Abstract

We study the effect of the COVID-19 pandemic on the groundnut value chain and all the actors involved in its value chain in Ananthapuramu district of Andhra Pradesh, a leading groundnut producing state in south India. The results revealed that the COVID-19 pandemic created a double burden on farmers by disrupting farm production on one side and decreased diet diversity on the other. Disruption in farm productions resulted in a decline in household income and increased consumer food prices. The effect on farmers snowballed to other actors in the value chain, and all the actors were affected variably. Availability of storage infrastructure would have saved the farmer’s household income to some extent during the pandemic. Supply of diverse nutrient foods through the existing public distribution system, which mostly provides wheat and rice, might have helped tackle the diet diversity issue amongst farmers. Farmer’s collectives were perceived to reduce the negative impact during natural disasters like the COVID-19 pandemic by helping to organise smallholder farmers, minimise transaction costs and increase their bargaining power. In addition, effective farm extension services, including market information, could have benefited farmers during the crisis.

1. Introduction

The COVID-19 pandemic has affected the whole world in an unprecedented way [1,2]. Researchers across disciplines grappled to analyse and understand the severity and complexity of the pandemic on food, nutrition, health and overall livelihoods, specifically in low and middle-income countries [3]. Both livelihoods and lives are at risk from the pandemic, and it has become not only a health crisis but an economic crisis too [4]. In India, the effect of the pandemic has hit the agricultural sector hard; it has disrupted whole agricultural value chains starting from production to final consumer [5]. Lack of transport, market restrictions, labour shortages, inadequate supply of quality inputs, opportunistic behaviour of intermediaries to retain high margins and the fear of infection from the COVID-19 have put enormous strain on India’s food supply [5,6]. Globally supply chains are disrupted especially for firms relying on international markets due to interruption of flights, port activities, and ferry routes [7]. During the second and third quarters of 2020, India’s export shrank significantly to a record low of 60.28%, and import plunged by 58.65% due to COVID-19 pandemic induced disruption in the supply chain [8]. In the same period consumer prices rose significantly [9]. Among small, marginal farmers and farm labourers, the COVID-19 pandemic has created a double impact. On one side, farm operations are delayed, post-harvest losses have increased, cost of production has increased due to increased labour charges and input price which all together resulted in significant decline in the household income [6]. On the other side, there has been an increase of expenditure on food, health, hygiene and other essential services. Even though life is slowly returning to normal, the impact of COVID-19 reverberates across sectors including Agriculture.

The purpose of our study was to assess the impact of COVID-19 pandemic through a case study of Anantha Samruddhi project beneficiaries. This project is implemented by Accion Fraterna Ecology Centre (AFEC), an NGO based in Ananthapuramu and International Crops Research Institute for the Semi-Arid Tropics (ICRISAT), an international non-profit organisation that undertakes scientific research for development with funding from Walmart Foundation, an NGO based in the United States. Our study particularly looks at the impact on farm livelihood, crop production, agri-input supply, marketing, and overall food environment. Groundnut is one of the major crops grown in the project area and this study examines the impact across the groundnut value chain. Most assessment on the impact of COVID-19 has been at generic and macro level. Thus, there exists an information/literature gap at microlevel. This study proposes to fill this gap by generating evidence at microlevel assessing impact of COVID-19 on different nodes of the groundnut value chain.

In Section 2, we present a discussion on the context of our study and the methods used for data collection and analysis. In Section 3, we provide groundnut value chain mapping developed from a scoping study and introduce the various value chain actors and elaborate their role. In Section 4, we present our results. In Section 5, Section 6 and Section 7 we present the impact of COVID-19 on input dealers, village-level brokers, and primary processors, respectively. In Section 8 we offer a few concluding observations.

2. Materials and Methods

2.1. Study Setting

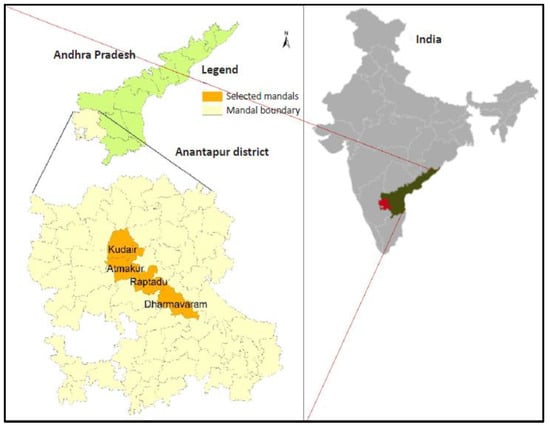

This study is part of a larger development research project being implemented by AFEC and ICRISAT with grant support from Walmart Foundation. The project aims to make dryland agriculture a profitable venture by addressing some of the critical challenges in the ecosystem such as vulnerability to natural and market shocks, lack of access to formal market supply chains and post-harvest losses. The project has introduced crop-specific value-chain development interventions to improve farm-based income and the overall livelihood of the communities. The survey was carried out in select administrative blocks (mandals) of Ananthapuramu district in Andhra Pradesh state of India. Ananthapuramu is an arid region prone to back-to-back droughts. The survey covered the four mandals namely Atmakur, Dharmavaram, Kudair and Raptadu (Figure 1). The characteristics of the study blocks are as mentioned in Table 1.

Figure 1.

Survey locations in Ananthapuramu district of Andhra Pradesh in south India.

Table 1.

Overview of study blocks.

Groundnut (Arachis hypogaea) has traditionally been one of the most important crops grown in the project area, and Andhra Pradesh (AP) is the second largest producer and exporter of groundnut in the country [10]. Ananthapuramu district is one of the major producers of groundnut in the state of AP and occupies a lion’s share in the total crop area (Figure 2). More than 85% of the farmers cultivate groundnut in the region, the majority of whom are small and marginal (Marginal (<1 ha), Small (1–<2 ha), Semi-medium (2–<4 ha), Medium (4–10 ha), and Large farmer (>10 ha)) farmers.

