Abstract

Environmental degradation is a serious global issue that has received increasing attention from scholars, policymakers, regulators, environmental activists, and the public as a whole. In the meantime, corporations have been criticized as major contributors to environmental pollution. Environmental accounting (EA) is a corporate practice that seeks to account for the cost of environmental impacts of business operations. However, it is questionable whether the true cost of environmental impacts of business operations is accounted for in the conventional accounting systems. In order to shed more light on this issue, this study examines key drivers of managerial intention to engage in EA practices in Sri Lanka. We employ the theory of planned behavior to conceptualize the antecedents of managers’ intention to engage in EA practices. The results of the partial least square structural equation model (PLS-SEM) evaluation revealed that managers’ intention is significantly influenced by the attitudes towards EA practices, subjective norms, and perceived behavioral control. Our results also indicate that a larger proportion of the variance of perceived behavioral control is explained by the perceived cost and complexity, perceived regulatory pressure, and organizational environmental orientation. The findings of this study provide important theoretical and practical implications for scholars, managers, and policymakers.

1. Introduction

Rapid industrialization, along with the increased globalization, has led to far-reaching, detrimental effects on the natural environment, such as environmental pollution and contamination, and sharp depletion of natural resources. Corporations, as a major source of environmental degradation [1], are now under immense pressure to undergo necessary reforms that ensure environmental preservation while achieving their financial goals [2]. Sustainable development has, thus, become indispensable for every organization to survive in the modern era [3]. Scholars have forwarded various concepts to promote sustainable development, among which environmental (green) accounting is one such concept that aims to incorporate the cost of the ecological impact of companies’ operations into conventional accounting systems. Schaltegger and Burritt [4] (p. 30) define environmental accounting as a “branch of accounting that deals with activities, methods, and systems; recording, analysis, and reporting; and environmentally induced financial impacts and ecological impacts of a defined economic system.” Environmental accounting (EA), in this way, incorporates environmental costs into the financial results of a company’s operations. This would help the companies to understand the magnitude of the impact of companies’ operations on the natural environment. Moreover, with the EA reports, business owners and managers will develop a better sense of their environmental expenditures, which is the first step towards strategic management and innovative planning for controlling these expenditures. Furthermore, it provides a holistic picture of the overall financial position and increases the awareness of management and other shareholders about the true cost of natural resources consumed in making revenues [5]. The EA practice, therefore, is seen as an essential component of the environmental decision-making process within the corporate sector [6]. The present study examines how well corporate managers in the developing world have perceived these benefits and how such perceptions shape their behavioral intentions towards EA practices.

The importance of EA is also reflected in the recent proliferation of rules and regulations that mandate companies to establish EA practices and to disclose environmental information for the reference of their stakeholders [3]. Countries like Denmark, Netherland, the US, and Japan have promulgated specific laws requiring companies to disclose environmental information. Multinational corporations are now evaluating their suppliers in terms of environmental performance and its disclosure before entering into business agreements [3,7]. However, despite all these efforts, major corporate scandals, such as the Volkswagen emissions scandal, Deepwater Horizon oil spill, Kobe steel scandal, and iPhone battery scandal, have raised serious concerns about the adoption and compliance with these regulations and the best practices within the corporate sector. In addition, these incidents shake stakeholders’ confidence in corporate conduct, which may have a widespread impact on the entire corporate sector. From the accounting standpoint, these scandals stress the importance of EA implementation. Some practitioners argued that the potential cost of environmental contingencies such as the Deepwater Horizon oil spill could have been estimated if a proper EA system was in place [5]. They further argue that massive financial losses (i.e., fines, penalties, loss of market value) associated with these environmental catastrophes could have been prevented with proper EA practices. However, implementation of such best practices (i.e., EA practices) within corporate sectors depends upon several factors, ranging from countries’ political, economic, and legal environments to corporate managers’ cognitive and psychological factors [8,9,10]. Therefore, a thorough investigation of these factors is inevitably needed, since the identification of key factors is the first step towards developing and implementing the necessary policies.

Although scholars have made substantial efforts to theorize the concept of EA [11,12], most empirical studies are largely narrowed around the disclosure issues of the corporate sector [9]. These studies predominantly focus on environmental disclosure and firm performance [10,13], determinates of environmental disclosure, level of environmental disclosure [14,15], development of disclosure indices [16,17], etc. However, the managerial side of EA implementation is often overlooked [18,19,20]. Few studies have investigated the managerial perspectives of other accounting and reporting practices related to sustainable development, such as sustainable reporting and corporate social responsibility reporting [8,18,21]. This specific issue of managers’ behavioral intention to engage in EA implementation, to the best of our knowledge, has not yet been studied in the accounting literature. Given this paucity of studies, there is a strong need to look at managers’ viewpoints, thus broadening the horizons and empirical evidence related to the subject matter. It is indeed a problem for managers to adopt a practice while ensuring the profitability of the business. Looking at this issue from the managers’ viewpoint can give an idea about pertinent hindrances to the adoption of EA practices by businesses. Thus, for recommending a suitable implementation strategy, it is important to analyze the current perceptions and attitudes of managers towards the EA practice for corporate sustainability. Therefore, the main objective of this study is to investigate the behavioral intentions of managers to engage in EA practices using a theory triangulation approach. To this end, theories such as neo-institutional theory [22], stakeholder theory [23], and legitimacy theory [24] explain why EA practices are important and how EA practices are diffused among companies [25], while the theory of planned behavior (TPB) provides the theoretical basis for conceptualizing managerial intentions towards EA practices. The TPB, with its roots in social psychology, tries to explain why people would favor one action over the other [26,27]. This will help to uncover factors that support or converse with the idea of EA in a business, which, in turn, provides an understanding of how EA can be promoted in the corporate industry and what regulatory measures need to be taken in order to make it an obligation for all applicable businesses.

While this study addresses the existing research gaps concerning the managerial aspect of EA implementation, it tries to apply novel theoretical approaches in the context of EA as a response to the call of Gray et al. [28] and Parker [19,20] for additional research in social and environmental accounting using psychology theories. This study is also motivated by the prevalent environmental issue in Sri Lanka, whose magnitude has grown considerably over the years [29]. Previous studies have found that the majority of business enterprises in Sri Lanka have neglected environmental restoration [30]. However, recently, public awareness and concern about environmentally harmful activities are growing in Sri Lanka and several other developing countries, making it an important topic of discussion within the corporate sector [31]. In Sri Lanka, public opinion is now forcing a radical change in corporate practices, and environmental restoration is now also appearing in electoral campaigns. These changing dynamics motivate the need for research to understand the internal and external drivers for EA practices in the developing countries, where businesses are just stepping into their role in protecting the environment.

