Abstract

This review article seeks to discuss the sustainability accounting concept by examining previously conducted studies on this topic in order to understand its thematic progress in the academic literature. This study is a metasynthesis, where, in the identification phase, 334 documents published in the Web of Science (WoS) database are selected, and in the literature review stages, 15 re-reviews are selected according to the Preferred Reporting Items for Systematic reviews and Meta-Analyses (PRISMA) method. The results reveal that businesses, academia, and regulatory bodies do not recognize a homogeneous terminology when it comes to sustainability accounting. There is a variety of synonyms that complicate the disclosure of activities carried out by companies in the pursuit of the sustainability development goals (SDGs), with SDGs 5, 6, 13, 14, and 15 being analyzed in the academic literature in relation to the sustainability accounting concept. For future research directions, the review articles analyzed suggest examining the concrete effects produced by practices related to sustainability performance in companies, linking the relevance of understanding the sustainability reports related to the sustainability performance of companies.

1. Introduction

To ensure that sustainability practices become deeply embedded in organizations, it is vital that reporting integrates sustainability measures and tools, such as social, environmental, and governance metrics, in order to demonstrate market interest in non-financial metrics, including sustainability [1,2,3]. Accounting work is closely related to what information needs to be collected because this depends on the accounting transactions that are processed and subsequently disclosed in financial, non-financial, and sustainability reports. There is a general agreement on the importance of disclosing companies’ sustainability performances, but there is a gap in accounting standards to delimit them [4,5].

However, the problem lies in the fact that there is no single standard that indicates the information that must be disclosed—or the obligation to disclose—on the actions carried out by companies and the economic, social, and environmental impacts that they generate [1,6]. In addition to the situation described above, there is a multitude of complex and confusing terminologies currently used in the sustainability accounting framework and its respective reports [7]. This situation complicates the recording, processing, and dissemination of information related to sustainability development.

The present review aims to analyze the sustainability accounting concept by examining previously conducted studies in order to understand the progress of the subject in the academic literature. This paper is structured as follows: Section 1, Introduction; Section 2, Background Literature; Section 3, Methods; Section 4, Metasynthesis Results; Section 5, Discussion; and Section 6, Conclusions.

2. Background Literature

2.1. Sustainability Accounting at Present

There are environmental, social, and ethical issues that can be managed in time by companies or organizations with an assessment of their interactions with the environment and society [8,9,10]. Many stakeholders expect companies or organizations to carry out practices aimed at sustainability and to report these actions and their results [11,12,13]. There is a need to understand sustainability development in a holistic and comprehensive manner, as it is essential for the future of the human species to ensure that we leave future generations with a habitable planet [14,15,16]. Under the heading of sustainability management or sustainability performance, companies are recognized for the sustainability impact of their actions [17,18,19]. The need for information from stakeholders, such as governments, communities where companies have operation centers, and processing plants, progressively expands the amount and types of information required to be disclosed [4,20,21]. This situation has led accountants, both practitioners and academics, to broaden their perspective on accounting and accountability, allowing them to develop the necessary skills and competencies to inform society about the sustainability impact of companies or organizations, linking sustainability with accounting [22]. Accountability systems provide an opportunity to demonstrate the results of the social commitment expressed in the missions and visions of organizations, as well as the effective delivery of goods and services aimed at meeting community needs [23]. In fact, accounting should tend to the search for a representation and measurement instrument of all patrimonial elements (an accountability system), as one of its main objectives is to conceptualize and measure the corporate social responsibility phenomenon [24].

In addition, accounting can help to achieve the sustainability development goals [25,26,27]. In this context, sustainability accounting emerges, dealing with the processing of business transactions. It considers economic, environmental, and social factors to safeguard business assets and protect the interests of society [28,29,30].

2.2. Sustainability Reporting and Accounting Reporting

A sustainability report completes the process by disclosing an organization’s sustainability performance (economic, environmental, and social performances) [31]. Although sustainability accounting and sustainability reporting are two distinct terms, together, they act as an accountability tool for a company’s sustainability production and operations [32], including corporate communication on a company’s performance in biodiversity, climate change, and human rights issues [33].

The sustainability accounting concept involves the treatment of business transactions performed by companies (considering economic, environmental, and social factors), the disclosure of the results through sustainability reports [34], the provision of adequate information on sustainability corporate performance to society [35], and the process of communicating an organization’s effects on internal and external users through financial and non-financial reporting. This concept recognizes the responsibility of organizations to provide financial information to shareholders about the impact of its non-financial activity (e.g., information concerning energy efficiency, waste management, wastewater, chemicals and waste metals, employment, occupational health and safety, human talent training, community and volunteerism, supply chain, quality control, regulation and compliance) in the triple bottom line framework [36].

3. Methods

To respond to the objective of the metasynthesis review, the following protocols were adhered to: (1) adopting a critical attitude toward the current state of the academic literature, (2) articulating and comparing theories, (3) analyzing the strengths and weaknesses contributed by publications to interpret pre-existing knowledge [37,38,39,40,41], (4) managing to facilitate a comprehensive understanding of qualitative findings through synthesis, but without testing a hypothesis or exploring the dependencies between variables in a model, and (5) developing more precise knowledge, allowing for a deeper and broader understanding than that presented in individual studies [42,43,44,45].

Therefore, seven items relevant to meta-analytic reviews and not metasynthesis reviews were excluded from the PRISMA statement, namely, 5 (protocol and registry), 12 (risk of bias in individual studies), 13 (summary measures), 14 (result synthesis), 15 and 22 (risk of bias between studies), and 19 (risk of bias in studies). Thus, this review was developed according to the PRISMA statement standards, following the quality steps for systematic reviews and considering the following items: 1 (title), 2 (structured abstract), 3 (rationale), 4 (objective), 6 (eligibility criteria), 7 (information sources), 8 (search), 9 (study selection), 10 (data extraction process), 11 (data list), 16 (additional analyses), 17 (study selection), 18 (study characteristics), 20 (individual study results), 21 (result synthesis), 23 (additional analyses), 24 (evidence summary), 25 (limitations), 26 (conclusions), and 27 (funding) [46,47].

