Abstract

Corporate social responsibility has been one of the main pillars of development for companies in developed countries and studies are being conducted for developed countries and the productive sector of the economy. Therefore, the main objective of this paper is to analyze the relationship between corporate social responsibility (CSR), corporate reputation (CR), and business confidence in the context of the banking sector in an emerging country (Peru). To test the hypotheses presented in this paper, we sent a survey to 1745 banking executive officers of the branch offices in Peru. These key individuals were selected as the target population of the study because the authors sought to study the management’s perception of CSR and business confidence. From the data obtained from the survey, it has been determined that the strategic consideration of CSR in Peruvian banks directly influences the perception of business confidence. Secondly, it has been demonstrated that the strategic consideration of CSR in Peruvian banks positively influences corporate reputation and, finally, the perception of the importance of the corporate reputation of Peruvian banks and significantly influences the perception of business confidence by the managers. The main contribution of this paper is that it analyzes empirically how business confidence is perceived by managers, who are the main agents involved in implementing CSR actions, based on their opinion of the strategic consideration of CSR and the perception of CR in a context barely investigated, an emerging country.

1. Introduction

Corporate social responsibility (CSR) has evolved over time and has positioned itself as one of the main pillars for the development of any project undertaken by a company in developed countries. From an academic point of view, there has been extensive research on its importance for the economic profits of companies and community development. Furthermore, as empirical evidence shows, CSR practices may have positive consequences in terms of both internal and external development of companies, reinforcing their reputation and improving confidence in them [1]. However, research on this topic is generally conducted within the context of developed countries and focused on the productive sector of the economy, overlooking emerging countries and the service sector and financial sector, which represents a gap in the research because CSR in these sectors is in an incipient phase compared to developed markets.

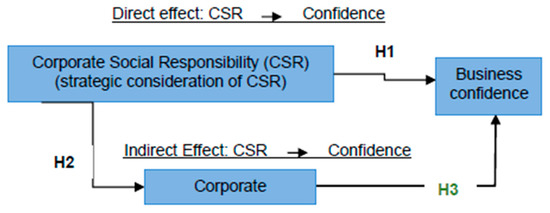

In order to reduce this research gap, the general model of this research (Figure 1) studies the relationship between corporate social responsibility (CSR), corporate reputation (CR), and business confidence in the context of the banking sector in an emerging country (Peru). Furthermore, it is important to understand that the Peruvian banking sector contributes to the growth of society, as demonstrated in a previous study [2], which is presented in Appendix A. However, they have not been well recognized by society in terms of CSR despite having clear plans and objectives. It was concluded in [2] that CSR actions were more relevant in the productive sector but the banking sector had its own agenda for the development of CSR and CR.

Figure 1.

Research model. Source: Own elaboration.

This general model considers two effects. The first one is the direct effect of CSR that studies the relationship between CSR and the perception of business confidence. The second is the indirect effect by which CSR actions influence the perception of business confidence through the mediation exercised by the corporate reputation variable. This indirect effect is analyzed in two stages: the first step is to study the effects of CSR on CR and the second step is to study the effects of this last variable on business confidence.

The paper is structured as follows: Firstly, we review the theory that explains the importance of the strategic conception of CSR in the company and its relationship with the improvement of business confidence. Secondly, we review the effect of CSR on corporate reputation (CR) and the influence of CR on business confidence. Then, we explain the methodology to test the hypotheses proposed in the theoretical section. Finally, we present the main results of the emerging country gap analysis and conclusions.

2. Direct Effect: Strategic Consideration of CSR in the Company and Its Effect on Business Confidence

The stakeholder concept appeared for the first time in the literature in the 1960s but the stakeholder approach remained dispersed and peripheral to management practices until the mid-80s, when Freeman (1984) gathered several concepts about the stakeholders approach and constructed a coherent and systematic stakeholder theory defining the stakeholder as “any group or individual that can affect or be affected by the achievement of the organization’s objectives” [3] (p. 46).

Responding to the objectives of various groups of interest, companies try to protect themselves against the risk of losing or reducing their capital. One way to achieve this protection is by considering CSR as a variable within the company’s strategy. Carroll (1979) [4] supports this analysis due to the fact that CSR implies connecting the obligations of the company with society and justifies that the strategic consideration of CSR can improve business confidence. According to Carroll (1979) and his followers [5], the strategic consideration of CSR includes assuming such responsibility in the economic, legal, ethical, and philanthropic ambit.

This conception of CSR will cause positive internal effects in the company and will also lead to positive external effects once the social impacts of CSR become visible [4,6] and the investments in CSR made by companies become better perceived by stakeholders, with a positive effect on their confidence. An example of this relationship is the study of [7] where they explain that NGOs (non-profit organizations) highly value the contribution of for-profit entities in human rights protection as well as occupational health and safety, benign environmental management, and anti-corruption practices. In the study [8], non-profit entities were an important part of general social policy in the economy. They realized important aims in healthcare, in education, and many other socially important areas, which are some areas of CSR.