This study contributes to the literature in three ways. First, this study can be considered as one of the first studies to extend the current empirical evidence related to EA practices from a socio-psychological context. Hence, in contrast with previous studies that are narrowed around EA goals, measures, and disclosure issues [8,18,32,33,34,35], this study fills the gap in the literature by providing pieces of evidence on the antecedents of managers’ behavioral intentions to engage in EA, making a significant theoretical contribution. The intensity of sustainable practices by a firm rests heavily on the green climate of an organization [36], and managers’ attitudes and intentions towards such practices are essential components of it [8,18]. Thus, by providing the managers’ perspectives related to EA implementation, this research has shed light on the underlying issues that revolve around the EA practice and its implementation. Second, this study demonstrates the usefulness of behavioral theories in explaining the importance of managers’ attitudes, perceptions, and intentions in the domain of EA practices. Linking the dimensions of TPB with other theories pertaining to EA practices, such as neo-institutional theory, stakeholder theory, and legitimacy theory, this study shows that managerial attitudes, subjective norms, and perceived behavioral control are significant predecessors to managerial intention to engage in EA practices. In addition, the integration of novel constructs, such as perceived cost and complexity, regulatory pressure, and organizational environmental orientation to TPB, in explaining managerial intentions towards EA practices is also a significant contribution to the literature. Third, the use of a novel approach, a partial least square structural equation modeling technique (PLS-SEM), in the context of EA for the assessment of socio-psychological parameters involved in the implementation of EA, can be considered as the methodological contribution of this study. The PLS-SEM approach is widely used in marketing and strategic management disciplines, but is rarely used in the EA context. This study shows the plausibility of the application of PLS-SEM in the context of EA. Furthermore, the majority of the previous research focused on developed countries, where there is a strong sense of environmental restoration and strict regulations towards it. On the contrary, many of the underdeveloped countries do not have the same favorable atmosphere to push strong environmental ethics, and, therefore, providing managerial perspective and intention from a developing country will contribute to expanding the present empirical evidence pertinent to the EA.

The remainder of this paper is organized as follows: Section 2 discusses the research context and the link between EA and corporate sustainability, and provides a theoretical framework and rationale for hypothesis development. Section 3 outlines the research methods of the study. In Section 4, the results of the PLS-SEM analysis are presented. Section 5 provides the results and discussion, followed by the conclusions, implications, and limitations in Section 6.

2. Literature Review

2.1. Sri Lanka as the Research Context

Sri Lanka is an island nation with a population of a little over 21 million, a per capita income of around 4000 USD, and is considered a developing country in South Asia. After the end of the civil war in 2009, which lasted some 30 years, the Sri Lankan economy has experienced a continued economic growth, which was recorded at an average rate of 5.6% over the last decade [37]. The Sri Lankan economy is moving from a mainly rural economy to a more urbanized, manufacturing, and service-oriented economy. The socio-economic indicators rank among the highest in South Asia and are good in comparison with middle-income countries. The national poverty rate has decreased over the years and was recorded at 4.1% in 2019. Economic growth has led to shared prosperity, and extreme poverty is rare; however, a relatively large proportion of the population remains slightly above the poverty line [37].

Environmental preservation is at the core of Sri Lankan culture, which has been shaped by Buddhist teachings for over 2600 years [8]. The conservation of resources, the preservation of wildlife, and the prudent use of natural resources are some of the values instilled in society as a predominantly Buddhist country. This is reflected in the conservation of natural habitats in 15 National Parks and the Strict Nature Reserve, which account for 13% of the landmass in the country [8]. In addition, the declaration of eight World Heritage Sites related to Buddhism by the United Nations Educational, Scientific, and Cultural Organization (UNESCO) provides further evidence of environmental values in Sri Lanka [38].

However, despite the long-standing social value and environmental preservation, the recent economic transition towards a more manufacturing- and service-based economy with the concept of profit maximization has led to the observation of a widespread negative impact on the natural environment in Sri Lanka. For instance, the Kelani River, which remains a vital resource for some 25% of the population of Sri Lanka, is considered to be the most polluted river in the country [39]. According to the Central Environmental Authority (CEA) in Sri Lanka, most of the pollution comes from liquid waste discharged by about 3000 businesses operating alongside the river [39]. In addition, a survey by the Asia Foundation and the Environmental Foundation Limited, a local nonprofit organization, has identified 150 sources of pollution, mainly from industries involved in food production, beverages, ceramics, textiles and clothing, oil refining, tanning, fertilizers, and plastics [39]. This is clear evidence that environmental conservation has been ignored by the corporate community in Sri Lanka. Thus, the trade-off between ecological preservation and profit maximization in the face of fierce competition between corporate industries is unclear. Factors such as economic turbulence, unstable exchange rates, political turmoil, and inadequate regulatory enforcement may also have compromised environmental protection over economic benefit maximization [40]. This is where research is needed to understand the factors that impel or impede the managerial intention to implement environmentally friendly practices, including EA.

2.2. Environmental Accounting and Corporate Sustainability

Considerable effort has been put towards environmental accounting over the past decade, and it has been linked to business efficiency and corporate sustainability [41,42]. According to Maama and Appiah [43], the environmental or green accounting practices allow managers to focus on non-monetary and quality measures, which may remain shadowed in traditional accounting practices. Thus, accounting for improved environmental practices would also help to achieve improved operational efficiency for the business. Wild and van Staden [44] note that the conventional accounting principles are only concerned with the monetary transactions; however, when businesses create their annual reports, they are based on both monetary and non-monetary data. Several quality issues that are identified during the annual reporting process could have been identified earlier by extending the nature of the accounting practices. Looking for stakeholders’ perspectives, Modell [45] notes that environmental accounting can help managers to provide a more holistic and meaningful representation of the business to its stakeholders.

There has been growing evidence of the role of environmental managerial accounting (EMA) in keeping a balance of the financial and non-financial information regarding the environmental impact of an organization [32]. Some of the common tools that are used for EMA are environmental cost accounting, full cost accounting, environmental lifecycle budgeting, and material and energy flow accounting [46]. The significance of these tools is that they try mapping resources with the business outcomes and the budget spent on them. Explaining the use of environmental lifecycle budgeting, Vejzagic, Brown, and Schmidt [47] propose that many organizations are oblivious to the lifecycles of their purchased resources, and often fail to realize their full value. This results in a lower benefit–cost ratio, and organizations keep on spending more to purchase more resources, rather than optimizing the lifecycle and usability of their resources. This is where environmental accounting practices can help managers achieve a better understanding of business purchases, consumption, and outcomes.

The primary goal of environmental accounting remains on policies and practices for environmental protection. Maama and Appiah [43] state that companies are often aware of the impact of their business operations on the environment. Only when they assess the impact of their business on the environment, they come to know how environmentally friendly or destructive their practices are. Therefore, the first step towards environmental restoration is to identify practices with a high impact on the environment, and then account for their costs and alternatives [43]. With the growing concern of stakeholders towards eco-friendly practices, there is an increasing need for managers to not only account for the monetary transactions, but also the overall impact of the business operations on the environment and plans for improved environmental practices [48]. However, this is not always the case due to the weak and blurred regulations towards environmental protection.

The question remains as to how EA can contribute to achieving corporate sustainability. According to Gray [49], the three pillars of corporate sustainability are economic, social, and environmental sustainability. However, the balance between the three areas is hard to achieve. For this reason, businesses need to designate corporate targets in the environmental and social dimensions. If companies would use the same matrix to measure their returns from economic investments as that for the investments towards environmental goals, they would always see environmental investment as an expense rather than an asset [50]. It is for this reason that EA needs to be embedded into the corporate system as a separate entity, where environmental protection measures are inferred as obligatory and a parameter for achieving sustainability.

2.3. Theoretical Framework

The theory of reasoned action (TRA) and TPB form the foundation of the theoretical framework for the study. The TRA concerns the attitude and subjective forms that affect the behavioral intentions of a person [51]. Öze and Yilmaz [52] explain that the cost and benefits attached to a decision shape the attitudes of managers toward the decision and, in turn, affect their behavioral intention for that decision. Attitudes can be shaped by internal factors like experience or external factors like regulations or norms. So, the premise of the TRA rests on the notion that understanding the internal and external factors that govern the attitude and subjective norms would give an understanding of the behavioral intention [26]. The TPB extends the boundaries of the TRA by adding the variable of “perceived behavioral control” to the TRA model. Explaining the notion of the TPB, the authors of [53] state that the resources and opportunities individuals think that they possess also govern their behavior. The greater the resources, the higher will be the perceived behavioral control, governing the intention.

