevant reports on potential and realized performances of the company’s management.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}