Figure 2.

Area under different crops in Ananthapuramu district of AP state. Source: Author’s compilation from ICRISAT District Level Data [11].

2.2. Study Design and Data Collection

The tab-based (CSPro software package) face-to-face interviews were conducted at the ICRISAT-Walmart project location during August–October 2020 (Figure 3). From each block, villages were randomly selected. Table 2 summarises the overall sample size of the study. Before going to the field survey, field enumerators were trained, and the questionnaire was pilot tested (Questionnaire provided as supplementary materials). The stratified random sampling method was applied to the list of 659 project beneficiary households from the project baseline survey, which was conducted in 2019. Twenty villages were randomly selected from 44 villages representing four blocks (mandals). Sample stratification ensured representation of all genders, diverse socioeconomic groups, classes, and categories. Sixty-six households from each block were selected for the survey. In addition to the farm households, eight each of input dealers, village-level brokers, and primary processors were also interviewed to understand the impact across the various groundnut crop value chain actors as it is the major crop in the region.

Figure 3.

Field enumerators interaction with survey respondents.

Table 2.

Sources of data.

2.3. Data Analysis

The data used is from two different field surveys at the project location for this analysis. One set of data is from a scoping study carried out as part of baseline survey before the start of the project during 2019 to map the value chain. The second set of data was collected during the post lockdown period to understand the impact of COVID-19 on value chain actors. We used SPSS statistical software and MS Office excel for data analysis. Garret ranking technique was used to analyse the concerns of crop production and other challenges faced by the households amid COVID-19 pandemic. The Garret Ranking technique, can provide numerical scores to an ordering of factors, in this case, the concerns and challenges faced by farm households. The prime advantage of this technique over simple frequency distribution is that the concerns raised by respondents are assigned simple ranks and then the specific statements of concerns and challenges are arranged based on their severity from the respondent’s point of view. By arranging the constraints based on their severity from the perspective of the respondents, this tool helps to suggest entry-points for addressing these constraints across contexts. Garrett’s formula for converting ranks into percent is:

where

- Rij = Rank given for the ith factor/variable by jth individual;

- Nj = number of constraint ranked by jth individual.

The percent position of each rank is then converted into Garret scores using the Garret conversion table [12]. For each challenge statement, the scores of individual respondents are added together and then divided by the total number of respondents to calculate the average score for that particular statement. These mean scores are arranged in descending order, and accordingly ranked.

3. Scoping Study

The scoping study was carried out to map the value chain of groundnut as part of the project baseline survey in the study region before the COVID-19 pandemic. The research methodology followed for the value chain analysis involved primary interviews with the stakeholders in the value chain (Table 2). Five each of village-level brokers and Agricultural Produce Market Committee (APMC)/urban traders, three primary processors were interviewed from the project area. Similarly, one secondary processor and three exporters were interviewed from outside the district, as they do not have their presence in the district.

3.1. Groundnut Value Chain Mapping

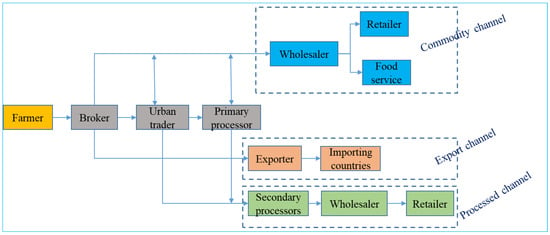

The value chain of groundnut has been split into the following three channels for easy understanding of the product flow and the stakeholders (Figure 4)

Figure 4.

Overview of groundnut value chain in the region. Source: Author’s own compilation based on the scoping study.

- The value chain for groundnut as a commodity: extends from the farmer level to the level of retailers and foodservice channels (mostly smaller vendors and hawkers).

- Export value chain: the exporters of groundnut are majorly based in the city of Chennai, which is around 450 km from the study area. These exporters have access to the produce grown in the study location (Ananthapuramu) and surrounding areas. They procure groundnut in-shell through both village-level brokers as well as through urban traders who are located at district headquarters. There is no direct link between exporters and farmers.

- Processed groundnut value chain: secondary processors are those who manufacture oil, snacks, and other value-added products. They source raw material from urban traders and primary processors. It has been observed that for most of the processors, regular access to the produce is one of the major challenges.

3.2. Key Actors in the Groundnut Value Chain

Farmers: The majority of the farmers in the region are small and marginal, they own less than 2 ha of land. Farmers in the project area have a ready channel for sale of groundnuts that is the village-level brokers, who are in regular touch with farmers. They provide farmers with the opportunity to sell their produce at the farm gate without having to incur hassles related to the logistics of marketing. There is a high level of information asymmetry at the farmer level, both in terms of market prices as well as in terms of grades and quality. Farmers receive market prices through their network of brokers and fellow farmers, while there is virtually very little talk about grades till the point of sale to brokers. In terms of access to markets, farmers do not venture out into other marketing opportunities mostly because of the costs associated with logistics. However, frequent cash flow is another benefit for the farmer. Therefore, there is heavy dependence on brokers, and brokers are ready sources of sale, many a times distress sale for small and marginal farmers. Export demand has an impact on the prices of groundnut, especially in the off-season.

Village-level brokers: Village-level brokers act as links between farmers and the other stakeholders further down the value chain. They perform important functions such as aggregation of the produce and its distribution. The brokers have an extensive network with farmers in their catchment area and are in regular touch with farmers during and after the season. They pick up the stock from farmers’ fields. Brokers generally do not own facilities for storage and primary processing. They have limited storage facilities, that is local godowns or sheds. Brokers have a major influence on the price of the produce. They set the price while buying produce from the farmers, on account of their superior knowledge about grades and quality.