The relevance of the TPB is evident in the context of EA, as managers’ intentions towards a practice are shaped by factors such as industry/subjective norms, regulations, organizations’ policies, and the perceived cost, benefit, and complexity of the practice [8,21]. If a corporate practice offers great benefits with low cost and complexity, there is a high probability that managers will have a positive behavioral intention towards it, and the opposite is also true for high-cost–low-benefit practices. Similarly, the implementation of certain corporate practices depends upon the acceptance and encouragement of those practices by influencing people within and around the company. Furthermore, the manager’s capacity (i.e., skills, experience, opportunity) to perform the behavior is also an important predictor of behavioral intention. Thus, the theoretical frameworks of the TPB govern behavioral understanding, which dictates whether or not a business would adopt the EA practice.

The notion that companies should follow the EA practices stems from the “legitimacy theory”, which explains organizational behavior in implementing corporate social responsibility (CSR) [24,54]. An organization has a contract to be fulfilled with its stakeholders, and there are documented mandates and regulations of how this contract shall be fulfilled. In a similar context, the legitimacy theory proposes a social contract that organizations need to abide by in order to fulfill their CSR [55]. This includes the recognition of their responsibility towards the environment and factual reporting of their efforts and shortcomings in meeting their social contract. According to Zyznarska-Dworczak [55], in the absence of a legitimacy rule, there will be no solid premise for governing socially responsible activities, and self-interest will govern the majority of the managerial decisions. In addition to the legitimacy theory, the “stakeholder theory” tries to build a connection between management practices and corporate sustainability [23]. The stakeholder theory extends the definition of business stakeholders to the local communities and environment or surroundings in which the business operates [56], all of which play their role in the long-term sustainability of the business.

Although there are several theories that can explain why and how sustainability management practices such as EA, EMA, and CSR are implemented in the corporate sector, an increasing number of studies suggest that neo-institutional theory offers the most useful framework for investigating the motivations and drivers that spur companies to adopt sustainability practices, including EA [40,57]. In our study, too, we get some insights from neo-institutional theory to identify the type of pressure exerted on companies that may alter conventional thinking, which ignores environmental preservation, of managers and leads to optimistic attitudes and behavioral intentions towards EA practices. According to neo-institutional theory, institutional isomorphism is the process by which organizations become homogeneous over time in terms of practices and procedures, irrespective of their effectiveness and rationality in the organizational context [22]. There are three types of institutional isomorphism [22], i.e., coercive isomorphism, mimetic isomorphism, and normative isomorphism.

The presence of multinational companies that follow the highest environmental standards, the regulatory agencies like CEA, foreign investors, non-governmental organizations, and industry norms may exert coercive pressure on the companies, which leads to coercive isomorphism [22,57]. Mimetic isomorphism occurs when the environment in which companies operate creates uncertainty, and, as results, companies model themselves after other companies [22]. The third mechanism, normative isomorphism, by which similarity of the practices and procedures among companies may occur, is a result of professionalization [22]. Recruitment of professionals from similar industries or in a narrow range of training institutions, as well as standard promotion and skill level criteria for specific jobs, may lead to normative isomorphism [57].

2.4. Hypothesis Development

An increasing number of studies have been directed towards the identification of factors that influence the implementation of various environmental practices within the corporate sector. Studies on EMA practices revealed that factors such as regulatory enforcement, stakeholders’ interests, professional networks, corporate environmental strategies, and financial conditions are key to the application of EMA [58]. Similar findings were reported by Yusoff et al. [59], where the primary drivers for EA and reporting were economical and financial incentives, need or culture of transparency, regulatory pressures, and availability of resources. Concerning the problem associated with environmental accounting and reporting (EAR) practices, Ahmad and Afzal [60] pointed out that the major problem faced by Bangladeshi companies for environmental reporting is lack of rules, regulations, and guidelines, lack of managerial support, lack of knowledge and training, and lack of favorable attitudes towards such practices. It seems that the implementation of EAR practices is largely influenced by resource availability, stakeholder pressure, regulatory pressure, and knowledge and training about the EAR.

Drawing on material accounting practices, Beierle [61] contended that the perceived costs of material accounting were higher than the perceived benefits. The perceived benefits were creating an information-rich decision environment and fulfilling the “right to know” of the company’s stakeholders. On the other hand, the perceived costs were the increased cost of environmental-impact-related data collection and reporting, risks of misplaced priorities, and the risk of unwanted use. Beierle noted that a community of full disclosure might not have any perceived advantage or return for the organization, resulting in managers avoiding EA for the community or as a whole. In his research on the EA practices of the pharmaceutical industries, Al-Nimer [62] found that more than 60% of the managers believe that an environmental impact report should be limited to the extent required by the management, and it is not advantageous to conduct a rigorous EA for public disclosure.

As discussed earlier, in the absence of regulatory pressures, socially responsible business practice will often come second to the economically profitable practices. Given the perceived cost and the absence of appropriate regulations, there is a high probability that managers would opt not to carry out the EA practice. In addition to this, the factor of availability of resources can be linked to the perceived behavior controls when shaping managerial intention. Yassin [63] further added that EA demands qualified personnel, and thus accountants, financial managers, and relevant staff should be provided with required education on the concepts and the general framework of EA. This requirement adds to the overall cost and complexity of EA. This further adds to the scenario of why businesses operating in less-developed regions are more likely to have a less favorable behavioral intention towards EA, considering their limited resources and the high complexity and cost requirements for EA.

The perceived factors drive the need and urgency of the EA practice. However, there is an evident lack of research mapping the perceived factors with the planned behavior of managers, which then shapes their behavioral intentions towards EA practices. While the TPB provides a framework for understanding the final behavior towards an objective, the factors driving the attitudes, subjective norms, and perceived behavioral control also need to be identified and coherently linked with the behavioral intention. The research methodology and hypotheses are built to address this research gap, mapping the perceived factors related to EA with the behavioral intentions of the managers to engage in EA practices.

2.4.1. Perceived Benefits, Cost, and Complexity of EA

According to Ajzen [64], attitudes towards specific behaviors refer to “the degree to which a person has favorable or unfavorable evaluation or appraisal of the behavior in question.” This means that an individual holds certain behavioral beliefs, and these beliefs linked the behavior to certain positive or negative outcomes [64]. These positive and negative outcomes that a person believes to have in a particular behavior form the attitudes towards the behavior. If the managers evaluate the outcomes that they believe in having in EA positively, then they acquire positive attitudes towards the EA practices. Conversely, if they have a negative evaluation of those outcomes, it automatically forms negative attitudes towards EA practices and, hence, a reluctance to engage in EA. For instance, if the managers believe that engaging in EA brings competitive advantages with the improved company reputation and that such competitive advantages are desirable, they are likely to hold positive attitudes towards EA. This is evident in the context of sustainability reporting. Thoradeniya et al. [8] found that the managers’ attitudes towards sustainability reporting are positive and have a significant influence on behavioral intention to engage in sustainability reporting when they have a positive evaluation of the outcome that they believe in having in sustainability reporting.

When the managers believe that engaging in certain practices would bring undesirable consequences, such as increased cost and increased complexity in systems, processes, and procedures, they are likely to have negative attitudes towards such practices. Mi et al. [21] argue that both the perceived benefit and effort positively influence the manager’s attitudes towards Corporate Social Responsibility (CSR) practices. They conceptualized the perceived effort as the ease of engaging in CSR practices. They further argued that the decision on whether or not to engage in CSR practices is subject to the perceived changes that a company has to undergo as a result of CSR practices. However, they concluded that there was an insignificant negative relationship between perceived effort and CSR practices while concluding that there was a significant positive relationship between perceived benefits and CSR practices.