Regarding the empirical analyses, the relationship between CSR strategic actions and the best perception of business confidence, had demonstrated that the strategic conception of CSR can be translated into improvements in economic and financial factors, either in the annual profit of the company [9,10], or in the creation of value for investors [11] and the financial profitability of the company [11,12]. Secondly, integrating CSR actions into the strategy of companies can improve business confidence through an emotional factor because companies will be perceived as agents of social improvement and people will be more confident in their management [10,12]. Furthermore, there are factors related to the market, such as the greater market share that can be achieved by accessing customer niches that are increasingly concerned with these matters or by obtaining contracts with Public Administrations that favor such companies in their public tenders [13].

In the financial sector of developed countries, corporate social responsibility has been solidly established, despite attracting criticism [14], due to its significant impact on society and its various interest groups [15], because of their undeniably crucial role in modern economies. The banking sector has presented significant transformations in recent years and has become one of the most proactive agents of CSR worldwide [16,17]. Its approach to CSR actions has changed significantly and, therefore, banks are closer to social and environmental problems, have a broader role in society by implementing CSR objectives and principles, and their transactions are more transparent and generate more value for society and various groups of interest, such as customers, suppliers, investors, and workers [18,19]. In addition, banks are implementing CSR strategies and practices with initiatives such as financial inclusion [20]. However, it is not clear yet if the positive response to CSR in developed countries will be the same in emerging countries and, therefore, if the managers, the main drivers of CSR actions, will perceive the advantages. In a study carried out in an emerging country (India) [11], it is evident that the strategic management of CSR is a useful tool and explains the better perception of business performance. In a study from [19], bank-specific strategies also drive the most-extensively addressed SDGs, overlooking any critical importance of certain GRI indicators with a multifaceted impact across several SDGs. The SDGs according to [21] reflect grand challenges that the global community needs to address in order to ensure economic welfare, environmental quality, social cohesion, and prosperity for future generations. In this respect, the role of the banking sector, among other critical business entities and key stakeholders, is vital.

From the theory and empirical analysis that relates CSR to business confidence especially in developed countries hypothesis 1 is formulated.

Hypothesis 1 (H1).

The strategic importance of corporate social responsibility will positively influence the perception of business confidence in the service industry (banking) of an emerging country.

3. Indirect Effect: Strategic Consideration of CSR in the Company–Corporate Reputation and Business Confidence

The strategic consideration of CSR within companies leads to positive effects on multiple dimensions of corporate reputation. The literature has identified some of the results, such as enhanced management quality, managerial ability and leadership [22,23], improved product quality and customer satisfaction [24,25], and the reinforcement of stakeholder confidence based on a stronger corporate image [26] and competitive positioning [27].

Several authors have indicated that perception of the impact of CSR on the different dimensions of corporate reputation is conditioned by the geographic location of the company [1,28,29]. In fact, all the empirical studies described are referring to developed countries.

At the beginning of the new millennium, world leaders went to a meeting of the United Nations to give shape to a broad vision of promoting CSR actions worldwide. This vision was translated into the eight Millennium Development Goals (MDGs). MDGs were replaced by the new Sustainable Development Goals (SDGs) of the United Nations (UN) in 2015, which have been in place since January 1st, 2016. The seventeen SDGs differ from MDGs because they are broader in number, represent larger aspirations, and also present a relevant program for all people and companies in all countries. Therefore, since CSR actions have been considered essential in the political field throughout the world, they should also be positively valued by companies from emerging countries. From this, hypothesis 2 is formulated.

Hypothesis 2 (H2).

The strategic importance of corporate social responsibility will positively influence the perception of corporate reputation in the service industry (banking) of an emerging country.

When a company improves in the dimensions of CR, it accumulates reputational capital that allows them to attract and motivate stakeholders, including employees, customers, and suppliers. As a result, companies that accumulate reputational capital gain a competitive advantage in the market. Besides, accumulated reputational capital can be used as a risk manager, by providing protection against negative publicity or skepticism when negative actions occur [30] and maintaining trust with stakeholders. Companies with high CR are perceived to have fewer risks and this is particularly relevant among interest groups that are susceptible to moving capital to other companies at any given time and make other financial decisions [22]. That is why the strengthening of the brand image and reputation can reduce operational risks. In [6], it is illustrated that CSR activities that have a positive impact on CR allow companies to differentiate from the competition, which translates into competitive advantages.

Several authors have found positive relationships between corporate reputation and its effects on business confidence [31,32,33], although analyses applied in emerging countries have been barely detected. In this case, the study by [34] shows a positive relationship between the corporate reputation and the confidence towards the company in the stock market in China. Yet, we believe that the positive effects of reputation are especially relevant in the banking sectors of emerging countries. After the last financial crisis that affected the world, the reputation of the financial sector was questioned, under an accusation of being the main culprit in the economic recession [35]. Given this situation, improving CR through CSR actions allows banks to improve their internal and external credibility, by avoiding the negative messages of the banking system. According to the study of [36], these negative messages are expanding rapidly through social networks. This study also indicated that the median of the tweets sent about banks express negative thoughts and emotions. Banks must be able to respond promptly in an appropriate manner to avoid damage and destruction of value. Therefore, emerging countries are not on the sidelines of this reality. From the theory that relates corporate reputation to business confidence, from empirical results detected for the stock market in China [34], hypothesis 3 is formulated.