Urban traders: Urban traders are mostly located in the urban and semiurban centres and in the APMC markets. While urban traders generally do not own storage and processing facilities, their network in sourcing and sales provides them with a high bargaining power in the market. They play an important role in the distribution of the commodity in the value chain from upstream channels such as brokers to downstream stakeholders and channels. This category of traders procures almost 75% of their produce from village-level brokers. The sales channels for urban traders are as diverse as that of brokers. However, most of the brokers have to depend on these urban traders for distribution of the produce as urban traders have direct access to exporters, wholesalers, and secondary processors. Moreover, they also operate with primary processors and other traders for supplying produce of the specification that their consumers want.

Primary processors: They act as important links in the chain on two counts. Primary processors perform the most important function of shelling groundnuts. They are also engaged in the trading of groundnuts, depending on whether they have space for storage of the pods and the finished product (kernels). They also have a business relationship with brokers and urban traders, where they engage in primary processing on a rental model. That is, they charge for processing each kilogram of groundnut from other agents in the value chain, including village-level brokers, urban traders, and secondary processors. The husk/shell from the processing is usually retained by the primary processor in the rental model and is then sold as a byproduct, and is thus a source of additional source of revenue to the primary processor. Primary processors mostly own the machinery used for shelling. The major clientele of processors includes village-level brokers and urban traders, who work on a rental model.

Secondary processors: The major products manufactured locally from groundnut include groundnut oil and chikki (caramelised groundnut granola bar). There are a limited number of secondary processors in the project area. While there is a significant bulk-trade channel in groundnut oil, there is very little emphasis on supplying branded products. Secondary processors of groundnut are greatly impacted by the price of raw material (groundnut pods and kernels). Off-season supply of groundnuts is a major challenge for secondary processors.

Exporters: Groundnut exporters who procure from the region are mostly concentrated in the city of Chennai in Tamil Nadu. Almost 75% of the groundnut exports from India happens through the Chennai seaport. Indonesia and Vietnam are the major importers of Indian groundnuts and account for almost 90% of the exports from Chennai port. While merchant-exporters deal in just the trade of groundnut, manufacturer-exporters have installed facilities for primary processing, and they export the finished produce (mainly kernels).

4. Results and Discussion

4.1. Socioeconomic Characteristics of Survey Respondents

A total of 264 respondents appeared for interviews from 20 villages representing four blocks in the Ananthapuramu district. Of 264 respondents, 131 were male, and 133 were female. The respondents’ age ranged from 24 to 80 years involved in farming, and the average age is 45 years. The survey respondents represented all the categories of landholdings. From the total respondents there were marginal (6%), small (9%), semi-medium (29%), medium (45%), and large (12%) farmers. Groundnut is one of the main crops of this region, and 55% of our survey respondents are growing groundnut as one of the main crops during both summer and kharif seasons. Pulses, Paddy and vegetables are other crops (Figure 2). Of total respondents, 76% reported agriculture as the primary source of livelihood, 15% from agricultural wages, 3% from allied sectors, and remaining from other income sources linked to agriculture.

COVID-19 has affected the whole world. It is much harder for poor people, particularly farmers, farm labourers, migrant workers, and other small businesses in rural areas struggling to sustain their livelihood activities and support their families [13]. The impact is indirect rather than direct to the farming communities. Though crop production and food availability were not very affected in the region, the impact on post-production is severe due to issues with logistics, market closure, and other government restrictions resulting in a decline in household income. The COVID-19 pandemic has exacerbated the strain that rural communities in the region already experience.

4.2. COVID-19 Induced Disruptions to Food Production System and Pathways

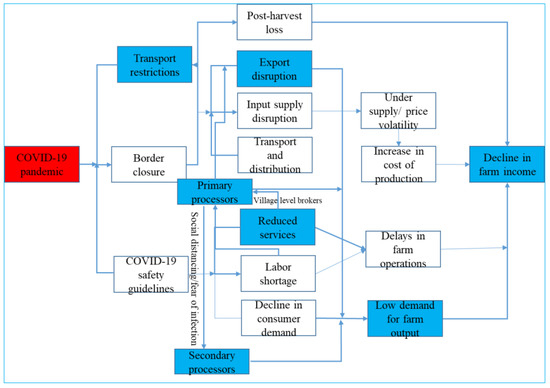

Our survey results revealed that the whole food production system is disrupted, starting from the input supplier to the end consumer. The impact varies among the different actors along the value chain. It is very severe for farmers, farm labourers, migrant workers, village-level aggregators, primary processors, secondary processors, and farm logistic service providers. The impact pathways are multiple, as shown in Figure 5. Our primary focus is on the groundnut value chain and associated livelihoods as it is one of the major crops of this region. The majority of the farmers produce groundnut as a main crop both in summer and kharif seasons and a few other crops. The intrastate, interstate, and international supply chains for commodities export, import, agricultural inputs, and seeds have been affected due to movement restrictions. At the production level, farm operations were impeded due to lack of transport facilities, local government restrictions, market closure, and non-availability of labour for farm activities. Lack of labour is not only because of local governments’ restrictions, but also because of the fear of disease among the rural community. Massive post-harvest losses were reported due to lack or limited transport facilities. Further, village-level brokers stopped buying farm output as there were border closures, resulting in a lack of demand from major buyers such as local markets, urban traders, and primary processors for the commodity.

Figure 5.

Flowchart showing COVID-19 induced groundnut value chain disruptions. (Note: blue boxes indicate major actors/activities affected and the thickness of the arrows depicts strong relation assessed based on the field survey).

In the groundnut value chain, the critical linkages (blue boxes in Figure 5) that are affected severely are logistics, which connects input suppliers to production to village-level brokers, primary processors, secondary processors, and export procurement firms. The specific sections are presented below.