While the costs and complexity involved in EA may influence the attitudes of managers, they may also be a barrier to perceived behavioral controls over EA practices. As perceived behavioral controls are dictated by the presence or absence of skills, resources, and opportunities required to perform the behavior in consideration, the limited availability of financial resources and a possible increase in complexity of accounting systems and procedures (see, for example, Tu and Huang [3]), requiring additional skillful human resources, may be seen as a perceived impediment to engaging in EA practices. Therefore, higher perceived cost and complexity involved in EA will lower the perceived behavioral control over the EA. Accordingly, managers’ perception of the benefits, cost, and complexity associated with EA would play a major role in the final decision-making process of whether or not to adopt the EA practices. This leads to the following hypotheses:

Hypothesis 1 (H1).

There is a positive relationship between perceived benefits and attitudes towards EA.

Hypothesis 2a (H2a).

There is a negative relationship between perceived cost/complexity and attitudes towards EA.

Hypothesis 2b (H2b).

There is a negative relationship between perceived cost/complexity and perceived behavioral control over EA.

2.4.2. Regulatory Pressure

The government implements and amends the environmental regulations from time to time in order to prevent and mitigate the adverse environmental practices of companies. Such regulations encourage businesses to participate effectively in environmental practices by providing companies with an array of guidelines, standards, and procedures that should be followed while conducting business operations. Even if the companies do not perceive that these regulations would ease their operations, they are forced to comply with them, since the non-compliance may bring them undesirable consequences, such as penalties and fines [8]. Failure to comply with environmental regulations may bring even more harm to a company, including damages to company image and customer relations. Considering the effect that environmental regulations can have on the companies, managers may implement various pro-environmental programs, including EA, to address the regulatory pressure.

Studies that investigated the regulatory pressures as a predecessor of behavioral intention have often conceptualized it as a normative factor [8,21]. However, another stream of studies argues that regulatory or government pressure could be seen as an external controlling factor rather than a normative factor [65]. In his study, Muthusamy [66] suggested that government pressure that comes from the various regulations on Malaysian companies to use forensic accounting services serves as an external controlling factor that shapes behavioral intention towards forensic accounting services. This idea is also supported by the innovation adoption studies. Applying the TPB as their theoretical framework, Tan and Teo [67] found that government intervention as an external controlling factor had a significant influence on the intention to adopt internet banking services. From an innovation adoption standpoint, Kuan and Chau [68] found that government pressure had a significant influence on the small business electronic data interchange (EDI) adoption in Hong Kong. They further emphasized that this pressure came from the government’s decision to terminate paper submission for import and export declarations. Following these arguments, we also assume, with its faciliatory role, that regulatory pressure may influence the intention to engage in EA through perceived behavioral control. This leads to the following hypothesis:

Hypothesis 3 (H3).

There is a positive relationship between regulatory pressure and perceived behavioral control.

2.4.3. Organizational Environmental Orientation

The existing organization’s environmental orientation may influence the manager’s behavioral intention to engage in EA practices. Environmental orientation can be defined as how well a firm has recognized its responsibility towards the natural environment [69], and it is reflected in their mission statement and policies. Having an environmentally favorable mission, policies, and procedures may facilitate the implementation of best environmental practices within the organization, including EA. In addition, companies that have already adopted advanced environmental management practices, such as eco-label systems, product life cycle analyses, and environmental audits, may require environmental information in order to assess their environmental performance [70]. Therefore, implementation of EA practices in these companies may be easier, and, hence, perceived behavioral control over EA implementation is higher than the companies without such practices.

Another avenue through which environmental orientation can affect managers’ perceived control over the implementation of EA is the link between environmental orientation and pro-environmental culture or climate. Scholars have argued that environmental orientation can be seen as a kind of pro-environmental culture or climate [36,71]. There is a myriad of evidence that pro-environmental culture or climate has a significant influence on the individual’s pro-environmental behavior within an organization [2,72,73]. Drawing on behavioral norm-activation theory, Chou [72] showed that green organizational climate has a moderating effect on employees’ environmental beliefs, norms, and environmental behavior. In their study, a green organizational climate was defined as an organization’s perceived environmental policies and practices. This seems perceived as environmental policies and practices of a firm encourage/discourage the individuals, including managers, towards pro-environmental behavior. Therefore, if a firm has already adopted environmentally friendly policies and practices, which will encourage and facilitate managers to implement further environmental practices such as EA within the organization, this leads to the following hypothesis.

Hypothesis 4 (H4).

There is a positive relationship between a firm’s environmental orientation and perceived behavioral control.

2.4.4. Subjective Norms

Researchers have tried to draw a relationship between subjective norms and behavioral intention. Subjective norms reflect an individual perception of social norms, pressures, ethics, and expectations [52,53]. This leads to the assumption that individuals are more likely to adopt a behavior that is regarded as desirable by the significant others. This indicates that environmental practices and ethics followed by the key stakeholders are likely to affect managers’ behavioral intentions towards EA. Several studies have confirmed a relationship between subjective norms and behavioral intention. For example, a study conducted on consumer buying intention of organic food found an indirect relation between subjective norms and intention through attitude formation [74]. Similarly, the authors of [21] revealed that subjective norms are significant predictors of CSR practices. They also showed that attitudes towards CSR practices are significantly influenced by subjective norms. The relationship between subjective norms and behavioral intention has been proven by several other studies related to accounting and financial reporting discipline (see, for example, [8,75,76]). This leads to the hypothesis that subjective norms indirectly influence behavioral intention through attitude and perceived behavioral control, while being directly related to the behavioral intention.

Hypothesis 5a (H5a).

There is a positive relationship between subjective norms and intention to engage in EA.

Hypothesis 5b (H5b).

There is a positive relationship between subjective norms and attitudes towards EA.

Hypothesis 5c (H5c).

There is a positive relationship between subjective norms and perceived behavioral control.

2.4.5. Attitudes towards EA

Attitude is a key antecedent of intention to act and reflects one’s overall assessment of an issue at hand [64]. Many researchers have explained attitude in terms of positive–negative or favorable–unfavorable towards a given issue [77,78]. A positive attitude is often mapped to a favorable intention or a supportive behavior towards an act, while the reverse of it is also true [77]. The discussion of attitude is important, as the perceived benefits, costs, and complexity not only shape a company’s culture, but also the attitude of managers, who are the decision-makers at the end [75]. The relationship between managers’ attitudes and behavioral intentions towards certain accounting and reporting practices is evident in the extant accounting literature. Thoradeniya et al. [8] revealed that the managers’ attitudes regarding the values of sustainability reporting are significantly associated with their behavioral intention to engage in sustainability reporting. These findings were supported by [75], where they found that professional accountants’ attitudes towards sustainability reporting are positively associated with their intention to engage in sustainability reporting. However, they conclude that this association is statistically insignificant. Given the evidence that supports the positive relationship between attitudes and behavioral intention to engage in certain accounting practices, the following hypothesis is proposed concerning EA.

Hypothesis 6 (H6).

There is a positive relationship between attitudes towards EA and intention to engage in EA.