Hypothesis 3 (H3).

Corporate reputation will positively influence the perception of business confidence in the service industry (banking) of an emerging country.

4. Methodology

To test the hypotheses presented in this paper, a quantitative methodology has been used. The empirical research began in March 2016 with the presentation of the initial questionnaire to the directors of the Association of Banks of Peru (ASBANC). This pilot served to prepare the final survey similar to the study of [7] where they emailed a cover letter and a link to a self-administered questionnaire. A cover letter and a self-administered questionnaire were also sent via e-mail in the study of [7].

The changes made to the original questionnaire involve adjustments to the writing and presentation style of the questions (the final survey was composed of different sections). In the first part, economic variables concerning the banks’ branches in an open-ended question format have been assessed. This section gathers data about the number of employees, economic benefit, market share, and others. The rest of the questionnaire was composed of close-ended questions with a scale ranging from Very Low (1) to Very High (5) in order to value the intensity. The questions are related to CSR actions concerning the triple bottom line and the strategic conception of CSR in the bank (Appendix B shows the questions used in the analysis).

Likewise, the survey appraised the perception of the financial institutions regarding corporate reputation and business confidence sourced from CSR activities. Later, ASBANC’s managers provided data of bank operations in Peru in January 2016, with a total of seventeen banks (Table 1), as well as the contact information of 1745 banking executive officers of the branch offices in Peru, because middle managers perceiving and prioritizing various CSR aspects can yield increased apprehension of how they process and make relevant decisions [7]. These key individuals were selected as the target population of the study because the authors sought to study the management’s perception of CSR and business confidence.

Table 1.

Banks in Peru (January 2016, compiled by authors).

The impact of managers on strategic decisions is transcendental, which justifies their selection as the unit of analysis when studying CSR. CSR actions of companies are largely promoted, defended, and developed by these managers [37]. Managers will directly influence the company’s commitment to CSR, allocating resources to different programs and practices and aligning these activities with the company’s objectives [38]. The perception and the capability of the influence of the managers will condition the success in relation to the application of CSR actions [33]. Therefore, if managers perceive that employees are involved in CSR actions and that they are positively influencing business confidence, their ability to influence will positively condition the company’s behavior towards CSR [39]. On the other hand, if managers perceive that employees do not get involved enough, their capability to influence will condition the non-continuation of this issue, since it will be considered a waste of resources [39].

In 2016, the questionnaire was sent to the managers of the banks with a message containing a detailed explanation of the relevance of the study. The message also included a promise made to send a results summary to the managers that participate. Finally, to give the message more credibility, copies of the previous studies were attached. The data gathering process was finished in 2–3 months with a total of 112 valid responses. The technical analysis and response rate statistical validation is presented in the following sub-sections, followed by an explanation of the dependent and independent variables.

4.1. Technical Data and Statistical Validity

Table 2 shows the characteristics of the empirical study, i.e., the universe or target population, geographical area and timeframe of the research, size, units, confidence (level), and sample error. The following expression was used to calculate the sample error. N stands for the population size, which is 1745, n will be the size of the sample (112), Z at a confidence level of 95.0% takes the value of 1.96, P is the population that holds the characteristic. In the worst case analysis, p = q = 0.5, and e is the sampling error, the variable to calculate. After applying the formula, the error rate was 0.0896. The error rate is higher because the response rate was low, even though, errors below 0.1 are acceptable (statistically) [40].

Table 2.

Technical Data.

To analyze whether the sample is representative of the population, the frequency distributions are shown by gender and by age (Table 3 and Table 4).

Table 3.

Representativeness of the sample by gender.

Table 4.

Representativeness of the sample by age.

In order to evaluate the representativeness of the sample with a higher degree of reliability, two logit analyses were performed. The probability of response was determined as the dependent variable [41]. Therefore, the independent variable for the first logit was gender, which was measured by the number of responses. In the second logit, the independent variable was age group, which was analyzed by the number of responses. The number of responses was not entered in the model and was not considered in any of the analyses. This result proved that the sample was objective and was guaranteeing external validity.

4.2. Measurement Scales

A multiple indicators approach was followed to construct the measurement scales of the concepts used in this study. Therefore, each concept was measured with random items or variables. Finally, the questionnaire was composed of close-ended questions with a scale ranging from Very Low (1) to Very High (5) in order to value the intensity.