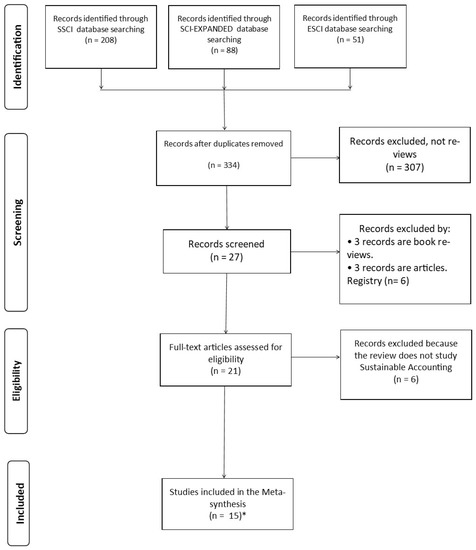

The information was approached inductively, that is, without predefined analysis categories, except for that included in the sustainability accounting conceptualization. We have focused only on the WoS journal indexing database, and have avoided adding information from other databases that are not comparable in terms of citations, since several studies point out that the results of systematic literature reviews may vary according to the database used [48,49,50,51,52] given the different criteria that exist for calculating the impact factor of journals [51,52]. Specifically, the search was conducted on 18 January 2022. The search term used was “sustainability accounting”, using topic field tags (TS, including title, abstract, author keywords, and keywords plus®) and the proximity search operator with word spacing equal to zero (NEAR/0), ensuring an in-depth search for the concept {TS = (Sustainability NEAR/0 Accounting)}, resulting in 334 records in the identification phase. In the check phase, 307 records were excluded because they were not reviews. Similarly, 3 records were excluded because they were not article reviews but book reviews, and 3 records were excluded because they were classified as reviews but were articles. Continuing with the checking phase, 4 reviews were excluded because they only addressed sustainability and not sustainability accounting, and 1 review was excluded because it addressed the national public current account from the payment balance. Finally, 1 review was excluded for addressing family accounting from management accounting. Finally, the PRISMA structure includes 2 reviews related to sustainability accounting in the public sector.

From the 334 records initially retrieved, 15 reviews were included (see Figure 1), conducted between the years 2017 and 2021. All articles selected for this review were published in English.

Figure 1.

Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA). * Registration includes 2 reviews of sustainability accounting in the public sector.

To extract data from the selected reviews and answer the research question “What is the current and future development of studies in the area of sustainability accounting?”, two processes were developed:

- A template design, where the information revealed in each article review was characterized in the form of a finding.

- Each article was read by three researchers participating in this study, who selected the significant topics. The reading began with an analysis of the summaries, using the PICOS framework: problem or topic of interest (P), intervention (I), comparison (C), outcome (O), and study designs (S) [53,54,55]. The criteria applied in this study were as follows: P = sustainability accounting, I = current study development and the future of sustainability accounting, C = non-comparator, O = re-interpretation of the findings, and S = systematic reviews where sustainability accounting or sustainability reporting is developed. A complete analysis of the reviews was conducted using the IMYRD structure: I = introduction; M = methods; R = results, and D = discussion of the reviews [56]. We analyzed the (1) title, (2) objective, (3) method, (4) theories, (5) results, and (6) future research directions.

Finally, the metasynthesis focused on examining 15 selected article reviews in order to develop an understanding of the current development of studies and the future of sustainability accounting. It was necessary to identify the related topics and categories presented by the authors. Each of these was then identified based on the theoretical meanings attributed to them by the main reference authors.

4. Results

4.1. Metasynthesis of Review Articles

The fifteen articles that met the eligibility criteria were reviewed at the full-text level to determine precisely whether their characteristics offered homogeneous criteria (sustainability accounting and sustainability reporting), which would make them comparable (Appendix A). Table 1 shows the main identification and retrieval information obtained from the WoS database.

Table 1.

Articles included in the metasynthesis.

The first analytical approximation in relation to the 15 reviews that were part of the present study is the number of articles published in the sustainability accounting area and all their associated terms. The number of terms has increased significantly in the academic world [1,22,28,57]. The fifteen review articles analyzed were published from 2017 to 2021. However, when examining the publications that were used as primary sources in these fifteen reviews, there was one document from 1964 [54], and this is the oldest indirect document involved in our review. Furthermore, the countries with publications related to the study topic are as follows: the United Kingdom, which leads the list, followed by the USA, Australia, Germany, Italy, and Spain [22].

Table 2 shows that the journals in which these articles were published are Sustainability (6), Journal of Cleaner Production (2), Accounting Auditing & Accountability Journal (1), Australian Accounting Review (1), Journal of Accounting and Organizational Change (1), Journal of Environmental Management (1), Pacific Accounting Review (1), Quality-Access to Success (1), and Sustainability Accounting Management and Policy Journal (1). A high concentration of articles was indexed in the following Web of Science categories: Environmental Sciences and Green Sustainability Science Technology (9), Environmental Sciences (9), Environmental Studies (7), Business Finance (5), and Engineering Environmental (2). The most frequently cited reviews are (citations in parentheses) those conducted by Onat et al. [14] (112), Buyukozkan and Karabulut [60] (73), and Farooq and Villiers [5] (39).

Table 2.

Primary sources in the systematic reviews studied.