4.3. COVID-19 Impact on Rural Livelihood

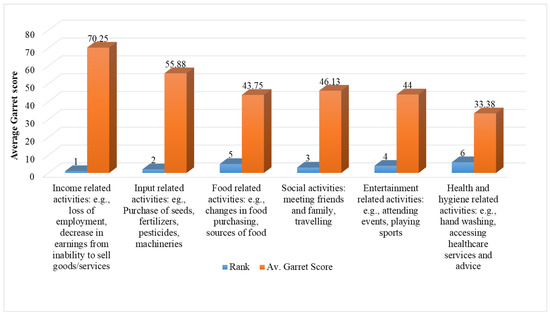

From the total survey respondents, 94% of households depend on agriculture for their livelihoods. Furthermore, 98.5% have reported that they are affected by the COVID-19 pandemic, and their income is decreased significantly during the COVID-19 induced restrictions. The impact is much more severe for small and marginal farmers compared to medium and large farm households, 54% of the households reported their income decreased by up to 25%, and 19% of the households reported their household income decreased by up to 50%. In total, 35% of the households feel uncertainty about their future source of income and are thinking of alternative livelihood options such as livestock breeding, dairy, tailoring and migrating to the city to work in malls as security and sales staff. Most of these households belong to small and marginal landholders. More than 96% of households have reported that they do not plan to migrate after the situation becomes normal and would like to continue farming. Almost every household received food grains (rice, wheat, sugar, and daal) through the government safety net program given via the public distribution system, which ensured their daily food during the COVID-19 pandemic. Travel, contact restrictions, and restrictions on transport of farm harvest were ranked as top specific restrictions (Figure 6A) imposed by local governments that have affected their livelihoods. As a result, the most disrupted activities reported are income-related activities (e.g., loss of employment, decrease in earnings from being unable to sell goods/services) and input related activities (e.g., purchase of seeds, fertilisers, pesticides) are concerns that ranked high for those whose daily life was affected (Figure 6B).

Figure 6.

(A) Specific restrictions imposed on the communities amidst the COVID-19 pandemic. (B) Routine daily activities disrupted amidst the COVID-19 pandemic on priority.

To meet their expenses, 54% of the households borrowed money from their friends, relatives, and local money lenders by paying an average of 22% of interest per annum. To borrow money, 61% of the households have mortgaged their assets (27% mortgaged jewellery, 14% land, 17.5% home/other machinery, and 3% mortgaged livestock). The reasons for borrowing, among the different landholders, is shown in Figure 7.

Figure 7.

(A) Household’s borrowing money among different categories of farmers during the COVID-19 pandemic. (B) Household’s reasons for borrowing money during the COVID-19 pandemic.

4.4. COVID-19 Impact on Crop Production

Summer season: The COVID-19 pandemic coincided with the summer crop season in south India. As a result, only 39% of the households cultivated the crops (Figure 8A) in the study villages, and 86% reported that their crop production was affected by the pandemic. Though the farm production per se was not affected by pandemic directly, lack of inputs and labour supply had an indirect impact. However, the post-production was significantly affected. Disruptions in logistics and marketing lead to colossal produce loss at the farm level, particularly perishables. In the case of nonperishable produce, particularly groundnut crop, it was difficult for farmers to store the harvested produce due to lack of public storage facilities at village or block-level. Even if there were few warehouses at taluks (revenue districts), it was difficult to store the produce from all the farmers. Generally, (in the absence of COVID-19) farmers sell the produce immediately after harvest, as village-level brokers procure at farm gate. Thus, most farmers stored the produce in open air, which might have reduced the weight of the groundnut due to moisture loss, rodents, insects, and physical damage. However, after a few months, the local government relaxed the guidelines that allowed farm activities, including transport and marketing. As a result, 66% of the farm households sold their produce directly to middlemen at lower prices, 16% to local markets, 5% continued to store the produce expecting higher price, and only 2% sold at the farm gate level. The most important challenges farmers faced during the summer crop production amid COVID-19 were labour shortage, lower demand/price for the produce, lack of transport services, market facility, and nonavailability of agricultural inputs.

Figure 8.

(A) Crops production during summer season amid the COVID-19 pandemic. (B) Crops production during kharif season amid the COVID-19 pandemic.

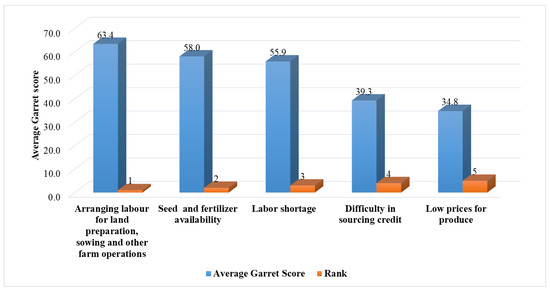

Kharif season: Prolonged restrictions and the fear of COVID-19 affected the succeeding kharif season crop production too. During the kharif season, 91% of the surveyed farm households cultivated various crops (Figure 8B) against 39% during the previous summer season. The various challenges/concerns farmers faced during the kharif season are Garret ranked from 1 to 6 based on their severity as shown in Figure 9.

Figure 9.

Challenges faced by farmers during the kharif season amid the COVID-19 pandemic.

The most critical challenge was arranging labour for land preparation and other farm activities with an average Garret score of 63.4. Due to the fear of the disease, the majority of the farm labourers were hesitant to go to farms despite higher wage rate offers. This led to delay in farm operations and high cost of production. The majority of the labourers were getting free food grains from the government under safety net programs. Thus, all the labourers had food security during the COVID-19 pandemic. Another important challenge during kharif season was the lack or under-supply of quality farm inputs such as seeds and fertilisers, which resulted in price volatility leading to high production costs for farmers. In total, 50% of the farmers reported that they purchased inputs at higher price, 17.5% of farmers did not get quality inputs, and only 30% got inputs at regular price from their input dealers. On the other hand, input dealers faced liquidity and input supply challenges (detailed discussion in the section on input dealers). Amid the COVID-19 pandemic, there were a significant reduction in the various public services to farmers, and farmers indicated their severity of need (Figure 10).

