The Effect of the Perceived Utility of a Management Control System with a Broad Scope on the Use of Food Waste Information and on Financial and Non-Financial Performances in Restaurants

Abstract

1. Introduction

2. Background

2.1. Broad-Scope of Management Control System

2.2. Use of Food Waste Information

3. Materials and Methods

3.1. Questionnaire Design and Data Collection

3.2. Variable Measurement

3.2.1. Perceived Utility of MCS

3.2.2. Use of Food Waste Information

3.2.3. Financial Performance

3.2.4. Non-Financial Performance

3.2.5. Control Variables

3.3. Data Analysis

4. Results

4.1. Measurement Model

4.2. Structural Model

5. Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Eriksson, M.; Strid, I.; Hansson, P.A. Carbon footprint of food waste management options in the waste hierarchy–a Swedish case study. J. Clean. Prod. 2015, 93, 115–125. [Google Scholar] [CrossRef]

- Bravi, L.; Murmura, F.; Savelli, E.; Viganò, E. Motivations and Actions to Prevent Food Waste among Young Italian Consumers. Sustainability 2019, 11, 1110. [Google Scholar] [CrossRef]

- Fanelli, R.M. Using Causal Maps to Analyse the Major Root Causes of Household Food Waste: Results of a Survey among People from Central and Southern Italy. Sustainability 2019, 11, 1183. [Google Scholar] [CrossRef]

- Thyberg, K.L.; Tonjes, D.J. Drivers of food waste and their implications for sustainable policy development. Resour. Conserv. Recycl. 2016, 106, 110–123. [Google Scholar] [CrossRef]

- Food and Agriculture Organization of the United Nations-FAO. Food Loss and Food Waste. Available online: http://www.fao.org/food-loss-and-foodwaste/en/ (accessed on 1 February 2019).

- Betz, A.; Buchli, J.; Göbel, C.; Müller, C. Food waste in the Swiss restaurants-magnitude and potential for reduction. Waste Manag. 2015, 35, 218–226. [Google Scholar] [CrossRef]

- Aamir, M.; Ahmad, H.; Javaid, Q.; Hasan, S.M. Waste Not, Want Not: A Case Study on Food Waste in Restaurants of Lahore, Pakistan. J. Food Prod. Market. 2018, 24, 591–610. [Google Scholar] [CrossRef]

- Sakaguchi, L.; Pak, N.; Potts, M.D. Tackling the issue of food waste in restaurants: Options for measurement method, reduction and behavioral change. J. Clean. Prod. 2018, 180, 430–436. [Google Scholar] [CrossRef]

- Langley, J.; Yoxall, A.; Heppell, G.; Rodriguez, E.M.; Bradbury, S.; Lewis, R.; Luxmoore, J.; Hodzic, A.; Rowson, J. Food for thought? A UK pilot study testing a methodology for compositional domestic food waste analysis. Waste Manag. Res. 2010, 28, 220–227. [Google Scholar] [CrossRef]

- Cicatiello, C.; Secondi, L.; Principato, L. Investigating Consumers’ Perception of Discounted Suboptimal Products at Retail Stores. Resources 2019, 8, 129. [Google Scholar] [CrossRef]

- Canali, M.; Amani, P.; Aramyan, L.; Gheoldus, M.; Moates, G.; Östergren, K.; Silvennoinen, K.; Waldron, K.; Vittuari, M. Food waste drivers in Europe, from identification to possible interventions. Sustainability 2017, 9, 37. [Google Scholar] [CrossRef]

- Derqui, B.; Fernandez, V. The opportunity of tracking food waste in school canteens: Guidelines for self-assessment. Waste Manag. 2017, 69, 431–444. [Google Scholar] [CrossRef] [PubMed]

- Irani, Z.; Sharif, A.M.; Lee, H.; Aktas, E.; Topalo, Z.; Wout, T.V.; Huda, S. Managing food security through food waste and loss: Small data to big data. Comput. Oper. Res. 2018, 98, 367–383. [Google Scholar] [CrossRef]