Another result that stands out in this review is that, among the 15 reviews under study, 2 reviews were focused on sustainability accounting in the public sector [61,63]. In terms of the research methods, systematic literature reviews, structured literature reviews, systematic literature reviews [1,4,7,14,55,57,58,59,64], bibliometric analyses [22], textual mining analyses [61], content analyses [63], or discourse analyses [28] were used.

The primary sources used by the authors of the 15 reviews (case studies) are listed in Table 2.

In relation to the keywords, the research reveals the diversity of the terms or synonyms used by researchers to refer to the sustainability accounting topic, resulting in 22 keywords related to the topic, with few repeated words, as detailed in Table 3 below.

Table 3.

Keyword relationships.

These articles present a variety of synonyms used by researchers in relation to the topic; the analysis categories identified are discussed below.

4.2. Sustainability Accounting Concept Interpretation

Sustainability accounting, or sustainability reporting, involves the treatment of business transactions, considering economic, environmental, and social factors in order to protect the interests of society, with subsequent disclosure in non-financial reports or sustainability reports [1,7,22,28].

In order to address the challenges related to sustainability accounting, it is essential to develop a common language to harmonize tools and methods [14], given that the boundaries of sustainability accounting research are not firmly defined [57]. Different terms, such as sustainability accounting, environmental accounting [7], sustainability reporting [1], non-financial reporting [22], social performance, social disclosure, and accountability [61], are recognized. Some scientific productions relate sustainability accounting to sustainability development, sustainability practices, and the sustainability development goals (SDGs). Since 1976, accounting academics have been engaged in debates, and these debates are behind the creation of the SDGs and their implementation [65].

According to Hopper [25], the important areas discussed are accountability for human rights, climate change mitigation, ensuring decent work, increasing accountability, democratic civil society participation, and greater and more equal partnership with stakeholders and developing countries in order to address their needs. Corporate sustainability strategies require organizations to make consistent decisions that bring their values in line with the sustainability development goals through the efficient allocation of their resources, such as people, land, equipment, and financial assets [66]. This situation has had results, as SDG 13 (Climate action) is one of the most analyzed sustainability development goals in the academic literature in relation to sustainability accounting, as well as SDGs 5 (Gender equality), 6 (Clean water and sanitation), 14 (Life below water), and 15 (Life on land) [67], which are related to accounting and human rights. However, in scientific research, less attention has been devoted to auditing, governance, strategic management control, and performance measurement, which are elements directly related to the triple bottom line in organizations [35,62].

Most sustainability development initiatives tend to focus on environmental and social aspects, although Ascani et al. [1] propose seven categories coinciding with the Brundtland Report [68] around the sustainability definition: three simple categories (environmental, social, and economic), three paired categories (environmental–social, environmental–economic, and social–economic), and one category that intersects them all (environmental–social–economic), with the latter being the category most used in studies to define sustainability. To understand the evolution of these categories, the sustainability accounting subdivisions are discussed below.

4.3. Sustainability Accounting Subdivisions

The findings allowed for the identification of the following subdivisions, which integrate sustainability accounting at present:

Environmental management accounting: This addresses concerns about the impact that organizations have on environmental issues [57]. It highlights water accounting, accounting, auditing, and carbon reporting [28]. In this type of accounting, information on the costs and benefits of mitigation strategies, such as emission reductions involving energy savings, is recorded [4]. In this regard, there is the Sustainability Accounting of Emission Reduction Credit, which presents confusions in the accounting of carbon emission reduction credits both in theory and in practice because of the lack of standardization [28]. Environmental management accounting is referred to as environmental accounting, which is itself a synonym for ecological accounting, although this term is distinct and does not cover many of the ecological challenges [7]. Another subdivision is defined as green accounting, which is analogous to conventional accounting, differing in the price estimations of goods and services using cost/benefit techniques instead of direct observations [69,70]. All of this is within the sustainability consumption framework, which recognizes a relationship between global climate change and the reduction of human impact on the environment [71].

Social accounting: This is related to economic inequality. It has action strategies, which describe the production process, the distribution, and the use of goods and services within a society [4]. It has its origin in sociology and allows for an understanding of corporate behaviors and decision-making processes in organizations [72]. Social accounting includes social responsibility accounting; total impact accounting; socioeconomic accounting; social indicator accounting; and public accounting [22]. In public accounting or national accounting, it measures macroeconomic phenomena through the description of supply and demand, considering statistical–analytical derivations. Its types and social categories and the results of its actions are highlighted [73].

4.4. Sustainability Accounting in Accountant Education

The theoretical and practical implications in the research conducted by Gulluscio et al. [4] unveil the need for an in-depth intervention by accounting practitioners and academics in sustainability accounting and its respective sustainability reports. Accountants and managers should be taught the importance of sustainability for both the profession and society at large [23]. Cho et al. [74] found that an appropriate approach that can be used to integrate sustainability development premises into accounting education is to include the topics as programmatic content in the specialty subject curricula.

4.5. Sustainability Reports

Sustainability reports, or integrated reports of financial and non-financial information, and corporate sustainability reports originate from the management attempts in favor of corporate social responsibility practices [60] since the 1970s. In 1997, the Global Reporting Initiative (GRI) was introduced with the aim of improving the quality, rigor, and usefulness of sustainability reporting. GRI provided certified tools in order to contribute to data collection and report preparation [4,6,75]. The United Nations Environment Programme (UNEP) and the non-governmental organization the Coalition for Environmentally Responsible Economies (CERES) are responsible for this initiative, which discloses information on companies or organizations related to emissions, economics, market, indirect economic impact and procurement, energy, employment, and compliance [28]. The International Financial Reporting Standards (IFRS) on sustainability reporting include risk assessments and the risk management of financial and non-financial issues in conjunction with stakeholder relations to address inclusive measures and mechanisms in order to assess decision making [46].