4.2.1. Perception of Business Confidence by Managers

The first group of questions refers to the perception of business confidence that reflects the dependent variable. Considering the contributions of the authors that have analyzed the improvement of the perception of business confidence, the questions also included a section about the importance of the variables analyzed by the authors like economic, emotional, and other variables. Regarding the factor of business confidence for economic improvements of the company, questions were asked about the following: (1) the assessment of the importance of the annual profit of the company (Y1) following several analyses [9,10]; (2) the assessment of the importance of the creation of value for the stakeholders (Y2) following different analysis [11,42]; (3) the assessment of the importance of the financial profitability of the company (Y3) following different analyses [11,12]. For the factor of improvement of business confidence through an emotional factor, a question was asked about the importance of the feeling of confidence towards the company (Y4) [10,12]. Furthermore, there are factors related to the market. Regarding this factor, questions were asked about the valuation of the market share (Y5) and the perception of the evaluation that clients give the company (Y6) [13,43]. Finally, there are external factors that can improve through CSR, which have an effect on business confidence. Among them, several works [44,45] have identified the environment as a variable, and, therefore, a question was asked concerning the environment (Y7).

4.2.2. Strategic Conception of CSR

The second group of questions refers to the strategic conception of CSR. This developed from contributions that consider the strategic conception of CSR as a social action that should be present in all policies and processes of the company and at all hierarchical levels, also including ethical principles of social action and, for some, even the mission, vision, and values of the company. The assessment of 4 variables already used in previous studies was requested: (a) role of CSR as a strategic pillar in the company (X1) [46,47]; (b) level of social impact of CSR programs carried out at a strategic level by the bank (X2) [5]; (c) level of investment in CSR programs carried out at a strategic level (X3) [48,49]; (d) CSR is part of the culture of the entity (X4) [3,6].

4.2.3. Corporate Reputation

The third group of questions refers to corporate reputation. The assessment of 4 variables already used in previous studies was requested: (a) perceived importance of the quality of management and business leadership (CR1) [23,50]; (b) perception of the image towards the outside (CR2) [26]; (c) supply and quality of products as well as customer satisfaction (CR3) [25]; and (d) stakeholder confidence regarding competition (CR4) [29].

5. Results

Table 5 shows the means and standard deviations of the items with which we have worked and Table 6 shows the correlations between the items used, which provides an idea of the relationships between them.

Table 5.

Descriptive variables analyzed.

Table 6.

Correlations.

Harman’s single factor test was used to verify that there was no common method bias (CMB); to do this, the items of the scale are constrained to just one. If all variables weigh a single factor or any factor explains most of the variance, then CMB is a problem. The importance of this method has been shown in the literature [51]. The exploratory factor analyses carried out are shown in Table 7. Three factors were generated using the eigenvalues >1 rule. Each factor explains 36.67%, 20.18%, and 18.03% of the variance of the data. The authors conclude that the results are not affected by CMB because there is no single factor and the first factor does not represent a majority of the variance of the data. Furthermore, the analysis reflected the accordance between the composition of the scales and the starting assumptions. In other words, it revealed the existence of three factors measured by the items suggested in the theoretical analysis.

Table 7.

Variance of the factors.

Next, we have used elaborated constructs with items that explain the variables. The validity of the construct about business confidence was tested by a factorial analysis. This indicated that the construct was an indicator of a single variable. Table 8 shows the main results in which a single factor explains 77.716% of the variance of the items about business confidence. The internal consistency of the responses was calculated using Cronbach’s Alpha (0.952). We call this factor Business Confidence (BC).

Table 8.

Factorial dimensions of business confidence.

The validity of the construct about corporate reputation was also tested by a factorial analysis. This shows that the construct was an indicator of a single variable. Table 9 shows the main results in which a single factor explains 61.557% of the variance of the items about corporate reputation. The internal consistency of the responses (0.791) was calculated using Cronbach’s Alpha. We call this factor CR.

Table 9.

Factorial dimensions of corporate reputation.

Finally, we have tested the validity of the construct about the strategic conception of CSR. Factorial analysis showed that the construct was an indicator of a single variable. Table 10 shows the main results in which a single factor explains 68.346% of the variance of the items. The internal consistency of the responses (0.842) was calculated using Cronbach’s Alpha. We call this factor StrategicCSR.

Table 10.

Factorial dimensions of the strategic conception of corporate social responsibility (CSR).

To test the hypotheses we worked with a dependent variable that is the construct of the perception of business confidence (BC), which explains 77.716% of the items that were used in the questionnaire for their analysis. We use two independent variables. The first refers to the strategic conception of CSR (StrategicCSR), which is the construct that explains 68.346% of the variance of the items that have been used in the questionnaire for analysis. The second refers to corporate reputation (CR), which explains 61.557% of the items that were used in the questionnaire for analysis.

The results obtained from the empirical study are shown in Table 11 and Table 12. Regression models are tested according to previously deduced hypotheses.

Table 11.

Regression models of independent variables on business confidence.

Table 12.

Regression model of CSR on corporate reputation (CR).