- Raimondo, M.; Caracciolo, F.; Cembalo, L.; Chinnici, G.; Pecorino, B.; D’Amico, M. Making Virtue Out of Necessity: Managing the Citrus Waste Supply Chain for Bioeconomy Applications. Sustainability 2018, 10, 4821. [Google Scholar] [CrossRef]

- Wen, Z.; Hu, S.; Clercq, D.; Beck, M.B.; Zhang, H.; Zhang, H. Design, implementation, and evaluation of an Internet of Things (IoT) network system for restaurant food waste management. Waste Manag. 2018, 73, 26–38. [Google Scholar] [CrossRef] [PubMed]

- Strotmann, C.; Friedrich, S.; Kreyenschmidt, J.; Teitscheid, P.; Ritter, G. Comparing food provided and wasted before and after implementing measures against food waste in three healthcare food service facilities. Sustainability 2017, 9, 1409. [Google Scholar] [CrossRef]

- Otten, J.; Getts, K.; Diedrich, S.; Benson, C. Commercial and anti-hunger sector views on local government strategies for helping to manage food waste. J. Agric. Food Syst. Community Dev. 2018, 8, 55–72. [Google Scholar] [CrossRef]

- Chenhall, R.H. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Account. Organ. Soc. 2003, 28, 127–168. [Google Scholar] [CrossRef]

- Otley, D. Performance management: A framework for management control systems research. Manag. Account. Res. 1999, 10, 363–382. [Google Scholar] [CrossRef]

- Cugueró-Escofet, N.; Rosanas, J.M. The just design and use of management control systems as requirements for goal congruence. Manag. Account. Res. 2013, 24, 23–40. [Google Scholar] [CrossRef]

- Langevin, P.; Mendoza, C. How can management control system fairness reduce managers’ unethical behaviours? Eur. Manag. J. 2013, 31, 209–222. [Google Scholar] [CrossRef]

- Lopez-Valeiras, E.; Gomez-Conde, J.; Naranjo-Gil, D. Sustainable innovation, management accounting and control systems, and international performance. Sustainability 2015, 7, 3479–3492. [Google Scholar] [CrossRef]

- Bouwens, J.; Abernethy, M.A. The consequences of customization on management accounting systems design. Account. Organ. Soc. 2000, 25, 221–259. [Google Scholar] [CrossRef]

- Naranjo-Gil, D.; Hartmann, F. Management accounting systems, top management team heterogeneity and strategic change. Account. Organ. Soc. 2007, 32, 735–756. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Morris, D. The impact of structure, environment, and interdependence on the perceived usefulness of management accounting systems. Account. Rev. 1986, 61, 16–35. [Google Scholar]

- Schanes, K.; Dobernig, K.; Gözet, B. Food waste matters-A systematic review of household food waste practices and their policy implications. J. Clean. Prod. 2018, 182, 978–991. [Google Scholar] [CrossRef]

- Dora, M.; Wesana, J.; Gellynck, X.; Seth, N.; Dey, B.; De Steur, H. Importance of sustainable operations in food loss: Evidence from the Belgian food processing industry. Ann. Oper. Res. 2020, 290, 47–72. [Google Scholar] [CrossRef]

- Warshawsky, D.N. The Challenge of Food Waste Governance in Cities: Case Study of Consumer Perspectives in Los Angeles. Sustainability 2019, 11, 847. [Google Scholar] [CrossRef]

- Ozbük, R.M.Y.; Coskun, A. Factors affecting food waste at the downstream entities of the supply chain: A critical review. J. Clean. Prod. 2020, 244, 118–628. [Google Scholar] [CrossRef]

- Mia, L.; Chenhall, R.H. The usefulness of management accounting systems, functional differentiation and managerial effectiveness. Account. Organ. Soc. 1994, 19, 1–13. [Google Scholar] [CrossRef]

- Tillema, S. Towards an integrated contingency framework for MAS sophistication Case studies on the scope of accounting instruments in Dutch power and gas companies. Manag. Account. Res. 2005, 16, 101–129. [Google Scholar] [CrossRef]

- Mia, L.; Winata, L. Manufacturing strategy, broad scope MAS information and information and communication technology. Br. Account. Rev. 2008, 40, 182–192. [Google Scholar] [CrossRef][Green Version]