The International Integrated Reporting Council (IIRC) is responsible for integrated reporting (IR), a report aimed primarily at investors, focusing on internal management [6]. Its purpose is to present a close link between the financial performance of a company or organization and the economic, environmental, and social contexts in which it operates through clearly written, understandable, and accessible information [76]. The Sustainability Accounting Standards Board (SASB), which is responsible for corporate reporting on environmental, social, and governance (ESG) issues, helps companies to create long-term value [77]. Finally, the Sustainability Stock Exchange (SSE) initiative is presented [78].

The credibility of sustainability reporting is obtained through sustainability assurance [79]. In their research, Farooq and De Villiers [5] explain that there are factors that drive sustainability assurance, highlighting among them organization size; media pressure; and, from the internal side, financial indicators with mixed results. However, the authors highlight some inhibiting factors for sustainability assurance, such as the high cost, no added value, the lack of external regulatory pressure, and the increased exposure to litigation. An additional element that contributes to the determination of the credibility of sustainability reports is materiality [6], which aims to enhance the relevance of sustainability reports for stakeholders [80]. Materiality is important because companies have the duty to identify, prioritize, and disclose information [81] related to the transactions that they consider material. Finally, there is the Sustainability Performance Assessment, a tool based on performance indicators that demonstrate the economic, social, and environmental results of an organization [64].

4.6. The Future of Sustainability Accounting

Future studies should discuss the value of generally applicable theories and include problem-focused research. Some cases are carbon accounting, water accounting, and human rights accounting [57]. This type of review contributes directly to environmental and social accounting and could even support and encourage the creation of an independent ecological accounting field [7], providing research on a management accounting system to improve sustainability in productive sectors that depend on changes in ecosystems and the natural environment [58].

Prospects for future research are related to the need for the further study of all theoretical and practical aspects of sustainability reporting, determining the composition of financial and non-financial indicators to be disclosed, and the justification of the methods to be used in order to determine individual indicators and costing [22]. According to Gulluscio et al. [4], attention should be paid to the concrete effects produced by practices related to the sustainability performance of companies, linking the importance of understanding sustainability reports and their impacts to management and policy issues [62]. In sustainability assurance, studies that investigate sustainability engagement from the initial phase through to the disclosure of an assurance statement are needed [5].

Regarding sustainability reporting, research has been proposed on GRI-SASB (2021), a joint project whose purpose is to explain the similarities and differences in reporting based on GRI and SASB standards, as well as research about the criteria governing regulatory agencies in relation to the effective control of environmental accounting and sustainability reports [28].

Finally, another direction for future research is sustainability accounting in the public sector. This recommendation is in the framework of the research conducted by Tommasetti et al. [61] in which there was little evidence of a relationship between the co-creation of public value and sustainability accounting practices.

5. Discussion

The present systematic review analyzes the concept of sustainability accounting through previous studies, with the aims of (1) understanding this topic in the academic literature without focusing on a specific target, such as the previous contributions of the role of management accounting to accounting or sustainability reporting [1], and (2) presenting the current status and suggestions for future research, e.g., that on climate action (SDG 13) [4] or on the market for sustainability assurance (SA) services [5]. The analyzed publications allow for the study of the common aspects among the mentioned reviews (e.g., interpretation of the concept of sustainability accounting and sustainability reporting), as not all topics evaluated in the articles on sustainability accounting are determinant [61], which is due to the lack of clear and uniform guidelines grouping the work of companies or organizations in the field of sustainability development.

Regarding the interpretation of the concept of sustainability accounting at present, the review articles analyzed above define it as the treatment of business transactions, considering economic, environmental, and social factors, with subsequent disclosure in non-financial reports or sustainability reports [1,28]; this information is presented in the publications of the countries in the United Kingdom, followed by the United States, Australia, Germany, Italy, and Spain [22]. This result agrees with the results found by Ascani et al. [1], who point out that, in Europe, countries such as France, Spain, Germany, and the United Kingdom are the most explored geographical areas in the field of sustainability accounting. However, they point out that China and the United States contribute little to this field of research in relation to the high environmental and social impacts of their economies. Brazil, Indonesia, and Poland, as countries where sustainability-related issues are disclosed, make up a smaller proportion [57].

This review introduces the premise of the existence of a single type of sustainability accounting, which, in turn, addresses different subdivisions related to the activities carried out by companies, such as social and environmental accounting. Thus, it is not correct to speak of environmental accounting [57], water accounting, and carbon accounting [28], as sustainability accounting revolves around ambiguous terms of sustainability [7].

The same situation occurs with so-called social accounting [22]. In fact, it is sustainability accounting that, in a standardized and predictable way, records the calculations of the social value provided to different stakeholders and to society in general and, consequently, maximizes the total value created [62]. Social accounting allows, through a standardized and scientifically based process, for the identification and the analysis of the needs and perceptions of stakeholders, generating social sustainability indicators for organizations [63,73].

Sustainability reports were also addressed in our review, and, according to Martínez-Ferrero, J, et al. [79], the credibility of sustainability reports is obtained through sustainability assurance. However, criticisms about the ability of these reports to promote sustainability development within organizations and to make their sustainability performance more accountable and transparent are evident [82]. The present study contributes to this field of research by showing that, to date, the organizations in charge of the quality, rigor, and usefulness of sustainability reports are in charge of the GRI-SASB project, whose objective is to explain the similarities and differences in the reports presented based on GRI and SASB standards. This project will allow for the unification of criteria when presenting sustainability reports generated by sustainability accounting.

6. Conclusions

This review article, in an effort to analyze the sustainability accounting concept used in previous studies, based on articles published in journals indexed in WoS, in a review process adjusted to the PRISMA protocol, distinguishes a set of fifteen articles, approximately 4.5% of the original records identified, as shown in Figure 1.