2.4.6. Perceived Behavioral Control

Perceived behavioral control includes the perception of personal capability and the sense of control over the behavior. Researchers have found a link between the perceived behavioral control and the ability to perform a task [8,64,75]. The extant studies have forwarded the idea that the managers’ control over and willingness to engage in certain corporate practices depend on factors such as resources and time availability, skills, knowledge, and experience they possessed, continuous training and improvement, and effective communication [75]. Therefore, the implementation of EA practices appears to be unlikely in the absence of these factors, even if corporate managers have a positive attitude towards EA and the pressure from significant others. The studies from accounting and reporting disciplines support the notion that perceived behavioral control is positively associated with behavioral intention. The authors of [75] and Thoradeniya et al. [8] revealed that professional accountants’ (former) and corporate managers’ (latter) behavioral intentions to engage in sustainability reporting were significantly and positively associated with perceived behavioral control. Based on this evidence, we propose the following hypothesis.

Hypothesis 7 (H7).

There is a positive relationship between perceived behavioral control and intention to engage in EA.

3. Research Methods

3.1. Data Collection

Data were collected using a questionnaire, which was developed following the approach suggested by Dillman, Smyth, and Christian [79] and the previous studies adopting a questionnaire based on the TPB and TRA [8,75]. We opted to select managing directors (MDs), chief executive officers (CEOs), and other key management personnel of listed and non-listed companies as the respondents for the questionnaire survey. The top-level managers are presumed to be responsible for adopting various practices in companies in the realization of their objectives. This study used both mail and internet surveys for the data collection. Mail and internet surveys are considered to be desirable and advantageous for a study of this scale, as they mitigate the problems of interviewer bias and social desirability bias [80,81]. Moreover, this method is rather practicable for collecting data from a large sample.

Initially, the sample of the study included 282 potential respondents from the companies listed in the Colombo Stock Exchange (CSE) in Sri Lanka and 1218 respondents from private companies (non-listed) in Sri Lanka. For the data collection, the mail survey method was used for listed companies, while a Google-doc-based email survey was used for non-listed companies. The postal addresses of listed companies were collected from their official websites, and email addresses of non-listed companies were accessed from several sources, such as the Sri Lanka Telecom (SLT) Rainbow Pages online directory and Kompass Sri Lanka Directory.

Before the final survey was conducted, the questionnaire was pre-tested among a sample of 50 respondents, including 20 university lecturers and 30 managers of listed companies. We made minor modifications in the wordings of the items included in the questionnaire based on the responses and suggestions received from the participants of the pilot study. This procedure allowed us to establish the external validity of the questionnaire.

The final survey was administered during March 2019 and August 2019. After three weeks of initial distribution, the first reminder was sent to both the public and private companies. However, around 300 email addresses were found to be incorrect, and the same were excluded from the first reminder onwards. A second follow-up was conducted after about eight weeks of the initial distribution. At the end of August 2019, a total of 254 questionnaires were received from both the mail (98) and internet (156) survey respondents. However, three paper-based responses were incomplete, and five web-based responses appeared irrational due to the fact that all of the responses were recorded as moderate (i.e., recorded as 4 on a 1 to 7 scale), and these were therefore eliminated from the analysis. This resulted in 246 usable responses and an overall response rate of 16.4%. We conducted the test for non-response bias using early and late responses, the results of which indicate that there is no significant difference between early and late responses.

The background analysis of the respondents showed that 28.34% of the responses were received from the manufacturing industry, followed by hotels and travel (20.47%) and banking, finance, and insurance (17.32%). Most of the respondents were top-level managers, 22.44% of which were managing directors. However, the responses from the chairmen were as low as 3.14%. As for the numbers of employees, the majority of the responses (32.67%) were received from companies with 101–250 employees. Responses from companies with more than 3000 employees were 7.1%.

3.2. Development of the Survey Instrument

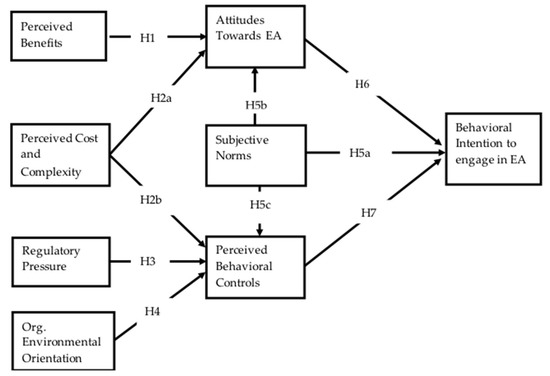

Each construct in the research model (Figure 1) was measured by using multiple items, consistently with previous studies. Thoradeniya et al. [8] stated that psychological concepts, such as perception, attitudes, and intention, cannot be measured with a single indicator. Accordingly, we included four items in the following construct: Attitudes towards EA, subjective norms, perceived behavioral controls, and behavioral intention to engage in EA practices, according to Kwakye et al. [75] and Thoradeniya et al. [8]. The measurement scale used in these studies is directly related to the accounting and reporting discipline, and is hence considered more suitable for the EA context. Durocher and Fortin [76] developed a scale consisting of five items in measuring perceived cost and complexity in the early adoption of International Financial Reporting Standards (IFRS), and the same was used in this study to measure the perceived cost and complexity involved in EA implementation. However, we made some minor modifications to the items to make them more appropriate for the present study. The perceived benefits associated with EA practices were measured using a four-item scale following Mi et al. [21]; they used this scale for measuring benefits associated with CSR practices. The measurement scales for the regulatory pressure were adopted from Wu et al. [82] and Chu et al. [83]. In their study, Wu et al. [82] conceptualized three types of institutional pressures, such as market, regulatory, and competitive pressure towards green supply chain management. In our study, however, we considered only regulatory pressure and, therefore, included only four items in the measurement scale. Organizational environmental orientation was measured using six items, which were adopted from Chou [72]. Overall, the questionnaire consisted of 35 questions that correspond to the items pertaining to each construct of the research model. Additionally, the questionnaire contained a question reflecting the job title, and two other questions for the industry sector and the number of employees. We used a seven-point Likert scale (1 = Strongly Disagree, 7 = Strongly Agree) to code the responses to the questions. The outline of the questionnaire is given in Appendix A.

Figure 1.

Conceptual model.

3.3. Data Analysis

This study is of an exploratory nature, in which the conceptual model developed intends to explore the antecedents of managers’ intentions to engage in EA practices and to determine the extent to which these antecedents impact the managers’ intentions. Previous studies suggest that the use of partial least square structural equation modeling (PLS-SEM) is more suitable when the goal of the developed model is to identify key drivers and to predict and explain the target constructs [84]. Accordingly, we adopted the PLS-SEM approach for data analysis using Smart PLS 3 software. Recently, PLS-SEM has been widely applied in different disciplines relative to covariance-based SEM (CB-SEM) due to its ability to handle complex models, flexibility in parametric assumption and sample size, high statistical power, and consistent estimation of parameters [84,85].

Following the procedure suggested by [84,85,86], first, we established the required criteria of the measurement model. For instance, we assessed the indicator loadings, internal consistency reliability, convergent validity, and discriminant validity, since the indicators are reflectively specified. Second, the structural model was evaluated, referring to the standard criteria such as variance inflation factor (VIF), coefficient of determination R2, cross-validated redundancy based on blindfolding procedure Q2, and the effect size f2. We ran the PLS algorithm for a blindfolding procedure based on the omission distance of six following previous studies [84,85,86]. The effect size f2, which measures the effect of removal of a certain predictor variable on the R2 of an endogenous variable, was calculated following the procedure suggested by [86]. Finally, the hypothesized relationships between intention to engage in EA practices and its antecedents were examined using path coefficients, T-statistics, and p-values. We ran the PLS algorithm using 5000 bootstrapping subsamples in estimating T-statistics and p-values following [86].