- Choe, J.M. The strategic alignment of management accounting information systems, and organizational performance. Global Bus. Financ. Rev. Open Access 2017, 22, 51–65. [Google Scholar] [CrossRef]

- Lunkes, R.J.; Naranjo-Gil, D.; Lopez-Valeiras, E. Management Control Systems and Clinical Experience of Managers in Public Hospitals. Int. J. Environ. Res. Public Health 2018, 15, 776. [Google Scholar] [CrossRef] [PubMed]

- Henri, J.F.; Journeault, M. Eco-control: The influence of management control systems on environmental and economic performance. Account. Organ. Soc. 2010, 35, 63–80. [Google Scholar] [CrossRef]

- Abdel-Maksoud, A.; Kamel, H.; Elbanna, S. Investigating relationships between stakeholders’ pressure, eco-control systems and hotel performance. Int. J. Hosp. Manag. 2016, 59, 95–104. [Google Scholar] [CrossRef]

- Goonan, S.; Mirosa, M.; Spence, H. Getting a taste for food waste: A mixed methods ethnographic study into hospital food waste before patient consumption conducted at three New Zealand foodservice facilities. J. Acad. Nutr. Diet. 2014, 114, 63–71. [Google Scholar] [CrossRef]

- Pirani, S.I.; Arafat, H.A. Reduction of food waste generation in the hospitality industry. J. Clean. Prod. 2016, 132, 129–145. [Google Scholar] [CrossRef]

- Derqui, B.; Fernandez, V.; Fayos, T. Towards more sustainable food systems. Addressing food waste at school canteens. Appetite 2018, 129, 1–11. [Google Scholar] [CrossRef]

- Pinto, R.S.; Pinto, R.M.S.; Melo, F.F.S.; Campos, S.S.; Cordovil, C.M.S. A simple awareness campaign to promote food waste reduction in a University canteen. Waste Manag. 2018, 76, 28–38. [Google Scholar] [CrossRef]

- Falasconi, L.; Vittuari, M.; Politano, A.; Segrè, A. Food waste in school catering: An Italian case study. Sustainability 2015, 7, 14745–14760. [Google Scholar] [CrossRef]

- Filimonau, V.; Gherbin, A. An exploratory study of food waste management practices in the UK grocery retail sector. J. Clean. Prod. 2017, 167, 1184–1194. [Google Scholar] [CrossRef]

- Ministry of Tourism (Brazil). Cadastur. Available online: http://www.classificacao.turismo.gov.br/MTUR-classificacao/mtur-site/cadastur.jsp. (accessed on 24 January 2020).

- Gomez-Conde, J.; Lunkes, R.J.; Rosa, F.S. Environmental innovation practices and operational performance. The joint effects of management accounting and control systems and environmental training. Account. Audit Account. J. 2019, 32, 1325–1357. [Google Scholar] [CrossRef]

- Bilska, B.; Tomaszewska, M.; Kołożyn-Krajewska, D. Managing the Risk of Food Waste in Foodservice Establishments. Sustainability 2020, 12, 2050. [Google Scholar] [CrossRef]

- Beretta, C.; Stoessel, F.; Baier, U.; Hellweg, S. Quantifying food losses and the potential for reduction in Switzerland. Waste Manag. 2013, 33, 764–773. [Google Scholar] [CrossRef]

- Dillman, D.A.; Smyth, J.D.; Cristian, L.M. Internet, Phone, Mail, and Mixed-Mode Surveys: The Tailored Design Method, 4th ed.; Wiley: New York, NY, USA, 2014. [Google Scholar]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879. [Google Scholar] [CrossRef] [PubMed]

- De Harlez, Y.; Malagueño, R. Examining the joint effects of strategic priorities, use of management control systems, and personal background on hospital performance. Manag. Account. Res. 2016, 30, 2–17. [Google Scholar] [CrossRef]

- Elbanna, S.; Eid, R.; Kamel, H. Measuring hotel performance using the balanced scorecard: A theoretical construct development and its empirical validation. Int. J. Hosp. Manag. 2015, 51, 105–114. [Google Scholar] [CrossRef]