The research methods used in the 15 reviews analyzed (see Table 1) allowed for a broad coverage of the criteria (sustainability accounting and sustainability reporting), identifying a variety of synonyms used by researchers in relation to the topic.

The results obtained permitted the interpretation of the sustainability accounting concept and sustainability reporting, subdividing accounting into environmental and social accounting. Likewise, when analyzing the 15 systematic reviews, the importance of accountants and company managers in financial reporting, which incorporates non-financial information or sustainability reports, is highlighted, thus demonstrating the economic, social, and environmental impacts that companies or organizations have on society.

As for the limitations, these are determined by the selection of the original review articles, which was limited to the WoS JCR indexes (SSCI, SCI-EXPANDED, and ESCI); the selection was made with the purpose of reviewing reviews with a high level of scientific rigor, guaranteeing that the theoretical construction identified contributes to providing a reliable understanding of sustainability accounting and reporting.

Finally, for future research directions, the proposals made by the authors of the systematic reviews are recognized. Among them, the concrete effects produced by the practices related to the corporate sustainability performance are highlighted, linking the importance of understanding sustainability reports to the sustainability performance of companies.

Author Contributions

Conceptualization, M.G.-M. and A.V.-M.; methodology, M.G.-M. and A.V.-M.; validation, S.V.-R.; formal analysis, A.V.-M. and N.C.-B.; writing—original draft preparation, A.V.-M., G.S.-S., and M.G.-M.; writing—review and editing, A.V.-M., G.S.-S., and N.C.-B.; supervision, S.V.-R., and A.V.L.; project administration, A.V.-M.; funding acquisition, N.C.-B., G.S.-S. and A.V.-M. All authors have read and agreed to the published version of the manuscript.

Funding

The article processing charge (APC) was partially funded by Universidad Católica de la Santísima Concepción (Code: APC2022) and was partially funded by Universidad Andres Bello (Code: APC2022). Additionally, the publication fee (APC) was partially financed by Universidad Autónoma de Chile through the publication incentive fund 2022 (Code: C.C. 456001).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors would like to thank the Postdoctoral Program in Psychology with Orientation in Research Methodology at the University of Flores, Argentina. The authors would also like to thank the program where Miseldra Gil-Marín is pursuing his postdoctoral fellowship with the research line sustainability accounting under the direction of Analia Verónica Losada.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

The Appendix shows the digital object identifiers (DOIs) for the fifteen articles selected for metasynthesis: DO = ((10.47750/QAS/22.185.14 OR 10.3390/su13042357 OR 10.1108/AAAJ-03-2018-3399 OR 10.1016/j.jclepro.2017.11.217 OR 10.3390/su12051909 OR 10.3390/su12135455 OR 10.1111/auar.12197 OR 10.1108/SAMPJ-01-2018-0017 OR 10.3390/su13020763 OR 10.1108/PAR-10-2016-0093 OR 10.1016/j.jclepro.2020.125330 OR 10.3390/su12218854 OR 10.1108/JAOC-05-2018-0044 OR 10.3390/su9050706 OR 10.1016/j.jenvman.2018.03.064)).

References

- Ascani, I.; Ciccola, R.; Chiucchi, M.S. A Structured Literature Review about the Role of Management Accountants in Sustainability Accounting and Reporting. Sustainability 2021, 13, 2357. [Google Scholar] [CrossRef]

- Widyawati, L.A. Systematic literature review of socially responsible investment and environmental social governance metrics. Bus. Strategy Environ. 2020, 29, 619–637. [Google Scholar] [CrossRef]

- Onwuka, I.O.; Okoro, B.C.; Onodugo, V.A. Measuring corporate governance performance beyond the financial metrics: A study based on deposit money banks in Nigeria. Bus. Strategy Dev. 2020, 2, 332–348. [Google Scholar] [CrossRef]

- Gulluscio, C.; Puntillo, P.; Luciani, V.; Huisingh, D. Climate Change Accounting and Reporting: A Systematic Literature Review. Sustainability 2020, 12, 5455. [Google Scholar] [CrossRef]

- Farooq, M.B.; de Villiers, C. The market for sustainability assurance services A comprehensive literature review and future avenues for research. Pac. Account. Rev. 2017, 29, 79–106. [Google Scholar] [CrossRef] [Green Version]

- Wu, S.R.; Shao, C.L.; Chen, J.Q. Approaches on the Screening Methods for Materiality in Sustainability Reporting. Sustainability 2018, 10, 3233. [Google Scholar] [CrossRef] [Green Version]

- Kelsall, C.A. Ecological Management Accounting-Taking into Account Sustainability, Does Accounting Have Far to Travel? Sustainability 2020, 12, 8854. [Google Scholar] [CrossRef]

- Ba, Y.H. Power Dynamics and Corporate Power in Governance Processes: Evidence from US Environmental Governance Systems. Amer. Rev. Public Adm. 2021, 52, 206–220. [Google Scholar] [CrossRef]

- Ballou, B.; Casey, R.J.; Grenier, J.H.; Heitger, D.L. Exploring the Strategic Integration of Sustainability Initiatives: Opportunities for Accounting Research. Account. Horiz. 2012, 26, 265–288. [Google Scholar] [CrossRef]

- Van Liempd, D.; Busch, J. Biodiversity reporting in Denmark. Account. Audit. Account. J. 2013, 26, 833–872. [Google Scholar] [CrossRef]

- Aguiar, A.P.D.; Collste, D.; Harmackova, Z.V.; Pereira, L.; Selomane, O.; Galafassi, D.; Van Vuuren, D.; Van Der Leeuw, S. Co-designing global target-seeking scenarios: A cross-scale participatory process for capturing multiple perspectives on pathways to sustainability. Glob. Environ. Chang. 2020, 65, 102198. [Google Scholar] [CrossRef]