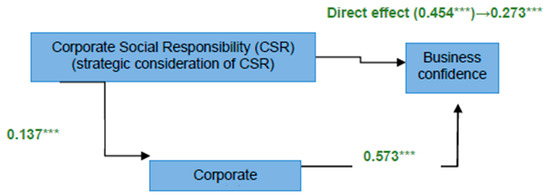

Following Baron and Kenny, for the existence of mediation, three conditions should be accomplished [52]. The first is that the predictor variable, in our case CSR, is related to the mediator, in our case CR. The second condition is that the mediating variable is related to the dependent variable (BC). Finally, that there is a significant relationship between the predictor (CSR) and the dependent variable (BC), so that once the mediating variable is introduced, it loses its significance (if it is total mediation) or decreases (if it is partial mediation). Once the existence of the mediating effect has been verified, it is recommended to demonstrate whether the mediation is statistically significant through the Sobel test [53]. Figure 2 shows the data from the regression models, including the coefficients of the predictor variable on the mediator that was performed in an additional model. Previously, to guarantee the starting conditions, the existence of multicollinearity between the explanatory variables (the factors CSR, CR, and BC) has been verified. Bivariate correlation values were examined and VIFs were calculated. In our case, all correlations are well below 0.8, and all VIFs reached values below 2, which is the cut-off value recommended by [54].

Figure 2.

Results; Source: Own elaboration.

From Table 11 and Figure 2, it has been observed that the strategic consideration of CSR in Peruvian banks influences the perception of business confidence, as had been proposed. The relationship found is statistically significant at a level of p < 0.001. Hypothesis 1 is, therefore, validated. That is, the strategic consideration of CSR positively influences the perception of business confidence in an emerging country. It supports previous analyses [4,6] concerning the need to internalize CSR in the company’s strategy to achieve positive effects internally and externally. Finally, the empirical studies in the banking sector [18] are confirmed, expanding them to an emerging country like Peru. These results further support arguments [39] that the behavior of a company in relation to CSR can be positively conditioned if managers perceive that the strategic implementation of CSR in activities leads to an improved perception of confidence in the company. Secondly, it has been demonstrated that the strategic consideration of CSR in Peruvian banks influences the corporate reputation, as had been proposed (Table 12 and Figure 2). Hypothesis 2 is, therefore, validated. That is, the strategic consideration of CSR positively influences the perception of corporate reputation in an emerging country. This result broadens previous empirical analyses [23,24,25,26,27,50] for a services sector (banking sector) in an emerging country.

Finally, both in Table 11 and in Figure 2, it is observed that once the mediating variable (CR) has been introduced, the significant direct effect of CSR on BC is reduced but not eliminated. It indicates that there is a partial mediation effect and, therefore, Hypothesis 3 is validated. Corporate reputation will positively influence the perception of business confidence in an emerging country. This result supports the approaches that consider CR to provide more confidence among the relevant stakeholders. Likewise, contributions of authors that justify the positive effect of CR in business confidence are ratified thanks to the positive effect of the reputational capital that attracts and motivates interest groups. Finally, the Sobel test allows us to confirm the indirect effect of CSR on BC through CR (z = 3.57; p < 0.001).

6. Conclusions

A healthy banking system is a key to sustained prosperity, as different authors have analyzed from different points of view, for example, that of treasury management [55]. The banking system plays an important role in economic development and sustainability [19,56,57,58] because its security and solidity create various external benefits to society [21].

Business confidence in Peruvian banking companies is important because of its impact not only on profitability and compliance with regulatory indicators [56], but also because it contributes to keeping these indicators in the ranges required by regulators, considering that these take captures and placements as bases. As these are “healthier”, in the end, they have a positive impact on the different variables that measure the perception of business confidence used in this chapter: benefit, value, profitability, market share, customer valuation, and environmental care. Therefore, companies could achieve sustainable development with stakeholders.

The Association of Banks of Peru–Asbanc and the specialized international journal América Economía have indicated, through their report on January 16th, 2017, Edition 226, that reputation is “key” to consolidating the results of banks in Peru. Likewise, corporate reputation has a positive impact on business confidence and is aligned with the products that the financial institution offers for the development of its operations (placements, deposits, and services), generating better financial results and confidence in its community. With an adequate reputation, greater confidence can be achieved by the most representative interest groups (collaborators, customers, and suppliers), who measure their investment according to the risk and the return over a period of time. People do not put their confidence in just any company. Following the line of [4], the strategic consideration of CSR involves assuming that the company has obligations to society in the economic, legal, ethical, and discretionary categories of business development and, for some, CSR should even be part of the mission, vision, and values of the company [3,6]. In this conception, CSR will begin to exert positive internal effects for the company and will also lead to positive external effects once the social impacts of the CSR actions become visible [4,6]. For the banking case, the strategic consideration of CSR should be aligned with the products and services offered by banks (such as placements and fundraising and the efficient management thereof) which would attract and generate greater business confidence.

Based on the perception of the Peruvian bank managers, it has been verified that the strategic consideration of CSR positively influences business confidence in an emerging country directly and influences business confidence indirectly through the best perception of CR. Thus, it supports the aforementioned theory that considers CSR as a means to maximize the value of the company for its stakeholders. The main contribution of this paper is that it empirically analyzes how business confidence is perceived by managers, who are the main agents involved in implementing CSR actions, based on their opinion of the strategic consideration of CSR and the perception of the CR in a context that has been barely investigated, an emerging country.