- Dennehy, C.; Lawlor, P.G.; Gardiner, G.E.; Jiang, Y.; Shalloo, L.; Zhan, X. Stochastic modelling of the economic viability of on-farm co-digestion of pig manure and food waste in Ireland. Appl. Energ. 2017, 205, 1528–1537. [Google Scholar] [CrossRef]

- Rosa, F.S.; Lunkes, R.J.; Brizzola, M.M.B. Exploring the relationship between internal pressures, greenhouse gas management and performance of Brazilian companies. J. Clean. Prod. 2019, 212, 567–575. [Google Scholar] [CrossRef]

- Koivupuro, H.K.; Hartikainen, H.; Silvennoinen, K.; Katajajuuri, J.M.; Heikintalo, M.; Reinikainen, A.; Jalkanen, L. Influence of socio-demographical, behavioural and attitudinal factors on the amount of avoidable food waste generated in Finnish households. Int. J. Consum. Stud. 2012, 36, 183–191. [Google Scholar] [CrossRef]

- Visschers, V.H.M.; Wickli, N.; Siegrist, M. Sorting out food waste behaviour: A survey on the motivators and barriers of self-reported amounts of food waste in households. J. Environ. Psychol. 2016, 45, 66–78. [Google Scholar] [CrossRef]

- Marais, M.L.; Smit, Y.; Koen, N.; Lötze, E. Are the attitudes and practices of food service managers, catering personnel and students contributing to excessive food wastage at Stellenbosch University? S. Afr. J. Clin. Nutr. 2017, 30, 15–22. [Google Scholar] [CrossRef]

- Hebrok, M.; Boks, C. Household food waste: Drivers and potential intervention points for design-An extensive review. J. Clean. Prod. 2017, 151, 380–392. [Google Scholar] [CrossRef]

- Wang, L.; Liu, G.; Liu, X.; Liu, Y.; Gao, J.; Zhou, B.; Gao, S.; Cheng, S. The weight of unfinished plate: A survey based characterization of restaurant food waste in Chinese cities. Waste Manag. 2017, 66, 3–12. [Google Scholar] [CrossRef]

- Bido, D.S.; Silva, D.; Souza, C.A.; Godoy, A.S. Mensuração com indicadores formativos nas pesquisas em administração de empresas: Como lidar com multicolinearidade entre eles? Administração 2010, 11, 245–269. [Google Scholar]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: Los Angeles, CA, USA, 2016. [Google Scholar]

- Bisbe, J.; Otley, D. The effects of the interactive use of management control systems on product innovation. Account. Organ. Soc. 2004, 29, 709–737. [Google Scholar] [CrossRef]

- Gerdin, J. The impact of departmental interdependencies and management accounting system use on subunit performance. Eur. Account. Rev. 2005, 14, 297–328. [Google Scholar] [CrossRef]

- Strotmann, C.; Göbel, C.; Friedrich, S.; Kreyenschmidt, J.; Ritter, G.; Teitscheid, P. A participatory approach to minimizing food waste in the food industry-A manual for managers. Sustainability 2017, 9, 66. [Google Scholar] [CrossRef]

- Silvennoinen, K.; Heikkilä, L.; Katajajuuri, J.M.; Reinikainen, A. Food waste volume and origin: Case studies in the Finnish food service sector. Waste Manag. 2015, 46, 140–145. [Google Scholar] [CrossRef]

- Goh, E.; Jie, F. To waste or not to waste: Exploring motivational factors of Generation Z hospitality employees towards food wastage in the hospitality industry. Int. J. Hosp. Manag. 2019, 80, 126–135. [Google Scholar] [CrossRef]

- Mondéjar-Jiménez, J.A.; Ferrari, G.; Secondi, L.; Principato, L. From the table to waste: An exploratory study on behaviour towards food waste of Spanish and Italian youths. J. Clean. Prod. 2016, 138, 8–18. [Google Scholar] [CrossRef]