- Santa-Maria, T.; Vermeulen, W.J.V.; Baumgartner, R.J. How do incumbent firms innovate their business models for the circular economy? Identifying micro-foundations of dynamic capabilities. Bus. Strategy Environ. 2021, 31, 1308–1333. [Google Scholar] [CrossRef]

- Johnson, M.P. Knowledge acquisition and development in sustainability-oriented small and medium-sized enterprises: Exploring the practices, capabilities and cooperation. J. Clean. Prod. 2017, 142, 3769–3781. [Google Scholar] [CrossRef]

- Onat, N.C.; Kucukvar, M.; Halog, A.; Cloutier, S. Systems Thinking for Life Cycle Sustainability Assessment: A Review of Recent Developments, Applications, and Future Perspectives. Sustainability 2017, 9, 706. [Google Scholar] [CrossRef] [Green Version]

- Liu, B.S.; Wang, T.; Zhang, J.M.; Wang, X.M.; Chang, Y.; Fang, D.P.; Yang, M.J.; Sun, X.Z. Sustained sustainability development actions of China from 1986 to 2020. Sci. Rep. 2021, 11, 8008. [Google Scholar] [CrossRef]

- Kluza, K.; Bak, I.; Ziolo, M.; Spoz, A. Achieving Environmental Policy Objectives through the Implementation of Sustainability Development Goals. The Case for European Union Countries. Energies 2021, 14, 2129. [Google Scholar] [CrossRef]

- Franco, A.E. Reference framework for the integration of social accounting in the strategic management of social economy enterprises. CIRIEC-ESPANA J. Soc. Coop. Public Econ. 2020, 100, 207–237. [Google Scholar] [CrossRef]

- Hernandez, I.M.D.; de Paula, L.B. Scientific mapping on the convergence of innovation and sustainability (innovability): 1990–2018. Kybernetes 2020, 50, 2917–2942. [Google Scholar] [CrossRef]

- Kang, X.Y.; Wang, M.X.; Lin, J.; Li, X. Trends and status in resources security, ecological stability, and sustainability development research: A systematic analysis. Environ. Sci. Pollut. Res. 2022, 29, 50192–50207. [Google Scholar] [CrossRef]

- Tettamanzi, P.; Venturini, G.Y.; Murgolo, M. Sustainability and Financial Accounting: A Critical Review on the ESG Dynamics. Environ. Sci. Pollut. Res. 2022, 29, 16758–16761. [Google Scholar] [CrossRef]

- Ogrean, C. The directive 2014/95/eu—Is there a “new” beginning for csr in romania? Stud. Bus. Econ. 2017, 12, 141–147. [Google Scholar] [CrossRef] [Green Version]

- Vysochan, O.; Hyk, V.; Vysochan, O.; Olshanska, M. Sustainability Accounting: A Systematic Literature Review and Bibliometric Analysis. Qual. Access Success. 2021, 22, 95–102. [Google Scholar] [CrossRef]

- Ebaid, I.E.S. Sustainability and accounting education: Perspectives of undergraduate accounting students in Saudi Arabia. J. Appl. Res. High. Educ. 2021; ahead-of-print. [Google Scholar] [CrossRef]

- Eugenio, T.; Carreira, P.; Miettinen, N.; Lourenço, I.M.E.C. Understanding students’ future intention to engage in sustainability accounting: The case of Malaysia and the Philippines. J. Account. Emerg. Econ. 2021, 12, 695–715. [Google Scholar] [CrossRef]

- Hopper, T. Stop accounting myopia: -think globally: A polemic. J. Account. Organ. Chang. 2019, 15, 87–99. [Google Scholar] [CrossRef]

- Niles, K.; Moore, W. Accounting for environmental assets as sovereign wealth funds. J. Sustain. Financ. Invest. 2021, 11, 62–81. [Google Scholar] [CrossRef]

- Di Vaio, A.; Hasan, S.; Hassan, R.; Palladino, R. The transition towards circular economy and waste within accounting and accountability models: A systematic literature review and conceptual framework. Environ. Dev. Sustain. 2022; ahead-of-print. [Google Scholar] [CrossRef]

- Imoniana, J.O.; Soares, R.R.; Domingos, L.C. A review of sustainability accounting for emission reduction credit and compliance with emission rules in Brazil: A discourse analysis. J. Clean. Prod. 2018, 172, 2045–2057. [Google Scholar] [CrossRef]

- Gadinis, S.; Miazad, A. Corporate Law and Social Risk. Vanderbilt Law Rev. 2020, 73, 1401–1477. [Google Scholar]

- Tooranloo, H.S.; Shahamabad, M.A. Designing the model of factors affecting in the implementation of social and environmental accounting with the ISM approach. Int. J. Ethics Syst. 2020, 36, 387–410. [Google Scholar] [CrossRef]

- Demir, M.; Min, M. Consistencies and discrepancies in corporate social responsibility reporting in the pharmaceutical industry. Sustain. Account. Manag. Policy J. 2019, 10, 333–364. [Google Scholar] [CrossRef]

- Macellari, M.; Yuriev, A.; Testa, F.; Boiral, O. Exploring bluewashing practices of alleged sustainability leaders through a counter-accounting analysis. Environ. Impact Assess. Rev. 2021, 86, 106489. [Google Scholar] [CrossRef]

- Adhariani, D.; Roof, E. Readability ofsustainability reports: Evidence from Indonesia. J. Account. Emerg. Econ. 2020, 10, 621–636. [Google Scholar] [CrossRef]