Figure 10.

Farmers perceptions on various services needed during the COVID-19 pandemic (% response rate).

In total, 30% of the farmers reported that there is a need for timely information about the market that is, prices and buyers. A total of 20% of farmers reported the need for information about quality inputs, followed by 17% health services, 11% weather information, and 12% reported need for agriculture extension services.

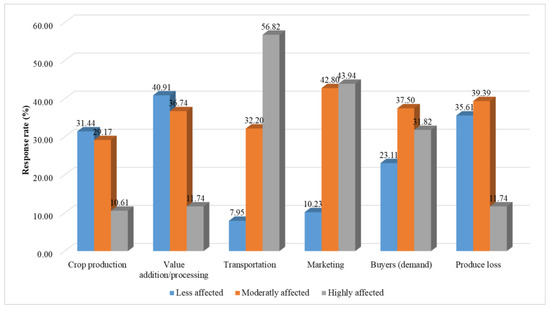

Based on the severity of the COVID-19 impact on different activities, 57% of the surveyed farmers reported that the transportation and marketing of farm output were most affected, followed by less demand for the produce (Figure 11). The most striking point is that 87.5% of the marginal and 56.5% of the small farmers are highly affected.

Figure 11.

Farmers perceptions on severity of the COVID-19 pandemic impact on different activities.

4.5. COVID-19 Impact on Rural Households’ Food Consumption

During the early days of the COVID-19 pandemic, there was a fear among the general public about food scarcity. As a result, people started stockpiling food products [14]. However, it was not the case in rural areas. Unlike in urban areas, food availability was not the major concern in rural areas during the pandemic. Availability of food for self-consumption was not largely affected by this pandemic in rural areas. It may be due to the fact that, generally, in villages, farm households store food grains for home consumption till the next seasons’ harvest. In addition, public distribution of food grains also might have helped. Close to 86% of the households reported that they had sufficient food for the family, and only 14% reported that they faced scarcity of food. However, 89% of the households indicated that food prices have increased amid this pandemic.

4.6. Availability of Essential Commodities in the Villages

When asked about the availability of various essential commodities (such as staple food grains, fruits, vegetables, and milk; hygiene items, essential medicines, non-vegetarian food, and beverages) in local village stores/markets, 88% of the households reported that fresh foods such as fruits, vegetables and milk were not ‘always’ available, but only ‘sometimes’ (Figure 12). Similarly, 94% of the households reported that non-vegetarian items were not available ‘regularly’, but only ‘occasionally’. Basic food items such as cereals and pulses were mainly distributed through public distribution system under safety net program. In total, 55% of the respondents mentioned essential medicines were ‘always’ available and 62.5% of the respondents said hygiene items were available ‘sometimes’. The diversity in farm production is less in the study location and farmers are specialised in production of only few crops, mainly groundnut which occupies a major share of crop area. The farm production diversity directly linked to household dietary diversity [15], and due to less diversity of crops in their farms, households tend to buy food products from the nearby markets. During the COVID-19 pandemic market closure and restrictions had an impact on household nutrition [16,17]. The availability of fruits, vegetables, meat products declined significantly in the study location during initial days of nationwide lockdown.

Figure 12.

Availability of commodities in the local stores and markets.

4.7. Purchase Behaviour of Farm Households Amid the COVID-19 Pandemic

When we asked about their food purchase behaviour, it seems unlike urban consumers, rural households were not panicky about the shortage of food during the lockdown. Around 82% of the households reported that they ‘sometimes’ bought larger quantities and stocked. However, it was not due to fear of unavailability but because of restrictions on movement of people. Further, around 43% of the households reported they ‘never purchased’ ready-to-cook (RTC) or ready-to-eat (RTE) foods, but 53% of HHs ‘sometimes’ bought RTC or RTE foods. Whereas, around 72% of households reported that they ‘sometimes’ bought cheaper food due to financial uncertainty amid the COVID-19 pandemic. The village-level stores were the main places of purchase as weekly markets had stopped during early months of the COVID-19 pandemic to avoid the spread of the disease at community level. The frequency of visits to local stores had significantly decreased compared to before the COVID-19 pandemic. Before the pandemic, 43% of the households reported that they visit local stores once in two to three days, whereas, during pandemic it reduced to 8%. A total of 43% of households reported that they visit local stores once a week and 29% of households reported that they visit stores once a month to buy the household essentials. When asked about any online food purchase, 97% of households reported that they never purchased anything online. Among the RTE products purchased by the households, 44% indicated biscuits, 40% bread, 20% potato crisps, 13% savoury mixture and 10% fruit jams. Similarly, RTC products include, 56% Noodles and 42% reported upma mixture (semolina porridge) and savoury mixture.

4.8. Change in Consumption Pattern

More than 87% of the households reported there was change in the food consumption pattern in terms of different food categories. There was a relatively increase in the consumption of grains (cereals and pulses) compared to pre-COVID-19 period. In total 60% of households reported that their cereals and pulse consumption had increased up to 10%, and only 11% of households reported their cereals consumption decreased by up to 10%. Similarly, around 45% of households reported that their consumption of vegetables and eggs increased up to 10%. Whereas, 30% of the households reported they had not consumed any processed and packed foods (Figure 13).

Figure 13.

Farmers perceptions on change in consumption of different food groups.