- Cicatiello, C.; Franco, S. Disclosure and assessment of unrecorded food waste at retail stores. J. Retail. Consum. Serv. 2020, 52, 101932. [Google Scholar] [CrossRef]

- Eriksson, M.; Strid, I.; Hansson, P.A. Food waste reduction in supermarkets–Net costs and benefits of reduced storage temperature. Resour. Conserv. Recycl. 2016, 107, 73–81. [Google Scholar] [CrossRef]

- Stancu, V.; Haugaard, P.; Lähteenmäki, L. Determinants of consumer food waste behaviour: Two routes to food waste. Appetite 2016, 96, 7–17. [Google Scholar] [CrossRef] [PubMed]

- Bamber, L.S.; Jiang, J.; Wang, I.Y. What’s my style? The influence of top managers on voluntary corporate financial disclosure. Account. Rev. 2010, 85, 1131–1162. [Google Scholar] [CrossRef]

- Ran, G.; Fang, Q.; Luo, S.; Chan, K.C. Supervisory board characteristics and accounting information quality: Evidence from China. Int. Rev. Econ. Financ. 2015, 37, 18–32. [Google Scholar] [CrossRef]

- Amran, N.A.; Yusof, M.A.M.; Ishak, R.; Aripin, N. Do characteristics of CEO and Chairman influence Government-Linked Companies performance? Procedia Soc. Behav. Sci. 2014, 109, 799–803. [Google Scholar] [CrossRef]

- Menegazzo, G.D.; Lunkes, R.J.; Mendes, A.; Schnorrenberger, D. Relação entre características demográficas dos gestores e uso de informações para tomada de decisões: Um estudo em micro e pequenas empresas. J. Glob. Compet. Gov. 2017, 11, 90–110. [Google Scholar] [CrossRef]

- Lunkes, R.J.; Pereira, B.D.S.; Santos, E.A.; Rosa, F.S. Analysis of the relationship between the observable characteristics of CEOs and organizational performance. Contaduría Adm. 2019, 64, 1–22. [Google Scholar] [CrossRef]

{kind=link}

| Panel A—Respondent Characteristics | |||||

| Academic education | High school | 82 | Gender | Female | 79 |

| Graduate | 119 | Male | 127 | ||

| MBA | 5 | Age (years) | 21–30 | 29 | |

| Tenure (years) | Up to 5 | 95 | 31–40 | 92 | |

| 6–10 | 66 | 41–50 | 40 | ||

| +10 | 63 | 51–60 | 31 | ||

| Over 61 | 8 | ||||

| Panel B—Restaurants Characteristics | |||||

| Number employees | Up to 100 | 34 | Food service (style) | À la carte | 65 |

| +100 | 183 | Buffet (kg) | 11 | ||

| Number seats | To 20 | 143 | Buffet free | 25 | |

| 21–40 | 57 | À la carte and buffet | 71 | ||

| 41–60 | 4 | Buffet (kg) and buffet free | 29 | ||

| 61–80 | 1 | Prato done | 3 | ||

| +81 | 1 | Other | 2 | ||

| Variables | Description |

|---|---|

| Perceived Utility of MCS (Broad-Scope) | Information characteristics: (i) past and future facts, (ii) internal and external information, (iii) financial and non-financial information, and (iv) short-term and long-term thinking. |

| Use of FW Information | Food waste information use: (i) monitor internal compliance, (ii) internal processes, (iii) internal decision-making, (iv) external reports. |

| Financial Performance | Perception of the financial performance of the restaurants: involves operating, net revenue, and return on investment. |

| Non-Financial Performance | Perception of (i) customer satisfaction, (ii) quality of products and services provided, (iii) development or product and service innovation, and (iv) employee resources. |

| Control variables | Manager characteristics (age, gender, and education) and the restaurants (number of employees and seats, and business maturity). |

| Variable | Item | Loading | Cronbach’s Alpha | CR | AVE |

|---|---|---|---|---|---|

| Perceived Utility of MCS (Broad-Scope) | Deb1 | 0.836 | 0.860 | 0.837 | 0.565 |