4. Reliability and Validity Test Results

The results of the relevant tests for the reliability and validity of the measurement model are reported in Table 1, Table 2, Table 3 and Table 4. Table 1 presents the descriptive statistics for each indicator along with the outer loading. The mean values for items pertaining to the latent construct of “Behavioral Intent to Engage in EA (INTENT)” are relatively low, indicating less managerial intention to engage in EA practices. However, the mean values of the items in the constructs of “Attitudes towards EA Practices (ATTI)” and “Subjective Norms (NORMA)” are above the theoretical average (i.e., 3.5), suggesting overall positive attitudes towards EA practices and increasing normative pressure towards EA implementation. On the other hand, the highest mean values can be observed in the items related to the latent construct of “Perceived Cost and Complexity (COXCS)”, which suggests that corporate managers in Sri Lanka consider EA practices to be more costly and burdensome. With regard to the normality of the data, excess kurtosis and skewness suggest that the data are non-normally distributed. However, this is not problematic, as the PLS-SEM can handle non-normal data effectively [87].

Table 1.

Indicators’ outer loadings and summary statistics.

Table 2.

Internal consistency and convergent validity.

Table 3.

Fornell–Larker Criterion analysis for assessing discriminant validity.

Table 4.

Heterotrait–Monotrait (HTMT) Ratio for assessing discriminant validity.

Consistently with the measurement theory, we first examine the outer loadings of indicators. The majority of the indicators (i.e., 28 indicators out of 35) have satisfactory outer loadings and exceed the recommended minimum value of 0.708 [81,85]. The outer loadings of the rest of the indicators are also not problematic, as they are between 0.4 and 0.7 [86]. Moreover, we observe that the removal of these indicators did not increase the composite reliability (CR) of the respective constructs [86]. As for the internal consistency reliability, we used two measures: Cronbach’s Alpha and CR, the results of which are reported in Table 1. Both the Cronbach’s Alpha and CR values are within the recommended range (Cronbach’s Alpha > 0.7 and 0.7 < CR > 0.95); hence, internal consistency reliability is established [84,85,86,88]. The convergent validity of each of the constructs was determined to refer to the average variance extracted (AVE). All the AVE values related to each of the constructs are above the minimum acceptable value (i.e., 0.5 or above), as shown in Table 2, and, therefore, exhibit an appropriate level of convergent validity [85,86].

The statistical properties related to the discriminant validity of the constructs in the structural model are also adequate. Three metrics were used to determine the discriminant validity (DV): Fornell–Larker Criterion, cross-loadings, and Heterotrait–Monotrait Ratio (HTMT) [85,86]. The outer loading of each indicator on the respective construct is higher than all of its cross-loadings on the other constructs in the model [89]. Similarly, the Fornell–Larker Criterion analysis reported in Table 3 also shows that the square root of the AVE value of each construct is greater than its correlation with other constructs [90]. Furthermore, the HTMT ratios of the correlations are well below the threshold value of 0.85, as shown in Table 4 [91]. Additionally, the VIF values reported in Table 5 indicate that there is no multicollinearity issue in the model, and, hence, each construct is unique and distinct from other constructs in the model [87].

Table 5.

The assessment of multi-collinearity.

5. Results and Discussion

The results of the structural model evaluation are reported in Table 6 and depicted in Figure 2 (see also Appendix B and Appendix C). The direction and extent of the relationship between latent constructs are determined based on path coefficients [85,86,92]. We used a 5000 subsample bootstrapping procedure to estimate the statistical significance of the path coefficients [85,86]. The hypothesized relationships between each variable were accepted or rejected accordingly.

Table 6.

Results of the hypothesis testing.

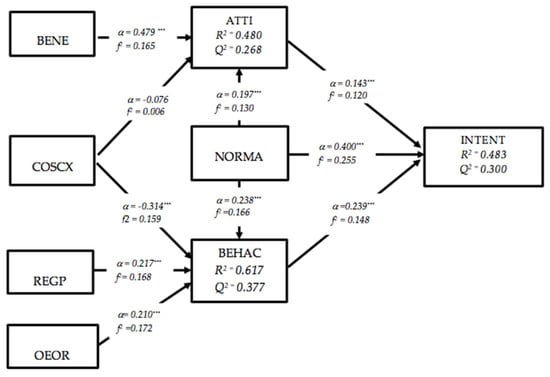

Figure 2.

Result of partial least square structural equation modeling (PLS-SEM) estimation. Significant at *** p < 0.01.

5.1. Hypothesis Testing

Consistently with the TPB, we hypothesized a positive relationship between perceived benefits (BENE) and attitudes (ATTI) towards EA in H1. A positive and significant path coefficient (α = 0.479, p < 0.001) obtained from PLS-SEM analysis provides strong support for the H1. The H2a and H2b predicted a negative relationship between perceived cost and complexity (COSCX) and ATTI and between COSCX and perceived behavioral controls (BEHAC), respectively. Although both the path coefficients are negative (α = −0.076, α = −0.314), only the path coefficient between COSCX and BEHAC is statistically significant (α = −0.314, p < 0.001). Therefore, there is not enough evidence to accept H2a, yet we can accept H2b based on the present evidence. The H3 predicted a positive association between the perceived regulatory pressure (REGP) and BEHAC. Likewise, H4 expected a positive relationship between the organizations’ environmental orientation (OEOR) and BEHAC. The results of the PLS-SEM analysis support both the hypotheses H3 and H4 (α = 0.217, α = 0.210, p < 0.01). In addition, we postulated a positive association between subjective norms (NORMA) and other constructs in the model, such as ATTI, BEHAC, and intention to engage in EA practices (INTENT) in H5a, H5b, and H5c, respectively. Interestingly, these three hypotheses were all supported by the results, as the path coefficients are statistically significant (α = 0.400, α = 0.197, α = 0.238, p < 0.05). Another integral part of the TPB is the relationship between attitudes towards behavior and behavioral intention. In our study, this is reflected in the H6. As expected, ATTI is positively and significantly associated with INTENT (α = 0.143, p < 0.05). The results suggest that an increase in one standard deviation of ATTI increases the INTENT by 14.3%. The relationship between perceived behavioral control and behavioral intention in the EA context is predicted in the H7, and the same is supported by PLS-SEM results. That is, BEHAC positively and significantly influences the INTENT (α = 0.239, p < 0.01).

Concerning the path coefficients, the largest coefficients can be seen between BENE and ATTI, suggesting that managers who have perceived higher benefits in EA practices have acquired strong positive attitudes towards EA practices and vice versa. The effect size (f2 = 0.165) also shows that the BENE is the best predictor of the ATTI in the present model. The coefficient of determination (R2) of the endogenous variable ATTI is 48%, which means that both the exogenous variable BENE and COXCS account for almost half of the variance of managers’ attitudes towards EA practices in Sri Lanka. Concerning perceived behavioral control, all three exogenous variables (COSCX, REGP, OEOR) are either positively or negatively and significantly associated with BEHAC. These three variables explain 61.7% (R2 = 0.617) of the variation of the BEHAC, as shown in Figure 2. The INTENT, as the ultimate construct in the model, is significantly influenced by all its predecessors (ATTI, NORMA, BEHAC). While all three variables account for 48.3% of the variation of the INTENT, NORMA has the highest impact on the INTENT (α = 0.400, α = 0.197). Concerning the predictive accuracy and relevance of the path coefficients, Q2 values of ATTI, BEHAC, and INTENT (0.268, 0.377, and 0.300) indicate an acceptable level [86].