Of course, there are limitations to this study and future improvements that can be made. To measure the strategic consideration of CSR, CR, and business confidence, scales of perceptions valued from 1 to 5 have been used (other articles have used the same procedure). However, it should be recognized that the conclusions could be improved or accredited if objective measures were used.

The study takes into consideration a questionnaire and this includes the evaluation of perceptions, which can create a subjective point of view related to the experience and personal opinions, beliefs, and mood of the people who answered the questionnaire. However, the questionnaire was sent to the directors of the bank branches and the managers were chosen because they are also employees. Therefore, they are internal stakeholders who also have relations with senior managers at the hierarchical level, and, therefore, have knowledge of their opinions on these issues. In addition, the managers control the employees of the branch, so they can perceive what they think about the bank’s CSR and CR. However, this does not prevent the study from being extended to other stakeholders in the future.

From the perspective of academic research, this investigation is novel because it analyzes how CSR, which is still in an incipient phase of application in emerging countries such as Peru, makes it possible to improve business confidence in the banking sector. From the business perspective, this work makes a fundamental contribution, providing reasons for banks to believe definitively that the integration of CSR in business strategy can improve business confidence.

Author Contributions

Conceptualization, E.L.B.; data curation, J.D.B. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A. Study Cases from Banks

This information is from the four most important banks in Peru, which account for 80% of deposits. We have omitted the names of the banks. For more information see [47].

• X BANK

Strategic objectives: Financial inclusion and financial education and culture

Actions: Program: “Reading is being ahead”. This program supports a significant number of teachers and students, in eight regions of the country, in achieving the objectives of increasing reading rates and improving levels of reading comprehension among Peruvian students.

• Y BANK

Strategic objectives: Education, financial inclusion, and the environment

Actions: Program: “Graceland”. At Graceland, all bank employees participate in groups made up of members from all areas of the institution, regardless of their position or hierarchy. “Todo terreno" This program facilitates access to financial services to workers in companies that operate in rural, agricultural, and/or hard-to-reach areas.

• Z BANK

Strategic objectives: To unite CSR transversally throughout the Bank. Includes development of management tools

Actions: Program: Improvement of income and food security with women in Santa Teresa − Cuzco Phase II. Capacity building for financial and social inclusion of low-income families in Piura, Ica, and Huancavelica

• M BANK

Strategic objectives: Promote financial inclusion in the less-favored populations of Peru

Actions: Program: M BANK is a leading national sponsor of the Mathematics for All (MPT) project to spark schoolchildren’s interest in mathematics and strengthen their learning. Beneficiaries: 59,460 schoolchildren, 38,822 educational materials delivered, 1,148 trained teachers, and 115 schools benefited in 15 regions of the country

Appendix B. Questionnaire

The following questionnaire is an adaptation to English from the real questionnaire (Spanish) presented to the banking executive officers of the branch offices in Peru.

Table A1.

Questions about Business Confidence.

Table A2.

Questions about CSR.

Table A3.

Questions about CR.

References

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Lizarzaburu, E.R.; del Brío, J.A. Responsabilidad Social Corporativa y Reputación Corporativa en el sector financiero de países en desarrollo. GCG Rev. Glob. Compet. Gob. 2016, 10, 42–65. [Google Scholar] [CrossRef]

- Freeman, R. Strategic Management: A Stakeholder’s Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Carroll, A.B. A Three-Dimensional Conceptual Model of Corporate Performance. Acad. Manag. Rev. 1979, 4, 497. [Google Scholar] [CrossRef]

- Wood, D.J. Corporate Social Performance Revisited. Acad. Manag. Rev. 1991, 16, 691. [Google Scholar] [CrossRef]

- Gupta, S. Strategic Dimensions of Corporate Image: Corporate Ability and Corporate Social Responsibility as Sources of Competitive Advantage Via Differentiation.; Temple University: Philadelphia, PA, USA, 2002. [Google Scholar]

- Skouloudis, A.; Evangelinos, K.; Malesios, C. Priorities and Perceptions for Corporate Social Responsibility: An NGO Perspective. Corp. Soc. Responsib. Environ. Manag. 2013, 22, 95–112. [Google Scholar] [CrossRef]

- Michalski, G.; Blendinger, G.; Rozsa, Z.; Cierniak-Emerych, A.; Svidronova, M.; Buleca, J.; Bulsara, H. Can We Determine Debt To Equity Levels In Non-Profit Organisations? Answer Based On Polish Case. Eng. Econ. 2018, 29, 526–535. [Google Scholar] [CrossRef]

- Eiadat, Y.; Kelly, A.; Roche, F.; Eyadat, H. Green and competitive? An empirical test of the mediating role of environmental innovation strategy. J. World Bus. 2008, 43, 131–145. [Google Scholar] [CrossRef]