| Deb2 | 0.743 | ||||

| Deb3 | 0.657 | ||||

| Deb4 | 0.758 | ||||

| Use of Food Waste Information | Use1 | 0.717 | 0.815 | 0.853 | 0.592 |

| Use2 | 0.804 | ||||

| Use3 | 0.719 | ||||

| Use4 | 0.832 | ||||

| Non-Financial Performance | Nof1 | 0.840 | 0.880 | 0.908 | 0.713 |

| Nof2 | 0.878 | ||||

| Nof3 | 0.836 | ||||

| Nof4 | 0.821 | ||||

| Financial Performance | Fin1 | 0.910 | 0.904 | 0.938 | 0.835 |

| Fin2 | 0.939 | ||||

| Fin3 | 0.890 |

| Broad-Scope MCS | Use of Food Waste Information | Financial Performance | Non-Financial Performance | |

|---|---|---|---|---|

| Perceived Utility of MCS (Broad-Scope) | 0.751 | |||

| Use of Food Waste Information | 0.356 | 0.770 | ||

| Financial Performance | 0.088 | 0.261 | 0.914 | |

| Non-Financial Performance | 0.137 | 0.325 | 0.498 | 0.844 |

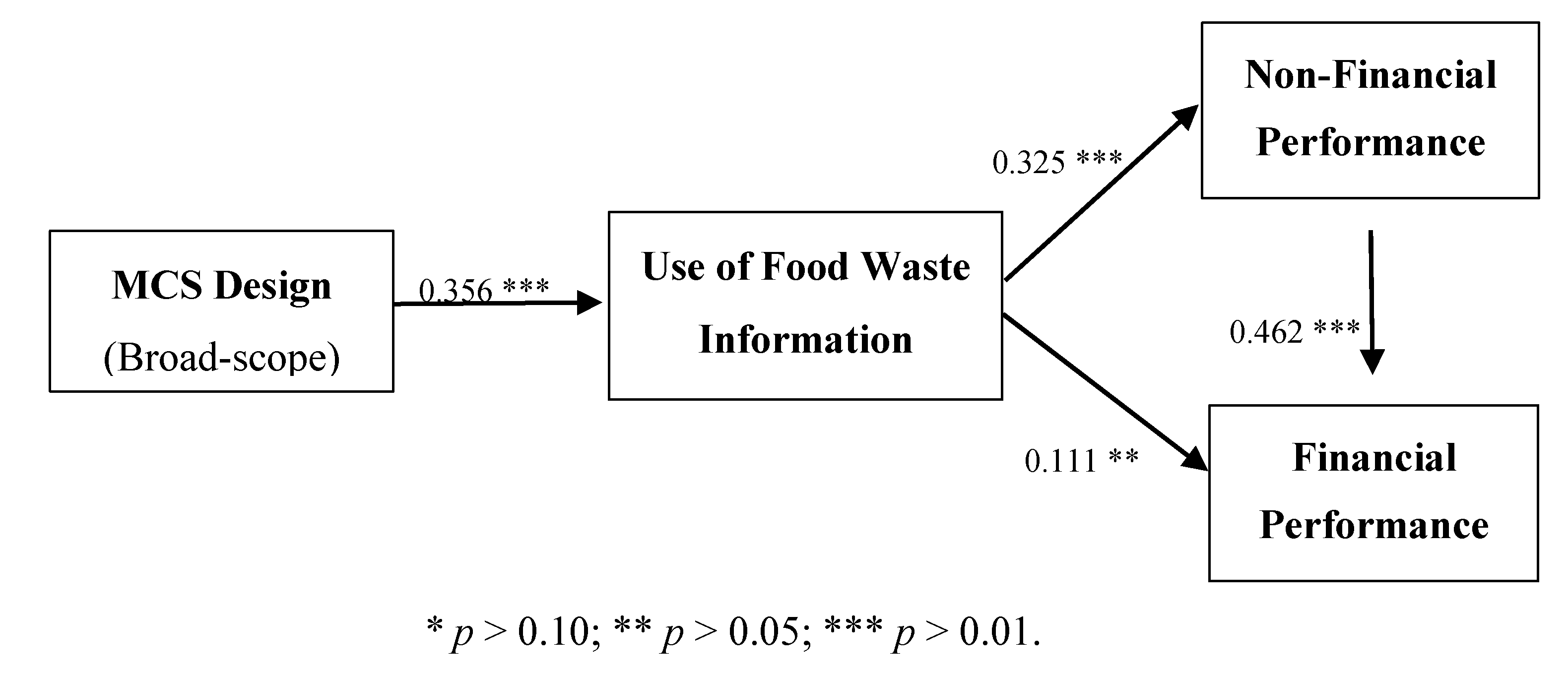

| Original Sample (O) | T Statistics (|O/STDEV|) | P Values | |

|---|---|---|---|

| Perceived Utility of MCS (Broad-scope) -> Use of Food Waste Inf. | 0.356 | 4.921 | 0.000 *** |

| Use of Food Waste Inf._ -> Financial Performance | 0.111 | 2.039 | 0.041 ** |

| Use of Food Waste _Inf. -> Non-Financial Performance | 0.325 | 4.265 | 0.000 *** |

| Non-Financial Performance -> Financial Performance | 0.462 | 6.019 | 0.000 *** |

| Panel A—Manager Control Variables | ||||||

| Relations | Age | Gender | Education | |||

| Less Than or Equal to 30 years | More Than 30 years | Male | Female | Background in Business | Other Education | |

| MSC-Sco→UseFW | 0.404 | 0.395 *** | 0.318 *** | 0.377 *** | 0.355 *** | 0.595 *** |

| UseFW→FinPerf | 0.192 | 0.096 | 0.147 * | 0.100 | 0.153 *** | 0.080 |

| UseFW→Non-FinPerf | 0.396 ** | 0.319 *** | 0.265 * | 0.364 *** | 0.406 *** | 0.020 |

| Non-FinPerf→FinPerf | 0.596 *** | 0.441 *** | 0.488 *** | 0.452 *** | 0.412 *** | 0.545 ** |