5.2. Multigroup Analysis

Our research involves listed companies as well as non-listed companies (private companies), and thus we performed a multi-group analysis (MGA) to determine the group-specific path coefficients, which are significantly different. This enables us to account for observed heterogeneity and thus avoid possible misinterpretations. This means that managerial intention towards corporate EA practices among listed and non-listed companies may vary to some degree due to various factors, such as the availability of resources, the extent of regulatory influence, geographic dispersion, and so on. This is evident from previous studies, such as that of Thoradeniya et al. [8], which revealed that there are some differences in behavioral intention and actual behavior towards sustainable reporting practices between listed and non-listed companies in Sri Lanka. The use of MGA, therefore, allows us to analyze whether the structure of the relation between latent variables is stable across the sub-group of companies and, thereby, the conclusion of significant differences, if any, between listed and non-listed companies with regard to managers’ intention to engage in EA practices.

As with the main analysis, the MGA was performed using the PLS-SEM approach, and the analysis was carried out in Smart PLS statistical software. In carrying out our MGA, a three-step procedure, as suggested by Matthews [93], was implemented. In the first step, we identified two pre-defined groups of companies as listed and non-listed companies. A total of 95 companies belonged to the group of listed companies, and 151 companies were included in the non-listed category. Upon defining the two groups, in the second step, we checked for measurement invariance to decide if the underline structures of the latent constructs of the two groups are comparable. To this end, we investigated configural invariance, compositional invariance, and equality of mean values and variance (i.e., measurement invariance of composite models) using the procedure suggested by Henseler et al. [94]. However, we were unable to establish full measurement invariance, and only partial invariance was established, i.e., configural invariance and compositional invariance. According to Henseler et al. [94], it is appropriate to compare path coefficients across multiple groups by establishing only partial invariances. The third step of the process was to assess the results of the statistical test for the MGA. The path coefficients of the two groups (i.e., listed and non-listed) were compared using the procedure called permutation, which is a separate option in the Smart PLS software. The permutation test is considered to be more appropriate than the other available methods (i.e., PLS-MGA, Parametric, Welch–Satterthwaite) [93,94]. Table 7 reports the results of the permutation test using 5000 iterations (it should be noted that Table 6 shows only part of the results of the permutation test, and the rest of the results are not reported for the brevity of the paper).

Table 7.

Results of the multi-group analysis (listed = 95, non-listed = 151).

The path coefficients for listed and non-listed companies are shown in columns one and two of Table 6. Column three shows the differences between the path coefficients and their significance in the last column. Concerning listed companies, path coefficients somewhat deviated from the main analysis. In comparison to the main analysis, we find that several path coefficients (α = 0.116, α = 0.130) were no longer statistically significant (results are not reported) for listed companies. These results suggest that listed companies’ managers’ attitudes towards EA do not have a substantial effect on their intention to engage in EA practices; in addition, their perceived cost and complexity associated with EA have no impact on perceived behavioral controls. However, we find that certain relationships between latent variables are more pronounced in listed companies as compared to in the main analysis (i.e., NORMA to ATTI, NORMA to BEHAC).

In the case of non-listed companies, the findings indicate a noticeable variation concerning the significance of path coefficients as compared to the main analysis. For non-listed companies, the path coefficients from ATTI to INTENT, BEHAC to INTENT, NORMA to ATTI, NORMA to BEHAC, NORMA to INTENT, and REGP to BEHAC are not significant (results are not reported), while all these path coefficients are significant in the main analysis. Conversely, we find strong relationships between BENE and ATTI and between COSCX and BEHAC. This suggests that the perceived benefits of EA form the managers’ attitudes towards EA practices in non-listed companies. Moreover, the perceived cost and complexity involved in EA practices appear to be a major impediment to engaging in EA practices in non-listed companies. However, most of the predicted relationships cannot be observed in this separate analysis for the non-listed companies. Arguably, the reasons for this would be the lack of self-interest in EA, lack of EA knowledge, and the lack of regulatory and public pressure on EA practices in the context of non-listed companies.

Turning to the differences in path coefficients between listed and non-listed companies, the results indicate that only four predicted relationships are significantly different. Although the perceived cost and complexity involved in EA practices have a significant negative effect on the perceived behavioral controls in non-listed companies, the same is not significant in listed companies despite the negative sign. This can be explained by the fact that non-listed companies have fewer resources (i.e., financial and human) compared to listed companies, and, therefore, the resources required for EA practices might be considered to be higher. Next, we observe that the impact of normative pressure on managers’ intentions, attitudes, and behavioral control is significantly different between public and private companies. Our findings regarding normative pressure are consistent with previous studies, particularly that of Thoradeniya et al. [8], which was conducted in Sri Lanka.

Additionally, our sample includes companies from different industries, such as manufacturing, hotel and leisure, banking, finance, and insurance, chemical and pharmaceutical, power and energy, construction, plantations, beverages, food, tobacco, etc. Previous studies suggest that firms operating in environmentally sensitive industries are heavily engaged in environmentally friendly practices, including EA, EMA, and CSR [8,95]. Thus, there might be a noticeable difference in managerial intention to engage in EA practice between companies in environmentally sensitive industries and other industries. Therefore, we identified two groups of companies based on their industry types, namely those in environmentally sensitive industries and others. In line with previous studies, companies that belong to the power and energy, chemical and pharmaceutical, and construction industries have been identified as being environmentally sensitive [8]. There were 52 companies in the environmentally sensitive industries, and the rest of the companies are in the non-environmentally sensitive industries. Although we were able to identify two separate groups, we were not able to conduct an MGA using the PLS-SEM approach, since the measurement invariance could not be established.

However, the impact of industry type on the managerial intention to engage in EA practices was examined by incorporating a dummy variable (ENSEN) into the model. In this case, companies in environmentally sensitive industries were assigned one and the rest of the companies were assigned zero. Then, we re-estimated the model, and the results are depicted in the Appendix D. The positive path coefficient indicates (α = 0.489, p < 0.001) that the managers’ intention to engage in EA practices is relatively high in the companies that belong to environmentally sensitive industries.

5.3. Discussion

Previous studies, which have examined the managers’ perspectives on CSR practices, have revealed attitudes, subjective norms, and perceived behavioral control as the immediate predecessors of their intentions towards the practices [8,21,75]. Drawing on the TPB and taking insights from the stakeholder theory, the legitimacy theory, and neo-institutional theory, this study empirically examined the antecedents of managers’ behavioral intention to engage in EA practices. The results suggest that the perceived benefits of EA practices have a significant effect on managers’ attitudes towards EA practices. On the other hand, perceived cost and complexity of EA practices have a substantial negative influence on perceived behavioral control, which could potentially minimize managers’ intention to engage in EA practices. The results also suggest that perceived regulatory pressure and organizational environmental orientation have a significant and positive relationship with perceived behavioral controls. In line with the main rationale of the TPB, this study demonstrates that the immediate predictors of managerial intention towards EA practices are attitudes towards the practices, subjective norms, and perceived behavioral controls.

There is a positive and significant relationship between the perceived benefits of EA and attitudes towards EA. However, in the MGA, this relationship only applies to listed companies. Indeed, managers in large companies are more knowledgeable and more concerned about environmental sustainability issues than managers in small companies [96]. Managers’ perceptions of the benefits of EA may be subject to the knowledge, experience, and other concerns they have on environmental issues, and this may be the reason for the aforementioned difference between listed and non-listed companies. While the benefits–attitudes relationship from the main analysis is comparable to previous studies, the findings with respect to non-listed companies are inconsistent with Thoradeniya et al. [8], where they found a significant and positive association between behavioral beliefs (mostly positive outcomes) and sustainability reporting attitudes in non-listed companies.