- De Leaniz, P.M.G.; Rodríguez, I.R.D.B.; Leaniz, I.R.D.B.R.P.M.G.D. Corporate Image and Reputation as Drivers of Customer Loyalty. Corp. Reput. Rev. 2016, 19, 166–178. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M. Perceptions of Investors and Stockbrokers on Corporate Social Responsibility: A Stakeholder Perspective from India. Knowl. Process. Manag. 2014, 21, 167–176. [Google Scholar] [CrossRef]

- Gonzalez-Padron, T.L.; Hult, G.T.M.; Ferrell, O.C.; Malhotra, N.K. A Stakeholder Marketing Approach to Sustainable Business. Rev. Mark. Res. 2016, 13, 61–101. [Google Scholar] [CrossRef]

- Miao, Z.; Cai, S.; Xu, D. Exploring the antecedents of logistics social responsibility: A focus on Chinese firms. Int. J. Prod. Econ. 2012, 140, 18–27. [Google Scholar] [CrossRef]

- Blendinger, G.; Michalski, G. Long-Term Competitiveness Based On Value Added Measures As Part Of Highly Professionalized Corporate Governance Management Of German Dax 30 Corporations. J. Compet. 2018, 10, 5–20. [Google Scholar] [CrossRef]

- Scholtens, B. Corporate Social Responsibility in the International Banking Industry. J. Bus. Ethics 2008, 86, 159–175. [Google Scholar] [CrossRef]

- Marin, L.; Ruiz, S.; Rubio, A. The Role of Identity Salience in the Effects of Corporate Social Responsibility on Consumer Behavior. J. Bus. Ethics 2008, 84, 65–78. [Google Scholar] [CrossRef]

- Truscott, R.A.; Bartlett, J.; Tywoniak, S.A. The reputation of the corporate social responsibility industry in Australia. Australas. Mark. J. 2009, 17, 84–91. [Google Scholar] [CrossRef]

- Prior, F.; Argandoña, A. Best Practices in Credit Accessibility and Corporate Social Responsibility in Financial Institutions. J. Bus. Ethics 2008, 87, 251–265. [Google Scholar] [CrossRef]

- Levine, R. Chapter 12 Finance and Growth: Theory and Evidence. In Handbook of Economic Growth; Elsevier BV: Amsterdam, The Netherlands, 2005; Volume 1, pp. 865–934. [Google Scholar]

- Decker, O.S. Corporate social responsibility and structural change in financial services. Manag. Audit. J. 2004, 19, 712–728. [Google Scholar] [CrossRef]

- Lizarzaburu, E.; Brio, J. Corporate Social Responsibility and Corporate Reputation in the financial sector of developing countries. GCG Glob. Compet. Gov. Mag. 2016, 10, 42–65. [Google Scholar]

- Helm, S. The Role of Corporate Reputation in Determining Investor Satisfaction and Loyalty. Corp. Reput. Rev. 2007, 10, 22–37. [Google Scholar] [CrossRef]

- Olmedo-Cifuentes, I.; Martínez-León, I.; Davies, G. Managing internal stakeholders’ views of corporate reputation. Serv. Bus. 2013, 8, 83–111. [Google Scholar] [CrossRef]

- Akdag, H.C.; Zineldin, M. Strategic positioning and quality determinants in banking service. TQM J. 2011, 23, 446–457. [Google Scholar] [CrossRef]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R.E. Law, endowments, and finance. J. Financial Econ. 2003, 70, 137–181. [Google Scholar] [CrossRef]

- Boshoff, C. A psychometric assessment of an instrument to measure a service firm’s customer-based corporate reputation. S. Afr. J. Bus. Manag. 2009, 40, 35–44. [Google Scholar] [CrossRef]

- Keh, H.T.; Xie, Y. Corporate reputation and customer behavioral intentions: The roles of trust, identification and commitment. Ind. Mark. Manag. 2009, 38, 732–742. [Google Scholar] [CrossRef]

- Matten, D.; Moon, J. “Implicit” and “Explicit” CSR: A Conceptual Framework for a Comparative Understanding of Corporate Social Responsibility. Acad. Manag. Rev. 2008, 33, 404–424. [Google Scholar] [CrossRef]

- Yoon, Y.; Gürhan-Canli, Z.; Schwarz, N. The Effect of Corporate Social Responsibility (CSR) Activities on Companies With Bad Reputations. J. Consum. Psychol. 2006, 16, 377–390. [Google Scholar] [CrossRef]

- Epstein, M.J.; Roy, M.-J. Sustainability in Action: Identifying and Measuring the Key Performance Drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Kotha, S.; Rajgopal, S.; Rindova, V. Reputation Building and Performance: An Empirical Analysis of the Top-50 Pure Internet Firms. Eur. Manag. J. 2001, 19, 571–586. [Google Scholar] [CrossRef]

- Bromley, D. Comparing Corporate Reputations: League Tables, Quotients, Benchmarks, or Case Studies? Corp. Reput. Rev. 2002, 5, 35–50. [Google Scholar] [CrossRef]

- Eberl, M.; Schwaiger, M. Corporate reputation: Disentangling the effects on financial performance. Eur. J. Mark. 2005, 39, 838–854. [Google Scholar] [CrossRef]