- Cantele, S.; Tsalis, T.A.; Nikolaou, I.E. A New Framework for Assessing theSustainabilityReporting Disclosure of Water Utilities. Sustainability 2018, 10, 433. [Google Scholar] [CrossRef] [Green Version]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainability operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Geerts, M.; Dooms, M. Sustainability Reporting for Inland Port Managing Bodies: A Stakeholder-Based View on Materiality. Sustainability 2020, 12, 1726. [Google Scholar] [CrossRef] [Green Version]

- Sandelowski, M.; Docherty, S.; Emden, C. Qualitative metasynthesis: Issues and techniques. Res. Nurs. Health 2007, 20, 365–371. [Google Scholar] [CrossRef]

- Finfgeld, D.L. Metasynthesis: The State of the Art—So Far. Qual. Health Res. 2003, 13, 893–904. [Google Scholar] [CrossRef]

- Bondas, T.; Hall, E.O.C. A decade of metasynthesis research in health sciences: A meta-method study. Int. J. Qual. Stud. Health Well-Being 2009, 2, 101–113. [Google Scholar] [CrossRef] [Green Version]

- Walsh, D.; Downe, S. Meta-synthesis method for qualitative research: A literature review. J. Adv. Nurs. 2005, 50, 204–211. [Google Scholar] [CrossRef]

- Leary, H.; Walker, A. Meta-Analysis and Meta-Synthesis Methodologies: Rigorously Piecing Together Research. Techtrends 2018, 62, 525–534. [Google Scholar] [CrossRef]

- Oesterreich, T.D.; Teuteberg, F. Behind the scenes: Understanding the socio-technical barriers to BIM adoption through the theoretical lens of information systems research. Teechnol. Forecast. Soc. Chang. 2019, 146, 413–431. [Google Scholar] [CrossRef]

- Zimmer, L. Qualitative meta-synthesis: A question of dialoguing with texts. J. Adv. Nurs. 2006, 53, 311–318. [Google Scholar] [CrossRef] [PubMed]

- Bondas, T.; Hall, E.O.C. Challenges in Approaching Metasynthesis Research. Qual. Health Res. 2007, 17, 113–121. [Google Scholar] [CrossRef] [PubMed]

- Jensen, L.A.; Allen, M.N. Meta-synthesis of qualitative findings. Qual. Health Res. 1996, 6, 553–560. [Google Scholar] [CrossRef]

- Urrutia, G.; Bonfill, X. PRISMA declaration: A proposal to improve the publication of systematic reviews and meta-analyses. Med. Clin. 2010, 135, 507–511. [Google Scholar] [CrossRef]

- Page, M.J.; McKenzie, J.E.; Bossuyt, P.M.; Boutron, I.; Hoffmann, T.C.; Mulrow, C.D.; Shamseer, L.; Tetzlaff, J.M.; Akl, E.A.; Brennan, S.E.; et al. The PRISMA 2020 statement: An updated guideline for reporting systematic reviews. Br. Med. J. 2021, 372, 71. [Google Scholar] [CrossRef]

- Mongeon, P.; Paul-Hus, A. The journal coverage of Web of Science and Scopus: A comparative analysis. Scientometrics 2021, 106, 213–228. [Google Scholar] [CrossRef]

- Harzing, A.W.; Alakangas, S. Google Scholar, Scopus and the Web of Science: A longitudinal and cross-disciplinary comparison. Scientometrics 2016, 106, 787–804. [Google Scholar] [CrossRef]

- Falagas, M.E.; Pitsouni, E.I.; Malietzis, G.A.; Pappas, G. Comparison of PubMed, Scopus, web of science, and Google scholar: Strengths and weaknesses. FASEB J. 2008, 22, 338–342. [Google Scholar] [CrossRef] [PubMed]

- Chadegani, A.A.; Salehi, H.; Yunus, M.M.; Farhadi, H.; Fooladi, M.; Farhadi, M.; Ebrahim, N.A. A comparison between two main academic literature collections: Web of Science and Scopus databases. Asian Soc. Sci. 2013, 9, 18–26. [Google Scholar] [CrossRef] [Green Version]

- Bakkalbasi, N.; Bauer, K.; Glover, J.; Wang, L. Three options for citation tracking: Google Scholar, Scopus and Web of Science. Biomed. Digit. Libr. 2006, 3, 7. [Google Scholar] [CrossRef] [Green Version]

- Methley, A.M.; Campbell, S.; Chew-Graham, C.; McNally, R.; Cheraghi-Sohi, S. PICO, PICOS and SPIDER: A comparison study of specificity and sensitivity in three search tools for qualitative systematic reviews. BMC Health Serv. Res. 2014, 14, 579. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Chabou, S.; Iglewski, M. Combination of conditional random field with a rule based method in the extraction of PICO elements. BMC Med. Inform. Decis. Mak. 2018, 18, 128. [Google Scholar] [CrossRef] [PubMed]

- Jin, D.; Szolovits, P. Advancing PICO element detection in biomedical text via deep neural networks. Bioinformatics 2020, 36, 3856–3862. [Google Scholar] [CrossRef]

- Gonzalez, M.; Mattar, S. IMRaD or IMRyD format for scientific articles? Rev. MVZ Cordoba 2010, 15, 1895–1896. [Google Scholar]

- Adams, C.A.; Larrinaga, C. Progress: Engaging with organisations in pursuit of improved sustainability accounting and performance. Account. Audit. Account. J. 2019, 32, 2367–2394. [Google Scholar] [CrossRef] [Green Version]

- Ndemewah, S.R.; Menges, K.; Hiebl, M.R.W. Management accounting research on farms: What is known and what needs knowing? J. Account. Organ. 2019, 15, 58–86. [Google Scholar] [CrossRef] [Green Version]