5. Input Dealers

Agricultural input dealers are important chain actors in the agricultural value chains. They provide inputs such as seeds, fertilisers, pesticides, farm machineries and other inputs to the farmers. The relationship between input dealers and farmers is an ongoing one. Many a times input dealers provide inputs on credit to farmers and information related to crop production and protection. Our field survey included face-to-face interviews with eight input dealers in the study location in different villages. All the input dealers were based at block level and provided services to nearby villages. During the COVID-19 pandemic input dealers were also badly affected due to restrictions on interstate transport, labour shortage, input price volatility, pressure from companies to pay previous outstanding bills and demand for inputs on credit from farmers. Input dealers’ business is mainly dependent on farmers. Due to transport and contact restrictions, they lost up to 75% of their business. Additionally, the demand from the input supplying companies to clear the previous seasons’ credit placed them under enormous pressure. In addition, overhead costs of input shops such as rent, electricity charges and higher wages for the labour confounded to the impact during the COVID-19 pandemic.

The various activities of input dealers affected during COVID-19 pandemic are:

- 83% input dealers reported transportation and marketing;

- 67% reported decline in the demand for inputs from the farmers;

- 50% reported labour shortage;

- 33% reported credit issues and

- 17% reported delayed supply of inputs from the companies.

Input dealers were affected by both decrease in the sale of inputs (75%) and decrease in the supply of inputs from the agro-companies (no promotion and demonstration). In total, 75% of the input dealers mentioned there was an average 44% decrease in the number of farmers visiting input shops to buy farm inputs. Due to disruption of input supply chain, there was price volatility in the inputs. A total of 50% of the input dealers reported an average 22.5% increase in the input’s prices, whereas 13% of dealers reported that there is no change in the prices of inputs during pandemic. At the same time 87.5% of the input dealers reported there was under-supply of inputs from the manufacturing companies due to logistic and other restrictions.

Input dealers were asked to report the severity of effects induced by COVID-19 on various activities (Figure 14). The income-related activities (loss of employment, decrease in sales, etc.) are most affected due to restrictions, followed by input related activities (purchase of seeds, fertilisers, pesticides and machineries). Due to the disruption in groundnut seeds production during summer season and transport restrictions amid the COVID-19 pandemic, supply of quality seeds was affected for the kharif season and it led to input price volatility in the study location.

Figure 14.

Input dealer’s routine daily activities disrupted amid the COVID-19 pandemic (rank 1–6, 1 being most affected and 6 is least affected).

6. COVID-19 Impact on Village-Level Brokers

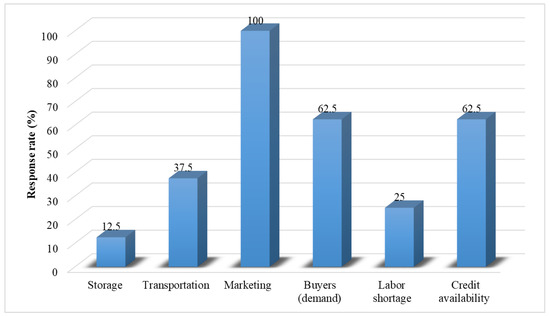

Our survey included face-to-face interviews with eight village-level brokers in different villages within the region of the study. Village-level brokers act as the connecting links between farmers and the other stakeholders further down the value chain. They perform important functions such as aggregation of the produce and its distribution, thus adding possession and time utility. Brokers have a network of farmers whom they can tap for the supply of produce. In general cases, brokers belong to the same village as the set of farmers from whom they generally purchase produce. The area of procurement for any broker is restricted to a few villages or a cluster. However, the sales geographies extend to nearby administrative blocks, districts, and even states. The marketing that happens in the APMC markets of the district is mostly done by brokers, while they also supply produce to nearby groundnut trade pockets in other districts and states. Most of the village-level brokers were also affected by the pandemic as they were not allowed to leave their villages due to contact restrictions, fear for their health and disease transfer. Though they have supply of commodities from whom they regularly buy, there was no demand from the exporters and secondary processors. As a result, 75% of the brokers reported that their economic activities were affected leading to economic loss during pandemic. In addition, brokers mentioned health expenditure increased during the pandemic. When asked about what activities were affected during the pandemic, 100% of brokers mentioned that marketing of the produce procured from the farmers was largely affected followed by low demand for the produce (62.5%) as indicated in Figure 15.

Figure 15.

Village level broker’s activities affected during the COVID-19 pandemic compared to pre-COVID-19 situation.

All the respondents reported that, there was an average 63% decrease in the business and there was no report of any increase in the business of village-level brokers. In total, 87.5% of the brokers reported that there was an average 56.43% decrease in the procurement price and 12.5% of the brokers reported there was no change in the procurement price. Due to disruption in the routine business of village-level brokers, 62.5% of the respondents reported they borrowed money from others to cover health, household and children’s education related expenses.

Brokers tap a variety of channels for the sale of produce. Although almost 80% of the produce goes to APMC markets and urban traders, they are also capable of serving stakeholders such as exporters and secondary processors.

Brokers do not own facilities for storage and primary processing. Their limited storage facilities are local godowns or sheds. If additional storage facilities are required, they depend on public or private warehouses such as the ones owned by Central Warehousing Corporation. However, due to transport restrictions amid COVID-19 they could not avail storage facilities, as a result brokers stopped procuring from farmers. Brokers work with other actors in the downstream of the value chain such as primary processors, urban traders, secondary processors and also exporters. The price at which a broker supplies produce to the downstream channels can vary with season. In terms of primary processing, brokers work with primary processing units for the shelling of groundnuts, on a rental basis. There is also a practice where the labour for primary processing is supplied by the brokers and the processor charges a fee for the usage of his facility.