| Panel B—Restaurants Control Variables | ||||||

| Relations | Employers | Seats | Business Maturity | |||

| Up to 10 employers | +10 employers | Up to 100 seats | +100 seats | Up to 10 years | +10 years | |

| MSC-Sco→UseFW | 0.458 *** | 0.345 *** | 0.364 *** | 0.473 *** | 0.426 *** | 0.389 *** |

| UseFW→FinPerf | 0.174 *** | 0.079 | 0.184 *** | −0.003 | 0.216 *** | 0.127 |

| UseFW→Non-FinPerf | 0.228 * | 0.400 *** | 0.359 *** | 0.210 | 0.329 *** | 0.258 *** |

| Non-FinPerf→FinPerf | 0.643 *** | 0.312 *** | 0.471 *** | 0.475 *** | 0.681 *** | 0.272 ** |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lunkes, R.J.; Rosa, F.S.d.; Lattanzi, P. The Effect of the Perceived Utility of a Management Control System with a Broad Scope on the Use of Food Waste Information and on Financial and Non-Financial Performances in Restaurants. Sustainability 2020, 12, 6242. https://doi.org/10.3390/su12156242

Lunkes RJ, Rosa FSd, Lattanzi P. The Effect of the Perceived Utility of a Management Control System with a Broad Scope on the Use of Food Waste Information and on Financial and Non-Financial Performances in Restaurants. Sustainability. 2020; 12(15):6242. https://doi.org/10.3390/su12156242

Chicago/Turabian StyleLunkes, Rogério João, Fabricia Silva da Rosa, and Pamela Lattanzi. 2020. "The Effect of the Perceived Utility of a Management Control System with a Broad Scope on the Use of Food Waste Information and on Financial and Non-Financial Performances in Restaurants" Sustainability 12, no. 15: 6242. https://doi.org/10.3390/su12156242

APA StyleLunkes, R. J., Rosa, F. S. d., & Lattanzi, P. (2020). The Effect of the Perceived Utility of a Management Control System with a Broad Scope on the Use of Food Waste Information and on Financial and Non-Financial Performances in Restaurants. Sustainability, 12(15), 6242. https://doi.org/10.3390/su12156242