This study predicted that the cost and complexity of EA practices [3] would negatively affect perceived behavioral control and attitudes towards EA practices. This suggests that managers who perceive EA practices as expensive and that such practices raise the administrative burden will have negative attitudes towards them. They may also perceive that higher costs and an increase in the complexity of administrative processes are obstacles to EA practices, and thus lower behavioral intentions through perceived behavioral control. However, our findings only endorse the expected relationship between COSCX and BEHAC. Although the relationship between COSCX and ATTI is negative, it is not statistically significant. While these results provide new evidence on how the cost and complexity involved in EA practices affect managers’ behavioral intentions, they are somewhat positioned with the findings of previous studies. For instance, Burzis Homi Ustad [97] found that New Zealand hotel managers consider cost as the major barrier for the implementation of the environmental management systems. Our MGA has revealed an interesting phenomenon, where the negative relationship between COSCX and BEHAC is much stronger in non-listed companies than in listed companies. The same applies to the relationship between COSCX and ATTI despite statistical insignificance. This can be interpreted as the following: Small businesses (i.e., non-listed companies) find EA practices to be more costly and administratively burdensome.

We extended the TPB by replacing behavioral beliefs with three variables, namely perceived cost and complexity, perceived regulatory pressure, and organizational environmental orientation. Our findings indicate that these three variables are significantly associated with perceived behavioral control. Both the regulatory pressure and environmental orientation have a positive impact on perceived behavioral control. This indicates that companies that have already implemented environmentally friendly policies or procedures are more likely to engage in EA practices. In addition, the intention of managers to engage in EA practices appears to be stimulated by environmental rules and regulations, particularly in public companies. Our results are consistent with the findings of Rebeiro et al. [70], where they found a positive association between the degree of development in environmental management practices and the level EA practices. These results also provide policymakers with the important insight that, by strengthening environmental regulations, they can encourage corporate managers to pursue more environmentally friendly practices within their firms.

There has been an increase in public concern over environmental degradation in Sri Lanka in recent years. Increased deforestation, garbage dumping problems in the capital city of Colombo, and rapid contamination of water were some of the main reasons for this. Ironically, our results indicate that the managers’ intention to engage in EA practices is mostly driven by normative pressure, which reflects growing public demand for environmental preservation in the country. Moreover, the impact of subjective norms on managerial intention to engage in EA practice is relatively higher in public companies. This could be because large companies are more visible and, therefore, subject to public criticism and scrutiny [70,98]. Our findings are consistent with previous studies [8,75]; Thoradeniya et al. [8] found that subjective norms have a great influence on managers’ intention to engage in sustainability reporting in listed companies. Our findings also indicate that subjective norms significantly influence both attitudes towards EA practices and perceived behavioral control. These results not only accord with the TPB’s rationale, but are also consistent with previous studies.

In summary, we found that managers’ intention to engage in EA practices is affected by attitudes towards EA practices, subjective norms, and perceived behavioral control. However, these three constructs can explain only less than half of the variance of managers’ intentions, which suggests that more than half of the variance of managerial intention is accounted for by some other variables not included in this analysis. In addition, out of the three antecedents of managerial intention, subjective norms are shown to have a greater effect on managerial intention, which is aligned with environmental issues and related developments in the research context, Sri Lanka.

6. Conclusions, Implications, and Limitations

Research into EA practices is a growth area that has received increasing attention from both scholars and practitioners. This study attempted to answer the question: “What are the driving factors of managerial intention to engage in EA practices in Sri Lanka?” The TPB provides a theoretical basis for the conceptual model that addresses the research question. The model was tested using data collected through a standardized questionnaire from a sample of 247 top-level and middle-level managers of listed and non-listed companies in Sri Lanka. The results demonstrate the structural relationship between managerial intention to engage in EA practices and attitudes towards EA practices, subjective norms, and perceived behavioral control. Our findings also indicate that the perceived benefits are the best predictors of attitudes towards EA practices. Moreover, the results indicate that the main barrier to engaging in EA practices is the cost and complexity involved in EA practices. Furthermore, organizational environmental orientation and perceived regulatory pressure are shown to have an incremental effect on the managers’ intention to engage in EA practices.

6.1. Theoretical Implications

Previous studies on EA and reporting have predominantly focused on the disclosure issue. However, the managerial side of EA implementation has often been overlooked. Shedding light on this issue, we contribute to the EA literature by examining managers’ intention to engage in EA practices and its key drivers. Our study also contributes to the literature by demonstrating the applicability of the TPB in the context of EA. Examining the influencing factors of behavioral intention to engage in EA practices in terms of multiple concepts and perspectives is vital, as it expands our understanding of the determinants of EA practices. Previous studies have predominantly used social theories, such as stakeholder theory, legitimacy theory, and neo-institutional theory, to explain the corporate adoption of sustainable management practices [18,40,57]. Even though these theories provide a useful framework to identify the mechanism that affects the diffusion of sustainability management practices, it is questionable whether these theories are sufficient to explain the psychological factors that may affect the adoption of those practices [8]. While there is a call for studies that explore new theoretical avenues [8,18], particularly psychological theories, in social and environmental accounting research, only a few studies have been directed towards this end so far [8,18]. As such, this study fills this void by illustrating the usefulness of the TPB in the EA domain, and empirically establishes the key influences of the managers’ intention to engage in EA practices. Although our descriptive analysis shows that the managers’ attitudes towards EA practices and intention to engage in EA practices are considerably low, there is a positive and significant relationship between attitudes and intention. Nonetheless, the most important predecessor of managerial intention to engage in EA practices is subjective norms, particularly in the case of listed companies. This is important because it is consistent with the findings of previous studies [40,58], which have used other social theories—for example, neo-institutional theory and stakeholder theory. Arguably, stakeholder pressure or institutional isomorphic forces first change the managers’ attitudes, perception, and behavioral intention over time, which ultimately results in structural changes in organizations.

Another key contribution of this study is the identification of novel constructs that explained more than half of the variance of perceived behavioral control. We showed that perceived regulatory pressure, organizational environmental orientation, and perceived cost and complexity have significantly influenced perceived behavioral control. We not only extend the TPB, but also provide a useful framework to identify behavioral factors that influence the adoption of sustainability practices. The findings show that the cost and complexity dimension has the most significant (negative) impact on the perceived behavioral control over EA practices. This may be the reason why most of the private companies in Sri Lanka have ignored environmentally friendly practices, including EA [39], which has led to the observation of vast environmental pollution in the country.

The application of PLS-SEM in the EA context is also a novel contribution. This is one of the first studies that employees the PLS-SEM approach in order to identify socio-psychological parameters related to EA implementation. Moreover, we performed an MGA using a permutation procedure, which also fills a methodological gap in the EA literature. In addition, our study expands the current empirical evidence by examining the managerial perspective on the implementation of the EA in a developing country. This is important because most of the current empirical evidence is based on developed countries and, therefore, lacks the transferability of those findings to the developing world.

6.2. Managerial and Policy Implications

This study provides important implications for managers and regulatory authorities. Our findings indicate that subjective norms have a greater influence on the managers’ intention to engage in EA practices. This implies that there is increasing pressure from stakeholders towards environmental preservation. Establishing environmentally friendly policies would, therefore, bring companies with competitive advantages. However, most managers perceive EA practices as more expensive and as increasing the complexity of the accounting and reporting systems, which may require additional resources and time. Even so, the benefits of EA practices should be understood not as short term, but as long term. Accounting for the impact of business operations on the natural environment not only provides stakeholders with a holistic perspective of business operations, but also helps managers to develop strategies to mitigate such impacts and, thus, improve financial performance.