7. COVID-19 Impacts on Groundnut Primary Processors and Their Livelihood

We conducted face-to-face interview with eight primary processors in the study villages. They are important intermediaries, and they perform the most important function of shelling groundnuts. Sometimes depending on whether they have space for storage of the pods and the finished product (kernels), they also trade groundnuts. They have a business relationship with brokers and urban traders, where they engage in primary processing on a rental model. Due to the COVID-19 pandemic the majority of the primary processors were also affected due to various restrictions as mentioned in Figure 16. Transport restrictions had greatly affected the primary processors too.

Figure 16.

Primary processors are affected by specific restrictions during the COVID-19 pandemic.

As a result, 87.5% of the respondents reported they were unable to procure materials from farmers or village-level brokers and supply to their buyers further downstream in the value chain. Some of the other issues they mentioned were restrictions in interstate movement, low demand for the processed goods, high overhead cost due to electricity bills and godown rents and not using machines to their optimum level. Figure 17 shows specific business activities that were most affected due to COVID-19. All the respondents reported that there was an average 54% decrease in the business income.

Figure 17.

Primary processor’s activities affected during the COVID-19 pandemic compared to the pre-COVID-19 situation.

8. Conclusions

The impact of COVID-19 is varied for different actors in the groundnut value chain. The most affected actors in chain are farmers and their livelihood, particularly small and marginal farmers. COVID-19 created double burden on farmers. On one side, their household income declined due to disruption in production and marketing of their farm produce. One the other side steep rise in farm input prices and consumer food prices resulted in increased household expenditure and decreased dietary diversity.

The majority of the producers are small and marginal, but they do not practice subsistence farming. Instead, they follow market-oriented production and grow few market-oriented crops in the study area. Even though crop production was not very affected, disruption of post-production supply chains resulted in a major adverse impact on farmers’ livelihood. The COVID-19 pandemic was a shock to farmers similar to other natural disasters like droughts, floods etc., however, the uncertainty was much greater making farmer’s decision making much more complex in the absence of appropriate information support. The smallholder farmers were the most affected amongst rural communities thus the pandemic adds to agrarian distress they continue to face. Therefore, there is need to safeguard the livelihoods of these vulnerable categories of farmers not only during COVID-19 situation, even beyond the pandemic to support recovery and resilience mechanism. Traditionally, Public Distribution System (PDS) supplies basic food like rice, wheat and sugar and to some extent pulses to the poor households. There is need to have a flexible strategy to include diverse and nutrient rich foods as part of PDS to the poor households during crisis situations like the COVID-19 pandemic to safeguard them from hunger and malnutrition.

Amidst the pandemic, post-production supply chain disruption was mainly due to lack of transport, storage infrastructure, information asymmetry and poor market linkages. As a result, there was reduction in the income of all the actors in the supply chain due to reduced business (for input dealers, brokers, processors), increase in the input price, reduction in the commodity prices and post-harvest losses for farmers. The COVID-19 pandemic has shown how digital technologies have helped to make supply chains more efficient [18]. Emergence of digital platforms in few places during the COVID-19 pandemic could effectively help in providing information and connecting producers to consumers, were a silver lining and these innovations need to provide support post-COVID-19 as well.

The impact of COVID-19 on local groundnut production was seen to have spread across the value chain actors starting from local farmer producers, primary and secondary processors (oil mills), exporters and end consumers. The majority of the hotels, restaurants, dhabas (roadside restaurants in India), canteens, and bakers use palm oil as a predominant frying medium [19]. From April to July, the import of palm oil declined by 40% in India. Simultaneously, there was no decline in indigenous oil (sesame, sunflower, groundnut) consumption in home kitchens. As a result of the disruption in the supply chain of groundnut, oil prices have surged in the domestic market [20,21] impacting the consumers adversely.

Currently Indian agriculture is witnessing a number of reforms particularly related to marketing. These reforms are targeted to enhance efficiency of agricultural value chains and to improve conditions for farmers’ participation in the value chain, income and their overall livelihood. Therefore, based on the empirical evidence we gathered via this study and also considering the general situation of farmers beyond the COVID-19 induced restrictions, we suggest the following interventions to help farmers take benefits of market reforms and secure sustainable livelihoods:

- Encouraging farmer’s collectives such as Farmer’s Producer Organisations (FPO), which potentially reduce the transaction costs for small and marginal farmers while selling produce, buying inputs, extension services, etc. FPOs also provide bargaining power to producers. Besides, FPOs operating as aggregators will also reduce transactions cost for the big buyers and processors making it a win-win relationship for both producers and buyers.

- Policy support for infrastructure development such as storage, cold chains and pack houses in strategic places.

- Market access through improved market information, contract farming and linking farmer’s collectives to e-commerce companies, agri-tech start-ups and export markets.

- Capacity building of farmers on improved production practices, quality standards, value addition, use of information and communication technologies, financial literacy, common pool resource utilisation and sensitising about government safety net programs to quickly make use of those programs during natural disasters.

We acknowledge that the limitation of this study is the sampling was confined to one geographic area in South India. Therefore, the results cannot be generalised. Further studies covering value chains of different crops in larger geographical areas could build on these findings and expand the validity of the results.

Supplementary Materials

The following are available online at https://www.mdpi.com/2071-1050/13/4/1707/s1, File S1: Perceptionof COVID-19 impacts on farmer’scrop production and livelihood in Anantapur District of Andhra Pradesh.

Author Contributions

Conceptualisation, R.N., S.N.; Methodology, R.N., S.N., A.S., S.D.M.; Writing—Original draft, R.N., S.N.; review and editing, R.N., S.N., A.S., S.K.; project administration and funding acquisition, A.S., S.D.M.; validation, formal analysis, investigation, data curation, Writing—Original draft, R.N. All authors have read and agreed to the published version of the manuscript.