- Sun, J.; Yuan, R.; Cao, F.; Wang, B. Principal-principal agency problems and stock price crash risk: Evidence from the split-share structure reform in China. Corp. Gov. Int. Rev. 2017, 25, 186–199. [Google Scholar] [CrossRef]

- Bravo, R.; Montaner, T.; Pina, J. The role of bank image for customers versus non-customers. Int. J. Bank Mark. 2009, 27, 315–334. [Google Scholar] [CrossRef]

- Issa, M. Preserving Corporate Reputation in the Social Media Era. Master’s Thesis, Iowa State University, Ames, IA, USA, 2018. [Google Scholar]

- Quazi, A.M. Identifying the determinants of corporate managers’ perceived social obligations. Manag. Decis. 2003, 41, 822–831. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations. Acad. Manag. Rev. 2007, 32, 836–863. [Google Scholar] [CrossRef]

- Fatma, M.; Rahman, Z. Consumer perspective on CSR literature review and future research agenda. Manag. Res. Rev. 2015, 38, 195–216. [Google Scholar] [CrossRef]

- Lind, D.A.; Marchal, G.M.; Wathen, S.A. Statistics Applied to Business and Economics, 15th ed.; McGrawHill: New York, NY, USA, 2015. [Google Scholar]

- Osterman, P. How Common is Workplace Transformation and Who Adopts it? ILR Rev. 1994, 47, 173–188. [Google Scholar] [CrossRef]

- Greening, D.W.; Turban, D.B. Corporate Social Performance As a Competitive Advantage in Attracting a Quality Workforce. Bus. Soc. 2000, 39, 254–280. [Google Scholar] [CrossRef]

- Fineman, S.; Clarke, K. Green Stakeholders: Industry Interpretations And Response. J. Manag. Stud. 1996, 33, 715–730. [Google Scholar] [CrossRef]

- Maignan, I. Consumers’ Perceptions of Corporate Social Responsibilities: A Cross-Cultural Comparison. J. Bus. Ethics 2001, 30, 57–72. [Google Scholar] [CrossRef]

- Bigné, E.; Andreu, L.; Chumpitaz, R.; Swaen, V. Perception of corporate social responsibility: A cross-cultural analysis. Universia Bus. Rev. 2005, 5, 14–27. [Google Scholar]

- Muñoz-Martín, J. Business Ethics, Corporate Social Responsibility (CSR) and Creation of Shared Value (CVC). J. Glob. Compet. Gov. 2013, 7, 76. [Google Scholar]

- Priego, A.M.; Lizano, M.M.; Merino, E. Business failure: Incidence of stakeholders’ behavior. Acad. Rev. Latinoam. Adm. 2014, 27, 75–91. [Google Scholar] [CrossRef]

- Hillman, A.J.; Keim, G.D. Shareholder Value. Stakeholder Management, and Social Issues: What’s the Bottom Line. Strateg. Manag. J. 2001, 22, 125–140. [Google Scholar] [CrossRef]

- Harjoto, M.A.; Laksmana, I.; Lee, R. Board Diversity and Corporate Social Responsibility. J. Bus. Ethics 2014, 132, 641–660. [Google Scholar] [CrossRef]

- Caruana, A.; Chircop, S. Measuring Corporate Reputation: A Case Example. Corp. Reput. Rev. 2000, 3, 43–57. [Google Scholar] [CrossRef]

- Diamantopoulos, A.; Winklhofer, H. Index Construction with Formative Indicators: An Alternative to Scale Development. J. Mark. Res. 2001, 38, 269–277. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Sobel, M.E. Asymptotic Confidence Intervals for Indirect Effects in Structural Equation Models. Sociol. Methodol. 1982, 13, 290. [Google Scholar] [CrossRef]

- Neter, J.; Wasserman, W.; Kutner, M.H. Applied Linear Statistical Models: Regression, Analysis of Variance, and Experimental Design; Richard, D., Ed.; Irwin: Homewood, IL, USA, 1990. [Google Scholar]

- Polak, P.; Masquelier, F.; Michalski, G. Towards treasury 4.0/The evolving role of corporate treasury management for 2020. Manag. J. Contemp. Manag. Issues 2018, 23, 189–197. [Google Scholar] [CrossRef]

- Bolaños, E.R.L.; Del Brío, J. Evolución del sistema financiero peruano y su reputación bajo el índice Merco. Período: 2010–2014. Suma Neg. 2016, 7, 94–112. [Google Scholar] [CrossRef]

- Avrampou, A.; Skouloudis, A.; Iliopoulos, G.; Khan, N. Advancing the Sustainable Development Goals: Evidence from leading European banks. Sustain. Dev. 2019, 27, 743–757. [Google Scholar] [CrossRef]

- Anagnostopoulos, T.; Skouloudis, A.; Khan, N.; Evangelinos, K. Incorporating Sustainability Considerations into Lending Decisions and the Management of Bad Loans: Evidence from Greece. Sustainsbility 2018, 10, 4728. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).