- Trautwein, C. Sustainability impact assessment of start-ups—Key insights on relevant assessment challenges and approaches based on an inclusive, systematic literature review. J. Clean. Prod. 2021, 281, 125330. [Google Scholar] [CrossRef]

- Fiandrino, S.; Tonelli, A. A Text-Mining Analysis on the Review of the Non-Financial Reporting Directive: Bringing Value Creation for Stakeholders into Accounting. Sustainability 2021, 13, 763. [Google Scholar] [CrossRef]

- Tommasetti, A.; Mussari, R.; Maione, G.; Sorrentino, D. Sustainability Accounting and Reporting in the Public Sector: Towards Public Value Co-Creation? Sustainability 2020, 12, 1909. [Google Scholar] [CrossRef] [Green Version]

- Patten, D.M.; Shin, H. Sustainability Accounting, Management and Policy Journal’s contributions to corporate social responsibility disclosure research A review and assessment. Sustain. Account. Manag. Policy J. 2019, 10, 26–40. [Google Scholar] [CrossRef]

- Sharma, U.; An, Y. Accounting and Accountability in Fiji: A Review and Synthesis. Aust. Account. Rev. 2018, 28, 421–427. [Google Scholar] [CrossRef]

- Buyukozkan, G.; Karabulut, Y. Sustainability performance evaluation: Literature review and future directions. J. Environ. Manag. 2018, 217, 253–267. [Google Scholar] [CrossRef]

- Bebbington, J.; Unerman, J. Advancing research into accounting and the UN Sustainability Development Goals. Account. Audit. Account. J. 2020, 33, 1657–1670. [Google Scholar] [CrossRef]

- Zyznarska-Dworczak, B. Sustainability Accounting-Cognitive and Conceptual Approach. Sustainability 2021, 12, 9936. [Google Scholar] [CrossRef]

- Sianes, A.; Vega-Munoz, A.; Tirado-Valencia, P.; Ariza-Montes, A. Impact of the Sustainability Development Goals on the academic research agenda. A scientometric analysis. PLoS ONE 2022, 17, e0265409. [Google Scholar] [CrossRef] [PubMed]

- Picardweyl, M. Ecology and the international community—The brundtland report of the united-nations. Pensee 1990, 274, 21–31. [Google Scholar]

- Thornton, D.B. Green accounting and green eyeshades twenty years later. Crit. Perspect. Account. 2013, 24, 438–442. [Google Scholar] [CrossRef]

- Da Silva, R.J.; Tommasetti, R.; Gomes, M.Z.; Macedo, M.A.D. How green is accounting? Brazilian students’ perception. Int. J. Sustain. High. Educ. 2020, 21, 228–243. [Google Scholar] [CrossRef]

- Howard, L. Sustainability consumption: Key issues. Local Environ. 2019, 24, 310–311. [Google Scholar] [CrossRef]

- Al Mahameed, M.; Belal, A.; Gebreiter, F.; Lowe, A. Social accounting in the context of profound political, social and economic crisis: The case of the Arab Spring. Account. Audit. Account. J. 2020, 34, 1080–1108. [Google Scholar] [CrossRef]

- Moya, M.A.; Rivera, R.P. Social Accounting Model for Mexico Based on Institutional Sector Accounts. Gest. Politica Publica 2021, 30, 61–99. [Google Scholar] [CrossRef]

- Cho, C.H.; Kim, A.; Rodrigue, M.; Schneider, T. Towards a better understanding of sustainability accounting and management research and teaching in North America: A look at the community. Sustain. Account. Manag. Policy J. 2020, 11, 985–1007. [Google Scholar] [CrossRef]

- Bektur, C.; Arzova, S.B. The effect of women managers in the board of directors of companies on the integrated reporting: Example of Istanbul Stock Exchange (ISE) Sustainability Index. J. Sustain. Financ. Invest. 2020, 12, 638–654. [Google Scholar] [CrossRef]

- Stone, G.W.; Lodhia, S. Readability of integrated reports: An exploratory global study. Account. Audit. Account. J. 2019, 32, 1532–1557. [Google Scholar] [CrossRef]

- Busco, C.; Consolandi, C.; Eccles, R.G.; Sofra, E. A Preliminary Analysis of SASB Reporting: Disclosure Topics, Financial Relevance, and the Financial Intensity of ESG Materiality. J. Appl. Corp. Financ. 2020, 32, 117–125. [Google Scholar] [CrossRef]

- Iamandi, I.E.; Constantin, L.G.; Munteanu, S.M.; Cernat-Gruici, B. Profiling the Sustainability of Stock Exchanges at Global Level Through an Optimal Scaling Process by Applying Catpca. Econ. Comput. Econ. Cybern. Stud. 2020, 54, 297–313. [Google Scholar] [CrossRef]

- Martinez-Ferrero, J.; Garcia-Sanchez, I.M.; Ruiz-Barbadillo, E. The quality of sustainability assurance reports: The expertise and experience of assurance providers as determinants. Bus. Strategy Environ. 2019, 27, 1181–1196. [Google Scholar] [CrossRef]

- Slacik, J.; Greiling, D. Compliance with materiality in G4-sustainability reports by electric utilities. Int. J. Energy Sect. Manag. 2020, 14, 583–608. [Google Scholar] [CrossRef]

- Jorgensen, S.; Mjos, A.; Pedersen, L.J.T. Sustainability reporting and approaches to materiality: Tensions and potential resolutions. Sustain. Account. Manag. Policy J. 2021, 13, 341–361. [Google Scholar] [CrossRef]

- Journeault, M.; Levant, Y.; Picard, C.F. Sustainability performance reporting: A technocratic shadowing and silencing. Crit. Perspect. Account. 2021, 74, 102145. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).