Funding

This work was undertaken as part of the Consultative Group for International Agricultural Research Program (CGIAR) on Grain Legumes and Dryland Cereals (GLDC) led by International Crops Research Institute for the Semi-Arid Tropics (ICRISAT). Funding support for this study was provided by Walmart foundation. And the first two lead author’s positions are funded by Transforming India’s Green Revolution by Research and Empowerment for Sustainable Food Supplies (TIGR2ESS) project under Flagship 1.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Is taken.

Data Availability Statement

Not applicable.

Acknowledgments

We would like to thank R Padmaja for providing her initial comments on the survey questionnaire, field investigators and technical team who helped us in designing tab-based survey and data collection.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Loayza, N.V.; Pennings, S. Macroeconomic Policy in the Time of COVID-19; World Bank: Washington, DC, USA, 2020. [Google Scholar] [CrossRef]

- Jámbor, A.; Czine, P.; Balogh, P. The Impact of the Coronavirus on Agriculture: First Evidence Based on Global Newspapers. Sustainability 2020, 12, 4535. [Google Scholar] [CrossRef]

- Galanakis, C.M. The Food Systems in the Era of the Coronavirus (COVID-19) Pandemic Crisis. Foods 2020, 9, 523. [Google Scholar] [CrossRef] [PubMed]

- Nandi, N. Broken Supply Chains: COVID-19 Lockdown Is Having a Devastating Effect on Livelihoods in Rural India—CGIAR. 2020. Available online: https://tigr2ess.globalfood.cam.ac.uk/news/broken-supply-chains-covid-19-lockdown-having-devastating-effect-livelihoods-rural-india (accessed on 17 December 2020).

- Siche, R. What Is the Impact of COVID-19 Disease on Agriculture? Sci. Agropecu. 2020, 11, 3–9. [Google Scholar] [CrossRef]

- NIAP. COVID-19 Lockdown and India Agriculture: Options to Reduce the Impact. 2020. Available online: http://www.ncap.res.in/agri_lock.pdf (accessed on 19 December 2020).

- Phillipson, J.; Gorton, M.; Turner, R.; Shucksmith, M.; Aitken-McDermott, K.; Areal, F.; Cowie, P.; Hubbard, C.; Maioli, S.; McAreavey, R.; et al. The COVID-19 Pandemic and Its Implications for Rural Economies. Sustainability 2020, 12, 3973. [Google Scholar] [CrossRef]

- Inidan Express. COVID-19 Impact: India’s Exports Plunge to Record Low of 60.28 per Cent in April-The New Indian Express. 2020. Available online: https://www.newindianexpress.com/business/2020/may/15/covid-19-impact-indias-exports-plunge-to-record-low-of-6028-per-cent-in-april-2143848.html (accessed on 19 December 2020).

- Nair, R. It’s not Just Food Prices, Covid Pandemic Has Also Helped Push Inflation to 7.6% in India. Available online: https://theprint.in/economy/its-not-just-food-prices-covid-pandemic-has-also-helped-push-inflation-to-7-6-in-india/546473/ (accessed on 19 December 2020).

- APEDA. Groundnut. Available online: http://apeda.gov.in/apedawebsite/SubHead_Products/Ground_Nut.htm (accessed on 3 December 2020).

- ICRISAT-DLD. ICRISAT-District Level Data. Available online: http://data.icrisat.org/dld/src/biophysical.html (accessed on 8 December 2020).

- Garrett, H.E.; Woodworth, R.S. Statistics in Psychology and Education, 2nd ed.; Vakils, Feffer and Simons Private Ltd.: Bombay, India, 1969; p. 329. [Google Scholar]

- Bhavani. Impact of COVID-19 on Rural Lives and Livelihoods in India | ORF. Available online: https://www.orfonline.org/expert-speak/impact-covid19-rural-lives-livelihoods-india-64889/ (accessed on 20 December 2020).

- Brizi, A.; Biraglia, A. “Do I Have Enough Food?” How Need for Cognitive Closure and Gender Impact Stockpiling and Food Waste during the COVID-19 Pandemic: A Cross-National Study in India and the United States of America. Pers. Individ. Dif. 2021, 168, 110396. [Google Scholar] [CrossRef] [PubMed]

- Gupta, S.; Sunder, N.; Pingali, P.L. Market Access, Production Diversity, and Diet Diversity: Evidence from India. Food Nutr. Bull. 2020, 41, 167–185. [Google Scholar] [CrossRef] [PubMed]

- FAO. Committee on World Food Security High Level Panel of Experts on Food Security and Nutrition. 2020. Available online: http://www.fao.org/3/cb1000en/cb1000en.pdf (accessed on 21 December 2020).

- Raghunathan, K. COVID-19: India’s Response and Diets of Rural Poor—IFPRI South Asia Office. Available online: http://southasia.ifpri.info/2020/05/18/covid-19-indias-response-and-diets-of-rural-poor/ (accessed on 21 December 2020).

- Kumar, A.; Padhee, A.K.; Kumar, S. How Indian Agriculture Should Change after COVID-19. Food Secur. 2020, 12, 837–840. [Google Scholar] [CrossRef] [PubMed]

- Gopal, K. Explained. How Covid-19 Has Helped the Groundnut Stage a Comeback. 2020. Available online: https://indianexpress.com/article/explained/how-covid-19-has-helped-the-groundnut-stage-a-comeback-6539602/ (accessed on 20 December 2020).

- Financial Express. Groundnut Oil Prices Surge on Raw Material Supply Chain Disruption—The Financial Express. 2020. Available online: https://www.financialexpress.com/market/commodities/groundnut-oil-prices-surge-on-raw-material-supply-chain-disruption/1917650/ (accessed on 6 December 2020).

- Deepak, D. Edible Oil Prices Rise by up to 30%, Set off Alarm Bells. 2020. Available online: https://timesofindia.indiatimes.com/india/edible-oil-prices-rise-by-up-to-30-set-off-alarm-bells/articleshow/79311145.cms (accessed on 20 December 2020).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).